University Business Report: Repsol's YPF Acquisition Strategy

VerifiedAdded on 2021/04/21

|16

|3802

|63

Report

AI Summary

This report provides a detailed analysis of Repsol's acquisition of YPF, focusing on the strategic management decisions and financial implications of the deal. The report begins with a historical background of Repsol and its position in the oil industry, highlighting its dominant market share and financial capacity. It then delves into the strategic formulation process, including the identification of strategic options and the rationale behind the acquisition of YPF, discussing the challenges and obstacles Repsol faced. The analysis covers corporate, international, and internet strategies, as well as business growth considerations. Furthermore, the report presents a stand-alone analysis of both Repsol and YPF, including financial data from 1995 to 2000, and calculations of Weighted Average Cost of Capital (WACC). The report uses formulas and financial data to analyze the acquisition's value and the synergies it aimed to achieve, offering insights into the strategic and financial aspects of the merger.

1

Name:

Course

Professor’s name

University name

City, State

Date of submission

Name:

Course

Professor’s name

University name

City, State

Date of submission

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Historical background

Repsol was the biggest oil company in 1999 in Spain and had a capacity of refining 60%

of the country’s oil. It had 50% of serving station in the entire country and had over 23,762

employees worldwide. With this in mind, Repsol had the capacity of bidding a takeover from

any company it deemed strategically worthy to its requirements. It had maintained a dominant

stake in the countries petro-chemical industry and was the main wholesaler of gas and natural

gas in the country.

Strategic management has the fundamental objective of supporting the administrator in the

continuous search for methods through the development of a set of tools and conceptual maps

that allow the discovery of systemic relations that exist between the decisions made by the

administrator and the performance achieved by the organization (DePamphilis, 2018).

b. strategy formulation

the formulation of the strategy consists of the identification and evaluation of the different

strategic options that are presented, and culminates with the selection of one of them state that to

an organization, formulating a strategy involves developing a coherent plan to achieve the

Historical background

Repsol was the biggest oil company in 1999 in Spain and had a capacity of refining 60%

of the country’s oil. It had 50% of serving station in the entire country and had over 23,762

employees worldwide. With this in mind, Repsol had the capacity of bidding a takeover from

any company it deemed strategically worthy to its requirements. It had maintained a dominant

stake in the countries petro-chemical industry and was the main wholesaler of gas and natural

gas in the country.

Strategic management has the fundamental objective of supporting the administrator in the

continuous search for methods through the development of a set of tools and conceptual maps

that allow the discovery of systemic relations that exist between the decisions made by the

administrator and the performance achieved by the organization (DePamphilis, 2018).

b. strategy formulation

the formulation of the strategy consists of the identification and evaluation of the different

strategic options that are presented, and culminates with the selection of one of them state that to

an organization, formulating a strategy involves developing a coherent plan to achieve the

3

objectives through the most appropriate adjustment of the organization with its environment,

after a thorough strategic analysis should be chosen a strategy that allows the organization, In

addition to staying in the environment, improving their competitive position and increasing their

market share, (Müller-Stewens, Kunisch and Binder, n.d.) agree on that the formulation of

strategies must be a rational, explicit and simple process.

Traditional competitive strategies are subject to erosion. The additional features of today will be

standard tomorrow and, therefore, will no longer be exclusive. "What companies are currently

looking for through strategic direction is to create advantages with added value (hardly equal)

that place the organization in a privileged position in front of the other organizations of its same

nature,that locate it as a really competitive company.An analysis of the strategic position of the

two companies before the acquisition, their alternative strategic options and the rationale for the

acquisition (Weber, 2013).

For Repsol, it was a dominant force in the petrochemical industry and by that had all the

financial muscle and strategic organization advantage to take over YPF Company and many

others. The decision to take over YPF was necessitated by the fact that negotiations for a merger

had come under considerable difficulties that may have necessitated the 100% company

takeover. The fact of the matter is, Repsol had tried to acquire the whole company as a whole but

the Argentinian company was not willing. An obstacle to takeover of YPF was brought about by

the company’s article of association. At a public auction in 1999, Repsol had bought 14.99% of

the company’s share at $38 per share which was equivalent to $ 2 billion (Meitner, 2006). This

transaction triggered a clause that gave the company the option to buy the rest of the company

within 3 years. Repsol was not given the chance to buy the remaining part of the company and

objectives through the most appropriate adjustment of the organization with its environment,

after a thorough strategic analysis should be chosen a strategy that allows the organization, In

addition to staying in the environment, improving their competitive position and increasing their

market share, (Müller-Stewens, Kunisch and Binder, n.d.) agree on that the formulation of

strategies must be a rational, explicit and simple process.

