Corporate Accounting Report: RFG Cash Flow, Income Tax Analysis

VerifiedAdded on 2021/05/30

|13

|3062

|37

Report

AI Summary

This report provides a comprehensive analysis of the corporate accounting practices of Retail Food Group (RFG). It begins with an examination of the cash flow statement, detailing cash flows from operating, investing, and financing activities from 2015 to 2017, including receipts from customers, payments to suppliers, and proceeds from share issues. The analysis then delves into the other comprehensive income statement, focusing on items such as exchange differences on foreign operations and changes in the fair value of cash flow hedges. The report also examines the accounting for corporate income tax, including the calculation of tax expenses, differences between reported and actual income tax, and the role of deferred tax assets and liabilities. The report highlights the impact of non-deductible expenses, varying tax rates among subsidiaries, and the impact of deferred tax assets and liabilities on RFG's financial position. Overall, the report offers a detailed overview of RFG's financial reporting, providing insights into its cash flow management, income tax strategies, and the importance of comprehensive income in presenting a complete financial picture.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Author’s Note

Corporate Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash Flow Statement.......................................................................................................................2

Requirement [i]............................................................................................................................2

Requirement [ii]...........................................................................................................................4

Other Comprehensive Income Statement........................................................................................5

Requirement [iii]..........................................................................................................................5

Requirement [iv]..........................................................................................................................5

Requirement [v]...........................................................................................................................6

Accounting for Corporate Income Tax............................................................................................7

Requirement [vi]..........................................................................................................................7

Requirement [vii].........................................................................................................................7

Requirement [viii]........................................................................................................................8

Requirement [ix]..........................................................................................................................9

Requirement [x]...........................................................................................................................9

Requirement [xi]........................................................................................................................10

References......................................................................................................................................11

Table of Contents

Cash Flow Statement.......................................................................................................................2

Requirement [i]............................................................................................................................2

Requirement [ii]...........................................................................................................................4

Other Comprehensive Income Statement........................................................................................5

Requirement [iii]..........................................................................................................................5

Requirement [iv]..........................................................................................................................5

Requirement [v]...........................................................................................................................6

Accounting for Corporate Income Tax............................................................................................7

Requirement [vi]..........................................................................................................................7

Requirement [vii].........................................................................................................................7

Requirement [viii]........................................................................................................................8

Requirement [ix]..........................................................................................................................9

Requirement [x]...........................................................................................................................9

Requirement [xi]........................................................................................................................10

References......................................................................................................................................11

2CORPORATE ACCOUNTING

Cash Flow Statement

Requirement [i]

The statement of cash flow is a major financial statements of the companies that shows

the major inflow and outflow of cash. The main aim of this part is to discuss about the items of

the cash flow statement of Retail Food Group (RFG) of Australia.

Cash Flow from Operating Activities: There are four major items under the cash flow from

operating activities of RFG. They are receipts from customers; payment to suppliers and

employees; payment of interest and other cost finance; and payment of income tax (rfg.com.au,

2018).

Receipts from customers refer to the amount that RFG receives from the customers due to

the credit sales. It can be seen that there has been increase in the receipts from customers in RFG

from 2015 to 2017; that is $263,555,000 in 2015, $332,754,000 in 2016 and $456,000,000 in

2017 (rfg.com.au, 2018). The main reason of this increase is the increase in credit sales. Payment

to suppliers is the amount that RFG is required to pay to their suppliers for credit purchase. The

same increasing trend can be seen in this item from2015 to 2017; and the main reason behind

this increase in payment is the increase in purchase. RFG is required to pay the interest on their

term loans. There is increase in these expenses from 2015 to 2017 that shows the increased

borrowing of the company. Decrease in the payment of interest can be from 2015 to 2016; but

again increase can be seen in 2017 due to the increase in profitability of RFG in 2017 (Reid &

Myddelton, 2017).

Cash Flow Statement

Requirement [i]

The statement of cash flow is a major financial statements of the companies that shows

the major inflow and outflow of cash. The main aim of this part is to discuss about the items of

the cash flow statement of Retail Food Group (RFG) of Australia.

