University Marketing Project: Restaurant Investment vs. Development

VerifiedAdded on 2020/05/01

|15

|3470

|115

Project

AI Summary

This project report, prepared for marketing students Mark and Paul, evaluates two investment opportunities: a restaurant and a new business development. The report analyzes financial figures, including sales, labor, and cash budgets, to determine the more profitable investment. It begins with an introduction and a discussion of the nature and scope of investments. The report then delves into the specifics of the restaurant investment, outlining expenses such as machinery, furniture, and operating costs. Sales, labor, and cash budgets are presented and analyzed to forecast financial performance. The report compares this investment with the new business development opportunity, although details of the second option aren't provided in the provided text. Various financial tools are employed to assess each project's potential profitability and risk. The conclusion aims to identify the superior investment opportunity and explain the rationale behind the decision. The report also includes references.

Running Head: Accounting for business

1

Project Report: Accounting for business

1

Project Report: Accounting for business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Accounting for business

2

Executive summary

Marketing student of the university, Mark and Paul wants to start their own start up

and want investment from the investors so that the business could be start by them smoothly.

This report has been prepared for them to analyze that which project is better in order to

make more profits and invest into the project. Mark and Paul have come up with two ideas

one is investment into the business of restaurant and other one is to invest into the new

business development. Through this report, it has been tried to evaluate that which

opportunity is investment is better and why it is better. Before it, the nature of the investment

has also been concerned. For this report, various financial tools have been used.

2

Executive summary

Marketing student of the university, Mark and Paul wants to start their own start up

and want investment from the investors so that the business could be start by them smoothly.

This report has been prepared for them to analyze that which project is better in order to

make more profits and invest into the project. Mark and Paul have come up with two ideas

one is investment into the business of restaurant and other one is to invest into the new

business development. Through this report, it has been tried to evaluate that which

opportunity is investment is better and why it is better. Before it, the nature of the investment

has also been concerned. For this report, various financial tools have been used.

Running Head: Accounting for business

3

Contents

Introduction.......................................................................................................................4

Nature and scope of investment........................................................................................4

Restaurant purchase and expenses....................................................................................4

Labor budget.................................................................................................................7

Cash budget..................................................................................................................8

Overview and analysis of budgets................................................................................9

Practical issues of investment.......................................................................................9

New business development...............................................................................................9

Comparison.....................................................................................................................10

Conclusion:.....................................................................................................................10

References.......................................................................................................................11

Appendix.........................................................................................................................12

3

Contents

Introduction.......................................................................................................................4

Nature and scope of investment........................................................................................4

Restaurant purchase and expenses....................................................................................4

Labor budget.................................................................................................................7

Cash budget..................................................................................................................8

Overview and analysis of budgets................................................................................9

Practical issues of investment.......................................................................................9

New business development...............................................................................................9

Comparison.....................................................................................................................10

Conclusion:.....................................................................................................................10

References.......................................................................................................................11

Appendix.........................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Accounting for business

4

Introduction:

Mark and Paul, two marketing students want to start their own start-up. They both

present two investment opportunity in front of the investors in which they could invest. As

they both are the student of marketing and wondering that which investment opportunity

would offer them more profitability and which opportunity would be better to attract more

investors to invest into the company. Mark and Paul have explained both the opportunities

and all the financial figures related to both the investment project.

Now in this report, the financial figures of the proposals have been organized to

evaluate and conclude a better result. Mark and Paul have come up with two ideas one is

investment into the business of restaurant and other one is to invest into the new business

development. Through this report, it has been tried to evaluate that which opportunity is

investment is better and why it is better. Before it, the nature of the investment has also been

concerned. For this report, various financial tools have been used.

Nature and scope of investment:

Investments are recognized as a key financial term. This is a process in which an

individual, company or society put some efforts and money to get back more money in

return. In financial terms, individuals or the groups invest their savings into the financial

market to increase the total worth of the invested amount. Investment is of numerous types.

An investor could invest into the financial securities according to the requirement such as for

short term investment, corporate securities and treasury bonds are good option whereas for

long term investment, share and debentures are good option. Investment nature is quite

complex (Gitman and Zutter, 2012). It is quite flexible, it is not required that the investment

would always offer the high return to the company. Investment is a process which provides

the various opportunities to the investors on the basis of risk and return factor.

Restaurant purchase and expenses:

Mark and Paul have come up with two ideas one is investment into the business of

restaurant and other one is to invest into the new business development. In first investment

proposal, both of them have explained that if the Mark and Paul would invest into this

opportunity than the following expenses and income would be got by the company (Lafond

and Roychowdhury, 2008). Both the students are not aware about the financial figures and

4

Introduction:

Mark and Paul, two marketing students want to start their own start-up. They both

present two investment opportunity in front of the investors in which they could invest. As

they both are the student of marketing and wondering that which investment opportunity

would offer them more profitability and which opportunity would be better to attract more

investors to invest into the company. Mark and Paul have explained both the opportunities

and all the financial figures related to both the investment project.

Now in this report, the financial figures of the proposals have been organized to

evaluate and conclude a better result. Mark and Paul have come up with two ideas one is

investment into the business of restaurant and other one is to invest into the new business

development. Through this report, it has been tried to evaluate that which opportunity is

investment is better and why it is better. Before it, the nature of the investment has also been

concerned. For this report, various financial tools have been used.

