HC2091 Finance: Reliance Worldwide Corp. Performance Analysis

VerifiedAdded on 2023/06/03

|22

|4027

|275

Report

AI Summary

This paper provides an in-depth financial analysis of Reliance Worldwide Corporation (RWC), utilizing financial ratio analysis, share valuation, and share price movement to assess the company's financial health and provide investment recommendations. The analysis reveals that RWC is profitable, as indicated by increased ROE, ROA, and net margin, and possesses sufficient liquidity to cover its short-term liabilities, supported by high current and quick ratios. Furthermore, the report observes a positive trend in RWC's share price over the past two years. Based on these findings, the report recommends that investors consider adding RWC shares to their portfolios.

Analysis of Reliance Worldwide 1

ANALYSIS OF RELIANCE WORLDWIDE

Author

Student’s Number

Court title

Course Number

Professor

City

Date

ANALYSIS OF RELIANCE WORLDWIDE

Author

Student’s Number

Court title

Course Number

Professor

City

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Reliance Worldwide 2

Executive Summary

The paper aims to investigate and evaluate financial performance of Reliance Worldwide

Company based on financial ratio analysis, share valuation and share price movement. From

the ratio analysis, it was found out that RWC is profitable through increased ROE, ROA as

well as net margin. Further, it was found out that RWC is liquid enough in settling most of its

short-run or current liabilities through its current assets. This was based its relatively high

current and quick ratios which were above one. It was also found that RWC share price was

doing relatively good over the past two years with significant increase being observed over

the years. As such, it would be recommendable for the investor to add RWC share in her

portfolio.

Executive Summary

The paper aims to investigate and evaluate financial performance of Reliance Worldwide

Company based on financial ratio analysis, share valuation and share price movement. From

the ratio analysis, it was found out that RWC is profitable through increased ROE, ROA as

well as net margin. Further, it was found out that RWC is liquid enough in settling most of its

short-run or current liabilities through its current assets. This was based its relatively high

current and quick ratios which were above one. It was also found that RWC share price was

doing relatively good over the past two years with significant increase being observed over

the years. As such, it would be recommendable for the investor to add RWC share in her

portfolio.

Analysis of Reliance Worldwide 3

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Calculation and Analysis of Performance Ratio........................................................................4

Liquidity Ratios......................................................................................................................5

Current Ratio.......................................................................................................................5

Quick Ratio.........................................................................................................................6

Working Capital..................................................................................................................6

Financial Leverage Ratios......................................................................................................7

Debt/asset ratio...................................................................................................................8

Debt/equity..........................................................................................................................8

Asset Utilization Ratios..........................................................................................................9

Asset turnover.....................................................................................................................9

Inventory turnover............................................................................................................10

Receivable turnover..........................................................................................................11

Profitability Ratios................................................................................................................12

Net Margin........................................................................................................................12

ROE..................................................................................................................................13

ROA..................................................................................................................................14

Market Value Ratios.............................................................................................................15

EPS....................................................................................................................................15

Graphical Representation of Reliance Worldwide Corporation Share Price and Comparison of

Its Share Price Movements with All Ordinaries Index............................................................16

Share Valuation........................................................................................................................18

Conclusion................................................................................................................................19

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Calculation and Analysis of Performance Ratio........................................................................4

Liquidity Ratios......................................................................................................................5

Current Ratio.......................................................................................................................5

Quick Ratio.........................................................................................................................6

Working Capital..................................................................................................................6

Financial Leverage Ratios......................................................................................................7

Debt/asset ratio...................................................................................................................8

Debt/equity..........................................................................................................................8

Asset Utilization Ratios..........................................................................................................9

Asset turnover.....................................................................................................................9

Inventory turnover............................................................................................................10

Receivable turnover..........................................................................................................11

Profitability Ratios................................................................................................................12

Net Margin........................................................................................................................12

ROE..................................................................................................................................13

ROA..................................................................................................................................14

Market Value Ratios.............................................................................................................15

EPS....................................................................................................................................15

Graphical Representation of Reliance Worldwide Corporation Share Price and Comparison of

Its Share Price Movements with All Ordinaries Index............................................................16

Share Valuation........................................................................................................................18

Conclusion................................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of Reliance Worldwide 4

Recommendation......................................................................................................................19

REFERENCES.........................................................................................................................20

Recommendation......................................................................................................................19

REFERENCES.........................................................................................................................20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Reliance Worldwide 5

Introduction

Reliance Worldwide Corporation commonly known as RWC is the Australian-based firm that

manufactures, designs as well as suppliers water flow and provide solution and control

products for use in wall plumbing (Reliance Worldwide Corporation 2017). It manufactures

brass push-to-connects plumbing fittings. The company chief products comprises of

thermostatic products, control valves, pipe and fittings as well as other products the Fitting

and pipe comprises of the plumbing fittings, related products for repair and installation of the

water reticulation systems as well as piping (Financial Times 2018).

