Management Accounting Report: Financial Analysis of Rio Tinto

VerifiedAdded on 2023/01/13

|22

|5429

|59

Report

AI Summary

This report delves into the realm of management accounting, providing a detailed analysis of its principles and applications within a business context, using Rio Tinto as a case study. The report begins by defining management accounting and outlining its essential requirements, including cost accounting, inventory management systems, job costing, and price optimization. It explores the differences between financial and management accounting, emphasizing the internal focus of the latter. The core of the report examines various management accounting reporting methods, such as inventory reports, cost accounting reports, and performance reports. Furthermore, it presents a comparative analysis of costing techniques, specifically marginal and absorption costing, including detailed cost cards and profit and loss statements. The report also touches upon the use of budgetary planning tools and management accounting's role in solving financial problems, including financial governance for prevention. Finally, it highlights the characteristics of an effective management accountant and concludes with a summary of the key findings and their implications for Rio Tinto's financial management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

Management accounting and essential requirements of MA Systems............................................1

MA- Definitions...........................................................................................................................1

Functions of management accounting includes...........................................................................1

Difference between Financial accounting and MA.....................................................................2

Essential requirements of MA systems, benefits and application..............................................2

Methods of management accounting reporting and integration with MA reporting...................4

Costing techniques in management accounting...............................................................................7

Report containing marginal and absorption costing techniques..................................................7

Use of Budgetary planning tools...................................................................................................12

Different types of budgetary planning tools used by organisation............................................12

MA in solving the financial problems...........................................................................................14

Methods to identify the financial problems...............................................................................14

Financial governance for preventing financial problems..........................................................16

Characteristics of the effective management accountant and its application............................16

MA systems in solving the financial problems..........................................................................16

CONCLUSIONS...........................................................................................................................17

REFERENCES..............................................................................................................................18

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

Management accounting and essential requirements of MA Systems............................................1

MA- Definitions...........................................................................................................................1

Functions of management accounting includes...........................................................................1

Difference between Financial accounting and MA.....................................................................2

Essential requirements of MA systems, benefits and application..............................................2

Methods of management accounting reporting and integration with MA reporting...................4

Costing techniques in management accounting...............................................................................7

Report containing marginal and absorption costing techniques..................................................7

Use of Budgetary planning tools...................................................................................................12

Different types of budgetary planning tools used by organisation............................................12

MA in solving the financial problems...........................................................................................14

Methods to identify the financial problems...............................................................................14

Financial governance for preventing financial problems..........................................................16

Characteristics of the effective management accountant and its application............................16

MA systems in solving the financial problems..........................................................................16

CONCLUSIONS...........................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting is used by organisation as it helps in integrating the financial

function and other activities of business. This is essential for the business enterprise to have an

effective management control. MA provides various concepts and techniques that helps

management in making decisions regarding the strategic and operational strategies of the

business. MA accounting helps company in establishing effective functions for the growth and

success and also for achieving the success in the organisation (Shea and et.al., 2018). Present

report is based on Rio Tinto that is a metal manufacturing and mining company. It will contain

management accounting systems and its application in organisation. The knowledge about the

MA reporting methods and its integrating with the MA systems. Study will also provide different

planning tools used by organisation for effective control and planning. Further use of MA

methods in solving the financial issues of company. The report will enhance the understanding of

the management accounting concepts.

Management accounting and essential requirements of MA Systems.

MA- Definitions

''It is defined as process involving identification, accumulation, measurement,

communication and interpretation of the financial informations used by the management for

planning, evaluating and controlling organisation.'' By – Institute of Management Accountants

(IMA)

''MA is an accounting process providing financials and the resources of company in

decision making. ''

Management accounting is for internal use of the organisation. Management accountants

are primarily concentrated over the identifying the loopholes in the operations and establishing

corrective strategies for organisational goals and objectives. They prepare reports based on the

operations and activities being carried out by the organisation (Abu, Nor and Rahman, 2018).

They play an effective role in management decision making.

Functions of management accounting includes

Margin analysis – To determine amount of profits and the cash flows that a business will be

generating from the specific products, product line, stores or customers.