Cash Flow from Operating Activities: There are four major items under the cash flow from

operating activities of RFG. They are receipts from customers; payment to suppliers and

employees; payment of interest and other cost finance; and payment of income tax (rfg.com.au,

2018).

Receipts from customers refer to the amount that RFG receives from the customers due to

the credit sales. It can be seen that there has been increase in the receipts from customers in RFG

from 2015 to 2017; that is $263,555,000 in 2015, $332,754,000 in 2016 and $456,000,000 in

2017 (rfg.com.au, 2018). The main reason of this increase is the increase in credit sales. Payment

to suppliers is the amount that RFG is required to pay to their suppliers for credit purchase. The

same increasing trend can be seen in this item from2015 to 2017; and the main reason behind

this increase in payment is the increase in purchase. RFG is required to pay the interest on their

term loans. There is increase in these expenses from 2015 to 2017 that shows the increased

borrowing of the company. Decrease in the payment of interest can be from 2015 to 2016; but

again increase can be seen in 2017 due to the increase in profitability of RFG in 2017 (Reid &

Myddelton, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

Cash Flow from Investing Activities: The major items under the cash flow from investing

activities of RFG are payment and proceed from property, plant and equipment, payment for

intangible assets and interest received (rfg.com.au, 2018).

Payment for property, plant and equipment is the amount that RFG pays for the

acquisition and purchase of these items. It can be observed that there has been an increase in this

payment by RFG; that is $6,551,000 in 2015, 14,429,000 in 2016 and $30,650,000 in 2017

(rfg.com.au, 2018). It implies that RFG is increasing their asset base by purchasing them. It can

also be observed that the company has not received significant amount from the selling of their

property, plant and equipment as the company is increasing their asset base. Payment of

intangible assets refers to the amount that RFG pays for the acquisition of intangible assets

(Miloš & Jovan, 2013). It can be seen that there is an increase in this payment from 2015 to

2016, but 2017 registered as slight decrease. Interest received refers to the process as a form of

interest from investment. There is a constant increase in this item from 2015 to 2017 that

indicates the increased investment of RFG.

Cash Flow from Financing Activities: The major items of RFG under this are proceed from

share issue, proceeds and repayment from borrowing, payment of dividend, payment for share

and debt issue (rfg.com.au, 2018).

Proceed from issue of share refers to the income of RFG from the share and security

issue. It can be seen that RFG did not receive any proceed due to not issuance of any share in

2016. In 2015 and 2017, this amount was $$68,280,000 and $35,600,000 respectively. It can also

be observed that there is a decrease in the proceeds from borrowings from 2015 to 2016

(rfg.com.au, 2018). However, increase in this item can be seen in 2017 due to the increase in

Cash Flow from Investing Activities: The major items under the cash flow from investing

activities of RFG are payment and proceed from property, plant and equipment, payment for

intangible assets and interest received (rfg.com.au, 2018).

Payment for property, plant and equipment is the amount that RFG pays for the

acquisition and purchase of these items. It can be observed that there has been an increase in this

payment by RFG; that is $6,551,000 in 2015, 14,429,000 in 2016 and $30,650,000 in 2017

(rfg.com.au, 2018). It implies that RFG is increasing their asset base by purchasing them. It can

also be observed that the company has not received significant amount from the selling of their

property, plant and equipment as the company is increasing their asset base. Payment of

intangible assets refers to the amount that RFG pays for the acquisition of intangible assets

(Miloš & Jovan, 2013). It can be seen that there is an increase in this payment from 2015 to

2016, but 2017 registered as slight decrease. Interest received refers to the process as a form of

interest from investment. There is a constant increase in this item from 2015 to 2017 that

indicates the increased investment of RFG.

Cash Flow from Financing Activities: The major items of RFG under this are proceed from

share issue, proceeds and repayment from borrowing, payment of dividend, payment for share

and debt issue (rfg.com.au, 2018).