Calculation and Analysis of Performance Ratio

Financial ratios are usually conducted by comparing at least two items reported in financial

statements. In other words, ratios are considered as mathematical comparisons of the

financial statements (Innocent, Mary & Matthew 2013). This assists internal organization

management, investors and creditors among others comprehend how well the company is

doing and those areas that require some improvements. They are crucial in determining an

entity’s financial position since they are easy to comprehend and easy to calculate. Further,

ratios are used in comparing different firms across the sector and with their competitors

(Higgins 2012). They enable analysts to compare organizations across the sectors, to identify

their weaknesses and strengths. Ratio analysis can be classified as liquidity, profitability,

market value, solvency or leverage as well as efficiency ratios.

Liquidity Ratios

Such ratio are useful in analysing capacity of Reliance Worldwide Corporation Ltd in settling

off both its short-term debts once they are due and long-term debts once they are current

(Innocent, Mary & Matthew 2013). They show Reliance Worldwide Corporation Ltd cash

Introduction

Reliance Worldwide Corporation commonly known as RWC is the Australian-based firm that

manufactures, designs as well as suppliers water flow and provide solution and control

products for use in wall plumbing (Reliance Worldwide Corporation 2017). It manufactures

brass push-to-connects plumbing fittings. The company chief products comprises of

thermostatic products, control valves, pipe and fittings as well as other products the Fitting

and pipe comprises of the plumbing fittings, related products for repair and installation of the

water reticulation systems as well as piping (Financial Times 2018).

Calculation and Analysis of Performance Ratio

Financial ratios are usually conducted by comparing at least two items reported in financial

statements. In other words, ratios are considered as mathematical comparisons of the

financial statements (Innocent, Mary & Matthew 2013). This assists internal organization

management, investors and creditors among others comprehend how well the company is

doing and those areas that require some improvements. They are crucial in determining an

entity’s financial position since they are easy to comprehend and easy to calculate. Further,

ratios are used in comparing different firms across the sector and with their competitors

(Higgins 2012). They enable analysts to compare organizations across the sectors, to identify

their weaknesses and strengths. Ratio analysis can be classified as liquidity, profitability,

market value, solvency or leverage as well as efficiency ratios.

Liquidity Ratios

Such ratio are useful in analysing capacity of Reliance Worldwide Corporation Ltd in settling

off both its short-term debts once they are due and long-term debts once they are current

(Innocent, Mary & Matthew 2013). They show Reliance Worldwide Corporation Ltd cash

