Postgraduate Research Proposal: Risk Management for Investors

VerifiedAdded on 2023/04/21

|19

|5321

|126

Report

AI Summary

This research proposal aims to identify suitable risk management techniques for investors, particularly in Emirates Airlines. It focuses on portfolio setting and strategies using VAR and CAPM approaches. The proposal discusses risk assessment, quantitative measurement of risk factors, and classifying risks from different viewpoints. The literature review covers risk management processes using CAPM and VAR, while the research methodology suggests exploratory research. The study intends to determine the best portfolio setting, effective risk management, and the impact of VAR on investors in Emirates Airlines. This document is a student contribution and more solved assignments are available on Desklib.

Running head: BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK

MANAGEMENT OF INVESTORS

Business Research Method Research Proposal- Risk Management of Investors

Name of the Student

Name of the University

Author’s Note

MANAGEMENT OF INVESTORS

Business Research Method Research Proposal- Risk Management of Investors

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

Executive Summary

The research aims to identify the most suitable technique of risk management for investors in the

Emirates Airlines. The main objective of the research is identified with recognising the best

portfolio setting and strategy to manage the risk of portfolio for investors in Emirates Airlines. In

addition to this, the portfolio risk management for investors in the Emirates Airlines will be used

with VAR and CAPM approach. The overall risk pertaining to the investment decision is seen

with understanding of the quantitative measurement of the occurrence of the various result along

with the anticipated risk factors. In several ways the risks are considered with different

viewpoints which provides the ease of classifying the risk for investors in the Emirates Airlines.

The overall depictions of the study will identify the best portfolio setting and way to manage the

risk of portfolio and assessment for effective risk management using VAR on the investors in the

Emirates Airlines. The discussion of the literature review is suggested with general information

on the risk management process using CAPM and VAR. The various types of the discussions on

the research methodology will be depicted with following exploratory research.

INVESTORS

Executive Summary

The research aims to identify the most suitable technique of risk management for investors in the

Emirates Airlines. The main objective of the research is identified with recognising the best

portfolio setting and strategy to manage the risk of portfolio for investors in Emirates Airlines. In

addition to this, the portfolio risk management for investors in the Emirates Airlines will be used

with VAR and CAPM approach. The overall risk pertaining to the investment decision is seen

with understanding of the quantitative measurement of the occurrence of the various result along

with the anticipated risk factors. In several ways the risks are considered with different

viewpoints which provides the ease of classifying the risk for investors in the Emirates Airlines.

The overall depictions of the study will identify the best portfolio setting and way to manage the

risk of portfolio and assessment for effective risk management using VAR on the investors in the

Emirates Airlines. The discussion of the literature review is suggested with general information

on the risk management process using CAPM and VAR. The various types of the discussions on

the research methodology will be depicted with following exploratory research.

2BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

Table of Contents

1.0 Introduction....................................................................................................................3

1.1 Research Aim.............................................................................................................4

1.2 Research Objective....................................................................................................4

1.3 Research Question.....................................................................................................4

1.4 Rationale for the research..........................................................................................4

2.0 Literature Review..........................................................................................................5

2.1 Risk Management Process.........................................................................................5

2.2 Capital Asset Pricing Model......................................................................................6

2.3 Value at Risk (VAR).................................................................................................8

3.0 Research Methodology................................................................................................10

3.1 Research Approach..................................................................................................10

3.2 Data Collection and Analysis..................................................................................10

3.3 Method of Analysis..................................................................................................11

3.4 Data Analysis...........................................................................................................11

3.5 Research Project Plan..............................................................................................13

4.0 Conclusion...................................................................................................................14

References..........................................................................................................................16

INVESTORS

Table of Contents

1.0 Introduction....................................................................................................................3

1.1 Research Aim.............................................................................................................4

1.2 Research Objective....................................................................................................4

1.3 Research Question.....................................................................................................4

1.4 Rationale for the research..........................................................................................4

2.0 Literature Review..........................................................................................................5

2.1 Risk Management Process.........................................................................................5

2.2 Capital Asset Pricing Model......................................................................................6

2.3 Value at Risk (VAR).................................................................................................8

3.0 Research Methodology................................................................................................10

3.1 Research Approach..................................................................................................10

3.2 Data Collection and Analysis..................................................................................10

3.3 Method of Analysis..................................................................................................11

3.4 Data Analysis...........................................................................................................11

3.5 Research Project Plan..............................................................................................13

4.0 Conclusion...................................................................................................................14

References..........................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

1.0 Introduction

In general, investment decisions are seen as those which are related to initiate an action to

improve the overall strategic position of the company. This needs to be related to risk analysis

which are based on fundamental changes pertaining to decision making. In this way, the risk

management is identified as the main criteria for decision making. The management decisions

need to be based on the magnitude of the risk taken and ways in which such risks are managed.

