Comprehensive Analysis of Management Accounting for Renishaw Company

VerifiedAdded on 2021/02/20

|17

|5001

|30

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on the application of various systems within the context of Renishaw Company. It begins by defining management accounting and its significance, differentiating it from financial accounting, and exploring different types of management accounting systems like cost accounting and inventory management. The report delves into cost accounting, standard costing, and activity-based costing. It also examines the importance of cost accounting in cost control, price determination, and fixing standards. Furthermore, it analyzes various management accounting reports, including budget reports, job cost reports, performance reports, and cost accounting reports. The report then explores the concepts of marginal costing and absorption costing, including their formulas. Finally, it touches upon planning tools for budgetary control and how organizations adapt management accounting in response to financial problems. The report provides a detailed analysis of financial planning, decision making, and the overall importance of management accounting in an organization.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P1 What is management accounting and its important of different types of management

accounting systems......................................................................................................................1

P2 Different types of management accounting reports................................................................4

LO 2.................................................................................................................................................5

P3 Income statement using marginal costing and absorption costing.........................................5

LO 3.................................................................................................................................................8

P4 Types of planning tools for budgetary control......................................................................8

P5 How organisations are adapt management accounting in responding financial problems...11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P1 What is management accounting and its important of different types of management

accounting systems......................................................................................................................1

P2 Different types of management accounting reports................................................................4

LO 2.................................................................................................................................................5

P3 Income statement using marginal costing and absorption costing.........................................5

LO 3.................................................................................................................................................8

P4 Types of planning tools for budgetary control......................................................................8

P5 How organisations are adapt management accounting in responding financial problems...11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Managerial accounting is also known as the management or cost accounting, focused n

the inside formation which can received through financial accounting. Managerial accounting is

concern with the field of accounting which assist in analysing, offering the information related to

the cost to the internal managerial process. it has objective such as controlling, planning and also

the decision making (Gibassier and Schaltegger, 2015). This report is based on Renishaw

company is one of the world's leading engineering and science technology which is expert in the

precise measurement and also the healthcare. It supply products and services which is used in the

application such as jet engine, wind turbine. This group currently had more than 80 offices in 36

countries and around 3,000 are employees worked here Present report lay emphasis on the about

the various management accounting system with the necessary requirements as well as the

managerial reports .it will also focus on the techniques of cost analysis ,preparation for the

income statement by using the marginal as well as the absorption costing.

LO 1

P1 What is management accounting and its important of different types of management

accounting systems.

Management Accounting:

Management accounting considers as the process of measuring, recognising, interpreting,

evaluating and communicating the financial information in the pursuance to accomplish the goal

of the company. It is also mentioned as the cost accounting. To distinguish the financial

accounting and the management accounting is that in management accounting its goal is to

assisting the mangers within an organisation while the financial accounting aimed is to targeting

to provide the information to the external parties of a company (Taylor and Scapens, 2016).

Accounting considers as the process of measurement, identification as well as

communication of the economical data that allows the informed decisions and the judgements by

the data users according to the (AAA) American Accounting Association thus there are various

types of the engagement accounting systems that involved different accounting objectives,

elements as well as the functions.

Cost accounting

Managerial accounting is also known as the management or cost accounting, focused n

the inside formation which can received through financial accounting. Managerial accounting is

concern with the field of accounting which assist in analysing, offering the information related to

the cost to the internal managerial process. it has objective such as controlling, planning and also

the decision making (Gibassier and Schaltegger, 2015). This report is based on Renishaw

company is one of the world's leading engineering and science technology which is expert in the

precise measurement and also the healthcare. It supply products and services which is used in the

application such as jet engine, wind turbine. This group currently had more than 80 offices in 36

countries and around 3,000 are employees worked here Present report lay emphasis on the about

the various management accounting system with the necessary requirements as well as the

managerial reports .it will also focus on the techniques of cost analysis ,preparation for the

income statement by using the marginal as well as the absorption costing.

LO 1

P1 What is management accounting and its important of different types of management

accounting systems.

Management Accounting:

Management accounting considers as the process of measuring, recognising, interpreting,

evaluating and communicating the financial information in the pursuance to accomplish the goal

of the company. It is also mentioned as the cost accounting. To distinguish the financial

accounting and the management accounting is that in management accounting its goal is to

assisting the mangers within an organisation while the financial accounting aimed is to targeting

to provide the information to the external parties of a company (Taylor and Scapens, 2016).

Accounting considers as the process of measurement, identification as well as

communication of the economical data that allows the informed decisions and the judgements by

the data users according to the (AAA) American Accounting Association thus there are various

types of the engagement accounting systems that involved different accounting objectives,

elements as well as the functions.

Cost accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is an accounting method whose goals is to capturing the cost of production of

Renishaw company through each step of the input cost also with the fixed cost. Firstly, it is

measures and record the cost on an individual basis then compare the input consequence to the

output consequence which assist the management of the company in analysing and measuring

the financial performance. The cost accounting system which allocates the cost either activity

based or traditional based costing system (Armitage, Webb and Glynn, 2016).

Cost accounting is also used in an organisation to help in decision making and financial

accounting differs in the representation of the cost as well as the financial performance which

includes organisation assets and liabilities. Cost accounting would most beneficial tool for the

managing tool and also in setting up the control programs which can amend net margins for an

organisation on the future references (Kastberg and Siverbo, 2016).

there are two main types of cost accounting given below

Standard cost accounting it can use the ration to the cost effective use of the materials

in the developing products as well as services.

