Taxation Law: Australian Resident and Overseas Income Taxation

VerifiedAdded on 2020/03/07

|13

|2242

|192

Report

AI Summary

This report delves into Australian taxation law, examining the tax implications for residents and non-residents, specifically addressing scenarios of individuals working overseas and self-employed professionals. The report analyzes relevant legislation, including the Income Tax Assessment Act 1936, and taxation rulings like IT 2650, to determine residency status and assessable income. It discusses cases such as F.C. of T. v. Jenkins, F.C. of T. v. Applegate, and Henderson v. Henderson to clarify tax liabilities on overseas employment income and income from professional services. The report also explores the application of accrual basis accounting for tax purposes, considering the timing of income recognition and the impact of recoverable debts on assessable income. The conclusion summarizes the tax treatment of the income, emphasizing the importance of understanding the relevant legislation and case law for accurate tax assessment.

Running head: TAXATION LAW

Taxation Law

Name of Student:

Name of University:

Author’s Note:

Taxation Law

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:......................................................................................................................2

Issues:..........................................................................................................................................2

Legislation:..................................................................................................................................2

Application:.................................................................................................................................2

Answer 2:.........................................................................................................................................5

Issues:..........................................................................................................................................5

Legislation:..................................................................................................................................5

Application:.................................................................................................................................5

Conclusion:......................................................................................................................................7

Reference List:.................................................................................................................................8

Table of Contents

Answer to question 1:......................................................................................................................2

Issues:..........................................................................................................................................2

Legislation:..................................................................................................................................2

Application:.................................................................................................................................2

Answer 2:.........................................................................................................................................5

Issues:..........................................................................................................................................5

Legislation:..................................................................................................................................5

Application:.................................................................................................................................5

Conclusion:......................................................................................................................................7

Reference List:.................................................................................................................................8

2TAXATION LAW

Answer to question 1:

Issues:

The issue which is discussed below depends on the evaluation of the effects of tax for the

wages or the salary which were derived by a resident of Australia who is working overseas and

for taxation purposes, has to leave the country.

Legislation:

a. F.C. of T. v. Jenkins 82 ATC 4098

b. F.C. of T. v. Applegate (1979) 9 ATR 899

c. Henderson v. Henderson [1965] 1 All E.R.179

d. Subsection 6 (1) of income tax assessment act 1936

e. Taxation rulings of IT 2650

Application:

This particular study considers the tax treatment of the salary which have been

ascertained by Can Robyn from the Indian Subcontinent in the form of an employment overseas

in order to work as an arranger for the University of Calcutta. The requirements for working as a

co-ordinator were lengthy, because Can Robyn desired to work for so long as there would be the

existence of the course in the University of Calcutta. According to the taxation rulings of IT

2650 the guidelines aim to be laid for ascertaining whether a particular person who leaves the

country Australia, to reside overseas temporarily due to work assignments ceases to remain an

Australian resident due to the reason of income tax during their stay outside the Country of

Australia. 1

1 Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-1762.

Answer to question 1:

Issues:

The issue which is discussed below depends on the evaluation of the effects of tax for the

wages or the salary which were derived by a resident of Australia who is working overseas and

for taxation purposes, has to leave the country.

Legislation:

a. F.C. of T. v. Jenkins 82 ATC 4098

b. F.C. of T. v. Applegate (1979) 9 ATR 899

c. Henderson v. Henderson [1965] 1 All E.R.179

d. Subsection 6 (1) of income tax assessment act 1936

e. Taxation rulings of IT 2650

Application:

This particular study considers the tax treatment of the salary which have been

ascertained by Can Robyn from the Indian Subcontinent in the form of an employment overseas

in order to work as an arranger for the University of Calcutta. The requirements for working as a

co-ordinator were lengthy, because Can Robyn desired to work for so long as there would be the

existence of the course in the University of Calcutta. According to the taxation rulings of IT

2650 the guidelines aim to be laid for ascertaining whether a particular person who leaves the

country Australia, to reside overseas temporarily due to work assignments ceases to remain an

Australian resident due to the reason of income tax during their stay outside the Country of

Australia. 1

1 Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-1762.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

In accordance with the subsection 6 (1) of income tax assessment act 1936 individuals

having domicile in Australia as given by the commissioner remains satisfied by their abode being

outside of the country Australia2. According to the statement under subsection 6 (1) an

individual residing in Australia, for more than half of the entire year of income will be

considered as a resident of Australia unless there is contentment within the commissioner that the

individual does not intend to stay in Australia for a permanent period of time.