1

Management accounting is used by organisation as it helps in integrating the financial

function and other activities of business. This is essential for the business enterprise to have an

effective management control. MA provides various concepts and techniques that helps

management in making decisions regarding the strategic and operational strategies of the

business. MA accounting helps company in establishing effective functions for the growth and

success and also for achieving the success in the organisation (Shea and et.al., 2018). Present

report is based on Rio Tinto that is a metal manufacturing and mining company. It will contain

management accounting systems and its application in organisation. The knowledge about the

MA reporting methods and its integrating with the MA systems. Study will also provide different

planning tools used by organisation for effective control and planning. Further use of MA

methods in solving the financial issues of company. The report will enhance the understanding of

the management accounting concepts.

Management accounting and essential requirements of MA Systems.

MA- Definitions

''It is defined as process involving identification, accumulation, measurement,

communication and interpretation of the financial informations used by the management for

planning, evaluating and controlling organisation.'' By – Institute of Management Accountants

(IMA)

''MA is an accounting process providing financials and the resources of company in

decision making. ''

Management accounting is for internal use of the organisation. Management accountants

are primarily concentrated over the identifying the loopholes in the operations and establishing

corrective strategies for organisational goals and objectives. They prepare reports based on the

operations and activities being carried out by the organisation (Abu, Nor and Rahman, 2018).

They play an effective role in management decision making.

Functions of management accounting includes

Margin analysis – To determine amount of profits and the cash flows that a business will be

generating from the specific products, product line, stores or customers.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Constraints analysis – This refers to identifying the bottlenecks in an enterprise and their impact

over ability of business in earning its profits and revenues.

Break even analysis – This involves calculating the break even from contribution and unit

volume mix. This helps in determines price levels for its products or services.

Inventory valuation – It is concerned with measuring the direct cost, cost of goods sold, and the

inventory items.

Forecasting – It is one of the major function of MA in which forecasts about the future income

and expenditures of company. This is done after analysing the previous trends and market

conditions.

Capital budgeting – It refers to identifying requirement of fixed assets and costs involved. This

involves allocation of costs to best option available.

Difference between Financial accounting and MA

Basis Management Accounting Financial Accounting

Objective To manage the operations of

company in cost efficient manner

identifying the financial issues.

It is concerned with representing the

financial transactions carried out by the

business.

Purpose They are prepared for the internal

management for decision making.

This is used for reporting to the

external parties for decision making.

Regulations Management accounting is not

regulated by law.

FA is regulated by the accounting

standards and reporting frameworks

(Geiszler, Baker and Lippitt, 2017).

Users It is used by internal managers and

executives of organisation.

The users of FA are investors,

shareholders and regulators.

Mandatory Presentation and preparation of

financial reports is not mandatory.

It is mandatory for the organisations to

prepare and present finacial statements.

Frequency MA reports are prepared as per the

requirement of management.

The financial statements are to be

prepared by organisation at every year

end.

Essential requirements of MA systems, benefits and application

Cost Accounting

Cost accounting refers to recording of financial transactions of business. Cost accounting

involves recording all the information related to direct and indirect costs incurred for

manufacturing the product. The cost accounting is used by organisation for pricing the products

2

over ability of business in earning its profits and revenues.

Break even analysis – This involves calculating the break even from contribution and unit

volume mix. This helps in determines price levels for its products or services.

Inventory valuation – It is concerned with measuring the direct cost, cost of goods sold, and the

inventory items.

Forecasting – It is one of the major function of MA in which forecasts about the future income

and expenditures of company. This is done after analysing the previous trends and market

conditions.

Capital budgeting – It refers to identifying requirement of fixed assets and costs involved. This

involves allocation of costs to best option available.

Difference between Financial accounting and MA

Basis Management Accounting Financial Accounting

Objective To manage the operations of

company in cost efficient manner

identifying the financial issues.

It is concerned with representing the

financial transactions carried out by the

business.

Purpose They are prepared for the internal

management for decision making.

This is used for reporting to the

external parties for decision making.

Regulations Management accounting is not

regulated by law.

FA is regulated by the accounting

standards and reporting frameworks

(Geiszler, Baker and Lippitt, 2017).

Users It is used by internal managers and

executives of organisation.