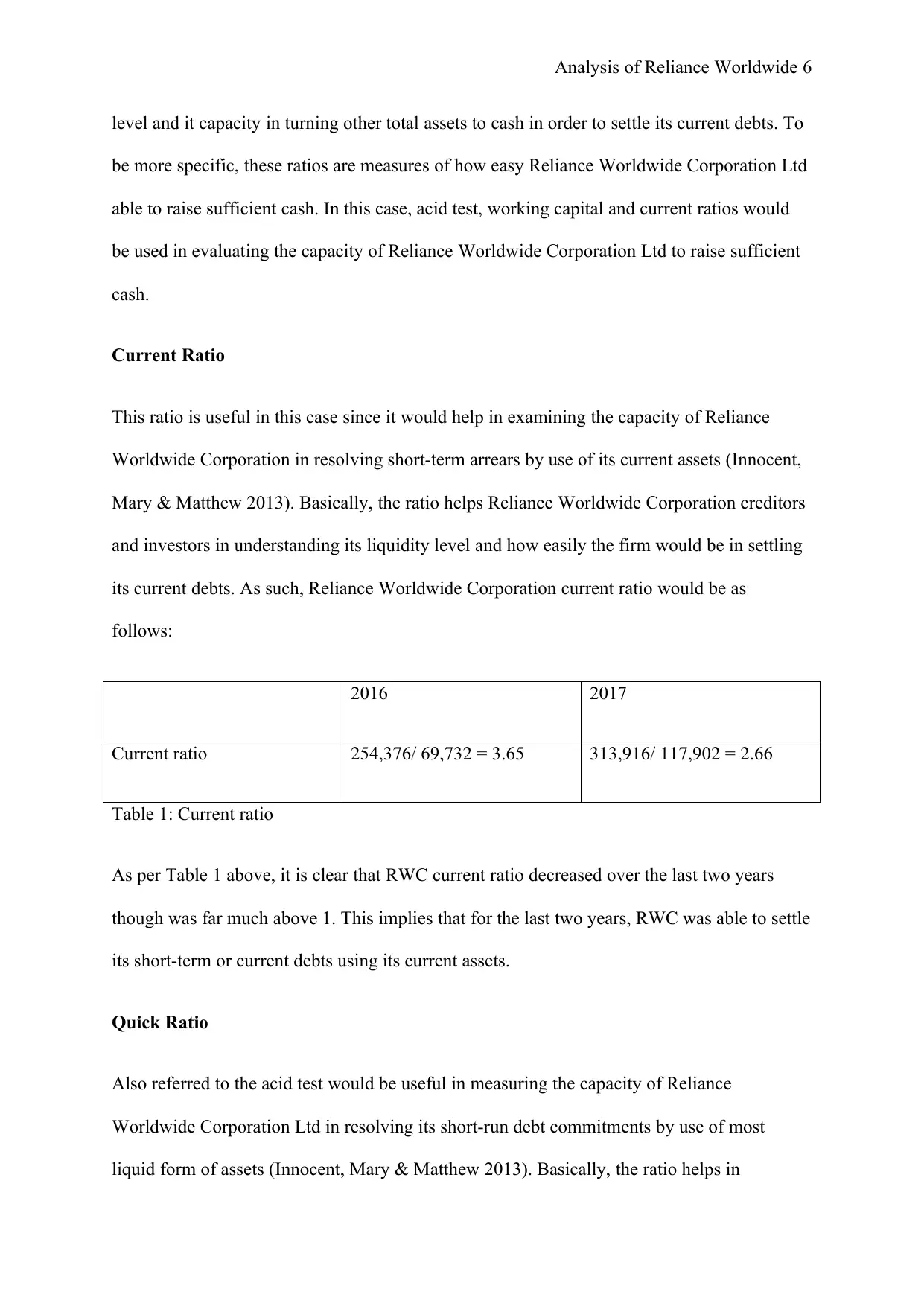

Analysis of Reliance Worldwide 6

level and it capacity in turning other total assets to cash in order to settle its current debts. To

be more specific, these ratios are measures of how easy Reliance Worldwide Corporation Ltd

able to raise sufficient cash. In this case, acid test, working capital and current ratios would

be used in evaluating the capacity of Reliance Worldwide Corporation Ltd to raise sufficient

cash.

Current Ratio

This ratio is useful in this case since it would help in examining the capacity of Reliance

Worldwide Corporation in resolving short-term arrears by use of its current assets (Innocent,

Mary & Matthew 2013). Basically, the ratio helps Reliance Worldwide Corporation creditors

and investors in understanding its liquidity level and how easily the firm would be in settling

its current debts. As such, Reliance Worldwide Corporation current ratio would be as

follows:

2016 2017

Current ratio 254,376/ 69,732 = 3.65 313,916/ 117,902 = 2.66

Table 1: Current ratio

As per Table 1 above, it is clear that RWC current ratio decreased over the last two years

though was far much above 1. This implies that for the last two years, RWC was able to settle

its short-term or current debts using its current assets.

Quick Ratio

Also referred to the acid test would be useful in measuring the capacity of Reliance

Worldwide Corporation Ltd in resolving its short-run debt commitments by use of most

liquid form of assets (Innocent, Mary & Matthew 2013). Basically, the ratio helps in

level and it capacity in turning other total assets to cash in order to settle its current debts. To

be more specific, these ratios are measures of how easy Reliance Worldwide Corporation Ltd

able to raise sufficient cash. In this case, acid test, working capital and current ratios would

be used in evaluating the capacity of Reliance Worldwide Corporation Ltd to raise sufficient

cash.

Current Ratio

This ratio is useful in this case since it would help in examining the capacity of Reliance

Worldwide Corporation in resolving short-term arrears by use of its current assets (Innocent,

Mary & Matthew 2013). Basically, the ratio helps Reliance Worldwide Corporation creditors

and investors in understanding its liquidity level and how easily the firm would be in settling

its current debts. As such, Reliance Worldwide Corporation current ratio would be as

follows:

2016 2017

Current ratio 254,376/ 69,732 = 3.65 313,916/ 117,902 = 2.66

Table 1: Current ratio

As per Table 1 above, it is clear that RWC current ratio decreased over the last two years

though was far much above 1. This implies that for the last two years, RWC was able to settle

its short-term or current debts using its current assets.

