ACCT20073 - Revaluations, Impairment Testing of Non-Current Assets

VerifiedAdded on 2023/04/17

|11

|2737

|184

Report

AI Summary

This report provides a detailed analysis of asset revaluations and impairment testing of non-current assets, addressing key concepts under accounting standards like AASB 13 and AASB 136, as well as US GAAP and IFRS. It discusses the adoption of the fair value concept, its benefits in improving financial statements and eliminating the need for depreciation, and compares impairment testing requirements under US GAAP and IFRS. The report also examines fair value measurement as per AASB 13, including disclosures related to asset valuation and impairment testing, using Medibank health insurance as an example. It further explains the process of impairment testing, the identification of recoverable amounts, and the grouping of assets for cash flow determination, highlighting the treatment of goodwill and other intangible assets. The assignment solution explores the practical implications of these accounting principles in real-world scenarios.

Running Head: REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT

ASSETS

REVALUATIONS AND IMPAIRMENT OF NON – CURRENT ASSETS

Name of the Student:

Name of the University:

Author’s note:

ASSETS

REVALUATIONS AND IMPAIRMENT OF NON – CURRENT ASSETS

Name of the Student:

Name of the University:

Author’s note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

Table of contents

In response to Question 1...........................................................................................................2

In response to Question 2...........................................................................................................2

In response to Question 3...........................................................................................................3

Reference list..............................................................................................................................9

Table of contents

In response to Question 1...........................................................................................................2

In response to Question 2...........................................................................................................2

In response to Question 3...........................................................................................................3

Reference list..............................................................................................................................9

2REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

In response to Question 1

Simba Ltd has come up with the adoption of revaluation model for the fixed assets but

the model has some limitations like the fair value of certain items cannot be determined. In

order to deal with this problem the director of Simba Ltd has put forward the proposal of

adopting the fair value concept as this tends to improve the scenario of the company’s

financial position and can eliminate the need of depreciation. The board should adopt the

proposal of the director because the fair market value concept is based on the current

information derived from the market (Goncharov, Riedl & Sellhorn 2014). The fair market

value concept is considered as a modern concept of valuing the assets which does not follow

the historical cost concepts wherein the companies measured the values of the assets based on

the nominal cost (Müller, Riedl & Sellhorn 2015). Simba Ltd can avail several benefits by

adopting this proposal which is discussed in the following sections:

Improvement in the financial statements: In fair market valuation the assets are

valued at current market price which can increase the valuation of the assets recorded in the

balance sheet. This appreciation of assets enhances the company’s economic condition which

indicates that the company has maintained a good wealth management (Yamamoto, 2014).

The financial ratios are also enhanced due to the appreciation and hence ensures a better

financial report which reveals the true and fair information to the stakeholder’s of the

company (Barker, & Schulte 2017).

Elimination of need of depreciation: In a situation where the fair market value has

fallen below the book value the assets become the impaired assets and their accounts are

written down and hence the amount of depreciation is adjusted based on the carrying cost of

the impaired assets (Bepari, Rahman & Mollik 2014).

In response to Question 2

According to US GAAP, Impairment is considered as an accounting concept that

describes the reduction of company’s listed assets especially the fixed assets. While testing

the impairment the calculation of total profit, cash flows and other items are expected to

estimated using the book value method that is cost model or in other id words it can be said

the book value minus accumulated depreciation and impaired loss identified in the pat years

(Hamberg & Beisland 2014). As per IFRS the revaluation model is considered as an

accounting principle wherein the fixed assets that are recorded in the balance sheet at cost are

carrying over the fair market value based on the current market activities and it can increase

In response to Question 1

Simba Ltd has come up with the adoption of revaluation model for the fixed assets but

the model has some limitations like the fair value of certain items cannot be determined. In

order to deal with this problem the director of Simba Ltd has put forward the proposal of

adopting the fair value concept as this tends to improve the scenario of the company’s

financial position and can eliminate the need of depreciation. The board should adopt the

proposal of the director because the fair market value concept is based on the current

information derived from the market (Goncharov, Riedl & Sellhorn 2014). The fair market

value concept is considered as a modern concept of valuing the assets which does not follow

the historical cost concepts wherein the companies measured the values of the assets based on

the nominal cost (Müller, Riedl & Sellhorn 2015). Simba Ltd can avail several benefits by

adopting this proposal which is discussed in the following sections:

Improvement in the financial statements: In fair market valuation the assets are

valued at current market price which can increase the valuation of the assets recorded in the

balance sheet. This appreciation of assets enhances the company’s economic condition which

indicates that the company has maintained a good wealth management (Yamamoto, 2014).

