A Report on Management Accounting Systems and Reporting for Creams Ltd

VerifiedAdded on 2023/01/12

|19

|5865

|79

Report

AI Summary

This report provides an in-depth analysis of management accounting (MA) systems and reporting methods, using Creams Ltd, an ice cream and waffle business, as a case study. It explores various MA systems like cost accounting, inventory management, job costing, and price optimization, detailing their benefits and applications within an organization. The report also discusses different MA reporting methods, including job costing reports, inventory reports, operating budgets, accounts receivable aging reports, and performance reports, highlighting their importance in organizational performance evaluation and decision-making. Furthermore, it addresses the integration of management accounting systems and reporting in achieving business targets and objectives, emphasizing the importance of timely information availability and systematic management of business operations. The report concludes by touching upon how companies are adapting their management accounting systems to meet evolving business needs.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

LO1............................................................................................................................................3

P1 Management accounting system and its essential requirements.......................................3

P2 Different methods of MA reporting..................................................................................6

LO2............................................................................................................................................8

P3 Management accounting techniques.................................................................................8

P4- Disadvantages and advantages of varied types of planning tools.................................12

P5- How companies are adapting management accounting systems...................................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION......................................................................................................................3

LO1............................................................................................................................................3

P1 Management accounting system and its essential requirements.......................................3

P2 Different methods of MA reporting..................................................................................6

LO2............................................................................................................................................8

P3 Management accounting techniques.................................................................................8

P4- Disadvantages and advantages of varied types of planning tools.................................12

P5- How companies are adapting management accounting systems...................................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

INTRODUCTION

Management accounting (MA) is the process of providing relevant information and

resources to the management team for decision making. This information is only used by

internal management team which makes it different from the financial accounting. In this,

information is shared by the finance department to the management team. The core aim is to

use this data to order to take accurate decision with respect to planning and controlling the

business activities and strategies. There is no fixed structure or format for doing it. It is done

as per the requirement and there is no statutory requirement to do it. In this report, Creams

Ltd is taken as an organization which sells ice creams, doughnuts, waffles etc. This report

provides a deep insight into the various types of management accounting systems and its

essentials along with their pros and cons. It throws light on different management accounting

reporting with the wide range of MA techniques used by the organization. The advantages

and disadvantages of various planning tools that can be used for establishing budgetary

control. Also, a comparison has been drawn by analysing the organizations using different

management accounting systems.

LO1

P1 Management accounting system and its essential requirements

According to the Institute od Management Accountants, London, MA refers to the

application of various professional skills in the preparation of relevant information which

helps in providing assistance to the management in effectively formulating policies and

planning strategies and implementing control on the same (Management Accounting –

Meaning, Advantages & Functions. 2019).

There are different types of management accounting system which are implemented

by the organizations as per the business requirements. A detailed description of different

management accounting system is given below.

Cost accounting system

The cost accounting system is used by the organizations for estimating cost of the

products produced by it. It is also used for inventory valuation, cost control and profitability

analysis as well.This system works by tracking the material when it goes through different

stages of production process (Datar and Rajan, 2018). For example, when the raw material

moves form one stage to another, the cost accounting system tracks the progress and updates

the same on the computerized system. This system is very helpful for the production manager

Management accounting (MA) is the process of providing relevant information and

resources to the management team for decision making. This information is only used by

internal management team which makes it different from the financial accounting. In this,

information is shared by the finance department to the management team. The core aim is to

use this data to order to take accurate decision with respect to planning and controlling the

business activities and strategies. There is no fixed structure or format for doing it. It is done

as per the requirement and there is no statutory requirement to do it. In this report, Creams

Ltd is taken as an organization which sells ice creams, doughnuts, waffles etc. This report

provides a deep insight into the various types of management accounting systems and its

essentials along with their pros and cons. It throws light on different management accounting

reporting with the wide range of MA techniques used by the organization. The advantages

and disadvantages of various planning tools that can be used for establishing budgetary

control. Also, a comparison has been drawn by analysing the organizations using different

management accounting systems.

LO1

P1 Management accounting system and its essential requirements

According to the Institute od Management Accountants, London, MA refers to the

application of various professional skills in the preparation of relevant information which

helps in providing assistance to the management in effectively formulating policies and

planning strategies and implementing control on the same (Management Accounting –

Meaning, Advantages & Functions. 2019).

There are different types of management accounting system which are implemented

by the organizations as per the business requirements. A detailed description of different

management accounting system is given below.