Nature and scope of investment:

Investments are recognized as a key financial term. This is a process in which an

individual, company or society put some efforts and money to get back more money in

return. In financial terms, individuals or the groups invest their savings into the financial

market to increase the total worth of the invested amount. Investment is of numerous types.

An investor could invest into the financial securities according to the requirement such as for

short term investment, corporate securities and treasury bonds are good option whereas for

long term investment, share and debentures are good option. Investment nature is quite

complex (Gitman and Zutter, 2012). It is quite flexible, it is not required that the investment

would always offer the high return to the company. Investment is a process which provides

the various opportunities to the investors on the basis of risk and return factor.

Restaurant purchase and expenses:

Mark and Paul have come up with two ideas one is investment into the business of

restaurant and other one is to invest into the new business development. In first investment

proposal, both of them have explained that if the Mark and Paul would invest into this

opportunity than the following expenses and income would be got by the company (Lafond

and Roychowdhury, 2008). Both the students are not aware about the financial figures and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Accounting for business

5

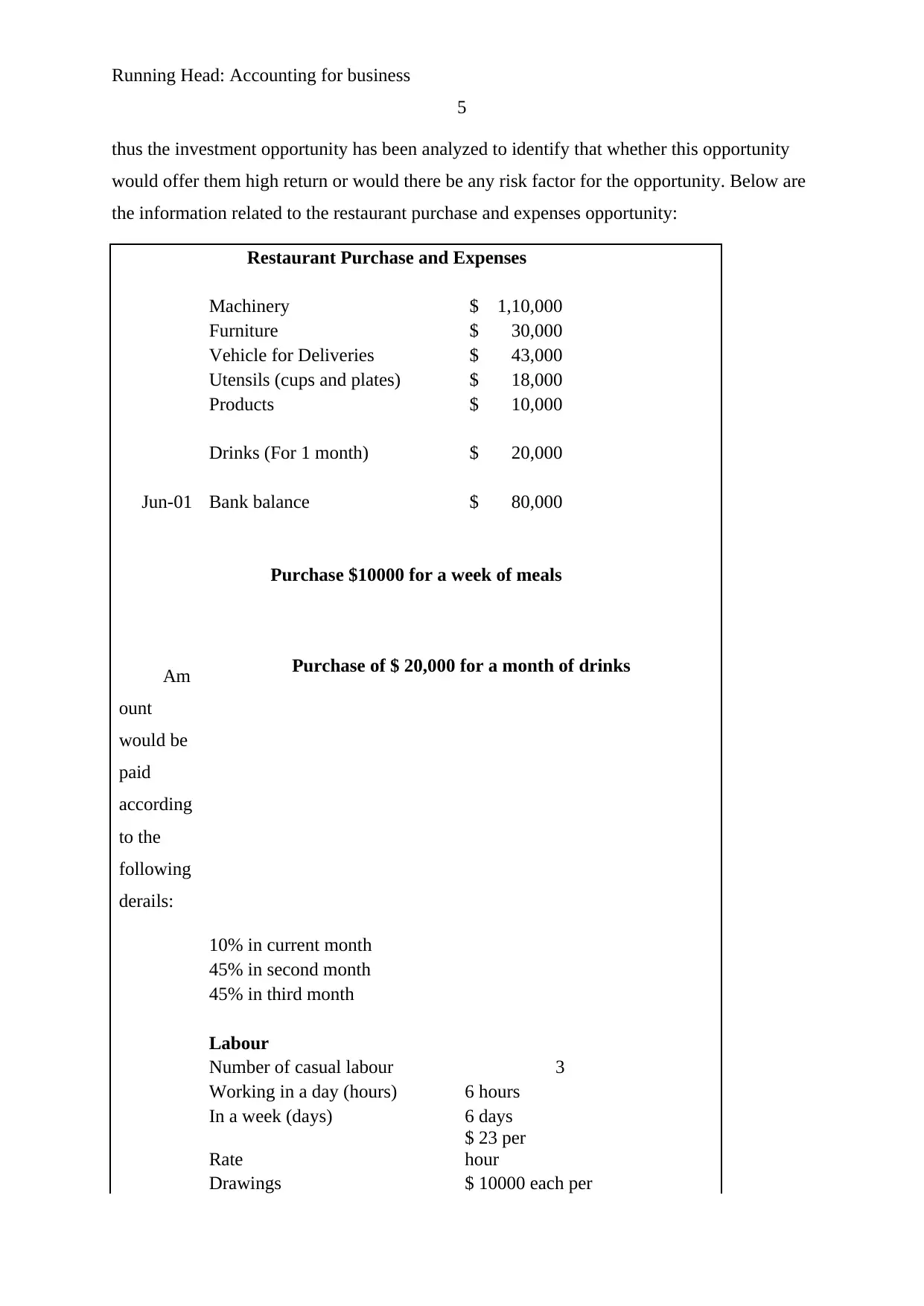

thus the investment opportunity has been analyzed to identify that whether this opportunity

would offer them high return or would there be any risk factor for the opportunity. Below are

the information related to the restaurant purchase and expenses opportunity:

Restaurant Purchase and Expenses

Machinery $ 1,10,000

Furniture $ 30,000

Vehicle for Deliveries $ 43,000

Utensils (cups and plates) $ 18,000

Products $ 10,000

Drinks (For 1 month) $ 20,000

Jun-01 Bank balance $ 80,000

Purchase $10000 for a week of meals

Purchase of $ 20,000 for a month of drinks

Am

ount

would be

paid

according

to the

following

derails:

10% in current month

45% in second month

45% in third month

Labour

Number of casual labour 3

Working in a day (hours) 6 hours

In a week (days) 6 days

Rate

$ 23 per

hour

Drawings $ 10000 each per

5

thus the investment opportunity has been analyzed to identify that whether this opportunity

would offer them high return or would there be any risk factor for the opportunity. Below are

the information related to the restaurant purchase and expenses opportunity:

Restaurant Purchase and Expenses

Machinery $ 1,10,000

Furniture $ 30,000

Vehicle for Deliveries $ 43,000

Utensils (cups and plates) $ 18,000

Products $ 10,000

Drinks (For 1 month) $ 20,000

Jun-01 Bank balance $ 80,000

Purchase $10000 for a week of meals

Purchase of $ 20,000 for a month of drinks

Am

ount

would be

paid

according

to the

following

derails:

10% in current month

45% in second month

45% in third month

Labour

Number of casual labour 3

Working in a day (hours) 6 hours

In a week (days) 6 days

Rate

$ 23 per

hour

Drawings $ 10000 each per

Running Head: Accounting for business

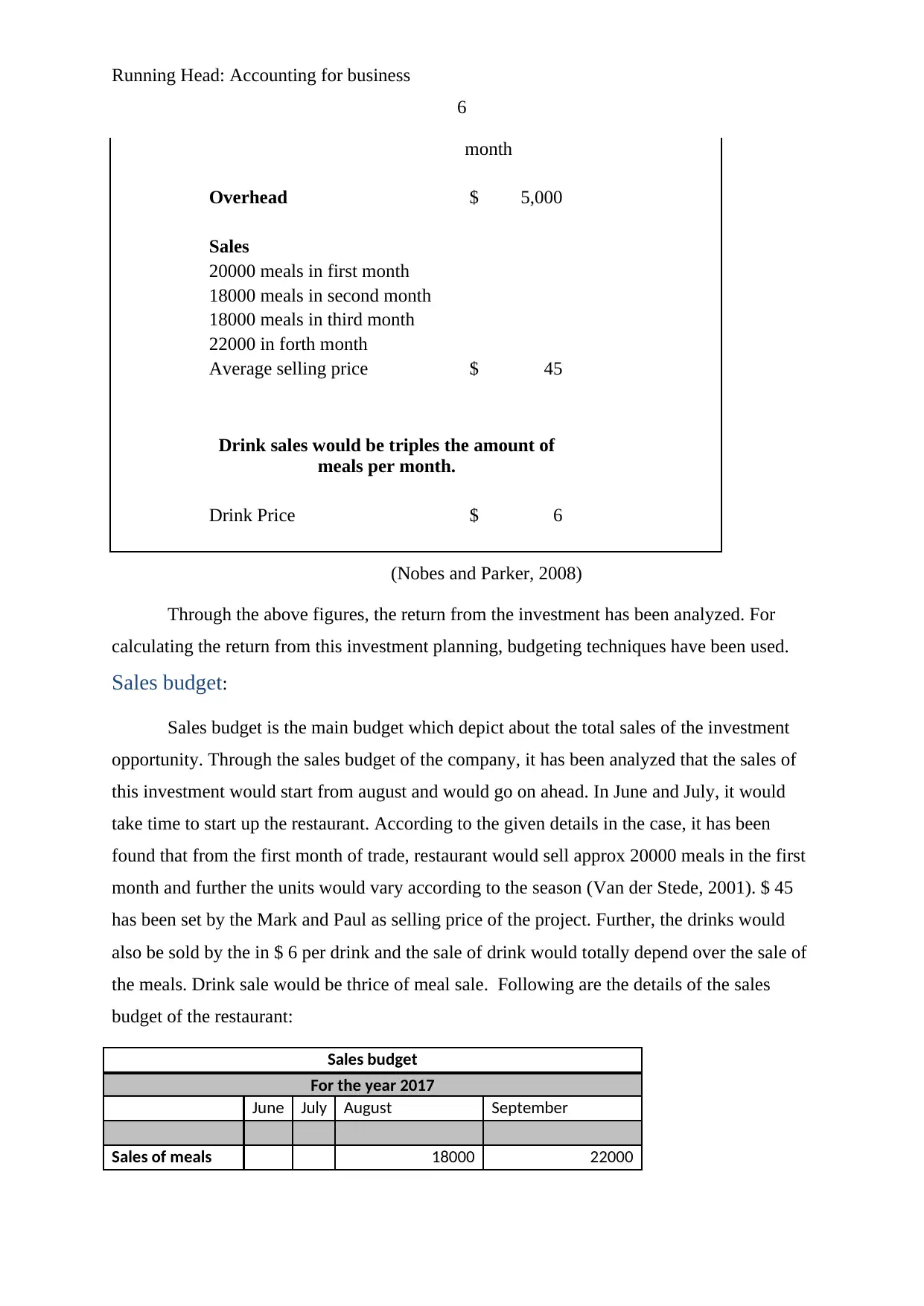

6

month

Overhead $ 5,000

Sales

20000 meals in first month

18000 meals in second month

18000 meals in third month

22000 in forth month

Average selling price $ 45

Drink sales would be triples the amount of

meals per month.

Drink Price $ 6

(Nobes and Parker, 2008)

Through the above figures, the return from the investment has been analyzed. For

calculating the return from this investment planning, budgeting techniques have been used.

