FIN200: Retirement Plan Comparison for Tertiary Sector Employees

VerifiedAdded on 2021/06/15

|9

|2719

|59

Report

AI Summary

This report, prepared for FIN200, assesses superannuation funds and the most suitable retirement plans for employees in the tertiary sector. It explores defined benefit and defined contribution plans, detailing their characteristics and implications for employees. The study emphasizes the importance of understanding these plans to make informed investment decisions, considering factors such as the time value of money, taxes, and inflation. The report analyzes the factors that tertiary sector employees should consider when planning for retirement, including investment earnings, contribution amounts, and potential risks. It highlights the impacts of the time value of money on retirement savings, emphasizing the benefits of early investment, and discusses the effects of taxes and inflation on retirement funds. The report also touches upon other factors like investment earning, progress and associated risks. The conclusion suggests that while both plans have their merits, the defined benefit plan is more suitable for tertiary employees, based on the research and analysis presented. This report provides valuable insights into retirement planning, offering comprehensive information for making sound financial decisions.

FIN200 Assignment T1, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The current study is about the assessment of superannuation funds and the most appropriate

type of retirement plan for the tertiary sector employees. The study will do research and

findings on retirement plans for facilitating the employees in making best retirement

decisions. Along with this study will also cover the factors that are required to be considered

before making investments in a particular retirement plan. Furthermore, there is two type of

retirement plan in which an employee can choose or invest which are Defined benefit plan

and defined contribution plan. Since, there is the high importance of gaining a better

understanding of this plan while making an investment, as these plans are very beneficial and

useful in future. These both plans are briefly analyzed and described in the current report; this

will help the employees in choosing the plan in accordance with their expectancy, interest

and interest and proficient and competence need. Furthermore, the study also covers and

discusses the impacts of the time value of money theory, taxes and inflation on the retirement

plans and decisions.

Important factors that should be considered by tertiary sector

employees for retirement planning to place their superannuation

contributions

Defined Benefit Plan

Defined Benefit plan offers employees a plan with a benefit which is a known amount. The

further employer, as well as the employee, might make a contribution to the plan; along with

this, the employer is liable for any shortfall in contribution while ensuring guaranteed pension

benefits. It takes place in two varieties which are traditional pensions as well as cash-balance

plans (Topa, Lunceford and Boyatzis, 2017). A defined benefit plan is also called as a

pension; it is a promissory account for retirement by which the employer integrates all the

money deposits and ensures a set payout at the stage of retirement. Under this plan, a fixed

and pre-set benefit is formed by the employer for employees. Generally, the employee does a

valuation of fixed benefit offered. While the employer, a business can make a contribution to

the plan and thereby deduction every year. On the other hand, this type of retirement plan is

complex yet costly to create and manage as compared to another type of plan.

A defined benefit plan determines the particular benefit that will be paid to retire at the

retirement (Clark and Newhouse, 2016)t. Further, the retirement benefit is based on a given

type of retirement plan for the tertiary sector employees. The study will do research and

findings on retirement plans for facilitating the employees in making best retirement

decisions. Along with this study will also cover the factors that are required to be considered

before making investments in a particular retirement plan. Furthermore, there is two type of

retirement plan in which an employee can choose or invest which are Defined benefit plan

and defined contribution plan. Since, there is the high importance of gaining a better

understanding of this plan while making an investment, as these plans are very beneficial and

useful in future. These both plans are briefly analyzed and described in the current report; this

will help the employees in choosing the plan in accordance with their expectancy, interest

and interest and proficient and competence need. Furthermore, the study also covers and

discusses the impacts of the time value of money theory, taxes and inflation on the retirement

plans and decisions.