Cost accounting system

The cost accounting system is used by the organizations for estimating cost of the

products produced by it. It is also used for inventory valuation, cost control and profitability

analysis as well.This system works by tracking the material when it goes through different

stages of production process (Datar and Rajan, 2018). For example, when the raw material

moves form one stage to another, the cost accounting system tracks the progress and updates

the same on the computerized system. This system is very helpful for the production manager

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as well as cost accountants as it helps them in knowing how much inventory is under each

production stages at a point of time. The essential requirement of cost accounting system is to

properly record the cost of each transaction and it helps in establishing control over cost and

expenditure of the organization.

Benefits:

It helps in identifying the profitable and non -profitable activities of the business.

The data provided about the cost associated with different processes assists in future

planning.

This system also helps in determining the profit or loss of the product periodically.

Cost accounting system helps in exercising control over the material and other

business supplies.

Application

This system is used in the manufacturing concerns for properly recording all the costs

related to the production.

Inventory management system

It is the system deployed by the organization with the objective to oversee the monitoring

and maintenance of the inventory of the products irrespective of whether those are raw

materials, finished goods or work in progress.This system provides a centralized database

with ability to generate relevant reports, effective management of inventory and also in future

forecasting of the same (Taschner and Charifzadeh, 2016). For big manufacturing companies,

having complex supply chain and processes, this system will be very helpful in managing the

inventory gluts and also times of shortages. This system is very essential for mostly all types

of businesses irrespective of size. This system is very essential as it helps in determining the

right time to place the order and storing and holding cost related to it and it also helps in

identifying what amount to be purchased and at what price which sometimes becomesthe

complex process.

Benefits:

It helps in avoiding the situation of out of stock or excess stock.

Better business negotiations with the suppliers and vendors benefiting the

business.

production stages at a point of time. The essential requirement of cost accounting system is to

properly record the cost of each transaction and it helps in establishing control over cost and

expenditure of the organization.

Benefits:

It helps in identifying the profitable and non -profitable activities of the business.

The data provided about the cost associated with different processes assists in future

planning.

This system also helps in determining the profit or loss of the product periodically.

Cost accounting system helps in exercising control over the material and other

business supplies.

Application

This system is used in the manufacturing concerns for properly recording all the costs

related to the production.

Inventory management system

It is the system deployed by the organization with the objective to oversee the monitoring

and maintenance of the inventory of the products irrespective of whether those are raw

materials, finished goods or work in progress.This system provides a centralized database

with ability to generate relevant reports, effective management of inventory and also in future

forecasting of the same (Taschner and Charifzadeh, 2016). For big manufacturing companies,

having complex supply chain and processes, this system will be very helpful in managing the

inventory gluts and also times of shortages. This system is very essential for mostly all types

of businesses irrespective of size. This system is very essential as it helps in determining the

right time to place the order and storing and holding cost related to it and it also helps in

identifying what amount to be purchased and at what price which sometimes becomesthe

complex process.

Benefits:

It helps in avoiding the situation of out of stock or excess stock.

Better business negotiations with the suppliers and vendors benefiting the

business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It also helps the businesses in timely placing the order for the raw materials.

This system also helps in making forecast about the future trends.

Application

This system is used by Creams Ltd. for effectively managing the inventory of the

business such as waffles, cream, flavours, cone etc.

Job costing

This management accounting system is best suited for situations where goods are

produced as per the specification and order given by the customer for example, the ship

manufacturer will like to know the price of each ship produced (Butterfield, 2016). This

system involves the process of gathering all the relevant information related to cost with a

specific production job. It enables the organization in quoting the price of the product with

areasonable profit. It measures all the direct and indirect cost in connection to the particular

job. It enables the company in taking better and improved decisions with respect to cost. This

method is very essential for the businesses where different products are produced which are

sufficiently different from each other with a significant cost.

Benefits:

This system provides analysis of various cost which helps in determining the

operational efficiency of the business.

It records the cost more accurately which facilitates cost control by comparing

budgeted with the actual outcomes.

It provides the company a basis to estimate the cost of the similar job that may be

taken up in the future which helps in future planning process.

It also helps in identifying any spoilage or defects in the production process which

enables the manager to take effective steps.

Application

This method will help in Creams Ltd in determining the profits associated with

different jobs carried out by it.

Price optimization system

It is the mathematical program which uses various calculations to determine the price

of the product. It evaluates the change in demand of the product with respect to the change in

This system also helps in making forecast about the future trends.

Application

This system is used by Creams Ltd. for effectively managing the inventory of the

business such as waffles, cream, flavours, cone etc.