Activity based costing here cost is monitored on the basis of the activities and resources

which are consumed by each activity as well the final output that can determines the cost of the

product.

it is beneficial for the Renishaw company manufactures company to measure, analyse ,

profitable, unprofitable activities ,to do proper training ,control and fully utilisation of the

resources which helps in the decision making regarding to the labours and machines

(Rikhardsson and Yigitbasioglu, 2018).

Importance of cost accounting

Classification of cost- cost accounting is the specialised branch which deals with the

classification well as recording of cost. For example-direct cost, prime cost selling coast and

factory cost..this classification allows the management to calculate the efficiency and also

control the cost and profitability of such kind of process as well as activities.

Cost control -it focuses on controlling the cost of labour, and various other costs .for

example by applying the labour cost and also the capacity of the machines which can boost their

efficient as well.

Renishaw company through each step of the input cost also with the fixed cost. Firstly, it is

measures and record the cost on an individual basis then compare the input consequence to the

output consequence which assist the management of the company in analysing and measuring

the financial performance. The cost accounting system which allocates the cost either activity

based or traditional based costing system (Armitage, Webb and Glynn, 2016).

Cost accounting is also used in an organisation to help in decision making and financial

accounting differs in the representation of the cost as well as the financial performance which

includes organisation assets and liabilities. Cost accounting would most beneficial tool for the

managing tool and also in setting up the control programs which can amend net margins for an

organisation on the future references (Kastberg and Siverbo, 2016).

there are two main types of cost accounting given below

Standard cost accounting it can use the ration to the cost effective use of the materials

in the developing products as well as services.

Activity based costing here cost is monitored on the basis of the activities and resources

which are consumed by each activity as well the final output that can determines the cost of the

product.

it is beneficial for the Renishaw company manufactures company to measure, analyse ,

profitable, unprofitable activities ,to do proper training ,control and fully utilisation of the

resources which helps in the decision making regarding to the labours and machines

(Rikhardsson and Yigitbasioglu, 2018).

Importance of cost accounting

Classification of cost- cost accounting is the specialised branch which deals with the

classification well as recording of cost. For example-direct cost, prime cost selling coast and

factory cost..this classification allows the management to calculate the efficiency and also

control the cost and profitability of such kind of process as well as activities.

Cost control -it focuses on controlling the cost of labour, and various other costs .for

example by applying the labour cost and also the capacity of the machines which can boost their

efficient as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price determination- cost accounting allows the management of the renishaw to find the

most perfect price for the product and services. Not too high and not too low. For example-when

the recession occurs and economy suffers a lot then the businessman has lowers the prices of

their product to survive in the circumstances (Kamal, 2015).

Fixing of standards-Company can use some standards to make the estimate and the

budget for the future references. Company can use these basis to analyse the efficiency of the

department.

Importance of costing to others:

Government- costing helps the government for the liabilities like income tax any other

such liabilities. It assists to set the industry standard and also help with the price fixing ,cost

control and also tariff plans.

Customers- its main aim are cost control and improvement of efficiency .both of these

were beneficial for the organisation and this benefit ultimately pass to the custom for the product

and services.

Inventory management system

it is a process of ordering and storing by using a company's inventory. it includes the

components of the raw material ,finished product and also the warehousing and processing with

such items (Ossimitz, Wieder and Chapman, 2016). For the organisation which has complex

supply chains and complex manufacturing process the risk if inventory oversupply and shortage

is more difficult to overcome such problems' management can developed two methods just in

time (JIT)and materials requirement planning (MRP).

importance of the inventory managements- Reducing risk shortages-to avoid or to minimize the shortage of the raw materials

company can maintain the larger inventories. Here the organised inventory results into

the more efficient present as well as future. it also includes cost saving and improvement

in the product. Increased efficiency and productivity-with the proper management of the inventory there

is less time and resources spent in managing as well as allocated to the other area. here

technology plays a greater role to speed up tracking and full fill the operational needs

most perfect price for the product and services. Not too high and not too low. For example-when

the recession occurs and economy suffers a lot then the businessman has lowers the prices of

their product to survive in the circumstances (Kamal, 2015).

Fixing of standards-Company can use some standards to make the estimate and the

budget for the future references. Company can use these basis to analyse the efficiency of the

department.

Importance of costing to others:

Government- costing helps the government for the liabilities like income tax any other

such liabilities. It assists to set the industry standard and also help with the price fixing ,cost

control and also tariff plans.

Customers- its main aim are cost control and improvement of efficiency .both of these

were beneficial for the organisation and this benefit ultimately pass to the custom for the product

and services.

Inventory management system

it is a process of ordering and storing by using a company's inventory. it includes the

components of the raw material ,finished product and also the warehousing and processing with

such items (Ossimitz, Wieder and Chapman, 2016). For the organisation which has complex

supply chains and complex manufacturing process the risk if inventory oversupply and shortage

is more difficult to overcome such problems' management can developed two methods just in

time (JIT)and materials requirement planning (MRP).

importance of the inventory managements- Reducing risk shortages-to avoid or to minimize the shortage of the raw materials

company can maintain the larger inventories. Here the organised inventory results into

the more efficient present as well as future. it also includes cost saving and improvement

in the product. Increased efficiency and productivity-with the proper management of the inventory there

is less time and resources spent in managing as well as allocated to the other area. here

technology plays a greater role to speed up tracking and full fill the operational needs

also ensuring inventory record that are accurate (Nuhu, Baird and Bala Appuhamilage,

2017). Save time and money- due to improved efficiency, product flow and also well

management of the inventory results into the saved time and money.

Improved accuracy of inventory orders-for the accuracy of the product orders, status as

well as tracking.

