Written Assignment: Superannuation and Retirement Planning (DFP3)

VerifiedAdded on 2022/12/15

|78

|19591

|125

Homework Assignment

AI Summary

This document is a written assignment for the Superannuation and Retirement Advice (DFP3v6) course, designed to be submitted with an Oral A assignment and audio recording. The assignment focuses on a case study involving Nathan and Mary Davidson, a couple seeking retirement planning advice. It requires students to establish a relationship with the client, analyze their financial situation, develop appropriate strategies, address client concerns about superannuation, present solutions, and agree on a financial plan. The assignment includes a fact finder, cash flow templates, and managed funds calculations, with a strong emphasis on demonstrating competency in financial planning, superannuation advice, and ongoing service. The document provides detailed instructions, a sample case study, and grading criteria, offering students a comprehensive framework for completing the assignment and preparing a Statement of Advice (SOA). Students must demonstrate a reasonable attempt to answer all questions and are graded based on their ability to demonstrate competence in key areas. The assignment covers all the required units of competency and provides students with an opportunity to develop and implement financial plans, provide superannuation advice, and offer ongoing service to clients.

Written Assignment

Superannuation and Retirement Planning

(DFP3_AS_v6A1)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Written assignment result (assessor to complete)

Result — first submission (details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary(assessor to complete)

First submission Resubmission (if required)

Section 1 Not yet demonstrated Not yet demonstrated

Section2 Not yet demonstrated Not yet demonstrated

Section3 Not yet demonstrated Not yet demonstrated

Section4 Not yet demonstrated Not yet demonstrated

Section 5 Not yet demonstrated Not yet demonstrated

Feedback(assessor to complete)

[insert assessor feedback]

DFP3_AS_v6A1

Superannuation and Retirement Planning

(DFP3_AS_v6A1)

Student identification (student to complete)

Please complete the fields shaded grey.

Student number

Written assignment result (assessor to complete)

Result — first submission (details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary(assessor to complete)

First submission Resubmission (if required)

Section 1 Not yet demonstrated Not yet demonstrated

Section2 Not yet demonstrated Not yet demonstrated

Section3 Not yet demonstrated Not yet demonstrated

Section4 Not yet demonstrated Not yet demonstrated

Section 5 Not yet demonstrated Not yet demonstrated

Feedback(assessor to complete)

[insert assessor feedback]

DFP3_AS_v6A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Before you begin

Read everything in this document before you start your written assignment for Superannuation and

Retirement Advice (DFP3v6).

About this document

This document is the written assignment, to be submitted with your Oral A assignment with audio

recording. These assessments must be submitted before submitting your Oral B assignment.

This document includes the following:

• Instructions for completing and submitting this assignment.

• Assignment sections (including factfinder templates, cash flow templates and managed funds

calculations).

– Section 1: Establish the relationship with the client and identify their objectives, needs and

financial situation.

– Section 2: Analyse client objectives, needs, financial situation and risk profile to develop

appropriate strategies and solutions.

– Section 3: Address clients’ questions and concerns about superannuation matters.

– Section 4: Present appropriate strategies and solutions to the client and negotiate a financial plan,

policy or transaction. Provide ongoing service where requested by the client.

– Section 5: Agree on the plan, policy or transaction.

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Superannuation and

Retirement Advice (DFP3v6) subject room. You must submit and complete your oral A assignment,

audio recording, written assignment and exam, prior to you commencing and submitting your oral B

assignment and audio recording. We strongly suggest completing your oral A assignment and audio

recording, written assignment and exam in Week 10 and once completed, to then commence and submit

oral B assignment and audio recording no later than Week 12.

Page 2 of 78

Read everything in this document before you start your written assignment for Superannuation and

Retirement Advice (DFP3v6).

About this document

This document is the written assignment, to be submitted with your Oral A assignment with audio

recording. These assessments must be submitted before submitting your Oral B assignment.

This document includes the following:

• Instructions for completing and submitting this assignment.

• Assignment sections (including factfinder templates, cash flow templates and managed funds

calculations).

– Section 1: Establish the relationship with the client and identify their objectives, needs and

financial situation.

– Section 2: Analyse client objectives, needs, financial situation and risk profile to develop

appropriate strategies and solutions.

– Section 3: Address clients’ questions and concerns about superannuation matters.

– Section 4: Present appropriate strategies and solutions to the client and negotiate a financial plan,

policy or transaction. Provide ongoing service where requested by the client.

– Section 5: Agree on the plan, policy or transaction.

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Superannuation and

Retirement Advice (DFP3v6) subject room. You must submit and complete your oral A assignment,

audio recording, written assignment and exam, prior to you commencing and submitting your oral B

assignment and audio recording. We strongly suggest completing your oral A assignment and audio

recording, written assignment and exam in Week 10 and once completed, to then commence and submit

oral B assignment and audio recording no later than Week 12.

Page 2 of 78

How to use the sample case study and SOA in KapLearn

The sample case study provides a model to help you prepare your SOA for this assignment. The case study

explains the process that is undertaken to develop the SOA with reference to an example and it is a very

useful resource. Download the sample SOA and refer to it as you work through the learning materials for

this subject.