In a similar way, the risk in the investment process is seen as a function of exercising the risk in

the investment process. In several cases the uncertainty related to the return in the project

management is considered with the risk of investment of the relevant projects which are needed

to be addressed in making the crucial investment decisions. The overall degree of risk and

profitability of the investment has been able to determine the acceptability of the project. The

overall risk impact of the project has been considered with the profitability which is multiplied as

per the nature of the investment in the project. The decision making under the risk is considered

with several alternatives along with assessment of the likelihood of each alternative. As per the

risk assessment it needs to be seen that decision maker is seen to be having more information

than the conditions pertaining to uncertainty (Golub, Greenberg and Ratcliffe 2018).

The risk is determined as a function for the length of the investment process and the

analysis of the risk is seen with a more efficient implementation of the investment project. This

is due to the fact that it considers investment in the project in a realistic manner thereby

considering the relationship among the technological parameters, time and cost. Moreover, the

risk analysis further contributes to the economic and financial evaluation of the project which is

conducive in revealing the risk factors and also influencing the decision-making criteria (Gatzert

and Kosub 2016).

INVESTORS

1.0 Introduction

In general, investment decisions are seen as those which are related to initiate an action to

improve the overall strategic position of the company. This needs to be related to risk analysis

which are based on fundamental changes pertaining to decision making. In this way, the risk

management is identified as the main criteria for decision making. The management decisions

need to be based on the magnitude of the risk taken and ways in which such risks are managed.

In a similar way, the risk in the investment process is seen as a function of exercising the risk in

the investment process. In several cases the uncertainty related to the return in the project

management is considered with the risk of investment of the relevant projects which are needed

to be addressed in making the crucial investment decisions. The overall degree of risk and

profitability of the investment has been able to determine the acceptability of the project. The

overall risk impact of the project has been considered with the profitability which is multiplied as

per the nature of the investment in the project. The decision making under the risk is considered

with several alternatives along with assessment of the likelihood of each alternative. As per the

risk assessment it needs to be seen that decision maker is seen to be having more information

than the conditions pertaining to uncertainty (Golub, Greenberg and Ratcliffe 2018).

The risk is determined as a function for the length of the investment process and the

analysis of the risk is seen with a more efficient implementation of the investment project. This

is due to the fact that it considers investment in the project in a realistic manner thereby

considering the relationship among the technological parameters, time and cost. Moreover, the

risk analysis further contributes to the economic and financial evaluation of the project which is

conducive in revealing the risk factors and also influencing the decision-making criteria (Gatzert

and Kosub 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

1.1 Research Aim

The research aims to identify the most suitable technique of risk management for

investors in the Emirates Airlines

1.2 Research Objective

The research objectives are listed as follows:

To identify the best portfolio setting and way to manage the risk of portfolio for investors

in the Emirates Airlines

To identify portfolio risk management for investors in the Emirates Airlines using VAR

and CAPM approach

1.3 Research Question

The research questions are listed below as follows:

How effective is investor risk management using CAPM?

What is effect of risk management using VAR on the investors?

1.4 Rationale for the research

The overall risk pertaining to the investment decision is seen with understanding of the

quantitative measurement of anticipated risk factors. In several ways the risks are considered

with different viewpoints which provides the ease of classifying the risk for investors in the

Emirates Airlines. The overall depictions of the study will identify the best portfolio setting and

way to manage the risk of portfolio and assessment of effect of risk management using VAR on

the investors in the Emirates Airlines (Calomiris and Carlson 2016).

INVESTORS

1.1 Research Aim

The research aims to identify the most suitable technique of risk management for

investors in the Emirates Airlines

1.2 Research Objective

The research objectives are listed as follows:

To identify the best portfolio setting and way to manage the risk of portfolio for investors

in the Emirates Airlines

To identify portfolio risk management for investors in the Emirates Airlines using VAR

and CAPM approach

1.3 Research Question

The research questions are listed below as follows:

How effective is investor risk management using CAPM?

What is effect of risk management using VAR on the investors?