Important factors that should be considered by tertiary sector

employees for retirement planning to place their superannuation

contributions

Defined Benefit Plan

Defined Benefit plan offers employees a plan with a benefit which is a known amount. The

further employer, as well as the employee, might make a contribution to the plan; along with

this, the employer is liable for any shortfall in contribution while ensuring guaranteed pension

benefits. It takes place in two varieties which are traditional pensions as well as cash-balance

plans (Topa, Lunceford and Boyatzis, 2017). A defined benefit plan is also called as a

pension; it is a promissory account for retirement by which the employer integrates all the

money deposits and ensures a set payout at the stage of retirement. Under this plan, a fixed

and pre-set benefit is formed by the employer for employees. Generally, the employee does a

valuation of fixed benefit offered. While the employer, a business can make a contribution to

the plan and thereby deduction every year. On the other hand, this type of retirement plan is

complex yet costly to create and manage as compared to another type of plan.

A defined benefit plan determines the particular benefit that will be paid to retire at the

retirement (Clark and Newhouse, 2016)t. Further, the retirement benefit is based on a given

formula that considers factors such as the working length of the employee, i.e., years of

service and the salary history of the employer.

Investment Choice Plan

A defined contribution plan, make no promises for a specified amount of benefit at the stage

of retirement. It is a retirement plan wherein both employers as well as the employee makes a

contribution on a frequent basis. Own and personal accounts are created for the employees

and benefits are totally based in on credit amount on the account through the contributions of

the employee, along with earnings of investments on the deposited account (Sialm, Starks

and Zhang, 2015). In this plan, fluctuations of future benefits are based on investment

earnings. Investment choice plan means a savings plan based on tax-deferred that individuals

financed with their individual's money instead of employers and utilized to secure for

retirement stage. The investment choice plan is a characteristic offered by a lot of

superannuation funds; this allows participants of super funds to make decision and choice on

the investment for their super money.

Factors that should be considered by tertiary sector employees for retirement planning

There are multiple factors affecting the benefits that cover the employee’s benefit from the

employer-sponsored retirement plan. In the side of definite benefit plan, the factors that can

impact are inclusive of benefit formula, service length, pre-retirement earnings and retirement

age (Rejda, 2015). On the side of investment choice plan, the factors are inclusive of

investment earnings and contribution amounts.

In any retirement plan, the more early an employee retires, the much smaller the benefit they

will get. In the investment choice plan, the retirement benefit is limited to the worth of the

participant account (Drucker, 2017). In a situation where an employee retires at an earlier

stage, then they will not be able to attain further contributions. The retirement plan sponsored

by the organization is either defined benefit or defined contribution.

The money earned on the type of retirement plan has a main impact on the retirement benefit.

By considering the defined benefit plan, the employer is generally liable for the contribution

of sufficient money in their account to the made payment of defined benefit at the phase of

retirement (Beehr and Bennett, 2015). The defined benefit plan, the entire retirement plan is

service and the salary history of the employer.

Investment Choice Plan

A defined contribution plan, make no promises for a specified amount of benefit at the stage

of retirement. It is a retirement plan wherein both employers as well as the employee makes a

contribution on a frequent basis. Own and personal accounts are created for the employees

and benefits are totally based in on credit amount on the account through the contributions of

the employee, along with earnings of investments on the deposited account (Sialm, Starks

and Zhang, 2015). In this plan, fluctuations of future benefits are based on investment

earnings. Investment choice plan means a savings plan based on tax-deferred that individuals

financed with their individual's money instead of employers and utilized to secure for

retirement stage. The investment choice plan is a characteristic offered by a lot of

superannuation funds; this allows participants of super funds to make decision and choice on

the investment for their super money.

Factors that should be considered by tertiary sector employees for retirement planning

There are multiple factors affecting the benefits that cover the employee’s benefit from the

employer-sponsored retirement plan. In the side of definite benefit plan, the factors that can

impact are inclusive of benefit formula, service length, pre-retirement earnings and retirement

age (Rejda, 2015). On the side of investment choice plan, the factors are inclusive of

investment earnings and contribution amounts.

In any retirement plan, the more early an employee retires, the much smaller the benefit they

will get. In the investment choice plan, the retirement benefit is limited to the worth of the

participant account (Drucker, 2017). In a situation where an employee retires at an earlier

stage, then they will not be able to attain further contributions. The retirement plan sponsored

by the organization is either defined benefit or defined contribution.