Sales budget:

Sales budget is the main budget which depict about the total sales of the investment

opportunity. Through the sales budget of the company, it has been analyzed that the sales of

this investment would start from august and would go on ahead. In June and July, it would

take time to start up the restaurant. According to the given details in the case, it has been

found that from the first month of trade, restaurant would sell approx 20000 meals in the first

month and further the units would vary according to the season (Van der Stede, 2001). $ 45

has been set by the Mark and Paul as selling price of the project. Further, the drinks would

also be sold by the in $ 6 per drink and the sale of drink would totally depend over the sale of

the meals. Drink sale would be thrice of meal sale. Following are the details of the sales

budget of the restaurant:

Sales budget

For the year 2017

June July August September

Sales of meals 18000 22000

6

month

Overhead $ 5,000

Sales

20000 meals in first month

18000 meals in second month

18000 meals in third month

22000 in forth month

Average selling price $ 45

Drink sales would be triples the amount of

meals per month.

Drink Price $ 6

(Nobes and Parker, 2008)

Through the above figures, the return from the investment has been analyzed. For

calculating the return from this investment planning, budgeting techniques have been used.

Sales budget:

Sales budget is the main budget which depict about the total sales of the investment

opportunity. Through the sales budget of the company, it has been analyzed that the sales of

this investment would start from august and would go on ahead. In June and July, it would

take time to start up the restaurant. According to the given details in the case, it has been

found that from the first month of trade, restaurant would sell approx 20000 meals in the first

month and further the units would vary according to the season (Van der Stede, 2001). $ 45

has been set by the Mark and Paul as selling price of the project. Further, the drinks would

also be sold by the in $ 6 per drink and the sale of drink would totally depend over the sale of

the meals. Drink sale would be thrice of meal sale. Following are the details of the sales

budget of the restaurant:

Sales budget

For the year 2017

June July August September

Sales of meals 18000 22000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Accounting for business

7

Sales per unit $ 45 $ 45

Sales price $ 8,10,000 $ 9,90,000

Sales of drink 54000 66000

Sales per unit $ 6 $ 6

Sales price $ 3,24,000 $ 3,96,000

Total Sales $ 11,34,000 $ 13,86,000

The above calculations express that the total sales of the drink and the meal of the

company would be $ 3,24,000 and $ 3,96,000 and $ 8,10,000 and $ 9,90,000 in the month of

august and sales. Through this, it has also found that the total sales of the company would be

$ 11,34,000 in the month of august and $ 13,86,000 in the month of September.

Labor budget:

Labour budget is the main budget which depict about the total labour hours and total

labour rate of the investment opportunity. Through the labour budget of the company, it has

been analyzed that the labour of this investment would be rigid from the first day of the June.

In June and July, it would take time to start up the restaurant. According to the given details

in the case, it has been found that from the first month of start up, 3 labours would work with

the company. Following are the details of the labour budget of the restaurant:

Restaurant Purchase and Expenses

Labour budget

For the year 2017

June July August September

Number of labour 3 3 3 3

Working in a day (hours) 6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working hours 432 432 432 432

Rate 23 23 23 23

Total Labour rate 9936 9936 9936 9936

7

Sales per unit $ 45 $ 45

Sales price $ 8,10,000 $ 9,90,000

Sales of drink 54000 66000

Sales per unit $ 6 $ 6

Sales price $ 3,24,000 $ 3,96,000

Total Sales $ 11,34,000 $ 13,86,000

The above calculations express that the total sales of the drink and the meal of the

company would be $ 3,24,000 and $ 3,96,000 and $ 8,10,000 and $ 9,90,000 in the month of

august and sales. Through this, it has also found that the total sales of the company would be

$ 11,34,000 in the month of august and $ 13,86,000 in the month of September.

Labor budget:

Labour budget is the main budget which depict about the total labour hours and total

labour rate of the investment opportunity. Through the labour budget of the company, it has

been analyzed that the labour of this investment would be rigid from the first day of the June.

In June and July, it would take time to start up the restaurant. According to the given details

in the case, it has been found that from the first month of start up, 3 labours would work with

the company. Following are the details of the labour budget of the restaurant:

Restaurant Purchase and Expenses

Labour budget

For the year 2017

June July August September

Number of labour 3 3 3 3

Working in a day (hours) 6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working hours 432 432 432 432

Rate 23 23 23 23

Total Labour rate 9936 9936 9936 9936

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Accounting for business

8

The above calculations express that the total labour hour of the company would be

432 in every month. All of them would work for 6 days in a week on the payment of $ 23 per

hour. The total labour hour of the company would be $ 9936 in every month.