Job costing

This management accounting system is best suited for situations where goods are

produced as per the specification and order given by the customer for example, the ship

manufacturer will like to know the price of each ship produced (Butterfield, 2016). This

system involves the process of gathering all the relevant information related to cost with a

specific production job. It enables the organization in quoting the price of the product with

areasonable profit. It measures all the direct and indirect cost in connection to the particular

job. It enables the company in taking better and improved decisions with respect to cost. This

method is very essential for the businesses where different products are produced which are

sufficiently different from each other with a significant cost.

Benefits:

This system provides analysis of various cost which helps in determining the

operational efficiency of the business.

It records the cost more accurately which facilitates cost control by comparing

budgeted with the actual outcomes.

It provides the company a basis to estimate the cost of the similar job that may be

taken up in the future which helps in future planning process.

It also helps in identifying any spoilage or defects in the production process which

enables the manager to take effective steps.

Application

This method will help in Creams Ltd in determining the profits associated with

different jobs carried out by it.

Price optimization system

It is the mathematical program which uses various calculations to determine the price

of the product. It evaluates the change in demand of the product with respect to the change in

the price level. This method also takes into consideration the willingness of the customers to

pay for the particular product (Wang and Wang, 2017). This method determines the price of

the product that helps in achieving the desired objectives along with maximising the profits of

the business. This system is essential for determining the price of the product based on it

demand.

Benefits:

This system helps in determining the change in the demand with respect to change in

the price level.

This technique helps in improving the profitability of the business.

It helps the business in understanding the market pattern which helps in better

decision making.

It optimizes the entire process which helps in minimising the manual task and reduces

errors.

Application

The price optimization process will help Creams Ltd in taking better business

decisions where it can analyse the pricing of its products.

Difference between Financial and management Accounting

Basis of comparison Management accounting Financial accounting

Aim The management accounting

information is mainly meant

for the internal management

for taking business decisions.

The aim is to provide relevant

information to the outside users

which includes creditors,

investors, financial institutions

etc.

Compliance Management accounting is the

internal report, so they do not

have to compile with any of the

standard.

Financial report at the same

time must compile with many

different standards in real

before showing the result.

Independent audit There is no particular review

prerequisite yet the

management can step up to

take initiative so as to lead an

independent review.

The independent audit is

mandatory for financial

accounting reports in all

countries.

P2 Different methods of MA reporting

MA reports helps the management in proper evaluation of company’s performance.

There are different types of management accounting report which are prepared as per the

requirement of the requirement. Some of them are stated below.

pay for the particular product (Wang and Wang, 2017). This method determines the price of

the product that helps in achieving the desired objectives along with maximising the profits of

the business. This system is essential for determining the price of the product based on it

demand.

Benefits:

This system helps in determining the change in the demand with respect to change in

the price level.

This technique helps in improving the profitability of the business.

It helps the business in understanding the market pattern which helps in better

decision making.

It optimizes the entire process which helps in minimising the manual task and reduces

errors.

Application

The price optimization process will help Creams Ltd in taking better business

decisions where it can analyse the pricing of its products.

Difference between Financial and management Accounting

Basis of comparison Management accounting Financial accounting

Aim The management accounting

information is mainly meant

for the internal management

for taking business decisions.

The aim is to provide relevant

information to the outside users

which includes creditors,

investors, financial institutions

etc.

Compliance Management accounting is the

internal report, so they do not

have to compile with any of the

standard.

Financial report at the same

time must compile with many

different standards in real

before showing the result.

Independent audit There is no particular review

prerequisite yet the

management can step up to

take initiative so as to lead an

independent review.

The independent audit is

mandatory for financial

accounting reports in all

countries.

P2 Different methods of MA reporting

MA reports helps the management in proper evaluation of company’s performance.

There are different types of management accounting report which are prepared as per the

requirement of the requirement. Some of them are stated below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costing

It is the tool used by the management in effectively evaluating the project against the

set standards. This report provides an overview of the total cost incurred in a project in

response to the expected revenue yielded. This report helps the management in evaluating the

profitability of the different jobs and optimizing the business operation by focusing on those

jobs which are more profitable instead of wasting time and efforts on those job which are less

profitable.It focusses on tracking the cost associated with the ongoing project. This report

provides an aspect to the management in analysing the expenses in a timely manner so that

actions can be taken before its too late, that is, cost exceeds profits.

Inventory report

This report provides the summary of existing inventory of the business. It provides

complete details about the how much stock is there, which product is selling faster, category

wise performance of the product. It involves complete record keeping of each and every

transaction separately and monitors every movement of inventory. Based on the information

provided in the report, helps the business organizations in making projections about the future

requirements. It also helps in identifying the any wastage of the inventory and highlights the

areas of improvement. Consequently, it leads to optimum utilization of resources.