P2 Different types of management accounting reports

Managerial accounting reports are the tools which provided the information needer to

trim the cost, also reward the high performing staff members and invests in the services and the

goods that can offers the best financial return to the Renishaw company. it depends on the type

of the project that undertakes by the company. The time sensitivity of the financial information

that may request or they generate reports that are quarterly, monthly and weekly even on daily

basis as well (Bennett and James, 2017).

These are the reports that are continuously generated throughout the accounting and the

bookkeeping period as per the requirement. as many decisions are depends on the authenticity of

the reports ,they should be more careful adapt by the experts in bookkeeping .Managers of the

Reinshaw company carefully scrutinised the focused on the certain patterns and know to convert

them into useful information for the organisation. Given below are the examples of the such

types of the reports.

Budget report-these reports are very critical in evaluating the performance of the

Reinshaw and also generated for the small business, and department wise in additional to the

large organisation however each and every company creates overall budget to understand the

overall schemes of Reinshaw company's business (Alawattage, Wickramasinghe and Uddin,

2017). A budget is estimated on the past experiences .as great budget always ready for the

unseen circumstances that might rise. a budget of the company can list all the sources of earning

as well as expenditures. Every organisation tries to achieve its goal and mission while following

the budgeted amount. Managerial report which is related to the budgeting can support the

mangers to offer the staff members incentives, also cut the cost and renegotiate the terms and

conditions with the suppliers thus budget report has its won significance to any business as it is

a critical analysis.

2017). Save time and money- due to improved efficiency, product flow and also well

management of the inventory results into the saved time and money.

Improved accuracy of inventory orders-for the accuracy of the product orders, status as

well as tracking.

P2 Different types of management accounting reports

Managerial accounting reports are the tools which provided the information needer to

trim the cost, also reward the high performing staff members and invests in the services and the

goods that can offers the best financial return to the Renishaw company. it depends on the type

of the project that undertakes by the company. The time sensitivity of the financial information

that may request or they generate reports that are quarterly, monthly and weekly even on daily

basis as well (Bennett and James, 2017).

These are the reports that are continuously generated throughout the accounting and the

bookkeeping period as per the requirement. as many decisions are depends on the authenticity of

the reports ,they should be more careful adapt by the experts in bookkeeping .Managers of the

Reinshaw company carefully scrutinised the focused on the certain patterns and know to convert

them into useful information for the organisation. Given below are the examples of the such

types of the reports.

Budget report-these reports are very critical in evaluating the performance of the

Reinshaw and also generated for the small business, and department wise in additional to the

large organisation however each and every company creates overall budget to understand the

overall schemes of Reinshaw company's business (Alawattage, Wickramasinghe and Uddin,

2017). A budget is estimated on the past experiences .as great budget always ready for the

unseen circumstances that might rise. a budget of the company can list all the sources of earning

as well as expenditures. Every organisation tries to achieve its goal and mission while following

the budgeted amount. Managerial report which is related to the budgeting can support the

mangers to offer the staff members incentives, also cut the cost and renegotiate the terms and

conditions with the suppliers thus budget report has its won significance to any business as it is

a critical analysis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

job cost report-it is the process which concerns the total cost obtain in a project and also

compared with the expected revenue. It can track the ongoing project in an organisation. This

benefits the company to analyse and evaluate the profitability of a particular job fully to modify

it. it is also helpful; for the company as it recognise the problems and avoided in the future

references. Reinshaw company can track the job cost report in the weekly basis so that the

problems can easily be solved as it can become the worse .it can also tell about the low profit

with the duration of the month or in the quarter ,as it is the consequence of the bad job or

downward trend as in the price of the product (Watson, 2015).

Performance reports-performance reports are created to check the performance of the

Reinshaw company. As the individual employees or in the team members at the end of the term.

There is departmental performance can also generate in the large organisation .managers of the

company can uses the performances to make the important decisions about the future of an

organisation. Individuals can awarded to the commitment to the organisation and under

performance are laid off as required (Christ, Burritt and Varsei, 2016). These reports also offers

deep evaluation into the working of the company .if an employee thinks about the performance

in a certain capacity but due to some reasons it is not happening, this information can points the

flaws. The role of the performance report is important for any organisation to keep an exact

measure of their planning and strategies towards their mission.

Cost accounting reports- all the raw material costs, labour any added costs are taken into

the deliberation the tools are divided by the amount of the products produced. Cost accounting

reports can summarised for all the information. This report offers the mangers of the Reinshaw

company to realize the cost prices as compare to the selling prices. Inventory waste, overhead

labour cost and also the inventory labour cost are all the parts of the managerial accounting

reports. They can provide an accurate understanding of all the expenses which is important for

the better improvement of resources among all the departments (Strauss, Kristandl and Quinn,

2015).