Regarding the subsection 6 (1) of the ITAA 1936 it can be stated that Can Robyn would

be considered as a resident of Australia as she has stayed in Australia for not less than half of the

entire year of income before leaving the country3. Evidently, a flat was under the ownership of

Can Robyn, and it was not abandoned by her. There is a possibility that the flat owned by Can

Robyn was on mortgage and the amount of mortgage was paid from the income of employment

which was received in the bank account in Australia.

According to the statement in Henderson v. Henderson [1965] 1 All E.R.179 the own

origin of a person’s domicile is maintained unless the particular individual acquires their own

choice of domicile in a different state by the law operations4. From the current study it can be

2 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016. Oxford University

Press, 2016.

3 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

4 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

In accordance with the subsection 6 (1) of income tax assessment act 1936 individuals

having domicile in Australia as given by the commissioner remains satisfied by their abode being

outside of the country Australia2. According to the statement under subsection 6 (1) an

individual residing in Australia, for more than half of the entire year of income will be

considered as a resident of Australia unless there is contentment within the commissioner that the

individual does not intend to stay in Australia for a permanent period of time.

Regarding the subsection 6 (1) of the ITAA 1936 it can be stated that Can Robyn would

be considered as a resident of Australia as she has stayed in Australia for not less than half of the

entire year of income before leaving the country3. Evidently, a flat was under the ownership of

Can Robyn, and it was not abandoned by her. There is a possibility that the flat owned by Can

Robyn was on mortgage and the amount of mortgage was paid from the income of employment

which was received in the bank account in Australia.

According to the statement in Henderson v. Henderson [1965] 1 All E.R.179 the own

origin of a person’s domicile is maintained unless the particular individual acquires their own

choice of domicile in a different state by the law operations4. From the current study it can be

2 Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016. Oxford University

Press, 2016.

3 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

4 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

stated that Can Robyn has kept her Melbourne flat retained, and it is her intention to return to

Australia clearly which foreseen as well as expected, as also the contingency after the end of her

employment in Calcutta University.

Based on the liability of Tax, on the segment of income which is assessable in the bank

account in Australia, the tax liability originates in the connected to the taxation ruling of IT

2650 the residence of the taxpayers must be considered after putting the rulings discussed

above5. In case the references F.C. of T. v. Applegate (1979) 9 ATR 899 the question of the

utmost importance is the residential status of an individual organisation leaving the Australian

country for the tax purpose. In general the particular individual leaving Australia permanently

would be regarded as upholding the Australian Domicile omitting the individual gets a different

place to stay based on the law operations6.

According to the present situation, Can Robyn will be considered to have kept her

Australian Citizenship due to the maintenance of her bank account in Australia such that it

becomes possible for her to pay for her mortgage flat from the remuneration amount provided to

her in her bank account in Australia. Thus, a Visa in working condition for a significant period of

time would not be thought of as sufficient evidence of attaining a new domicile for Can Robyn.

5 Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1

(2013): 3-10.

6 Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

stated that Can Robyn has kept her Melbourne flat retained, and it is her intention to return to

Australia clearly which foreseen as well as expected, as also the contingency after the end of her

employment in Calcutta University.

Based on the liability of Tax, on the segment of income which is assessable in the bank

account in Australia, the tax liability originates in the connected to the taxation ruling of IT

2650 the residence of the taxpayers must be considered after putting the rulings discussed

above5. In case the references F.C. of T. v. Applegate (1979) 9 ATR 899 the question of the

utmost importance is the residential status of an individual organisation leaving the Australian

country for the tax purpose. In general the particular individual leaving Australia permanently

would be regarded as upholding the Australian Domicile omitting the individual gets a different

place to stay based on the law operations6.

According to the present situation, Can Robyn will be considered to have kept her

Australian Citizenship due to the maintenance of her bank account in Australia such that it

becomes possible for her to pay for her mortgage flat from the remuneration amount provided to

her in her bank account in Australia. Thus, a Visa in working condition for a significant period of

time would not be thought of as sufficient evidence of attaining a new domicile for Can Robyn.

