HI5020 - Corporate Accounting: Retail Food Group's Cash Flow Statement

VerifiedAdded on 2023/06/11

|10

|2193

|349

Report

AI Summary

This report provides a comprehensive analysis of the cash flow statement of Retail Food Group (RFG) using their financial statements from 2015 to 2017. It examines cash flows from operations, financing, and investing activities, highlighting key items such as finance costs, income tax payments, and proceeds from borrowings. The analysis includes a comparative overview of cash flow statements over the three years, noting trends and significant changes. Additionally, the report discusses other comprehensive income items, corporate income tax accounting, deferred tax assets and liabilities, and explores the consistency of RFG's tax treatment with Australian taxation laws. The assessment concludes that RFG's tax operations align with Australian taxation laws, with some variations due to deferred tax assets.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:..................................................................................................................2

Requirement (i):.....................................................................................................................2

Requirement (ii):....................................................................................................................4

Other CIT:..................................................................................................................................5

Requirement (iii):...................................................................................................................5

Requirement (iv):...................................................................................................................5

Requirement (v):....................................................................................................................5

Accounting for CIT....................................................................................................................6

Requirement (vi):...................................................................................................................6

Requirement (vii):..................................................................................................................6

Requirement (viii):.................................................................................................................6

Requirement (ix):...................................................................................................................6

Requirement (x):....................................................................................................................7

Requirement (xi):...................................................................................................................7

References..................................................................................................................................8

Table of Contents

Cash flow statement:..................................................................................................................2

Requirement (i):.....................................................................................................................2

Requirement (ii):....................................................................................................................4

Other CIT:..................................................................................................................................5

Requirement (iii):...................................................................................................................5

Requirement (iv):...................................................................................................................5

Requirement (v):....................................................................................................................5

Accounting for CIT....................................................................................................................6

Requirement (vi):...................................................................................................................6

Requirement (vii):..................................................................................................................6

Requirement (viii):.................................................................................................................6

Requirement (ix):...................................................................................................................6

Requirement (x):....................................................................................................................7

Requirement (xi):...................................................................................................................7

References..................................................................................................................................8

2CORPORATE ACCOUNTING

Cash flow statement:

Requirement (i):

The report has aimed to highlight on the various types of flow of cash in a business

concern. The main assessment of the cash flow is depicted in terms of “Retail Food Group

(RFG)” which consists of cash flows in three categories namely CF from operations, CF from

financing activities and CF from investing activities. These depictions are considered with

the financial statement of the company published in 2017.

Cash flows from operations:

The important assessment of the items has been seen with the items such as finance

cost, IT payment, CP to the suppliers and CR from the customers. These values are depicted

with the various types of the considerations which are seen to be depicted in terms of the

recovery made with the CR and credit sales. These items are further seen to increase to more

in 2017. This is able to depict that there was more amount of cash recovered in terms of the

depictions which are able to state on the considerations related to the amounts of the

materials purchases and payments made to the suppliers. This demand is further considered

with the various types of the other depictions which are considered with the increase in the

market risk followed by increase in the RFG products.

In addition to this, the RFG accountable will be able to make the interest payments in

terms of the borrowings which needs to be raised in terms of the different sources. As it has it

has undertaken interest payment the total amount has increased from 2016 to 2017. In

addition to this, the profit level of organization has also increased with the payment of

“$19,298,000 in 2016 to $21,460,000 in 2017” (Rfg.com.au., 2018).

Cash flow statement:

Requirement (i):

The report has aimed to highlight on the various types of flow of cash in a business

concern. The main assessment of the cash flow is depicted in terms of “Retail Food Group

(RFG)” which consists of cash flows in three categories namely CF from operations, CF from

financing activities and CF from investing activities. These depictions are considered with

the financial statement of the company published in 2017.

Cash flows from operations:

The important assessment of the items has been seen with the items such as finance

cost, IT payment, CP to the suppliers and CR from the customers. These values are depicted

with the various types of the considerations which are seen to be depicted in terms of the

recovery made with the CR and credit sales. These items are further seen to increase to more

in 2017. This is able to depict that there was more amount of cash recovered in terms of the

depictions which are able to state on the considerations related to the amounts of the

materials purchases and payments made to the suppliers. This demand is further considered

with the various types of the other depictions which are considered with the increase in the

market risk followed by increase in the RFG products.