LO 2

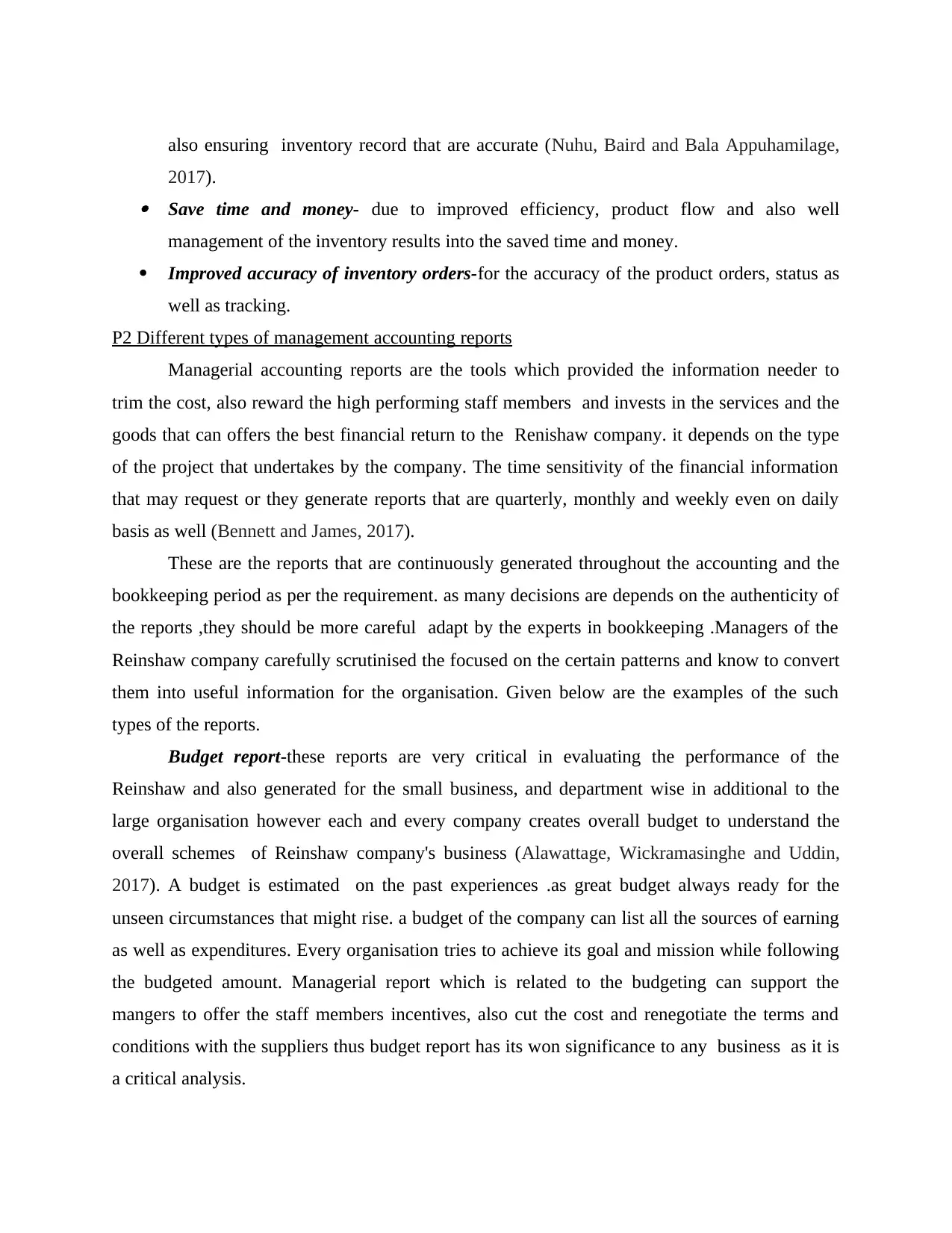

P3 Income statement using marginal costing and absorption costing

Marginal costing:

compared with the expected revenue. It can track the ongoing project in an organisation. This

benefits the company to analyse and evaluate the profitability of a particular job fully to modify

it. it is also helpful; for the company as it recognise the problems and avoided in the future

references. Reinshaw company can track the job cost report in the weekly basis so that the

problems can easily be solved as it can become the worse .it can also tell about the low profit

with the duration of the month or in the quarter ,as it is the consequence of the bad job or

downward trend as in the price of the product (Watson, 2015).

Performance reports-performance reports are created to check the performance of the

Reinshaw company. As the individual employees or in the team members at the end of the term.

There is departmental performance can also generate in the large organisation .managers of the

company can uses the performances to make the important decisions about the future of an

organisation. Individuals can awarded to the commitment to the organisation and under

performance are laid off as required (Christ, Burritt and Varsei, 2016). These reports also offers

deep evaluation into the working of the company .if an employee thinks about the performance

in a certain capacity but due to some reasons it is not happening, this information can points the

flaws. The role of the performance report is important for any organisation to keep an exact

measure of their planning and strategies towards their mission.

Cost accounting reports- all the raw material costs, labour any added costs are taken into

the deliberation the tools are divided by the amount of the products produced. Cost accounting

reports can summarised for all the information. This report offers the mangers of the Reinshaw

company to realize the cost prices as compare to the selling prices. Inventory waste, overhead

labour cost and also the inventory labour cost are all the parts of the managerial accounting

reports. They can provide an accurate understanding of all the expenses which is important for

the better improvement of resources among all the departments (Strauss, Kristandl and Quinn,

2015).

LO 2

P3 Income statement using marginal costing and absorption costing

Marginal costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is defined as the additional cost involved in the production of one extra unit. It can be

computed by assigning total variable cost to one unit. It is used in classification of cost. Cost can

be differentiated on the basis of fixed and variable cost. It also benefits company in determining

price. It helps manager of company to take decisions such as discontinuation of a product or

service and replacing the machines etc (Marginal and absorption costing, 2019). Marginal

costing ascertain the level of activity which reflects the outcome on decrease and increase in

level of production. They are also called variable cost which includes material cost, labour cost

administration and selling overhead. Formula for calculating marginal costing is:

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overheads

Absorption costing:

It is an accounting method to value inventory. It absorbs all the direct cost of

manufacturing such as overhead cost, material cost. It provides exact cost for producing a

computed by assigning total variable cost to one unit. It is used in classification of cost. Cost can

be differentiated on the basis of fixed and variable cost. It also benefits company in determining

price. It helps manager of company to take decisions such as discontinuation of a product or

service and replacing the machines etc (Marginal and absorption costing, 2019). Marginal

costing ascertain the level of activity which reflects the outcome on decrease and increase in

level of production. They are also called variable cost which includes material cost, labour cost

administration and selling overhead. Formula for calculating marginal costing is:

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overheads

Absorption costing:

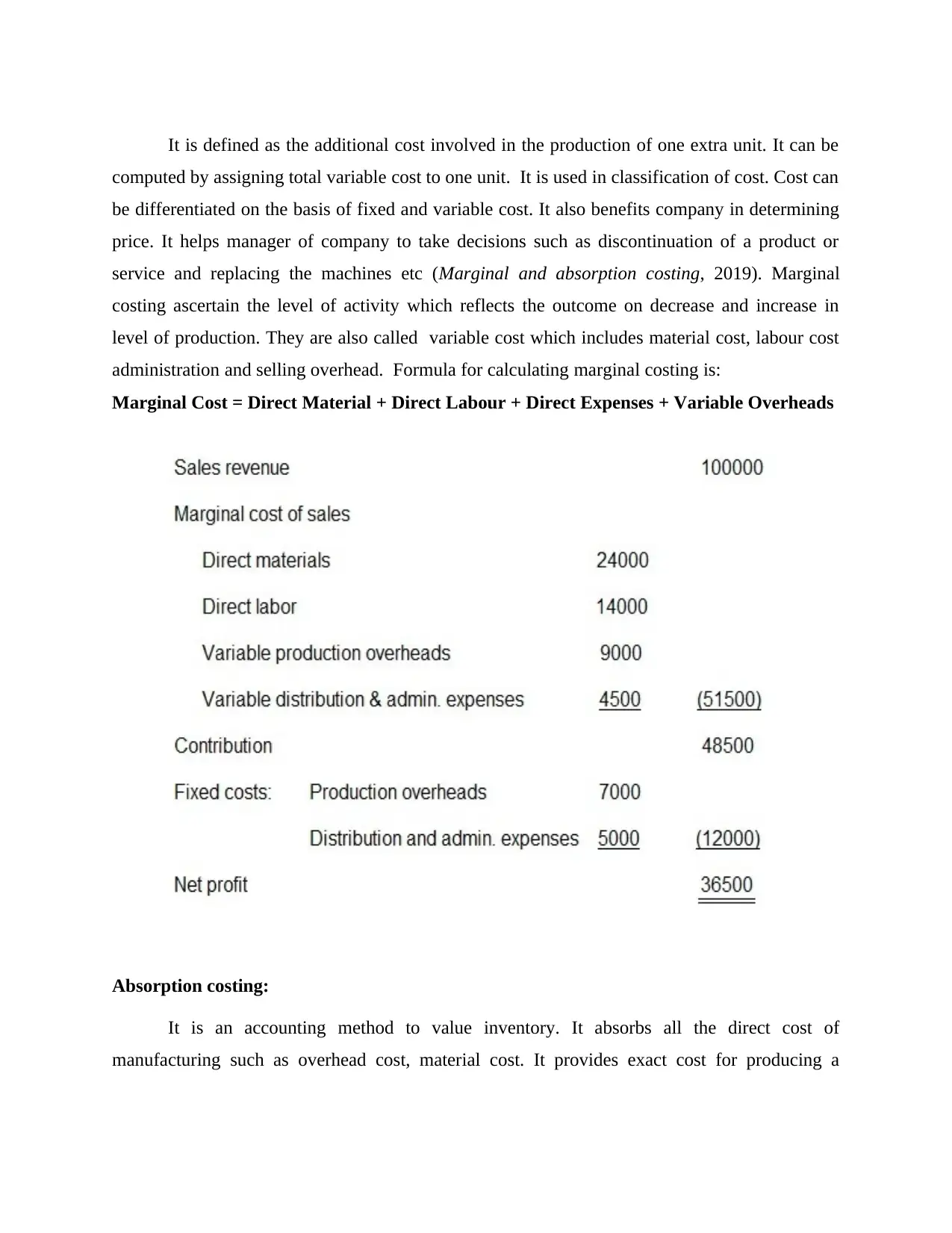

It is an accounting method to value inventory. It absorbs all the direct cost of

manufacturing such as overhead cost, material cost. It provides exact cost for producing a

product. It is better than variable costing. It is a process of adding all the cost manufacturing cost

i.e. direct or indirect cost to find out the accurate cost. Renishaw company will benefit from

absorption costing by preparing accurate financial statements, there is no need to differentiate

between variable and fixed cost. As the name says, it absorbs all the cost of production of each

unit therefore if more units are produced cost of each unit will be lower (Marginal and absorption

costing, 2019). Both the costing techniques generate different profits because marginal costing

uses only direct expenses and absorption costing uses both direct and indirect costing. Formula

for calculating absorption costing is:

Absorption cost formula = Direct labor cost per unit + Direct material cost per unit +

Variable manufacturing overhead cost per unit + Fixed manufacturing overhead per unit

Interpretation:

From the above income statement prepared by using marginal and absorption costing it

can be interpreted that while using marginal costing all the direct expenses of £51500 are

i.e. direct or indirect cost to find out the accurate cost. Renishaw company will benefit from

absorption costing by preparing accurate financial statements, there is no need to differentiate

between variable and fixed cost. As the name says, it absorbs all the cost of production of each

unit therefore if more units are produced cost of each unit will be lower (Marginal and absorption

costing, 2019). Both the costing techniques generate different profits because marginal costing

uses only direct expenses and absorption costing uses both direct and indirect costing. Formula

for calculating absorption costing is:

Absorption cost formula = Direct labor cost per unit + Direct material cost per unit +

Variable manufacturing overhead cost per unit + Fixed manufacturing overhead per unit

Interpretation:

From the above income statement prepared by using marginal and absorption costing it

can be interpreted that while using marginal costing all the direct expenses of £51500 are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

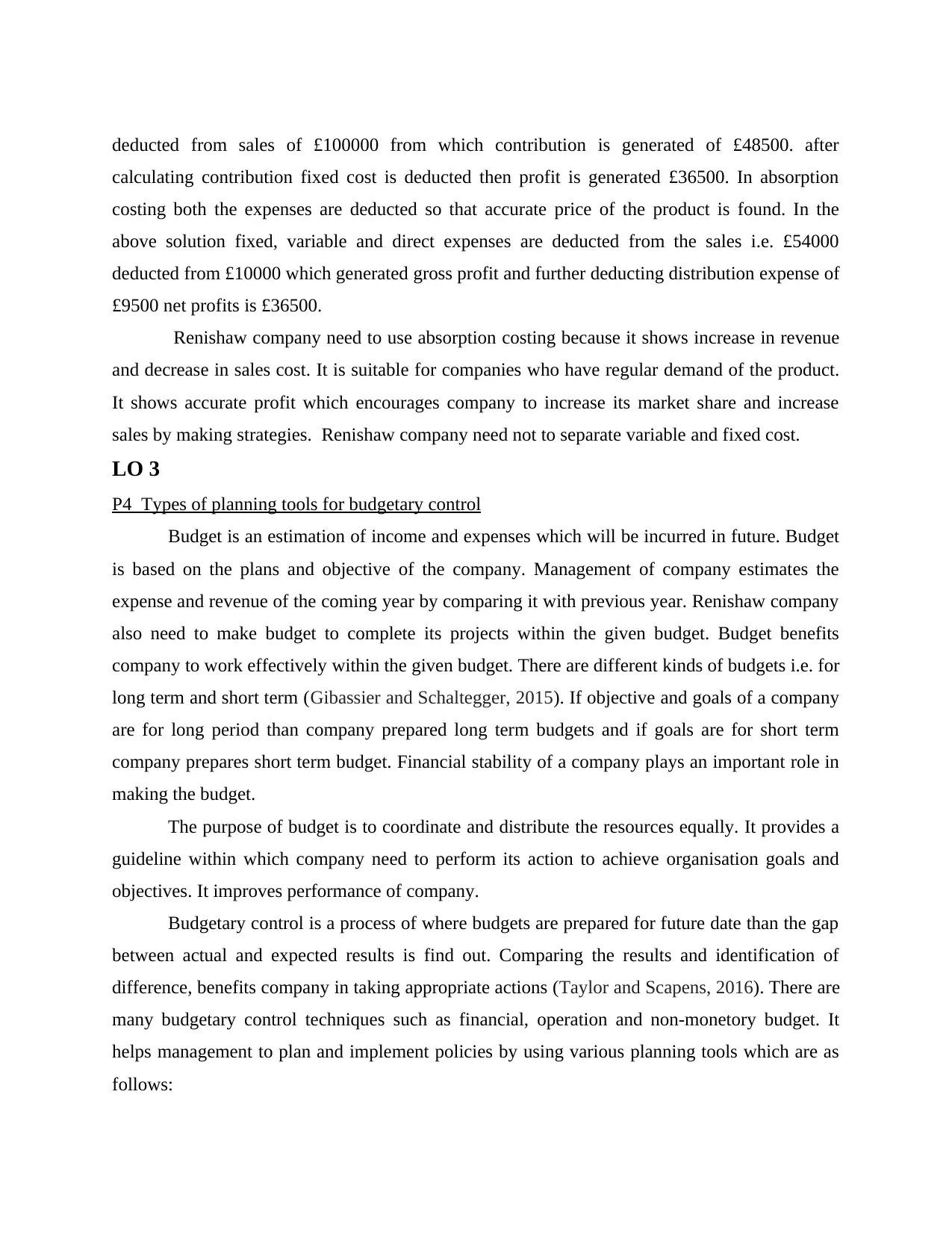

deducted from sales of £100000 from which contribution is generated of £48500. after

calculating contribution fixed cost is deducted then profit is generated £36500. In absorption

costing both the expenses are deducted so that accurate price of the product is found. In the

above solution fixed, variable and direct expenses are deducted from the sales i.e. £54000

deducted from £10000 which generated gross profit and further deducting distribution expense of

£9500 net profits is £36500.

Renishaw company need to use absorption costing because it shows increase in revenue

and decrease in sales cost. It is suitable for companies who have regular demand of the product.

It shows accurate profit which encourages company to increase its market share and increase

sales by making strategies. Renishaw company need not to separate variable and fixed cost.

LO 3

P4 Types of planning tools for budgetary control

Budget is an estimation of income and expenses which will be incurred in future. Budget

is based on the plans and objective of the company. Management of company estimates the

expense and revenue of the coming year by comparing it with previous year. Renishaw company

also need to make budget to complete its projects within the given budget. Budget benefits

company to work effectively within the given budget. There are different kinds of budgets i.e. for

long term and short term (Gibassier and Schaltegger, 2015). If objective and goals of a company

are for long period than company prepared long term budgets and if goals are for short term

company prepares short term budget. Financial stability of a company plays an important role in

making the budget.

The purpose of budget is to coordinate and distribute the resources equally. It provides a

guideline within which company need to perform its action to achieve organisation goals and

objectives. It improves performance of company.

