Comprehensive Review of Firm's Accounting Practices

VerifiedAdded on 2020/06/06

|10

|1670

|56

AI Summary

The provided text is an analysis covering different aspects of accounting within business firms. It discusses how companies record and manage various transactions, such as sales with credit terms, cash and bank deposits, accounts receivable, and inventory purchases. The importance of lease repayment schedules in decision-making for lessors is emphasized, along with the need to account for intangible assets properly under AASB standards. The text concludes by asserting the necessity for businesses to have strong accounting practices to measure performance accurately and make informed decisions.

FINANCIAL

ACCOUNTING PROCESS

ACCOUNTING PROCESS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Scenerio 1........................................................................................................................................1

(a)Preparing journal entry............................................................................................................1

(b) Equity schedule......................................................................................................................2

Scenerio 2........................................................................................................................................2

Scenerio 3........................................................................................................................................3

(a)Determinatiion of sort of lease................................................................................................3

(b)Lease repayment schedule......................................................................................................4

©Preparation of journal entry......................................................................................................4

Scenerio 4........................................................................................................................................5

AASB provisions.........................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

Table 1Input details.........................................................................................................................1

Table 2Raw calculation...................................................................................................................1

Table 3Journal entry........................................................................................................................1

Table 4Equity schedule of firms......................................................................................................2

Table 5Input for calculation of values for journal entries...............................................................2

Table 6Journal entry........................................................................................................................3

Table 7Lease repayment schedule for the business firm.................................................................4

Table 8Journal entry for the business firm......................................................................................4

INTRODUCTION...........................................................................................................................1

Scenerio 1........................................................................................................................................1

(a)Preparing journal entry............................................................................................................1

(b) Equity schedule......................................................................................................................2

Scenerio 2........................................................................................................................................2

Scenerio 3........................................................................................................................................3

(a)Determinatiion of sort of lease................................................................................................3

(b)Lease repayment schedule......................................................................................................4

©Preparation of journal entry......................................................................................................4

Scenerio 4........................................................................................................................................5

AASB provisions.........................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

Table 1Input details.........................................................................................................................1

Table 2Raw calculation...................................................................................................................1

Table 3Journal entry........................................................................................................................1

Table 4Equity schedule of firms......................................................................................................2

Table 5Input for calculation of values for journal entries...............................................................2

Table 6Journal entry........................................................................................................................3

Table 7Lease repayment schedule for the business firm.................................................................4

Table 8Journal entry for the business firm......................................................................................4