The users of FA are investors,

shareholders and regulators.

Mandatory Presentation and preparation of

financial reports is not mandatory.

It is mandatory for the organisations to

prepare and present finacial statements.

Frequency MA reports are prepared as per the

requirement of management.

The financial statements are to be

prepared by organisation at every year

end.

Essential requirements of MA systems, benefits and application

Cost Accounting

Cost accounting refers to recording of financial transactions of business. Cost accounting

involves recording all the information related to direct and indirect costs incurred for

manufacturing the product. The cost accounting is used by organisation for pricing the products

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

appropriately. Cost accounting is required for having proper record of all the cost transactions for

management decision-making. It is used by the enterprise for pricing its goods or services and

for determining the profit margins associated with each product. It helps in controlling the cost

and expenditures using variance analysis.

Benefits

Cost accounting helps Rio Tinto in keeping track of all cost information.

It involves comparing the actual and budgeted outputs and taking steps for reducing the

variances. It helps business to keep its costs under control.

Application.

Cost accounting is applied in the production process for keeping record of all the costs

and business informations for pricing its metals and materials (Chouhan, Soral and Chandra,

2017).

Inventory management systems

Inventory management system refers to the process of having proper record of each and

every stock of company. It records every inventory information like of raw materials, inventory

consumption, finished goods and company assets. There are technologies available that helps

company in maintaining the inventory information. Inventory management has helped

management in taking steps related to the effective management of all the company stocks.

Using the inventory management makes forecast about its future requirement of the production

based on the frequency of movements. This helps the business in keeping proper stock of all the

material of the business and prevent it from going out of stock.

Benefits

Inventory management has helped company in keeping track of all the inventory

movements within the organisation.

It helps business in placing timely orders for raw materials. This helps the business in making forecasts about future requirement analysing the

trends.

Applications

This is used by Rio Tinto for maintaining a structured information about the stocks of

each metals and materials separately.

3

management decision-making. It is used by the enterprise for pricing its goods or services and

for determining the profit margins associated with each product. It helps in controlling the cost

and expenditures using variance analysis.

Benefits

Cost accounting helps Rio Tinto in keeping track of all cost information.

It involves comparing the actual and budgeted outputs and taking steps for reducing the

variances. It helps business to keep its costs under control.

Application.

Cost accounting is applied in the production process for keeping record of all the costs

and business informations for pricing its metals and materials (Chouhan, Soral and Chandra,

2017).

Inventory management systems

Inventory management system refers to the process of having proper record of each and

every stock of company. It records every inventory information like of raw materials, inventory

consumption, finished goods and company assets. There are technologies available that helps

company in maintaining the inventory information. Inventory management has helped

management in taking steps related to the effective management of all the company stocks.

Using the inventory management makes forecast about its future requirement of the production

based on the frequency of movements. This helps the business in keeping proper stock of all the

material of the business and prevent it from going out of stock.

Benefits

Inventory management has helped company in keeping track of all the inventory

movements within the organisation.

It helps business in placing timely orders for raw materials. This helps the business in making forecasts about future requirement analysing the

trends.

Applications

This is used by Rio Tinto for maintaining a structured information about the stocks of

each metals and materials separately.

3

Job Costing

Job Costing refers to measuring the direct and indirect costs associated with a particular

job. It involves recording of cost for manufacturing job in place of the process involved. The

company can calculate the costs associated every job separately (Aleem, Khan and Hamad,

2016). It requires company to keep track of all the cost related to the job. This helps

managements in taking decisions related to the costs of job.

Benefits

This is used by organisation for identifying the cost of every job.

Job costing helps in costing the special orders by major clients. This helps company in deciding the profit margins for the job.

Application

It is applied by Rio Tinto in measuring the profitability of the job carried out for the

special orders for the metals.

Price Optimisation

This is a model used by organisation which involves mathematical programs and

calculations for the different price level and its impact over demand. This is an effective where

the mathematical concepts are used for assessing the variations accurately and reliably by the

business (Labro, 2019). Results obtained from the mathematical concepts are used along with

stock levels and costs for deciding the optimum price levels for a product.

Benefits

It helps in deciding the price of products that is reasonable.