The financial ratios are also enhanced due to the appreciation and hence ensures a better

financial report which reveals the true and fair information to the stakeholder’s of the

company (Barker, & Schulte 2017).

Elimination of need of depreciation: In a situation where the fair market value has

fallen below the book value the assets become the impaired assets and their accounts are

written down and hence the amount of depreciation is adjusted based on the carrying cost of

the impaired assets (Bepari, Rahman & Mollik 2014).

In response to Question 2

According to US GAAP, Impairment is considered as an accounting concept that

describes the reduction of company’s listed assets especially the fixed assets. While testing

the impairment the calculation of total profit, cash flows and other items are expected to

estimated using the book value method that is cost model or in other id words it can be said

the book value minus accumulated depreciation and impaired loss identified in the pat years

(Hamberg & Beisland 2014). As per IFRS the revaluation model is considered as an

accounting principle wherein the fixed assets that are recorded in the balance sheet at cost are

carrying over the fair market value based on the current market activities and it can increase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

and decrease the value of the assets (Bepari & Mollik 2015). The fair value of assets dictate

whether the carrying costs are adjusted up or down. For an instance depreciation of an

impaired capital assets based on carrying costs is dictated by the fair value because the

amount of the depreciation is adjusted and are carried forward in order to re estimate the total

amount based on the carrying cost of the impaired assets. In such a situation the test for

impairments is not necessary (Baboukardos & Rimmel 2014). Under the cost model it is a

compulsion to carry out the test or impaired assets in order to understand the significant

changes in the market price of the assets. According to US GAAP a business does not require

to impair its assets if the fair market value decreases but on the other hand as per IFRS after

the revaluation of book value of the fixed assets they can be adjusted to the market value

periodically by using both the models (Glau, Landsman & Wyrwa 2015.

In response to Question 3

(a). The fair value as per AASB 13 is a market based estimation and is not an entity

based measurement (Johansson, Hjelström & Hellman 2016). There are some assets and

liabilities for which the market information are available and some assets and liabilities for

which the information are not available the objective of fair market value in both the cases

will be same that is estimating the price in order to sell out the assets or transferring the

liabilities. The assets and liabilities that are estimated under fair market value are standalone

assets or liabilities or group of cash generating assets or liabilities (Griffin, 2014).