Proceed from issue of share refers to the income of RFG from the share and security

issue. It can be seen that RFG did not receive any proceed due to not issuance of any share in

2016. In 2015 and 2017, this amount was $$68,280,000 and $35,600,000 respectively. It can also

be observed that there is a decrease in the proceeds from borrowings from 2015 to 2016

(rfg.com.au, 2018). However, increase in this item can be seen in 2017 due to the increase in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

investment. From the year 2015, RFG has taken the strategy to make the repayment of their

borrowings; for this reason there is increase in this expenses from 2015 to 2016. It can also be

seen that the company has increased the payment of dividend from 2015 to 2017 due to the

increase in the profit of the company (Pavlović & Bogdanović, 2013).

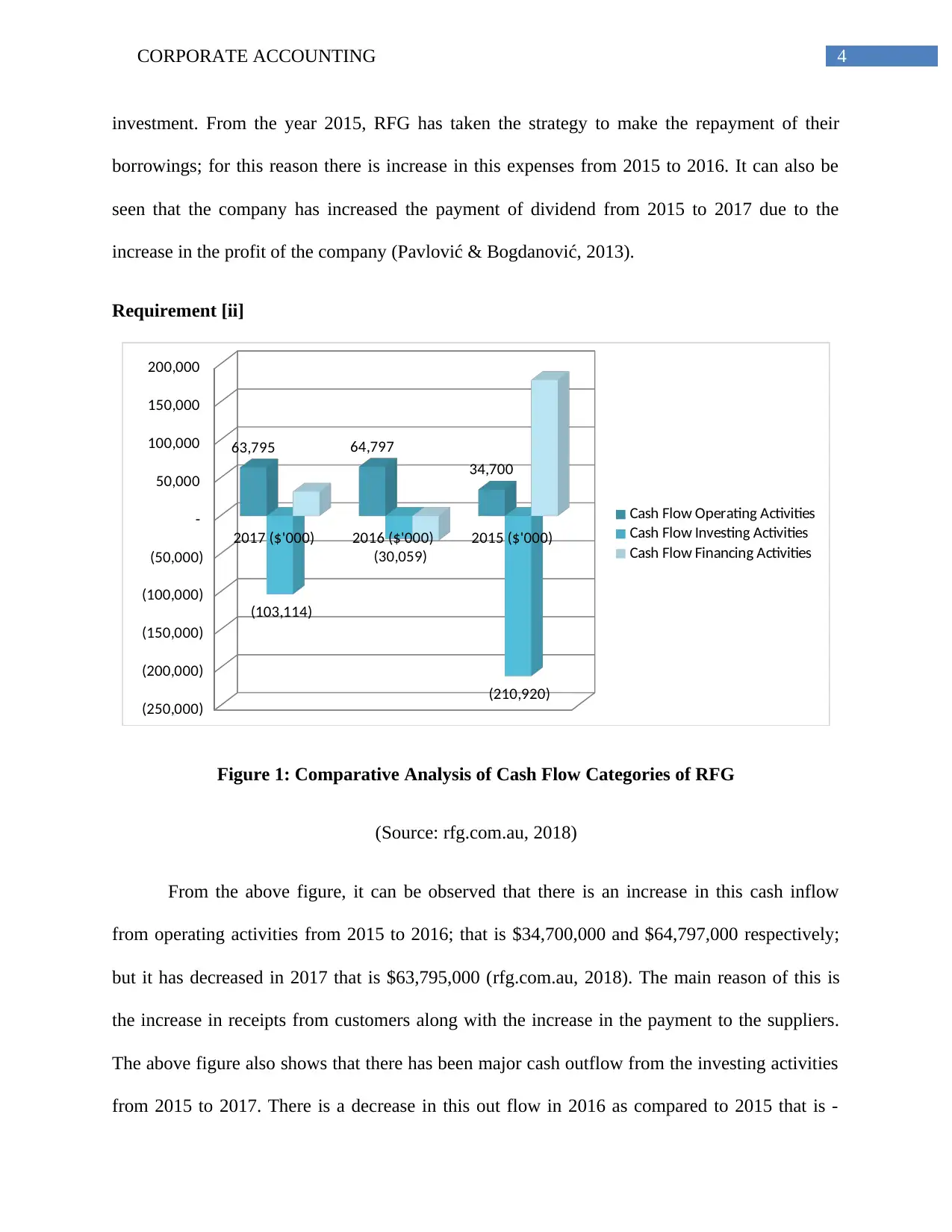

Requirement [ii]

