White Elephant Restaurant: Management Accounting Systems Analysis

VerifiedAdded on 2023/03/23

|13

|4800

|95

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and reporting methods, specifically in the context of the White Elephant Restaurant. It begins by defining management accounting and outlining the essential requirements of various systems, including cost accounting, job costing, process accounting, and throughput accounting. The report then discusses different methods used for management accounting reporting, such as job cost reports, budget reports, and sales and profit reports, highlighting their importance in making informed business decisions. The analysis covers the advantages and disadvantages of each method, emphasizing the need for proper implementation to achieve optimal results in cost control and business performance improvement. The document concludes by underscoring the significance of these accounting tools in helping managers track performance, formulate strategies, and ultimately enhance profitability.

INTRODUCTION

Management accounting is one of the most important domains that assist firm in

managing cost in its business. In present research work management accounting concept is

defined clearly and requirements of varied systems are explained. In middle part of the report,

profit computation is done on basis of marginal costing and absorption costing approaches and

their suitability for business is identified. Along with this, merits and demerits of different

planning tools is explained in respect to budgetary control. At end of the report, varied methods

that can be used to respond to financial problems are explained. By covering all these things in

proper manner research work is completed.

P1 Management accounting and essential requirements of different management

accounting systems

From: Budgeting officer

To General manager of White elephant restaurant

Subject: Management accounting system

Management accounting refers to the tools and methods that are used for doing costing of

product and identifying lots of facts and figures in respect to costing of products and services.

Usually, in management accounting there are number of tools and methods like variance analysis

and budgeting that can be used for cost control and analysis (Burns. and Scapens, 2000). There

are number of advantage and disadvantage of these methods and due to this reason it is very

important to use all these methods in proper manner in appropriate manner so that best rules can

be obtained in the business. Management accounting systems are widely used by all sorts of

business firms. It is the system in which in systematic manner and in specific way transactions

related to specific product are recorded. There are varied sort of management accounting systems

and essential requirement of these accounting systems are explained below. Cost accounting systems: Cost accounting system is one of the most important systems

because under this all sort of expenses related to all products that are produced by the

firm are recorded collectively. All these expenses are aggregated to arrive at amount of

overall cost that is incurred in the business. White elephant restaurant can make use of his

accounting system because it simply need to sum all relevant expenses in category of

Management accounting is one of the most important domains that assist firm in

managing cost in its business. In present research work management accounting concept is

defined clearly and requirements of varied systems are explained. In middle part of the report,

profit computation is done on basis of marginal costing and absorption costing approaches and

their suitability for business is identified. Along with this, merits and demerits of different

planning tools is explained in respect to budgetary control. At end of the report, varied methods

that can be used to respond to financial problems are explained. By covering all these things in

proper manner research work is completed.

P1 Management accounting and essential requirements of different management

accounting systems

From: Budgeting officer

To General manager of White elephant restaurant

Subject: Management accounting system

Management accounting refers to the tools and methods that are used for doing costing of

product and identifying lots of facts and figures in respect to costing of products and services.

Usually, in management accounting there are number of tools and methods like variance analysis

and budgeting that can be used for cost control and analysis (Burns. and Scapens, 2000). There

are number of advantage and disadvantage of these methods and due to this reason it is very

important to use all these methods in proper manner in appropriate manner so that best rules can

be obtained in the business. Management accounting systems are widely used by all sorts of

business firms. It is the system in which in systematic manner and in specific way transactions

related to specific product are recorded. There are varied sort of management accounting systems

and essential requirement of these accounting systems are explained below. Cost accounting systems: Cost accounting system is one of the most important systems

because under this all sort of expenses related to all products that are produced by the

firm are recorded collectively. All these expenses are aggregated to arrive at amount of

overall cost that is incurred in the business. White elephant restaurant can make use of his

accounting system because it simply need to sum all relevant expenses in category of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fixed, variable and semi variable expenses. By using this accounting system managers

can prudently make decisions. Under cost accounting systems all expenses are classified

into fixed expenses, variable expenses and semi variable expenses (Angelakis, Theriou

and Floropoulos, 2010). Fixed expense is the cost which remains stable and does not alter

during entire life of the project. It can be said that cost accounting system have due

importance for the firms because in it one can easily get segregation of expenses in

different categories. It can be observed that managers always required classification of

cost in all these categories because on basis of same they identify that to what extent

variable expenses increased in the business. Variable expenses are those expenses that

keep on fluctuating consistently in the business and never remain stable at specific point.