The money earned on the type of retirement plan has a main impact on the retirement benefit.

By considering the defined benefit plan, the employer is generally liable for the contribution

of sufficient money in their account to the made payment of defined benefit at the phase of

retirement (Beehr and Bennett, 2015). The defined benefit plan, the entire retirement plan is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

employer-sponsored, and the associated risk and management of portfolio are completely

borne and controlled by the organization.

There are some of the factors that can have a direct and indirect impact on the contributions

which are higher payment than expected, lower return on investment than expected, lower

interest rate than expected, changes in the requirement of federal and recruitment of new

employee (Henretta, 2018). In addition, employees must also consider their future goals,

wherein they must consider that whether their financial obligations and targets are satisfying

or not. Along with this, employees must also consider their future expenses alongside, on the

basis of this they must make a decision whether they want the pension in lump-sum or in

instalments.

Issues to be considered in the decision-making process of

retirement planning

Time value of money

The time value of money is the most basic and integral theory in financial aspects and depicts

that a dollar is highly worthwhile today as compared to the dollar of at a later date. It is

because the dollar can be now invested in order to gain interest on the dame, and the earned

interest can be put on reinvestment to gain more interest, and the process will be continued to

earn higher returns which are known as compounding interest (Findley and Caliendo, 2015).

This concept is vital while planning for retirement; it is because when the retiree makes a

decision of investment is probably the most significant aspect in the size of their nest egg at

retirement.

The concept of time value is applicable to every area of financial planning and can be

implemented while identifying capital budgeting. Further, it is a crucial element of capital

budgeting and the NPV approach, as it picturizes a better image in front of investors about

the returns and benefits on investment and retirement plans. Particular differences of TVM

of money computation are Net Present Value, Present Value and Future Value.

In accordance with the time value of money concept, money is entirely based on time; the

earlier an individual will invest the money, the more valuable and beneficial the investment

money will (Earl, Bednall and Muratore, 2015). It can be seen as; if the money is invested

now by the employee, then they will be entitled to earn interests or returns on the invested

borne and controlled by the organization.

There are some of the factors that can have a direct and indirect impact on the contributions

which are higher payment than expected, lower return on investment than expected, lower

interest rate than expected, changes in the requirement of federal and recruitment of new

employee (Henretta, 2018). In addition, employees must also consider their future goals,

wherein they must consider that whether their financial obligations and targets are satisfying

or not. Along with this, employees must also consider their future expenses alongside, on the

basis of this they must make a decision whether they want the pension in lump-sum or in

instalments.

Issues to be considered in the decision-making process of

retirement planning

Time value of money

The time value of money is the most basic and integral theory in financial aspects and depicts

that a dollar is highly worthwhile today as compared to the dollar of at a later date. It is

because the dollar can be now invested in order to gain interest on the dame, and the earned

interest can be put on reinvestment to gain more interest, and the process will be continued to

earn higher returns which are known as compounding interest (Findley and Caliendo, 2015).

This concept is vital while planning for retirement; it is because when the retiree makes a

decision of investment is probably the most significant aspect in the size of their nest egg at

retirement.

The concept of time value is applicable to every area of financial planning and can be

implemented while identifying capital budgeting. Further, it is a crucial element of capital

budgeting and the NPV approach, as it picturizes a better image in front of investors about

the returns and benefits on investment and retirement plans. Particular differences of TVM

of money computation are Net Present Value, Present Value and Future Value.

