Accounting Report: Analysis of Reliance Worldwide Company's Financials

VerifiedAdded on 2023/01/18

|13

|2229

|53

Report

AI Summary

This report provides a comprehensive analysis of the financial reporting practices of Reliance Worldwide Company (RWC). It begins with an executive summary and an introduction to contemporary accounting issues. The report provides a company overview, detailing RWC's global presence and business operations. The core of the report examines the conceptual framework of financial reporting, assessing RWC's compliance with measurement requirements. It then delves into the fundamental and enhancing qualitative characteristics of financial statements, evaluating how RWC adheres to these principles. The report explores the usability of RWC's financial statements for various stakeholders, including investors and creditors, and assesses whether the company meets the requirements for general-purpose financial reporting. The analysis is supported by references to academic literature and RWC's annual report, concluding with a summary of the findings and recommendations for improving financial reporting practices. The report also evaluates the needs of users of financial statements, and the application of the conceptual framework.

Running head: REPORT 0

CONTEMPORARY ISSUES IN ACCOUNTING

APRIL 15, 2019

student details:

CONTEMPORARY ISSUES IN ACCOUNTING

APRIL 15, 2019

student details:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Executive Summary

The conceptual framework is very essential in respect of the financial reporting. The

conceptual framework creates the basis at that the accounting standards can be established

such as liabilities, expenses and incomes can be identified. This report states the

contemporary issues related to the Reliance Worldwide Company.

Executive Summary

The conceptual framework is very essential in respect of the financial reporting. The

conceptual framework creates the basis at that the accounting standards can be established

such as liabilities, expenses and incomes can be identified. This report states the

contemporary issues related to the Reliance Worldwide Company.

REPORT 2

Contents

Executive Summary...................................................................................................................1

Introduction................................................................................................................................3

Company Overview- Reliance Worldwide Company................................................................3

Conceptual framework- measurement of financial statement....................................................3

Fundamental qualitative characteristics.....................................................................................4

Enhancing qualitative characteristics.........................................................................................4

Requirement of financial statements for the users of company.................................................5

General purpose financial statements.........................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Contents

Executive Summary...................................................................................................................1

Introduction................................................................................................................................3

Company Overview- Reliance Worldwide Company................................................................3

Conceptual framework- measurement of financial statement....................................................3

Fundamental qualitative characteristics.....................................................................................4

Enhancing qualitative characteristics.........................................................................................4

Requirement of financial statements for the users of company.................................................5

General purpose financial statements.........................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Introduction

The accounting is constantly advancing, significantly affected by exterior elements in the

markets globally. The contemporary issues are the issues, which are faced by the

professionals of accounting. This report directs the Reliance Worldwide Company to handle

the contemporary issues of accounting. In the following parts, the contemporary issues like

compliance with enhancing qualitative characteristics, compliance with fundamental

qualitative characteristics, use of financial statements by the users of company, requirements

by the users to make decisions, assessment of need of the conceptual framework, and

requirements of general purpose financial statements (GPFSs), are evaluated to support

informed debate.

Company Overview- Reliance Worldwide Company

Reliance Worldwide Company is the provider of water control system at international level.

This company provides the plumbing solution for local application, industrial application and

corporate applications. This Reliance Worldwide Company is established in year 1949; the

family of Reliance Worldwide Company of brands has frequently developed to go above

industrial standards at international level with varied operations related to the manufacturing

and distribution diagonally 3 continents. Reliance Worldwide Company has devoted more

than sixty years to the production, brand and product. This company promises to make

innovation through making investment in high-value mechanization to stay competitive in the

international atmosphere. Various product lines are truthfully the entire package of water

control solution, and achieved something on the global stage with the smooth approaches of

functions and local centres of superiority across the portfolio of corporation. The capacities of

production and distribution are the drivers of product lines of the leading market everywhere

Introduction

The accounting is constantly advancing, significantly affected by exterior elements in the

markets globally. The contemporary issues are the issues, which are faced by the

professionals of accounting. This report directs the Reliance Worldwide Company to handle

the contemporary issues of accounting. In the following parts, the contemporary issues like

compliance with enhancing qualitative characteristics, compliance with fundamental

qualitative characteristics, use of financial statements by the users of company, requirements

by the users to make decisions, assessment of need of the conceptual framework, and

requirements of general purpose financial statements (GPFSs), are evaluated to support

informed debate.