This reflects that there is huge difference between fixed and variable expenses in the

business. It is very important for the firm to maintain control on its expenses so that

profitability can be enhanced in the business. Cost accounting system is currently

employed by all range of enterprises in their business due to its unique and easy

implementation phase. This is the reason due to which cost accounting system is gaining

wide popularity among business firms. It can be said that there is huge importance of cost

accounting system for the business firms. Job cost system: Job costing is one of the unique methods of costing and under this for

each job or product line separately costing is done. For example there are 5 products then

in that case for each product separately costing will be done in the business (Figge and

Hahn, 2013). Under this accounting system aggregately costing of products is not done

and due to this reason this accounting system is considered better than other accounting

systems. This is because in other managers does not get an overview of product lines

separately but in case of job cost system for each product individually information is

obtained by the business firms. Thus, it can be said that there is huge importance of job

cost system for the business firms. This is because under this system management gets

report of costing of all products separately. On the basis of information obtained they

become able to identify that which of product lines is more profitable and expenses are

low. In other words it can be said that managers comes to know about products where

expenses are very high. It can be said that there is huge importance of job cost system for

the business firms. This accounting system is used in the firms that are operating

can prudently make decisions. Under cost accounting systems all expenses are classified

into fixed expenses, variable expenses and semi variable expenses (Angelakis, Theriou

and Floropoulos, 2010). Fixed expense is the cost which remains stable and does not alter

during entire life of the project. It can be said that cost accounting system have due

importance for the firms because in it one can easily get segregation of expenses in

different categories. It can be observed that managers always required classification of

cost in all these categories because on basis of same they identify that to what extent

variable expenses increased in the business. Variable expenses are those expenses that

keep on fluctuating consistently in the business and never remain stable at specific point.

This reflects that there is huge difference between fixed and variable expenses in the

business. It is very important for the firm to maintain control on its expenses so that

profitability can be enhanced in the business. Cost accounting system is currently

employed by all range of enterprises in their business due to its unique and easy

implementation phase. This is the reason due to which cost accounting system is gaining

wide popularity among business firms. It can be said that there is huge importance of cost

accounting system for the business firms. Job cost system: Job costing is one of the unique methods of costing and under this for

each job or product line separately costing is done. For example there are 5 products then

in that case for each product separately costing will be done in the business (Figge and

Hahn, 2013). Under this accounting system aggregately costing of products is not done

and due to this reason this accounting system is considered better than other accounting

systems. This is because in other managers does not get an overview of product lines

separately but in case of job cost system for each product individually information is

obtained by the business firms. Thus, it can be said that there is huge importance of job

cost system for the business firms. This is because under this system management gets

report of costing of all products separately. On the basis of information obtained they

become able to identify that which of product lines is more profitable and expenses are

low. In other words it can be said that managers comes to know about products where

expenses are very high. It can be said that there is huge importance of job cost system for

the business firms. This accounting system is used in the firms that are operating

production plant and producing multiple sorts of products in the business (Lavia López

and Hiebl, 2014). On the basis of reporting system they get an entire detail about single

product specifically and decide that on which product they need to pay due attention. It

can be said that there is huge importance of job cost system for the business firms. Process accounting system: Process costing system is one of the important system and

under this for entire process costing is done separately. It can be seen that for each

product there is specific process that is followed for production of goods at workplace. In

this process there are different stages that are performed by the business firms in order to

produce specific product. For each product production stage separately costing is done.

This is one of the important costing systems that are followed by the business firm. This

is because under this more accurately overview of costing of product is obtained (van der

Steen, 2011). In the stage of production where cost is much high can be analyzed by

performing process reengineering stage and activities that are producing high amount of

wastage can be simplified so that cost can be reduced in the business. It can be said that

process costing system is one of the most important system that is used by the business

firm’s at large scale in the workplace. In current time period there are large numbers of

firms that are operating process costing system at workplace because it has number of

advantage for the firm. Hence, it is the attractive features of the process accounting

system that make it more popular among business firms. Throughput accounting system: It is one of the common accounting systems that come

in modern category. It is the accounting system which is newly prepared by the Israeli

business man so that wastage can be detected in the business and same can be removed. It

can be said that there is huge importance of throughput accounting system for the firms

because it lead to reduction in cost in the business along with decline in wastage in the

business.

P2 Different methods use for management accounting reporting

From: Budgeting officer

To General manager of White elephant restaurant

Subject: Management accounting reporting

Reporting is the one of the major task that is performed in every business. This is because in

and Hiebl, 2014). On the basis of reporting system they get an entire detail about single

product specifically and decide that on which product they need to pay due attention. It

can be said that there is huge importance of job cost system for the business firms. Process accounting system: Process costing system is one of the important system and

under this for entire process costing is done separately. It can be seen that for each

product there is specific process that is followed for production of goods at workplace. In

this process there are different stages that are performed by the business firms in order to

produce specific product. For each product production stage separately costing is done.

This is one of the important costing systems that are followed by the business firm. This

is because under this more accurately overview of costing of product is obtained (van der

Steen, 2011). In the stage of production where cost is much high can be analyzed by

performing process reengineering stage and activities that are producing high amount of

wastage can be simplified so that cost can be reduced in the business. It can be said that

process costing system is one of the most important system that is used by the business

firm’s at large scale in the workplace. In current time period there are large numbers of

firms that are operating process costing system at workplace because it has number of

advantage for the firm. Hence, it is the attractive features of the process accounting

system that make it more popular among business firms. Throughput accounting system: It is one of the common accounting systems that come

in modern category. It is the accounting system which is newly prepared by the Israeli

business man so that wastage can be detected in the business and same can be removed. It

can be said that there is huge importance of throughput accounting system for the firms

because it lead to reduction in cost in the business along with decline in wastage in the

business.