5 Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1

(2013): 3-10.

6 Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

5TAXATION LAW

Determining the consequences of tax, the salary received by Can in her bank account

would be considered as foreign employment of income. The foreign employment and its income,

can be defined as that income of a particular individual who is an Australian resident working as

an employee overseas. Any resident of Australia, is usually taxed on the basis of income which is

obtained in every quarter of the world. In connection to the present scenario, Can Robyn’s

income amount obtained from the Australian bank account belonging to her would be treated as

assessable income. It is to be understood that the a payment given in Australia can still qualify

for foreign income even if the amount is not derived by a person working outside the country

anywhere overseas. With regard to F.C. of T. v. Jenkins 82 ATC 4098 the foreign employment

obtained from the Indian subcontinent, would attract the liability of tax and is likely to comprise

a segment of the assessable income in the form of overseas employment income7.

Answer 2:

Issues:

The present issue depends on the determination of taxable income of the payer of tax

which has the personal business of the Teacher of Golf.

Legislation:

a. Barratt v. FC of T 92 ATC

b. Henderson v. FC of T (1970)

c. Taxation Rulings TR 93/11

d. Subsection 6-5 (2) and (3) of the Income Tax Assessment Act 1997

7Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue(2016).

Determining the consequences of tax, the salary received by Can in her bank account

would be considered as foreign employment of income. The foreign employment and its income,

can be defined as that income of a particular individual who is an Australian resident working as

an employee overseas. Any resident of Australia, is usually taxed on the basis of income which is

obtained in every quarter of the world. In connection to the present scenario, Can Robyn’s

income amount obtained from the Australian bank account belonging to her would be treated as

assessable income. It is to be understood that the a payment given in Australia can still qualify

for foreign income even if the amount is not derived by a person working outside the country

anywhere overseas. With regard to F.C. of T. v. Jenkins 82 ATC 4098 the foreign employment

obtained from the Indian subcontinent, would attract the liability of tax and is likely to comprise

a segment of the assessable income in the form of overseas employment income7.

Answer 2:

Issues:

The present issue depends on the determination of taxable income of the payer of tax

which has the personal business of the Teacher of Golf.

Legislation:

a. Barratt v. FC of T 92 ATC

b. Henderson v. FC of T (1970)

c. Taxation Rulings TR 93/11

d. Subsection 6-5 (2) and (3) of the Income Tax Assessment Act 1997

7Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue(2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

e. Subsection 25 (1)

Application:

In compliance with subsection 6-5 (2) and (3) of the Income Tax Assessment Act 1997

it is compulsory for each of the taxpayers to take account of the income which is taxable in the

gross or total income which they generate8. As mentioned in subsections 6-5 (2) and (3) an

income ascertained at the time of the income year but obtained from another income year was

thought of as a topic of speculation by the taxpayers. It is crucial for the taxpayers to apply the

suitable method of ascertaining the earnings applied in a particular year of income9. As defined

in taxation rulings of TR 93/11 it is important for each individual to apply one of the two

processes namely the earning process or receipt process of the accounting tax in order to

determine the assessable income.

Based on the TR 93/11 the fee income receipt, under the subsection 25 (1) will be

regarded as connected to the ordinary conceptions of ITAA 1936 for experts or professionals

whose income is to be assessed under the accrual basis10. As is clear from the scenario discussed,

8 Snape, John, and Jeremy De Souza. Environmental taxation law: policy, contexts and practice.

Routledge, 2016.

9 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

10 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms." Journal of International Accounting, Auditing and

e. Subsection 25 (1)

Application:

In compliance with subsection 6-5 (2) and (3) of the Income Tax Assessment Act 1997

it is compulsory for each of the taxpayers to take account of the income which is taxable in the

gross or total income which they generate8. As mentioned in subsections 6-5 (2) and (3) an

income ascertained at the time of the income year but obtained from another income year was

thought of as a topic of speculation by the taxpayers. It is crucial for the taxpayers to apply the

suitable method of ascertaining the earnings applied in a particular year of income9. As defined

in taxation rulings of TR 93/11 it is important for each individual to apply one of the two

processes namely the earning process or receipt process of the accounting tax in order to

determine the assessable income.