Company Overview- Reliance Worldwide Company

Reliance Worldwide Company is the provider of water control system at international level.

This company provides the plumbing solution for local application, industrial application and

corporate applications. This Reliance Worldwide Company is established in year 1949; the

family of Reliance Worldwide Company of brands has frequently developed to go above

industrial standards at international level with varied operations related to the manufacturing

and distribution diagonally 3 continents. Reliance Worldwide Company has devoted more

than sixty years to the production, brand and product. This company promises to make

innovation through making investment in high-value mechanization to stay competitive in the

international atmosphere. Various product lines are truthfully the entire package of water

control solution, and achieved something on the global stage with the smooth approaches of

functions and local centres of superiority across the portfolio of corporation. The capacities of

production and distribution are the drivers of product lines of the leading market everywhere

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

in the world, involving Reliance Water Controls, RMC, Ryemetal and Titon (Annual report,

2018).

Conceptual framework- measurement of financial statement

The major purpose of the conceptual framework is that the conceptual framework gives

the framework to establish the accounting standards, the reasons to solve the disputes related

the accounting and finance, and the fundamental principles that don’t have to be taking place

in the accounting standards (Ridker, et. al, 2017). The conceptual framework’s measurement

requirements include the general purpose financial reporting; the financial reporting’s aims,

fundamental qualitative characteristics related to accounting data, the measurements of

financial statement, and the financial statement’s fundamental features.

The annual report of the Reliance Worldwide Company has been made and presented the

financial statements as per the requirements of the Corporation Act 2001, the announcement

of AASB, and the of Australian Accounting standards. The financial statements of entity are

complied with the Australian IFRS issued by IASB and Australian Accounting Standards. In

addition, the financial statements of company comply with and the accounting standards and

the Corporations Regulations 2001. Considering the director’s resolution of the Reliance

Worldwide Company, it can be stated that the financial statements are prepared as per the

Corporation Act 2001. The financial statements of corporation give true and fair view of

financial positions and corporation’s performances (Kelley and Knowles, 2016). Reliance

Worldwide Company follows accounting policies to make basis for valuation of assets,

liabilities, income, equity and expenses. It can be observed from the annual report of

company-

in the world, involving Reliance Water Controls, RMC, Ryemetal and Titon (Annual report,

2018).

Conceptual framework- measurement of financial statement

The major purpose of the conceptual framework is that the conceptual framework gives

the framework to establish the accounting standards, the reasons to solve the disputes related

the accounting and finance, and the fundamental principles that don’t have to be taking place

in the accounting standards (Ridker, et. al, 2017). The conceptual framework’s measurement

requirements include the general purpose financial reporting; the financial reporting’s aims,

fundamental qualitative characteristics related to accounting data, the measurements of

financial statement, and the financial statement’s fundamental features.

The annual report of the Reliance Worldwide Company has been made and presented the

financial statements as per the requirements of the Corporation Act 2001, the announcement

of AASB, and the of Australian Accounting standards. The financial statements of entity are

complied with the Australian IFRS issued by IASB and Australian Accounting Standards. In

addition, the financial statements of company comply with and the accounting standards and

the Corporations Regulations 2001. Considering the director’s resolution of the Reliance

Worldwide Company, it can be stated that the financial statements are prepared as per the

Corporation Act 2001. The financial statements of corporation give true and fair view of

financial positions and corporation’s performances (Kelley and Knowles, 2016). Reliance