Quick Ratio

Also referred to the acid test would be useful in measuring the capacity of Reliance

Worldwide Corporation Ltd in resolving its short-run debt commitments by use of most

liquid form of assets (Innocent, Mary & Matthew 2013). Basically, the ratio helps in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of Reliance Worldwide 7

measuring Reliance Worldwide Corporation Ltd capacity in settling its current or short-term

debts with quick assets. The ratio is computed by dividing quick assets with company’s

current liabilities. As such, Reliance Worldwide Corporation quick ratio would be as follows:

2016 2017

Quick ratio (254,376 – 119,109)/ 69,732

= 1.94

(313,916 – 162,422)/

117,902 = 1.28

Table 2: Quick ratio

In the Table 2 above, it is clear that Reliance Worldwide Corporation quick ratio was

relatively high over the past two years. Despite the decrease within the year, the ratios were

above one meaning that RWC was able to settle some of its short-run debt commitments with

its quick assets.

Working Capital

This value would be useful in determining whether Reliance Worldwide Corporation Ltd is

able to meet most of its short-term or current obligations using its short-term assets (Penman

& Penman 2007). In other words, it would help in determining how much deficiency or

excess there is in Reliance Worldwide Corporation Ltd. As such, Reliance Worldwide

Corporation working capital in 2016 and 2017 would be as follows:

2016 2017

Working capital 254,376 - 69,732 = 184,644 313,916 - 117,902 = 196,014

Table 3: Working capital

measuring Reliance Worldwide Corporation Ltd capacity in settling its current or short-term

debts with quick assets. The ratio is computed by dividing quick assets with company’s

current liabilities. As such, Reliance Worldwide Corporation quick ratio would be as follows:

2016 2017

Quick ratio (254,376 – 119,109)/ 69,732

= 1.94

(313,916 – 162,422)/

117,902 = 1.28

Table 2: Quick ratio

In the Table 2 above, it is clear that Reliance Worldwide Corporation quick ratio was

relatively high over the past two years. Despite the decrease within the year, the ratios were

above one meaning that RWC was able to settle some of its short-run debt commitments with

its quick assets.

Working Capital

This value would be useful in determining whether Reliance Worldwide Corporation Ltd is

able to meet most of its short-term or current obligations using its short-term assets (Penman

& Penman 2007). In other words, it would help in determining how much deficiency or

excess there is in Reliance Worldwide Corporation Ltd. As such, Reliance Worldwide

Corporation working capital in 2016 and 2017 would be as follows:

2016 2017

Working capital 254,376 - 69,732 = 184,644 313,916 - 117,902 = 196,014

Table 3: Working capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Reliance Worldwide 8

