BUSI 201 Project: Building a Retirement Plan with Excel Formulas

VerifiedAdded on 2023/06/09

|3

|668

|76

Project

AI Summary

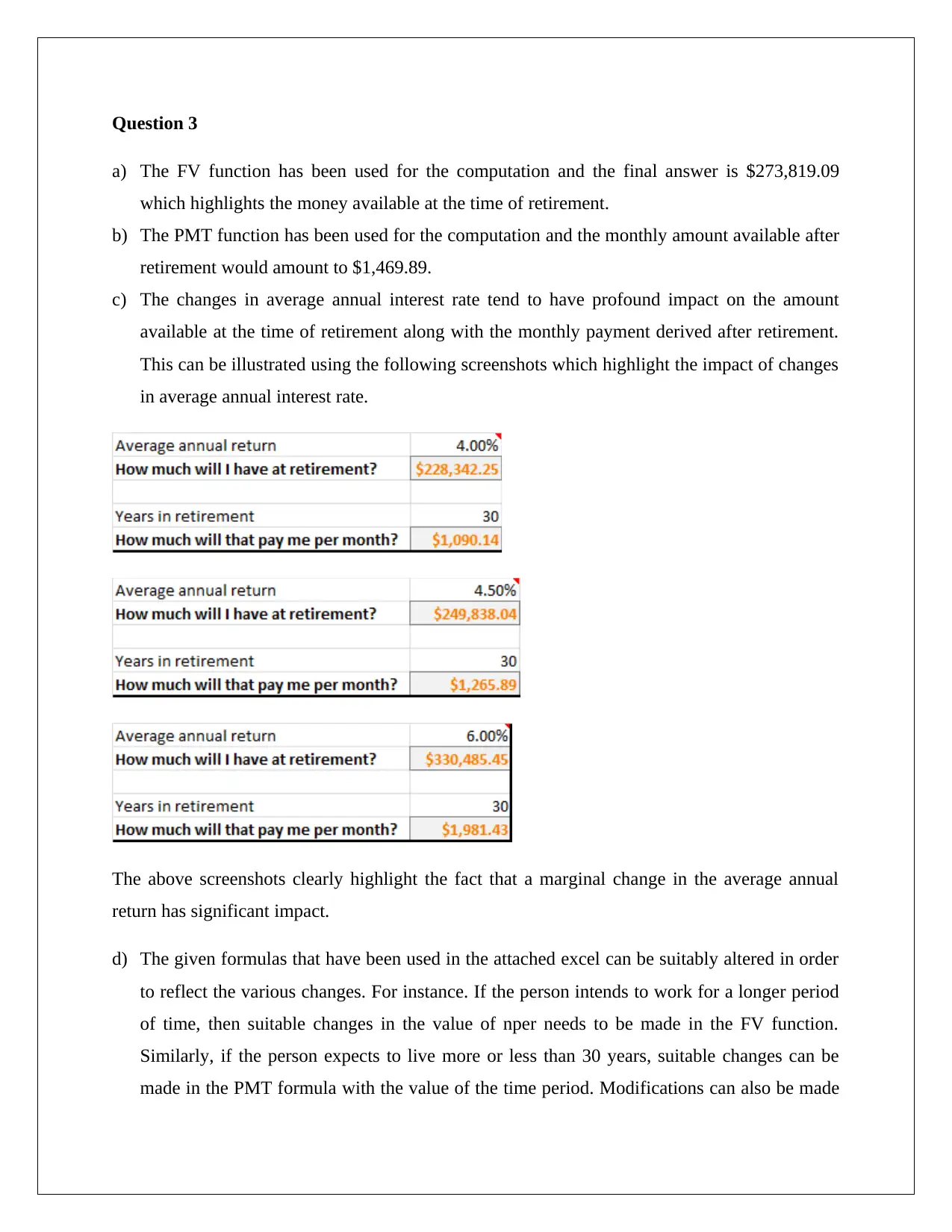

This project utilizes Microsoft Excel to create a retirement plan for an employee, focusing on calculating retirement savings and potential monthly withdrawals. The solution employs Excel functions like FV and PMT to determine the future value of retirement funds and the monthly income post-retirement. It examines the impact of varying interest rates on retirement outcomes and discusses how to modify formulas to accommodate different scenarios, such as changes in work duration or inheritance. Key assumptions, such as a constant annual interest rate and consistent salary, are outlined. The project emphasizes the importance of savings rates, early planning, and the role of Excel as a planning tool, referencing financial management principles and practices. It highlights the need to consider tax implications and retirement objectives when determining contribution amounts, and the role of Excel in helping employees objectively plan for retirement and meet their financial goals. This resource is available on Desklib, where students can find more solved assignments and past papers.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.