Worldwide Company follows accounting policies to make basis for valuation of assets,

liabilities, income, equity and expenses. It can be observed from the annual report of

company-

REPORT 5

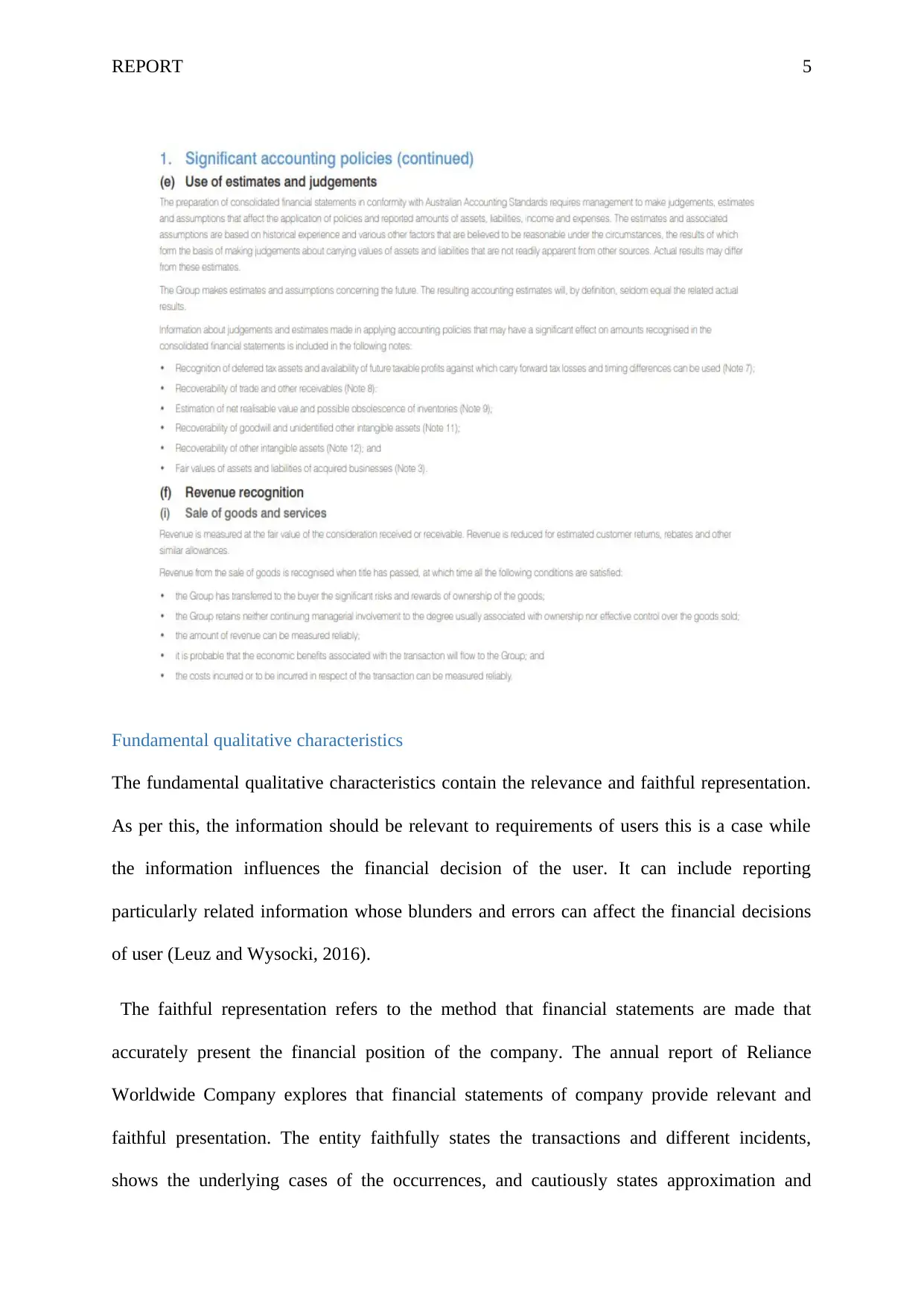

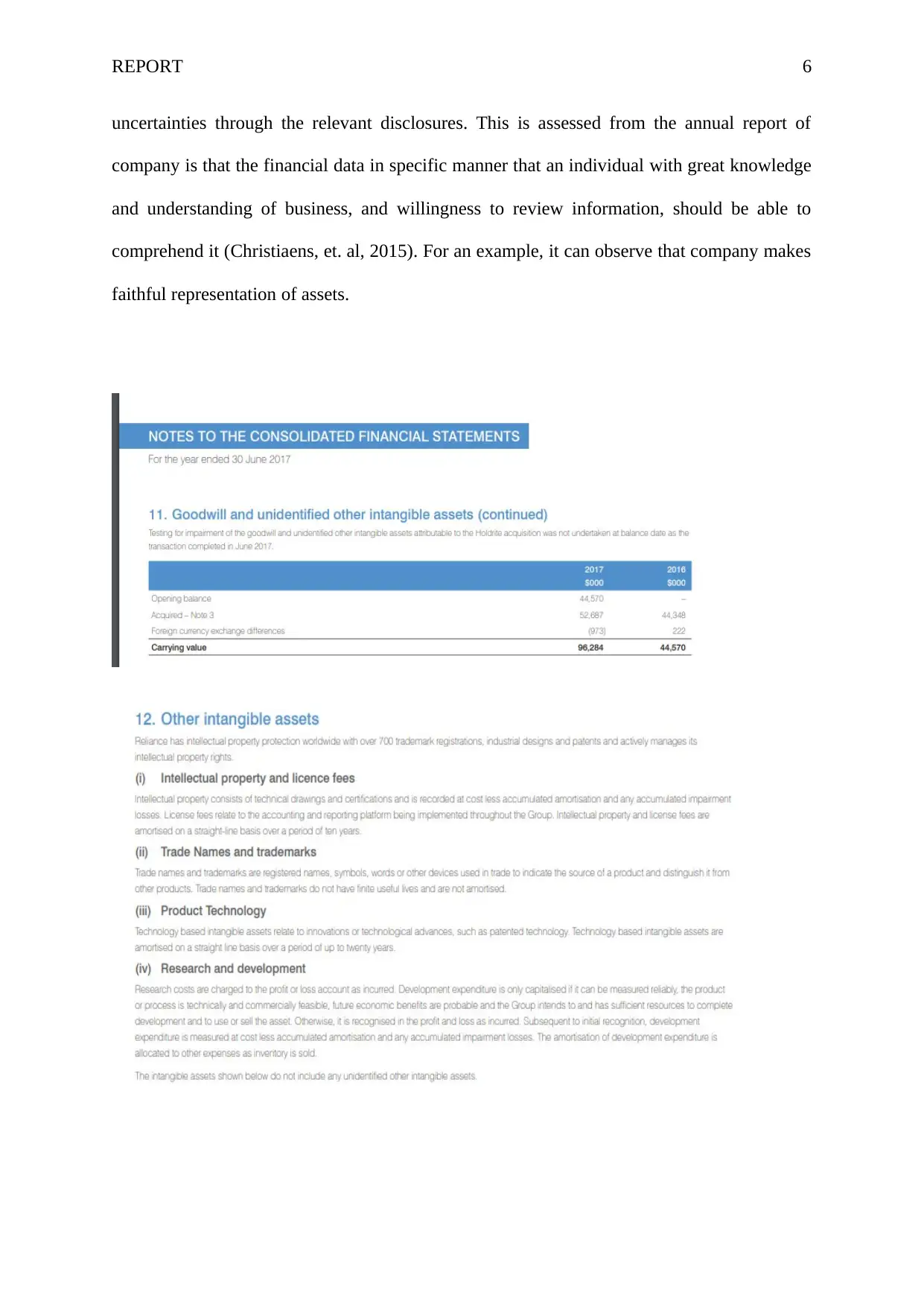

Fundamental qualitative characteristics

The fundamental qualitative characteristics contain the relevance and faithful representation.

As per this, the information should be relevant to requirements of users this is a case while

the information influences the financial decision of the user. It can include reporting

particularly related information whose blunders and errors can affect the financial decisions

of user (Leuz and Wysocki, 2016).

The faithful representation refers to the method that financial statements are made that

accurately present the financial position of the company. The annual report of Reliance

Worldwide Company explores that financial statements of company provide relevant and

faithful presentation. The entity faithfully states the transactions and different incidents,

shows the underlying cases of the occurrences, and cautiously states approximation and

Fundamental qualitative characteristics

The fundamental qualitative characteristics contain the relevance and faithful representation.