Operating budget

It is the detailed statement which shows all the estimated operational expenses to be

incurred and revenue to be generated in a particular period. In this report, all the operating

expenses such as raw material, processing cost, administrative expenses are all considered.

This budget report helps in tracking the income and expenses of the company (Li, 2018). It

also helps in implementing control over expenses in order to achieve the desired sales target.

It helps the company in improving its efficiency by operating at the optimum level.This

report provides guidance to the employees for better and efficient planning which helps in

effective functioning of the business performance.This budget is prepared by taking previous

year as the base.

Account receivable aging report

It is the critical tool which is used for managing the cash flow of the business in case

credit is provided to the customers. This report provides the complete breakdown of the

customers remaining balance (MANAGERIAL ACCOUNTING REPORTS. 2020). This report

It is the tool used by the management in effectively evaluating the project against the

set standards. This report provides an overview of the total cost incurred in a project in

response to the expected revenue yielded. This report helps the management in evaluating the

profitability of the different jobs and optimizing the business operation by focusing on those

jobs which are more profitable instead of wasting time and efforts on those job which are less

profitable.It focusses on tracking the cost associated with the ongoing project. This report

provides an aspect to the management in analysing the expenses in a timely manner so that

actions can be taken before its too late, that is, cost exceeds profits.

Inventory report

This report provides the summary of existing inventory of the business. It provides

complete details about the how much stock is there, which product is selling faster, category

wise performance of the product. It involves complete record keeping of each and every

transaction separately and monitors every movement of inventory. Based on the information

provided in the report, helps the business organizations in making projections about the future

requirements. It also helps in identifying the any wastage of the inventory and highlights the

areas of improvement. Consequently, it leads to optimum utilization of resources.

Operating budget

It is the detailed statement which shows all the estimated operational expenses to be

incurred and revenue to be generated in a particular period. In this report, all the operating

expenses such as raw material, processing cost, administrative expenses are all considered.

This budget report helps in tracking the income and expenses of the company (Li, 2018). It

also helps in implementing control over expenses in order to achieve the desired sales target.

It helps the company in improving its efficiency by operating at the optimum level.This

report provides guidance to the employees for better and efficient planning which helps in

effective functioning of the business performance.This budget is prepared by taking previous

year as the base.

Account receivable aging report

It is the critical tool which is used for managing the cash flow of the business in case

credit is provided to the customers. This report provides the complete breakdown of the

customers remaining balance (MANAGERIAL ACCOUNTING REPORTS. 2020). This report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is very important as it helps the management in identifying the any problem in the company’s

collection process. Apart from this, it also allows manager in identifying the defaulters. Based

on this report, provision is created for defaulters and if any change in the credit policy is

required, the same is also done.

Performance report

This report is prepared for reviewing the performance of the business. It takes into

consideration whole organization including each and every employee separately. In big

organizations, department wise reports are prepared. These reports are very useful for the

organization in order to take strategic business decisions with respect to the future of the

organization (Collis and Hussey, 2017). Based on this report, employees are rewarded for

their commitmenttowards work and the organization and the under performers are either laid

off or dealt in other way. This report provides deep insight about the working condition of the

company based on its performance with respect to the certain criteria. It indicates any flaw in

the system which is restricting it for achieving optimum performance level. Thus, the role of

this report is very essential for any organization in keeping accurate measure of the strategy

for achieving the goals.

Integration of management accounting system and reporting in the organizational

process

The integration of management accounting and reporting will help in effectively

achieving the business targets and objectives. It will assist the organization in managing its

business operation and performance in a systematic manner with the timely availability of

information. It will help in analysing the areas of improvement of the business which will

result into increase in the performance and productivity of the business. This integration will

also help in proper decision making and gives direction to effective planning.

LO2

P3 Management accounting techniques

The management accounting is a system that involves techniques of cost accounting

that is used for recording the transactions and preparing the profit or loss statements for the

company. The various cost associated with management accounting techniques are stated

below.

collection process. Apart from this, it also allows manager in identifying the defaulters. Based

on this report, provision is created for defaulters and if any change in the credit policy is

required, the same is also done.

Performance report

This report is prepared for reviewing the performance of the business. It takes into

consideration whole organization including each and every employee separately. In big

organizations, department wise reports are prepared. These reports are very useful for the

organization in order to take strategic business decisions with respect to the future of the

organization (Collis and Hussey, 2017). Based on this report, employees are rewarded for

their commitmenttowards work and the organization and the under performers are either laid

off or dealt in other way. This report provides deep insight about the working condition of the

company based on its performance with respect to the certain criteria. It indicates any flaw in

the system which is restricting it for achieving optimum performance level. Thus, the role of

this report is very essential for any organization in keeping accurate measure of the strategy

for achieving the goals.