P2 Different methods use for management accounting reporting

From: Budgeting officer

To General manager of White elephant restaurant

Subject: Management accounting reporting

Reporting is the one of the major task that is performed in every business. This is because in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports lots of facts and figures are presented that are used by the managers for making business

decisions. These facts may be related to sales and revenue that are earned in the business. On the

basis of these facts managers comes to know about area where they need to work in order to

improve performance of the business firm (Kotas, 2014). Different sort of reporting are used by

the firms in their business and same are explained below. Job cost report: Job cost report is one under for each product separately report is

generated in the business. White elephant restaurant can use this sort of report so as to get

better overview of costing of all products separately. In the job cost report there are

different product lines that are operated by the business or different orders of customized

products that are received from customers are also treated as job. It can be said that there

is huge importance of job cost report for the business firms. From this report managers

get information about different sort of variable expenses that are made in the business.

Job cost report is prepared by most of business firms because it help them in making

relevant business decisions. In large size firms usually there are job cost system and due

to this reason job cost report is prepared in the business. Time to time on monthly basis or

within every 15 days job cost report is prepared. This is done because by doing so

managers keep close track of variable expenses in the business (DRURY, 2013). On

other hand, by preparing cost control strategy on initial stage expenses are control in the

business. This lead to strict control on expenses in the business. Overall due to reduction

in expenses in the business product cost decline and due to this reason firm earn good

amount of margin in its business on per unit sold. It can be said that this sort of reporting

greatly help managers in managing efficiency in the business. Hence, it can be said that

there are multiple reasons due to which it is assumed that there is wide level of benefits

of using job cost report in the business. Budget report: Budget report is also one of the important tools of reporting because in

this report standards are clearly communicated and actual facts are recorded in alignment

to it. On this basis it is identified whether firm perform good or bad in its business. Firm

performance is considered good when it successfully beat standard and considered worst

when it failed to beat standards. It can be said that it is one of the important tool of

reporting for the firms. On basis of variance analysis that is done in budget report it is

identified that which are areas where work need to be done in the business. For example

decisions. These facts may be related to sales and revenue that are earned in the business. On the

basis of these facts managers comes to know about area where they need to work in order to

improve performance of the business firm (Kotas, 2014). Different sort of reporting are used by

the firms in their business and same are explained below. Job cost report: Job cost report is one under for each product separately report is

generated in the business. White elephant restaurant can use this sort of report so as to get

better overview of costing of all products separately. In the job cost report there are

different product lines that are operated by the business or different orders of customized

products that are received from customers are also treated as job. It can be said that there

is huge importance of job cost report for the business firms. From this report managers

get information about different sort of variable expenses that are made in the business.

Job cost report is prepared by most of business firms because it help them in making

relevant business decisions. In large size firms usually there are job cost system and due

to this reason job cost report is prepared in the business. Time to time on monthly basis or

within every 15 days job cost report is prepared. This is done because by doing so

managers keep close track of variable expenses in the business (DRURY, 2013). On

other hand, by preparing cost control strategy on initial stage expenses are control in the

business. This lead to strict control on expenses in the business. Overall due to reduction

in expenses in the business product cost decline and due to this reason firm earn good

amount of margin in its business on per unit sold. It can be said that this sort of reporting

greatly help managers in managing efficiency in the business. Hence, it can be said that

there are multiple reasons due to which it is assumed that there is wide level of benefits

of using job cost report in the business. Budget report: Budget report is also one of the important tools of reporting because in

this report standards are clearly communicated and actual facts are recorded in alignment

to it. On this basis it is identified whether firm perform good or bad in its business. Firm

performance is considered good when it successfully beat standard and considered worst

when it failed to beat standards. It can be said that it is one of the important tool of

reporting for the firms. On basis of variance analysis that is done in budget report it is

identified that which are areas where work need to be done in the business. For example

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

if variable expenses variance is negative then it can be said that variable expense is the

area where work need to be done in proper manner so that cost can be controlled in the

business. It can be said that budget report help Company in tracking its performance time

to time. There are different sort of budgets that are prepared by the firms like zero based

budgeting and incremental budgeting (Li and et.al., 2012). Both budgeting approaches

are totally different from each other. Budgeting methods does not affect budget report of

the business firms. It can be said that budget report help firms to measure their

performance in systematic way and due to this reason there is huge importance of budget

report for the firms. Sales and profit report: Sales report can be prepared by White elephant restaurant on

quarter basis and yearly basis. On basis of quarter results managers determine strategy on

which they need to work for next quarter. By doing so an attempt is made to improve

performance of business. It can be said that sales report not only help firm in measuring

its performance but it also help it in formulating business strategy so that performance

can be improved more for next time period. However, it is not necessary that firms

prepare sales report on quarter basis (Cuganesan, Dunford and Palmer, 2012). Mentioned

sort of report can be prepared on monthly basis or in every 15 days. It can be said that

there is great significance of sales report for the firms. On other hand, there is another

report which is known as profit report. Usually, sales and profit report is prepared

individually. This is because it is not necessary that if in respect to any product there is

high amount of sales then profit amount will also be high. It is possible that sales amount

will be high but profit amount may be low. Hence, managers often prefer to prepare sales

and profit report individually. There is another reason behind preparing this report and

one of them is that by obtaining profit report managers get information about level of

profit that is earned on product line which may be super normal profit or normal profit.