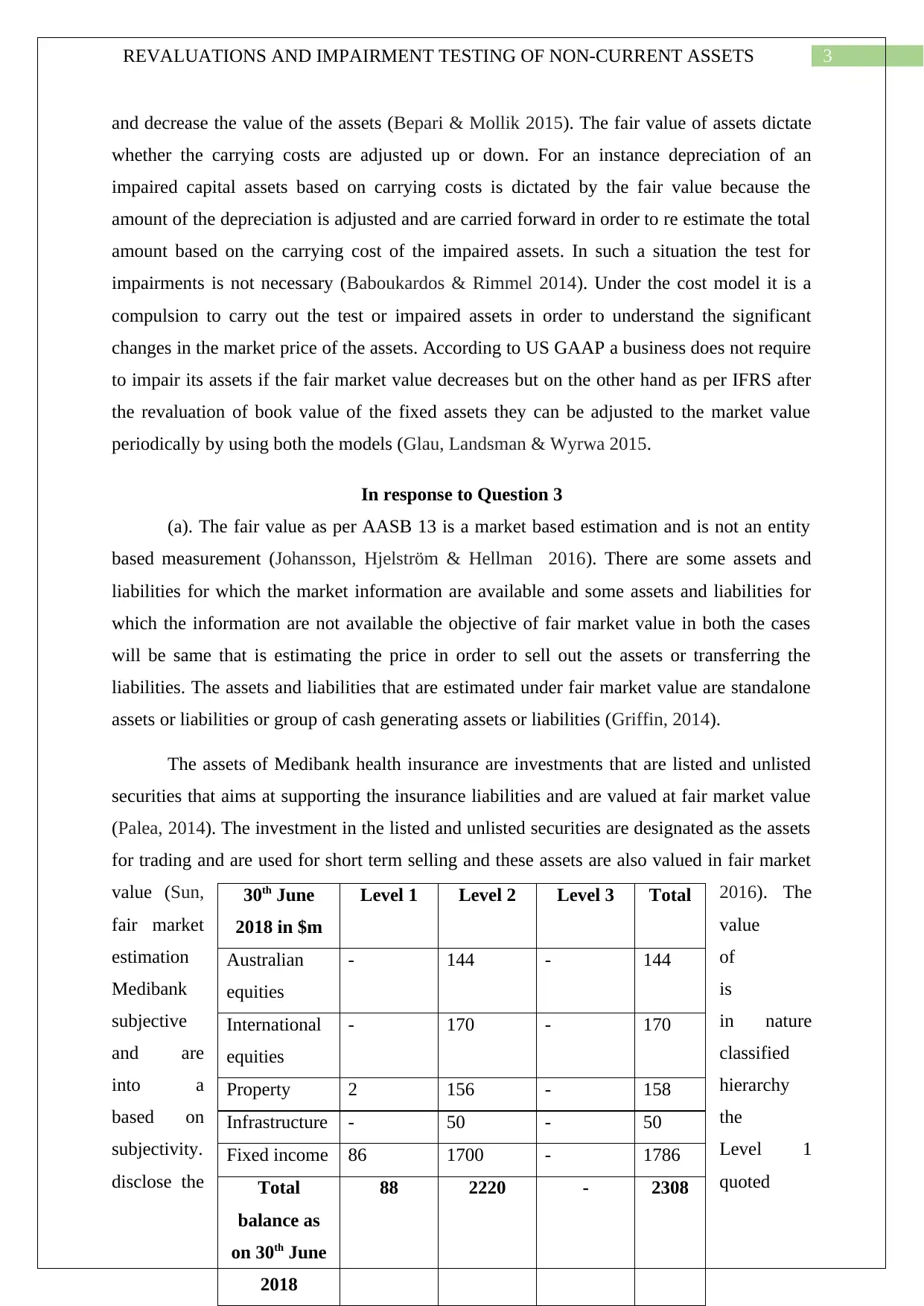

The assets of Medibank health insurance are investments that are listed and unlisted

securities that aims at supporting the insurance liabilities and are valued at fair market value

(Palea, 2014). The investment in the listed and unlisted securities are designated as the assets

for trading and are used for short term selling and these assets are also valued in fair market

value (Sun, 2016). The

fair market value

estimation of

Medibank is

subjective in nature

and are classified

into a hierarchy

based on the

subjectivity. Level 1

disclose the quoted

30th June

2018 in $m

Level 1 Level 2 Level 3 Total

Australian

equities

- 144 - 144

International

equities

- 170 - 170

Property 2 156 - 158

Infrastructure - 50 - 50

Fixed income 86 1700 - 1786

Total

balance as

on 30th June

2018

88 2220 - 2308

and decrease the value of the assets (Bepari & Mollik 2015). The fair value of assets dictate

whether the carrying costs are adjusted up or down. For an instance depreciation of an

impaired capital assets based on carrying costs is dictated by the fair value because the

amount of the depreciation is adjusted and are carried forward in order to re estimate the total

amount based on the carrying cost of the impaired assets. In such a situation the test for

impairments is not necessary (Baboukardos & Rimmel 2014). Under the cost model it is a

compulsion to carry out the test or impaired assets in order to understand the significant

changes in the market price of the assets. According to US GAAP a business does not require

to impair its assets if the fair market value decreases but on the other hand as per IFRS after

the revaluation of book value of the fixed assets they can be adjusted to the market value

periodically by using both the models (Glau, Landsman & Wyrwa 2015.

In response to Question 3

(a). The fair value as per AASB 13 is a market based estimation and is not an entity

based measurement (Johansson, Hjelström & Hellman 2016). There are some assets and

liabilities for which the market information are available and some assets and liabilities for

which the information are not available the objective of fair market value in both the cases

will be same that is estimating the price in order to sell out the assets or transferring the

liabilities. The assets and liabilities that are estimated under fair market value are standalone

assets or liabilities or group of cash generating assets or liabilities (Griffin, 2014).

The assets of Medibank health insurance are investments that are listed and unlisted

securities that aims at supporting the insurance liabilities and are valued at fair market value

(Palea, 2014). The investment in the listed and unlisted securities are designated as the assets

for trading and are used for short term selling and these assets are also valued in fair market

value (Sun, 2016). The

fair market value

estimation of

Medibank is

subjective in nature

and are classified

into a hierarchy

based on the

subjectivity. Level 1

disclose the quoted

30th June

2018 in $m

Level 1 Level 2 Level 3 Total

Australian

equities

- 144 - 144

International

equities

- 170 - 170

Property 2 156 - 158

Infrastructure - 50 - 50

Fixed income 86 1700 - 1786

Total

balance as

on 30th June

2018

88 2220 - 2308

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

prices for the identical assets and liabilities in the active market. Level 2 determines the

inputs other than the quoted prices directly or indirectly (Badia, et al. 2017). Level 3 discloses

the inputs for the assets or liabilities that are not related with the observable market

information.