As per this, the information should be relevant to requirements of users this is a case while

the information influences the financial decision of the user. It can include reporting

particularly related information whose blunders and errors can affect the financial decisions

of user (Leuz and Wysocki, 2016).

The faithful representation refers to the method that financial statements are made that

accurately present the financial position of the company. The annual report of Reliance

Worldwide Company explores that financial statements of company provide relevant and

faithful presentation. The entity faithfully states the transactions and different incidents,

shows the underlying cases of the occurrences, and cautiously states approximation and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

uncertainties through the relevant disclosures. This is assessed from the annual report of

company is that the financial data in specific manner that an individual with great knowledge

and understanding of business, and willingness to review information, should be able to

comprehend it (Christiaens, et. al, 2015). For an example, it can observe that company makes

faithful representation of assets.

uncertainties through the relevant disclosures. This is assessed from the annual report of

company is that the financial data in specific manner that an individual with great knowledge

and understanding of business, and willingness to review information, should be able to

comprehend it (Christiaens, et. al, 2015). For an example, it can observe that company makes

faithful representation of assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

Enhancing qualitative characteristics

. The enhancing qualitative characteristics are describes as follows-

1. Understand ability- The Understand ability requires financial information to be

apparent or clear to the users, who have relevant knowledge related to the

financial functions and the business. For great understanding, it is needed that the

data should be described evidently and rapidly. However, it is unfortunate to ban

tricky things only for making the reports easy and logical.

2. Comparability- As per this enhancing qualitative characteristic, the comparable

data makes capable the comparison between the corporation and across

corporations. When comparison is conducted in an entity, data are compared from

one accounting period to other accounting period (Epstein, et. al, 2016).

3. Verifiability- The accounting result of company is verifiable at the time of

reproduction. For providing the same data and expectation, the independent

Enhancing qualitative characteristics

. The enhancing qualitative characteristics are describes as follows-

1. Understand ability- The Understand ability requires financial information to be

apparent or clear to the users, who have relevant knowledge related to the

financial functions and the business. For great understanding, it is needed that the

data should be described evidently and rapidly. However, it is unfortunate to ban

tricky things only for making the reports easy and logical.

2. Comparability- As per this enhancing qualitative characteristic, the comparable

data makes capable the comparison between the corporation and across

corporations. When comparison is conducted in an entity, data are compared from

one accounting period to other accounting period (Epstein, et. al, 2016).

3. Verifiability- The accounting result of company is verifiable at the time of

reproduction. For providing the same data and expectation, the independent

REPORT 8

accountant might get same results the organisation did (Ahmed, Mahmood and

Islam, 2016). The verifiability is helpful in helping that data faithfully states the

financial phenomena it purports to state. In different terms, it can say that the

specialists may receive the consents that the precise representations are the

faithful representation.

4. Timeliness- The timeliness of accounting data is provision of information to use

rapidly sufficient for them to take step. The data become out-dated and

impractical in the case where this is not reported in prescribed period.

In this way, the company has followed these enhancing qualitative characteristics.

Requirement of financial statements for the users of company

The financial statements are very useful and helpful for various users of the company. These

users of company are the investors, lenders, potential investors and creditors. These financial

statements can be helpful for investors, lenders, potential investors and creditors to take quick

and relevant decisions. By considering the annual report of the Reliance Worldwide

Company, it can be said that the financial data are required by the shareholders and investors

to take financial decision and more relevant decisions. In addition, the bank’s lenders or

financial institution’s lenders are desired to have the knowledge of ability of the corporation

to pay liabilities at the time of maturity. Besides this, the financial data are required by the

creditors to have the ability to make pay the obligations by company at a time when they

become payable (Sampaio and González, 2017). The annual report of company discovers that

the financial statements do not only give basic knowledge of accounting but also the

knowledge of advanced features and practices of the accounting. The company’s users will be

able to know the IFRS and International Accounting Standards from company’s financial

statements. In this way, they can handle or manage the transactions according to the

Australian Accounting Standards.

accountant might get same results the organisation did (Ahmed, Mahmood and

Islam, 2016). The verifiability is helpful in helping that data faithfully states the

financial phenomena it purports to state. In different terms, it can say that the

specialists may receive the consents that the precise representations are the

faithful representation.

