MGT723 Research Project: Data Collection and Analysis Report - 2XXX

VerifiedAdded on 2021/06/18

|7

|1807

|128

Report

AI Summary

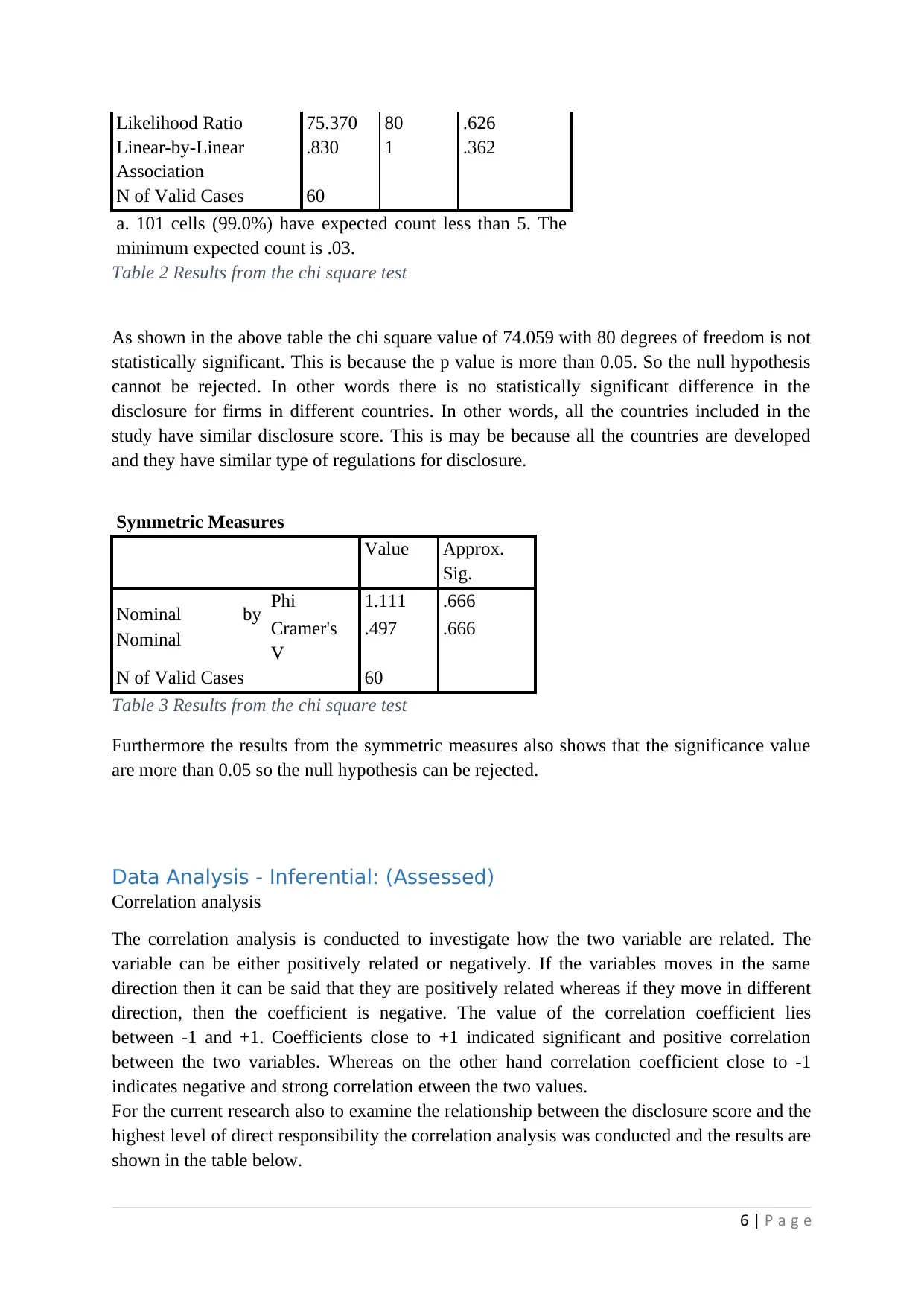

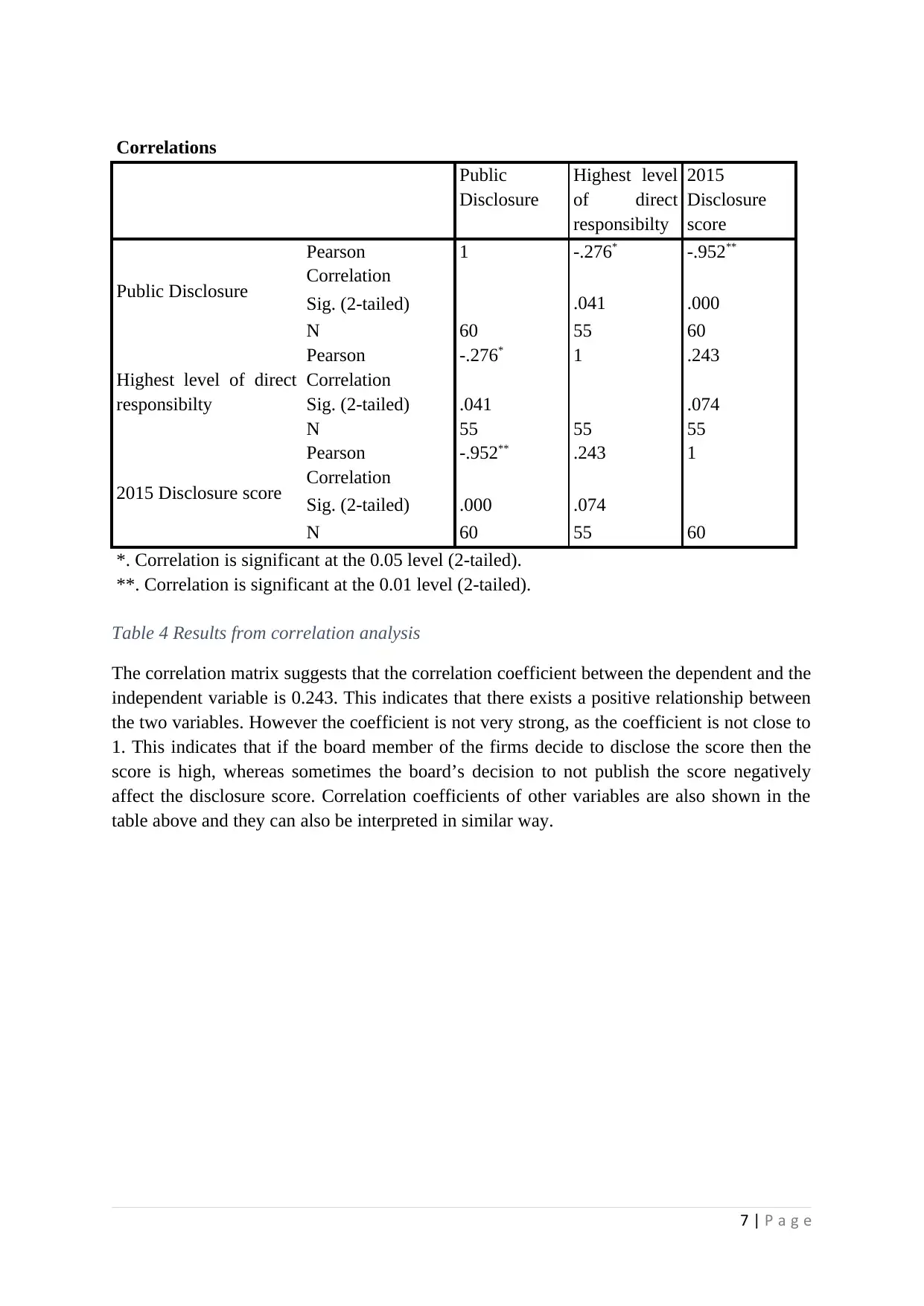

This report presents the data collection and analysis for a research project (MGT723) examining the relationship between board effectiveness and voluntary carbon disclosure. The study utilizes secondary data from 60 firms across different countries and industries, employing random sampling to ensure generalizability. The data underwent cleaning and processing, including handling missing values. The report details the descriptive statistics of the disclosure score, showing measures of central tendency and distribution. It also includes descriptive statistics for categorical variables such as country, public disclosure, and the highest level of direct responsibility. Inferential analysis involves chi-square tests to examine differences in disclosure scores across countries and correlation analysis to investigate the relationship between the disclosure score and the highest level of direct responsibility. The results indicate no statistically significant difference in disclosure scores across countries, and a positive, but not strong, correlation between disclosure score and board responsibility. The report concludes with an interpretation of the findings and implications for further research.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.