Comprehensive Project Report: Accounting System and Processes

VerifiedAdded on 2023/06/04

|17

|2646

|448

Report

AI Summary

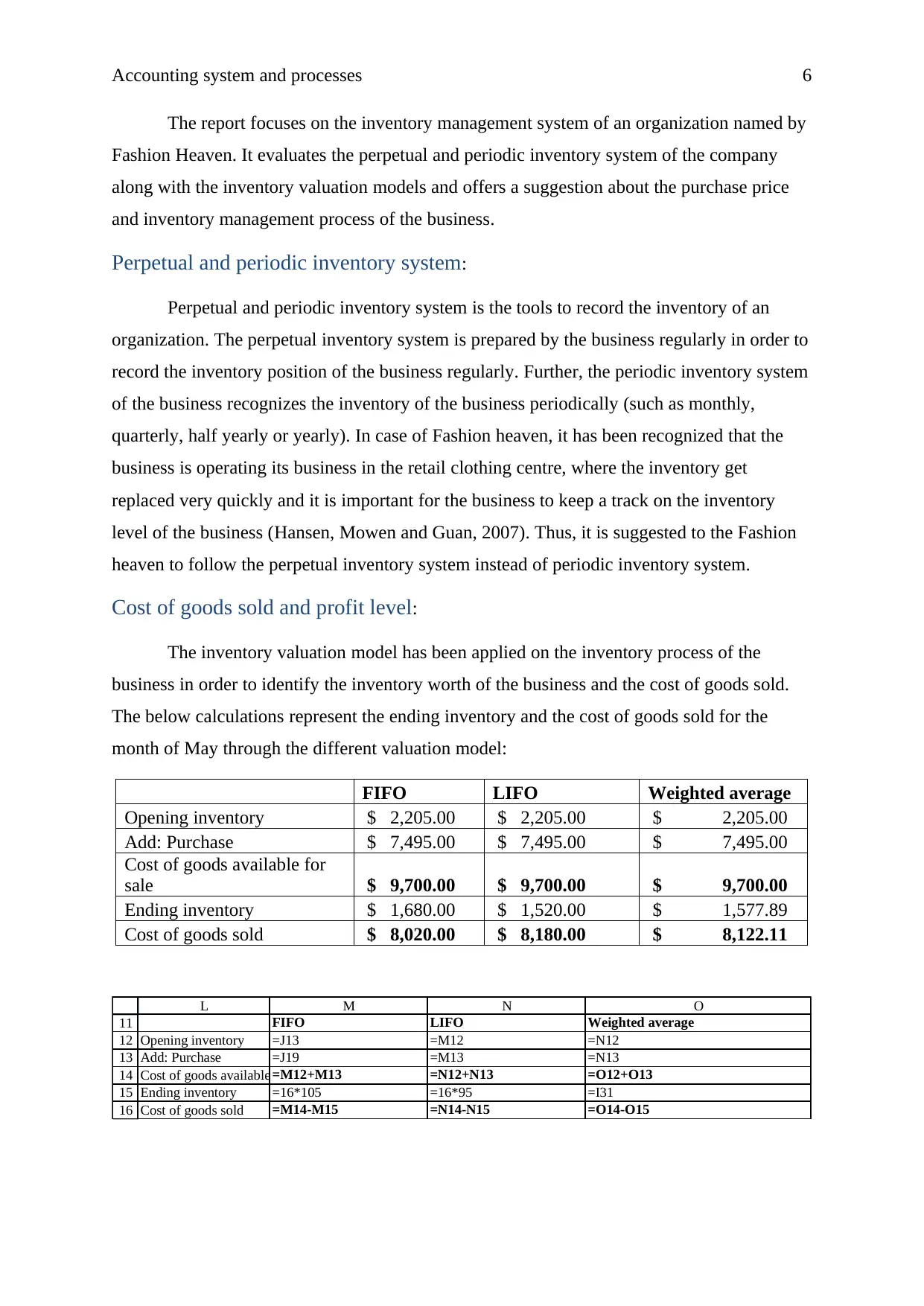

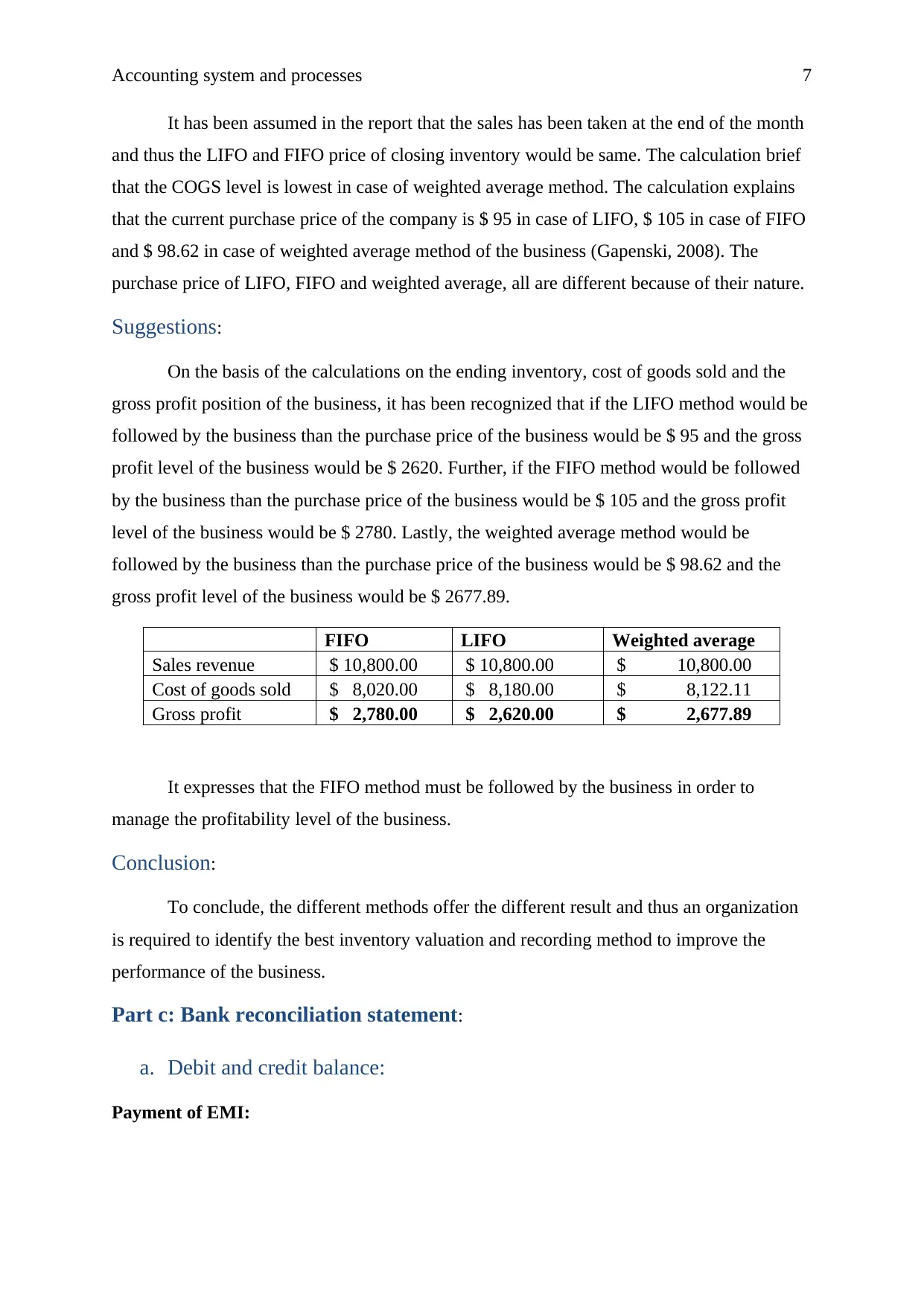

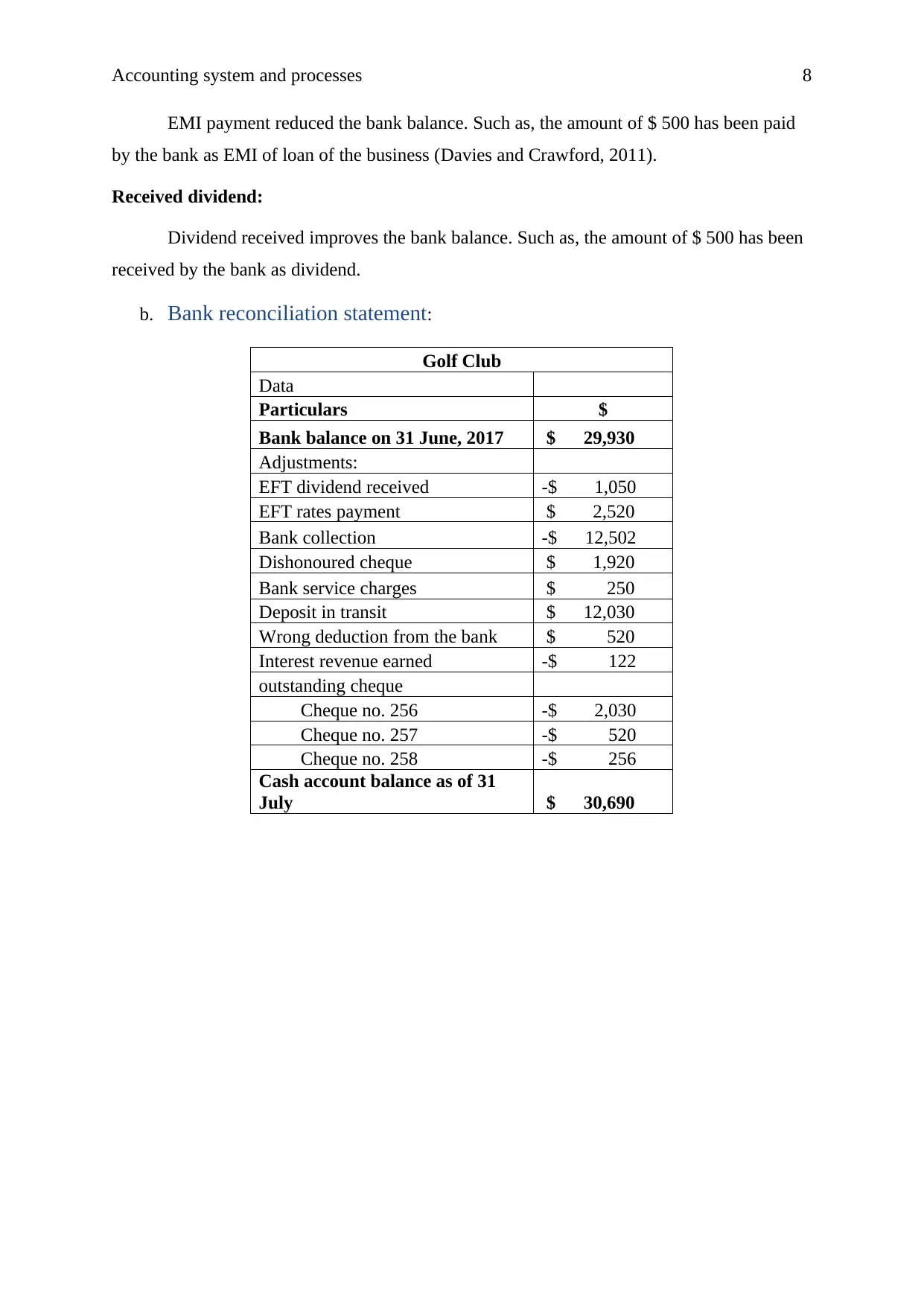