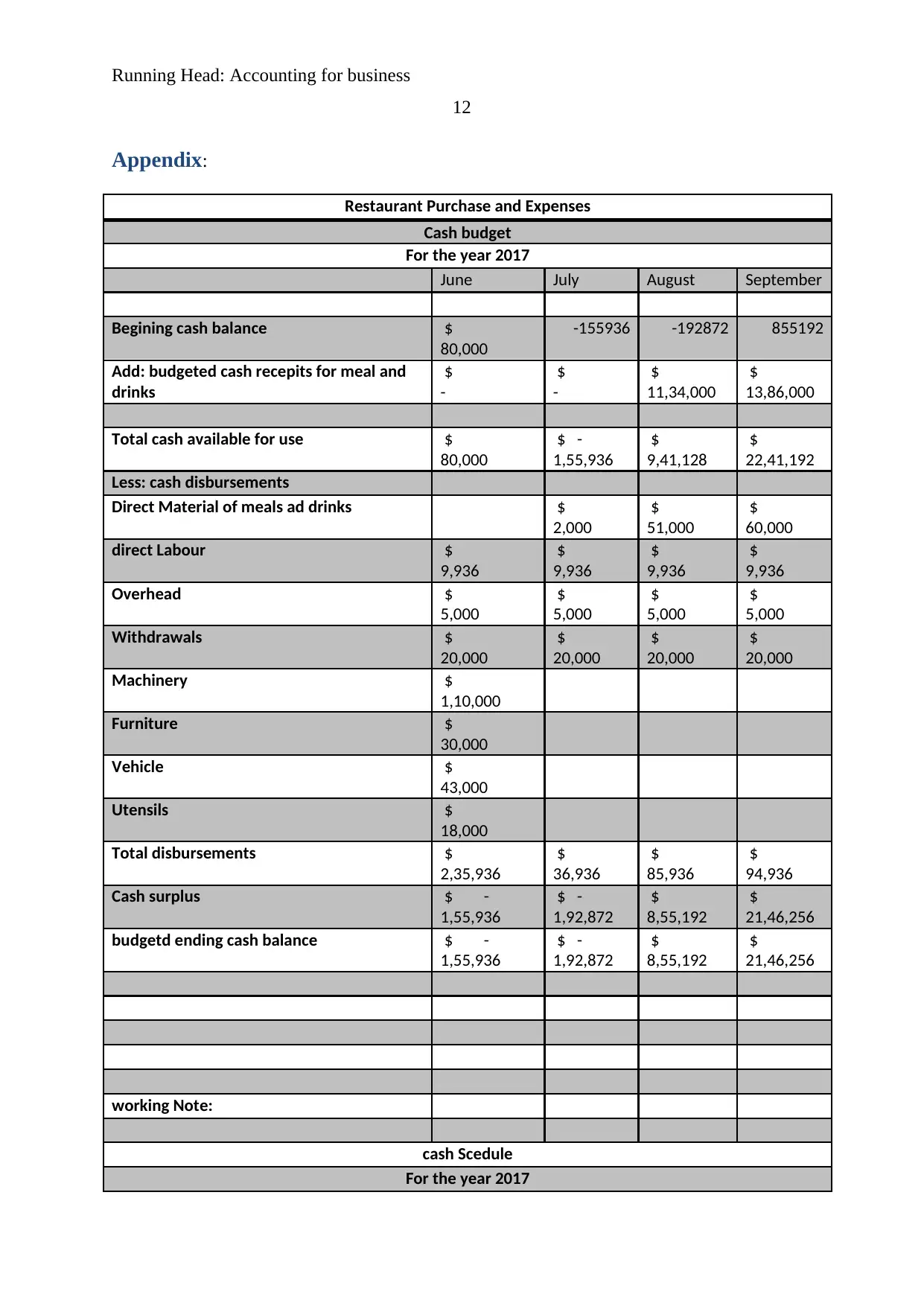

Cash budget:

Cash budget is the main budget which depict about the total cash outflow and inflow

of the investment opportunity. Through the cash budget of the company, it has been analyzed

that ho much cash outflow and cash inflow would take place from the first day of the

investment. In June and July, it would take time to start up the restaurant and thus the revenue

would not be there (Garrison et al, 2010). According to the given details in the case, it has

been found that from the first month of start up, cash outflow of the company has taken place.

Following are the details of the cash budget of the restaurant:

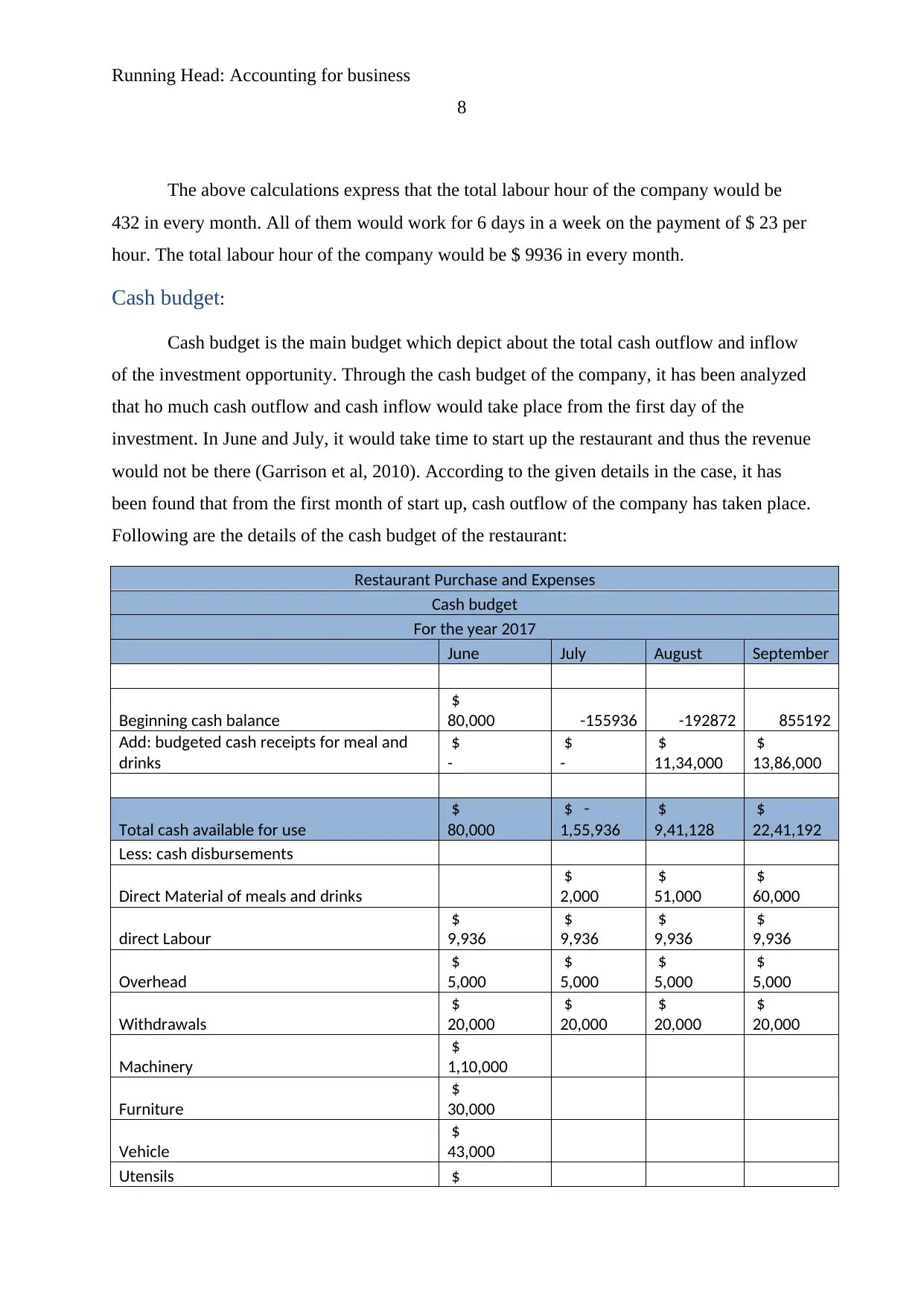

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Beginning cash balance

$

80,000 -155936 -192872 855192

Add: budgeted cash receipts for meal and

drinks

$

-

$

-

$

11,34,000

$

13,86,000

Total cash available for use

$

80,000

$ -

1,55,936

$

9,41,128

$

22,41,192

Less: cash disbursements

Direct Material of meals and drinks

$

2,000

$

51,000

$

60,000

direct Labour

$

9,936

$

9,936

$

9,936

$

9,936

Overhead

$

5,000

$

5,000

$

5,000

$

5,000

Withdrawals

$

20,000

$

20,000

$

20,000

$

20,000

Machinery

$

1,10,000

Furniture

$

30,000

Vehicle

$

43,000

Utensils $

8

The above calculations express that the total labour hour of the company would be

432 in every month. All of them would work for 6 days in a week on the payment of $ 23 per

hour. The total labour hour of the company would be $ 9936 in every month.

Cash budget:

Cash budget is the main budget which depict about the total cash outflow and inflow

of the investment opportunity. Through the cash budget of the company, it has been analyzed

that ho much cash outflow and cash inflow would take place from the first day of the

investment. In June and July, it would take time to start up the restaurant and thus the revenue

would not be there (Garrison et al, 2010). According to the given details in the case, it has

been found that from the first month of start up, cash outflow of the company has taken place.

Following are the details of the cash budget of the restaurant:

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Beginning cash balance

$

80,000 -155936 -192872 855192

Add: budgeted cash receipts for meal and

drinks

$

-

$

-

$

11,34,000

$

13,86,000

Total cash available for use

$

80,000

$ -

1,55,936

$

9,41,128

$

22,41,192

Less: cash disbursements

Direct Material of meals and drinks

$

2,000

$

51,000

$

60,000

direct Labour

$

9,936

$

9,936

$

9,936

$

9,936

Overhead

$

5,000

$

5,000

$

5,000

$

5,000

Withdrawals

$

20,000

$

20,000

$

20,000

$

20,000

Machinery

$

1,10,000

Furniture

$

30,000

Vehicle

$

43,000

Utensils $

Running Head: Accounting for business

9

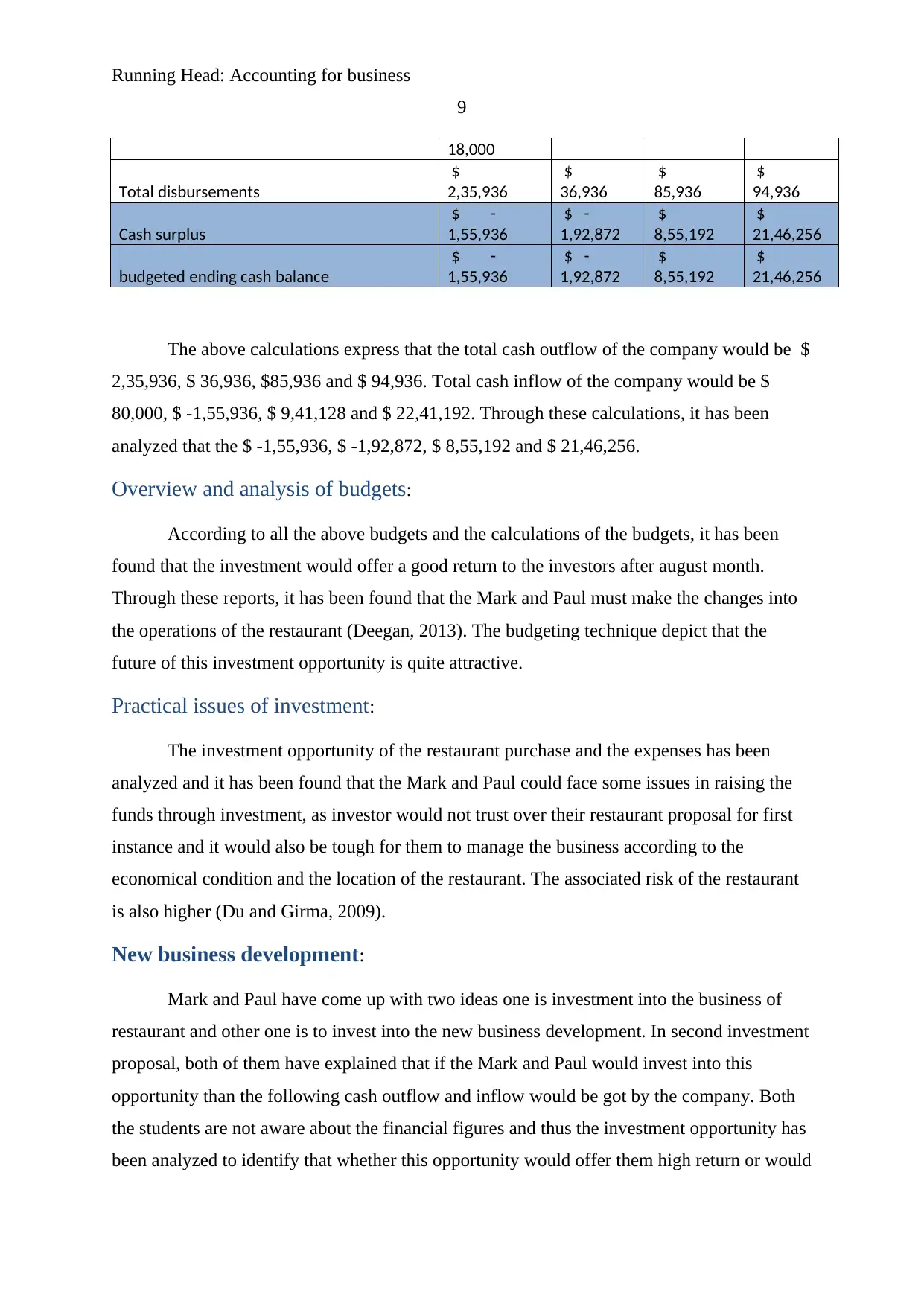

18,000

Total disbursements

$

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus

$ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

budgeted ending cash balance

$ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

The above calculations express that the total cash outflow of the company would be $

2,35,936, $ 36,936, $85,936 and $ 94,936. Total cash inflow of the company would be $

80,000, $ -1,55,936, $ 9,41,128 and $ 22,41,192. Through these calculations, it has been

analyzed that the $ -1,55,936, $ -1,92,872, $ 8,55,192 and $ 21,46,256.

Overview and analysis of budgets:

According to all the above budgets and the calculations of the budgets, it has been

found that the investment would offer a good return to the investors after august month.

Through these reports, it has been found that the Mark and Paul must make the changes into

the operations of the restaurant (Deegan, 2013). The budgeting technique depict that the

future of this investment opportunity is quite attractive.

Practical issues of investment:

The investment opportunity of the restaurant purchase and the expenses has been

analyzed and it has been found that the Mark and Paul could face some issues in raising the

funds through investment, as investor would not trust over their restaurant proposal for first

instance and it would also be tough for them to manage the business according to the

economical condition and the location of the restaurant. The associated risk of the restaurant

is also higher (Du and Girma, 2009).

New business development:

Mark and Paul have come up with two ideas one is investment into the business of

restaurant and other one is to invest into the new business development. In second investment

proposal, both of them have explained that if the Mark and Paul would invest into this

opportunity than the following cash outflow and inflow would be got by the company. Both

the students are not aware about the financial figures and thus the investment opportunity has

been analyzed to identify that whether this opportunity would offer them high return or would

9

18,000

Total disbursements

$

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus

$ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

budgeted ending cash balance

$ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

The above calculations express that the total cash outflow of the company would be $

2,35,936, $ 36,936, $85,936 and $ 94,936. Total cash inflow of the company would be $

80,000, $ -1,55,936, $ 9,41,128 and $ 22,41,192. Through these calculations, it has been

analyzed that the $ -1,55,936, $ -1,92,872, $ 8,55,192 and $ 21,46,256.

Overview and analysis of budgets:

According to all the above budgets and the calculations of the budgets, it has been

found that the investment would offer a good return to the investors after august month.

Through these reports, it has been found that the Mark and Paul must make the changes into

the operations of the restaurant (Deegan, 2013). The budgeting technique depict that the

future of this investment opportunity is quite attractive.

Practical issues of investment:

The investment opportunity of the restaurant purchase and the expenses has been

analyzed and it has been found that the Mark and Paul could face some issues in raising the

funds through investment, as investor would not trust over their restaurant proposal for first

instance and it would also be tough for them to manage the business according to the

economical condition and the location of the restaurant. The associated risk of the restaurant

is also higher (Du and Girma, 2009).