Managers often combine both reports and on that basis identify variable expenses due to

which low amount of profit is earned in the business. It can be said that sales and profit

report both have due advantage for the firms and both must be prepared time to time in

order to make business decisions in systematic manner in order to improve business

performance.

area where work need to be done in proper manner so that cost can be controlled in the

business. It can be said that budget report help Company in tracking its performance time

to time. There are different sort of budgets that are prepared by the firms like zero based

budgeting and incremental budgeting (Li and et.al., 2012). Both budgeting approaches

are totally different from each other. Budgeting methods does not affect budget report of

the business firms. It can be said that budget report help firms to measure their

performance in systematic way and due to this reason there is huge importance of budget

report for the firms. Sales and profit report: Sales report can be prepared by White elephant restaurant on

quarter basis and yearly basis. On basis of quarter results managers determine strategy on

which they need to work for next quarter. By doing so an attempt is made to improve

performance of business. It can be said that sales report not only help firm in measuring

its performance but it also help it in formulating business strategy so that performance

can be improved more for next time period. However, it is not necessary that firms

prepare sales report on quarter basis (Cuganesan, Dunford and Palmer, 2012). Mentioned

sort of report can be prepared on monthly basis or in every 15 days. It can be said that

there is great significance of sales report for the firms. On other hand, there is another

report which is known as profit report. Usually, sales and profit report is prepared

individually. This is because it is not necessary that if in respect to any product there is

high amount of sales then profit amount will also be high. It is possible that sales amount

will be high but profit amount may be low. Hence, managers often prefer to prepare sales

and profit report individually. There is another reason behind preparing this report and

one of them is that by obtaining profit report managers get information about level of

profit that is earned on product line which may be super normal profit or normal profit.

Managers often combine both reports and on that basis identify variable expenses due to

which low amount of profit is earned in the business. It can be said that sales and profit

report both have due advantage for the firms and both must be prepared time to time in

order to make business decisions in systematic manner in order to improve business

performance.