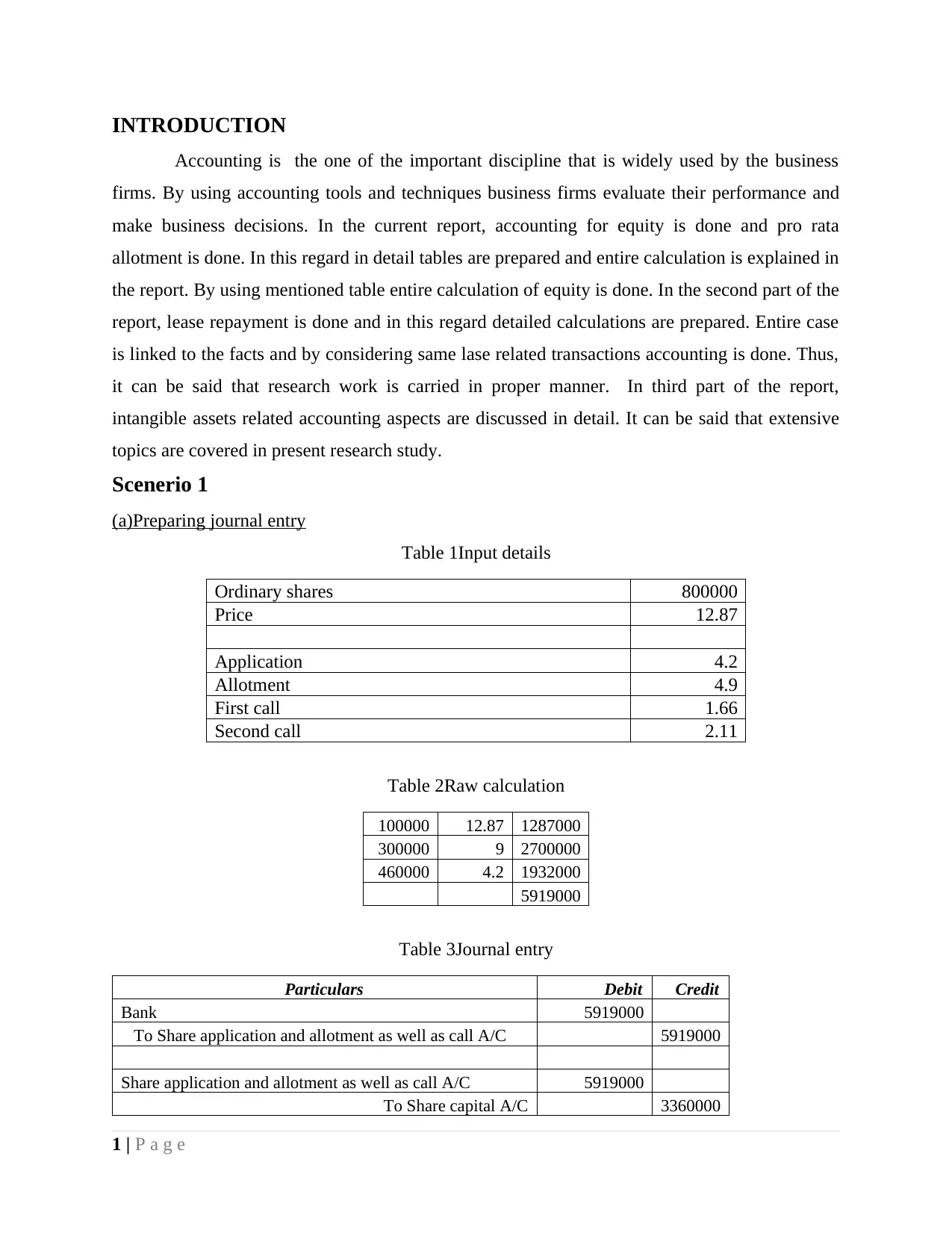

INTRODUCTION

Accounting is the one of the important discipline that is widely used by the business

firms. By using accounting tools and techniques business firms evaluate their performance and

make business decisions. In the current report, accounting for equity is done and pro rata

allotment is done. In this regard in detail tables are prepared and entire calculation is explained in

the report. By using mentioned table entire calculation of equity is done. In the second part of the

report, lease repayment is done and in this regard detailed calculations are prepared. Entire case

is linked to the facts and by considering same lase related transactions accounting is done. Thus,

it can be said that research work is carried in proper manner. In third part of the report,

intangible assets related accounting aspects are discussed in detail. It can be said that extensive

topics are covered in present research study.

Scenerio 1

(a)Preparing journal entry

Table 1Input details

Ordinary shares 800000

Price 12.87

Application 4.2

Allotment 4.9

First call 1.66

Second call 2.11

Table 2Raw calculation

100000 12.87 1287000

300000 9 2700000

460000 4.2 1932000

5919000

Table 3Journal entry

Particulars Debit Credit

Bank 5919000

To Share application and allotment as well as call A/C 5919000

Share application and allotment as well as call A/C 5919000

To Share capital A/C 3360000

1 | P a g e

Accounting is the one of the important discipline that is widely used by the business

firms. By using accounting tools and techniques business firms evaluate their performance and

make business decisions. In the current report, accounting for equity is done and pro rata

allotment is done. In this regard in detail tables are prepared and entire calculation is explained in

the report. By using mentioned table entire calculation of equity is done. In the second part of the

report, lease repayment is done and in this regard detailed calculations are prepared. Entire case

is linked to the facts and by considering same lase related transactions accounting is done. Thus,

it can be said that research work is carried in proper manner. In third part of the report,

intangible assets related accounting aspects are discussed in detail. It can be said that extensive

topics are covered in present research study.

Scenerio 1

(a)Preparing journal entry

Table 1Input details

Ordinary shares 800000

Price 12.87

Application 4.2

Allotment 4.9

First call 1.66

Second call 2.11

Table 2Raw calculation

100000 12.87 1287000

300000 9 2700000

460000 4.2 1932000

5919000

Table 3Journal entry

Particulars Debit Credit

Bank 5919000

To Share application and allotment as well as call A/C 5919000

Share application and allotment as well as call A/C 5919000

To Share capital A/C 3360000

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To bank 84000

To share allotment 2098000

To share call 377000

Share allotment A/C 3920000

To Share capital A/C 3920000

Bank A/C 3920000

To Share allotment A/C 1822000

To call in advance 2098000

Share call A/C 3016000

To Share capital A/C 3016000

Bank A/C 2639000

Call in advance 377000

To share first call A/C 3016000

Share issue expenses 12000

To Bank A/C 12000

(b) Equity schedule

Table 4Equity schedule of firms

Particulars Amount

Equity 10296000

It can be seen from table that equity is valued at above givcen value. This value is

computed by adding entire application, allotment and call amount. Thus, it can be said that

through different stages mentioned amount of money is collected.