2017 ($'000) 2016 ($'000) 2015 ($'000)

(250,000)

(200,000)

(150,000)

(100,000)

(50,000)

-

50,000

100,000

150,000

200,000

63,795 64,797

34,700

(103,114)

(30,059)

(210,920)

Cash Flow Operating Activities

Cash Flow Investing Activities

Cash Flow Financing Activities

Figure 1: Comparative Analysis of Cash Flow Categories of RFG

(Source: rfg.com.au, 2018)

From the above figure, it can be observed that there is an increase in this cash inflow

from operating activities from 2015 to 2016; that is $34,700,000 and $64,797,000 respectively;

but it has decreased in 2017 that is $63,795,000 (rfg.com.au, 2018). The main reason of this is

the increase in receipts from customers along with the increase in the payment to the suppliers.

The above figure also shows that there has been major cash outflow from the investing activities

from 2015 to 2017. There is a decrease in this out flow in 2016 as compared to 2015 that is -

investment. From the year 2015, RFG has taken the strategy to make the repayment of their

borrowings; for this reason there is increase in this expenses from 2015 to 2016. It can also be

seen that the company has increased the payment of dividend from 2015 to 2017 due to the

increase in the profit of the company (Pavlović & Bogdanović, 2013).

Requirement [ii]

2017 ($'000) 2016 ($'000) 2015 ($'000)

(250,000)

(200,000)

(150,000)

(100,000)

(50,000)

-

50,000

100,000

150,000

200,000

63,795 64,797

34,700

(103,114)

(30,059)

(210,920)

Cash Flow Operating Activities

Cash Flow Investing Activities

Cash Flow Financing Activities

Figure 1: Comparative Analysis of Cash Flow Categories of RFG

(Source: rfg.com.au, 2018)

From the above figure, it can be observed that there is an increase in this cash inflow

from operating activities from 2015 to 2016; that is $34,700,000 and $64,797,000 respectively;

but it has decreased in 2017 that is $63,795,000 (rfg.com.au, 2018). The main reason of this is

the increase in receipts from customers along with the increase in the payment to the suppliers.

The above figure also shows that there has been major cash outflow from the investing activities

from 2015 to 2017. There is a decrease in this out flow in 2016 as compared to 2015 that is -

5CORPORATE ACCOUNTING

$210,920,000 in 2015 and -$30,059,000 in 2016. However, massive increase in this outflow can

be seen in 2017 that is -$103,115,000 due to the payment for property, plant and equipment,

payment of intangible assets and payment for businesses (rfg.com.au, 2018). In case of cash flow

from financing activities, a massive decrease in this can be seen in 2016 as compared to 2015;

that is $179,056,000 in 2015 and -$32,177,000 in 2016. However, increase in this cash inflow

can be seen in the year 2017 that is $31,946,000 (rfg.com.au, 2018). The major reason for this

increase in this cash inflow is the increase in the proceeds of RFG from the issue of shares,

securities, borrowings and others. Thus, from the above discussion, it can be seen that there are

some major increase as well as decrease in the cash flow from all these broad categories.

Other Comprehensive Income Statement

Requirement [iii]

From the 2017 other income statement of RFG, it can be observed that the company has

reported three major items; they are ‘Exchange difference on translation of foreign operations’,

‘Changes in the fair value of Cash flow Hedges’ and ‘Income tax relating to these items’

(rfg.com.au, 2018).

Requirement [iv]

From the above discussion, it can be seen that there are three major items in the other

comprehensive income statement of the company and they are discussed below:

It needs to be mentioned that business organizations use to use the foreign currency

translation reserve with the aim to convert the results of the foreign subsidiaries of the parent

business entity to the currency in which financial reporting has been done. For this reason, it is

considered as a major part of the process of consolidation for the business entities, in which the

$210,920,000 in 2015 and -$30,059,000 in 2016. However, massive increase in this outflow can

be seen in 2017 that is -$103,115,000 due to the payment for property, plant and equipment,

payment of intangible assets and payment for businesses (rfg.com.au, 2018). In case of cash flow

from financing activities, a massive decrease in this can be seen in 2016 as compared to 2015;

that is $179,056,000 in 2015 and -$32,177,000 in 2016. However, increase in this cash inflow

can be seen in the year 2017 that is $31,946,000 (rfg.com.au, 2018). The major reason for this

increase in this cash inflow is the increase in the proceeds of RFG from the issue of shares,

securities, borrowings and others. Thus, from the above discussion, it can be seen that there are

some major increase as well as decrease in the cash flow from all these broad categories.