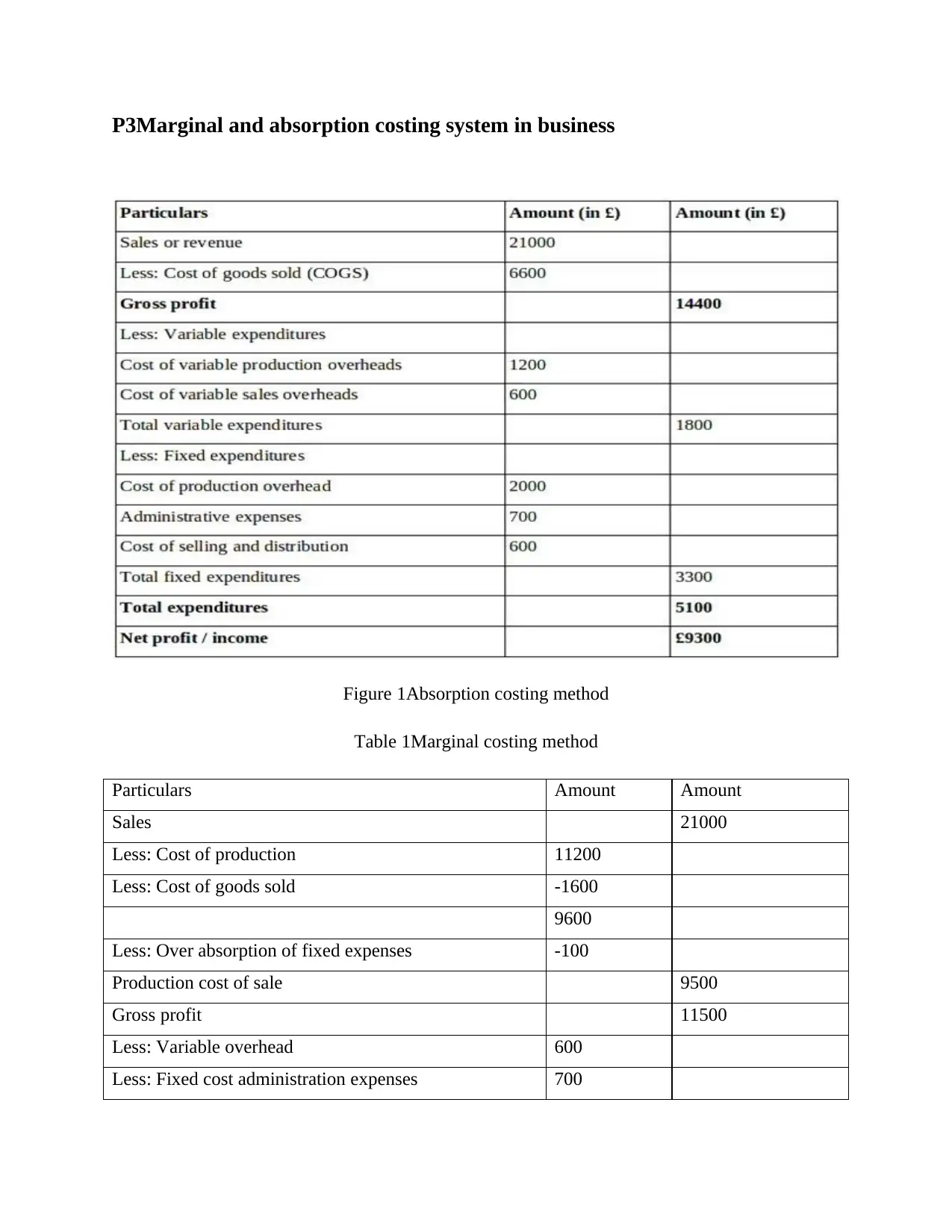

P3Marginal and absorption costing system in business

Figure 1Absorption costing method

Table 1Marginal costing method

Particulars Amount Amount

Sales 21000

Less: Cost of production 11200

Less: Cost of goods sold -1600

9600

Less: Over absorption of fixed expenses -100

Production cost of sale 9500

Gross profit 11500

Less: Variable overhead 600

Less: Fixed cost administration expenses 700

Figure 1Absorption costing method

Table 1Marginal costing method

Particulars Amount Amount

Sales 21000

Less: Cost of production 11200

Less: Cost of goods sold -1600

9600

Less: Over absorption of fixed expenses -100

Production cost of sale 9500

Gross profit 11500

Less: Variable overhead 600

Less: Fixed cost administration expenses 700

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling cost 600 1900

Net profit 9600

In cost accounting there are two approaches of profit computation which are marginal and

absorption costing. In case of marginal costing approach variable expenses are only taken in to

account which means that fixed expenses are not considered for profit computation. Opposite to

this method of costing there is another approach of profit computation under which all sort of

expenses are taken in to account which are fixed expenses, variable expenses and semi variable

expenses. It must be noted that all these expenses are different from each other and they have

heavy impact on the firm profitability. Variable expenses are those expenses that keep on

fluctuating consistently and never remain stable at specific point of time (Cadez and Guilding,

2012). Fixed expenses are equal opposite of variable expenses because in this expenses remain

unchanged. Semi variable expenses are combination of fixed and variable expenses because

same remain fixed and its some portion remains variable in nature. In case of absorption

expenses both fixed and variable expenses values are taken in to account and from sales revenue

amount these expenses amount is deducted. By doing so profit amount is calculated in the

business. It can be observed that net profit in case of marginal costing method is 9600 and value

of same in case of absorption costing method is 9300. Comparison of both values is indicating

that huge amount of profit is earned in case of marginal costing then absorption costing method.

It can be seen from table which is given above that in case of marginal costing method cost of

production, cost of goods sold, production cost of sale are taken in to account. Apart from this,

variable overhead and fixed cost administration expenses are taken in to account.

It is clear that there is gap between marginal and absorption costing method. Firms can

choose either of these methods or can choose both approaches to compute profit in the business.

It will be better to use marginal costing method in the business because variable expenses are

only made in the business to produce goods and making available services to the customers.

Hence, if only variable expense is only taken in to consideration for calculation of profit then it

cannot be considered wrong. On other hand, there is logic behind using absorption costing

method in the business. It is well known fact that in absorption costing method both fixed and

variable expenses are taken in to account (Burritt and Schaltegger, 2010). Fixed expenses are

directly not related to production of specific number of unit but same support manufacturing of

goods at workplace. Hence, it is not completely possible to not include fixed expenses in costing

Net profit 9600

In cost accounting there are two approaches of profit computation which are marginal and

absorption costing. In case of marginal costing approach variable expenses are only taken in to

account which means that fixed expenses are not considered for profit computation. Opposite to

this method of costing there is another approach of profit computation under which all sort of

expenses are taken in to account which are fixed expenses, variable expenses and semi variable

expenses. It must be noted that all these expenses are different from each other and they have

heavy impact on the firm profitability. Variable expenses are those expenses that keep on

fluctuating consistently and never remain stable at specific point of time (Cadez and Guilding,

2012). Fixed expenses are equal opposite of variable expenses because in this expenses remain

unchanged. Semi variable expenses are combination of fixed and variable expenses because

same remain fixed and its some portion remains variable in nature. In case of absorption

expenses both fixed and variable expenses values are taken in to account and from sales revenue

amount these expenses amount is deducted. By doing so profit amount is calculated in the

business. It can be observed that net profit in case of marginal costing method is 9600 and value

of same in case of absorption costing method is 9300. Comparison of both values is indicating

that huge amount of profit is earned in case of marginal costing then absorption costing method.

It can be seen from table which is given above that in case of marginal costing method cost of

production, cost of goods sold, production cost of sale are taken in to account. Apart from this,

variable overhead and fixed cost administration expenses are taken in to account.

It is clear that there is gap between marginal and absorption costing method. Firms can

choose either of these methods or can choose both approaches to compute profit in the business.

It will be better to use marginal costing method in the business because variable expenses are

only made in the business to produce goods and making available services to the customers.