Integration of management accounting system and reporting in the organizational

process

The integration of management accounting and reporting will help in effectively

achieving the business targets and objectives. It will assist the organization in managing its

business operation and performance in a systematic manner with the timely availability of

information. It will help in analysing the areas of improvement of the business which will

result into increase in the performance and productivity of the business. This integration will

also help in proper decision making and gives direction to effective planning.

LO2

P3 Management accounting techniques

The management accounting is a system that involves techniques of cost accounting

that is used for recording the transactions and preparing the profit or loss statements for the

company. The various cost associated with management accounting techniques are stated

below.

Fixed cost:It is the cost that remains unchanged at the certain range of output level.

These are those expenses which are required to be paid by the organization. Fixed cost can

create economies of scale which decreases the per unit cost of the product. The organizations

with higher fixed cost are different from those organizations having higher variable cost. This

difference has a huge impact on the financial structure of the business along with pricing and

profits (Manyaeva, Piskunov and Fomin, 2016). In such organizations, the break-even point

is higher and marginal profit is also higher. Even at the zero level of output, the fixed will

remain the same and it cannot be avoided.

Variable cost:These costs are those which varies with the change in the level of

output or sales.The cost increases with the increase in the volume and decreases with the

decrease in volume. It includes direct material and labour, direct expenses, transaction fees,

utility cost etc. At the zero level of production, the variable cost will also be zero.

Real cost: It is the overall actual expenses that is involved in creating the goods and

services with the purpose of sale to the end consumers.For businesses, the real cost of

production of the product mainly includes cost of all tangible resources like material and

labour which is used in production process. The real cost considers opportunity cost and

inflation as well.

Prime cost:It refers to the expenses that are directly related to the production process

such as material, labour and other direct expenses. The combination of all this makes prime

cost.It does not take into consideration any indirect expenses (LIMAREV and et.al, 2019). It

is very important for businesses to calculate prime cost for each product in order to ensure

that they are generating profits.

Total cost: It is sum total of all cost, that is, fixed cost, variable cost and semi variable

cost (Total cost. 2018). For calculating its, all these costs are required to be determined

separately because a product is combination of all these costs.

Average cost: It is the average per unit cost of the product is determined by dividing

total cost of production by the total units produced. In long term, it normalizes the cost per

unit and smooths out the fluctuations which is caused by change in demand seasonally.

Marginal cost:It refers to the change in the cost of production because of producing

an additional unit of the product.It is calculated by dividing change in production by change

in quantity. The purpose of calculating it is to determine the point at which the business can

These are those expenses which are required to be paid by the organization. Fixed cost can

create economies of scale which decreases the per unit cost of the product. The organizations

with higher fixed cost are different from those organizations having higher variable cost. This

difference has a huge impact on the financial structure of the business along with pricing and

profits (Manyaeva, Piskunov and Fomin, 2016). In such organizations, the break-even point

is higher and marginal profit is also higher. Even at the zero level of output, the fixed will

remain the same and it cannot be avoided.

Variable cost:These costs are those which varies with the change in the level of

output or sales.The cost increases with the increase in the volume and decreases with the

decrease in volume. It includes direct material and labour, direct expenses, transaction fees,

utility cost etc. At the zero level of production, the variable cost will also be zero.

Real cost: It is the overall actual expenses that is involved in creating the goods and

services with the purpose of sale to the end consumers.For businesses, the real cost of

production of the product mainly includes cost of all tangible resources like material and

labour which is used in production process. The real cost considers opportunity cost and

inflation as well.

Prime cost:It refers to the expenses that are directly related to the production process

such as material, labour and other direct expenses. The combination of all this makes prime

cost.It does not take into consideration any indirect expenses (LIMAREV and et.al, 2019). It

is very important for businesses to calculate prime cost for each product in order to ensure

that they are generating profits.

Total cost: It is sum total of all cost, that is, fixed cost, variable cost and semi variable

cost (Total cost. 2018). For calculating its, all these costs are required to be determined

separately because a product is combination of all these costs.

Average cost: It is the average per unit cost of the product is determined by dividing

total cost of production by the total units produced. In long term, it normalizes the cost per

unit and smooths out the fluctuations which is caused by change in demand seasonally.

Marginal cost:It refers to the change in the cost of production because of producing

an additional unit of the product.It is calculated by dividing change in production by change

in quantity. The purpose of calculating it is to determine the point at which the business can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

achieve economies of scale (TUOVILA, 2019). If the marginal cost is below than per unit

price, it means that the organization has the potential to gain higher profits.