Other Comprehensive Income Statement

Requirement [iii]

From the 2017 other income statement of RFG, it can be observed that the company has

reported three major items; they are ‘Exchange difference on translation of foreign operations’,

‘Changes in the fair value of Cash flow Hedges’ and ‘Income tax relating to these items’

(rfg.com.au, 2018).

Requirement [iv]

From the above discussion, it can be seen that there are three major items in the other

comprehensive income statement of the company and they are discussed below:

It needs to be mentioned that business organizations use to use the foreign currency

translation reserve with the aim to convert the results of the foreign subsidiaries of the parent

business entity to the currency in which financial reporting has been done. For this reason, it is

considered as a major part of the process of consolidation for the business entities, in which the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

functional currency of the cross-border business entity is determined on the initial basis. After

this process, the business organizations use to re-measure the foreign currency in the current on

which financial reporting is done. Lastly, the profit or loss is recorded on the actual reporting

currency (Eaton, Easterday & Rhodes, 2013).

Business organizations use to use the cash flow hedge reserve at the time of the planning

of removal or minimization of the exposures that arises due to the major change in the cash flow

of the financial assets or liabilities; this is done due to the change in some specific risks like

interest rate, interest of debt and others (Hodgson & Russell, 2014).

The above discussion shows two of the major items that do not come in the consolidated

income statement. Now, it needs to be mentioned that it is the obligation on the business

organizations to impose tax in these financial transactions according to the taxation rules. As the

above discussed items do not appear in the consolidated income statement, the income tax

related to this item do not appear in the consolidated income statement (Eaton, Easterday &

Rhodes, 2013).

Requirement [v]

In this context, it needs to be mentioned that the business organizations use to consider

the other comprehensive income as a diversified view of the net profit of the company. In the

past times, the variation in the profit used to be considered as the external factors of the core

business operations; and the shareholders had to face major volatilities related to their share

capital. However, in case of RFG, the company uses to use the other comprehensive income

statement in order to provide all the required details related to the above-mentioned items

(Bertoni & De Rosa, 2013). For this reason, comprehensive income is considered as the mixture

functional currency of the cross-border business entity is determined on the initial basis. After

this process, the business organizations use to re-measure the foreign currency in the current on

which financial reporting is done. Lastly, the profit or loss is recorded on the actual reporting

currency (Eaton, Easterday & Rhodes, 2013).

Business organizations use to use the cash flow hedge reserve at the time of the planning

of removal or minimization of the exposures that arises due to the major change in the cash flow

of the financial assets or liabilities; this is done due to the change in some specific risks like

interest rate, interest of debt and others (Hodgson & Russell, 2014).

The above discussion shows two of the major items that do not come in the consolidated

income statement. Now, it needs to be mentioned that it is the obligation on the business

organizations to impose tax in these financial transactions according to the taxation rules. As the

above discussed items do not appear in the consolidated income statement, the income tax

related to this item do not appear in the consolidated income statement (Eaton, Easterday &

Rhodes, 2013).

Requirement [v]

In this context, it needs to be mentioned that the business organizations use to consider

the other comprehensive income as a diversified view of the net profit of the company. In the

past times, the variation in the profit used to be considered as the external factors of the core

business operations; and the shareholders had to face major volatilities related to their share

capital. However, in case of RFG, the company uses to use the other comprehensive income

statement in order to provide all the required details related to the above-mentioned items

(Bertoni & De Rosa, 2013). For this reason, comprehensive income is considered as the mixture

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

of other comprehensive income and the standard net income. For this reason, business

organizations use this statement in order to provide a holistic and comprehensive view of the

items that come under the other comprehensive income statement of the business organizations.