Scenerio 2

Table 5Input for calculation of values for journal entries

30-Jun-16 31-Dec-16 30-Jun-17

Cost Carrying amount Carrying amount Carrying amount

Machine A 300000 180000 180000 163000

Machine B 200000 170000 155000 136500

Depreciation Depreciation Depreciation

2 | P a g e

To share allotment 2098000

To share call 377000

Share allotment A/C 3920000

To Share capital A/C 3920000

Bank A/C 3920000

To Share allotment A/C 1822000

To call in advance 2098000

Share call A/C 3016000

To Share capital A/C 3016000

Bank A/C 2639000

Call in advance 377000

To share first call A/C 3016000

Share issue expenses 12000

To Bank A/C 12000

(b) Equity schedule

Table 4Equity schedule of firms

Particulars Amount

Equity 10296000

It can be seen from table that equity is valued at above givcen value. This value is

computed by adding entire application, allotment and call amount. Thus, it can be said that

through different stages mentioned amount of money is collected.

Scenerio 2

Table 5Input for calculation of values for journal entries

30-Jun-16 31-Dec-16 30-Jun-17

Cost Carrying amount Carrying amount Carrying amount

Machine A 300000 180000 180000 163000

Machine B 200000 170000 155000 136500

Depreciation Depreciation Depreciation

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

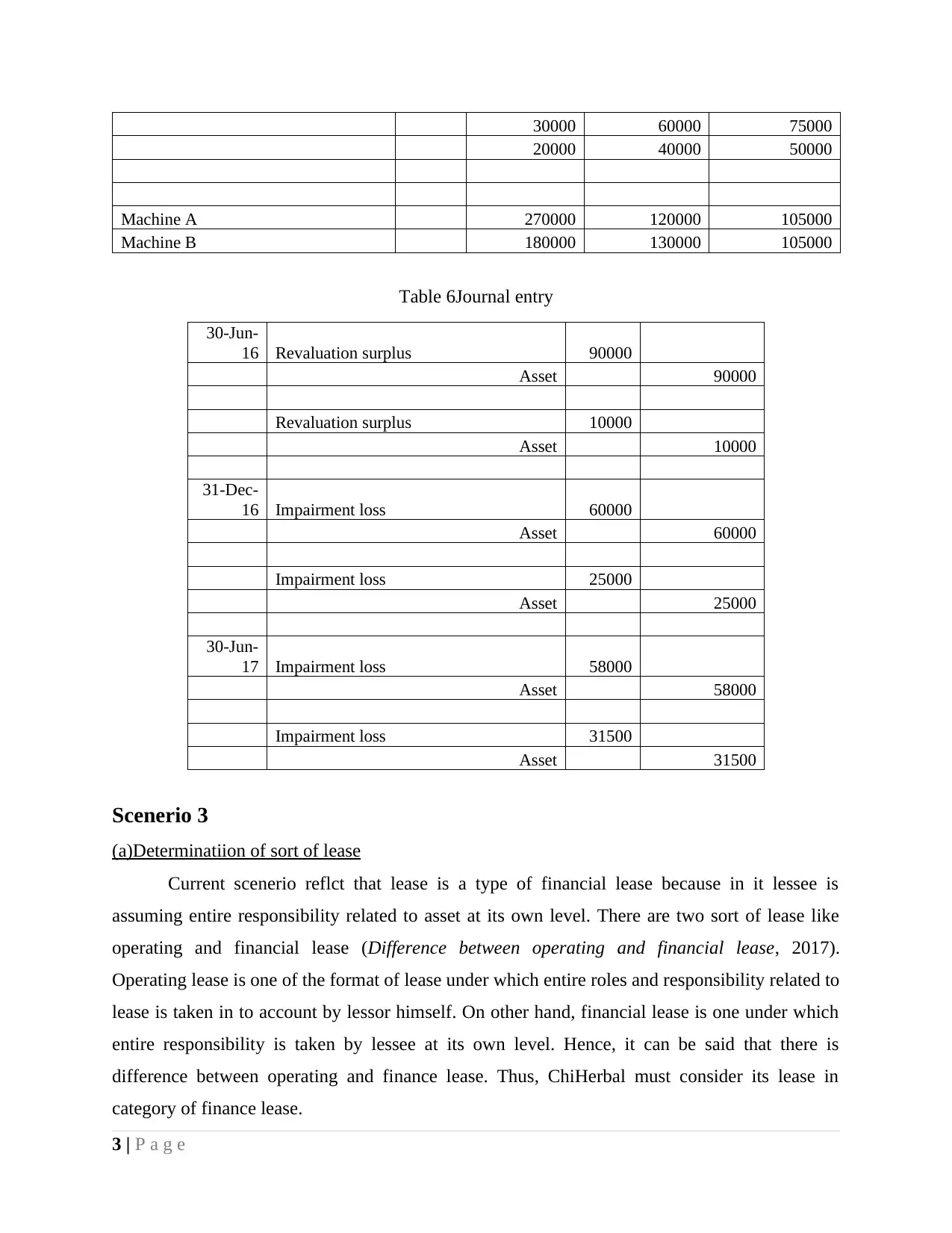

30000 60000 75000

20000 40000 50000

Machine A 270000 120000 105000

Machine B 180000 130000 105000

Table 6Journal entry

30-Jun-

16 Revaluation surplus 90000

Asset 90000

Revaluation surplus 10000

Asset 10000

31-Dec-

16 Impairment loss 60000

Asset 60000

Impairment loss 25000

Asset 25000

30-Jun-

17 Impairment loss 58000

Asset 58000

Impairment loss 31500

Asset 31500

Scenerio 3

(a)Determinatiion of sort of lease