In accordance with the time value of money concept, money is entirely based on time; the

earlier an individual will invest the money, the more valuable and beneficial the investment

money will (Earl, Bednall and Muratore, 2015). It can be seen as; if the money is invested

now by the employee, then they will be entitled to earn interests or returns on the invested

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

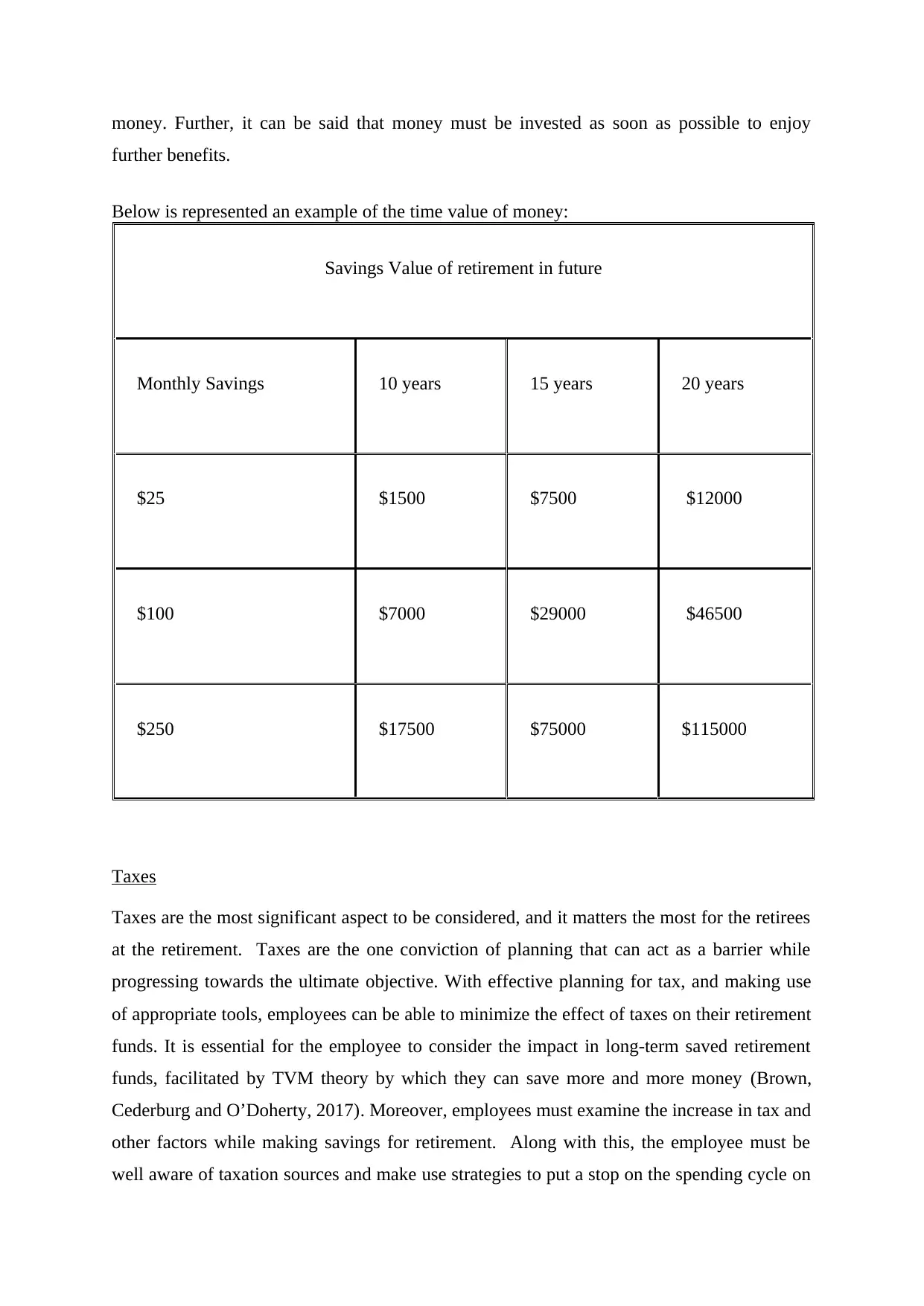

money. Further, it can be said that money must be invested as soon as possible to enjoy

further benefits.