Before you start work on this assignment, go back to the sample SOA and:

• compare how the SOA matches with the goals and objectives identified in the case study

• consider what information has been included in the SOA

• consider why this information has been included.

This exercise will help you prepare an SOA for this assignment that addresses your client’s goals.

Please bear in mind that not all SOAs are exactly alike in their construction, but all have common heading

topics within them. Accordingly, there may be minor differences between the sample SOA and the SOA

template in this assignment. However, all the required compliance elements will be included in both

formats.

Page 3 of 78

The sample case study provides a model to help you prepare your SOA for this assignment. The case study

explains the process that is undertaken to develop the SOA with reference to an example and it is a very

useful resource. Download the sample SOA and refer to it as you work through the learning materials for

this subject.

Before you start work on this assignment, go back to the sample SOA and:

• compare how the SOA matches with the goals and objectives identified in the case study

• consider what information has been included in the SOA

• consider why this information has been included.

This exercise will help you prepare an SOA for this assignment that addresses your client’s goals.

Please bear in mind that not all SOAs are exactly alike in their construction, but all have common heading

topics within them. Accordingly, there may be minor differences between the sample SOA and the SOA

template in this assignment. However, all the required compliance elements will be included in both

formats.

Page 3 of 78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Instructions for completing and submitting this written

assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DFP3_AS_v6_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The written assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB for the Written and Oral AAssignment. Once you submit your written

assignment for marking you will be unable to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions (pdf) in the Assessment section of

KapLearn for details on how to submit your written assignment.

Refer to your study guide so you can plan ahead to complete your audio recording before the written and

oral A assignment is due.

Note: The written assignment (in Word), oral A assignment (in Word) and audio recording must all be

submitted together.

The written assignment marking process

Please note: You have 12 weeks from the date of your enrolment in this subject to submit your

completed oral A assignment and audio recording, written assignment, exam and oral B assignment and

audio recording.

Page 4 of 78

assignment

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your work

regularly.

• Use the template provided, as other formats will not be accepted for these assignments.

• Name your file as follows: Studentnumber_SubjectCode_Assignment_versionnumber_Submissionnumber

(e.g. 12345678_DFP3_AS_v6_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the written assignment

Only Microsoft Office compatible written assignments submitted in the template file will be accepted for

marking by Kaplan Professional Education. You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The written assignment must be completed before submitting it to Kaplan Professional Education.

Incomplete written assignments will be returned to you unmarked.

The maximum file size is 20MB for the Written and Oral AAssignment. Once you submit your written

assignment for marking you will be unable to make any further changes to it.

You are able to submit your written assignment earlier than the deadline if you are confident you have

completed all parts and have prepared a quality submission.

Please refer to the Assignment submission/resubmission instructions (pdf) in the Assessment section of

KapLearn for details on how to submit your written assignment.

Refer to your study guide so you can plan ahead to complete your audio recording before the written and

oral A assignment is due.

Note: The written assignment (in Word), oral A assignment (in Word) and audio recording must all be

submitted together.

The written assignment marking process

Please note: You have 12 weeks from the date of your enrolment in this subject to submit your

completed oral A assignment and audio recording, written assignment, exam and oral B assignment and

audio recording.

Page 4 of 78

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

You must submit and complete your oral A assignment, audio recording, written assignment and exam,

prior to you commencing and submitting your oral B assignment and audio recording. We strongly

suggest completing your oral A assignment and audio recording, written assignment and exam in Week 10

and once completed, to then commence and submit oral B assignment and audio recording no later than

Week 12.

If you reach the end of your initial enrolment period and have been deemed ‘Not Yet demonstrated’ in one

or more assessment items, then an additional four (4) weeks will be granted, provided you attempted all

assessment tasks during the initial enrolment period. Please note, you must complete all the assessments

in Oral A assignment, audio recording, written assignment and exam prior to commencing and submitting

your Oral B assignment and audio recording.

Your assessor will mark your assignments and return them to you in the subject room in KapLearn under

the ‘Written and Oral Assessment’ page.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore, you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral A assignment.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required

knowledge and/or skills for each subject. As a result, you will be graded as either ’demonstrated’ or

‘not yet demonstrated’.

Your assessor will follow the below process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed to be ‘demonstrated’ in all assessment items in order to be awarded the units of

competency in this subject, including:

• all of the exam questions

• the written and oral A and oral B assignment.

Page 5 of 78

prior to you commencing and submitting your oral B assignment and audio recording. We strongly

suggest completing your oral A assignment and audio recording, written assignment and exam in Week 10

and once completed, to then commence and submit oral B assignment and audio recording no later than

Week 12.

If you reach the end of your initial enrolment period and have been deemed ‘Not Yet demonstrated’ in one

or more assessment items, then an additional four (4) weeks will be granted, provided you attempted all

assessment tasks during the initial enrolment period. Please note, you must complete all the assessments

in Oral A assignment, audio recording, written assignment and exam prior to commencing and submitting

your Oral B assignment and audio recording.

