Motherboards and More: Revenue Cycle, Ransomware and Controls Report

VerifiedAdded on 2020/04/07

|9

|1642

|30

Report

AI Summary

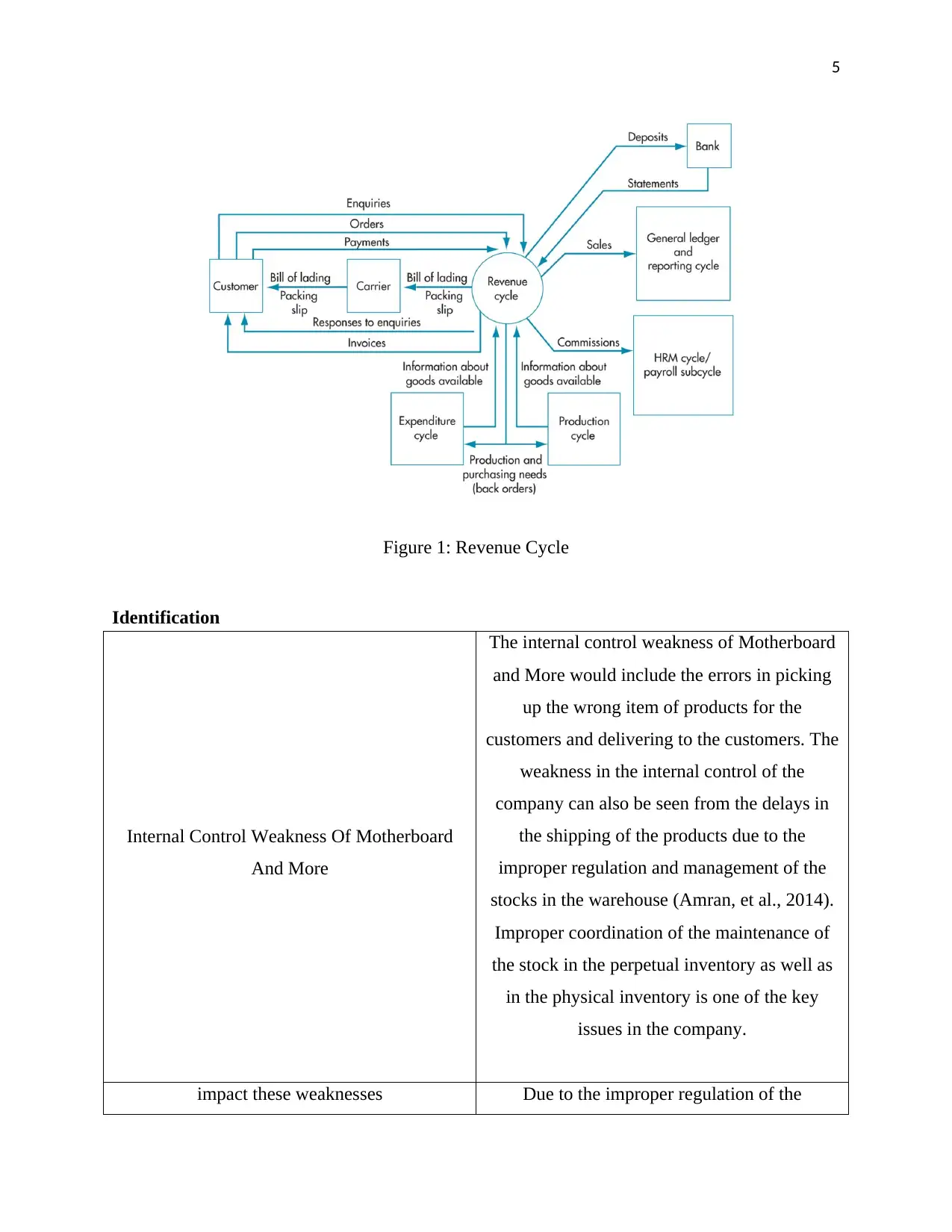

This report analyzes the revenue cycle of Motherboards and More Pty Ltd, focusing on the implications of a ransomware attack in May 2017. It provides an overview of the revenue cycle, from order placement to invoicing, and identifies internal control weaknesses, such as errors in product picking and shipping delays. The report details the impact of these weaknesses, including customer dissatisfaction and potential business losses. It recommends specific internal controls, such as establishing a regulatory body for inventory management and strengthening relationships with shipping companies, to mitigate these issues and protect against future ransomware attacks. The report also provides a brief overview of the ransomware attack and emphasizes the importance of data backup systems and anti-virus protection.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.