The variations in demand at different prices helps them in taking pricing decisions. Using this technique company can improve its profitability.

Application

Price optimisation process is used by Rio Tinto in decision making process where it

makes analysis for pricing the metals based on their demand.

Methods of management accounting reporting and integration with MA reporting

Inventory reports

Inventory reports contains the detailed information about all the company inventory

related to every separately. This involves keeping record of all the transactions and inventory

4

Job Costing refers to measuring the direct and indirect costs associated with a particular

job. It involves recording of cost for manufacturing job in place of the process involved. The

company can calculate the costs associated every job separately (Aleem, Khan and Hamad,

2016). It requires company to keep track of all the cost related to the job. This helps

managements in taking decisions related to the costs of job.

Benefits

This is used by organisation for identifying the cost of every job.

Job costing helps in costing the special orders by major clients. This helps company in deciding the profit margins for the job.

Application

It is applied by Rio Tinto in measuring the profitability of the job carried out for the

special orders for the metals.

Price Optimisation

This is a model used by organisation which involves mathematical programs and

calculations for the different price level and its impact over demand. This is an effective where

the mathematical concepts are used for assessing the variations accurately and reliably by the

business (Labro, 2019). Results obtained from the mathematical concepts are used along with

stock levels and costs for deciding the optimum price levels for a product.

Benefits

It helps in deciding the price of products that is reasonable.

The variations in demand at different prices helps them in taking pricing decisions. Using this technique company can improve its profitability.

Application

Price optimisation process is used by Rio Tinto in decision making process where it

makes analysis for pricing the metals based on their demand.

Methods of management accounting reporting and integration with MA reporting

Inventory reports

Inventory reports contains the detailed information about all the company inventory

related to every separately. This involves keeping record of all the transactions and inventory

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

movements. Inventory management system provide the information based on which projections

about the future requirements and frequency of inventory movements can be made.