Based on the TR 93/11 the fee income receipt, under the subsection 25 (1) will be

regarded as connected to the ordinary conceptions of ITAA 1936 for experts or professionals

whose income is to be assessed under the accrual basis10. As is clear from the scenario discussed,

8 Snape, John, and Jeremy De Souza. Environmental taxation law: policy, contexts and practice.

Routledge, 2016.

9 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

10 Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms." Journal of International Accounting, Auditing and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

which was received by Paul, he received a free earning from the golf’s private lessons from his

clients. This gave the introduction to the concepts discussed under subsection 25 (1) of the

ITAA11. This needs to be ascertained from the current study on Paul with regard to the contract

that Paul entered. It has also been determined that the Paul was given a fee by Doreen, after

imparting five years of golf lessons. This resulted in the recoverable debt establishment in case

the professional person is not required to perform any actions before the debt is entitled to be

paid. There is the possibility of recovering the fees if the time for reimbursement has been

sanctioned.

In the case of Henderson v. FC of T (1970) assessable income in terms of accrual basis

is ascertained under the subsection 25 (1) of the ITAA where a recoverable debt is formed.

Along with this particular development, an individual who is extremely professional receives the

fee income beforehand and an arrangement has been created between the client and the

professional’s fee income, which is generated becomes connected either entirely or partially for

which the person completes the work12. From the current scenario it is evident that the derivable

Taxation 22.1 (2013): 12-25.

11 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57.1 (2017): 49-63.

12 Ross, Monique, Jarrod Walker, and John Walker. "Multinationals targeted down

under." Taxation in Australia 52.1 (2017): 22.

which was received by Paul, he received a free earning from the golf’s private lessons from his

clients. This gave the introduction to the concepts discussed under subsection 25 (1) of the

ITAA11. This needs to be ascertained from the current study on Paul with regard to the contract

that Paul entered. It has also been determined that the Paul was given a fee by Doreen, after

imparting five years of golf lessons. This resulted in the recoverable debt establishment in case

the professional person is not required to perform any actions before the debt is entitled to be

paid. There is the possibility of recovering the fees if the time for reimbursement has been

sanctioned.

In the case of Henderson v. FC of T (1970) assessable income in terms of accrual basis

is ascertained under the subsection 25 (1) of the ITAA where a recoverable debt is formed.

Along with this particular development, an individual who is extremely professional receives the

fee income beforehand and an arrangement has been created between the client and the

professional’s fee income, which is generated becomes connected either entirely or partially for

which the person completes the work12. From the current scenario it is evident that the derivable

Taxation 22.1 (2013): 12-25.

11 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57.1 (2017): 49-63.

12 Ross, Monique, Jarrod Walker, and John Walker. "Multinationals targeted down

under." Taxation in Australia 52.1 (2017): 22.

8TAXATION LAW

fee income by Paul, is thought of as a part of his assessable income will be considered at the time

of considering the determination of tax liability.

From the current study of Paul, the fee income receipt by Doreen would be considered as

a segment of assessable income. The amount of fees that Paul received would be regarded as the

assessable income. This is because, the fee receipt would be considered as assessable income for

the lesson he provided to his client13. During the time of ascertaining the assessable income

belonging to Paul, receipt of sum $6,000 and $28,000 from the lessons on Golf, would be

considered as taxable income. As in the case of Barratt v. FC of T 92 ATC the court of Australia

has also taken the statutory impediment under consideration at the beginning of the proceedings

of bad but recoverable debt14.

13 Anderson, Colin, Jennifer Dickfos, and Catherine Brown. "The Australian Taxation Office-

what role does it play in anti-phoenix activity?." INSOLVENCY LAW JOURNAL 24.2 (2016):

127-140.

14 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

fee income by Paul, is thought of as a part of his assessable income will be considered at the time

of considering the determination of tax liability.

From the current study of Paul, the fee income receipt by Doreen would be considered as

a segment of assessable income. The amount of fees that Paul received would be regarded as the

assessable income. This is because, the fee receipt would be considered as assessable income for

the lesson he provided to his client13. During the time of ascertaining the assessable income

belonging to Paul, receipt of sum $6,000 and $28,000 from the lessons on Golf, would be

considered as taxable income. As in the case of Barratt v. FC of T 92 ATC the court of Australia

has also taken the statutory impediment under consideration at the beginning of the proceedings

of bad but recoverable debt14.