Your assessor will mark your assignments and return them to you in the subject room in KapLearn under

the ‘Written and Oral Assessment’ page.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your written assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore, you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your submission

deadline to submit your completed written and oral A assignment.

How your written assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required

knowledge and/or skills for each subject. As a result, you will be graded as either ’demonstrated’ or

‘not yet demonstrated’.

Your assessor will follow the below process when marking your written assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall

competence.

You must be deemed to be ‘demonstrated’ in all assessment items in order to be awarded the units of

competency in this subject, including:

• all of the exam questions

• the written and oral A and oral B assignment.

Page 5 of 78

‘Not yet demonstrated’ and resubmissions

Should sections of your assignment be marked as ‘not yet demonstrated’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet demonstrated’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against these units:

FNSFPL503 Develop and prepare financial plan

FNSFPL504 Implement financial plan

FNSFPL505 Review financial plans and provide ongoing service

FNSASICU503 Provide advice in superannuation

FNSASICZ503 Provide advice in financial planning

We are here to help

If you have any questions about this written assignment, you can post your query at the ‘Ask your Tutor’

forum in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or student support staff.

Page 6 of 78

Should sections of your assignment be marked as ‘not yet demonstrated’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet demonstrated’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This written assignment is your opportunity to demonstrate your competency against these units:

FNSFPL503 Develop and prepare financial plan

FNSFPL504 Implement financial plan

FNSFPL505 Review financial plans and provide ongoing service

FNSASICU503 Provide advice in superannuation

FNSASICZ503 Provide advice in financial planning

We are here to help

If you have any questions about this written assignment, you can post your query at the ‘Ask your Tutor’

forum in your subject room. You can expect an answer within 24 hours of your posting from one of our

technical advisers or student support staff.

Page 6 of 78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Case study — Nathan and Mary Davidson

You are a financial planner for AFS licensee EANWB Financial Planning. Nathan and Mary Davidson have

been undertaking their own research into planning their retirement, and recently attended one of your

firm’s retirement seminars. After this seminar they spoke with you about their concerns that they may not

accumulate enough money in superannuation to fund their retirement.

You met with them and during your initial meeting you provided them with some basic information,

including a fact finder for them to fill out. You then organised a second meeting, at which you collected

more information on their current financial situation and spent time clarifying their needs and objectives.

A summary of their financial situation,based on your interviews with the clients,is provided below.

The completed fact finder,including the risk profile questionnaire,can be found on page 11 of this

assignment.

Current situation

Nathan, age 54, and Mary, age 52, are married and have two children, Jonathan and Sarah, who are nearing

the end of their schooling.

They own their own home, valued at $600,000, and have recently received an inheritance from the estate

of Mary’s mother.

Although theyhave cleared their mortgage,they still have access to a redraw facility of $100,000.

However, they do not want to access this unless there is as an emergency.

Nathan is a full-time sales representative for an agricultural supplies company. He earns $140,000 annually

plus superannuation guarantee (SG) contributions from his employer paid into the employer’s default fund.

Mary is primarily a self-employed marketing consultant and has business income net of expenses of

$65,000 annually. She also works as a contracted employee in a mining engineering company. Her hours

vary, but typically she earns about $5,600 annually, plus SG which is paid into the employer’s default fund.

Jonathan and Sarah attend a private school and Nathan and Mary pay a total of $7,000 annually in fees,

uniforms, books, school trips etc.

The only other assets they have are their two cars.

Superannuation

Nathan has $270,000 in his superannuation fund and Mary has $99,000. They are both invested in the

default balanced option. Further details of their superannuation are in the fact find (Appendix 1).

Neither Nathan nor Mary has made any personal contributions to their superannuation fund.

Nathan’s employer will allow salary sacrificing to superannuation without impacting on any other employee

benefits and will maintain his SG contribution based on his pre-salary sacrifice income.

Mary’s employer will not allow her to salary sacrifice to superannuation, but does make SG contributions to

her superannuation fund.

Nathan and Mary are happy with their current superannuation funds and the underlying investments

they are invested in. They do not wish to receive advice in regard to changing their funds or

investment portfolios.

Page 7 of 78

You are a financial planner for AFS licensee EANWB Financial Planning. Nathan and Mary Davidson have

been undertaking their own research into planning their retirement, and recently attended one of your

firm’s retirement seminars. After this seminar they spoke with you about their concerns that they may not

accumulate enough money in superannuation to fund their retirement.

You met with them and during your initial meeting you provided them with some basic information,

including a fact finder for them to fill out. You then organised a second meeting, at which you collected

more information on their current financial situation and spent time clarifying their needs and objectives.

A summary of their financial situation,based on your interviews with the clients,is provided below.

The completed fact finder,including the risk profile questionnaire,can be found on page 11 of this

assignment.

Current situation

Nathan, age 54, and Mary, age 52, are married and have two children, Jonathan and Sarah, who are nearing

the end of their schooling.

They own their own home, valued at $600,000, and have recently received an inheritance from the estate

of Mary’s mother.