Budgetary control is a process of where budgets are prepared for future date than the gap

between actual and expected results is find out. Comparing the results and identification of

difference, benefits company in taking appropriate actions (Taylor and Scapens, 2016). There are

many budgetary control techniques such as financial, operation and non-monetory budget. It

helps management to plan and implement policies by using various planning tools which are as

follows:

calculating contribution fixed cost is deducted then profit is generated £36500. In absorption

costing both the expenses are deducted so that accurate price of the product is found. In the

above solution fixed, variable and direct expenses are deducted from the sales i.e. £54000

deducted from £10000 which generated gross profit and further deducting distribution expense of

£9500 net profits is £36500.

Renishaw company need to use absorption costing because it shows increase in revenue

and decrease in sales cost. It is suitable for companies who have regular demand of the product.

It shows accurate profit which encourages company to increase its market share and increase

sales by making strategies. Renishaw company need not to separate variable and fixed cost.

LO 3

P4 Types of planning tools for budgetary control

Budget is an estimation of income and expenses which will be incurred in future. Budget

is based on the plans and objective of the company. Management of company estimates the

expense and revenue of the coming year by comparing it with previous year. Renishaw company

also need to make budget to complete its projects within the given budget. Budget benefits

company to work effectively within the given budget. There are different kinds of budgets i.e. for

long term and short term (Gibassier and Schaltegger, 2015). If objective and goals of a company

are for long period than company prepared long term budgets and if goals are for short term

company prepares short term budget. Financial stability of a company plays an important role in

making the budget.

The purpose of budget is to coordinate and distribute the resources equally. It provides a

guideline within which company need to perform its action to achieve organisation goals and

objectives. It improves performance of company.

Budgetary control is a process of where budgets are prepared for future date than the gap

between actual and expected results is find out. Comparing the results and identification of

difference, benefits company in taking appropriate actions (Taylor and Scapens, 2016). There are

many budgetary control techniques such as financial, operation and non-monetory budget. It

helps management to plan and implement policies by using various planning tools which are as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero-based budgeting: It is an approach for planning and preparing budget from the

scrap. It starts with zero, but traditional budget rely on previous budget. It is used to

implement strategic goals in specific functional areas of Renishaw company. All the

expenses need to be justifies at first before including it in actual budget. The main

purpose of using zero-based budgeting is to reduce the unnecessary cost. It helps

company to utilize the resources effectively and efficiently. For making this type of

budget employees need to be involved in figuring out the expenses.

Advantages Disadvantages

It increases efficiency of Renishaw

company in allocating resources. It

does not rely on previous budget.

This planning tools benefits all the

department of the company in re-

looking their cash flows constantly and

get a fair idea of expenses(Kamal,

2015).

It reacts to the changes which arise in

business environment.

It uses high manpower because budget

is prepared manually, it involves

employees of every department in

making a budget.

It is a time consuming process because

Renishaw company need to prepare

budget annual.

Management of Renishaw company

feel demotivated because budget is

prepared manually.