13 Anderson, Colin, Jennifer Dickfos, and Catherine Brown. "The Australian Taxation Office-

what role does it play in anti-phoenix activity?." INSOLVENCY LAW JOURNAL 24.2 (2016):

127-140.

14 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

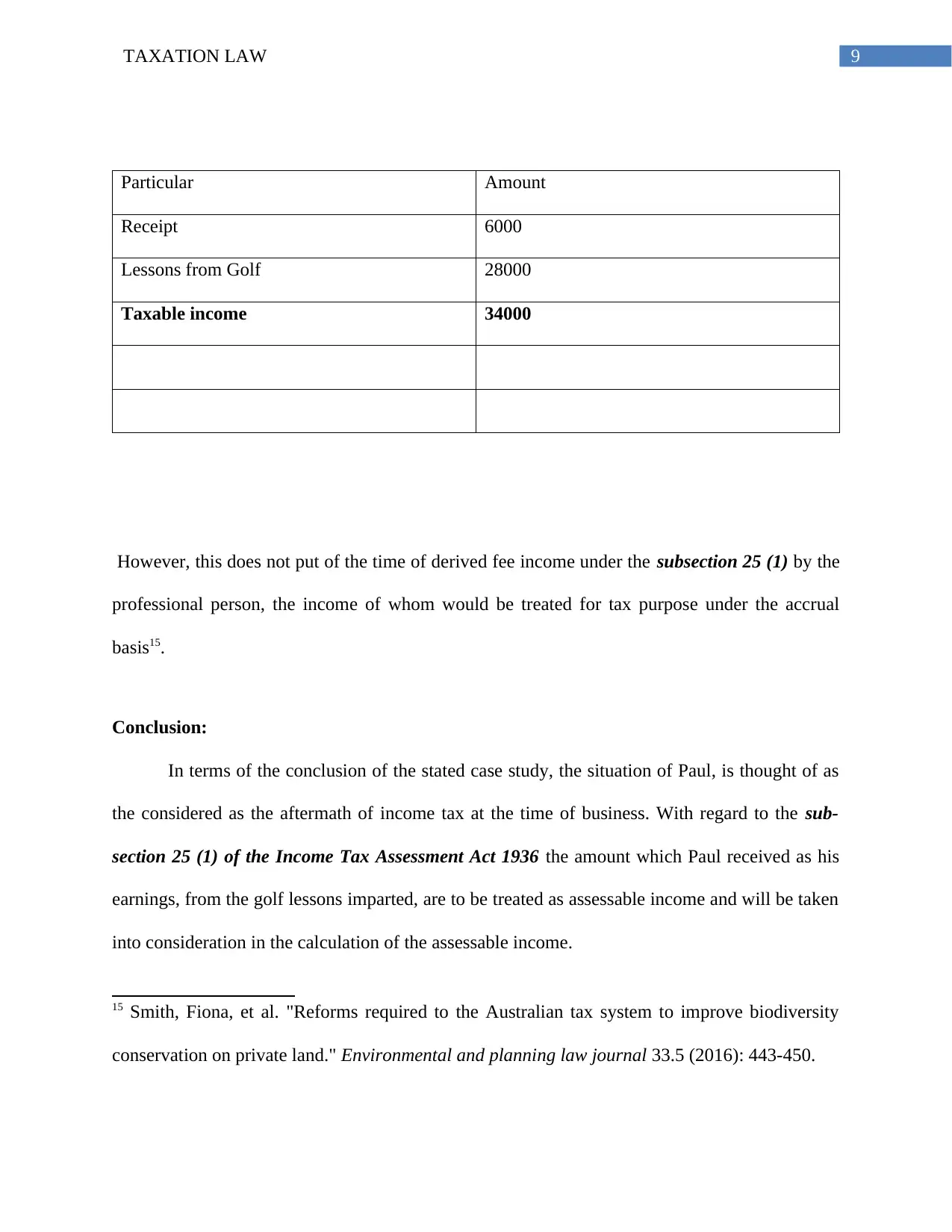

Particular Amount

Receipt 6000

Lessons from Golf 28000

Taxable income 34000

However, this does not put of the time of derived fee income under the subsection 25 (1) by the

professional person, the income of whom would be treated for tax purpose under the accrual

basis15.