In the presence of the above discussed reasons, the items do not appear in the comprehensive

income statement or the statement of profit and loss of the companies (Bertoni & De Rosa,

2013).

Accounting for Corporate Income Tax

Requirement [vi]

Business organizations have to incur different types of expense at the time of conducting

the business operations and one of such expenses is taxation expenses. It needs to be mentioned

that RFG is subjected to taxation under the Australian taxation rules.

From the 2017 Annual Report of RFG, it can be seen that the profit before income tax of

the company for the year 2017 and 2016 is $ 87,613,000 and $76,583,000. According to the

Australian taxation law, the applicable tax rate of RFG for 2017 and 2016 is 30%. Thus, the

company gets their taxation expenses by applying this tax rate on the profit before income tax.

Hence, as per the consolidated statement of profit or loss, the reported taxation expenses of the

company for the year 2017 and 2016 are $25,686,000 and $23,620,000 respectively (rfg.com.au,

2018).

Requirement [vii]

From the analysis of the annual report of RFG, it can be seen that there is difference

between the reported income tax expenses and the actual income tax expenses by applying the

tax rate. In RFG, there are certain factors that contribute to this difference. Non-deductible

of other comprehensive income and the standard net income. For this reason, business

organizations use this statement in order to provide a holistic and comprehensive view of the

items that come under the other comprehensive income statement of the business organizations.

In the presence of the above discussed reasons, the items do not appear in the comprehensive

income statement or the statement of profit and loss of the companies (Bertoni & De Rosa,

2013).

Accounting for Corporate Income Tax

Requirement [vi]

Business organizations have to incur different types of expense at the time of conducting

the business operations and one of such expenses is taxation expenses. It needs to be mentioned

that RFG is subjected to taxation under the Australian taxation rules.

From the 2017 Annual Report of RFG, it can be seen that the profit before income tax of

the company for the year 2017 and 2016 is $ 87,613,000 and $76,583,000. According to the

Australian taxation law, the applicable tax rate of RFG for 2017 and 2016 is 30%. Thus, the

company gets their taxation expenses by applying this tax rate on the profit before income tax.

Hence, as per the consolidated statement of profit or loss, the reported taxation expenses of the

company for the year 2017 and 2016 are $25,686,000 and $23,620,000 respectively (rfg.com.au,

2018).

Requirement [vii]

From the analysis of the annual report of RFG, it can be seen that there is difference

between the reported income tax expenses and the actual income tax expenses by applying the

tax rate. In RFG, there are certain factors that contribute to this difference. Non-deductible

8CORPORATE ACCOUNTING

expenses in order to determine the taxable profit is the first factor as this factors leads to the

addition of $ 879,000 and $ 638,000 for 2017 and 2016 respectively with the taxable expenses.

The presence of different taxation rate is the next reason. The tax rate of RFG is 30% where the

subsidiaries of the company have taxation rates of 28% and 34% (rfg.com.au, 2018). The

presence of deferred tax assets is another reason for the difference as the companies can enjoy

taxation benefit in the presence of deferred tax assets. In the presence of this aspect, there has

been a deduction of $177,000 from the taxation expenses for RFG. The presence of all these

aspects creates the difference.

Requirement [viii]

Deferred tax assets and liabilities are considered as the major aspects of the taxation of

the business organizations; and there is not any exception of this for RFG. From the annual

report of RFG, it can be seen that the company has both deferred tax assets and liabilities. The

amounts of differed tax assets of RFG for 2017 and 2016 are $ 13,657,000 and $ 7,394,000

respectively. At the same time, the amounts of deferred tax liabilities are $ 119,433,000 in 2017

and $ 115,908,000 in 2016 (rfg.com.au, 2018).

There are certain reassigns or which RFG has recorded deferred tax assets and liabilities.

The main reason for the recoding of deferred tax assets is that the company has paid depreciation

for excess amount due to the difference in original depreciation rate and taxable depreciation

rate. The main reason for the development of deferred tax liabilities is the difference in the profit

of the company as RFG had to pay less tax in the present year (Laux, 2013).

expenses in order to determine the taxable profit is the first factor as this factors leads to the

addition of $ 879,000 and $ 638,000 for 2017 and 2016 respectively with the taxable expenses.