Table 1: Medibank’s financial assets valued at fair value

Source: Created by learner

(b). The disclosures are made regarding the fair value measurement of the assets in the

financial reports (Caruso, Ferrari & Pisano 2016). The disclosures related to the fair value of

assets and information related to each group of assets are discussed below:

Basis for the calculation of the carrying amount.

The rates applied to the depreciation.

The methods that are used while depreciating the assets.

The calculation of gross carrying amount and the accumulated depreciation along

with the loss of impairment.

The restoration of the carrying amount at starting and ending period reveals :

1. Disposals

2. Additions

3. Business combinations acquisitions

prices for the identical assets and liabilities in the active market. Level 2 determines the

inputs other than the quoted prices directly or indirectly (Badia, et al. 2017). Level 3 discloses

the inputs for the assets or liabilities that are not related with the observable market

information.

Table 1: Medibank’s financial assets valued at fair value

Source: Created by learner

(b). The disclosures are made regarding the fair value measurement of the assets in the

financial reports (Caruso, Ferrari & Pisano 2016). The disclosures related to the fair value of

assets and information related to each group of assets are discussed below:

Basis for the calculation of the carrying amount.

The rates applied to the depreciation.

The methods that are used while depreciating the assets.

The calculation of gross carrying amount and the accumulated depreciation along

with the loss of impairment.

The restoration of the carrying amount at starting and ending period reveals :

1. Disposals

2. Additions

3. Business combinations acquisitions

5REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

4. Increase or decrease in revaluation

5. Depreciation

6. Impairment losses

7. The net amount of difference between foreign exchange rates

8. Others

Some additional disclosures are made regarding property, plant and equipment that are

required (as per IAS 16.77):

The effective date on which the revaluation made

Involvement of independent valuer

The class of properties that are applied for revaluation the carrying cost associated with

that would have been carried out following the cost model

The surplus arising from revaluation including the changes related to that period and

distribution of balance to the shareholders with some restrictions.

Additional disclosures as per IAS 16.74 are discussed below:

o The restrictions on the items and titles guaranteed as security for liability.

o Expenditures related to the construction of property, plant and other assets.

o Acquisition of property , plant and equipment as per the contractual commitment

o Compensation received from other parties related to the items of plant, equipment and

property that were subjected to impairment profit and loss.

Disclosures made by Medibank regarding the revaluation of assets in fair value are

related to net investment income (Paugam & Ramond 2015). Profits or losses that are

arising from the changes in the fair value of the “financial assets at fair value through

profit and loss” group are reflected in the statement of income within the net income

from investment in the time span in which they arise. Trust distribution income that is

derived at fair value from the financial assets are recognised in the consolidate income

statement through profit and loss and is considered as a part of investment income when

there will be establishment made by the group to receive the payments. The income that is

generated from the interest of financial assets are outstanding using the considered

method of calculation including in the investment.

(c). According to AASB 136 an asset is subjected for impairment when the carrying

value of the same exceeds the recoverable amount and as a result of that the impairment loss

4. Increase or decrease in revaluation

5. Depreciation

6. Impairment losses

7. The net amount of difference between foreign exchange rates

8. Others

Some additional disclosures are made regarding property, plant and equipment that are

required (as per IAS 16.77):

The effective date on which the revaluation made

Involvement of independent valuer

The class of properties that are applied for revaluation the carrying cost associated with

that would have been carried out following the cost model

The surplus arising from revaluation including the changes related to that period and

distribution of balance to the shareholders with some restrictions.

Additional disclosures as per IAS 16.74 are discussed below:

o The restrictions on the items and titles guaranteed as security for liability.

o Expenditures related to the construction of property, plant and other assets.

o Acquisition of property , plant and equipment as per the contractual commitment

o Compensation received from other parties related to the items of plant, equipment and

property that were subjected to impairment profit and loss.