Below is represented an example of the time value of money:

Savings Value of retirement in future

Monthly Savings 10 years 15 years 20 years

$25 $1500 $7500 $12000

$100 $7000 $29000 $46500

$250 $17500 $75000 $115000

Taxes

Taxes are the most significant aspect to be considered, and it matters the most for the retirees

at the retirement. Taxes are the one conviction of planning that can act as a barrier while

progressing towards the ultimate objective. With effective planning for tax, and making use

of appropriate tools, employees can be able to minimize the effect of taxes on their retirement

funds. It is essential for the employee to consider the impact in long-term saved retirement

funds, facilitated by TVM theory by which they can save more and more money (Brown,

Cederburg and O’Doherty, 2017). Moreover, employees must examine the increase in tax and

other factors while making savings for retirement. Along with this, the employee must be

well aware of taxation sources and make use strategies to put a stop on the spending cycle on

further benefits.

Below is represented an example of the time value of money:

Savings Value of retirement in future

Monthly Savings 10 years 15 years 20 years

$25 $1500 $7500 $12000

$100 $7000 $29000 $46500

$250 $17500 $75000 $115000

Taxes

Taxes are the most significant aspect to be considered, and it matters the most for the retirees

at the retirement. Taxes are the one conviction of planning that can act as a barrier while

progressing towards the ultimate objective. With effective planning for tax, and making use

of appropriate tools, employees can be able to minimize the effect of taxes on their retirement

funds. It is essential for the employee to consider the impact in long-term saved retirement

funds, facilitated by TVM theory by which they can save more and more money (Brown,

Cederburg and O’Doherty, 2017). Moreover, employees must examine the increase in tax and

other factors while making savings for retirement. Along with this, the employee must be

well aware of taxation sources and make use strategies to put a stop on the spending cycle on

taxes. The amount obtained as superannuation fund is exempted from tax obligation, in case

the amount is payable to an employee in the event of death, in against of or as annuity and

retirement.

The compounding power has a great effect on taxes. It is significant for the employee to

make use of investment accounts which are sponsored by the government like IRAs highly

while conducting the retirement plan, as they will generally afford the benefits of tax-deferred

payments (Dalton, Dalton and Cangelosi, 2016). It is important for the employee to save as

much as for retirement and as soon as possible while taking full benefit of available tax

related opportunities.

Inflation

Inflation affects every type of retirement plan, and it has a larger impact on long-term

workings and savings, so it is essential to adjust the savings in order to prevent the impact of

inflation which can decrease the value of saved money. Inflation affects in making a

reduction in purchasing power, as when the prices for products and services increases rapidly

than the deposited money in the account, then the money will have the value to but lesser and

lesser products and services over the period of time (Hanna and Kim, 2017). Thus, an

investor is required to sure to have enough retirement income in order to satisfy own

expenses. Moreover, inflation also consumer the savings or deposits rapidly, while

identifying the yearly retirement budget, one needs to effectively adjust the funds and

associated costs to make sure that investor has enough money to satisfy their financial targets

and goals.

Inflation is the factor which must be given high consideration while saving money for

retirement, as this risk can threaten the secured money in near future. This affects the money

by reducing its value, by considering this aspect tertiary employees must consider the risk of

inflation before making an investment in a retirement plan (Wakeman, Tashman and Yan,

2016). Appropriate measures must be taken into account so as to ensure anti-inflation pension

plan.

Other related factors

Risks: Risk variable in the Defined benefit plan is less or no, it is because the risk is bear by

organization or employee as the plan is sponsored by them. Further, in defined benefit plan

the amount is payable to an employee in the event of death, in against of or as annuity and

retirement.

The compounding power has a great effect on taxes. It is significant for the employee to

make use of investment accounts which are sponsored by the government like IRAs highly

while conducting the retirement plan, as they will generally afford the benefits of tax-deferred

payments (Dalton, Dalton and Cangelosi, 2016). It is important for the employee to save as

much as for retirement and as soon as possible while taking full benefit of available tax

related opportunities.