The presence of different taxation rate is the next reason. The tax rate of RFG is 30% where the

subsidiaries of the company have taxation rates of 28% and 34% (rfg.com.au, 2018). The

presence of deferred tax assets is another reason for the difference as the companies can enjoy

taxation benefit in the presence of deferred tax assets. In the presence of this aspect, there has

been a deduction of $177,000 from the taxation expenses for RFG. The presence of all these

aspects creates the difference.

Requirement [viii]

Deferred tax assets and liabilities are considered as the major aspects of the taxation of

the business organizations; and there is not any exception of this for RFG. From the annual

report of RFG, it can be seen that the company has both deferred tax assets and liabilities. The

amounts of differed tax assets of RFG for 2017 and 2016 are $ 13,657,000 and $ 7,394,000

respectively. At the same time, the amounts of deferred tax liabilities are $ 119,433,000 in 2017

and $ 115,908,000 in 2016 (rfg.com.au, 2018).

There are certain reassigns or which RFG has recorded deferred tax assets and liabilities.

The main reason for the recoding of deferred tax assets is that the company has paid depreciation

for excess amount due to the difference in original depreciation rate and taxable depreciation

rate. The main reason for the development of deferred tax liabilities is the difference in the profit

of the company as RFG had to pay less tax in the present year (Laux, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Requirement [ix]

From the 2017 Annual Report of RFG, it can be seen that there is not any current tax

assets of the company for the year 2017. However, the current tax asset for RFG for 2016 is

$4,455,000. The current tax liabilities of RFG are $2,546,000 (rfg.com.au, 2018).

There are some major reasons for which there is difference in income tax expenses and

income tax payable and the presence of deferred tax assets is one major reason for this

difference. Companies often pay extra amount of tax as compared to the actual tax expenses. The

extra payment of tax is considered as the deferred tax that is responsible for the difference. The

regulation of financial accounting and taxation accounting is the second reason. For example,

variation in the depreciation expenses can be seen due to this different in accounting ruling.

These are the major reason for the difference (Markle, 2016).

Requirement [x]

RFG has reported $ 25,686,000 in 2017 and 23,620,000 in 2016 as the income tax

expense in income statement; and $ 21,460,000 and $ 19,298,000 for 2017 and 2016 respectively

as income tax expenses in the cash flow statement. Some specific reasons contribute to this

difference (rfg.com.au, 2018). RFG gets the values of income tax expenses of income tax by

applying 30% tax rate on the profit before income tax. However, RFG considers the payment of

income tax under the cash flow from operating activities. It implies that the payment of income

tax is considered as the fulfillment of the current obligation of the companies. In the income

statement, RFG shows the payment of income tax expenses for the current financial year.

However, in case of the taxation expenses in cash flow, the payment is the tax expenses of the

previous year or the tax expenses for the coming years. Thus, in the presence of these reason, the

major difference can be seen in the taxation expenses.

Requirement [ix]

From the 2017 Annual Report of RFG, it can be seen that there is not any current tax

assets of the company for the year 2017. However, the current tax asset for RFG for 2016 is

$4,455,000. The current tax liabilities of RFG are $2,546,000 (rfg.com.au, 2018).

There are some major reasons for which there is difference in income tax expenses and

income tax payable and the presence of deferred tax assets is one major reason for this

difference. Companies often pay extra amount of tax as compared to the actual tax expenses. The

extra payment of tax is considered as the deferred tax that is responsible for the difference. The

regulation of financial accounting and taxation accounting is the second reason. For example,

variation in the depreciation expenses can be seen due to this different in accounting ruling.

These are the major reason for the difference (Markle, 2016).