Disclosures made by Medibank regarding the revaluation of assets in fair value are

related to net investment income (Paugam & Ramond 2015). Profits or losses that are

arising from the changes in the fair value of the “financial assets at fair value through

profit and loss” group are reflected in the statement of income within the net income

from investment in the time span in which they arise. Trust distribution income that is

derived at fair value from the financial assets are recognised in the consolidate income

statement through profit and loss and is considered as a part of investment income when

there will be establishment made by the group to receive the payments. The income that is

generated from the interest of financial assets are outstanding using the considered

method of calculation including in the investment.

(c). According to AASB 136 an asset is subjected for impairment when the carrying

value of the same exceeds the recoverable amount and as a result of that the impairment loss

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

occurs. An organization at the end of the reporting period should check whether there is any

indication related to the impairment of the asset. The entity should take into consideration

these few points related to the impairment of assets:

The test for impairment of asset has been made compulsory using the indefinite useful

life and by comparing the carrying amount of the assets with the recoverable amount.

The condition for performing this impairment test is it should be performed at same

time every year. There are several intangible assets in a business depending on the

types and if any intangible asset is recognized during the current period it is subjected

to the test at ends of the current period.

According to the paragraphs 80 – 99 of AASB 136 the goodwill is subjected to the

impairment test even though they are acquired at the time of business combination.

While assessing the assets for impairment test the entity should consider some sources of

information like:

The fluctuations in the market rates or rate of return on investments and their

impact on the discount rates that are used in estimating the value of the asset and

recoverable amount.

Checking the market capitalisation rate whether it is more than the carrying

amount of the assets.

The obsolescence or physical damage of the assets are supported by the evidence.

The economic performance of the asset is evidenced by internal reporting which

reveals how the assets performed in the financial year.

The significant changes in the assets in future that can impact its valuation is also

considered as a major issue because this can lead to restructuring of the operation

and reassessment of useful like of assets.

Impairment testing refers to the identification of the recoverable amount having

higher fair value. There are some assets for which the fair value is observed from market

information and for some the valuation model is used for the determination of the fair value

method. The test for impairment involves comparing the carrying amount with the

recoverable amount and hence this test ensures that the recoverable amount is exceeded by

the carrying value. According to AASB 136 the test of impairment is applied to the group of

assets which are considered as cash generating units compared to other assets in the balance

sheet. The goodwill is a cash generating unit and is impaired first along with a condition that

occurs. An organization at the end of the reporting period should check whether there is any

indication related to the impairment of the asset. The entity should take into consideration

these few points related to the impairment of assets:

The test for impairment of asset has been made compulsory using the indefinite useful

life and by comparing the carrying amount of the assets with the recoverable amount.

The condition for performing this impairment test is it should be performed at same

time every year. There are several intangible assets in a business depending on the

types and if any intangible asset is recognized during the current period it is subjected

to the test at ends of the current period.

According to the paragraphs 80 – 99 of AASB 136 the goodwill is subjected to the

impairment test even though they are acquired at the time of business combination.

While assessing the assets for impairment test the entity should consider some sources of

information like:

The fluctuations in the market rates or rate of return on investments and their

impact on the discount rates that are used in estimating the value of the asset and

recoverable amount.

Checking the market capitalisation rate whether it is more than the carrying

amount of the assets.

The obsolescence or physical damage of the assets are supported by the evidence.

The economic performance of the asset is evidenced by internal reporting which

reveals how the assets performed in the financial year.

The significant changes in the assets in future that can impact its valuation is also

considered as a major issue because this can lead to restructuring of the operation

and reassessment of useful like of assets.

Impairment testing refers to the identification of the recoverable amount having

higher fair value. There are some assets for which the fair value is observed from market

information and for some the valuation model is used for the determination of the fair value

method. The test for impairment involves comparing the carrying amount with the

recoverable amount and hence this test ensures that the recoverable amount is exceeded by

the carrying value. According to AASB 136 the test of impairment is applied to the group of

assets which are considered as cash generating units compared to other assets in the balance

sheet. The goodwill is a cash generating unit and is impaired first along with a condition that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

other cash generating units will be impaired following the pro rata basis (AASB 136, para

104). This condition sometimes creates trouble for the organization if there are numerous

cash generating assets. The accounts receivable and long term assets are also impaired and

the test of impairment to these assets are applied due to the longer span of time in carrying

value. Medibank’s impairment test for goodwill states that goodwill and other intangible

assets are subjected to amortisation and impairment test. The impairment loss is identified by

Medibank when the carrying value exceeds the recoverable amount.