Current scenerio reflct that lease is a type of financial lease because in it lessee is

assuming entire responsibility related to asset at its own level. There are two sort of lease like

operating and financial lease (Difference between operating and financial lease, 2017).

Operating lease is one of the format of lease under which entire roles and responsibility related to

lease is taken in to account by lessor himself. On other hand, financial lease is one under which

entire responsibility is taken by lessee at its own level. Hence, it can be said that there is

difference between operating and finance lease. Thus, ChiHerbal must consider its lease in

category of finance lease.

3 | P a g e

20000 40000 50000

Machine A 270000 120000 105000

Machine B 180000 130000 105000

Table 6Journal entry

30-Jun-

16 Revaluation surplus 90000

Asset 90000

Revaluation surplus 10000

Asset 10000

31-Dec-

16 Impairment loss 60000

Asset 60000

Impairment loss 25000

Asset 25000

30-Jun-

17 Impairment loss 58000

Asset 58000

Impairment loss 31500

Asset 31500

Scenerio 3

(a)Determinatiion of sort of lease

Current scenerio reflct that lease is a type of financial lease because in it lessee is

assuming entire responsibility related to asset at its own level. There are two sort of lease like

operating and financial lease (Difference between operating and financial lease, 2017).

Operating lease is one of the format of lease under which entire roles and responsibility related to

lease is taken in to account by lessor himself. On other hand, financial lease is one under which

entire responsibility is taken by lessee at its own level. Hence, it can be said that there is

difference between operating and finance lease. Thus, ChiHerbal must consider its lease in

category of finance lease.