Requirement [x]

RFG has reported $ 25,686,000 in 2017 and 23,620,000 in 2016 as the income tax

expense in income statement; and $ 21,460,000 and $ 19,298,000 for 2017 and 2016 respectively

as income tax expenses in the cash flow statement. Some specific reasons contribute to this

difference (rfg.com.au, 2018). RFG gets the values of income tax expenses of income tax by

applying 30% tax rate on the profit before income tax. However, RFG considers the payment of

income tax under the cash flow from operating activities. It implies that the payment of income

tax is considered as the fulfillment of the current obligation of the companies. In the income

statement, RFG shows the payment of income tax expenses for the current financial year.

However, in case of the taxation expenses in cash flow, the payment is the tax expenses of the

previous year or the tax expenses for the coming years. Thus, in the presence of these reason, the

major difference can be seen in the taxation expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Requirement [xi]

From the above discussion, it can be observed that there is not any confusing or

surprising factor in the taxation accounting of RFG as the company has carried out their taxation

operations by complying with the Australian taxation law. However, it an interesting factor to

observe the way in which RFG has carried out their taxation expenses. Thus, from observing the

taxation accounting of RFG, one can get deep insight about how to carry on the taxation

operations of the companies.

Requirement [xi]

From the above discussion, it can be observed that there is not any confusing or

surprising factor in the taxation accounting of RFG as the company has carried out their taxation

operations by complying with the Australian taxation law. However, it an interesting factor to

observe the way in which RFG has carried out their taxation expenses. Thus, from observing the

taxation accounting of RFG, one can get deep insight about how to carry on the taxation

operations of the companies.

11CORPORATE ACCOUNTING

References

2017 Annual Report. (2018). Retrieved from

http://rfg.com.au/wp-content/uploads/2018/02/RFGLAnnualReport2017.pdf

Annual Report 2015. (2018). Retrieved from

http://rfg.com.au/wp-content/uploads/2018/02/RFG2015AnnualReport.pdf

Bertoni, M., & De Rosa, B. (2013). Comprehensive income, fair value, and conservatism: A

conceptual framework for reporting financial performance.

Black, D. E. (2016). Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), 9-45.

Celebrating 10 Years Of Transformative Growth, Creating Australia’S Premier Food &

Beverage Comp. (2018). Annual Report 2016. Retrieved from http://rfg.com.au/wp-

content/uploads/2018/02/RFGAnnualReport2016.pdf

Eaton, T. V., Easterday, K. E., & Rhodes, M. R. (2013). The presentation of other

comprehensive income. The CPA Journal, 83(3), 32.

Hodgson, A., & Russell, M. (2014). Comprehending comprehensive income. Australian

Accounting Review, 24(2), 100-110.

Laux, R. C. (2013). The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), 1357-1383.

Markle, K. (2016). A Comparison of the Tax‐Motivated Income Shifting of Multinationals in

Territorial and Worldwide Countries. Contemporary Accounting Research, 33(1), 7-43.

References

2017 Annual Report. (2018). Retrieved from

http://rfg.com.au/wp-content/uploads/2018/02/RFGLAnnualReport2017.pdf

Annual Report 2015. (2018). Retrieved from

http://rfg.com.au/wp-content/uploads/2018/02/RFG2015AnnualReport.pdf

Bertoni, M., & De Rosa, B. (2013). Comprehensive income, fair value, and conservatism: A

conceptual framework for reporting financial performance.

Black, D. E. (2016). Other comprehensive income: a review and directions for future

research. Accounting & Finance, 56(1), 9-45.

Celebrating 10 Years Of Transformative Growth, Creating Australia’S Premier Food &

Beverage Comp. (2018). Annual Report 2016. Retrieved from http://rfg.com.au/wp-

content/uploads/2018/02/RFGAnnualReport2016.pdf

Eaton, T. V., Easterday, K. E., & Rhodes, M. R. (2013). The presentation of other

comprehensive income. The CPA Journal, 83(3), 32.

Hodgson, A., & Russell, M. (2014). Comprehending comprehensive income. Australian

Accounting Review, 24(2), 100-110.

Laux, R. C. (2013). The association between deferred tax assets and liabilities and future tax

payments. The Accounting Review, 88(4), 1357-1383.

Markle, K. (2016). A Comparison of the Tax‐Motivated Income Shifting of Multinationals in

Territorial and Worldwide Countries. Contemporary Accounting Research, 33(1), 7-43.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.