Revenue Law Assignment: Income, Deductions, and Tax Calculation

VerifiedAdded on 2022/08/25

|6

|910

|28

Homework Assignment

AI Summary

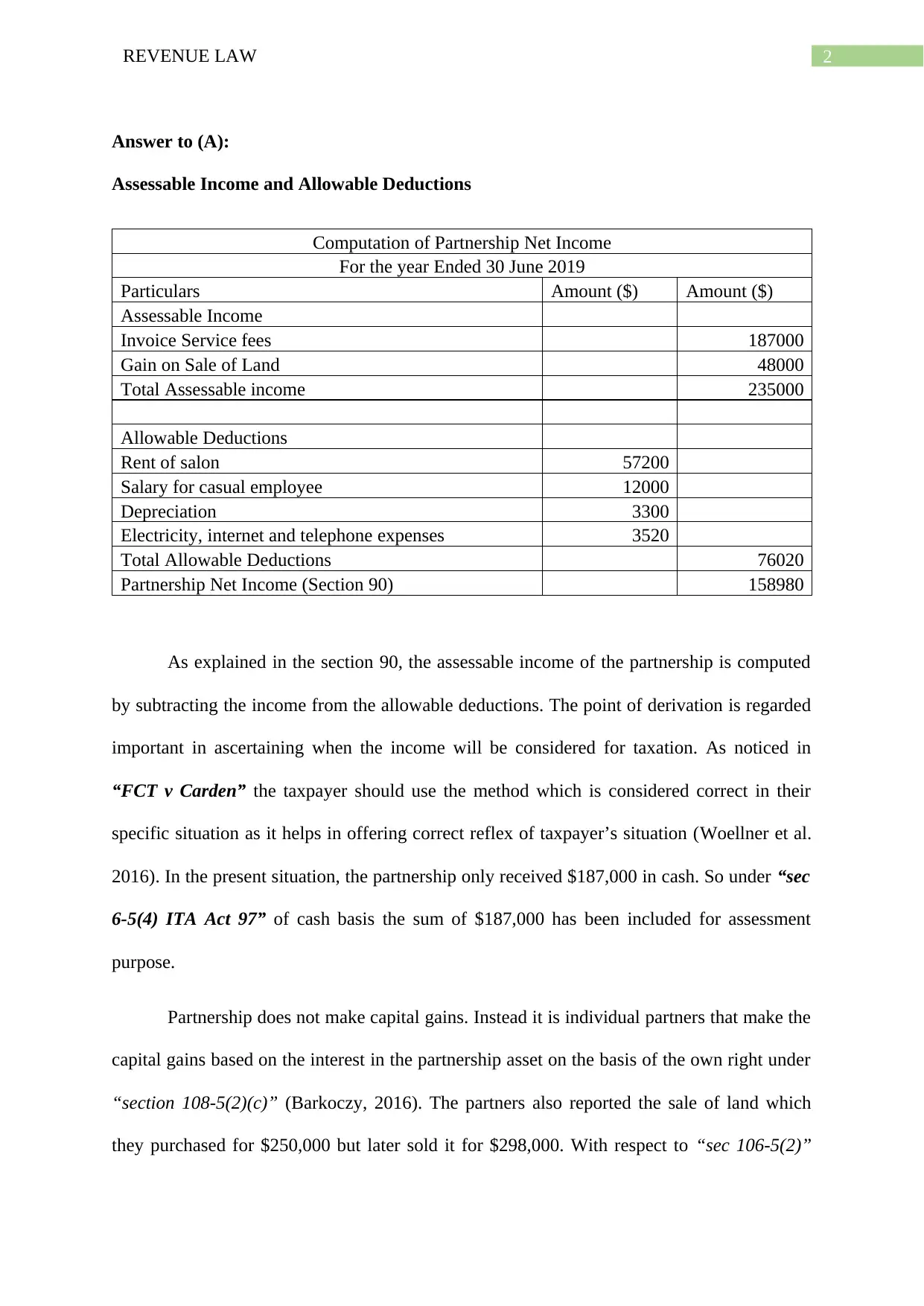

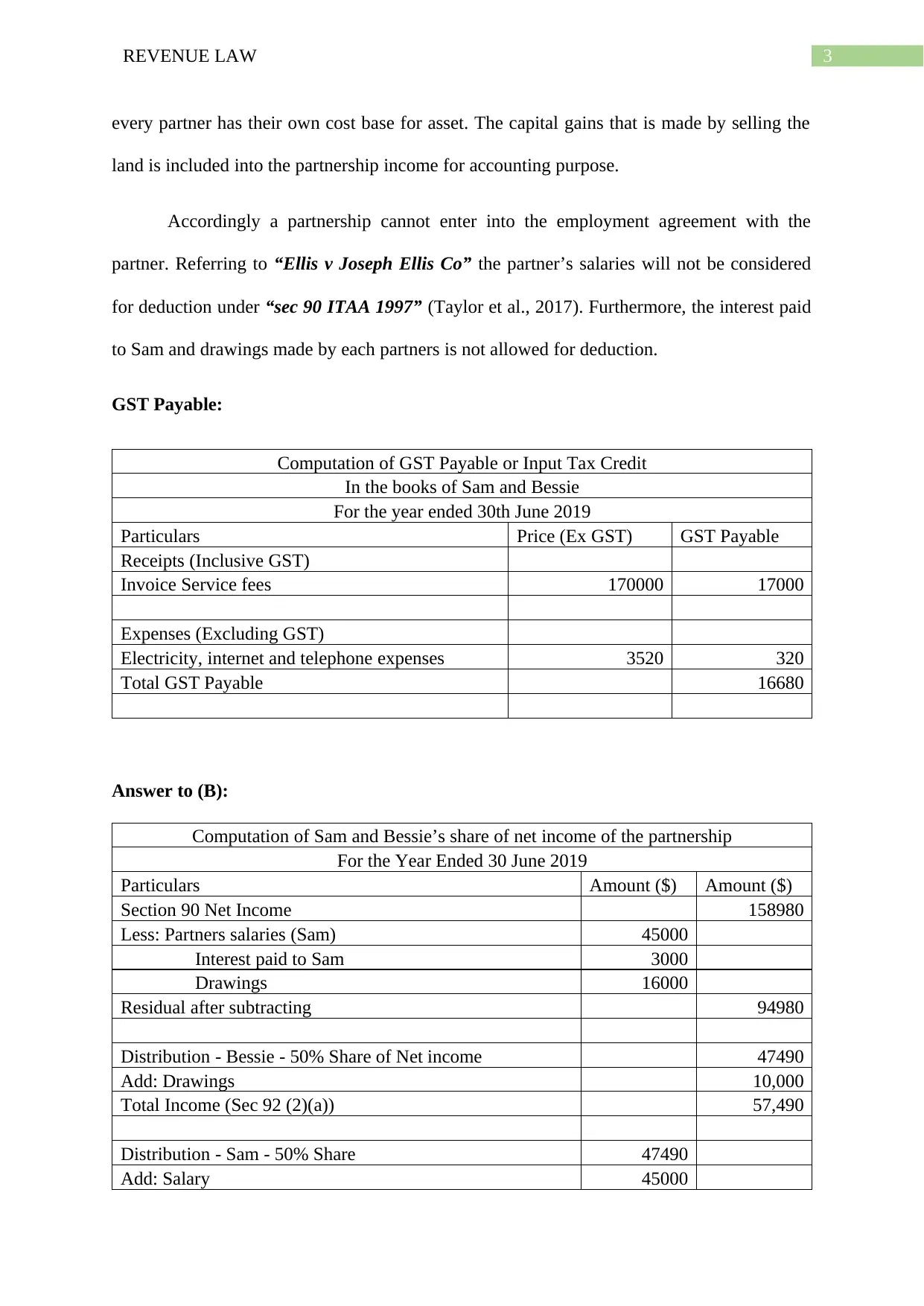

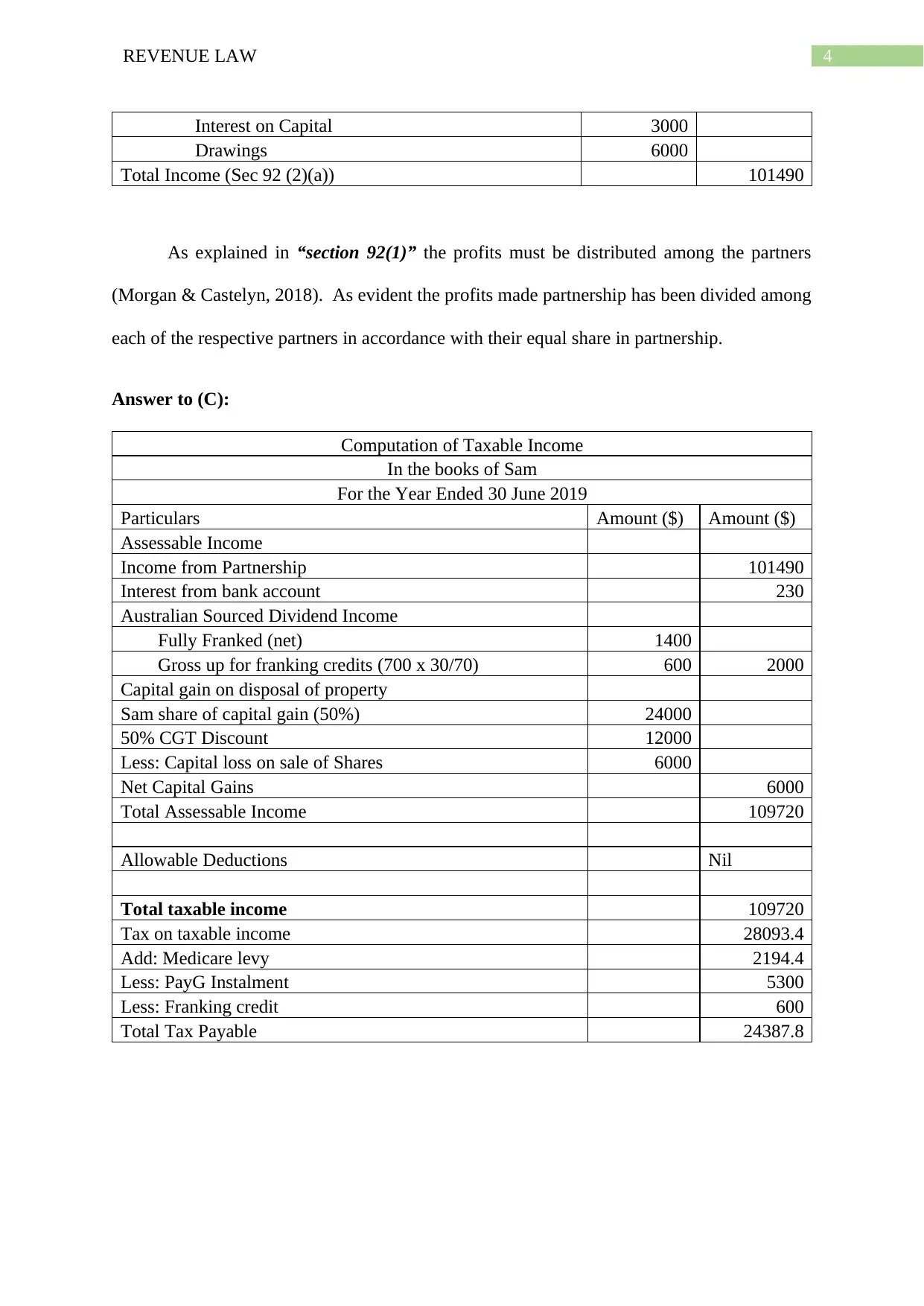

This revenue law assignment analyzes the assessable income and allowable deductions of a partnership, calculating the partnership's net income for the year ended June 30, 2019. It includes the computation of GST payable and input tax credit for the partners, Sam and Bessie. The assignment then details the calculation of Sam and Bessie’s share of the net income, considering partner salaries, interest, and drawings. Finally, it computes Sam's taxable income, including income from the partnership, interest, dividends, and capital gains, along with the calculation of total tax payable, incorporating deductions, franking credits, and pay-as-you-go (PAYG) installments. The assignment references relevant sections of the Income Tax Assessment Act 1997 and case law to support the calculations and explanations.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.