Traditional competitive strategies are subject to erosion. The additional features of today will be

standard tomorrow and, therefore, will no longer be exclusive. "What companies are currently

looking for through strategic direction is to create advantages with added value (hardly equal)

that place the organization in a privileged position in front of the other organizations of its same

nature,that locate it as a really competitive company.An analysis of the strategic position of the

two companies before the acquisition, their alternative strategic options and the rationale for the

acquisition (Weber, 2013).

For Repsol, it was a dominant force in the petrochemical industry and by that had all the

financial muscle and strategic organization advantage to take over YPF Company and many

others. The decision to take over YPF was necessitated by the fact that negotiations for a merger

had come under considerable difficulties that may have necessitated the 100% company

takeover. The fact of the matter is, Repsol had tried to acquire the whole company as a whole but

the Argentinian company was not willing. An obstacle to takeover of YPF was brought about by

the company’s article of association. At a public auction in 1999, Repsol had bought 14.99% of

the company’s share at $38 per share which was equivalent to $ 2 billion (Meitner, 2006). This

transaction triggered a clause that gave the company the option to buy the rest of the company

within 3 years. Repsol was not given the chance to buy the remaining part of the company and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

was unable to get genuine control of the company at the auction. To obtain necessary synergies,

the company had to make a public offer of buying the remaining 85% of ypf at the stock market.

According to YPF s articles of association, it meant that Repsol required ready cash for this type

of transaction. A significant increase in the company’s debt would lead to financial risk on

Repsols side which could shake the petro chemical industry (Schmidlin, 2014).

Repsol strategy in investing in the Latin –American company was to increase its investment and

the geographical axis that was necessitated by the company. The gulf crisis of 1990, had slowed

growth of the brand that is Repsol but its investment strategy was not in any way blurred. Its end

sight game was to increase profits due to the company.

YPF Company on the other hand had significant stakes in the production and exploration

business in the south America in countries like chile, Argentina, Bolivia, brazil, peru, Venezuela

and the united states of America,. It made a lot of sense doing this. Its turnover in 1997 was 1500

million dollars which is respectable and a sizable company like this would bring effective

synergy and control (Thomas and Gup, 2010).

Corporate laws establish that corporate or corporate-level strategy is one that "solves the

fundamental questions: in what business or business should we be to maximize the long-term

profitability of the organization? Should we join and increase our presence in these businesses to

achieve a competitive advantage? “state corporate strategies as "the way in which the company

creates value through the configuration and coordination of multi-market activities". These

was unable to get genuine control of the company at the auction. To obtain necessary synergies,

the company had to make a public offer of buying the remaining 85% of ypf at the stock market.

According to YPF s articles of association, it meant that Repsol required ready cash for this type

of transaction. A significant increase in the company’s debt would lead to financial risk on

Repsols side which could shake the petro chemical industry (Schmidlin, 2014).

Repsol strategy in investing in the Latin –American company was to increase its investment and

the geographical axis that was necessitated by the company. The gulf crisis of 1990, had slowed

growth of the brand that is Repsol but its investment strategy was not in any way blurred. Its end

sight game was to increase profits due to the company.

YPF Company on the other hand had significant stakes in the production and exploration

business in the south America in countries like chile, Argentina, Bolivia, brazil, peru, Venezuela

and the united states of America,. It made a lot of sense doing this. Its turnover in 1997 was 1500

million dollars which is respectable and a sizable company like this would bring effective

synergy and control (Thomas and Gup, 2010).

Corporate laws establish that corporate or corporate-level strategy is one that "solves the

fundamental questions: in what business or business should we be to maximize the long-term

profitability of the organization? Should we join and increase our presence in these businesses to

achieve a competitive advantage? “state corporate strategies as "the way in which the company

creates value through the configuration and coordination of multi-market activities". These

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

strategies should allow to identify and delimit which is the business to which it is dedicated and

wants to dedicate the company now and in the future.