Although theyhave cleared their mortgage,they still have access to a redraw facility of $100,000.

However, they do not want to access this unless there is as an emergency.

Nathan is a full-time sales representative for an agricultural supplies company. He earns $140,000 annually

plus superannuation guarantee (SG) contributions from his employer paid into the employer’s default fund.

Mary is primarily a self-employed marketing consultant and has business income net of expenses of

$65,000 annually. She also works as a contracted employee in a mining engineering company. Her hours

vary, but typically she earns about $5,600 annually, plus SG which is paid into the employer’s default fund.

Jonathan and Sarah attend a private school and Nathan and Mary pay a total of $7,000 annually in fees,

uniforms, books, school trips etc.

The only other assets they have are their two cars.

Superannuation

Nathan has $270,000 in his superannuation fund and Mary has $99,000. They are both invested in the

default balanced option. Further details of their superannuation are in the fact find (Appendix 1).

Neither Nathan nor Mary has made any personal contributions to their superannuation fund.

Nathan’s employer will allow salary sacrificing to superannuation without impacting on any other employee

benefits and will maintain his SG contribution based on his pre-salary sacrifice income.

Mary’s employer will not allow her to salary sacrifice to superannuation, but does make SG contributions to

her superannuation fund.

Nathan and Mary are happy with their current superannuation funds and the underlying investments

they are invested in. They do not wish to receive advice in regard to changing their funds or

investment portfolios.

Page 7 of 78

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Insurance

Nathan and Mary’s their life insurance and total and permanent disability (TPD) insurance are owned by

their superannuation funds.

Nathan and Mary both have self-owned trauma policies and income protection policies. Mary also has

business overheads insurance.

Their cars are comprehensively insured and they have home building and contents insurance cover

including legal liability cover.

Nathan and Mary have family private health insurance cover.

Further details on their insurance policies are in the fact find.

They have specifically stated that they do not require any advice on their insurance policies.

Investments

Nathan and Mary have not had any investments other than their superannuation. Surplus income had been

used to pay off their mortgage.

However, they do have $350,000 in their savings account that was left over from the inheritance from

Mary’s mother’s estate after paying off their mortgage. This savings account, which is their bank’s ordinary

transaction account, does not pay any interest.

Other information

Nathan and Mary have a credit card with a limit of $30,000 that they use for all their general expenses

and entertainment. However, they never spend up to their limit and their average expenses are

$7,500 per month, which they repay within the interest-free period.

Nathan and Mary take regular annual holidays with their children, and spend approximately $10,000 per

trip.

Other expenses include deductible charity donations of $1,220 and accountant’s expenses of $500

annually.

Needs and objectives

Nathan and Mary are concerned they will not have enough money to provide an adequate income in

retirement. They do not want to rely on the age pension and would like to be fully self-sufficient if possible.

After your initial meeting with them, they reviewed their situation and decided they would like you to

prepare advice using a retirement income of $80,000 a year (in today’s dollars). They based this figure on

their current spending after deleting items that will not apply after retirement (such as school fees) and

considering their desired lifestyle in retirement. They have used their bank’s ‘Retirement Projector’ and

determined that if they live to age 95 and earn 4% (net of inflation) on their investments, they will need

almost $1.3 million in retirement savings when Nathan is age 65.

Nathan and Mary would like to channel their surplus income into their retirement planning now that they

do not owe anything on their mortgage.

Page 8 of 78

Nathan and Mary’s their life insurance and total and permanent disability (TPD) insurance are owned by

their superannuation funds.

Nathan and Mary both have self-owned trauma policies and income protection policies. Mary also has

business overheads insurance.

Their cars are comprehensively insured and they have home building and contents insurance cover

including legal liability cover.

Nathan and Mary have family private health insurance cover.

Further details on their insurance policies are in the fact find.

They have specifically stated that they do not require any advice on their insurance policies.

Investments

Nathan and Mary have not had any investments other than their superannuation. Surplus income had been

used to pay off their mortgage.

However, they do have $350,000 in their savings account that was left over from the inheritance from

Mary’s mother’s estate after paying off their mortgage. This savings account, which is their bank’s ordinary

transaction account, does not pay any interest.

Other information

Nathan and Mary have a credit card with a limit of $30,000 that they use for all their general expenses

and entertainment. However, they never spend up to their limit and their average expenses are

$7,500 per month, which they repay within the interest-free period.

Nathan and Mary take regular annual holidays with their children, and spend approximately $10,000 per

trip.

Other expenses include deductible charity donations of $1,220 and accountant’s expenses of $500

annually.

Needs and objectives

Nathan and Mary are concerned they will not have enough money to provide an adequate income in

retirement. They do not want to rely on the age pension and would like to be fully self-sufficient if possible.

After your initial meeting with them, they reviewed their situation and decided they would like you to

prepare advice using a retirement income of $80,000 a year (in today’s dollars). They based this figure on

their current spending after deleting items that will not apply after retirement (such as school fees) and

considering their desired lifestyle in retirement. They have used their bank’s ‘Retirement Projector’ and

determined that if they live to age 95 and earn 4% (net of inflation) on their investments, they will need

almost $1.3 million in retirement savings when Nathan is age 65.