New business development:

Mark and Paul have come up with two ideas one is investment into the business of

restaurant and other one is to invest into the new business development. In second investment

proposal, both of them have explained that if the Mark and Paul would invest into this

opportunity than the following cash outflow and inflow would be got by the company. Both

the students are not aware about the financial figures and thus the investment opportunity has

been analyzed to identify that whether this opportunity would offer them high return or would

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: Accounting for business

10

there be any risk factor for the opportunity. Below are the information related to the new

business development opportunity:

Initial Cost

$ -

3,90,000

Cash Inflows

June

$

1,00,000

July

$

2,30,000

Aug

$

1,90,000

Sept

$

1,40,000

The above figures depict that the NPV of the company is $ 1,06,851.08 which depict

about the positive results. Further, it has been found that the payback period calculation

depict that the investor would get back the amount in 3.77 years and accounting rate of

return depict that 27.40% would be the average return of the company.

Comparison:

An investment opportunity is basically depends over the risk and return factor

associated with the proposal. Through comparing and analyzing both the projects, it has been

analyzed that the return from the first proposal is bit higher whereas it has also been found

that the associated risk of second proposal is bit lower. The investors must consider both

these factors and must make a better decision on the basis of this.

Conclusion:

Lastly, it has been concluded that the return from the first proposal is bit higher

whereas it has also been found that the associated risk of second proposal is bit lower. The

investors must consider both these factors and must make a better decision on the basis of

this.

10

there be any risk factor for the opportunity. Below are the information related to the new

business development opportunity:

Initial Cost

$ -

3,90,000

Cash Inflows

June

$

1,00,000

July

$

2,30,000

Aug

$

1,90,000

Sept

$

1,40,000

The above figures depict that the NPV of the company is $ 1,06,851.08 which depict

about the positive results. Further, it has been found that the payback period calculation

depict that the investor would get back the amount in 3.77 years and accounting rate of

return depict that 27.40% would be the average return of the company.

Comparison:

An investment opportunity is basically depends over the risk and return factor

associated with the proposal. Through comparing and analyzing both the projects, it has been

analyzed that the return from the first proposal is bit higher whereas it has also been found

that the associated risk of second proposal is bit lower. The investors must consider both

these factors and must make a better decision on the basis of this.

Conclusion:

Lastly, it has been concluded that the return from the first proposal is bit higher

whereas it has also been found that the associated risk of second proposal is bit lower. The

investors must consider both these factors and must make a better decision on the basis of

this.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: Accounting for business

11

References:

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Du, J. and Girma, S., 2009. Source of finance, growth and firm size: evidence from

China (No. 2009.03). Research paper/UNU-WIDER.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, (25(4), pp.79(2-793.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lafond, R. and Roychowdhury, S. 2008. Managerial ownership and accounting

conservatism. Journal of accounting research, 46(1), pp.101-135.

Nobes, C. and Parker, R.H. 2008. Comparative international accounting. Pearson Education.

Van der Stede, W.A. 2001. Measuring ‘tight budgetary control’. Management Accounting

Research, 1(2(1), pp.119-137.

11

References:

Deegan, C., 2013. Financial accounting theory. McGraw-Hill Education Australia.

Du, J. and Girma, S., 2009. Source of finance, growth and firm size: evidence from

China (No. 2009.03). Research paper/UNU-WIDER.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, (25(4), pp.79(2-793.

Gitman, L.J. and Zutter, C.J., 2012. Principles of managerial finance. Prentice Hall.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Lafond, R. and Roychowdhury, S. 2008. Managerial ownership and accounting

conservatism. Journal of accounting research, 46(1), pp.101-135.

Nobes, C. and Parker, R.H. 2008. Comparative international accounting. Pearson Education.

Van der Stede, W.A. 2001. Measuring ‘tight budgetary control’. Management Accounting

Research, 1(2(1), pp.119-137.

Running Head: Accounting for business

12

Appendix:

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Begining cash balance $

80,000

-155936 -192872 855192

Add: budgeted cash recepits for meal and

drinks

$

-

$

-

$

11,34,000

$

13,86,000

Total cash available for use $

80,000

$ -

1,55,936

$

9,41,128

$

22,41,192

Less: cash disbursements

Direct Material of meals ad drinks $

2,000

$

51,000

$

60,000

direct Labour $

9,936

$

9,936

$

9,936

$

9,936

Overhead $

5,000

$

5,000

$

5,000

$

5,000

Withdrawals $

20,000

$

20,000

$

20,000

$

20,000

Machinery $

1,10,000

Furniture $

30,000

Vehicle $

43,000

Utensils $

18,000

Total disbursements $

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus $ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

budgetd ending cash balance $ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

working Note:

cash Scedule

For the year 2017

12

Appendix:

Restaurant Purchase and Expenses

Cash budget

For the year 2017

June July August September

Begining cash balance $

80,000

-155936 -192872 855192

Add: budgeted cash recepits for meal and

drinks

$

-

$

-

$

11,34,000

$

13,86,000

Total cash available for use $

80,000

$ -

1,55,936

$

9,41,128

$

22,41,192

Less: cash disbursements

Direct Material of meals ad drinks $

2,000

$

51,000

$

60,000

direct Labour $

9,936

$

9,936

$

9,936

$

9,936

Overhead $

5,000

$

5,000

$

5,000

$

5,000

Withdrawals $

20,000

$

20,000

$

20,000

$

20,000

Machinery $

1,10,000

Furniture $

30,000

Vehicle $

43,000

Utensils $

18,000

Total disbursements $

2,35,936

$

36,936

$

85,936

$

94,936

Cash surplus $ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

budgetd ending cash balance $ -

1,55,936

$ -

1,92,872

$

8,55,192

$

21,46,256

working Note:

cash Scedule

For the year 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.