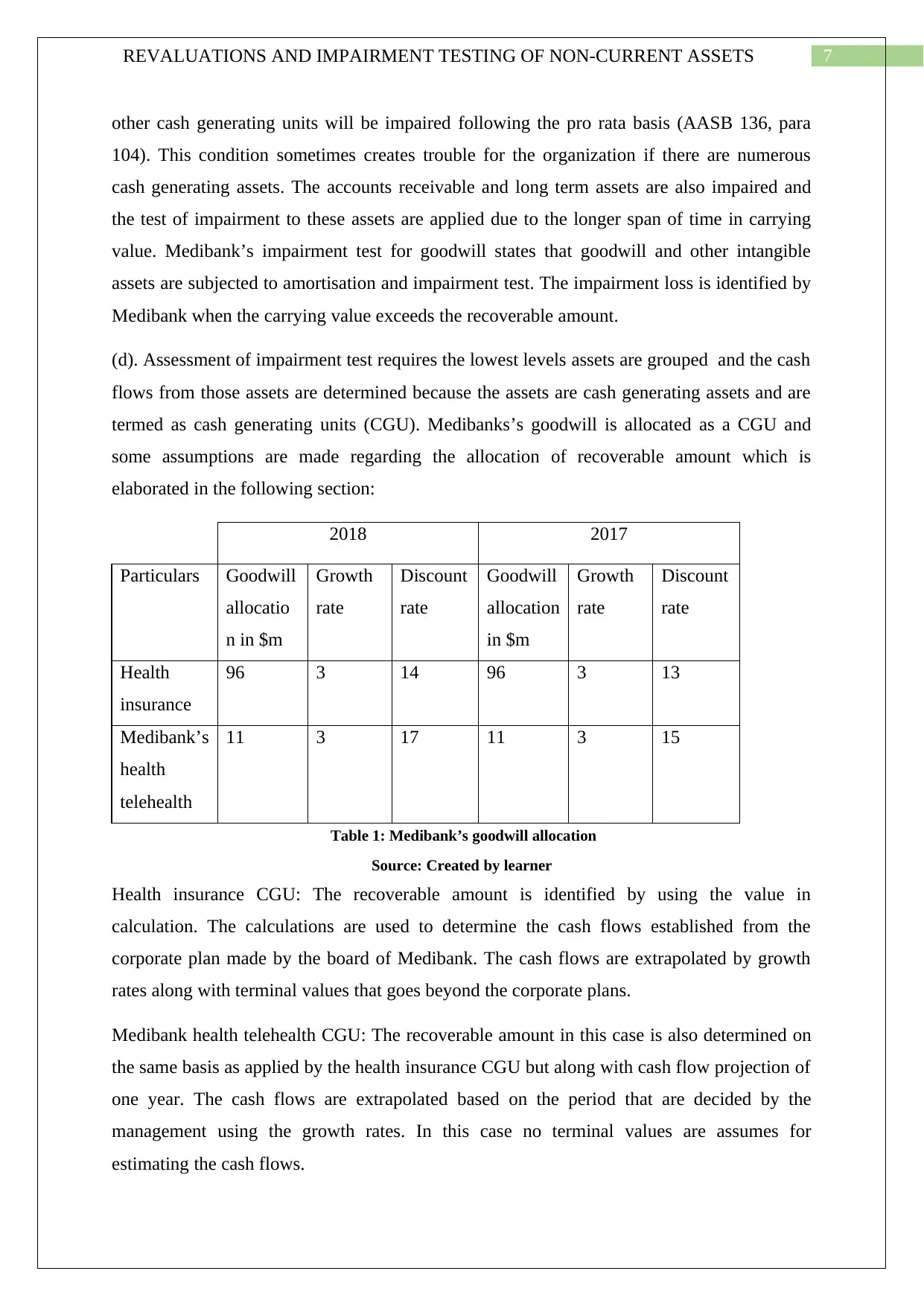

(d). Assessment of impairment test requires the lowest levels assets are grouped and the cash

flows from those assets are determined because the assets are cash generating assets and are

termed as cash generating units (CGU). Medibanks’s goodwill is allocated as a CGU and

some assumptions are made regarding the allocation of recoverable amount which is

elaborated in the following section:

2018 2017

Particulars Goodwill

allocatio

n in $m

Growth

rate

Discount

rate

Goodwill

allocation

in $m

Growth

rate

Discount

rate

Health

insurance

96 3 14 96 3 13

Medibank’s

health

telehealth

11 3 17 11 3 15

Table 1: Medibank’s goodwill allocation

Source: Created by learner

Health insurance CGU: The recoverable amount is identified by using the value in

calculation. The calculations are used to determine the cash flows established from the

corporate plan made by the board of Medibank. The cash flows are extrapolated by growth

rates along with terminal values that goes beyond the corporate plans.