1.4 Rationale for the research

The overall risk pertaining to the investment decision is seen with understanding of the

quantitative measurement of anticipated risk factors. In several ways the risks are considered

with different viewpoints which provides the ease of classifying the risk for investors in the

Emirates Airlines. The overall depictions of the study will identify the best portfolio setting and

way to manage the risk of portfolio and assessment of effect of risk management using VAR on

the investors in the Emirates Airlines (Calomiris and Carlson 2016).

5BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

2.0 Literature Review

The risk management is a phrase which is referred with buying and selling of the

investment under a certain portfolio. The risk management is also seen to cover the various

aspects of different securities such as assets, such as “bonds, shares and real estate”. The

appropriate process of the risk management is often built on the contracts available with the fund

managers, institutional investors and educational establishments. The service related to the

investment management are depicted to be considered as per allocation of asset, stock selection,

financial statement and implementation of plan. Based on the previous literature, the investors

management has been considered with appointing financial brokers who will provide sufficient

details on the existing risk of the portfolio (Brustbauer 2016).

2.1 Risk Management Process

The beginning of the risk management process is aimed at identifying the potential risk

factors for the investors. These are ranging in terms of risk identification which starts with

sourcing of the problems such as deviations in the return of the portfolio of the company. In the

process of source analysis, the risk may be either internal or external which is considered as the

target of risk management. The overall use of risk management process is considered to

commence with the use of mitigation strategies instead of the definition of risk used with the

factors of decision making. The main of the sources of the risk are inferred with stakeholders of

the project (McNeil, Freyand Embrechts 2015).

The depiction of the problem analysis is created on the risks which are related to the

initial threats of investment in a certain company. For instance, in the stage of problem analysis

the important nature of the difficulties needs to be depicted with the threat of the abuse of the

confidential information and the threat of the human errors in depicting the risk management of a

portfolio. These threats still be persistent on the different types of the entities which are most

INVESTORS

2.0 Literature Review

The risk management is a phrase which is referred with buying and selling of the

investment under a certain portfolio. The risk management is also seen to cover the various

aspects of different securities such as assets, such as “bonds, shares and real estate”. The

appropriate process of the risk management is often built on the contracts available with the fund

managers, institutional investors and educational establishments. The service related to the

investment management are depicted to be considered as per allocation of asset, stock selection,

financial statement and implementation of plan. Based on the previous literature, the investors

management has been considered with appointing financial brokers who will provide sufficient

details on the existing risk of the portfolio (Brustbauer 2016).

2.1 Risk Management Process

The beginning of the risk management process is aimed at identifying the potential risk

factors for the investors. These are ranging in terms of risk identification which starts with

sourcing of the problems such as deviations in the return of the portfolio of the company. In the

process of source analysis, the risk may be either internal or external which is considered as the

target of risk management. The overall use of risk management process is considered to

commence with the use of mitigation strategies instead of the definition of risk used with the

factors of decision making. The main of the sources of the risk are inferred with stakeholders of

the project (McNeil, Freyand Embrechts 2015).

The depiction of the problem analysis is created on the risks which are related to the

initial threats of investment in a certain company. For instance, in the stage of problem analysis

the important nature of the difficulties needs to be depicted with the threat of the abuse of the

confidential information and the threat of the human errors in depicting the risk management of a

portfolio. These threats still be persistent on the different types of the entities which are most

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

crucial to the legislative bodies, shareholders and the customers. The financial risk considered

with the investment projects are also seen to be based on several number of other factors which

are depicted to be considered with the fluctuation in the currency. This is seen to be especially

evident among the different types of the international projects. In the recent countries the

constructions of the privately financed infrastructures are depicted to be based on the use of

foreign capital. This is further seen to be considered as per running the risk of devaluation of

local currency. The international lenders have rarely shown their interest on preferred payments

associated to the foreign currency. In the past the government and the companies are seen to be

accepting the currency risk which are inferred with the increasing demand of the private

financing. The past public companies and the government has been seen to be accepting the

number of the factors which are inferred to be considered with the political stability. These

techniques are mainly considered as the investor risk management of the unsystematic risks

(Olson and Wu 2015).