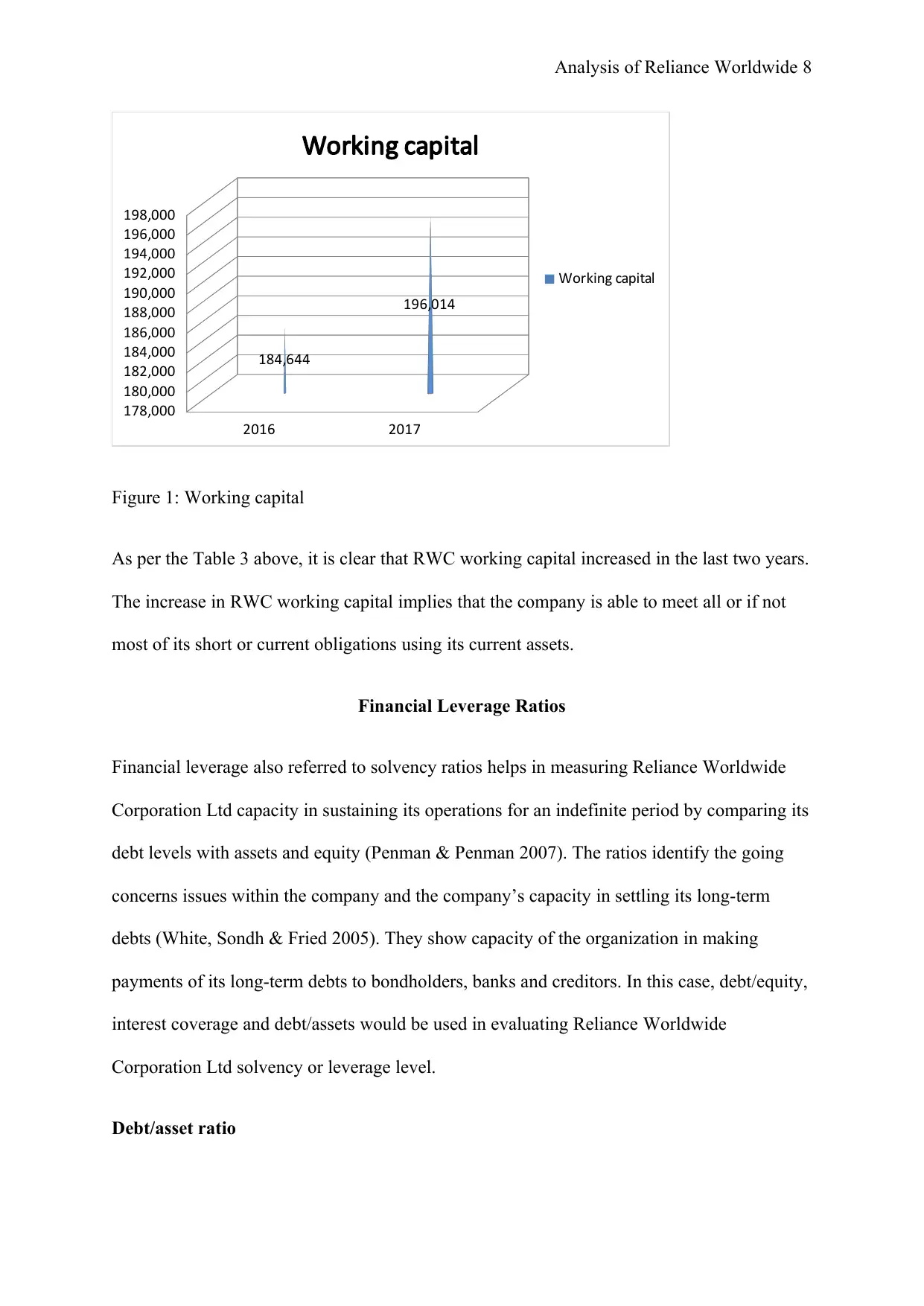

2016 2017

178,000

180,000

182,000

184,000

186,000

188,000

190,000

192,000

194,000

196,000

198,000

184,644

196,014

Working capital

Working capital

Figure 1: Working capital

As per the Table 3 above, it is clear that RWC working capital increased in the last two years.

The increase in RWC working capital implies that the company is able to meet all or if not

most of its short or current obligations using its current assets.

Financial Leverage Ratios

Financial leverage also referred to solvency ratios helps in measuring Reliance Worldwide

Corporation Ltd capacity in sustaining its operations for an indefinite period by comparing its

debt levels with assets and equity (Penman & Penman 2007). The ratios identify the going

concerns issues within the company and the company’s capacity in settling its long-term

debts (White, Sondh & Fried 2005). They show capacity of the organization in making

payments of its long-term debts to bondholders, banks and creditors. In this case, debt/equity,

interest coverage and debt/assets would be used in evaluating Reliance Worldwide

Corporation Ltd solvency or leverage level.

Debt/asset ratio

2016 2017

178,000

180,000

182,000

184,000

186,000

188,000

190,000

192,000

194,000

196,000

198,000

184,644

196,014

Working capital

Working capital

Figure 1: Working capital

As per the Table 3 above, it is clear that RWC working capital increased in the last two years.

The increase in RWC working capital implies that the company is able to meet all or if not

most of its short or current obligations using its current assets.

Financial Leverage Ratios

Financial leverage also referred to solvency ratios helps in measuring Reliance Worldwide

Corporation Ltd capacity in sustaining its operations for an indefinite period by comparing its

debt levels with assets and equity (Penman & Penman 2007). The ratios identify the going

concerns issues within the company and the company’s capacity in settling its long-term

debts (White, Sondh & Fried 2005). They show capacity of the organization in making

payments of its long-term debts to bondholders, banks and creditors. In this case, debt/equity,

interest coverage and debt/assets would be used in evaluating Reliance Worldwide

Corporation Ltd solvency or leverage level.

Debt/asset ratio

Analysis of Reliance Worldwide 9

The ratio is useful in measuring portion of Reliance Worldwide Corporation Ltd total assets

which is financed through debts (White, Sondh & Fried 2005). It can be gotten by dividing

total debts with the total assets. This ratio is useful in examining the entity’s total debts as the

fraction of its assets. The ratio, displays Reliance Worldwide Corporation Ltd capacity in

settling its liabilities using its assets. As such, Reliance Worldwide Corporation debt/assets

ratio in 2016 and 2017 would be as follows:

2016 2017

Debt/assets 256,088/423,075 = 0.61 395,041/599,787 = 0.66

Table 4: debt/assets

Based on Table 4 above, it is evident that Reliance Worldwide Corporation debt/assets ratio

was relatively low over the past two years. The figures show that for the past two years,

RWC was able to settle its liabilities using its assets.

