University Project: Life Insurance and Retirement Valuation Analysis

VerifiedAdded on 2022/08/13

|21

|2921

|55

Project

AI Summary

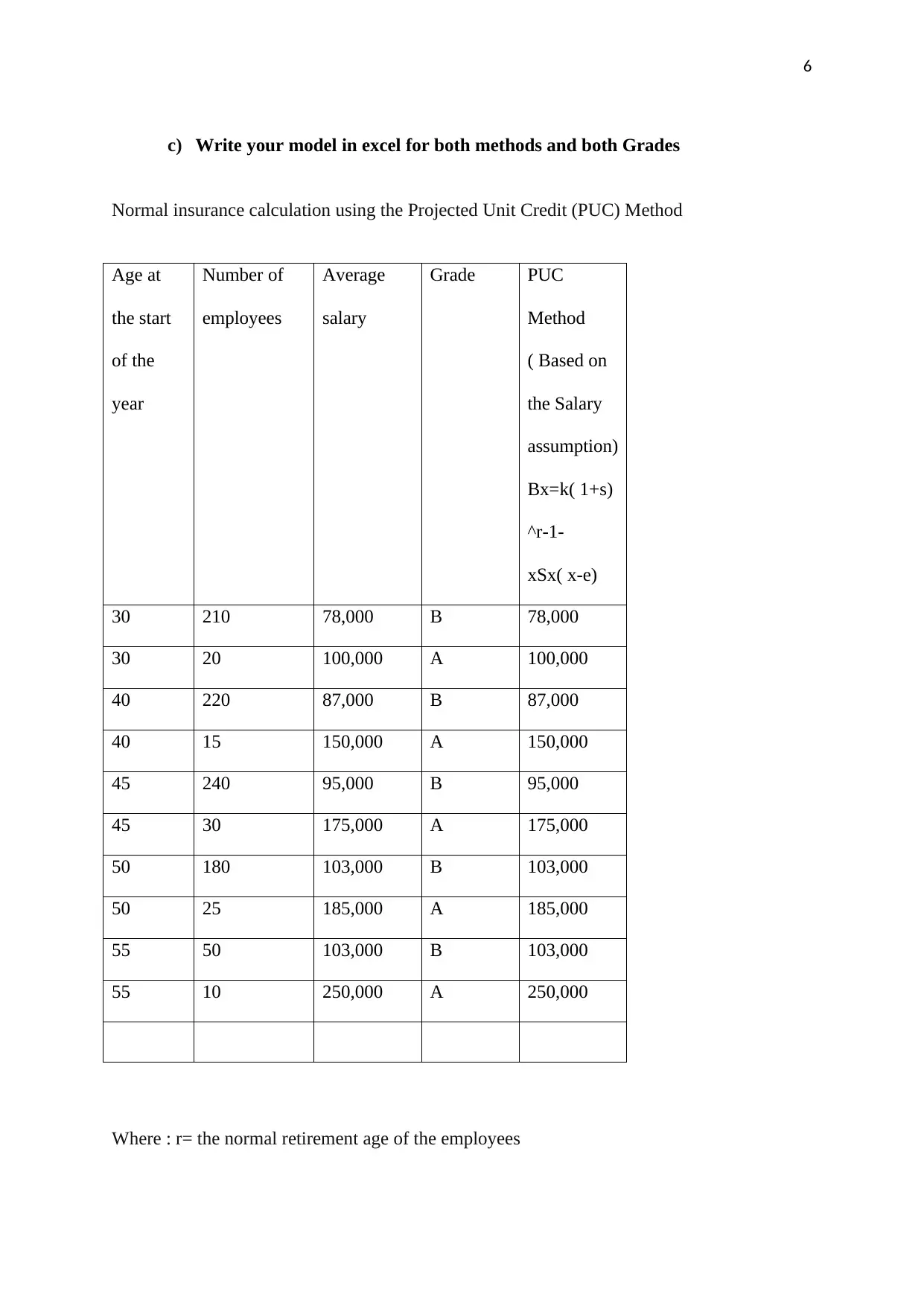

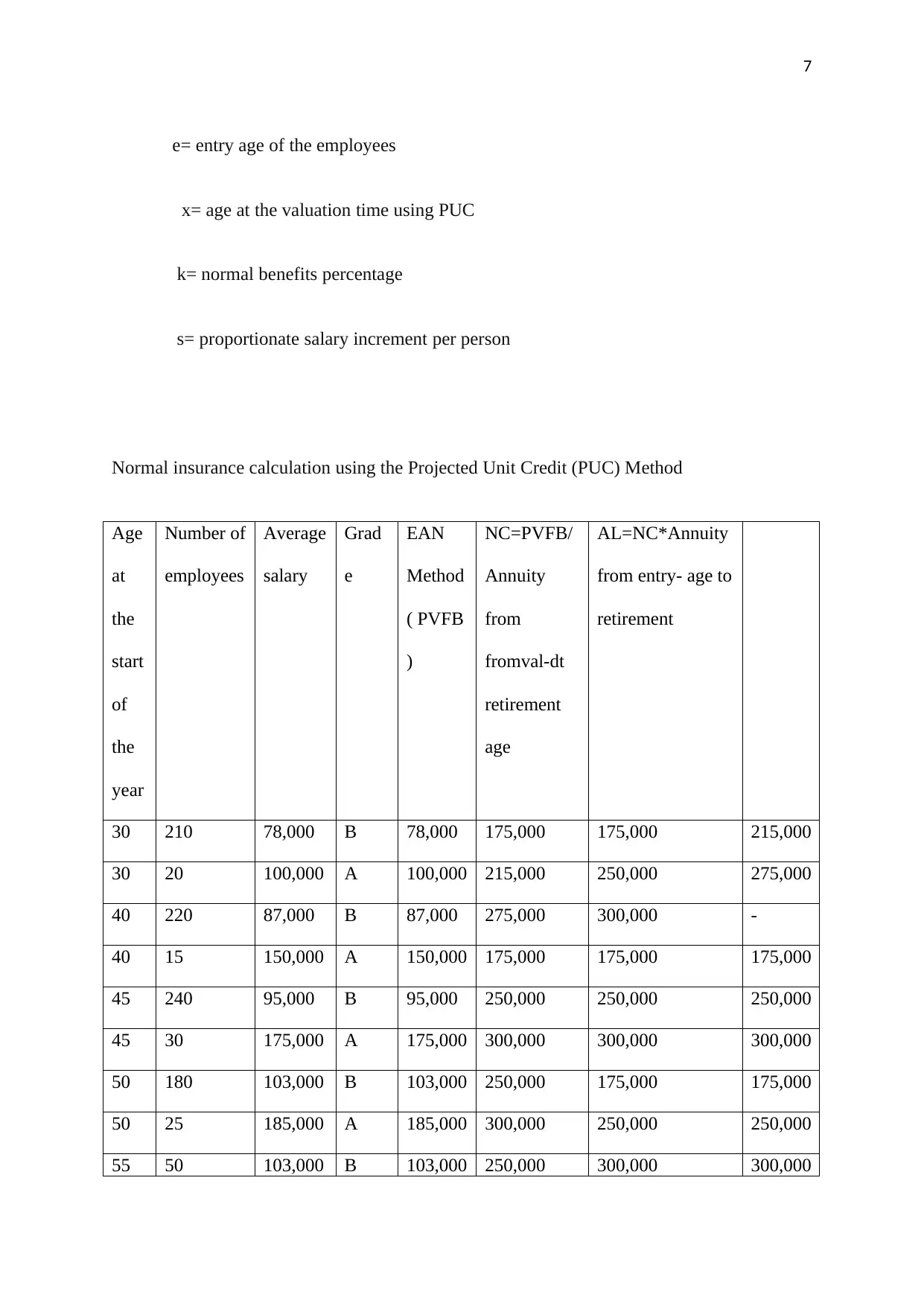