Cost accounting report

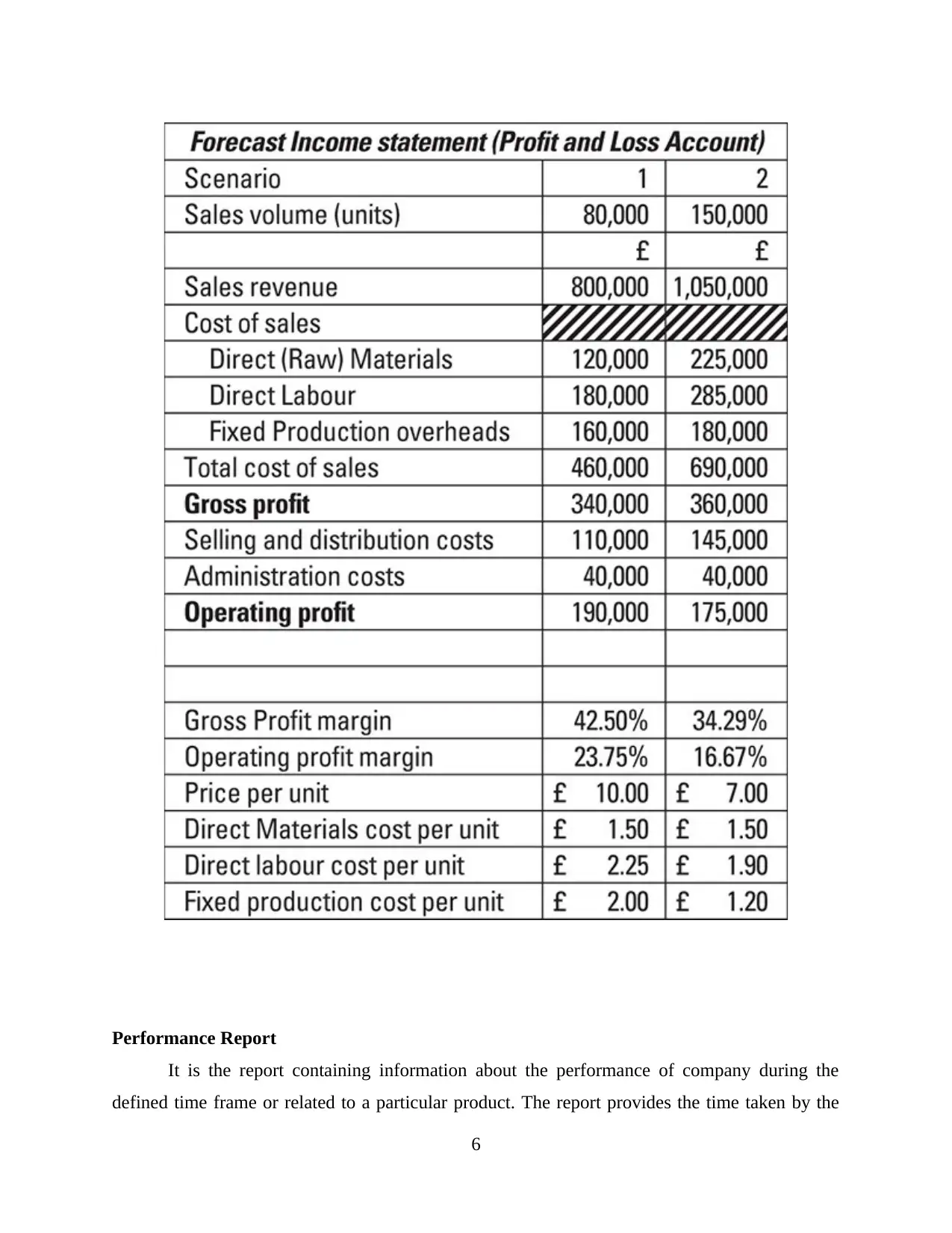

This report contain information on different products and its manufacturing costs

(Agrawal, 2018). These costs provide important information for decision making. Cost

accounting systems provide information about the costs incurred on the basis of which costs

reports are prepared. It contains the variations between the actual and budgeted cost levels. On

this basis it takes corrective steps for reducing the variations and controlling costs. Example of

cost report is as follows:

5

about the future requirements and frequency of inventory movements can be made.

Cost accounting report

This report contain information on different products and its manufacturing costs

(Agrawal, 2018). These costs provide important information for decision making. Cost

accounting systems provide information about the costs incurred on the basis of which costs

reports are prepared. It contains the variations between the actual and budgeted cost levels. On

this basis it takes corrective steps for reducing the variations and controlling costs. Example of