Nathan and Mary would like to channel their surplus income into their retirement planning now that they

do not owe anything on their mortgage.

Page 8 of 78

They have ‘parked’ the inheritance money in their savings account and plan to retain $50,000 in a secure

investment to support the children in their last years at school and into university. They want to invest the

balance in a tax-effective way, and are considering adding it to Mary’s superannuation to help her

‘catch up’ because she earns less than Nathan and took time out of the workforce to raise the children

when they were young.

Like most people, they would also like to reduce their overall tax liability.

Closing the interview

Before concluding your meeting, you review the information Nathan and Mary provided to check that it is

complete and accurate and ask if they have any questions.

Nathan and Mary understand from their own research that there are many ways to add money to their

superannuation, but are confused about which will be the most appropriate for them.

You advise Nathan and Mary what happens next and explain that, with their agreement, you will prepare a

written report based on the information they have shared with you, which will include recommended

strategies to help them toachieve their financial goal of having adequate funds for retirement.

Nathan and Mary agree to proceed to the next stage of the financial planning process and you make an

appointment to present the plan in a fortnight.

As their financial planner, your task is to prepare a statement of advice (SOA) that will include strategies to

meet Nathan and Mary’s goals.

Page 9 of 78

investment to support the children in their last years at school and into university. They want to invest the

balance in a tax-effective way, and are considering adding it to Mary’s superannuation to help her

‘catch up’ because she earns less than Nathan and took time out of the workforce to raise the children

when they were young.

Like most people, they would also like to reduce their overall tax liability.

Closing the interview

Before concluding your meeting, you review the information Nathan and Mary provided to check that it is

complete and accurate and ask if they have any questions.

Nathan and Mary understand from their own research that there are many ways to add money to their

superannuation, but are confused about which will be the most appropriate for them.

You advise Nathan and Mary what happens next and explain that, with their agreement, you will prepare a

written report based on the information they have shared with you, which will include recommended

strategies to help them toachieve their financial goal of having adequate funds for retirement.

Nathan and Mary agree to proceed to the next stage of the financial planning process and you make an

appointment to present the plan in a fortnight.

As their financial planner, your task is to prepare a statement of advice (SOA) that will include strategies to

meet Nathan and Mary’s goals.