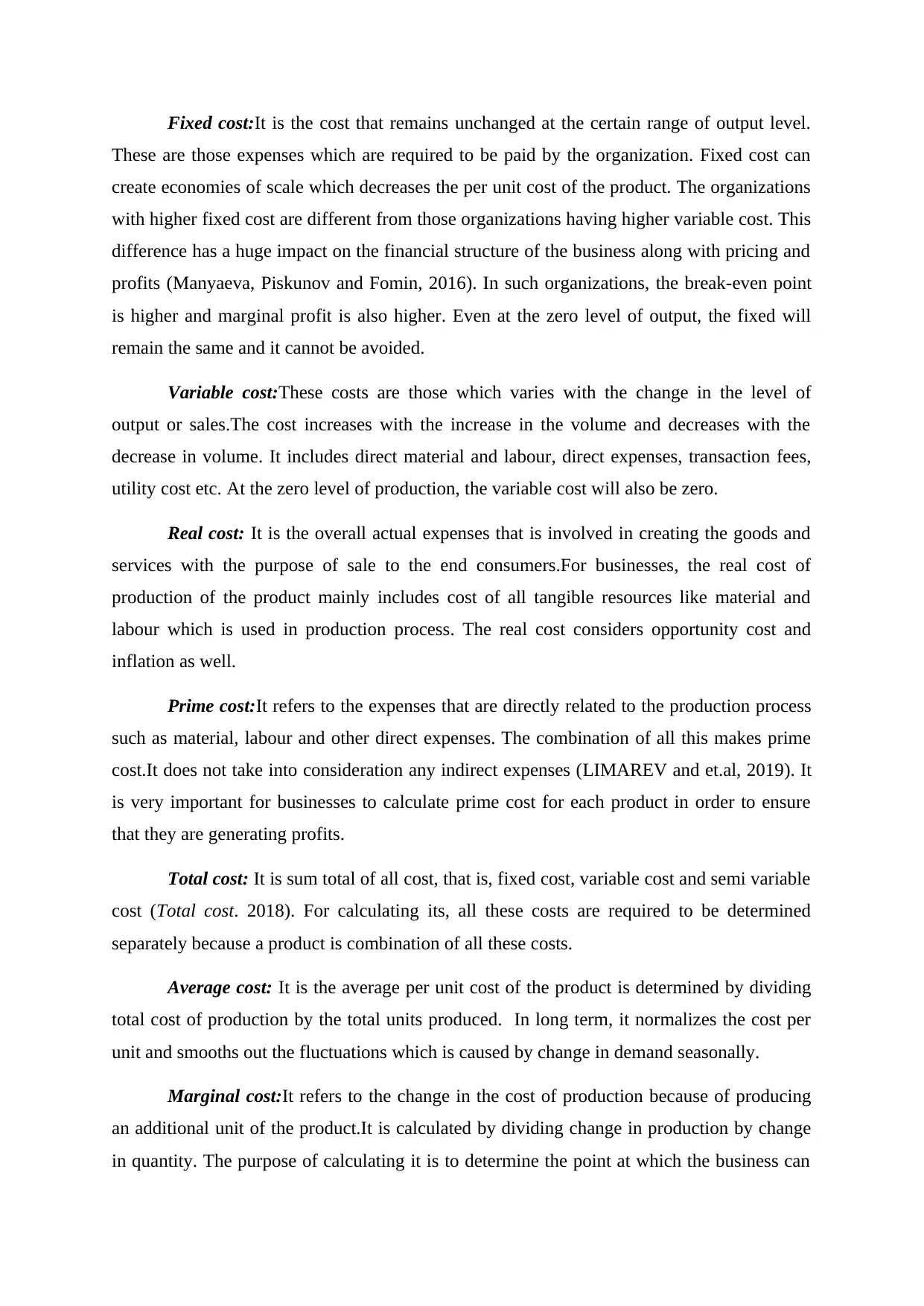

Income statement as per Marginal Costing

Particulars Januar

y

Februar

y

Sales Revenue (10000*25) 250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production Overheads (10000*2) 20000 (10000*2) 20000

100000 100000

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5000/10000)*100000 50000

100000 50000

Contribution 150000 75000

Fixed production overheads 40000 40000

Fixed selling & admin Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000 -25000

Income statement as per Absorption Costing

Particulars January Februar

y

Sales Revenue (10000*25

)

250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production Overheads (10000*2) 20000 (10000*2) 20000

price, it means that the organization has the potential to gain higher profits.