International strategies: (Weber, 2013) state that "international strategy implies that the

company sells its goods or services outside of your national market. " The managers of the

organizations must not only decide on the most appropriate entry strategy, but also on how to

obtain competitive advantages in international markets. This type of strategy takes into account

the territorial scope, which is one of the three that according to merger laws should contemplate

any organization for the formulation of strategies; apart from the territorial one, there are the

scope of the product and that of the company. According to merger laws, there are many reasons

for a company to decide to follow an international expansion; but the most obvious one is to

increase the size of the potential markets for its products and services (Pécherot Petitt and Ferris,

2013). When entering new world markets, the company obtains an increase in its income and

assets, but this also means a necessary adjustment in its operational activities and in the

personnel and infrastructure requirements.

The basic benefits that companies obtain once they have used the internationalization strategy: a

larger market; greater return on important capital investments, or investments in new products

and processes; more economies of scale and scope, or greater learning; and a competitive

advantage in terms of location. Internet strategies: the effective use of Internet and e-

comillionerce strategies can help an organization improve its competitive position in a sector and

increase its ability to create advantages based on low cost and differentiation strategies (Pécherot

Petitt and Ferris, 2013). merger laws state that the important thing for the company is not the

strategies should allow to identify and delimit which is the business to which it is dedicated and

wants to dedicate the company now and in the future.

International strategies: (Weber, 2013) state that "international strategy implies that the

company sells its goods or services outside of your national market. " The managers of the

organizations must not only decide on the most appropriate entry strategy, but also on how to

obtain competitive advantages in international markets. This type of strategy takes into account

the territorial scope, which is one of the three that according to merger laws should contemplate

any organization for the formulation of strategies; apart from the territorial one, there are the

scope of the product and that of the company. According to merger laws, there are many reasons

for a company to decide to follow an international expansion; but the most obvious one is to

increase the size of the potential markets for its products and services (Pécherot Petitt and Ferris,

2013). When entering new world markets, the company obtains an increase in its income and

assets, but this also means a necessary adjustment in its operational activities and in the

personnel and infrastructure requirements.

The basic benefits that companies obtain once they have used the internationalization strategy: a

larger market; greater return on important capital investments, or investments in new products

and processes; more economies of scale and scope, or greater learning; and a competitive

advantage in terms of location. Internet strategies: the effective use of Internet and e-

comillionerce strategies can help an organization improve its competitive position in a sector and

increase its ability to create advantages based on low cost and differentiation strategies (Pécherot

Petitt and Ferris, 2013). merger laws state that the important thing for the company is not the

6

Internet technology itself, but the actual use that the Internet makes to obtain profitable

transactions. These authors argue that the Internet phenomenon has reinforced the need for

effective strategic direction. The authors clarify that to achieve success, companies require more

than creating a website or a dot-com company. The success of e-business requires a new strategic

perspective that is built on the possibilities provided by information technologies, to the extent

that it allows Internet connectivity to transform the way business is carried out. It is noteworthy

that Vargas emphasize the need for organizations to create strategies to remain in the market, and

also highlight the role of the strategist to achieve this goal (Pécherot Petitt and Ferris, 2013) .

BUSINESS GROWTH

. The concept Before mentioning the definition of business growth, it is worth clarifying that, as,

there is no criterion unit with respect to this concept within the economic and administrative

literature ; This makes some authors consider growth as a desired goal and others as a

consequence of the "proper" management of organizations (Cooper and Finkelstein, 2013). Not

all organizations have growth as their main objective; However, this can also be generated with

an adequate use of the resources coming from the strategic addressing process. Some authors

propose definition.

When calculating the value of the price of the merger, Tangible operating synergies are the

benefits that can be easily isolated and quantified in terms of increased future cash flows, such as

income opportunities and specific cost reductions. The quantification of tangible operating

synergies usually consists of determining the expected incremental cash flow net of the costs of

realizing the expected synergies, and related taxes (Cooper and Finkelstein, 2013).