2.2 Capital Asset Pricing Model

It is depicted that CAPM is built on the portfolio model suggested by Harry Markowitz in

1959. The Capital Asset Pricing Model (CAPM) describes the relationship between systematic

risk and expected return for assets, particularly stocks. CAPM is widely used throughout finance

for pricing risky securities and generating expected returns for assets given the risk of those

assets and cost of capital. This model considers the risk as “mean-variance of the efficient

portfolio”. This portfolio risk management tool is seen to infer whether the risk will be

minimized with expected return or maximized with a given level of risk. Typically, such a

technique of the risk management procedure is seen to be ideal for managing systematic risk of

the investors. The depiction of the systematic risk is considered with various types of the

underlying investment risks. In case there is situation of inflation which resists the economic

sectors. In case the rates of the interest are seen to be high then an individual can consider the

INVESTORS

crucial to the legislative bodies, shareholders and the customers. The financial risk considered

with the investment projects are also seen to be based on several number of other factors which

are depicted to be considered with the fluctuation in the currency. This is seen to be especially

evident among the different types of the international projects. In the recent countries the

constructions of the privately financed infrastructures are depicted to be based on the use of

foreign capital. This is further seen to be considered as per running the risk of devaluation of

local currency. The international lenders have rarely shown their interest on preferred payments

associated to the foreign currency. In the past the government and the companies are seen to be

accepting the currency risk which are inferred with the increasing demand of the private

financing. The past public companies and the government has been seen to be accepting the

number of the factors which are inferred to be considered with the political stability. These

techniques are mainly considered as the investor risk management of the unsystematic risks

(Olson and Wu 2015).

2.2 Capital Asset Pricing Model

It is depicted that CAPM is built on the portfolio model suggested by Harry Markowitz in

1959. The Capital Asset Pricing Model (CAPM) describes the relationship between systematic

risk and expected return for assets, particularly stocks. CAPM is widely used throughout finance

for pricing risky securities and generating expected returns for assets given the risk of those

assets and cost of capital. This model considers the risk as “mean-variance of the efficient

portfolio”. This portfolio risk management tool is seen to infer whether the risk will be

minimized with expected return or maximized with a given level of risk. Typically, such a

technique of the risk management procedure is seen to be ideal for managing systematic risk of

the investors. The depiction of the systematic risk is considered with various types of the

underlying investment risks. In case there is situation of inflation which resists the economic

sectors. In case the rates of the interest are seen to be high then an individual can consider the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

inflation resistant factors. If the rates of the inflation are high then utility stocks move slowly

with the issuing of the bonds (Freyman Collins and Barton 2015).

In the later stages CAPM model was identified with mean-variance with two more

assumptions added in Markowitz’s assumptions. CAPM is seen with vast meaning of the

practical application for estimating the cost of capital for evaluating performance of managing

the portfolio. The main assumption of the CAPM is considered among the investors as attaining

the target point on effective frontier at which the return will be capitalized on for the same level

of risk. The assumptions also hold the consideration for the investors in lending and borrowing

unlimited sum of money at a risk-free rate of return. It needs to be also seen that the nominal

risk-free rate of return can be collected through buying stability and government T-Bills. In

general, the capital markets are often identified to be in equilibrium and the initial investment is

prices as per the risk level. This model also assumes perfect market with no additional taxes,

transaction costs and inflation. The changes pertaining to adjustment in inflation and inflation

rate are not fully anticipated (Hoyt and Liebenberg 2015).

These investments can be absolutely divisible and understood in case there are barriers

for preventing the investors from selling or buying of fractional shares of asset or portfolio. The

calculation used in CAPM can be described as following:

𝐸(𝑅! ) = 𝑅! + 𝛽! (𝑅! − 𝑅! )

where:“𝐸 𝑅!

𝑖𝑠 𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑅𝑒𝑡𝑢𝑟𝑛 𝑐𝑜𝑚𝑝𝑢𝑡𝑒𝑑 𝑎𝑐𝑐𝑜𝑟𝑑𝑖𝑛𝑔 𝑡𝑜 𝐶𝐴𝑃𝑀”

“𝑅! 𝑖𝑠 𝑅𝑖𝑠𝑘𝑙𝑒𝑠𝑠 𝑅𝑎𝑡𝑒 𝑜𝑓 𝑅𝑒𝑡𝑢𝑟𝑛”

“𝛽! 𝑖𝑠 𝐵𝑒𝑡𝑎 (Systematic risks)”

INVESTORS

inflation resistant factors. If the rates of the inflation are high then utility stocks move slowly

with the issuing of the bonds (Freyman Collins and Barton 2015).