4. Timeliness- The timeliness of accounting data is provision of information to use

rapidly sufficient for them to take step. The data become out-dated and

impractical in the case where this is not reported in prescribed period.

In this way, the company has followed these enhancing qualitative characteristics.

Requirement of financial statements for the users of company

The financial statements are very useful and helpful for various users of the company. These

users of company are the investors, lenders, potential investors and creditors. These financial

statements can be helpful for investors, lenders, potential investors and creditors to take quick

and relevant decisions. By considering the annual report of the Reliance Worldwide

Company, it can be said that the financial data are required by the shareholders and investors

to take financial decision and more relevant decisions. In addition, the bank’s lenders or

financial institution’s lenders are desired to have the knowledge of ability of the corporation

to pay liabilities at the time of maturity. Besides this, the financial data are required by the

creditors to have the ability to make pay the obligations by company at a time when they

become payable (Sampaio and González, 2017). The annual report of company discovers that

the financial statements do not only give basic knowledge of accounting but also the

knowledge of advanced features and practices of the accounting. The company’s users will be

able to know the IFRS and International Accounting Standards from company’s financial

statements. In this way, they can handle or manage the transactions according to the

Australian Accounting Standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

General purpose financial statements

The general-purpose financial statements are very useful for the investors, lenders, potential

investors and creditors and lenders in a procedure related to the decisions taking. The income

statement, balance sheet, the statement of equity of owner or statement of retained earnings,

and cash flow statement are considered as general-purpose financial statements. These

financial statements are considered as general purpose financial statements, prepared by the

for-profit entity, as per the requirements of the Corporations Act 2001, the Accounting

Standards of Australia and the reliable pronouncements of Accounting Standard Australian

Board. Reliance Worldwide Company prepares and presents the income statement, balance

sheet, the statement of equity, the retained earnings statement, and statement of cash flow

(Leuz and Wysocki, 2016).

1. Historical cost principle- The financial statements of company have prepared as

per the historical cost except the land & building and derivative financial

instruments that measured at the fair value.

2. Terminologies utilised in the financial statements of company- In the financial

statements, reference to we, us, brands, RWC family, all are considered as the

Reliance Worldwide Company.

3. Compliance with IFRS- The financial statements of Reliance Worldwide

Company comply with IFRS issued by International Accounting Standard Board.

4. Required accounting estimates- to make the financial statements, numerous

significant accounting estimates are needed. It also requires the management to

use the judgements in an application’s procedure and the accounting policies of

entities (Henderson, et. al, 2015). It can be observed from annual report of

company that the general purpose financial statements comply with the

General purpose financial statements

The general-purpose financial statements are very useful for the investors, lenders, potential

investors and creditors and lenders in a procedure related to the decisions taking. The income

statement, balance sheet, the statement of equity of owner or statement of retained earnings,

and cash flow statement are considered as general-purpose financial statements. These

financial statements are considered as general purpose financial statements, prepared by the

for-profit entity, as per the requirements of the Corporations Act 2001, the Accounting

Standards of Australia and the reliable pronouncements of Accounting Standard Australian

Board. Reliance Worldwide Company prepares and presents the income statement, balance

sheet, the statement of equity, the retained earnings statement, and statement of cash flow

(Leuz and Wysocki, 2016).

1. Historical cost principle- The financial statements of company have prepared as

per the historical cost except the land & building and derivative financial

instruments that measured at the fair value.

2. Terminologies utilised in the financial statements of company- In the financial

statements, reference to we, us, brands, RWC family, all are considered as the

Reliance Worldwide Company.

3. Compliance with IFRS- The financial statements of Reliance Worldwide

Company comply with IFRS issued by International Accounting Standard Board.

4. Required accounting estimates- to make the financial statements, numerous

significant accounting estimates are needed. It also requires the management to

use the judgements in an application’s procedure and the accounting policies of

entities (Henderson, et. al, 2015). It can be observed from annual report of

company that the general purpose financial statements comply with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

Corporation Act 2001 and AASBs. The consolidation financial statements comply

with IFRS and IASB.

