Finance Assignment: Reserves, Dividends, and Asset Impairment

VerifiedAdded on 2023/04/03

|5

|1643

|60

Homework Assignment

AI Summary

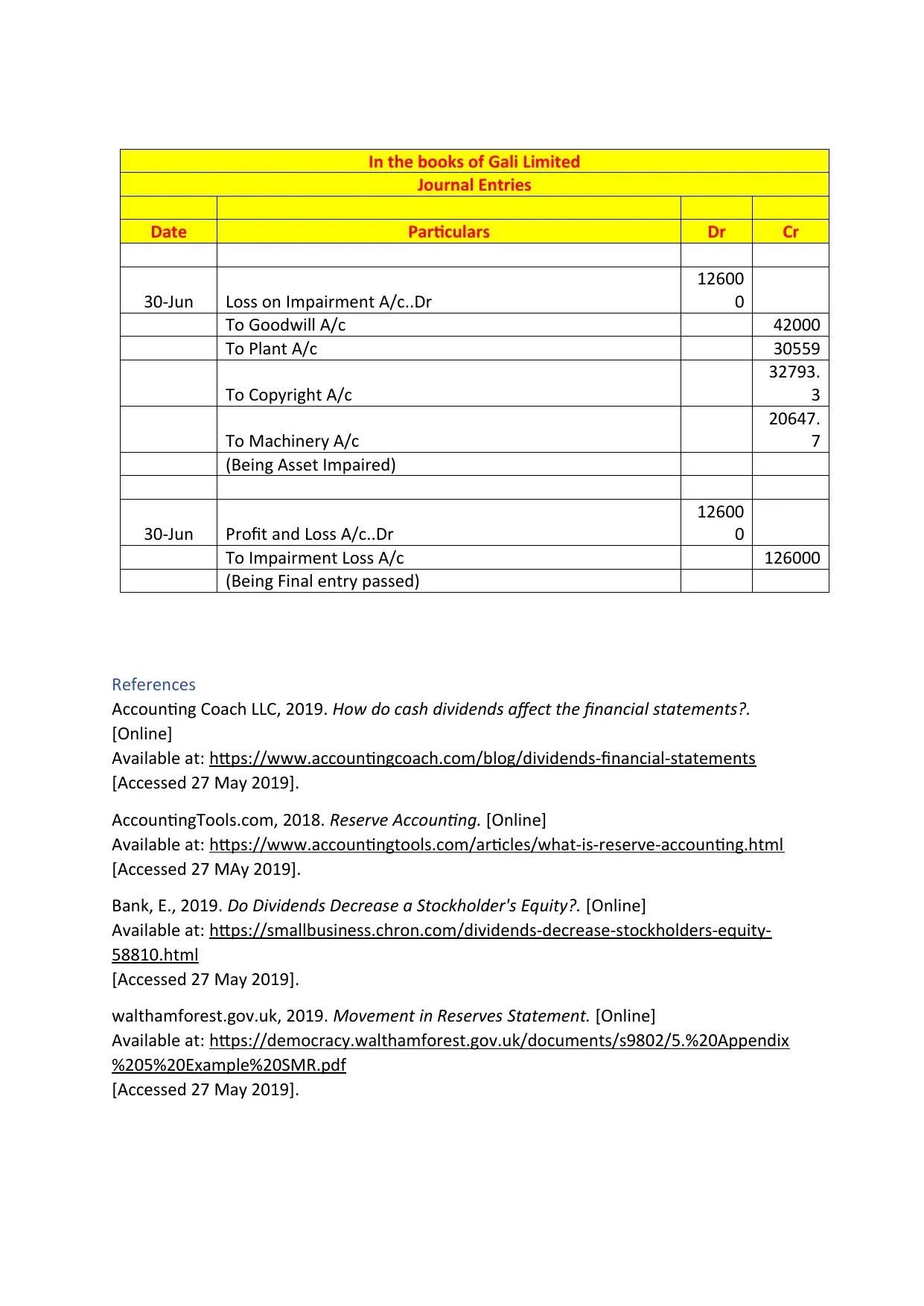

This assignment delves into the nature of reserves and their accounting treatment, including the allocation of funds for specific purposes and the process of debiting and crediting reserve accounts. It then explores the concept of dividends, examining their impact on financial statements, the different types of dividends, and the accounting entries associated with their distribution. The assignment also covers the accounting standard AASB 136, focusing on the impairment of assets. It provides a detailed case study involving Gali Ltd, calculating impairment losses, determining recoverable amounts, and preparing the necessary journal entries to reflect the impairment of various assets, including goodwill, plant, copyright, and machinery. The assignment uses examples, charts, and references to explain the concepts.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.