Hence, if only variable expense is only taken in to consideration for calculation of profit then it

cannot be considered wrong. On other hand, there is logic behind using absorption costing

method in the business. It is well known fact that in absorption costing method both fixed and

variable expenses are taken in to account (Burritt and Schaltegger, 2010). Fixed expenses are

directly not related to production of specific number of unit but same support manufacturing of

goods at workplace. Hence, it is not completely possible to not include fixed expenses in costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of product. Secondly, fixed expenses after all are cost to the firm and same can be covered by

sales revenue. Thus, from this point of view it can be said that it is very important to include

fixed expenses in profit computation. Firms have to choose whether they will use specific

method in profit computation or will use both approaches at same time to compute profit in the

business. It can be said that there is huge significance of both approaches for the firms because

same help them in making decisions in right direction. Firms must prepare both marginal and

absorption costing statements in their business so that they get an overview of entire profitability

(Englund and Gerdin, 2011). Means that if managers will compare profit when only variable

expenses are considered and when both sort of expense are taken in to account then in that case

they will come to know about exact impact that these expenses have on the firm profitability.

Accordingly, steps can be taken in to account to control expenses in the business. Thus, it can be

said that both marginal and absorption costing methods assist firms in formulation of strategy in

the business. Hence, both approaches must be used in the business so that prudent decisions can

be made in the business.

P4 Advantage and disadvantage of using different planning tools in the

budgetary control

Planning is the important function of management. For every business operation

performance planning need to be done in the business. It can be observed that it is the planning

that help firms in performing their operations in proper manner at workplace. Before planning it

is important to collect some of the important facts and figures in the business so that decisions

can be made in proper manner at workplace. Budgetary control is another term that is widely

used in the business. This term reflect control on the budget and making expenses within limit

that is determined in the budget. Different planning tools need to be used in the business because

by using same input can be obtained about areas where work need to be done in the business. It

can be said that there is huge importance of different planning tools that are used in the business.

Some of planning tools that can be used in respect to budgetary control are explained below. Variance analysis: It is the one of the widely used approach as under this method

standards are determined and against it real performance of the company is measured. On

basis of comparison it is determined whether firm performs good or bad in the business.

sales revenue. Thus, from this point of view it can be said that it is very important to include

fixed expenses in profit computation. Firms have to choose whether they will use specific

method in profit computation or will use both approaches at same time to compute profit in the

business. It can be said that there is huge significance of both approaches for the firms because

same help them in making decisions in right direction. Firms must prepare both marginal and

absorption costing statements in their business so that they get an overview of entire profitability

(Englund and Gerdin, 2011). Means that if managers will compare profit when only variable

expenses are considered and when both sort of expense are taken in to account then in that case

they will come to know about exact impact that these expenses have on the firm profitability.

Accordingly, steps can be taken in to account to control expenses in the business. Thus, it can be

said that both marginal and absorption costing methods assist firms in formulation of strategy in

the business. Hence, both approaches must be used in the business so that prudent decisions can

be made in the business.

P4 Advantage and disadvantage of using different planning tools in the

budgetary control

Planning is the important function of management. For every business operation

performance planning need to be done in the business. It can be observed that it is the planning

that help firms in performing their operations in proper manner at workplace. Before planning it

is important to collect some of the important facts and figures in the business so that decisions

can be made in proper manner at workplace. Budgetary control is another term that is widely

used in the business. This term reflect control on the budget and making expenses within limit

that is determined in the budget. Different planning tools need to be used in the business because

by using same input can be obtained about areas where work need to be done in the business. It

can be said that there is huge importance of different planning tools that are used in the business.

Some of planning tools that can be used in respect to budgetary control are explained below. Variance analysis: It is the one of the widely used approach as under this method

standards are determined and against it real performance of the company is measured. On

basis of comparison it is determined whether firm performs good or bad in the business.

This method is used by all sorts of firms whether they are small or large in size because it

is very easy to make use of this method in the business (Quinn, 2014). Simply mangers

needs to determine standards on the basis of past data or forecast that is available to them

and need to compare actual with determined standard in order to measure firm

performance.

Merits

Variance analysis helps managers in measuring firm performance and identifying areas

where immediate action need to be taken to solve business problem.

Cost is controlled and efficiency level in business gets improved at fat rate.

Demerits

One of major demerit of variance analysis is that gap that is between actual and budgeted

values can be interpreted by every manager in different manager (Merchant, 2012). One

manager can say it moderate gap while other one may say it large gap. Hence, it is

difficult to determine intensity of action that need to be taken on basis of variance. Zero based budgeting: In this sort of budgeting initially no amount is allocated to any

department and manager for each department have to make projection about cash flows.

If top manager think that determined value is accurate then in that case budget is passed

from their side. Finally, all departments budget are added to develop final budget for the

firm.

Merits

One of main merit of zero based budgeting is that it is systematic approach of budgeting

and helps budgetary control in systematic manner because standards are determined by

considering multiple factors.

Other major benefit of zero based budgeting is that it enhances accuracy of manager in

terms of performance measurement.