In addition to this, the RFG accountable will be able to make the interest payments in

terms of the borrowings which needs to be raised in terms of the different sources. As it has it

has undertaken interest payment the total amount has increased from 2016 to 2017. In

addition to this, the profit level of organization has also increased with the payment of

“$19,298,000 in 2016 to $21,460,000 in 2017” (Rfg.com.au., 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Cash flows from financing activities:

The different types of the other consideration which are related to the proceeds from

the borrowings, issue cost related to payment and the debt issue payment needs to be

significant considered with the disclosures made in the overhead. It needs to be further

discerned that the share issues need to be taken into consideration with the earnings that the

RFG has made in terms of the investments. Additionally, the increase in the cash borrowings

with the proceeds was also evident during the FY 2017. On the contrary RFG was able to

decrease the borrowings payment to $ 148372000 in 2017. This is a positive aspect for the

company (Frischmann, Pumphrey, & Santhanakrishnan, 2015).

The distribution of the dividend payment of the company can be depicted with the

different types of the consideration which are seen to be associated with the consideration of

increasing of net earnings. During the issue of shares the company issued additional shares

which needs to be considered in terms of the additional cost of issuing of shares. Despite of

this, there was not much amount of debt issues which shows that the overall cost for the debt

issues has reduced to $ 223000 in 2017.

CF pertaining to investing activities:

In this area the important items for the payments and proceeds from the PPE and

intangible assets are considered with the interest received. Additionally, the payment for the

PPE have amounted as per the purchase and acquiring of all the necessary items which need

to be taken into consideration with the various type the depictions for raising the asset base.

Due to this, the proceeds pertaining to these assets have reduced in 2017 in compare to 2016.

Additionally, the IP needs to be defined with the total money incurred from the banks. This

needs to be identified that the increase in the cash flows from the capital projects (Chang,

Dasgupta, Wong, & Yao, 2014).

Cash flows from financing activities:

The different types of the other consideration which are related to the proceeds from

the borrowings, issue cost related to payment and the debt issue payment needs to be

significant considered with the disclosures made in the overhead. It needs to be further

discerned that the share issues need to be taken into consideration with the earnings that the

RFG has made in terms of the investments. Additionally, the increase in the cash borrowings

with the proceeds was also evident during the FY 2017. On the contrary RFG was able to

decrease the borrowings payment to $ 148372000 in 2017. This is a positive aspect for the

company (Frischmann, Pumphrey, & Santhanakrishnan, 2015).

The distribution of the dividend payment of the company can be depicted with the

different types of the consideration which are seen to be associated with the consideration of

increasing of net earnings. During the issue of shares the company issued additional shares

which needs to be considered in terms of the additional cost of issuing of shares. Despite of

this, there was not much amount of debt issues which shows that the overall cost for the debt

issues has reduced to $ 223000 in 2017.

CF pertaining to investing activities:

In this area the important items for the payments and proceeds from the PPE and

intangible assets are considered with the interest received. Additionally, the payment for the

PPE have amounted as per the purchase and acquiring of all the necessary items which need

to be taken into consideration with the various type the depictions for raising the asset base.

Due to this, the proceeds pertaining to these assets have reduced in 2017 in compare to 2016.

Additionally, the IP needs to be defined with the total money incurred from the banks. This

needs to be identified that the increase in the cash flows from the capital projects (Chang,