Page 9 of 78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

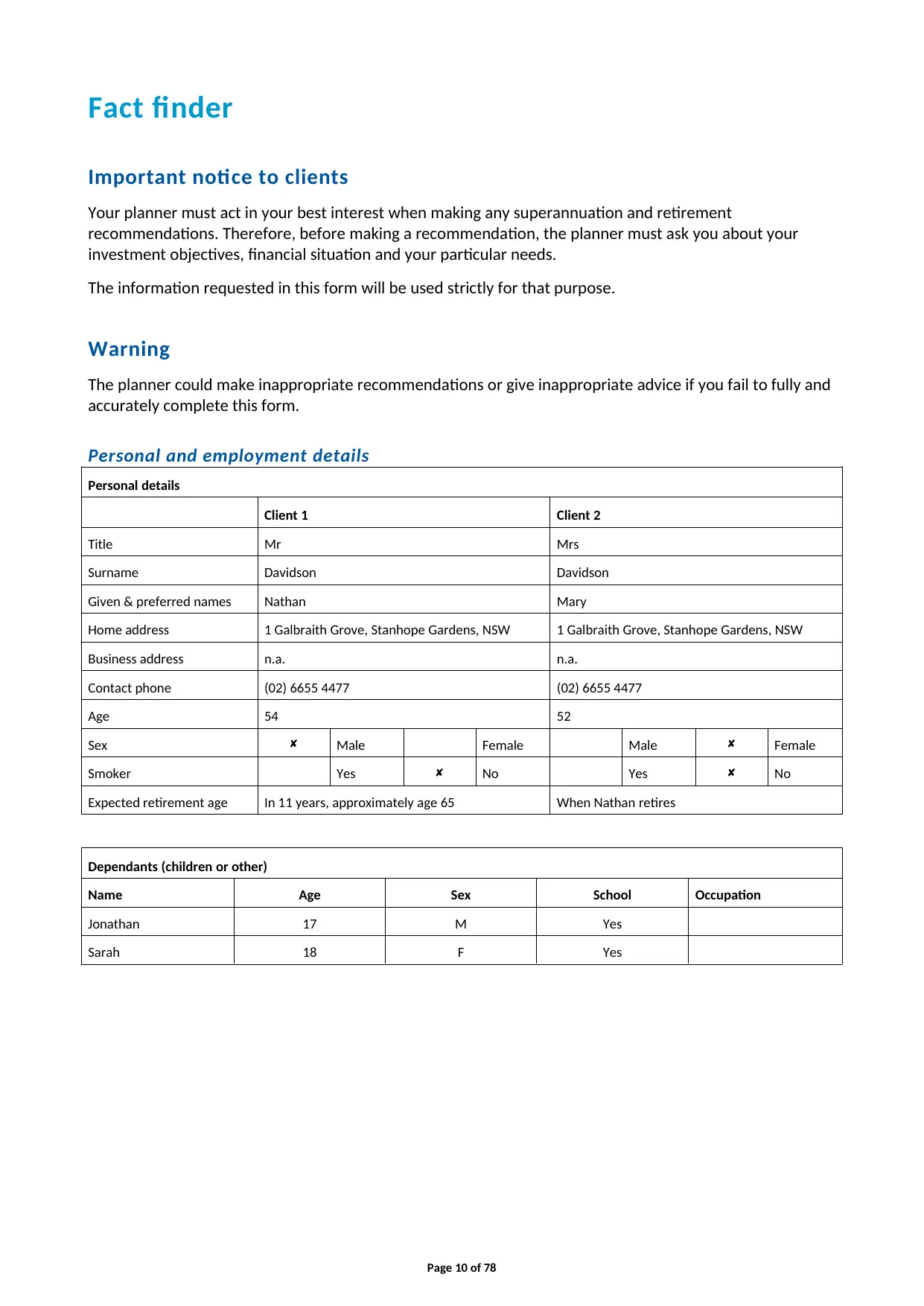

Fact finder

Important notice to clients

Your planner must act in your best interest when making any superannuation and retirement

recommendations. Therefore, before making a recommendation, the planner must ask you about your

investment objectives, financial situation and your particular needs.

The information requested in this form will be used strictly for that purpose.

Warning

The planner could make inappropriate recommendations or give inappropriate advice if you fail to fully and

accurately complete this form.

Personal and employment details

Personal details

Client 1 Client 2

Title Mr Mrs

Surname Davidson Davidson

Given & preferred names Nathan Mary

Home address 1 Galbraith Grove, Stanhope Gardens, NSW 1 Galbraith Grove, Stanhope Gardens, NSW

Business address n.a. n.a.

Contact phone (02) 6655 4477 (02) 6655 4477

Age 54 52

Sex Male Female Male Female

Smoker Yes No Yes No

Expected retirement age In 11 years, approximately age 65 When Nathan retires

Dependants (children or other)

Name Age Sex School Occupation

Jonathan 17 M Yes

Sarah 18 F Yes

Page 10 of 78

Important notice to clients

Your planner must act in your best interest when making any superannuation and retirement

recommendations. Therefore, before making a recommendation, the planner must ask you about your

investment objectives, financial situation and your particular needs.

The information requested in this form will be used strictly for that purpose.

Warning

The planner could make inappropriate recommendations or give inappropriate advice if you fail to fully and

accurately complete this form.

Personal and employment details

Personal details

Client 1 Client 2

Title Mr Mrs

Surname Davidson Davidson

Given & preferred names Nathan Mary

Home address 1 Galbraith Grove, Stanhope Gardens, NSW 1 Galbraith Grove, Stanhope Gardens, NSW

Business address n.a. n.a.

Contact phone (02) 6655 4477 (02) 6655 4477

Age 54 52

Sex Male Female Male Female

Smoker Yes No Yes No

Expected retirement age In 11 years, approximately age 65 When Nathan retires

Dependants (children or other)