Inflation

Inflation affects every type of retirement plan, and it has a larger impact on long-term

workings and savings, so it is essential to adjust the savings in order to prevent the impact of

inflation which can decrease the value of saved money. Inflation affects in making a

reduction in purchasing power, as when the prices for products and services increases rapidly

than the deposited money in the account, then the money will have the value to but lesser and

lesser products and services over the period of time (Hanna and Kim, 2017). Thus, an

investor is required to sure to have enough retirement income in order to satisfy own

expenses. Moreover, inflation also consumer the savings or deposits rapidly, while

identifying the yearly retirement budget, one needs to effectively adjust the funds and

associated costs to make sure that investor has enough money to satisfy their financial targets

and goals.

Inflation is the factor which must be given high consideration while saving money for

retirement, as this risk can threaten the secured money in near future. This affects the money

by reducing its value, by considering this aspect tertiary employees must consider the risk of

inflation before making an investment in a retirement plan (Wakeman, Tashman and Yan,

2016). Appropriate measures must be taken into account so as to ensure anti-inflation pension

plan.

Other related factors

Risks: Risk variable in the Defined benefit plan is less or no, it is because the risk is bear by

organization or employee as the plan is sponsored by them. Further, in defined benefit plan

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the risk is relatively low, but it required effective planning and strategies in order to prevent

risk is arises. Employees who do not want to face any risk with their plan, then they must

choose defined benefit plan as this will ensure in properly safeguarding their deposits and

pensions (Wang and Shi, 2014). On the other hand, the investment choice plan has associated

risk, as the contribution of the plan is based on the employee, and also employee is unknown

about how much benefit they will get in future. The plan is also entitled to tax, and the

employee is not aware of the fact whether they will receive the desired benefit or not.

Investment earning and progress:

The performance and earnings on investments are also essential factors to be considered, to

know that the invested money is worthwhile or not. This can be done by considering the

benefits and progress of the plan; if the investment seems beneficial, then the investor must

carry on the same process (Beshears and et al., 2015). On the other hand, if the investment

seems non-effective, then the investor must stop making more investment in the plan, rather

than this they must choose another option to secure their life savings.

On the basis of the present study, the conclusion can be drawn that both the plans are best in

their own way, but it the based on the willingness of the employee to choose one of them.

However, according to the study, it can be suggested that tertiary employees must go for

defined benefit plan, as the amount is fixed and the employee knew how much benefit they

will receive and the most important thing it is risk-free.

risk is arises. Employees who do not want to face any risk with their plan, then they must

choose defined benefit plan as this will ensure in properly safeguarding their deposits and

pensions (Wang and Shi, 2014). On the other hand, the investment choice plan has associated

risk, as the contribution of the plan is based on the employee, and also employee is unknown

about how much benefit they will get in future. The plan is also entitled to tax, and the

employee is not aware of the fact whether they will receive the desired benefit or not.

Investment earning and progress:

The performance and earnings on investments are also essential factors to be considered, to

know that the invested money is worthwhile or not. This can be done by considering the

benefits and progress of the plan; if the investment seems beneficial, then the investor must

carry on the same process (Beshears and et al., 2015). On the other hand, if the investment

seems non-effective, then the investor must stop making more investment in the plan, rather

than this they must choose another option to secure their life savings.

On the basis of the present study, the conclusion can be drawn that both the plans are best in

their own way, but it the based on the willingness of the employee to choose one of them.

However, according to the study, it can be suggested that tertiary employees must go for

defined benefit plan, as the amount is fixed and the employee knew how much benefit they

will receive and the most important thing it is risk-free.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Beehr, T.A. and Bennett, M.M., 2015. Working after retirement: Features of bridge

employment and research directions. Work, Aging and Retirement, 1(1), pp.112-128.

Beshears, J., Choi, J.J., Laibson, D., Madrian, B.C. and Milkman, K.L., 2015. The effect of

providing peer information on retirement savings decisions. The Journal of finance, 70(3),

pp.1161-1201.

Brown, D.C., Cedarburg, S. and O’Doherty, M.S., 2017. Tax uncertainty and retirement

savings diversification. Journal of Financial Economics, 126(3), pp.689-712.

Dalton, J.F., Dalton, M.A. and Cangelosi, R.R., 2016. Retirement planning and employee

benefits. Money Education (Me).

