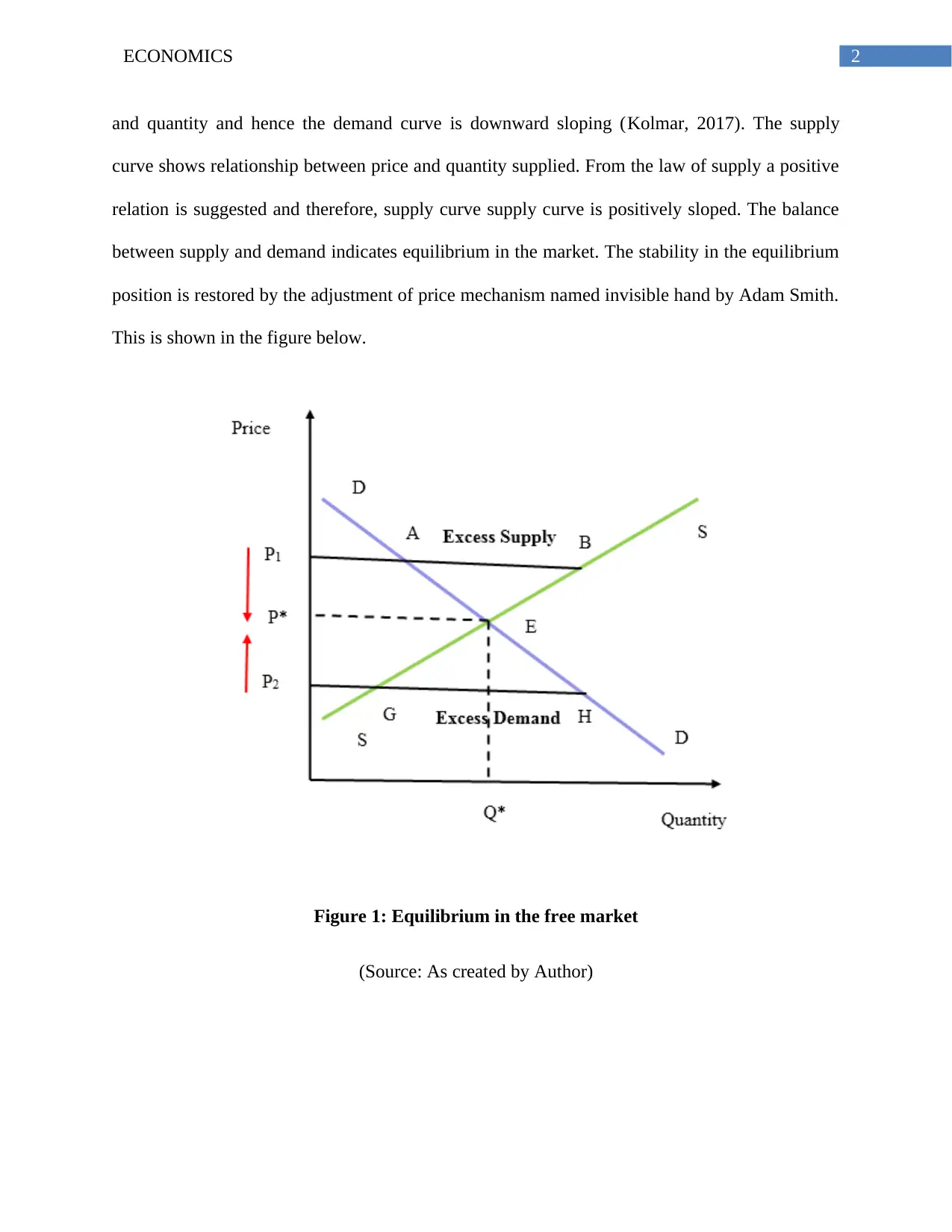

Economics: Market Analysis, Equilibrium, and Resource Allocation

VerifiedAdded on 2020/04/29

|7

|1342

|416

Essay

AI Summary

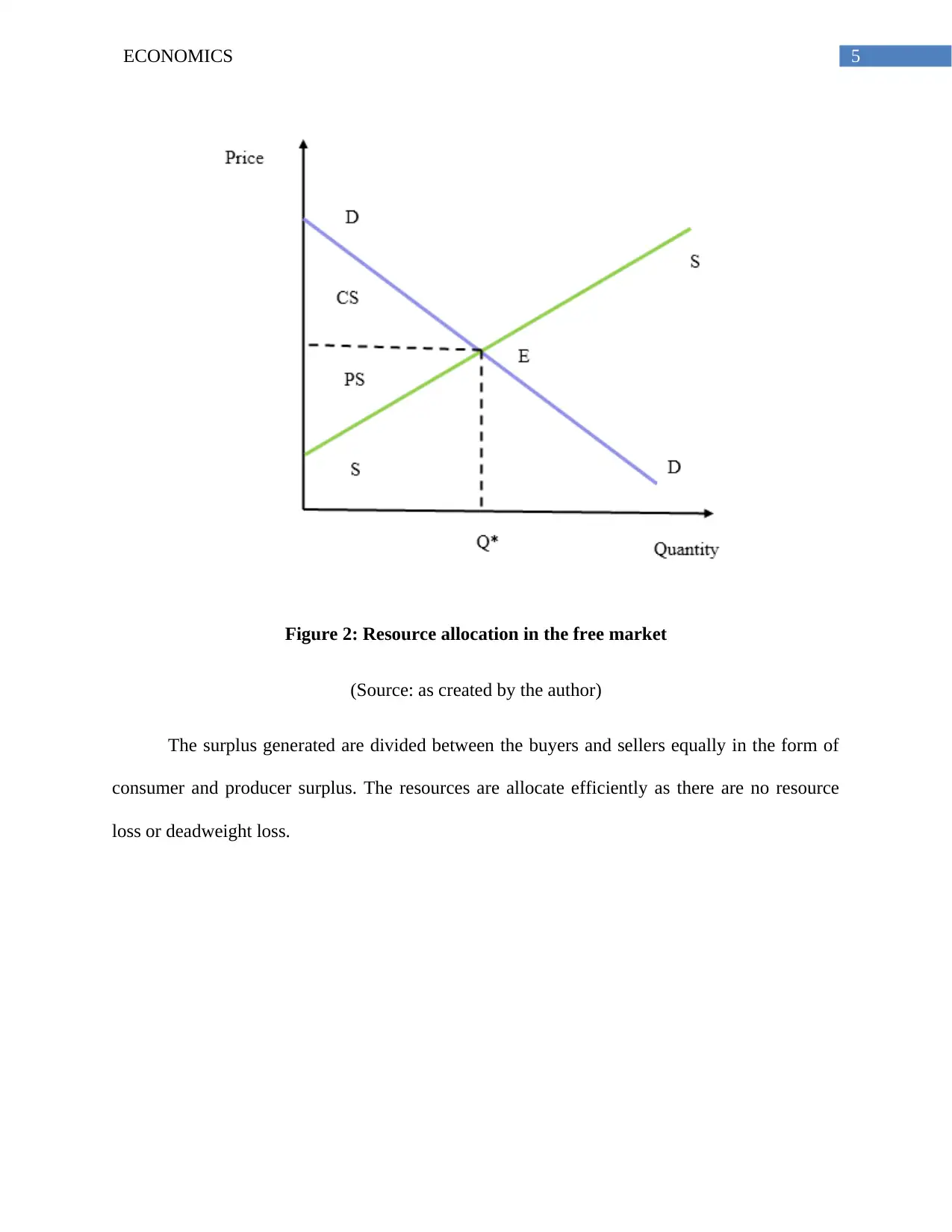

This economics assignment provides an overview of market dynamics, focusing on the concepts of demand, supply, and equilibrium within a free market context. The assignment explains how the interaction of buyers and sellers determines market prices and quantities, illustrating these principles with a graphical representation of the equilibrium point. It discusses the law of demand and supply, the factors influencing them, and how the price mechanism allocates resources efficiently. The assignment further explores the concepts of consumer and producer surplus, highlighting how they are generated in a free market. It also examines the role of price signals in resource allocation, addressing the questions of what to produce, how to produce, and for whom to produce, thereby demonstrating the efficient functioning of the market. The assignment concludes by emphasizing the role of the market in maximizing welfare for both consumers and producers.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.