Debt/equity

It is helpful in determining portion of Reliance Worldwide Corporation Ltd that is financed

by debts and the one financed by equity (Penman & Penman 2007). In other words, the ratio

helps in assessing capital structure of Reliance Worldwide Corporation Ltd over time (White,

Sondh & Fried 2005). In this case, debt/equity is gotten by dividing total liabilities or debts

with the total shareholders’ equity where a ratio more than one means that the organization is

leveraged while value less than one means that the company is conservative. As such,

Reliance Worldwide Corporation debt/equity ratio in 2016 and in 2017 would be as follows:

2016 2017

Debt/equity 256,088/166,987 = 1.53 395,041/204,746 = 1.93

The ratio is useful in measuring portion of Reliance Worldwide Corporation Ltd total assets

which is financed through debts (White, Sondh & Fried 2005). It can be gotten by dividing

total debts with the total assets. This ratio is useful in examining the entity’s total debts as the

fraction of its assets. The ratio, displays Reliance Worldwide Corporation Ltd capacity in

settling its liabilities using its assets. As such, Reliance Worldwide Corporation debt/assets

ratio in 2016 and 2017 would be as follows:

2016 2017

Debt/assets 256,088/423,075 = 0.61 395,041/599,787 = 0.66

Table 4: debt/assets

Based on Table 4 above, it is evident that Reliance Worldwide Corporation debt/assets ratio

was relatively low over the past two years. The figures show that for the past two years,

RWC was able to settle its liabilities using its assets.

Debt/equity

It is helpful in determining portion of Reliance Worldwide Corporation Ltd that is financed

by debts and the one financed by equity (Penman & Penman 2007). In other words, the ratio

helps in assessing capital structure of Reliance Worldwide Corporation Ltd over time (White,

Sondh & Fried 2005). In this case, debt/equity is gotten by dividing total liabilities or debts

with the total shareholders’ equity where a ratio more than one means that the organization is

leveraged while value less than one means that the company is conservative. As such,

Reliance Worldwide Corporation debt/equity ratio in 2016 and in 2017 would be as follows:

2016 2017

Debt/equity 256,088/166,987 = 1.53 395,041/204,746 = 1.93

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of Reliance Worldwide 10

Table 5: Debt/equity

As per the Table 5 above, it is clear that RWC debt/equity experienced an increasing

debt/equity ratio over the last two years. The increasing trend in the ratio is a clear sign that

for the last two years, RWC has been highly leveraged.

Asset Utilization Ratios

The efficiency also referred to asset utilization ratios help in measuring how well Reliance

Worldwide Corporation Ltd utilizes its total assets in generating some income (White, Sondh

& Fried 2005). They usually look at time taken by Reliance Worldwide Corporation Ltd in

collecting cash from the clients or time take in converting inventories into cash. Asset

turnover, receivable turnover and inventory turnover would be the efficiency ratios evaluated

to determining how Reliance Worldwide Corporation Ltd is efficient in its operations.

Asset turnover

It is useful in determining overall efficiency of Reliance Worldwide Corporation Ltd in

generating revenues through its assets (White, Sondh & Fried 2005). The ratio indicates how

efficiently Reliance Worldwide Corporation Ltd could utilize its total assets in generating

revenue. It is gotten by dividing net revenue with the average total assets. As such, Reliance

Worldwide Corporation asset turnover in 2016 and 2017 would be as follows:

2016 2017

Asset turnover 98,290 /423,075 = 0.23 601,693 /599,787 = 1.00

Table 6: Asset turnover

Table 5: Debt/equity

As per the Table 5 above, it is clear that RWC debt/equity experienced an increasing

debt/equity ratio over the last two years. The increasing trend in the ratio is a clear sign that

for the last two years, RWC has been highly leveraged.

Asset Utilization Ratios

The efficiency also referred to asset utilization ratios help in measuring how well Reliance

Worldwide Corporation Ltd utilizes its total assets in generating some income (White, Sondh

& Fried 2005). They usually look at time taken by Reliance Worldwide Corporation Ltd in

collecting cash from the clients or time take in converting inventories into cash. Asset

turnover, receivable turnover and inventory turnover would be the efficiency ratios evaluated

to determining how Reliance Worldwide Corporation Ltd is efficient in its operations.