In the later stages CAPM model was identified with mean-variance with two more

assumptions added in Markowitz’s assumptions. CAPM is seen with vast meaning of the

practical application for estimating the cost of capital for evaluating performance of managing

the portfolio. The main assumption of the CAPM is considered among the investors as attaining

the target point on effective frontier at which the return will be capitalized on for the same level

of risk. The assumptions also hold the consideration for the investors in lending and borrowing

unlimited sum of money at a risk-free rate of return. It needs to be also seen that the nominal

risk-free rate of return can be collected through buying stability and government T-Bills. In

general, the capital markets are often identified to be in equilibrium and the initial investment is

prices as per the risk level. This model also assumes perfect market with no additional taxes,

transaction costs and inflation. The changes pertaining to adjustment in inflation and inflation

rate are not fully anticipated (Hoyt and Liebenberg 2015).

These investments can be absolutely divisible and understood in case there are barriers

for preventing the investors from selling or buying of fractional shares of asset or portfolio. The

calculation used in CAPM can be described as following:

𝐸(𝑅! ) = 𝑅! + 𝛽! (𝑅! − 𝑅! )

where:“𝐸 𝑅!

𝑖𝑠 𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑅𝑒𝑡𝑢𝑟𝑛 𝑐𝑜𝑚𝑝𝑢𝑡𝑒𝑑 𝑎𝑐𝑐𝑜𝑟𝑑𝑖𝑛𝑔 𝑡𝑜 𝐶𝐴𝑃𝑀”

“𝑅! 𝑖𝑠 𝑅𝑖𝑠𝑘𝑙𝑒𝑠𝑠 𝑅𝑎𝑡𝑒 𝑜𝑓 𝑅𝑒𝑡𝑢𝑟𝑛”

“𝛽! 𝑖𝑠 𝐵𝑒𝑡𝑎 (Systematic risks)”

8BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS “𝑅! 𝑖𝑠 𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑚𝑎𝑟𝑘𝑒𝑡 𝑟𝑒𝑡𝑢𝑟𝑛”

The initial consideration is taken into consideration with riskless return in this formula.

This is taken into consideration as per 10- year UK government bond rate required for

calculating the expected return in the portfolio stock and individual stock. The next aspect of the

formula considered Beta which is identified as systematic risk or can be understood as the

response of stock for marketing the investment risk. Beta is considered as the measure of value

pertaining to the systematic risk in compare to the market in general. This value is seen to be

conducive comparison of market risk of the stock with other stock (Alviniussen and Jankensgard

2015).

The application of this model is depicted to begin with building the optimal portfolio with

minimum risk and also checking the reliability of the principles associated to diversification.

Lastly, the portfolio selection is also considered with portfolio model as per the CAPM and other

supportive materials (De Dreu and Bikker 2017).

2.3 Value at Risk (VAR)

The computation of VAR is based on largest value for the decrease for a certain period

with consideration of a specific degree of confidence. Value at risk is a statistic that measures

and quantifies the level of financial risk within a firm, portfolio or position over a specific time

frame. The use of Non-parametric VAR is regardless of the type of distribution. The knowledge

and the initial value W0 along with the final value of the portfolio is seen as W. The

representation of this equation is identified with W0(1+R) and R. This is further considered with

the return earned by the investors. It needs to be further see that the expected return and volatility

of R is seen to be expressed as per μ and σ. As VAR is measured with the greatest loss measured

for a certain confidence the formula becomes viable with the formula W*=W0(1+R*). VAR

modelling determines the potential for loss in the entity being assessed and the probability of

INVESTORS “𝑅! 𝑖𝑠 𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑚𝑎𝑟𝑘𝑒𝑡 𝑟𝑒𝑡𝑢𝑟𝑛”

The initial consideration is taken into consideration with riskless return in this formula.

This is taken into consideration as per 10- year UK government bond rate required for

calculating the expected return in the portfolio stock and individual stock. The next aspect of the

formula considered Beta which is identified as systematic risk or can be understood as the

response of stock for marketing the investment risk. Beta is considered as the measure of value

pertaining to the systematic risk in compare to the market in general. This value is seen to be

conducive comparison of market risk of the stock with other stock (Alviniussen and Jankensgard

2015).

The application of this model is depicted to begin with building the optimal portfolio with

minimum risk and also checking the reliability of the principles associated to diversification.

Lastly, the portfolio selection is also considered with portfolio model as per the CAPM and other

supportive materials (De Dreu and Bikker 2017).