Dasgupta, Wong, & Yao, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

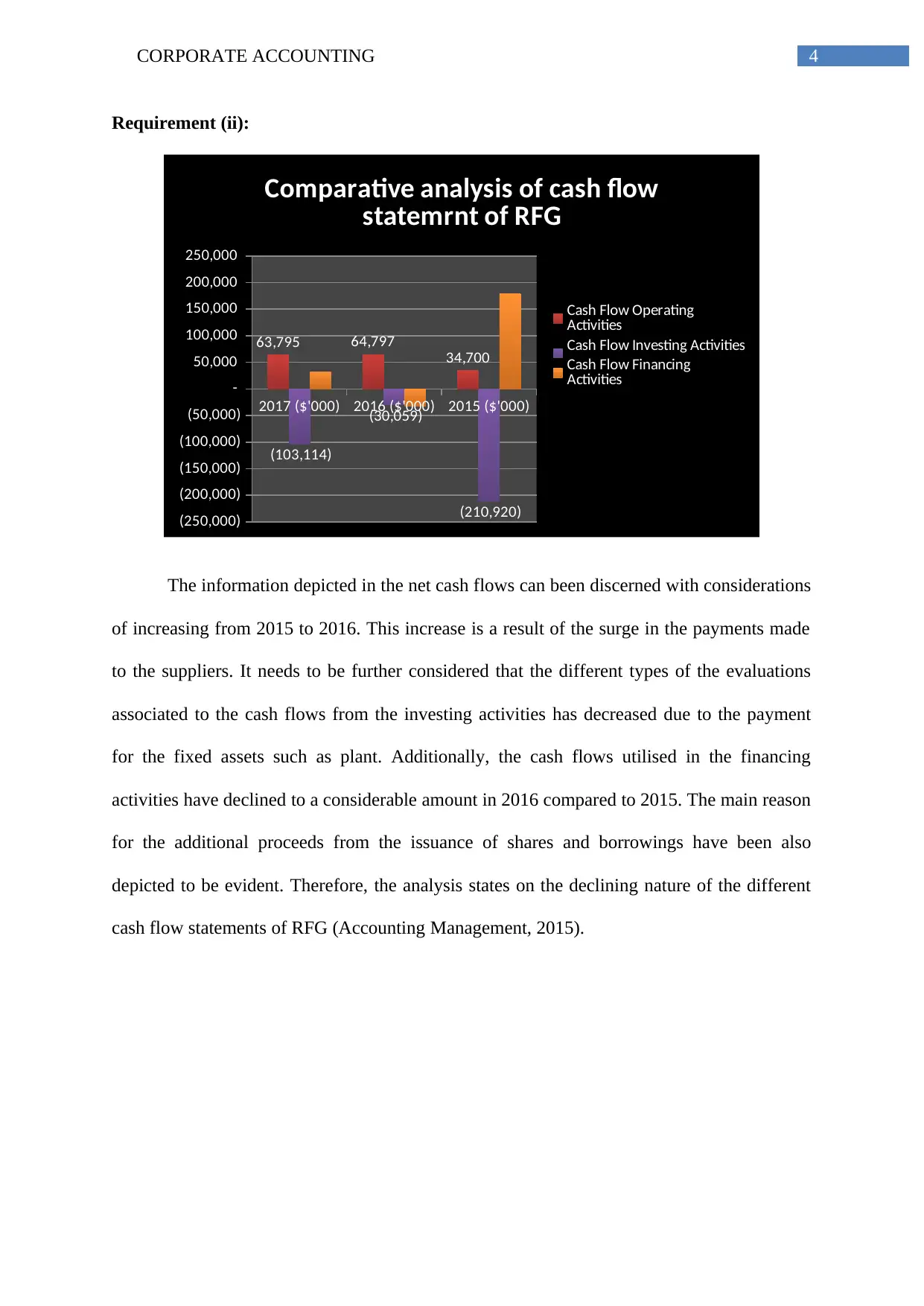

Requirement (ii):

2017 ($'000) 2016 ($'000) 2015 ($'000)

(250,000)

(200,000)

(150,000)

(100,000)

(50,000)

-

50,000

100,000

150,000

200,000

250,000

63,795 64,797

34,700

(103,114)

(30,059)

(210,920)

Comparative analysis of cash flow

statemrnt of RFG

Cash Flow Operating

Activities

Cash Flow Investing Activities

Cash Flow Financing

Activities

The information depicted in the net cash flows can been discerned with considerations

of increasing from 2015 to 2016. This increase is a result of the surge in the payments made

to the suppliers. It needs to be further considered that the different types of the evaluations

associated to the cash flows from the investing activities has decreased due to the payment

for the fixed assets such as plant. Additionally, the cash flows utilised in the financing

activities have declined to a considerable amount in 2016 compared to 2015. The main reason

for the additional proceeds from the issuance of shares and borrowings have been also

depicted to be evident. Therefore, the analysis states on the declining nature of the different

cash flow statements of RFG (Accounting Management, 2015).