Name Age Sex School Occupation

Jonathan 17 M Yes

Sarah 18 F Yes

Page 10 of 78

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

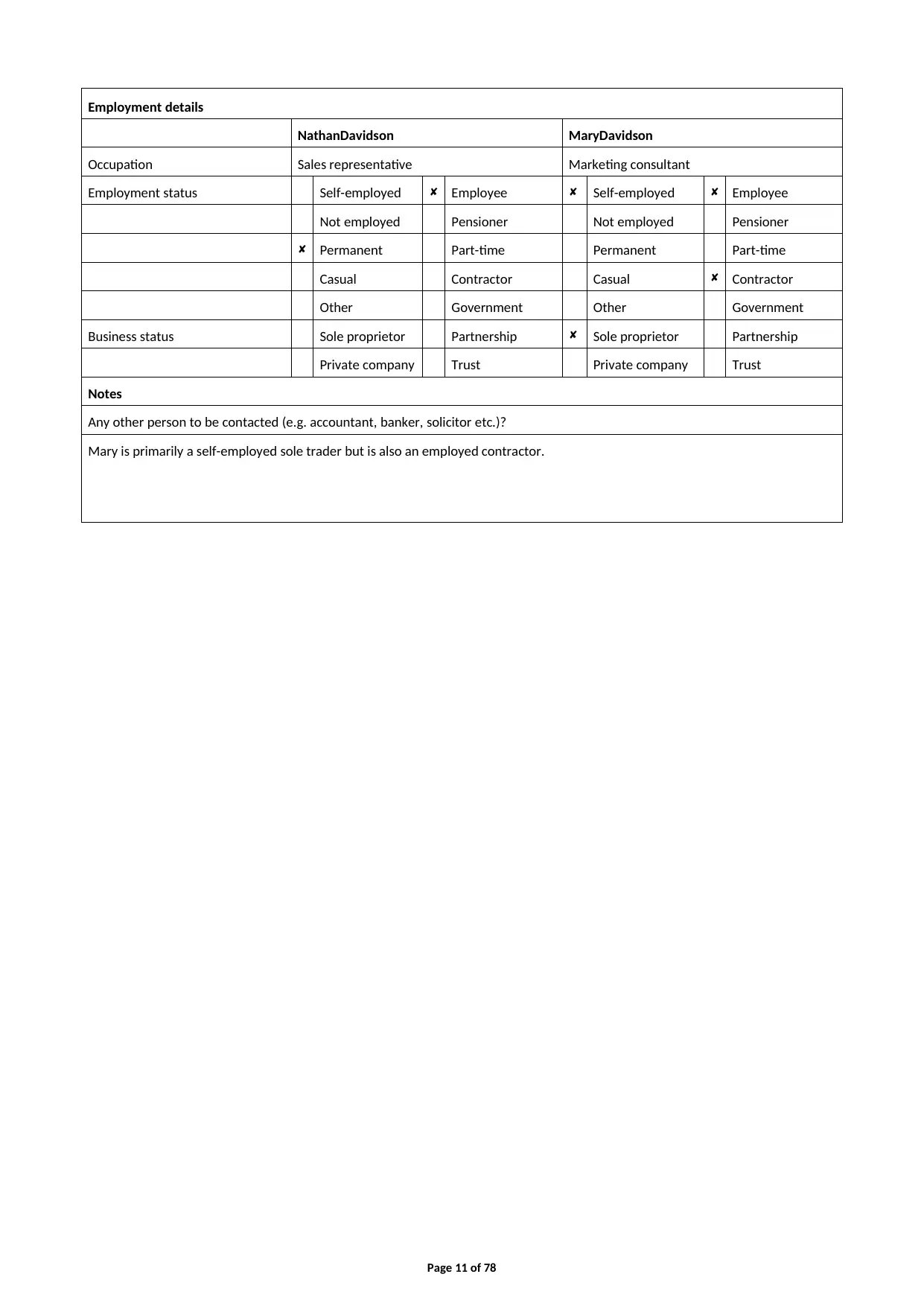

Employment details

NathanDavidson MaryDavidson

Occupation Sales representative Marketing consultant

Employment status Self-employed Employee Self-employed Employee

Not employed Pensioner Not employed Pensioner

Permanent Part-time Permanent Part-time

Casual Contractor Casual Contractor

Other Government Other Government

Business status Sole proprietor Partnership Sole proprietor Partnership

Private company Trust Private company Trust

Notes

Any other person to be contacted (e.g. accountant, banker, solicitor etc.)?

Mary is primarily a self-employed sole trader but is also an employed contractor.

Page 11 of 78

NathanDavidson MaryDavidson

Occupation Sales representative Marketing consultant

Employment status Self-employed Employee Self-employed Employee

Not employed Pensioner Not employed Pensioner

Permanent Part-time Permanent Part-time

Casual Contractor Casual Contractor

Other Government Other Government

Business status Sole proprietor Partnership Sole proprietor Partnership

Private company Trust Private company Trust

Notes

Any other person to be contacted (e.g. accountant, banker, solicitor etc.)?

Mary is primarily a self-employed sole trader but is also an employed contractor.