Demerit

One of major demerit of zero based budgeting is that if department budgets are not

matching each other then same cannot be prepared in proper manner. For example

finance manager allocate less amount of budget but production manager allocate huge

amount budget then both will be contradict. If budget of both managers will be passed

then same will be prepared in wrong manner.

is very easy to make use of this method in the business (Quinn, 2014). Simply mangers

needs to determine standards on the basis of past data or forecast that is available to them

and need to compare actual with determined standard in order to measure firm

performance.

Merits

Variance analysis helps managers in measuring firm performance and identifying areas

where immediate action need to be taken to solve business problem.

Cost is controlled and efficiency level in business gets improved at fat rate.

Demerits

One of major demerit of variance analysis is that gap that is between actual and budgeted

values can be interpreted by every manager in different manager (Merchant, 2012). One

manager can say it moderate gap while other one may say it large gap. Hence, it is

difficult to determine intensity of action that need to be taken on basis of variance. Zero based budgeting: In this sort of budgeting initially no amount is allocated to any

department and manager for each department have to make projection about cash flows.

If top manager think that determined value is accurate then in that case budget is passed

from their side. Finally, all departments budget are added to develop final budget for the

firm.

Merits

One of main merit of zero based budgeting is that it is systematic approach of budgeting

and helps budgetary control in systematic manner because standards are determined by

considering multiple factors.

Other major benefit of zero based budgeting is that it enhances accuracy of manager in

terms of performance measurement.

Demerit

One of major demerit of zero based budgeting is that if department budgets are not

matching each other then same cannot be prepared in proper manner. For example

finance manager allocate less amount of budget but production manager allocate huge

amount budget then both will be contradict. If budget of both managers will be passed

then same will be prepared in wrong manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incremental budgeting: It is one of the most important type of budget because in this

previous year budget is considered and increment is made to past year values of

components (Angelakis, Theriou. and Floropoulos, 2010). This budget is gaining wide

popularity among people. Merit and demerit of incremental budget is given below.

Merit

One of major merit of incremental budget is that it is very easy to prepare mentioned sort

of budget as it can be prepared in very short duration by the business managers.

Demerit

One of major demerit of incremental budget is that it is not necessary that every year

sales revenue increased in the business. It is assumed that sales will increase and in

alignment to same expenses will also enhance. It is not necessary that always sales

revenue increased and on this basis it can be said that incremental budget sometimes may

carry out budgetary control in wrong direction.

P5 Adoption of management accounting system to respond to financial

problems

There are different sort of management accounting systems that can be used to respond to

financial problems. Financial problem may be related to less availability of cash in the business

or ineffective use of same in business. Different management accounting systems that can be

used to respond to financial problems are given below. Financial governance: It is one of the most important tools of management accounting

as under this system there are employees and their accountability is determined. In

proportion of accountability sufficient authority is given to them. In case any task is

performed in wrong manner then in that case there is any specific employee that can be

easily made responsible for non performance of task that is related to effective use of

cash in business in proper manner (Figge and Hahn, 2013). It can be said that financial

governance have due importance for the firms. KPI: KPI refers to the key performance indicators and under this standard in respect to

effective use of cash in business can be determined by using budget. In this way KPI can

be used to respond to financial problems.

previous year budget is considered and increment is made to past year values of

components (Angelakis, Theriou. and Floropoulos, 2010). This budget is gaining wide

popularity among people. Merit and demerit of incremental budget is given below.

Merit

One of major merit of incremental budget is that it is very easy to prepare mentioned sort

of budget as it can be prepared in very short duration by the business managers.

Demerit

One of major demerit of incremental budget is that it is not necessary that every year

sales revenue increased in the business. It is assumed that sales will increase and in

alignment to same expenses will also enhance. It is not necessary that always sales

revenue increased and on this basis it can be said that incremental budget sometimes may

carry out budgetary control in wrong direction.

P5 Adoption of management accounting system to respond to financial

problems

There are different sort of management accounting systems that can be used to respond to

financial problems. Financial problem may be related to less availability of cash in the business

or ineffective use of same in business. Different management accounting systems that can be

used to respond to financial problems are given below. Financial governance: It is one of the most important tools of management accounting

as under this system there are employees and their accountability is determined. In

proportion of accountability sufficient authority is given to them. In case any task is

performed in wrong manner then in that case there is any specific employee that can be

easily made responsible for non performance of task that is related to effective use of

cash in business in proper manner (Figge and Hahn, 2013). It can be said that financial

governance have due importance for the firms. KPI: KPI refers to the key performance indicators and under this standard in respect to

effective use of cash in business can be determined by using budget. In this way KPI can

be used to respond to financial problems.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital budgeting tools: Capital budgeting tools can be used to evaluate project and

make proper decisions. On basis of capital budgeting it is determined that what will be

cash inflow amount. On this basis it can be determined that what amount of money need

to be borrowed from banks to meet financial needs so that effective use of cash can be

made in business according to requirements. Ratio analysis: Ratio analysis help managers in evaluating firm debt and equity mix. It

must be noted that debt and equity mix reflect a lot of things for the business firm. Debt

and equity mix reflect whether in the upcoming time period financial problem will

increased for the firm or will remain same. Apart from this, current ratio can also be used

to respond to financial problem because it reflect proportion of current assets to current

liability. In case current asset ratio is low then it means that firm is not able to pay current

liability on time. By using this ratio financial problem is detected at initial stage and steps

are taken on time to respond to financial problems.