Requirement (ii):

2017 ($'000) 2016 ($'000) 2015 ($'000)

(250,000)

(200,000)

(150,000)

(100,000)

(50,000)

-

50,000

100,000

150,000

200,000

250,000

63,795 64,797

34,700

(103,114)

(30,059)

(210,920)

Comparative analysis of cash flow

statemrnt of RFG

Cash Flow Operating

Activities

Cash Flow Investing Activities

Cash Flow Financing

Activities

The information depicted in the net cash flows can been discerned with considerations

of increasing from 2015 to 2016. This increase is a result of the surge in the payments made

to the suppliers. It needs to be further considered that the different types of the evaluations

associated to the cash flows from the investing activities has decreased due to the payment

for the fixed assets such as plant. Additionally, the cash flows utilised in the financing

activities have declined to a considerable amount in 2016 compared to 2015. The main reason

for the additional proceeds from the issuance of shares and borrowings have been also

depicted to be evident. Therefore, the analysis states on the declining nature of the different

cash flow statements of RFG (Accounting Management, 2015).

5CORPORATE ACCOUNTING

Other CIT:

Requirement (iii):

The comprehensive income from the RFG is depicted to consist of the significant

nature of the items in terms of the cash flow hedges, cash flow reserve and foreign currency

translation reserve.

Requirement (iv):

The business entities in general are depicted to use the foreign currency translation

reserve with the intention transferring the outcomes of the foreign unit as per the currency of

the domestic unit which is conducted in the financial reporting. Due to this, a considerable

amount of consolidation is taken into account with the entities relating to the determination of

the foreign currency. At the end of this process, the foreign currency is seen to be measured

in terms of the various type the factors which is measured pertaining to the present date of

reporting (Fernandes, Lynch, & Netemeyer, 2014).

As the cash flow reserve are not reported it is the obligation of the company apply tax

on such financial transactions.

Requirement (v):

The differentiated nature of the net income of an organization is seen to be based on

the different types of the considerations which are based on the variations in terms of the net

earnings pertaining to the external influence. The details of the account on OCI is stated in

the annual report of RFG. Additionally, the holistic view of the disclosure of the of the

income statement has been conducive in disclosing the items of the income statement.

Other CIT:

Requirement (iii):

The comprehensive income from the RFG is depicted to consist of the significant

nature of the items in terms of the cash flow hedges, cash flow reserve and foreign currency

translation reserve.

Requirement (iv):

The business entities in general are depicted to use the foreign currency translation

reserve with the intention transferring the outcomes of the foreign unit as per the currency of

the domestic unit which is conducted in the financial reporting. Due to this, a considerable

amount of consolidation is taken into account with the entities relating to the determination of

the foreign currency. At the end of this process, the foreign currency is seen to be measured

in terms of the various type the factors which is measured pertaining to the present date of

reporting (Fernandes, Lynch, & Netemeyer, 2014).

As the cash flow reserve are not reported it is the obligation of the company apply tax

on such financial transactions.

Requirement (v):

The differentiated nature of the net income of an organization is seen to be based on

the different types of the considerations which are based on the variations in terms of the net

earnings pertaining to the external influence. The details of the account on OCI is stated in

the annual report of RFG. Additionally, the holistic view of the disclosure of the of the

income statement has been conducive in disclosing the items of the income statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

Accounting for CIT

Requirement (vi):

The corporate income tax assessment needs to be prepared as per the compliance to

the taxation law of Australia. As per the annual report of RFG the PBT has significantly

increased from 2016 to 2017. The corporate tax rate is estimated with 30%, however the

reported taxable income is depicted as $25,686,000 in 2017 and $23,620,000 in 2016 (Risk,

2014).