2.3 Value at Risk (VAR)

The computation of VAR is based on largest value for the decrease for a certain period

with consideration of a specific degree of confidence. Value at risk is a statistic that measures

and quantifies the level of financial risk within a firm, portfolio or position over a specific time

frame. The use of Non-parametric VAR is regardless of the type of distribution. The knowledge

and the initial value W0 along with the final value of the portfolio is seen as W. The

representation of this equation is identified with W0(1+R) and R. This is further considered with

the return earned by the investors. It needs to be further see that the expected return and volatility

of R is seen to be expressed as per μ and σ. As VAR is measured with the greatest loss measured

for a certain confidence the formula becomes viable with the formula W*=W0(1+R*). VAR

modelling determines the potential for loss in the entity being assessed and the probability of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

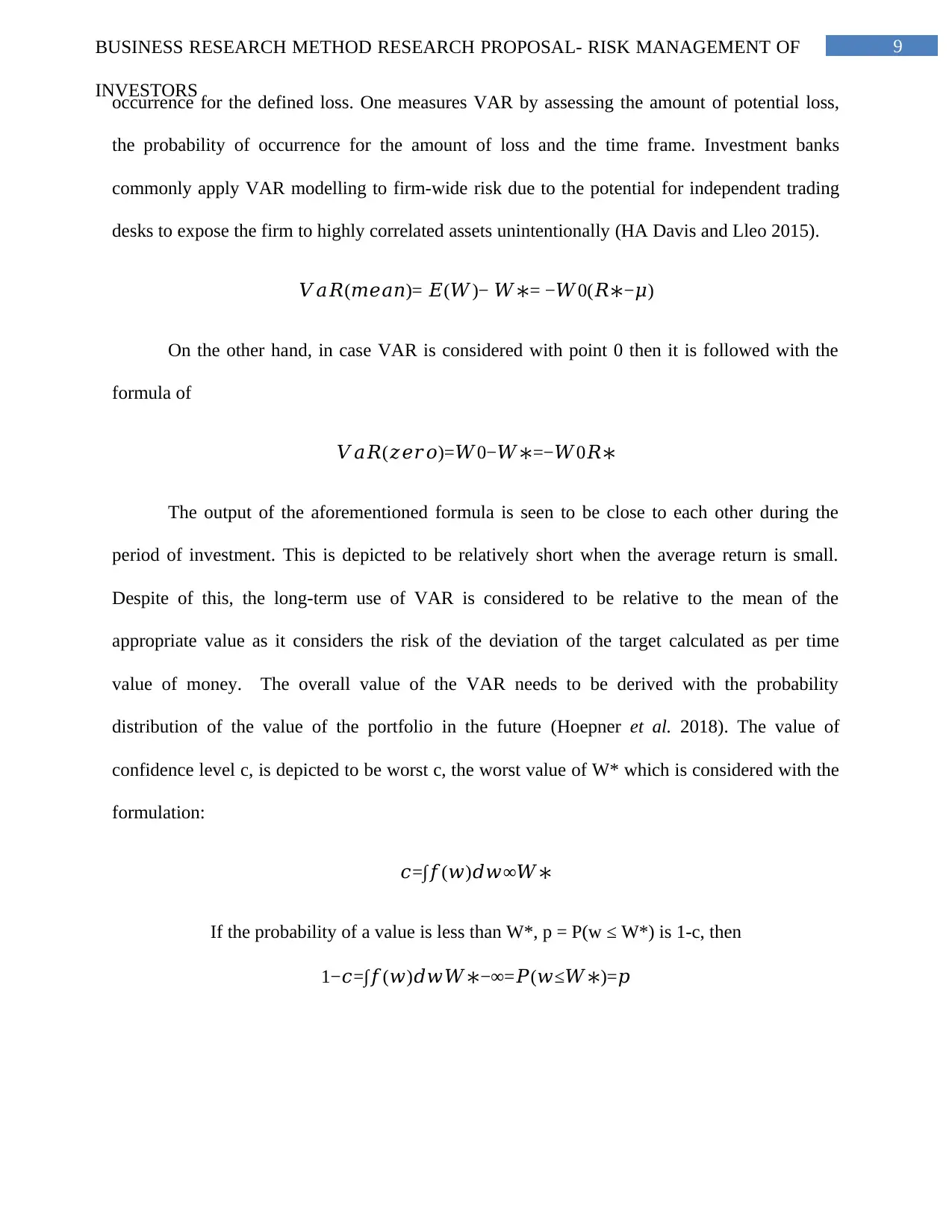

occurrence for the defined loss. One measures VAR by assessing the amount of potential loss,

the probability of occurrence for the amount of loss and the time frame. Investment banks

commonly apply VAR modelling to firm-wide risk due to the potential for independent trading

desks to expose the firm to highly correlated assets unintentionally (HA Davis and Lleo 2015).