3 | P a g e

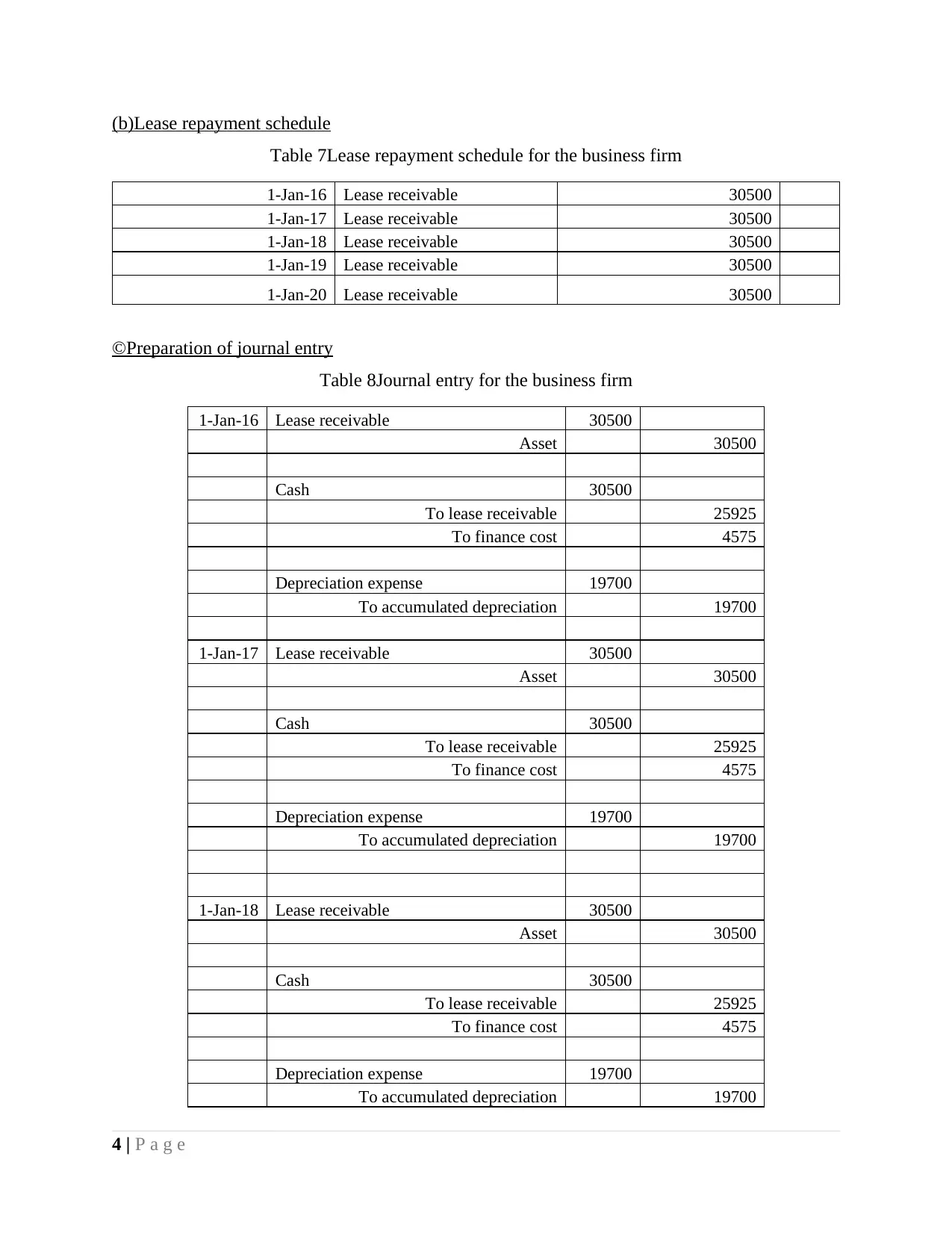

(b)Lease repayment schedule

Table 7Lease repayment schedule for the business firm

1-Jan-16 Lease receivable 30500

1-Jan-17 Lease receivable 30500

1-Jan-18 Lease receivable 30500

1-Jan-19 Lease receivable 30500

1-Jan-20 Lease receivable 30500

©Preparation of journal entry

Table 8Journal entry for the business firm

1-Jan-16 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

1-Jan-17 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

1-Jan-18 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

4 | P a g e

Table 7Lease repayment schedule for the business firm

1-Jan-16 Lease receivable 30500

1-Jan-17 Lease receivable 30500

1-Jan-18 Lease receivable 30500

1-Jan-19 Lease receivable 30500

1-Jan-20 Lease receivable 30500

©Preparation of journal entry

Table 8Journal entry for the business firm

1-Jan-16 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

1-Jan-17 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

1-Jan-18 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

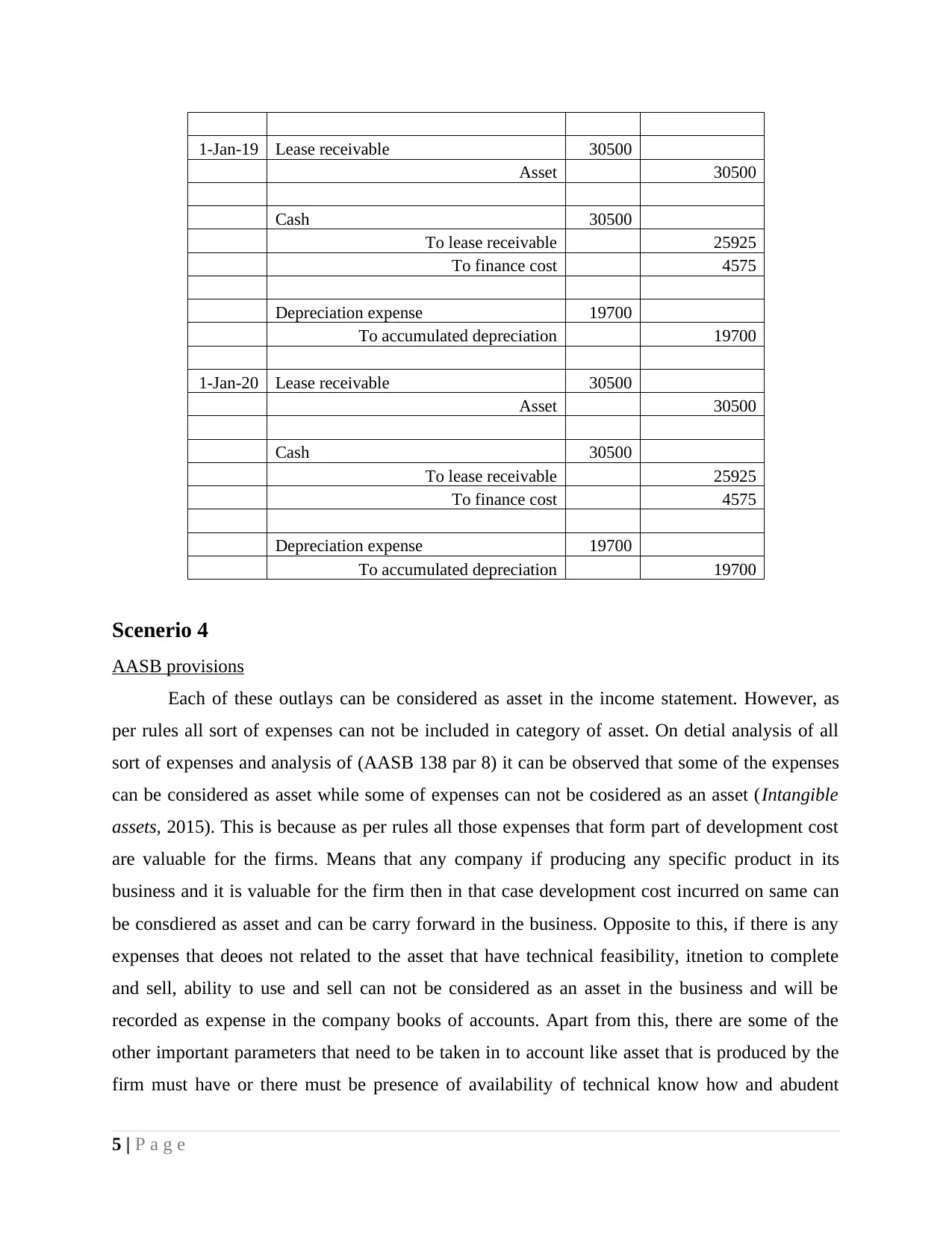

1-Jan-19 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

1-Jan-20 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

Scenerio 4

AASB provisions

Each of these outlays can be considered as asset in the income statement. However, as

per rules all sort of expenses can not be included in category of asset. On detial analysis of all

sort of expenses and analysis of (AASB 138 par 8) it can be observed that some of the expenses

can be considered as asset while some of expenses can not be cosidered as an asset (Intangible

assets, 2015). This is because as per rules all those expenses that form part of development cost

are valuable for the firms. Means that any company if producing any specific product in its

business and it is valuable for the firm then in that case development cost incurred on same can

be consdiered as asset and can be carry forward in the business. Opposite to this, if there is any