Conclusion

In the conclusion, it is stated that the conceptual framework is very essential for the

companies. Otherwise, the accounting system prepared on the basis of rules, may be made

having the objective that a treatment of each transaction of accounting must be dealt with by

proper particular rules, or the provisions. The accounting system made on the basis of rules,

is very rigid and inflexible; though has the magnetism of financial statements being same and

reliable. Therefore, it is recommended to utilise the conceptual framework to give the

fundamental principles to enhance the setting of standards for the finance and accounting.

Corporation Act 2001 and AASBs. The consolidation financial statements comply

with IFRS and IASB.

Conclusion

In the conclusion, it is stated that the conceptual framework is very essential for the

companies. Otherwise, the accounting system prepared on the basis of rules, may be made

having the objective that a treatment of each transaction of accounting must be dealt with by

proper particular rules, or the provisions. The accounting system made on the basis of rules,

is very rigid and inflexible; though has the magnetism of financial statements being same and

reliable. Therefore, it is recommended to utilise the conceptual framework to give the

fundamental principles to enhance the setting of standards for the finance and accounting.

REPORT 11

References

Ahmed, M., Mahmood, A.N. and Islam, M.R. (2016) A survey of anomaly detection

techniques in financial domain. Future Generation Computer Systems, 55, pp.278-288.

Annual Report (2018) Reliance Worldwide Company. [Online] Available at:

https://www.rwc.com/sites/g/files/rgohfh266/files/2019-02/2017%20Annual

%20Report_0.pdf [Accessed 16/4/2019]

Christiaens, J., Vanhee, C., Manes-Rossi, F., Aversano, N. and Van Cauwenberge, P.,(2015.

0The effect of IPSAS on reforming governmental financial reporting: An international

comparison. International Review of Administrative Sciences, 81(1), pp.158-177.

Epstein, J.I., Zelefsky, M.J., Sjoberg, D.D., Nelson, J.B., Egevad, L., Magi-Galluzzi, C.,

Vickers, A.J., Parwani, A.V., Reuter, V.E., Fine, S.W. and Eastham, J.A. (2016) A

contemporary prostate cancer grading system: a validated alternative to the Gleason

score. European urology, 69(3), pp.428-435.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., (2015) Issues in financial

accounting. Pearson Higher Education AU.

Kelley, T.R. and Knowles, J.G. (2016) A conceptual framework for integrated STEM

education. International Journal of STEM Education, 3(1), p.11.

Leuz, C. and Wysocki, P.D. (2016) The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting

Research, 54(2), pp.525-622.

References

Ahmed, M., Mahmood, A.N. and Islam, M.R. (2016) A survey of anomaly detection

techniques in financial domain. Future Generation Computer Systems, 55, pp.278-288.

Annual Report (2018) Reliance Worldwide Company. [Online] Available at:

https://www.rwc.com/sites/g/files/rgohfh266/files/2019-02/2017%20Annual

%20Report_0.pdf [Accessed 16/4/2019]

Christiaens, J., Vanhee, C., Manes-Rossi, F., Aversano, N. and Van Cauwenberge, P.,(2015.

0The effect of IPSAS on reforming governmental financial reporting: An international

comparison. International Review of Administrative Sciences, 81(1), pp.158-177.

Epstein, J.I., Zelefsky, M.J., Sjoberg, D.D., Nelson, J.B., Egevad, L., Magi-Galluzzi, C.,

Vickers, A.J., Parwani, A.V., Reuter, V.E., Fine, S.W. and Eastham, J.A. (2016) A

contemporary prostate cancer grading system: a validated alternative to the Gleason

score. European urology, 69(3), pp.428-435.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., (2015) Issues in financial

accounting. Pearson Higher Education AU.

Kelley, T.R. and Knowles, J.G. (2016) A conceptual framework for integrated STEM

education. International Journal of STEM Education, 3(1), p.11.

Leuz, C. and Wysocki, P.D. (2016) The economics of disclosure and financial reporting

regulation: Evidence and suggestions for future research. Journal of Accounting

Research, 54(2), pp.525-622.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.