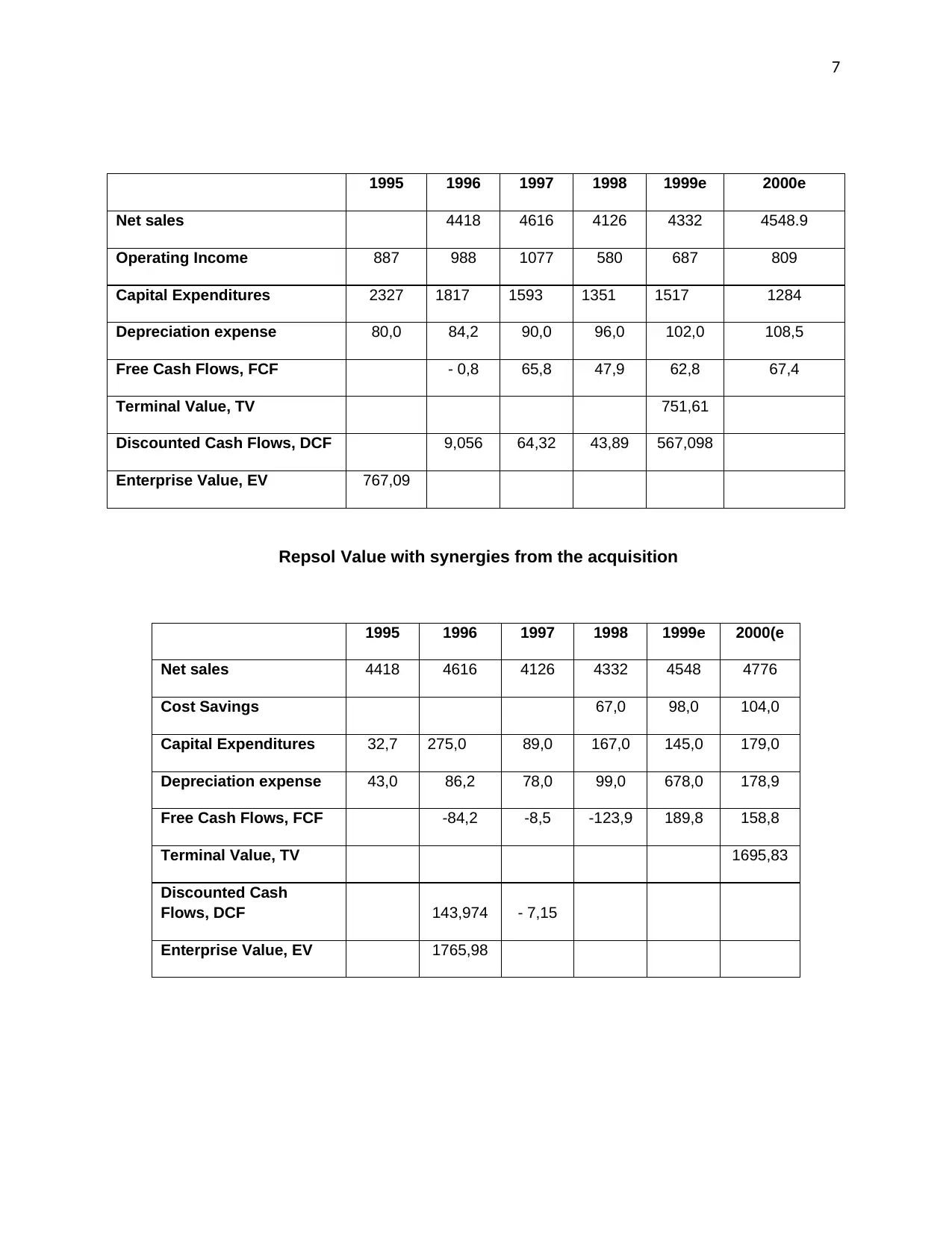

Repsol and YSP: Stand-Along Analysis

Internet technology itself, but the actual use that the Internet makes to obtain profitable

transactions. These authors argue that the Internet phenomenon has reinforced the need for

effective strategic direction. The authors clarify that to achieve success, companies require more

than creating a website or a dot-com company. The success of e-business requires a new strategic

perspective that is built on the possibilities provided by information technologies, to the extent

that it allows Internet connectivity to transform the way business is carried out. It is noteworthy

that Vargas emphasize the need for organizations to create strategies to remain in the market, and

also highlight the role of the strategist to achieve this goal (Pécherot Petitt and Ferris, 2013) .