expenses that deoes not related to the asset that have technical feasibility, itnetion to complete

and sell, ability to use and sell can not be considered as an asset in the business and will be

recorded as expense in the company books of accounts. Apart from this, there are some of the

other important parameters that need to be taken in to account like asset that is produced by the

firm must have or there must be presence of availability of technical know how and abudent

5 | P a g e

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

1-Jan-20 Lease receivable 30500

Asset 30500

Cash 30500

To lease receivable 25925

To finance cost 4575

Depreciation expense 19700

To accumulated depreciation 19700

Scenerio 4

AASB provisions

Each of these outlays can be considered as asset in the income statement. However, as

per rules all sort of expenses can not be included in category of asset. On detial analysis of all

sort of expenses and analysis of (AASB 138 par 8) it can be observed that some of the expenses

can be considered as asset while some of expenses can not be cosidered as an asset (Intangible

assets, 2015). This is because as per rules all those expenses that form part of development cost

are valuable for the firms. Means that any company if producing any specific product in its

business and it is valuable for the firm then in that case development cost incurred on same can

be consdiered as asset and can be carry forward in the business. Opposite to this, if there is any

expenses that deoes not related to the asset that have technical feasibility, itnetion to complete

and sell, ability to use and sell can not be considered as an asset in the business and will be

recorded as expense in the company books of accounts. Apart from this, there are some of the

other important parameters that need to be taken in to account like asset that is produced by the

firm must have or there must be presence of availability of technical know how and abudent