𝑉𝑎𝑅(𝑚𝑒𝑎𝑛)= 𝐸(𝑊)− 𝑊∗= −𝑊0(𝑅∗−𝜇)

On the other hand, in case VAR is considered with point 0 then it is followed with the

formula of

𝑉𝑎𝑅(𝑧𝑒𝑟𝑜)=𝑊0−𝑊∗=−𝑊0𝑅∗

The output of the aforementioned formula is seen to be close to each other during the

period of investment. This is depicted to be relatively short when the average return is small.

Despite of this, the long-term use of VAR is considered to be relative to the mean of the

appropriate value as it considers the risk of the deviation of the target calculated as per time

value of money. The overall value of the VAR needs to be derived with the probability

distribution of the value of the portfolio in the future (Hoepner et al. 2018). The value of

confidence level c, is depicted to be worst c, the worst value of W* which is considered with the

formulation:

𝑐=∫𝑓(𝑤)𝑑𝑤∞𝑊∗

If the probability of a value is less than W*, p = P(w ≤ W*) is 1-c, then

1−𝑐=∫𝑓(𝑤)𝑑𝑤𝑊∗−∞=𝑃(𝑤≤𝑊∗)=𝑝

INVESTORS

occurrence for the defined loss. One measures VAR by assessing the amount of potential loss,

the probability of occurrence for the amount of loss and the time frame. Investment banks

commonly apply VAR modelling to firm-wide risk due to the potential for independent trading

desks to expose the firm to highly correlated assets unintentionally (HA Davis and Lleo 2015).

𝑉𝑎𝑅(𝑚𝑒𝑎𝑛)= 𝐸(𝑊)− 𝑊∗= −𝑊0(𝑅∗−𝜇)

On the other hand, in case VAR is considered with point 0 then it is followed with the

formula of

𝑉𝑎𝑅(𝑧𝑒𝑟𝑜)=𝑊0−𝑊∗=−𝑊0𝑅∗

The output of the aforementioned formula is seen to be close to each other during the

period of investment. This is depicted to be relatively short when the average return is small.

Despite of this, the long-term use of VAR is considered to be relative to the mean of the

appropriate value as it considers the risk of the deviation of the target calculated as per time

value of money. The overall value of the VAR needs to be derived with the probability

distribution of the value of the portfolio in the future (Hoepner et al. 2018). The value of

confidence level c, is depicted to be worst c, the worst value of W* which is considered with the

formulation:

𝑐=∫𝑓(𝑤)𝑑𝑤∞𝑊∗

If the probability of a value is less than W*, p = P(w ≤ W*) is 1-c, then

1−𝑐=∫𝑓(𝑤)𝑑𝑤𝑊∗−∞=𝑃(𝑤≤𝑊∗)=𝑝

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

3.0 Research Methodology

3.1 Research Approach

The research will be conducted with the use of exploratory research which will identify

the problem of identifying the best portfolio setting and way to manage the risk of portfolio for

investors in the Emirates Airline. The research will contribute to identify portfolio risk

management for investors in the Emirates Airlines using the different types of approach like

secondary research process. The process of research will be considered in five stages. This

relates to research ideation, research design, collection of data, process of publication and

analysing the data. It is important to understand the research process will be formulated with the

identification of the main methods which are available for the risk management process. Some of

the various types of thee other process of the risk management has been further able to show that

the methods of the risk management process will be only based on the information available in

the secondary sources (Evans et al. 2016).

3.2 Data Collection and Analysis

The process of collection of data will be taken into account with consideration of

secondary source of information. The different types of the secondary information will include

the value of the returns of the portfolio available in the websites such as Yahoo Finance and

Bloomberg and annual report of the company. The information available for return of portfolio

from these sources will be conducive in for application of the risk identification and risk

mitigation strategy pertaining to the use of CAPM technique and VAR. The information

collected from the annual report of the company will be helpful in the consideration of the

different types of the information which are associated to the financial health of the company. It

needs to be also seen that such information will be used by the investors in knowing about the

various types of risk management process by identification of the available information such as

INVESTORS

3.0 Research Methodology

3.1 Research Approach

The research will be conducted with the use of exploratory research which will identify

the problem of identifying the best portfolio setting and way to manage the risk of portfolio for

investors in the Emirates Airline. The research will contribute to identify portfolio risk

management for investors in the Emirates Airlines using the different types of approach like

secondary research process. The process of research will be considered in five stages. This

relates to research ideation, research design, collection of data, process of publication and

analysing the data. It is important to understand the research process will be formulated with the

identification of the main methods which are available for the risk management process. Some of

the various types of thee other process of the risk management has been further able to show that

the methods of the risk management process will be only based on the information available in

the secondary sources (Evans et al. 2016).