BUSINESS GROWTH

. The concept Before mentioning the definition of business growth, it is worth clarifying that, as,

there is no criterion unit with respect to this concept within the economic and administrative

literature ; This makes some authors consider growth as a desired goal and others as a

consequence of the "proper" management of organizations (Cooper and Finkelstein, 2013). Not

all organizations have growth as their main objective; However, this can also be generated with

an adequate use of the resources coming from the strategic addressing process. Some authors

propose definition.

When calculating the value of the price of the merger, Tangible operating synergies are the

benefits that can be easily isolated and quantified in terms of increased future cash flows, such as

income opportunities and specific cost reductions. The quantification of tangible operating

synergies usually consists of determining the expected incremental cash flow net of the costs of

realizing the expected synergies, and related taxes (Cooper and Finkelstein, 2013).

Repsol and YSP: Stand-Along Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

1995 1996 1997 1998 1999e 2000e

Net sales 4418 4616 4126 4332 4548.9

Operating Income 887 988 1077 580 687 809

Capital Expenditures 2327 1817 1593 1351 1517 1284

Depreciation expense 80,0 84,2 90,0 96,0 102,0 108,5

Free Cash Flows, FCF - 0,8 65,8 47,9 62,8 67,4

Terminal Value, TV 751,61

Discounted Cash Flows, DCF 9,056 64,32 43,89 567,098

Enterprise Value, EV 767,09

Repsol Value with synergies from the acquisition

1995 1996 1997 1998 1999e 2000(e

Net sales 4418 4616 4126 4332 4548 4776

Cost Savings 67,0 98,0 104,0

Capital Expenditures 32,7 275,0 89,0 167,0 145,0 179,0

Depreciation expense 43,0 86,2 78,0 99,0 678,0 178,9

Free Cash Flows, FCF -84,2 -8,5 -123,9 189,8 158,8

Terminal Value, TV 1695,83

Discounted Cash

Flows, DCF 143,974 - 7,15

Enterprise Value, EV 1765,98

1995 1996 1997 1998 1999e 2000e

Net sales 4418 4616 4126 4332 4548.9

Operating Income 887 988 1077 580 687 809

Capital Expenditures 2327 1817 1593 1351 1517 1284

Depreciation expense 80,0 84,2 90,0 96,0 102,0 108,5

Free Cash Flows, FCF - 0,8 65,8 47,9 62,8 67,4

Terminal Value, TV 751,61

Discounted Cash Flows, DCF 9,056 64,32 43,89 567,098

Enterprise Value, EV 767,09

Repsol Value with synergies from the acquisition

1995 1996 1997 1998 1999e 2000(e

Net sales 4418 4616 4126 4332 4548 4776