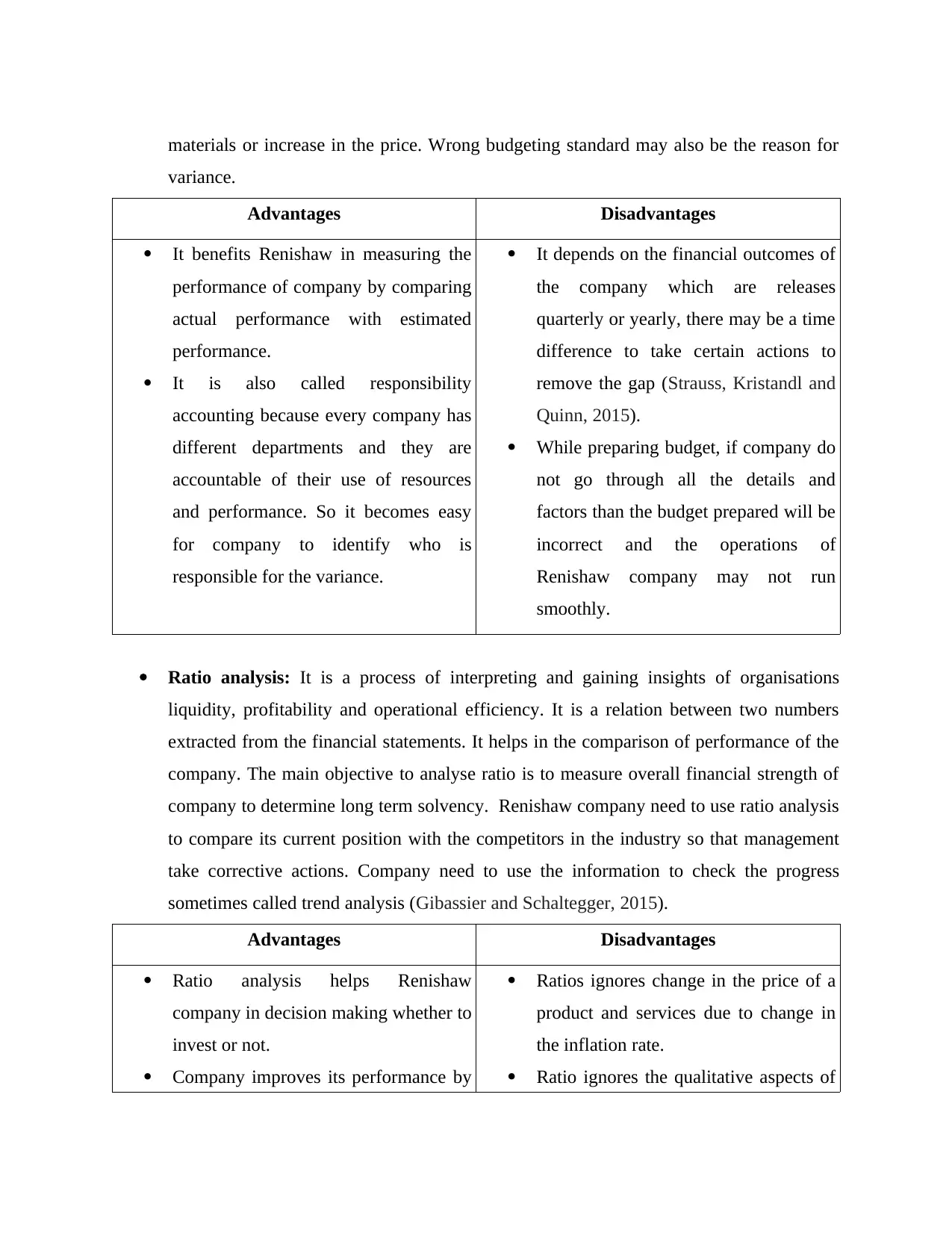

Variance analysis: It provides difference between the actual and planned performance.

This analysis helps Renishaw company to maintain control over business. It is a

quantitative investigation in finding out the gap between actual performance and

estimated performance. By using variance analysis company find out the trend in change

in the performance and use that information in making financial budget. There are many

types of variance such as purchase price, labour rate, fixed overhead, selling price and

material yield variance (Alawattage, Wickramasinghe and Uddin, 2017). The objective of

using variance analysis is to take control of cost and reduce it. Reason behind the

difference can be change in the market conditions i.e. decrease in the supply of raw

scrap. It starts with zero, but traditional budget rely on previous budget. It is used to

implement strategic goals in specific functional areas of Renishaw company. All the

expenses need to be justifies at first before including it in actual budget. The main

purpose of using zero-based budgeting is to reduce the unnecessary cost. It helps

company to utilize the resources effectively and efficiently. For making this type of

budget employees need to be involved in figuring out the expenses.

Advantages Disadvantages

It increases efficiency of Renishaw

company in allocating resources. It

does not rely on previous budget.

This planning tools benefits all the

department of the company in re-

looking their cash flows constantly and

get a fair idea of expenses(Kamal,

2015).

It reacts to the changes which arise in

business environment.

It uses high manpower because budget

is prepared manually, it involves

employees of every department in

making a budget.

It is a time consuming process because

Renishaw company need to prepare

budget annual.

Management of Renishaw company

feel demotivated because budget is

prepared manually.

Variance analysis: It provides difference between the actual and planned performance.

This analysis helps Renishaw company to maintain control over business. It is a

quantitative investigation in finding out the gap between actual performance and

estimated performance. By using variance analysis company find out the trend in change

in the performance and use that information in making financial budget. There are many

types of variance such as purchase price, labour rate, fixed overhead, selling price and

material yield variance (Alawattage, Wickramasinghe and Uddin, 2017). The objective of

using variance analysis is to take control of cost and reduce it. Reason behind the

difference can be change in the market conditions i.e. decrease in the supply of raw

materials or increase in the price. Wrong budgeting standard may also be the reason for

variance.

Advantages Disadvantages

It benefits Renishaw in measuring the

performance of company by comparing

actual performance with estimated

performance.

It is also called responsibility

accounting because every company has

different departments and they are

accountable of their use of resources

and performance. So it becomes easy

for company to identify who is

responsible for the variance.

It depends on the financial outcomes of

the company which are releases

quarterly or yearly, there may be a time

difference to take certain actions to

remove the gap (Strauss, Kristandl and

Quinn, 2015).

While preparing budget, if company do

not go through all the details and

factors than the budget prepared will be

incorrect and the operations of

Renishaw company may not run

smoothly.

Ratio analysis: It is a process of interpreting and gaining insights of organisations

liquidity, profitability and operational efficiency. It is a relation between two numbers

extracted from the financial statements. It helps in the comparison of performance of the

company. The main objective to analyse ratio is to measure overall financial strength of

company to determine long term solvency. Renishaw company need to use ratio analysis

to compare its current position with the competitors in the industry so that management

take corrective actions. Company need to use the information to check the progress

sometimes called trend analysis (Gibassier and Schaltegger, 2015).

Advantages Disadvantages

Ratio analysis helps Renishaw

company in decision making whether to

invest or not.

Company improves its performance by

Ratios ignores change in the price of a

product and services due to change in

the inflation rate.

Ratio ignores the qualitative aspects of

variance.

Advantages Disadvantages

It benefits Renishaw in measuring the

performance of company by comparing

actual performance with estimated

performance.

It is also called responsibility

accounting because every company has

different departments and they are

accountable of their use of resources

and performance. So it becomes easy

for company to identify who is

responsible for the variance.

It depends on the financial outcomes of

the company which are releases

quarterly or yearly, there may be a time

difference to take certain actions to

remove the gap (Strauss, Kristandl and

Quinn, 2015).

While preparing budget, if company do

not go through all the details and

factors than the budget prepared will be

incorrect and the operations of

Renishaw company may not run

smoothly.

Ratio analysis: It is a process of interpreting and gaining insights of organisations

liquidity, profitability and operational efficiency. It is a relation between two numbers

extracted from the financial statements. It helps in the comparison of performance of the

company. The main objective to analyse ratio is to measure overall financial strength of

company to determine long term solvency. Renishaw company need to use ratio analysis

to compare its current position with the competitors in the industry so that management

take corrective actions. Company need to use the information to check the progress

sometimes called trend analysis (Gibassier and Schaltegger, 2015).

Advantages Disadvantages

Ratio analysis helps Renishaw

company in decision making whether to

invest or not.

Company improves its performance by

Ratios ignores change in the price of a

product and services due to change in

the inflation rate.

Ratio ignores the qualitative aspects of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.