Conclusion:

In terms of the conclusion of the stated case study, the situation of Paul, is thought of as

the considered as the aftermath of income tax at the time of business. With regard to the sub-

section 25 (1) of the Income Tax Assessment Act 1936 the amount which Paul received as his

earnings, from the golf lessons imparted, are to be treated as assessable income and will be taken

into consideration in the calculation of the assessable income.

15 Smith, Fiona, et al. "Reforms required to the Australian tax system to improve biodiversity

conservation on private land." Environmental and planning law journal 33.5 (2016): 443-450.

Particular Amount

Receipt 6000

Lessons from Golf 28000

Taxable income 34000

However, this does not put of the time of derived fee income under the subsection 25 (1) by the

professional person, the income of whom would be treated for tax purpose under the accrual

basis15.

Conclusion:

In terms of the conclusion of the stated case study, the situation of Paul, is thought of as

the considered as the aftermath of income tax at the time of business. With regard to the sub-

section 25 (1) of the Income Tax Assessment Act 1936 the amount which Paul received as his

earnings, from the golf lessons imparted, are to be treated as assessable income and will be taken

into consideration in the calculation of the assessable income.

15 Smith, Fiona, et al. "Reforms required to the Australian tax system to improve biodiversity

conservation on private land." Environmental and planning law journal 33.5 (2016): 443-450.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Anderson, Colin, Jennifer Dickfos, and Catherine Brown. "The Australian Taxation Office-what

role does it play in anti-phoenix activity?." INSOLVENCY LAW JOURNAL 24.2 (2016): 127-

140.

Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue(2016).

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor,

The 37.6 (2017): 18.

Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1

(2013): 3-10.

Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57.1 (2017): 49-63.

Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-1762.

ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

Reference List:

Anderson, Colin, Jennifer Dickfos, and Catherine Brown. "The Australian Taxation Office-what

role does it play in anti-phoenix activity?." INSOLVENCY LAW JOURNAL 24.2 (2016): 127-

140.

Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue(2016).

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor,

The 37.6 (2017): 18.

Braithwaite, Valerie. "Responsive regulation and taxation: Introduction." Law & Policy 29.1

(2013): 3-10.

Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Treasury WP 1 (2015).

Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The Accounting

Review 91.1 (2015): 47-68.

Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57.1 (2017): 49-63.

Pinto, Dale. "State taxes." Australian Taxation Law. CCH Australia Limited, 2011. 1763-1762.

ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

11TAXATION LAW

Ross, Monique, Jarrod Walker, and John Walker. "Multinationals targeted down

under." Taxation in Australia 52.1 (2017): 22.

Smith, Fiona, et al. "Reforms required to the Australian tax system to improve biodiversity

conservation on private land." Environmental and planning law journal 33.5 (2016): 443-450.

Snape, John, and Jeremy De Souza. Environmental taxation law: policy, contexts and practice.

Routledge, 2016.

Tan, Lin Mei, Valerie Braithwaite, and Monika Reinhart. "Why do small business taxpayers stay

with their practitioners? Trust, competence and aggressive advice." International Small Business

Journal 34.3 (2016): 329-344.

Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms." Journal of International Accounting, Auditing and

Taxation 22.1 (2013): 12-25.

Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

Ross, Monique, Jarrod Walker, and John Walker. "Multinationals targeted down

under." Taxation in Australia 52.1 (2017): 22.

Smith, Fiona, et al. "Reforms required to the Australian tax system to improve biodiversity

conservation on private land." Environmental and planning law journal 33.5 (2016): 443-450.

Snape, John, and Jeremy De Souza. Environmental taxation law: policy, contexts and practice.

Routledge, 2016.

Tan, Lin Mei, Valerie Braithwaite, and Monika Reinhart. "Why do small business taxpayers stay

with their practitioners? Trust, competence and aggressive advice." International Small Business

Journal 34.3 (2016): 329-344.

Taylor, Grantley, and Grant Richardson. "The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms." Journal of International Accounting, Auditing and

Taxation 22.1 (2013): 12-25.

Vann, Richard J. "Hybrid Entities in Australia: Resource Capital Fund III LP Case." (2016).

Woellner, R. H., et al. Australian Taxation Law Select: Legislation and Commentary 2016.

Oxford University Press, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.