Asset turnover

It is useful in determining overall efficiency of Reliance Worldwide Corporation Ltd in

generating revenues through its assets (White, Sondh & Fried 2005). The ratio indicates how

efficiently Reliance Worldwide Corporation Ltd could utilize its total assets in generating

revenue. It is gotten by dividing net revenue with the average total assets. As such, Reliance

Worldwide Corporation asset turnover in 2016 and 2017 would be as follows:

2016 2017

Asset turnover 98,290 /423,075 = 0.23 601,693 /599,787 = 1.00

Table 6: Asset turnover

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Reliance Worldwide 11

In the Table 7 below, it is evident that Reliance Worldwide Corporation asset turnover

increased from 0.23 to 1 in 2017. The increasing trend in the company asset turnover implies

that the company is becoming more efficient in managing its assets or in utilizing its assets to

generate revenue.

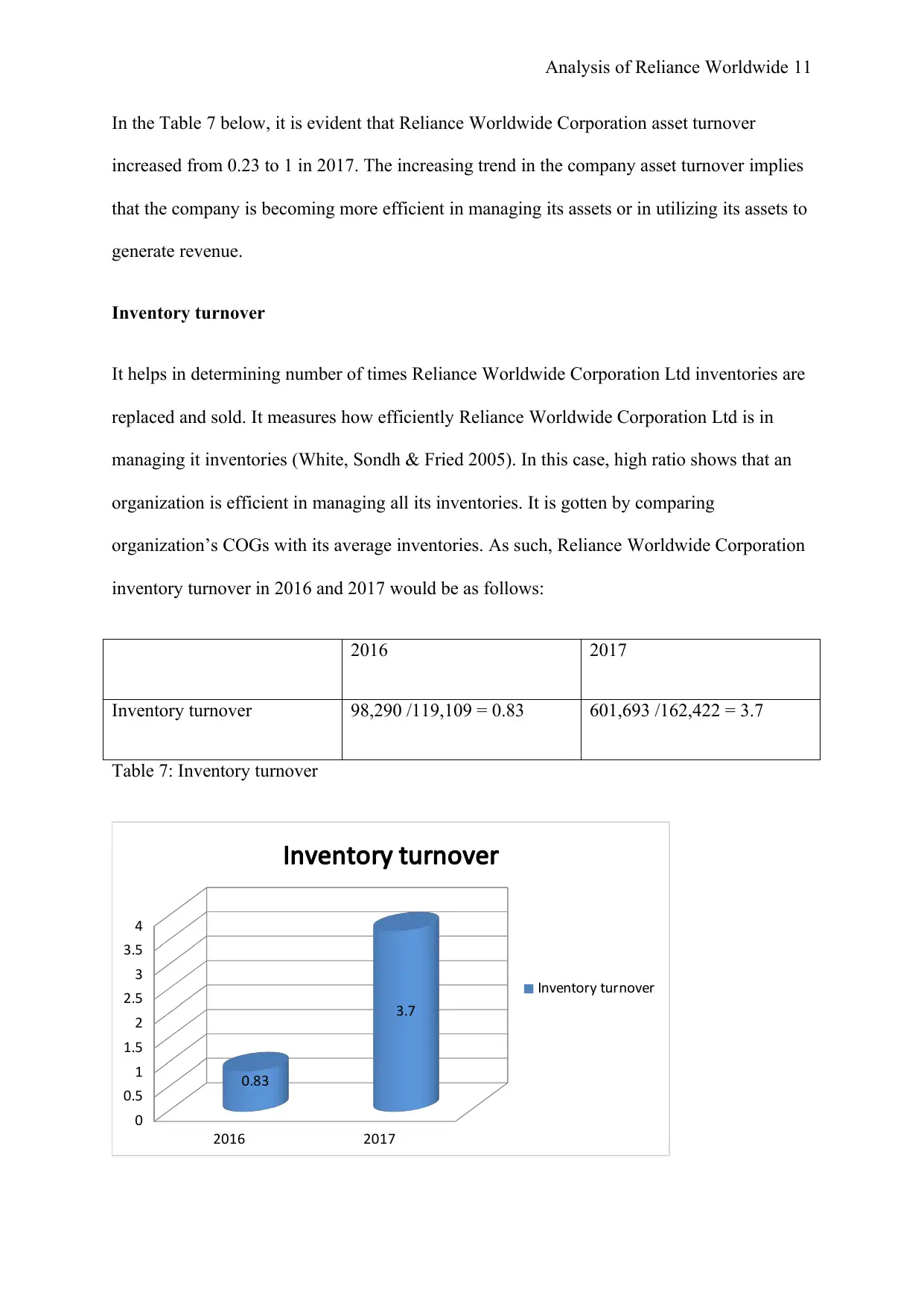

Inventory turnover

It helps in determining number of times Reliance Worldwide Corporation Ltd inventories are