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

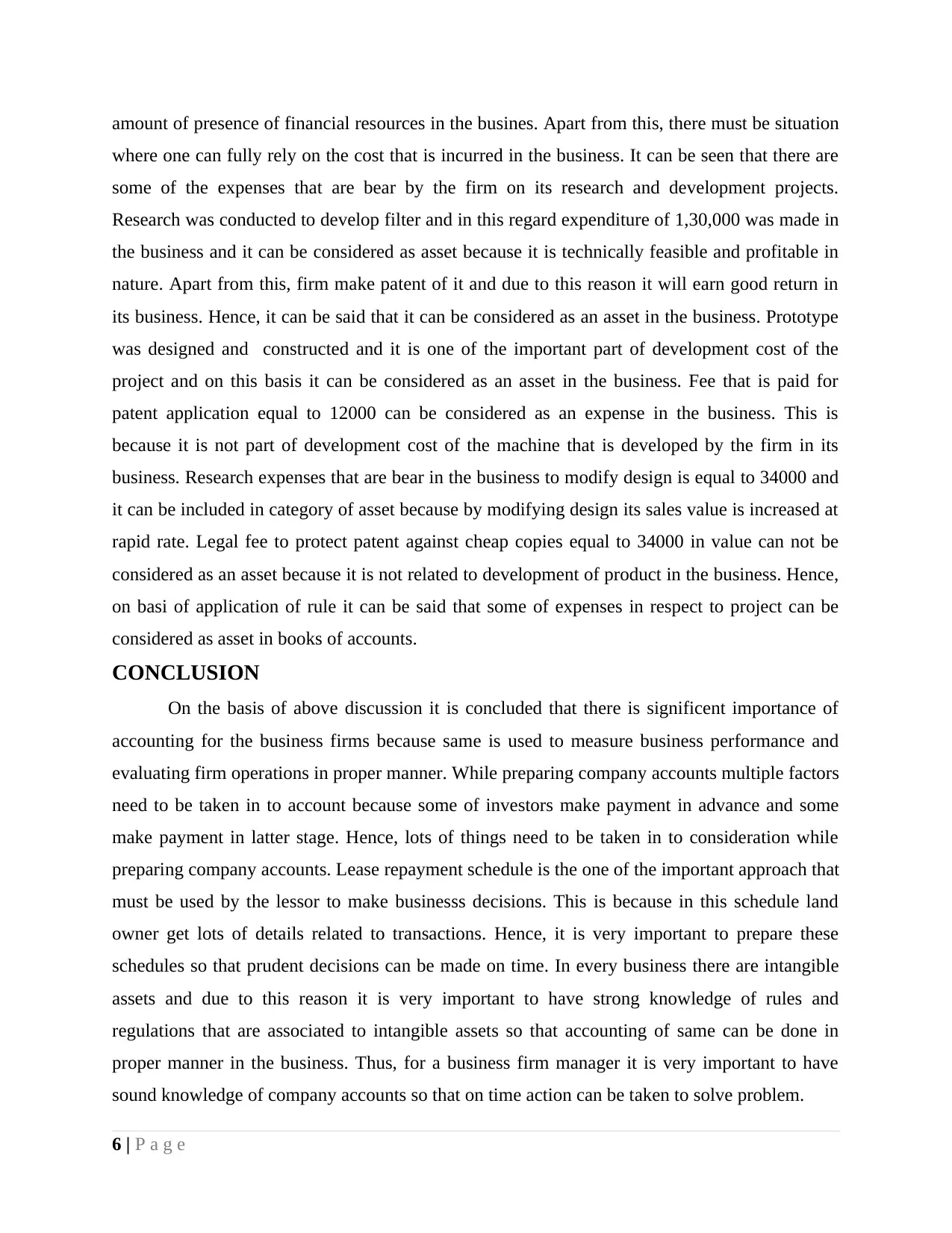

amount of presence of financial resources in the busines. Apart from this, there must be situation

where one can fully rely on the cost that is incurred in the business. It can be seen that there are

some of the expenses that are bear by the firm on its research and development projects.