CONCLUSION

On the basis of above discussion it is concluded that there are number of tools and

methods in the business that can be used to respond to financial problems. Hence, relevant tools

must be used to respond to financial problems. It is also deduced that both approaches to

compute profit are effective and according to need relevant method must be used in the business.

Apart from this, different sort of reporting must be used in the business so that performance of

the firm can be evaluated from different angles and steps can be take on time to improve

performance of company. Management accounting systems of different types are available and

they must be cautiously used by the firms at workplace.

make proper decisions. On basis of capital budgeting it is determined that what will be

cash inflow amount. On this basis it can be determined that what amount of money need

to be borrowed from banks to meet financial needs so that effective use of cash can be

made in business according to requirements. Ratio analysis: Ratio analysis help managers in evaluating firm debt and equity mix. It

must be noted that debt and equity mix reflect a lot of things for the business firm. Debt

and equity mix reflect whether in the upcoming time period financial problem will

increased for the firm or will remain same. Apart from this, current ratio can also be used

to respond to financial problem because it reflect proportion of current assets to current

liability. In case current asset ratio is low then it means that firm is not able to pay current

liability on time. By using this ratio financial problem is detected at initial stage and steps

are taken on time to respond to financial problems.

CONCLUSION

On the basis of above discussion it is concluded that there are number of tools and

methods in the business that can be used to respond to financial problems. Hence, relevant tools

must be used to respond to financial problems. It is also deduced that both approaches to

compute profit are effective and according to need relevant method must be used in the business.

Apart from this, different sort of reporting must be used in the business so that performance of

the firm can be evaluated from different angles and steps can be take on time to improve

performance of company. Management accounting systems of different types are available and

they must be cautiously used by the firms at workplace.

REFERENCES

Books and Journals

Angelakis, G., Theriou, N. and Floropoulos, I., 2010. Adoption and benefits of management

accounting practices: Evidence from Greece and Finland. Advances in accounting. 26(1).

pp.87-96.

Burns, J. and Scapens, R.W., 2000. Conceptualizing management accounting change: an

institutional framework. Management accounting research. 11(1). pp.3-25.

Burritt, R.L. and Schaltegger, S., 2010. Sustainability accounting and reporting: fad or trend?.

Accounting, Auditing & Accountability Journal. 23(7). pp.829-846.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Cuganesan, S., Dunford, R. and Palmer, I., 2012. Strategic management accounting and strategy

practices within a public sector agency. Management Accounting Research. 23(4). pp.245-

260.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Englund, H. and Gerdin, J., 2011. Agency and structure in management accounting research:

reflections and extensions of Kilfoyle and Richardson. Critical Perspectives on

Accounting. 22(6). pp.581-592.

Figge, F. and Hahn, T., 2013. Value drivers of corporate eco-efficiency: Management accounting

information for the efficient use of environmental resources. Management Accounting

Research. 24(4). pp.387-400.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research. 27(1). pp.81-119.

Li, X. and et.al., 2012. A comparative analysis of management accounting systems’ impact on

lean implementation. International Journal of Technology Management. 57(1/2/3). pp.33-

48.

Merchant, K.A., 2012. Making management accounting research more useful. Pacific

Accounting Review. 24(3). pp.334-356.

Books and Journals

Angelakis, G., Theriou, N. and Floropoulos, I., 2010. Adoption and benefits of management

accounting practices: Evidence from Greece and Finland. Advances in accounting. 26(1).

pp.87-96.

Burns, J. and Scapens, R.W., 2000. Conceptualizing management accounting change: an

institutional framework. Management accounting research. 11(1). pp.3-25.

Burritt, R.L. and Schaltegger, S., 2010. Sustainability accounting and reporting: fad or trend?.

Accounting, Auditing & Accountability Journal. 23(7). pp.829-846.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance: a

configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Cuganesan, S., Dunford, R. and Palmer, I., 2012. Strategic management accounting and strategy

practices within a public sector agency. Management Accounting Research. 23(4). pp.245-

260.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Englund, H. and Gerdin, J., 2011. Agency and structure in management accounting research:

reflections and extensions of Kilfoyle and Richardson. Critical Perspectives on

Accounting. 22(6). pp.581-592.

Figge, F. and Hahn, T., 2013. Value drivers of corporate eco-efficiency: Management accounting

information for the efficient use of environmental resources. Management Accounting

Research. 24(4). pp.387-400.

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Lavia López, O. and Hiebl, M.R., 2014. Management accounting in small and medium-sized

enterprises: current knowledge and avenues for further research. Journal of Management

Accounting Research. 27(1). pp.81-119.

Li, X. and et.al., 2012. A comparative analysis of management accounting systems’ impact on

lean implementation. International Journal of Technology Management. 57(1/2/3). pp.33-

48.

Merchant, K.A., 2012. Making management accounting research more useful. Pacific

Accounting Review. 24(3). pp.334-356.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.