replaced and sold. It measures how efficiently Reliance Worldwide Corporation Ltd is in

managing it inventories (White, Sondh & Fried 2005). In this case, high ratio shows that an

organization is efficient in managing all its inventories. It is gotten by comparing

organization’s COGs with its average inventories. As such, Reliance Worldwide Corporation

inventory turnover in 2016 and 2017 would be as follows:

2016 2017

Inventory turnover 98,290 /119,109 = 0.83 601,693 /162,422 = 3.7

Table 7: Inventory turnover

2016 2017

0

0.5

1

1.5

2

2.5

3

3.5

4

0.83

3.7

Inventory turnover

Inventory turnover

In the Table 7 below, it is evident that Reliance Worldwide Corporation asset turnover

increased from 0.23 to 1 in 2017. The increasing trend in the company asset turnover implies

that the company is becoming more efficient in managing its assets or in utilizing its assets to

generate revenue.

Inventory turnover

It helps in determining number of times Reliance Worldwide Corporation Ltd inventories are

replaced and sold. It measures how efficiently Reliance Worldwide Corporation Ltd is in

managing it inventories (White, Sondh & Fried 2005). In this case, high ratio shows that an

organization is efficient in managing all its inventories. It is gotten by comparing

organization’s COGs with its average inventories. As such, Reliance Worldwide Corporation

inventory turnover in 2016 and 2017 would be as follows:

2016 2017

Inventory turnover 98,290 /119,109 = 0.83 601,693 /162,422 = 3.7

Table 7: Inventory turnover

2016 2017

0

0.5

1

1.5

2

2.5

3

3.5

4

0.83

3.7

Inventory turnover

Inventory turnover

Analysis of Reliance Worldwide 12

Figure 2: Inventory turnover

From Table 8 above, it is clear that RWC inventory turnover increased over the past two

years. The increase implies that Reliance Worldwide Corporation is efficient in managing its

inventories.

Receivable turnover

The ratio would be used in measuring or determining efficiency of Reliance Worldwide

Corporation Ltd in extending credit or collecting the same (White, Sondh & Fried 2005). In

other words, it would be used in determining number of times Reliance Worldwide

Corporation Ltd collects its account receivables within one year. Here, a high value means

efficiency in collection process. As such, Reliance Worldwide Corporation receivable

turnover in 2016 and 2017 would be as follows:

2016 2017

Receivable turnover 98,290 /94,954 = 1.04 601,693 /109,727 = 5.48

Table 8: Receivable turnover

As per Table 9 above, it is clear that Reliance Worldwide Corporation receivable turnover

increased over the years. The increase is a good sign that the company is becoming more

efficient in collecting its receivables from debtors.

Profitability Ratios

The ratios compare the income statement items aiming to indicate the organization’s capacity

in generating income from operations (White, Sondh & Fried 2005). They focus on

organization’s return on equity and the other assets (Sueyoshi 2005). The ratios can also be

Figure 2: Inventory turnover

From Table 8 above, it is clear that RWC inventory turnover increased over the past two

years. The increase implies that Reliance Worldwide Corporation is efficient in managing its

inventories.

Receivable turnover

The ratio would be used in measuring or determining efficiency of Reliance Worldwide

Corporation Ltd in extending credit or collecting the same (White, Sondh & Fried 2005). In

other words, it would be used in determining number of times Reliance Worldwide

Corporation Ltd collects its account receivables within one year. Here, a high value means

efficiency in collection process. As such, Reliance Worldwide Corporation receivable

turnover in 2016 and 2017 would be as follows:

2016 2017

Receivable turnover 98,290 /94,954 = 1.04 601,693 /109,727 = 5.48

Table 8: Receivable turnover

As per Table 9 above, it is clear that Reliance Worldwide Corporation receivable turnover

increased over the years. The increase is a good sign that the company is becoming more

efficient in collecting its receivables from debtors.

Profitability Ratios

The ratios compare the income statement items aiming to indicate the organization’s capacity

in generating income from operations (White, Sondh & Fried 2005). They focus on

organization’s return on equity and the other assets (Sueyoshi 2005). The ratios can also be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.