Medibank health telehealth CGU: The recoverable amount in this case is also determined on

the same basis as applied by the health insurance CGU but along with cash flow projection of

one year. The cash flows are extrapolated based on the period that are decided by the

management using the growth rates. In this case no terminal values are assumes for

estimating the cash flows.

other cash generating units will be impaired following the pro rata basis (AASB 136, para

104). This condition sometimes creates trouble for the organization if there are numerous

cash generating assets. The accounts receivable and long term assets are also impaired and

the test of impairment to these assets are applied due to the longer span of time in carrying

value. Medibank’s impairment test for goodwill states that goodwill and other intangible

assets are subjected to amortisation and impairment test. The impairment loss is identified by

Medibank when the carrying value exceeds the recoverable amount.

(d). Assessment of impairment test requires the lowest levels assets are grouped and the cash

flows from those assets are determined because the assets are cash generating assets and are

termed as cash generating units (CGU). Medibanks’s goodwill is allocated as a CGU and

some assumptions are made regarding the allocation of recoverable amount which is

elaborated in the following section:

2018 2017

Particulars Goodwill

allocatio

n in $m

Growth

rate

Discount

rate

Goodwill

allocation

in $m

Growth

rate

Discount

rate

Health

insurance

96 3 14 96 3 13

Medibank’s

health

telehealth

11 3 17 11 3 15

Table 1: Medibank’s goodwill allocation

Source: Created by learner

Health insurance CGU: The recoverable amount is identified by using the value in

calculation. The calculations are used to determine the cash flows established from the

corporate plan made by the board of Medibank. The cash flows are extrapolated by growth

rates along with terminal values that goes beyond the corporate plans.

Medibank health telehealth CGU: The recoverable amount in this case is also determined on

the same basis as applied by the health insurance CGU but along with cash flow projection of

one year. The cash flows are extrapolated based on the period that are decided by the

management using the growth rates. In this case no terminal values are assumes for

estimating the cash flows.

8REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

Some disclosures made by Medibank regarding the impairment tests are as follows:

The growth rates used by the organization are the weighted average growth rate that

are used for the purpose of extrapolation.

The growth rates used does not exceeds the average long term growth rates and for

this the CGU of the organization operated according to the forecasts made.

For the purpose of estimating the recoverable amount the organization has applied the

discount rates after taxation which again discount the cash flows for next period.

The discount rates used reflects the associated risks related to the CGU because of the

usage of pre-tax discount rates.

Some disclosures made by Medibank regarding the impairment tests are as follows:

The growth rates used by the organization are the weighted average growth rate that

are used for the purpose of extrapolation.

The growth rates used does not exceeds the average long term growth rates and for

this the CGU of the organization operated according to the forecasts made.

For the purpose of estimating the recoverable amount the organization has applied the

discount rates after taxation which again discount the cash flows for next period.

The discount rates used reflects the associated risks related to the CGU because of the

usage of pre-tax discount rates.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

Reference list

Baboukardos, D., & Rimmel, G. (2014, March). Goodwill under IFRS: Relevance and

disclosures in an unfavorable environment. In Accounting Forum (Vol. 38, No. 1, pp.

1-17). Elsevier.

Badia, M., Duro, M., Penalva, F., & Ryan, S. (2017). Conditionally conservative fair value

measurements. Journal of Accounting and Economics, 63(1), 75-98.

Barker, R., & Schulte, S. (2017). Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society, 56, 55-

67.

Bepari, M. K., & Mollik, A. T. (2015). Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for

goodwill impairment testing. Journal of Applied Accounting Research, 16(2), 196-

220.

Bepari, M. K., Rahman, S. F., & Mollik, A. T. (2014). Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting and Organizational

Change, 10(1), 116-149.

Caruso, G. D., Ferrari, E. R., & Pisano, V. (2016). Earnings management and goodwill

impairment: An empirical analysis in the Italian M & A context. Journal of

Intellectual Capital, 17(1), 120-147.

Glaum, M., Landsman, W. R., & Wyrwa, S. (2015). Determinants of goodwill impairment

under IFRS: international evidence. Working paper, WHU–Otto Beisheim School of

Management, University of North Carolina, and Justus-Liebig-University Giessen.