Requirement (vii):

The analysis shows that the disclosure of the expenses of tax and tax amount needs to

be applicable with 30%. In several instances there has been no resemblance of the reported

amount of the tax expense in terms of the real tax expense. The initial factors show a non-

deductible amount of taxable income and additional amount of $638,000 in 2016. The these

factors have been depicted to result in variation pertaining to the actual expense and disclosed

expenses (Management, 2014).

Requirement (viii):

The significant assessment is able to state that in 2017 the RFG has included the

deferred tax assets as per the DTL as per the notes to the financial statement. Increase of the

of the DTA can be seen to be increasing from 2016 to 2017. Additionally, the DTL has

increased from 2016 to 2017.

Requirement (ix):

As per the financial statement assessment there is no instance of the IT payable in

2017. Despite of this, the IT payable amount to $4,455,000 in 2016. The ITE and the CTA is

seen to be differentiating from one another for several reasons. One of the main reason for

this can be depicted with the consideration of the various type of the factors which are

Accounting for CIT

Requirement (vi):

The corporate income tax assessment needs to be prepared as per the compliance to

the taxation law of Australia. As per the annual report of RFG the PBT has significantly

increased from 2016 to 2017. The corporate tax rate is estimated with 30%, however the

reported taxable income is depicted as $25,686,000 in 2017 and $23,620,000 in 2016 (Risk,

2014).

Requirement (vii):

The analysis shows that the disclosure of the expenses of tax and tax amount needs to

be applicable with 30%. In several instances there has been no resemblance of the reported

amount of the tax expense in terms of the real tax expense. The initial factors show a non-

deductible amount of taxable income and additional amount of $638,000 in 2016. The these

factors have been depicted to result in variation pertaining to the actual expense and disclosed

expenses (Management, 2014).

Requirement (viii):

The significant assessment is able to state that in 2017 the RFG has included the

deferred tax assets as per the DTL as per the notes to the financial statement. Increase of the

of the DTA can be seen to be increasing from 2016 to 2017. Additionally, the DTL has

increased from 2016 to 2017.

Requirement (ix):

As per the financial statement assessment there is no instance of the IT payable in

2017. Despite of this, the IT payable amount to $4,455,000 in 2016. The ITE and the CTA is

seen to be differentiating from one another for several reasons. One of the main reason for

this can be depicted with the consideration of the various type of the factors which are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

associated to the relevancy of the information in terms of the availability of the DTA. RFG

has been seen to be making several types of the additional payments which are considered as

per the actual tax expense. The surplus payment is responsible for the difference (Australian

Office of Financial Management, 2016).

Requirement (x):

The income statement clearly shows a tax expense paid amounting to $25,686,000 in

2017 and $23,620,000 in 2016, whereas this amount was different in the initial case. During

the initial computation the corporate tax rate of 30% was imposed. However, it needs to be

observed that the IT payable was reported under the CF from the operating activities. In

addition to this. The IT payment for the present year is seen to be depicted in terms of the

various type of the findings which are based on the inclusion of the several types of the cash

flow items included in the income statement of RFG (Bucci, 2014).

Requirement (xi):

Based on the findings from the discourse, there is absence of surprising factors

pertaining to the tax treatment for RFG. This is due to the fact that the tax operations in RFG

is applied as per the different types of the factors which are considered in agreement with the

taxation law in Australia. Despite of this it is important to note that RFG has adopted the

carrying amount off the treatment showed in the IT. The presence of the DTA is also

responsible for some variations (Frischmann et al., 2015).

associated to the relevancy of the information in terms of the availability of the DTA. RFG

has been seen to be making several types of the additional payments which are considered as

per the actual tax expense. The surplus payment is responsible for the difference (Australian

Office of Financial Management, 2016).

Requirement (x):

The income statement clearly shows a tax expense paid amounting to $25,686,000 in

2017 and $23,620,000 in 2016, whereas this amount was different in the initial case. During

the initial computation the corporate tax rate of 30% was imposed. However, it needs to be

observed that the IT payable was reported under the CF from the operating activities. In

addition to this. The IT payment for the present year is seen to be depicted in terms of the

various type of the findings which are based on the inclusion of the several types of the cash

flow items included in the income statement of RFG (Bucci, 2014).