Cost Savings 67,0 98,0 104,0

Capital Expenditures 32,7 275,0 89,0 167,0 145,0 179,0

Depreciation expense 43,0 86,2 78,0 99,0 678,0 178,9

Free Cash Flows, FCF -84,2 -8,5 -123,9 189,8 158,8

Terminal Value, TV 1695,83

Discounted Cash

Flows, DCF 143,974 - 7,15

Enterprise Value, EV 1765,98

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

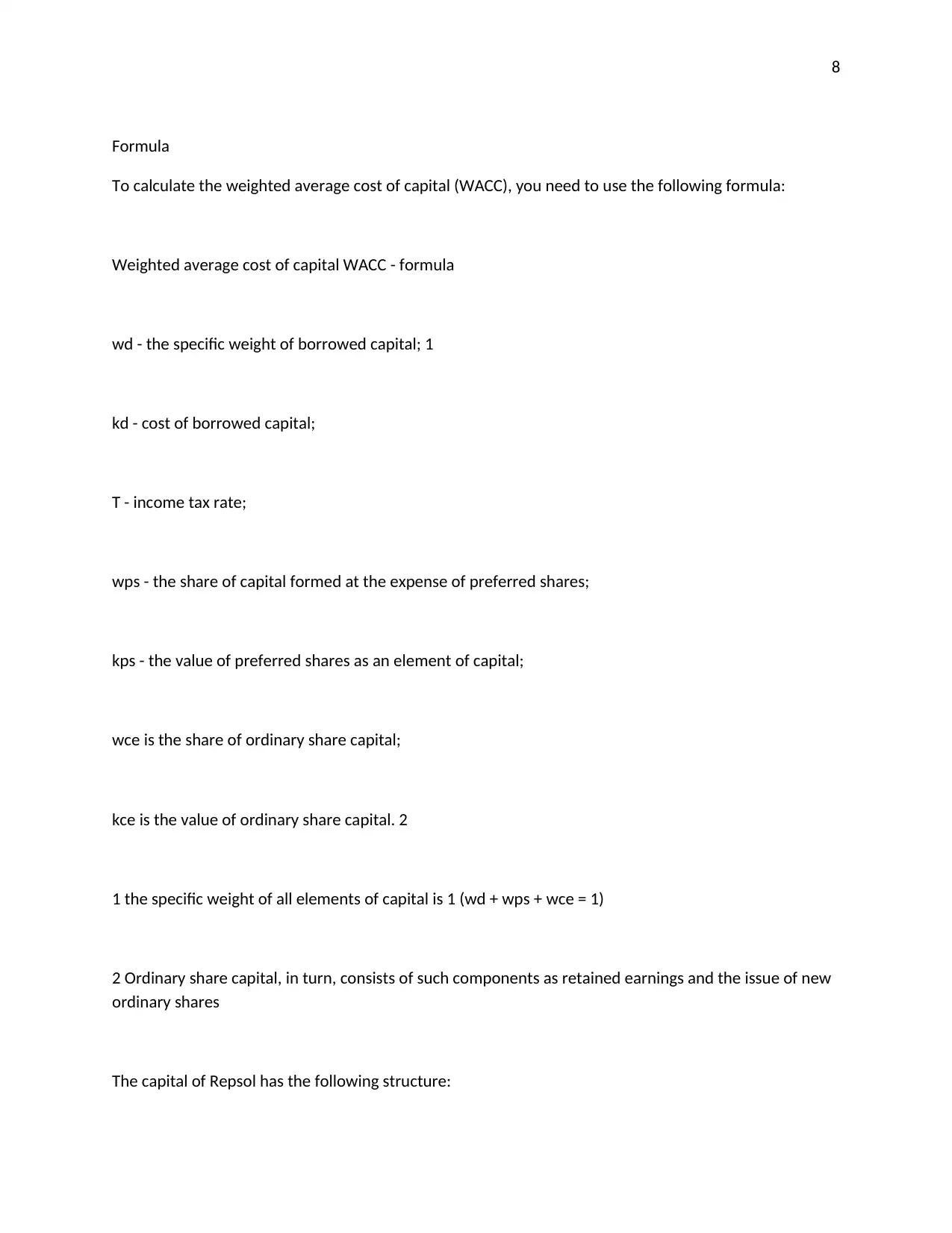

Formula

To calculate the weighted average cost of capital (WACC), you need to use the following formula:

Weighted average cost of capital WACC - formula

wd - the specific weight of borrowed capital; 1

kd - cost of borrowed capital;

T - income tax rate;

wps - the share of capital formed at the expense of preferred shares;

kps - the value of preferred shares as an element of capital;

wce is the share of ordinary share capital;

kce is the value of ordinary share capital. 2

1 the specific weight of all elements of capital is 1 (wd + wps + wce = 1)

2 Ordinary share capital, in turn, consists of such components as retained earnings and the issue of new

ordinary shares

The capital of Repsol has the following structure:

Formula

To calculate the weighted average cost of capital (WACC), you need to use the following formula:

Weighted average cost of capital WACC - formula

wd - the specific weight of borrowed capital; 1

kd - cost of borrowed capital;

T - income tax rate;

wps - the share of capital formed at the expense of preferred shares;

kps - the value of preferred shares as an element of capital;

wce is the share of ordinary share capital;

kce is the value of ordinary share capital. 2

1 the specific weight of all elements of capital is 1 (wd + wps + wce = 1)

2 Ordinary share capital, in turn, consists of such components as retained earnings and the issue of new

ordinary shares

The capital of Repsol has the following structure:

9

ordinary share capital of $ 75 million;

preferred share capital is 5 million cu.

borrowed capital is 30 million cu.

Ordinary share capital was formed by ordinary shares, the beta coefficient of which is 1.57. The

preferred share capital is formed by preferred shares, for which a fixed dividend of $ 3.5 is paid, and

their market value is 18.75 USD. The borrowed capital was formed by issuing bonds with a fixed coupon

rate of 16.5%. Suppose that the expected market yield is 15.5%, a risk-free interest rate of 4.75%, and a

profit tax rate of 30%.