Goncharov, I., Riedl, E. J., & Sellhorn, T. (2014). Fair value and audit fees. Review of

Accounting Studies, 19(1), 210-241.

Griffin, J. B. (2014). The effects of uncertainty and disclosure on auditors' fair value

materiality decisions. Journal of Accounting Research, 52(5), 1165-1193.

Reference list

Baboukardos, D., & Rimmel, G. (2014, March). Goodwill under IFRS: Relevance and

disclosures in an unfavorable environment. In Accounting Forum (Vol. 38, No. 1, pp.

1-17). Elsevier.

Badia, M., Duro, M., Penalva, F., & Ryan, S. (2017). Conditionally conservative fair value

measurements. Journal of Accounting and Economics, 63(1), 75-98.

Barker, R., & Schulte, S. (2017). Representing the market perspective: Fair value

measurement for non-financial assets. Accounting, Organizations and Society, 56, 55-

67.

Bepari, M. K., & Mollik, A. T. (2015). Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for

goodwill impairment testing. Journal of Applied Accounting Research, 16(2), 196-

220.

Bepari, M. K., Rahman, S. F., & Mollik, A. T. (2014). Firms' compliance with the disclosure

requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting and Organizational

Change, 10(1), 116-149.

Caruso, G. D., Ferrari, E. R., & Pisano, V. (2016). Earnings management and goodwill

impairment: An empirical analysis in the Italian M & A context. Journal of

Intellectual Capital, 17(1), 120-147.

Glaum, M., Landsman, W. R., & Wyrwa, S. (2015). Determinants of goodwill impairment

under IFRS: international evidence. Working paper, WHU–Otto Beisheim School of

Management, University of North Carolina, and Justus-Liebig-University Giessen.

Goncharov, I., Riedl, E. J., & Sellhorn, T. (2014). Fair value and audit fees. Review of

Accounting Studies, 19(1), 210-241.

Griffin, J. B. (2014). The effects of uncertainty and disclosure on auditors' fair value

materiality decisions. Journal of Accounting Research, 52(5), 1165-1193.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REVALUATIONS AND IMPAIRMENT TESTING OF NON-CURRENT ASSETS

Hamberg, M., & Beisland, L. A. (2014). Changes in the value relevance of goodwill

accounting following the adoption of IFRS 3. Journal of International Accounting,

Auditing and Taxation, 23(2), 59-73.

Johansson, S. E., Hjelström, T., & Hellman, N. (2016). Accounting for goodwill under IFRS:

A critical analysis. Journal of International Accounting, Auditing and Taxation, 27,

13-25.

Müller, M. A., Riedl, E. J., & Sellhorn, T. (2015). Recognition versus disclosure of fair

values. The Accounting Review, 90(6), 2411-2447.

Palea, V. (2014). Fair value accounting and its usefulness to financial statement

users. Journal of Financial Reporting and Accounting, 12(2), 102-116.

Paugam, L., & Ramond, O. (2015). Effect of impairment‐testing disclosures on the cost of

equity capital. Journal of Business Finance & Accounting, 42(5-6), 583-618.

Sun, L. (2016). Managerial ability and goodwill impairment. Advances in accounting, 32, 42-

51.

Yamamoto, T. (2014). Fair Value of Investment Property and independent Appraisers: The

Experience in the UK and Japan. Appraisal Journal, 82(2).

Hamberg, M., & Beisland, L. A. (2014). Changes in the value relevance of goodwill

accounting following the adoption of IFRS 3. Journal of International Accounting,

Auditing and Taxation, 23(2), 59-73.

Johansson, S. E., Hjelström, T., & Hellman, N. (2016). Accounting for goodwill under IFRS:

A critical analysis. Journal of International Accounting, Auditing and Taxation, 27,

13-25.

Müller, M. A., Riedl, E. J., & Sellhorn, T. (2015). Recognition versus disclosure of fair

values. The Accounting Review, 90(6), 2411-2447.

Palea, V. (2014). Fair value accounting and its usefulness to financial statement

users. Journal of Financial Reporting and Accounting, 12(2), 102-116.

Paugam, L., & Ramond, O. (2015). Effect of impairment‐testing disclosures on the cost of

equity capital. Journal of Business Finance & Accounting, 42(5-6), 583-618.

Sun, L. (2016). Managerial ability and goodwill impairment. Advances in accounting, 32, 42-

51.

Yamamoto, T. (2014). Fair Value of Investment Property and independent Appraisers: The

Experience in the UK and Japan. Appraisal Journal, 82(2).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.