Page 11 of 78

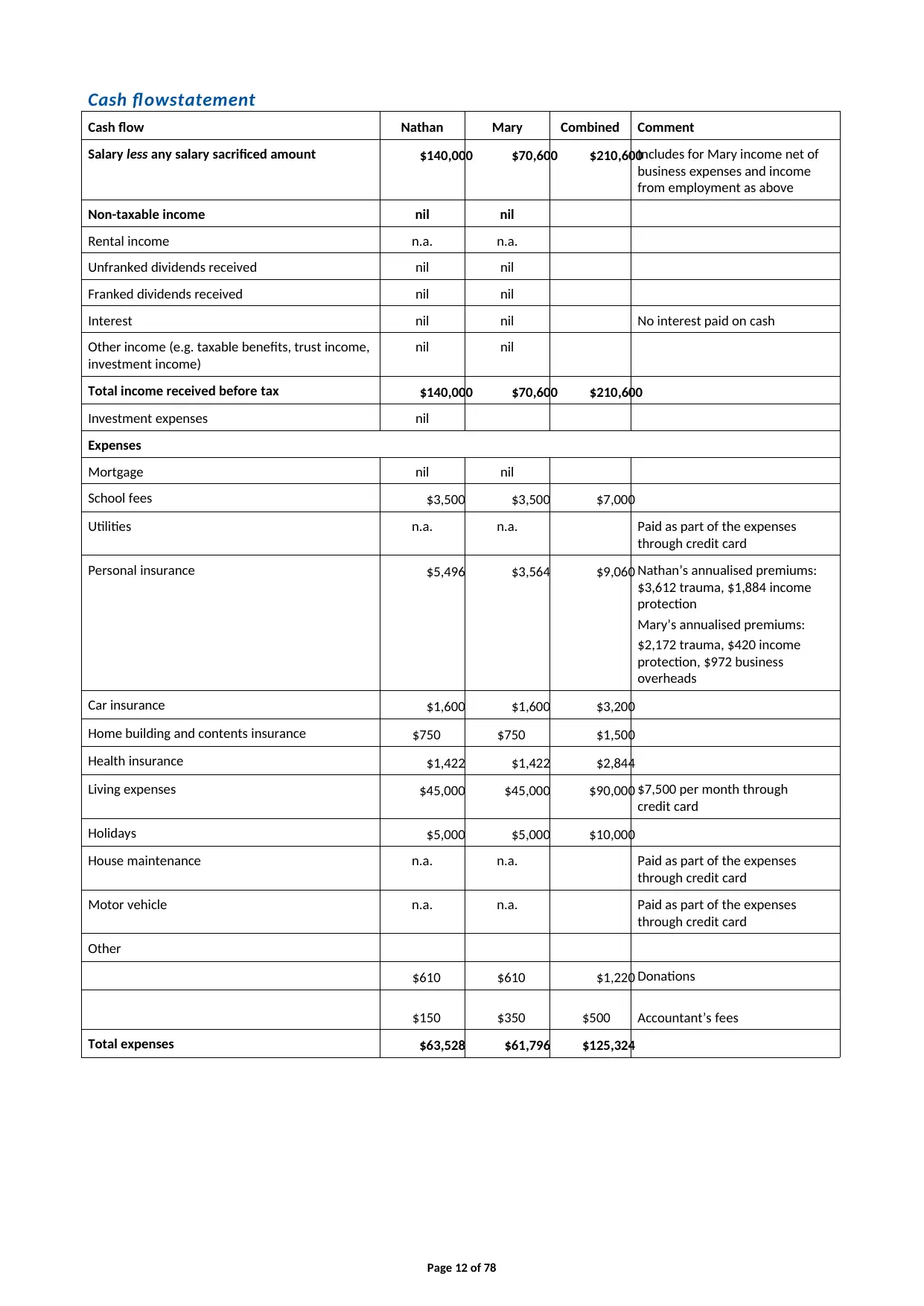

Cash flowstatement

Cash flow Nathan Mary Combined Comment

Salary less any salary sacrificed amount $140,000 $70,600 $210,600Includes for Mary income net of

business expenses and income

from employment as above

Non-taxable income nil nil

Rental income n.a. n.a.

Unfranked dividends received nil nil

Franked dividends received nil nil

Interest nil nil No interest paid on cash

Other income (e.g. taxable benefits, trust income,

investment income)

nil nil

Total income received before tax $140,000 $70,600 $210,600

Investment expenses nil

Expenses

Mortgage nil nil

School fees $3,500 $3,500 $7,000

Utilities n.a. n.a. Paid as part of the expenses

through credit card

Personal insurance $5,496 $3,564 $9,060 Nathan’s annualised premiums:

$3,612 trauma, $1,884 income

protection

Mary’s annualised premiums:

$2,172 trauma, $420 income

protection, $972 business

overheads

Car insurance $1,600 $1,600 $3,200

Home building and contents insurance $750 $750 $1,500

Health insurance $1,422 $1,422 $2,844

Living expenses $45,000 $45,000 $90,000 $7,500 per month through

credit card

Holidays $5,000 $5,000 $10,000

House maintenance n.a. n.a. Paid as part of the expenses

through credit card

Motor vehicle n.a. n.a. Paid as part of the expenses

through credit card

Other

$610 $610 $1,220 Donations

$150 $350 $500 Accountant’s fees

Total expenses $63,528 $61,796 $125,324

Page 12 of 78

Cash flow Nathan Mary Combined Comment

Salary less any salary sacrificed amount $140,000 $70,600 $210,600Includes for Mary income net of

business expenses and income

from employment as above

Non-taxable income nil nil

Rental income n.a. n.a.

Unfranked dividends received nil nil

Franked dividends received nil nil

Interest nil nil No interest paid on cash

Other income (e.g. taxable benefits, trust income,

investment income)

nil nil

Total income received before tax $140,000 $70,600 $210,600

Investment expenses nil

Expenses

Mortgage nil nil

School fees $3,500 $3,500 $7,000

Utilities n.a. n.a. Paid as part of the expenses

through credit card

Personal insurance $5,496 $3,564 $9,060 Nathan’s annualised premiums:

$3,612 trauma, $1,884 income

protection

Mary’s annualised premiums:

$2,172 trauma, $420 income

protection, $972 business

overheads

Car insurance $1,600 $1,600 $3,200

Home building and contents insurance $750 $750 $1,500

Health insurance $1,422 $1,422 $2,844

Living expenses $45,000 $45,000 $90,000 $7,500 per month through

credit card

Holidays $5,000 $5,000 $10,000

House maintenance n.a. n.a. Paid as part of the expenses

through credit card

Motor vehicle n.a. n.a. Paid as part of the expenses

through credit card

Other

$610 $610 $1,220 Donations

$150 $350 $500 Accountant’s fees

Total expenses $63,528 $61,796 $125,324

Page 12 of 78

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 78

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.