In order to use the above formula and calculate the WACC, it is necessary to determine the specific

weight of each source of capital, as well as their cost. The share of the ordinary share capital is 0.682,

the preferred share capital is 0.045 and the borrowed capital is 0.273.

wce = 75 / (75 + 5 + 30) = 0.682

wps = 5 / (75 + 5 + 30) = 0.045

wd = 30 / (75 + 5 + 30) = 0.273

The required rate of return for ordinary shares can be estimated using the Capital Asset Price Model:

Capital Assets Pricing Model CAPM - formula

where ki is the required rate of return for the i-th stock;

KRF - risk-free interest rate;

ordinary share capital of $ 75 million;

preferred share capital is 5 million cu.

borrowed capital is 30 million cu.

Ordinary share capital was formed by ordinary shares, the beta coefficient of which is 1.57. The

preferred share capital is formed by preferred shares, for which a fixed dividend of $ 3.5 is paid, and

their market value is 18.75 USD. The borrowed capital was formed by issuing bonds with a fixed coupon

rate of 16.5%. Suppose that the expected market yield is 15.5%, a risk-free interest rate of 4.75%, and a

profit tax rate of 30%.

In order to use the above formula and calculate the WACC, it is necessary to determine the specific

weight of each source of capital, as well as their cost. The share of the ordinary share capital is 0.682,

the preferred share capital is 0.045 and the borrowed capital is 0.273.

wce = 75 / (75 + 5 + 30) = 0.682

wps = 5 / (75 + 5 + 30) = 0.045

wd = 30 / (75 + 5 + 30) = 0.273

The required rate of return for ordinary shares can be estimated using the Capital Asset Price Model:

Capital Assets Pricing Model CAPM - formula

where ki is the required rate of return for the i-th stock;

KRF - risk-free interest rate;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

βi - beta coefficient of the i-th stock;

- Expected market yield.

Substituting the initial data in the CAPM model, we obtain the required rate of return for ordinary

shares equal to 21.63%.

kce = 4.75 + 1.57 (15.5-4.75) = 21.63%

The required rate of return for preferred shares (kps) is calculated by the formula:

Required rate of return for preferred shares - formula

where Dps is the dividend on preferred shares;

Pps is the market price of a preferred share.

Therefore, the required rate of return for preferred shares of YFP is 18.67%.

kps = 3.5 / 18.75 * 100% = 18.67%

Thus, the weighted average cost of YFP's capital will be 18.74%.

WACC = 0.273 * 16.5 * (1-0.3) + 0.045 * 18.67 + 0.682 * 21.63 = 18.74%

βi - beta coefficient of the i-th stock;

- Expected market yield.

Substituting the initial data in the CAPM model, we obtain the required rate of return for ordinary

shares equal to 21.63%.

kce = 4.75 + 1.57 (15.5-4.75) = 21.63%

The required rate of return for preferred shares (kps) is calculated by the formula:

Required rate of return for preferred shares - formula

where Dps is the dividend on preferred shares;

Pps is the market price of a preferred share.

Therefore, the required rate of return for preferred shares of YFP is 18.67%.

kps = 3.5 / 18.75 * 100% = 18.67%

Thus, the weighted average cost of YFP's capital will be 18.74%.

WACC = 0.273 * 16.5 * (1-0.3) + 0.045 * 18.67 + 0.682 * 21.63 = 18.74%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Modern methods of valuation of companies, I must admit, have not far gone from the classical

book truths prescribed by Mason and Harrison. Business angels, private investors, venture funds

and entrepreneurs continue to use coefficients and multipliers, discounted cash flows and net

assets for business valuation. But which method is right for you?

General Provisions

Valuation of the company assumes a number of assumptions, in particular, the real volume of the

market (it is especially difficult to "digitize" the young, emerging industries), as well as the

financial forecast. Often business plans of an entrepreneur may not coincide with the investor's

vision.

At the earliest stage of the company's development, the investor pays special attention to analysis

and other indicators of the company: the team, the potential demand for technology, systemic

risks associated with the overall economic and political background, as well as possible barriers

to entry into the competitors' market.Basis of valuation: the company's value is determined from

the amount of free cash flow of future periods. The value of the flow is discounted taking into

account the risks of future years. The discount rate is determined based on the weighted average

cost of capital(Breunsbach, 2011).