Research was conducted to develop filter and in this regard expenditure of 1,30,000 was made in

the business and it can be considered as asset because it is technically feasible and profitable in

nature. Apart from this, firm make patent of it and due to this reason it will earn good return in

its business. Hence, it can be said that it can be considered as an asset in the business. Prototype

was designed and constructed and it is one of the important part of development cost of the

project and on this basis it can be considered as an asset in the business. Fee that is paid for

patent application equal to 12000 can be considered as an expense in the business. This is

because it is not part of development cost of the machine that is developed by the firm in its

business. Research expenses that are bear in the business to modify design is equal to 34000 and

it can be included in category of asset because by modifying design its sales value is increased at

rapid rate. Legal fee to protect patent against cheap copies equal to 34000 in value can not be

considered as an asset because it is not related to development of product in the business. Hence,

on basi of application of rule it can be said that some of expenses in respect to project can be

considered as asset in books of accounts.

CONCLUSION

On the basis of above discussion it is concluded that there is significent importance of

accounting for the business firms because same is used to measure business performance and

evaluating firm operations in proper manner. While preparing company accounts multiple factors

need to be taken in to account because some of investors make payment in advance and some

make payment in latter stage. Hence, lots of things need to be taken in to consideration while

preparing company accounts. Lease repayment schedule is the one of the important approach that

must be used by the lessor to make businesss decisions. This is because in this schedule land

owner get lots of details related to transactions. Hence, it is very important to prepare these

schedules so that prudent decisions can be made on time. In every business there are intangible

assets and due to this reason it is very important to have strong knowledge of rules and

regulations that are associated to intangible assets so that accounting of same can be done in

proper manner in the business. Thus, for a business firm manager it is very important to have

sound knowledge of company accounts so that on time action can be taken to solve problem.

6 | P a g e

where one can fully rely on the cost that is incurred in the business. It can be seen that there are

some of the expenses that are bear by the firm on its research and development projects.

Research was conducted to develop filter and in this regard expenditure of 1,30,000 was made in

the business and it can be considered as asset because it is technically feasible and profitable in

nature. Apart from this, firm make patent of it and due to this reason it will earn good return in

its business. Hence, it can be said that it can be considered as an asset in the business. Prototype

was designed and constructed and it is one of the important part of development cost of the

project and on this basis it can be considered as an asset in the business. Fee that is paid for

patent application equal to 12000 can be considered as an expense in the business. This is

because it is not part of development cost of the machine that is developed by the firm in its

business. Research expenses that are bear in the business to modify design is equal to 34000 and

it can be included in category of asset because by modifying design its sales value is increased at

rapid rate. Legal fee to protect patent against cheap copies equal to 34000 in value can not be

considered as an asset because it is not related to development of product in the business. Hence,

on basi of application of rule it can be said that some of expenses in respect to project can be

considered as asset in books of accounts.

CONCLUSION

On the basis of above discussion it is concluded that there is significent importance of

accounting for the business firms because same is used to measure business performance and

evaluating firm operations in proper manner. While preparing company accounts multiple factors

need to be taken in to account because some of investors make payment in advance and some

make payment in latter stage. Hence, lots of things need to be taken in to consideration while

preparing company accounts. Lease repayment schedule is the one of the important approach that

must be used by the lessor to make businesss decisions. This is because in this schedule land

owner get lots of details related to transactions. Hence, it is very important to prepare these

schedules so that prudent decisions can be made on time. In every business there are intangible

assets and due to this reason it is very important to have strong knowledge of rules and

regulations that are associated to intangible assets so that accounting of same can be done in

proper manner in the business. Thus, for a business firm manager it is very important to have

sound knowledge of company accounts so that on time action can be taken to solve problem.

6 | P a g e

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Online

Difference between operating and financial lease, 2017. [Online]. Available through:<

https://efinancemanagement.com/sources-of-finance/difference-between-operating-and-

financial-lease>.

Intangible assets, 2015. [PDF]. Available through:<

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-

18.pdf>

8 | P a g e

Online

Difference between operating and financial lease, 2017. [Online]. Available through:<

https://efinancemanagement.com/sources-of-finance/difference-between-operating-and-

financial-lease>.

Intangible assets, 2015. [PDF]. Available through:<

http://www.aasb.gov.au/admin/file/content105/c9/AASB138_08-15_COMPoct15_01-

18.pdf>

8 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.