Income statement as per Marginal Costing

Particulars Januar

y

Februar

y

Sales Revenue (10000*25) 250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production Overheads (10000*2) 20000 (10000*2) 20000

100000 100000

Add:

Opening Stock 0 0

Less:

Closing Stock 0 (5000/10000)*100000 50000

100000 50000

Contribution 150000 75000

Fixed production overheads 40000 40000

Fixed selling & admin Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000 -25000

Income statement as per Absorption Costing

Particulars January Februar

y

Sales Revenue (10000*25

)

250000 (5000*25) 125000

Marginal Cost of Sales

Direct Materials (10000*5) 50000 (10000*5) 50000

Direct Labour (10000*3) 30000 (10000*3) 30000

Variable Production Overheads (10000*2) 20000 (10000*2) 20000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed production overheads 40000 40000

140000 140000

Add:

Opening Stock 0 0

Less:

Closing Stock 0.00 (5000/10000)*140000 70000.00

140000.00 70000.00

Gross profit 110000.00 55000.00

Fixed selling & admin. Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000.00 -5000.00

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£10 - £9.5) * 2200 kg

1100 (Fav)

i) Material Usage Variance = Standard Usage - Actual

Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2200 kg) *£10

-2000 (Adv)

i) Labour Rate Variance = Standard Rate - Actual Rate

(Std Rate - Actual Rate) x Actual Hours Worked)

( £ 5 -£ 5.2) * 3400

-680 (Adv)

140000 140000

Add:

Opening Stock 0 0

Less:

Closing Stock 0.00 (5000/10000)*140000 70000.00

140000.00 70000.00

Gross profit 110000.00 55000.00

Fixed selling & admin. Overhead 30000 30000

Variable sell. Overhead (10000*3) 30000 (5000*6) 30000

Net Income 50000.00 -5000.00

CALCULATION OF VARIANCES:

i) Material Price Variance = Standard Price - Actual Price

= (Std Price - Actual Price) x Actual Qty)

(£10 - £9.5) * 2200 kg

1100 (Fav)

i) Material Usage Variance = Standard Usage - Actual

Usage

= (Std Qty - Actual Qty) x Std Price)

(2000 kg - 2200 kg) *£10

-2000 (Adv)

i) Labour Rate Variance = Standard Rate - Actual Rate

(Std Rate - Actual Rate) x Actual Hours Worked)

( £ 5 -£ 5.2) * 3400

-680 (Adv)