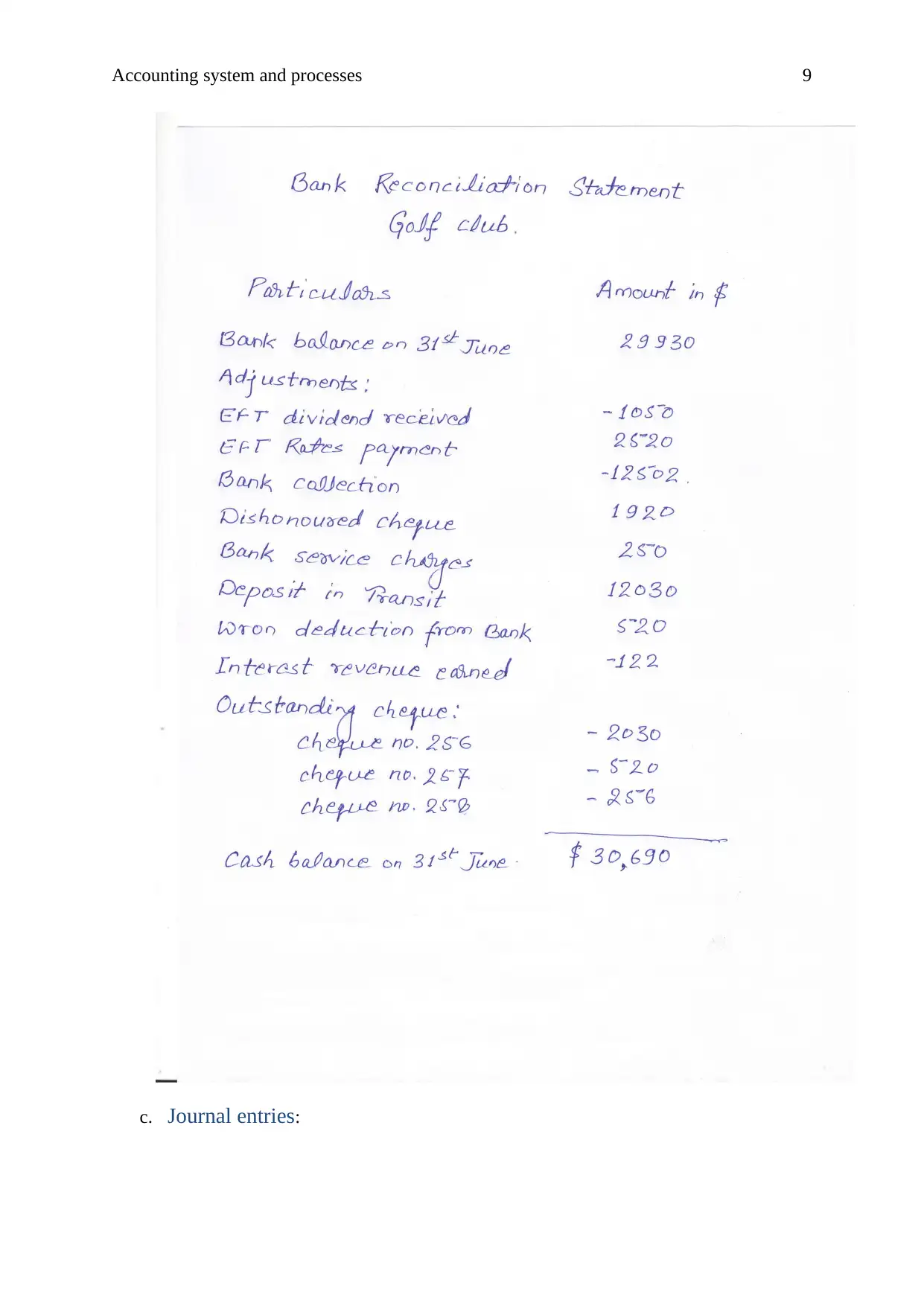

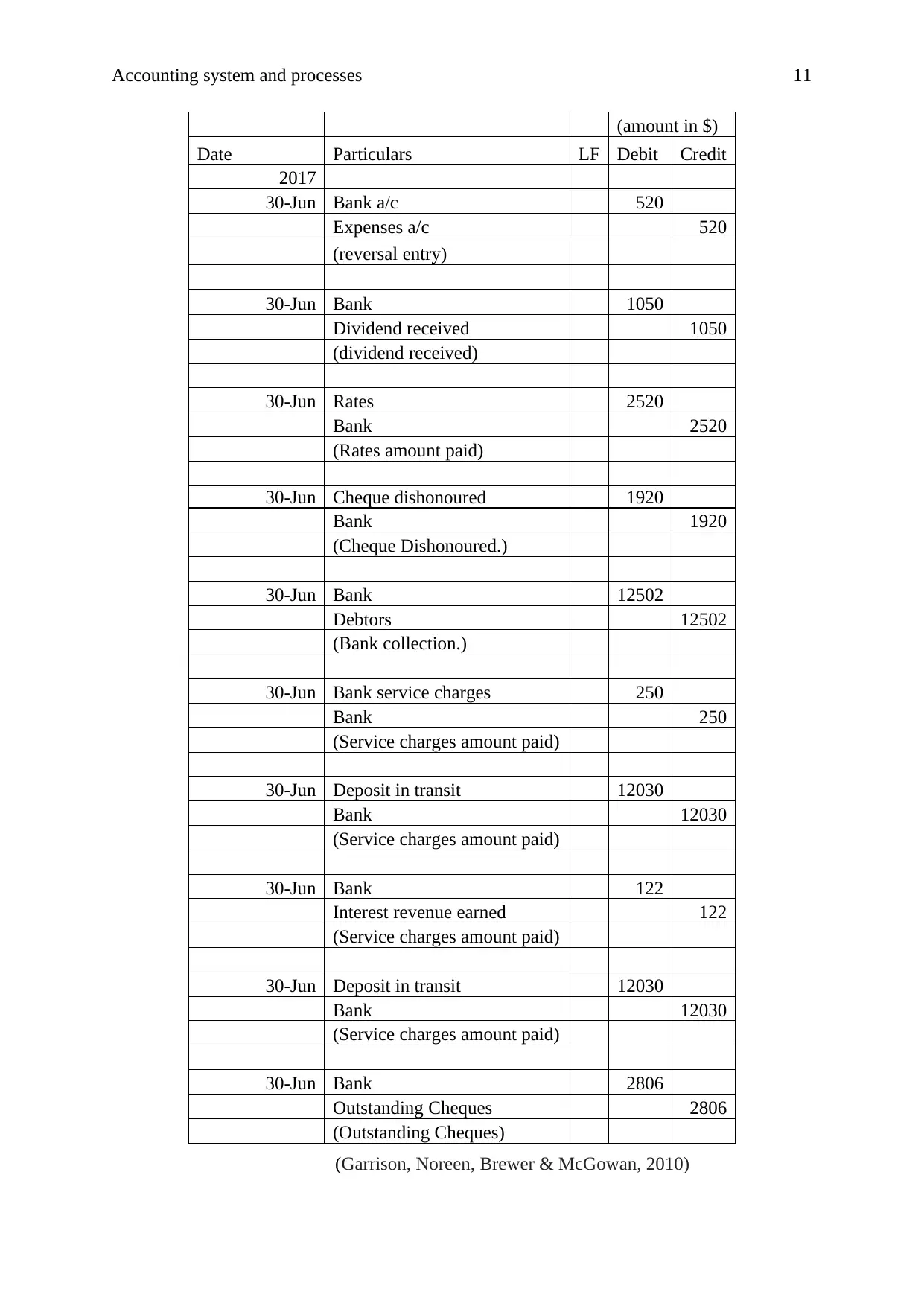

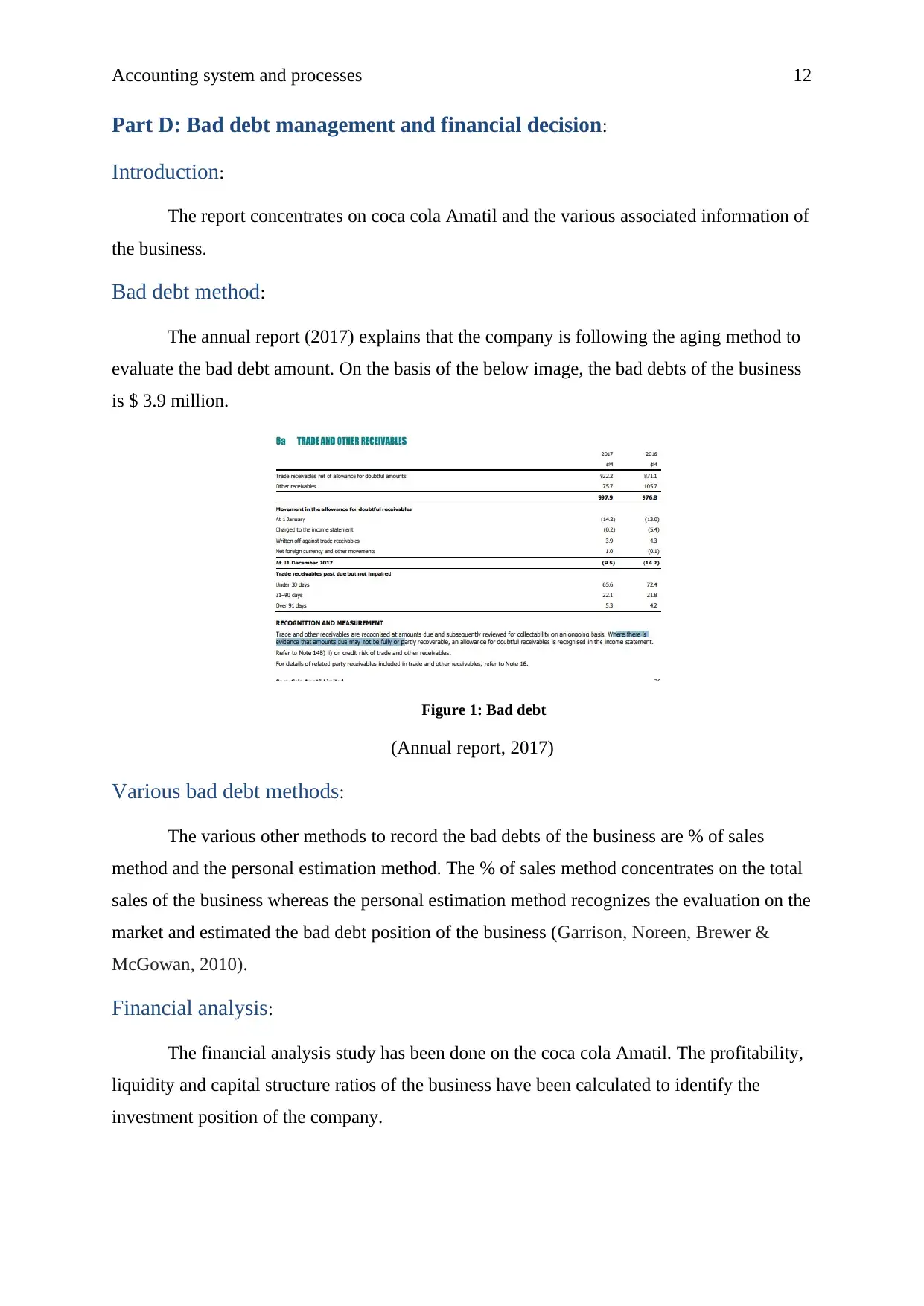

This project report provides a detailed analysis of accounting systems and processes, covering spreadsheet applications, inventory management, bank reconciliation, and bad debt management. The report begins with an examination of spreadsheet usage in accounting, including the advantages and disadvantages, separation of data reports, and practical examples using IF functions and cell referencing. It then transitions to inventory management, comparing perpetual and periodic systems, evaluating cost of goods sold using FIFO, LIFO, and weighted average methods, and offering suggestions for Fashion Heaven's inventory practices. The report further addresses bank reconciliation, explaining debit and credit balances, constructing a bank reconciliation statement, and providing relevant journal entries. Lastly, it delves into bad debt management, discussing various methods and conducting a financial analysis of Coca-Cola Amatil, including profitability, liquidity, capital structure, and sustainability, ultimately recommending long-term investment. Desklib offers a wealth of similar solved assignments and study resources for students.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.