3.2 Data Collection and Analysis

The process of collection of data will be taken into account with consideration of

secondary source of information. The different types of the secondary information will include

the value of the returns of the portfolio available in the websites such as Yahoo Finance and

Bloomberg and annual report of the company. The information available for return of portfolio

from these sources will be conducive in for application of the risk identification and risk

mitigation strategy pertaining to the use of CAPM technique and VAR. The information

collected from the annual report of the company will be helpful in the consideration of the

different types of the information which are associated to the financial health of the company. It

needs to be also seen that such information will be used by the investors in knowing about the

various types of risk management process by identification of the available information such as

11BUSINESS RESEARCH METHOD RESEARCH PROPOSAL- RISK MANAGEMENT OF

INVESTORS

liquidity position of the company and the various types of the information such as leverage and

efficiency ratio (Bolton, Wang and Yang 2015).

The method of data collection as per the websites such as Yahoo Finance and Bloomberg

has been conducive in highlighting the various types of the important information which are

depicted to be based on monthly returns of the stock. The information such as UAE 10-year bond

yield or the risk-free market rate will be collected from the website Cbonds website.

3.3 Method of Analysis

The important method of the analysis for the data needs will be identified as per

quantitative research technique. The method of analysis will be also inferred as per the use of

CAPM and VAR. The CAPM will be identified with mean-variance with two more assumptions

added in Markowitz’s assumptions. CAPM will be seen with vast meaning of the practical

application for estimating the cost of capital for evaluating performance of managing the

portfolio. The main assumption of the CAPM will be considered among the investors for

attaining the target point on effective frontier at which the return will be capitalized on for the

same level of risk (Paquin, Gauthier and Morin 2016).

3.4 Data Analysis

The construction of the CAPM will be focused on the basic assumptions with the

consideration of portfolio diversification and required rate of return. The CAPM will be

considered with Test of stability with the use of Stability of Beta Coefficients. The measurement

portfolio effectiveness be further seen to be based on the measurement of the beta stability. This

will be able to conclude whether the beta of the individual stock is table in nature and can be

used for the purpose of predicting future risk. CAPM is seen to be effective as per structuring of

investment portfolio and estimating the cost of capital. The results pertaining to the CAPM will

be considered with evaluating the risk of portfolio through slope of SML. This technique will

INVESTORS

liquidity position of the company and the various types of the information such as leverage and

efficiency ratio (Bolton, Wang and Yang 2015).

The method of data collection as per the websites such as Yahoo Finance and Bloomberg

has been conducive in highlighting the various types of the important information which are

depicted to be based on monthly returns of the stock. The information such as UAE 10-year bond

yield or the risk-free market rate will be collected from the website Cbonds website.

3.3 Method of Analysis

The important method of the analysis for the data needs will be identified as per

quantitative research technique. The method of analysis will be also inferred as per the use of

CAPM and VAR. The CAPM will be identified with mean-variance with two more assumptions

added in Markowitz’s assumptions. CAPM will be seen with vast meaning of the practical

application for estimating the cost of capital for evaluating performance of managing the

portfolio. The main assumption of the CAPM will be considered among the investors for

attaining the target point on effective frontier at which the return will be capitalized on for the

same level of risk (Paquin, Gauthier and Morin 2016).

3.4 Data Analysis

The construction of the CAPM will be focused on the basic assumptions with the

consideration of portfolio diversification and required rate of return. The CAPM will be

considered with Test of stability with the use of Stability of Beta Coefficients. The measurement

portfolio effectiveness be further seen to be based on the measurement of the beta stability. This

will be able to conclude whether the beta of the individual stock is table in nature and can be

used for the purpose of predicting future risk. CAPM is seen to be effective as per structuring of

investment portfolio and estimating the cost of capital. The results pertaining to the CAPM will

be considered with evaluating the risk of portfolio through slope of SML. This technique will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.