Drucker, P.F., 2017. The pension fund revolution. Routledge.

Earl, J.K., Bednall, T.C. and Muratore, A.M., 2015. A matter of time: Why some people plan

for retirement and others do not. Work, Aging and Retirement, 1(2), pp.181-189.

Findley, T.S. and Caliendo, F.N., 2015. Time inconsistency and retirement

choice. Economics Letters, 129, pp.4-8.

Hanna, S.D. and Kim, K.T., 2017. Treatment of Inflation in Retirement Planning

Calculations: An Improved Method. Journal of Financial Planning, 30(1), pp.44-53.

Henretta, J.C., 2018. The life-course perspective on work and retirement. In Lives in Time

and Place and Invitation to the Life Course (pp. 85-105). Routledge.

Rejda, G.E., 2015. Social insurance and economic security. Routledge.

Sialm, C., Starks, L.T. and Zhang, H., 2015. Defined contribution pension plans: Sticky or

discerning money?. The Journal of Finance, 70(2), pp.805-838.

Topa, G., Lunceford, G. and Boyatzis, R.E.D., 2017. Financial planning for retirement: A

psychosocial perspective. Frontiers in Psychology, 8, p.2338.

Clark, R.L. and Newhouse, J.P., 2016. Challenges are facing public retirement plans. Journal

of Pension Economics & Finance, 15(3), p.249.

Wakeman, L.K., Tashman, A. and Yan, F., FINMASON Inc, 2016. Systems and methods for

retirement planning. U.S. Patent Application 15/075,613.

Wang, M. and Shi, J., 2014. Psychological research on retirement. Annual review of

psychology, 65, pp.209-233.

Beehr, T.A. and Bennett, M.M., 2015. Working after retirement: Features of bridge

employment and research directions. Work, Aging and Retirement, 1(1), pp.112-128.

Beshears, J., Choi, J.J., Laibson, D., Madrian, B.C. and Milkman, K.L., 2015. The effect of

providing peer information on retirement savings decisions. The Journal of finance, 70(3),

pp.1161-1201.

Brown, D.C., Cedarburg, S. and O’Doherty, M.S., 2017. Tax uncertainty and retirement

savings diversification. Journal of Financial Economics, 126(3), pp.689-712.

Dalton, J.F., Dalton, M.A. and Cangelosi, R.R., 2016. Retirement planning and employee

benefits. Money Education (Me).

Drucker, P.F., 2017. The pension fund revolution. Routledge.

Earl, J.K., Bednall, T.C. and Muratore, A.M., 2015. A matter of time: Why some people plan

for retirement and others do not. Work, Aging and Retirement, 1(2), pp.181-189.

Findley, T.S. and Caliendo, F.N., 2015. Time inconsistency and retirement

choice. Economics Letters, 129, pp.4-8.

Hanna, S.D. and Kim, K.T., 2017. Treatment of Inflation in Retirement Planning

Calculations: An Improved Method. Journal of Financial Planning, 30(1), pp.44-53.

Henretta, J.C., 2018. The life-course perspective on work and retirement. In Lives in Time

and Place and Invitation to the Life Course (pp. 85-105). Routledge.

Rejda, G.E., 2015. Social insurance and economic security. Routledge.

Sialm, C., Starks, L.T. and Zhang, H., 2015. Defined contribution pension plans: Sticky or

discerning money?. The Journal of Finance, 70(2), pp.805-838.

Topa, G., Lunceford, G. and Boyatzis, R.E.D., 2017. Financial planning for retirement: A

psychosocial perspective. Frontiers in Psychology, 8, p.2338.

Clark, R.L. and Newhouse, J.P., 2016. Challenges are facing public retirement plans. Journal

of Pension Economics & Finance, 15(3), p.249.

Wakeman, L.K., Tashman, A. and Yan, F., FINMASON Inc, 2016. Systems and methods for

retirement planning. U.S. Patent Application 15/075,613.

Wang, M. and Shi, J., 2014. Psychological research on retirement. Annual review of

psychology, 65, pp.209-233.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.