Suppose that the company Buyer REPSOL intends to buy Target YFP and has estimated the

Modern methods of valuation of companies, I must admit, have not far gone from the classical

book truths prescribed by Mason and Harrison. Business angels, private investors, venture funds

and entrepreneurs continue to use coefficients and multipliers, discounted cash flows and net

assets for business valuation. But which method is right for you?

General Provisions

Valuation of the company assumes a number of assumptions, in particular, the real volume of the

market (it is especially difficult to "digitize" the young, emerging industries), as well as the

financial forecast. Often business plans of an entrepreneur may not coincide with the investor's

vision.

At the earliest stage of the company's development, the investor pays special attention to analysis

and other indicators of the company: the team, the potential demand for technology, systemic

risks associated with the overall economic and political background, as well as possible barriers

to entry into the competitors' market.Basis of valuation: the company's value is determined from

the amount of free cash flow of future periods. The value of the flow is discounted taking into

account the risks of future years. The discount rate is determined based on the weighted average

cost of capital(Breunsbach, 2011).

Suppose that the company Buyer REPSOL intends to buy Target YFP and has estimated the

12

value of Target REPSOL in US $ 23.0 million based on a free cash flow of US $ 2.5MILLION

per year with a discount rate of 11.0%. Additionally, Buyer REPSOL anticipates certain

synergies and expenses once the transaction has been closed, such as: Reduction of personnel

costs of US $ 400,000 per year due to the merger. Personnel settlement expenses of US $

200,000.Buyer REPSOL It has a 40% tax margin Additional sales of US $ 1.0MILLION in the

first year after the acquisition, US $ 2.0MILLION in the second year and US $ 3.0MILLION in

the third year and beyond. The net contribution of these incremental sales is 30%.Because Target

YFP has excess capacity, will not incur fixed costs or capital increases. The working capital is

projected at 10% of the sales of Target YFP. Because the synergy will help Buyer REPSOL to

obtain a better capital structure, the discount rate of 11.0% is reduced to 10% (like better credit

rates). Buyer REPSOL estimates that with the acquisition, it will be able to penetrate into a new

market, which is valued at US $ 5.0MILLION.

A smart merger and acquisition can give a small company the needed boost to become big.

There are factors that both parties should look at that may affect mergers and acquisitions. When

two companies merge their operations, it is called a merger. An acquisition is when a company

decides to purchase another it is called an acquisition (Thomas and Gup, 2010). Both

acquisitions and mergers result in a combined entity. There is requirement for regulatory and

shareholders approvals before any merger or acquisition can take place. In the case of Respol

acquiring YPF, there are several factors that were put in place that affect and influence any

merger or acquisition. Some of the factors include; access to talented employees and the

synergies of revenues and costs of the two companies.

value of Target REPSOL in US $ 23.0 million based on a free cash flow of US $ 2.5MILLION

per year with a discount rate of 11.0%. Additionally, Buyer REPSOL anticipates certain

synergies and expenses once the transaction has been closed, such as: Reduction of personnel

costs of US $ 400,000 per year due to the merger. Personnel settlement expenses of US $

200,000.Buyer REPSOL It has a 40% tax margin Additional sales of US $ 1.0MILLION in the

first year after the acquisition, US $ 2.0MILLION in the second year and US $ 3.0MILLION in

the third year and beyond. The net contribution of these incremental sales is 30%.Because Target

YFP has excess capacity, will not incur fixed costs or capital increases. The working capital is

projected at 10% of the sales of Target YFP. Because the synergy will help Buyer REPSOL to

obtain a better capital structure, the discount rate of 11.0% is reduced to 10% (like better credit

rates). Buyer REPSOL estimates that with the acquisition, it will be able to penetrate into a new

market, which is valued at US $ 5.0MILLION.

A smart merger and acquisition can give a small company the needed boost to become big.

There are factors that both parties should look at that may affect mergers and acquisitions. When

two companies merge their operations, it is called a merger. An acquisition is when a company

decides to purchase another it is called an acquisition (Thomas and Gup, 2010). Both

acquisitions and mergers result in a combined entity. There is requirement for regulatory and

shareholders approvals before any merger or acquisition can take place. In the case of Respol

acquiring YPF, there are several factors that were put in place that affect and influence any

merger or acquisition. Some of the factors include; access to talented employees and the

synergies of revenues and costs of the two companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.