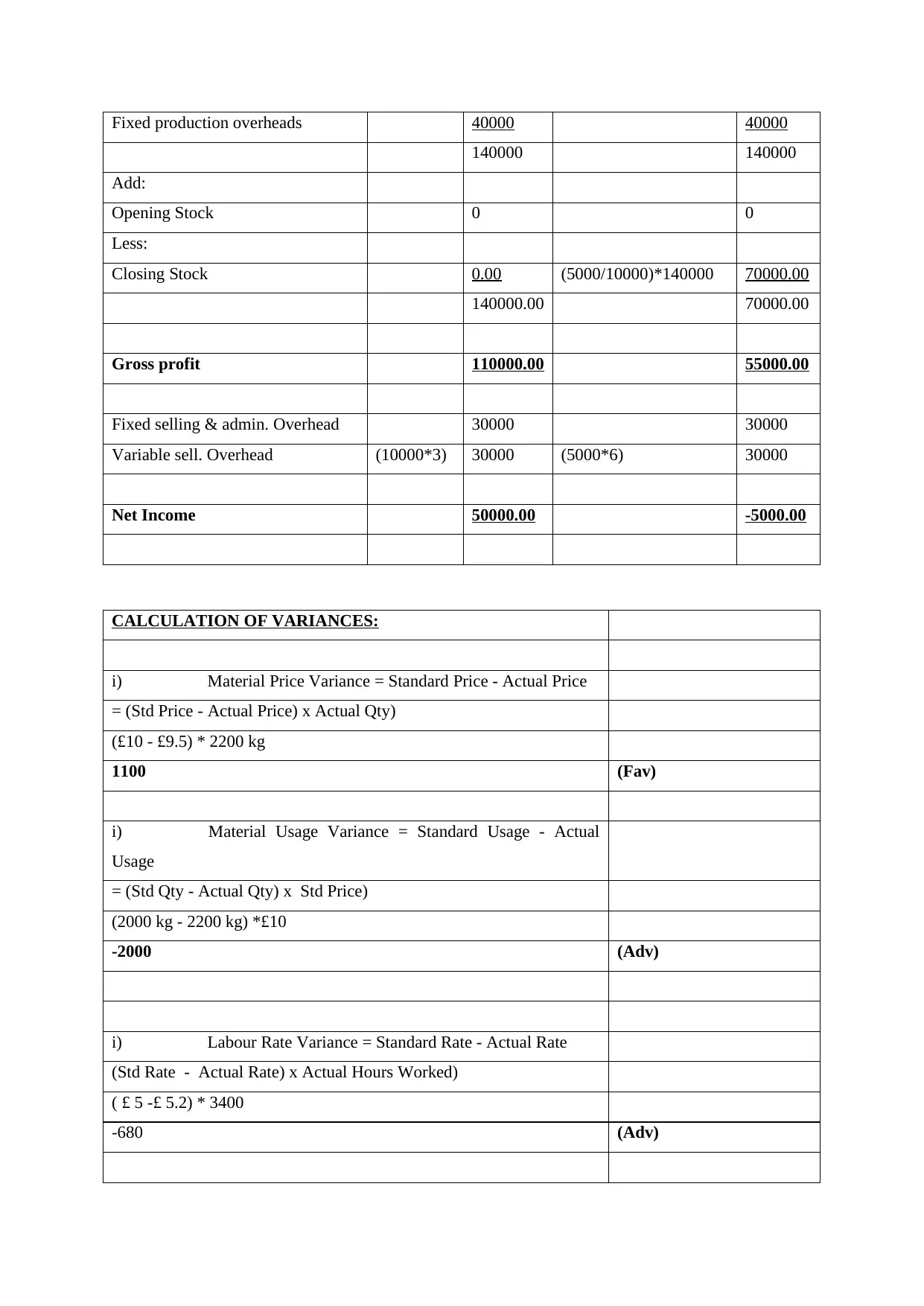

Labour Efficiency Variance = (standard hours - Actual hours worked)

X Std Rate

(3000 hrs - 3400 hrs) * £5

-2000 (Adv)

From the above it can be said that absorption costing method is a better method in

comparison to marginal costing in terms of usefulness. The profits shown by absorption

costing is more accurate and reliable as it takes into consideration both fixed and variable

cost manufacturing in calculating cost of production.Marginal costing is beneficial for newly

started business but for Creams Ltd. absorption costing is more appropriate.Along with that

absorption costing is recognised by GAAP which is preferred for external reporting

purpose.Also, except material price variance, all other variances are unfavourable to the

company which means that the company was not able to perform well as per the set

standards.

P4- Disadvantages and advantages of varied types of planning tools

There are several kinds of planning tools utilize for budgetary control in organization,

that is beneficial for them.

Zero based budgeting-

It is one of the best approaches of budgeting in which all expenses will be clarified for

each new period. The procedure of zero based budgeting begins from a zero base and all

function within company is analyzed for their costs and needs. It is management accounting

includes preparing and controlling budget from scratch with a zero base. Budgets are then

creating around what is required for upcoming time, instead of whether each budget is lower

or higher than previous one.

Advantages-

Zero based budgeting aid company in allocation of important resources efficiently, as

it does not look at earlier budget number instead looks at actual numbers (Petroia, 2017).

Against traditional budgeting approach that consist some arbitrary changes to previous

budget, this method makes all section relook every item of cash flow and manage their

operation costs. Thus, zero based budgeting considered as method of budgeting whereby all

X Std Rate

(3000 hrs - 3400 hrs) * £5

-2000 (Adv)

From the above it can be said that absorption costing method is a better method in

comparison to marginal costing in terms of usefulness. The profits shown by absorption

costing is more accurate and reliable as it takes into consideration both fixed and variable

cost manufacturing in calculating cost of production.Marginal costing is beneficial for newly

started business but for Creams Ltd. absorption costing is more appropriate.Along with that

absorption costing is recognised by GAAP which is preferred for external reporting

purpose.Also, except material price variance, all other variances are unfavourable to the

company which means that the company was not able to perform well as per the set

standards.

P4- Disadvantages and advantages of varied types of planning tools

There are several kinds of planning tools utilize for budgetary control in organization,

that is beneficial for them.

Zero based budgeting-

It is one of the best approaches of budgeting in which all expenses will be clarified for

each new period. The procedure of zero based budgeting begins from a zero base and all

function within company is analyzed for their costs and needs. It is management accounting

includes preparing and controlling budget from scratch with a zero base. Budgets are then

creating around what is required for upcoming time, instead of whether each budget is lower

or higher than previous one.

Advantages-

Zero based budgeting aid company in allocation of important resources efficiently, as

it does not look at earlier budget number instead looks at actual numbers (Petroia, 2017).

Against traditional budgeting approach that consist some arbitrary changes to previous

budget, this method makes all section relook every item of cash flow and manage their

operation costs. Thus, zero based budgeting considered as method of budgeting whereby all

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.