University Accounting Report: ACC204 Corporate Financial Reporting

VerifiedAdded on 2020/05/28

|9

|1505

|61

Report

AI Summary

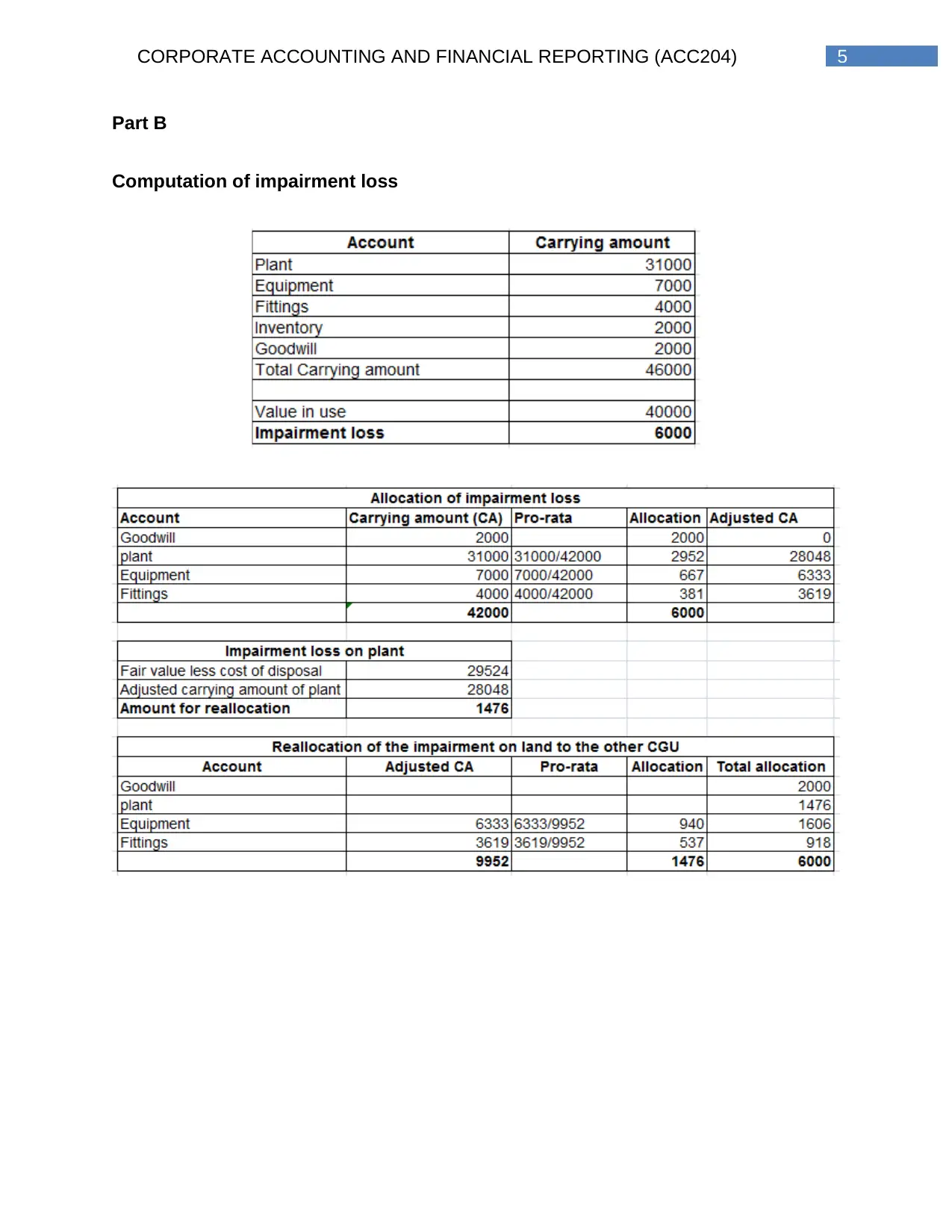

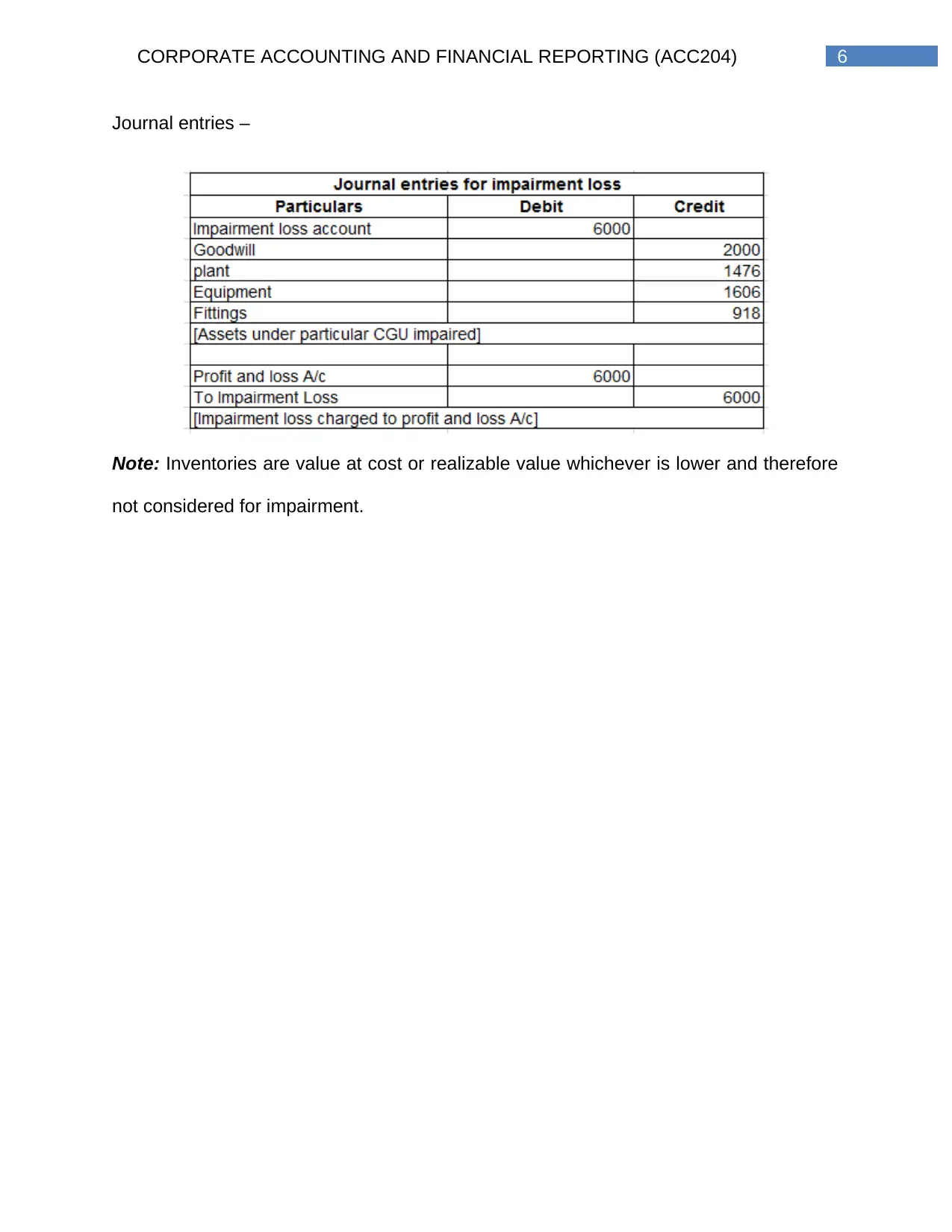

This report focuses on corporate accounting and financial reporting (ACC204), specifically addressing the reversal of impairment loss for cash-generating units (CGUs). It begins by defining impaired assets according to AASB 136 and explains the process of determining recoverable amounts, including the use of both external and internal sources of information to identify impairment indicators. The report details the calculation of the value in use and fair value less costs of disposal, which are critical for assessing impairment. The guidelines for identifying CGUs, determining their carrying amounts, and recognizing impairment loss are also provided. The report further explains the allocation of impairment loss to goodwill and other assets within a CGU. Part A of the report focuses on the reversal of impairment loss for CGUs and Part B provides the computation of impairment loss and related journal entries. The report emphasizes that the reversal of impairment loss is allocated to assets under the unit without considering the goodwill on a pro-rata basis dependent on the carrying amount of the asset. The increase in carrying amount must be treated as the reversal for the impairment losses for each of the assets and are recognized immediately under the profit and loss account. The report also includes references to relevant academic literature, providing context and supporting evidence for the concepts discussed.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.