Requirement (xi):

Based on the findings from the discourse, there is absence of surprising factors

pertaining to the tax treatment for RFG. This is due to the fact that the tax operations in RFG

is applied as per the different types of the factors which are considered in agreement with the

taxation law in Australia. Despite of this it is important to note that RFG has adopted the

carrying amount off the treatment showed in the IT. The presence of the DTA is also

responsible for some variations (Frischmann et al., 2015).

8CORPORATE ACCOUNTING

References

Accounting Management. (2015). Debt to equity ratio - explanation, formula, example and

interpretation | Accounting for Management.

Australian Office of Financial Management. (2016). Public Register of Government

Borrowings. Retrieved from http://aofm.gov.au/statistics/public-register-of-

government-borrowings/

Bucci, R. V. (2014). Statement of Cash Flows. In Medicine and Business (pp. 59–67).

https://doi.org/10.1007/978-3-319-04060-8_7

Chang, X., Dasgupta, S., Wong, G., & Yao, J. (2014). Cash-flow sensitivities and the

allocation of internal cash flow. Review of Financial Studies.

https://doi.org/10.1093/rfs/hhu066

Fernandes, D., Lynch, J. G., & Netemeyer, R. G. (2014). Financial Literacy, Financial

Education, and Downstream Financial Behaviors. Management Science, 60(8), 1861–

1883. https://doi.org/10.1287/mnsc.2013.1849

Frischmann, P. J., Pumphrey, L. D., & Santhanakrishnan, M. (2015). TEACHING THE

STATEMENT OF CASH FLOWS AND FREE CASH FLOW ESTIMATION

WHEN NONARTICULATION IS PRESENT. In Advances in Accounting

Education: Teaching and Curriculum Innovations (Vol. 17, pp. 145–165).

https://doi.org/10.1108/s1085-462220150000017018

Management, H. C. F. (2014). The ICD-10 Delay: What’s Next for Your Strategy. Healthcare

Financial Management, 68(6), 59–66.

References

Accounting Management. (2015). Debt to equity ratio - explanation, formula, example and

interpretation | Accounting for Management.

Australian Office of Financial Management. (2016). Public Register of Government

Borrowings. Retrieved from http://aofm.gov.au/statistics/public-register-of-

government-borrowings/

Bucci, R. V. (2014). Statement of Cash Flows. In Medicine and Business (pp. 59–67).

https://doi.org/10.1007/978-3-319-04060-8_7

Chang, X., Dasgupta, S., Wong, G., & Yao, J. (2014). Cash-flow sensitivities and the

allocation of internal cash flow. Review of Financial Studies.

https://doi.org/10.1093/rfs/hhu066

Fernandes, D., Lynch, J. G., & Netemeyer, R. G. (2014). Financial Literacy, Financial

Education, and Downstream Financial Behaviors. Management Science, 60(8), 1861–

1883. https://doi.org/10.1287/mnsc.2013.1849

Frischmann, P. J., Pumphrey, L. D., & Santhanakrishnan, M. (2015). TEACHING THE

STATEMENT OF CASH FLOWS AND FREE CASH FLOW ESTIMATION

WHEN NONARTICULATION IS PRESENT. In Advances in Accounting

Education: Teaching and Curriculum Innovations (Vol. 17, pp. 145–165).

https://doi.org/10.1108/s1085-462220150000017018

Management, H. C. F. (2014). The ICD-10 Delay: What’s Next for Your Strategy. Healthcare

Financial Management, 68(6), 59–66.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Rfg.com.au., 2018. [online] Available at:

http://rfg.com.au/wp-content/uploads/2018/02/RFGLAnnualReport2017.pdf

[Accessed 22 May 2018].

Risk, F. (2014). Financial Statements & Analysis of Shareholdings. Journal of Knowledge

Management, Economics and Information Technology, IV(5), 1–12.

Rfg.com.au., 2018. [online] Available at:

http://rfg.com.au/wp-content/uploads/2018/02/RFGLAnnualReport2017.pdf

[Accessed 22 May 2018].

Risk, F. (2014). Financial Statements & Analysis of Shareholdings. Journal of Knowledge

Management, Economics and Information Technology, IV(5), 1–12.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.