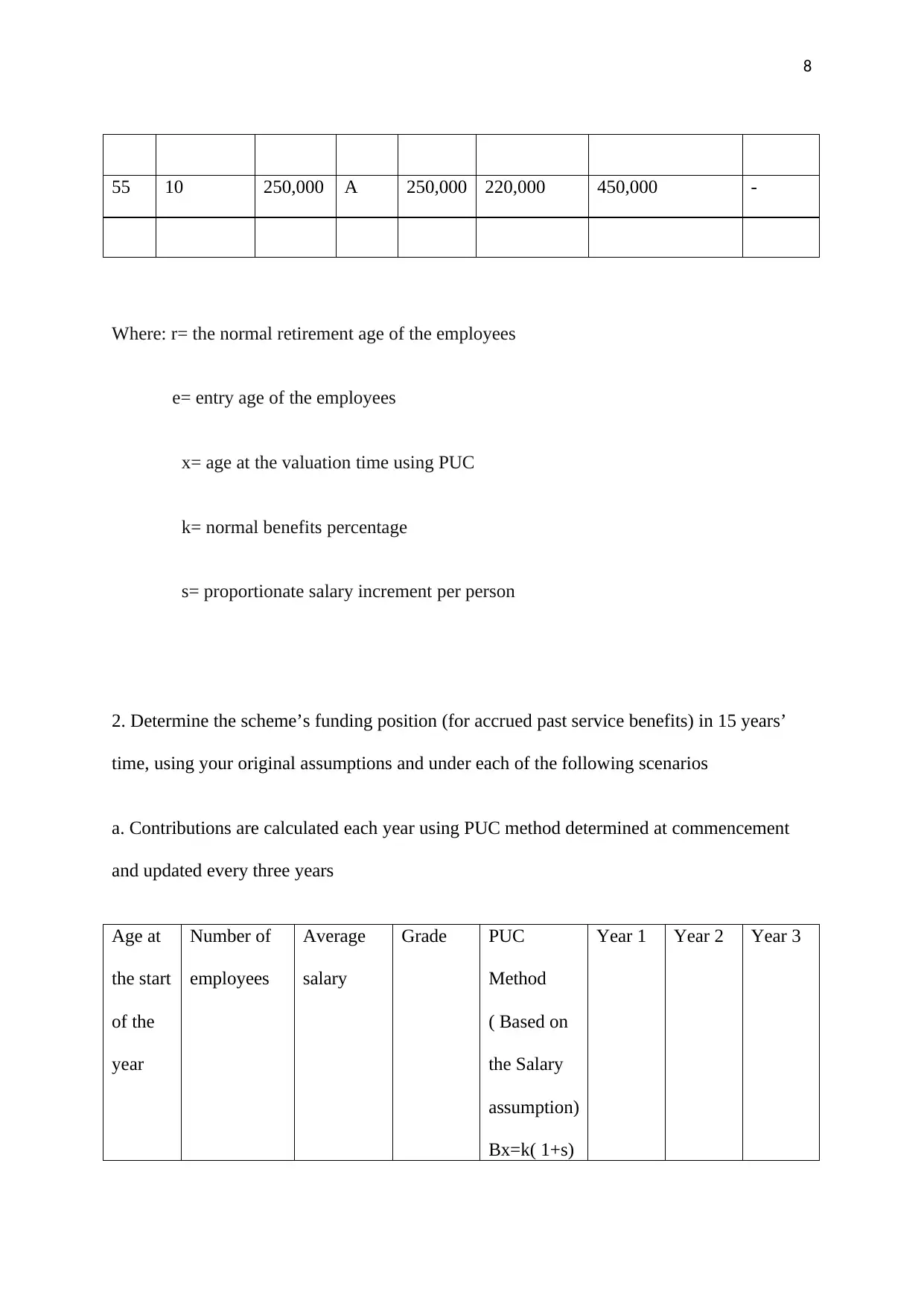

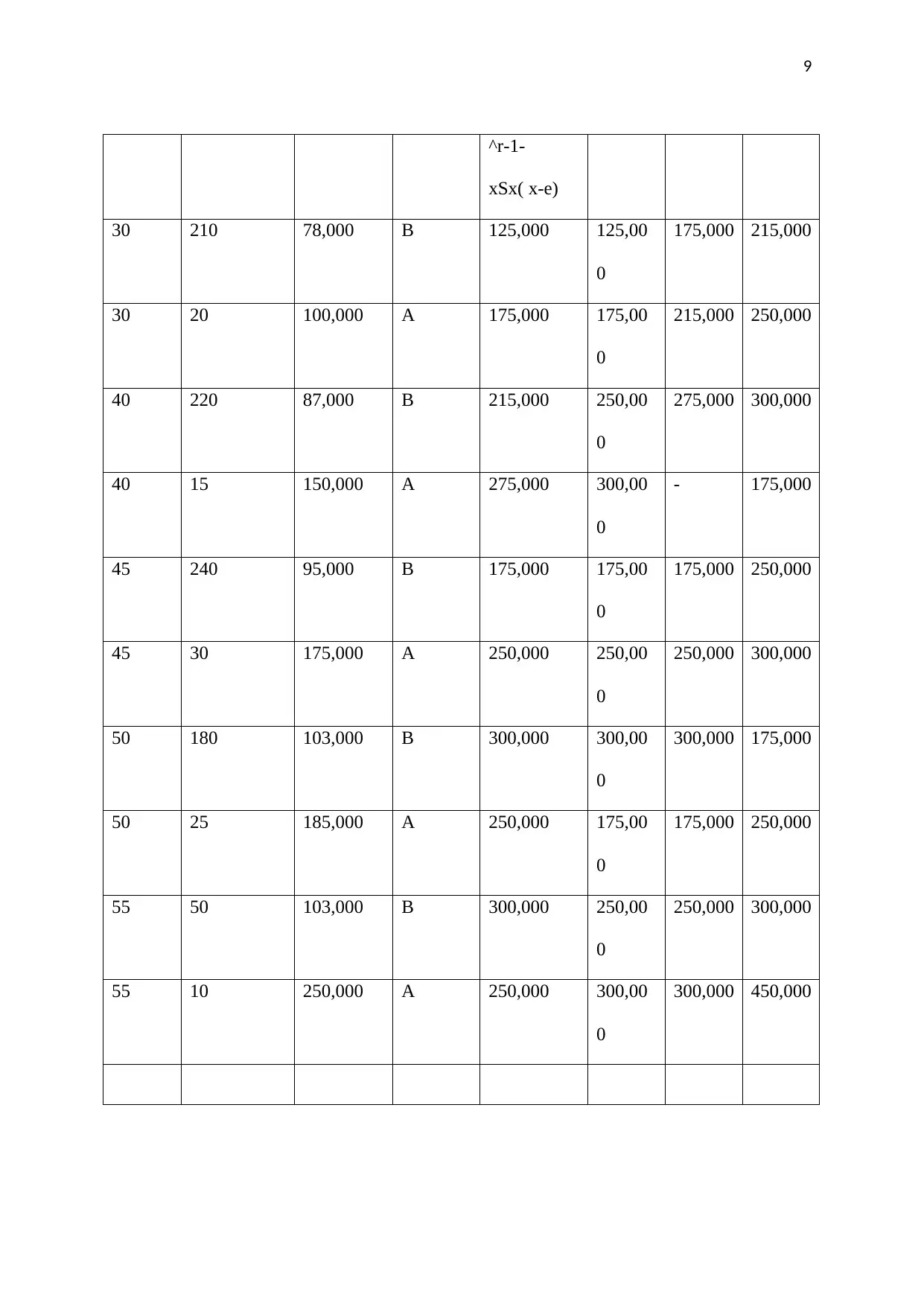

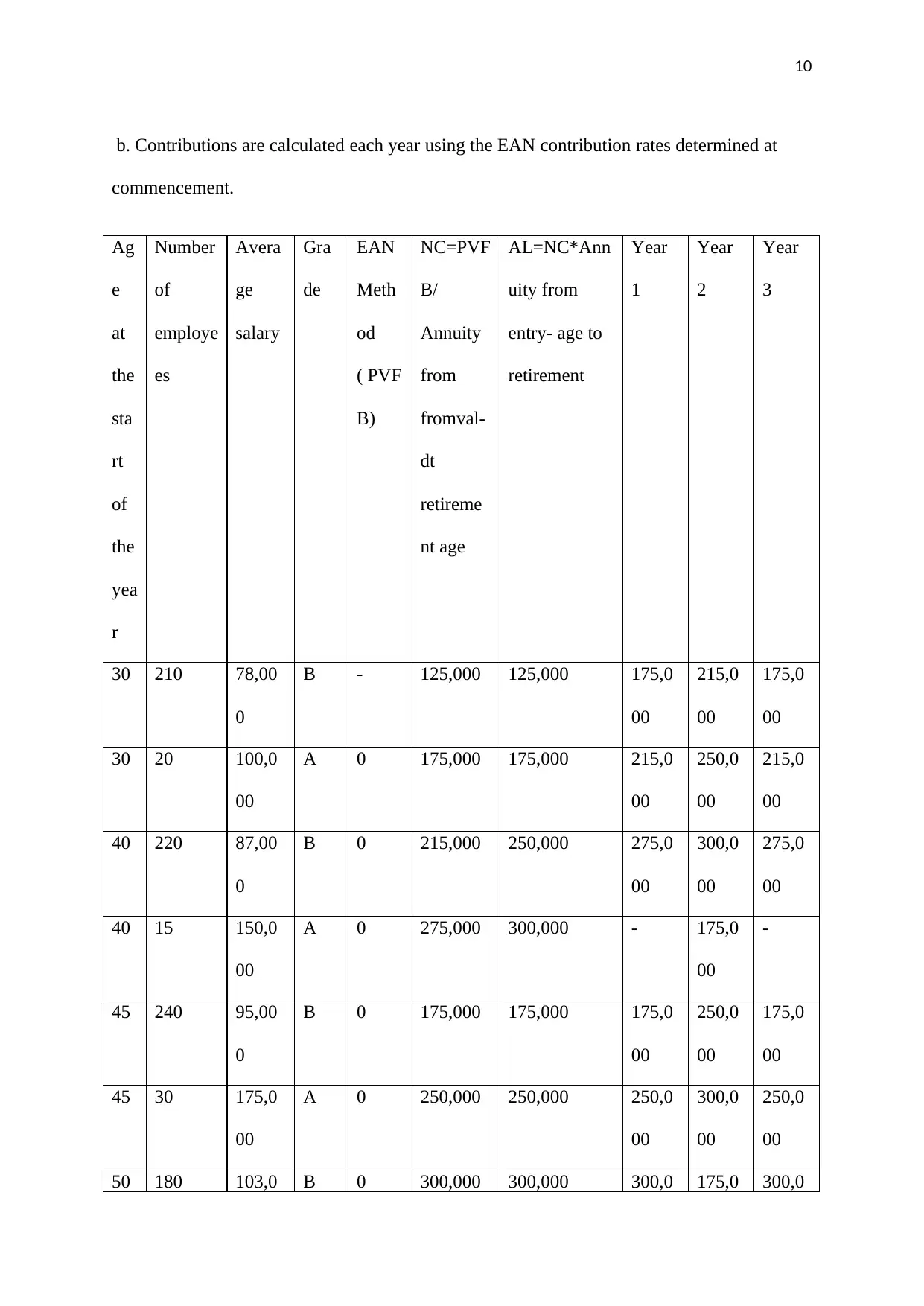

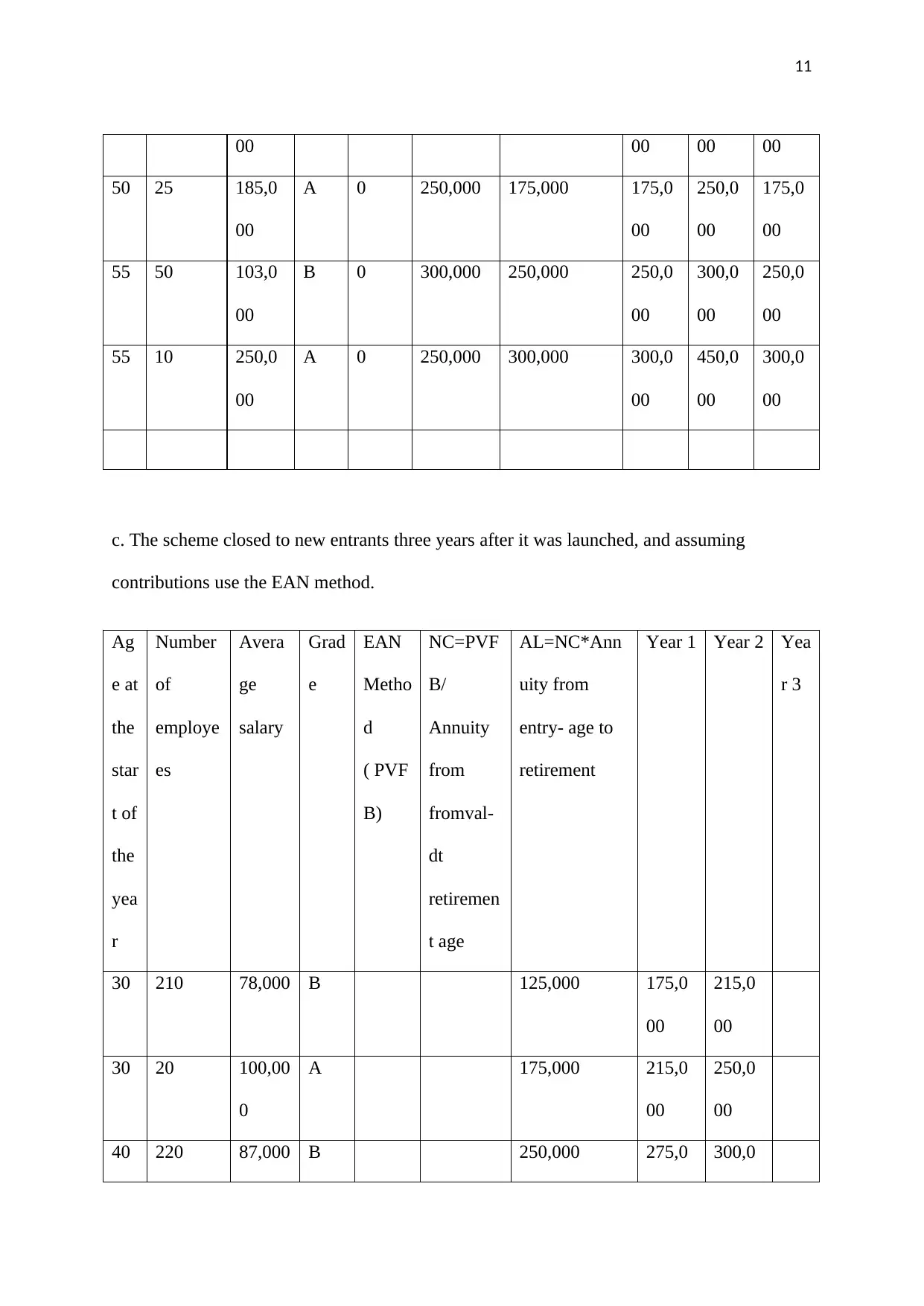

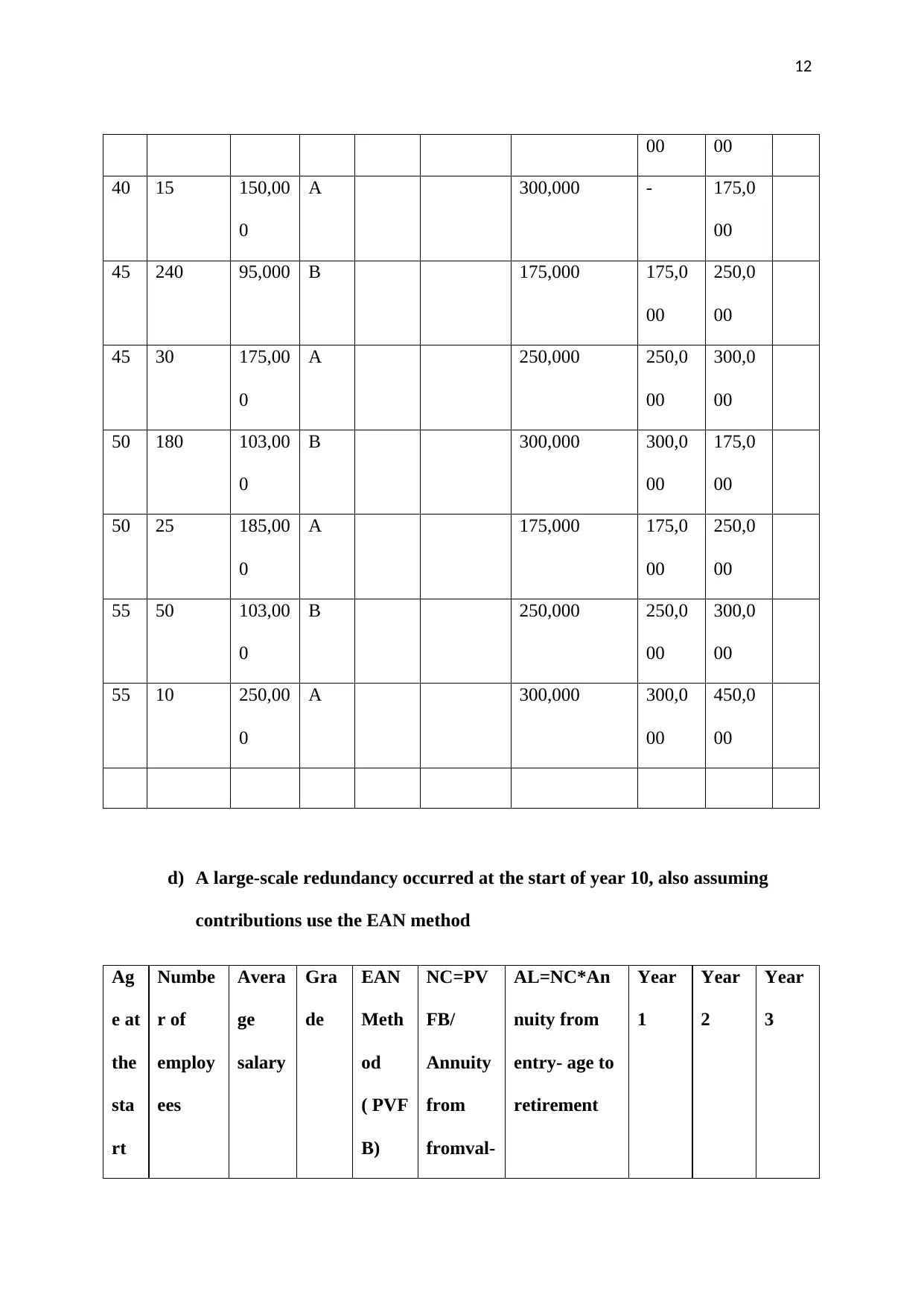

This assignment delves into the intricacies of life insurance and retirement valuation, focusing on the application of the Projected Unit Credit (PUC) and Entry Age Normal (EAN) methods. It involves creating assumptions for both methods within a defined-benefit pension scheme, considering factors like employee age, salary, and contribution rates. The project requires building Excel models to determine initial contribution rates and assess the scheme's funding position over a 15-year period under various scenarios, including changes in contribution calculation methods, scheme closures, and large-scale redundancies. Furthermore, the assignment explores the impact of different scenarios on the scheme's progression. The student also identifies potential factors influencing the scheme's progress and contribution requirements, such as demographic shifts, economic conditions, and policy adjustments, culminating in a business memo to the Board of Trustees outlining funding speeds and strategies for managing conflicts among stakeholders.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.