cost report is as follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

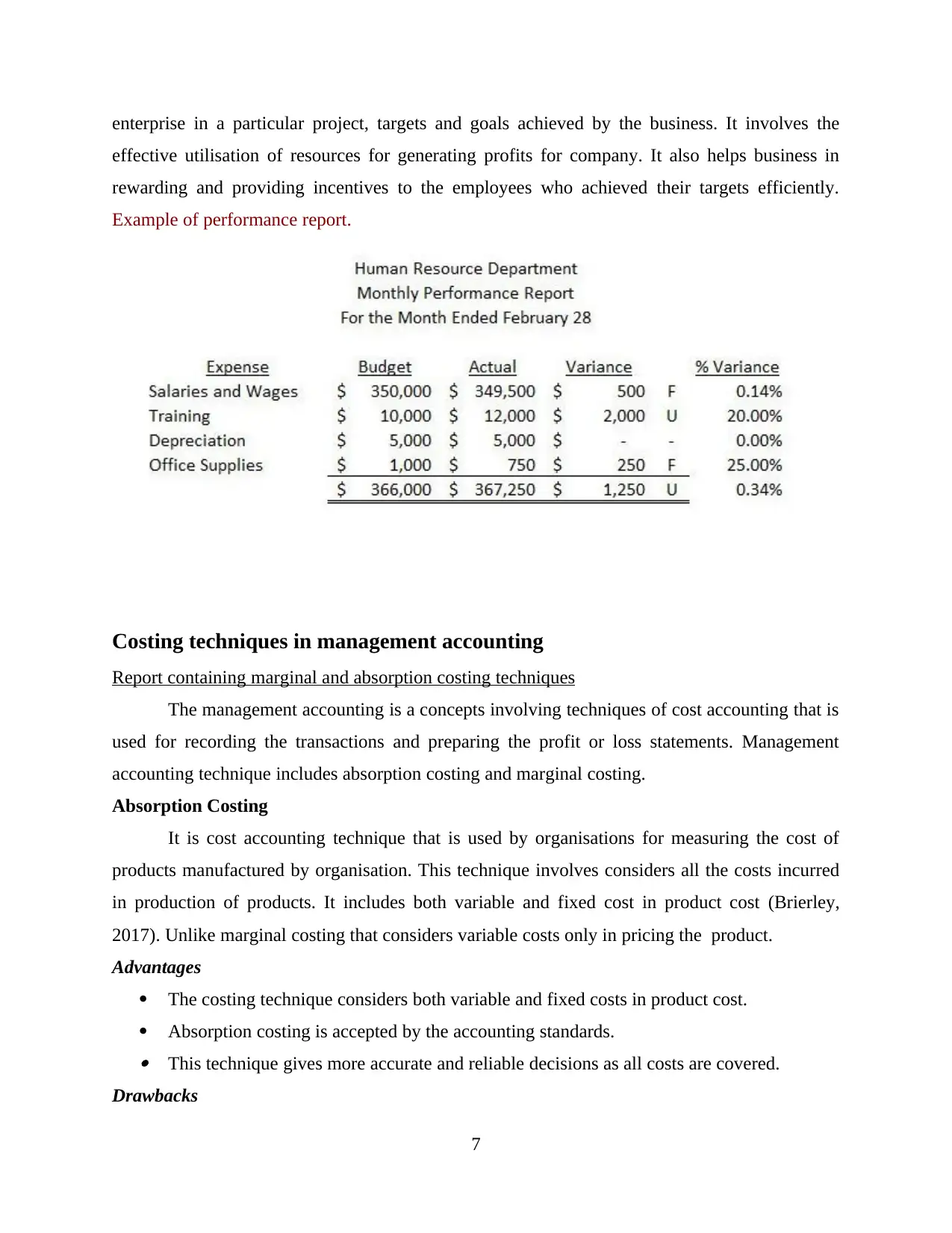

Performance Report

It is the report containing information about the performance of company during the

defined time frame or related to a particular product. The report provides the time taken by the

6

It is the report containing information about the performance of company during the

defined time frame or related to a particular product. The report provides the time taken by the

6

enterprise in a particular project, targets and goals achieved by the business. It involves the

effective utilisation of resources for generating profits for company. It also helps business in

rewarding and providing incentives to the employees who achieved their targets efficiently.

Example of performance report.

Costing techniques in management accounting

Report containing marginal and absorption costing techniques

The management accounting is a concepts involving techniques of cost accounting that is

used for recording the transactions and preparing the profit or loss statements. Management

accounting technique includes absorption costing and marginal costing.

Absorption Costing

It is cost accounting technique that is used by organisations for measuring the cost of

products manufactured by organisation. This technique involves considers all the costs incurred

in production of products. It includes both variable and fixed cost in product cost (Brierley,

2017). Unlike marginal costing that considers variable costs only in pricing the product.

Advantages

The costing technique considers both variable and fixed costs in product cost.

Absorption costing is accepted by the accounting standards. This technique gives more accurate and reliable decisions as all costs are covered.

Drawbacks

7

effective utilisation of resources for generating profits for company. It also helps business in

rewarding and providing incentives to the employees who achieved their targets efficiently.

Example of performance report.

Costing techniques in management accounting

Report containing marginal and absorption costing techniques

The management accounting is a concepts involving techniques of cost accounting that is

used for recording the transactions and preparing the profit or loss statements. Management

accounting technique includes absorption costing and marginal costing.

Absorption Costing

It is cost accounting technique that is used by organisations for measuring the cost of

products manufactured by organisation. This technique involves considers all the costs incurred

in production of products. It includes both variable and fixed cost in product cost (Brierley,

2017). Unlike marginal costing that considers variable costs only in pricing the product.

Advantages

The costing technique considers both variable and fixed costs in product cost.

Absorption costing is accepted by the accounting standards. This technique gives more accurate and reliable decisions as all costs are covered.

Drawbacks

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

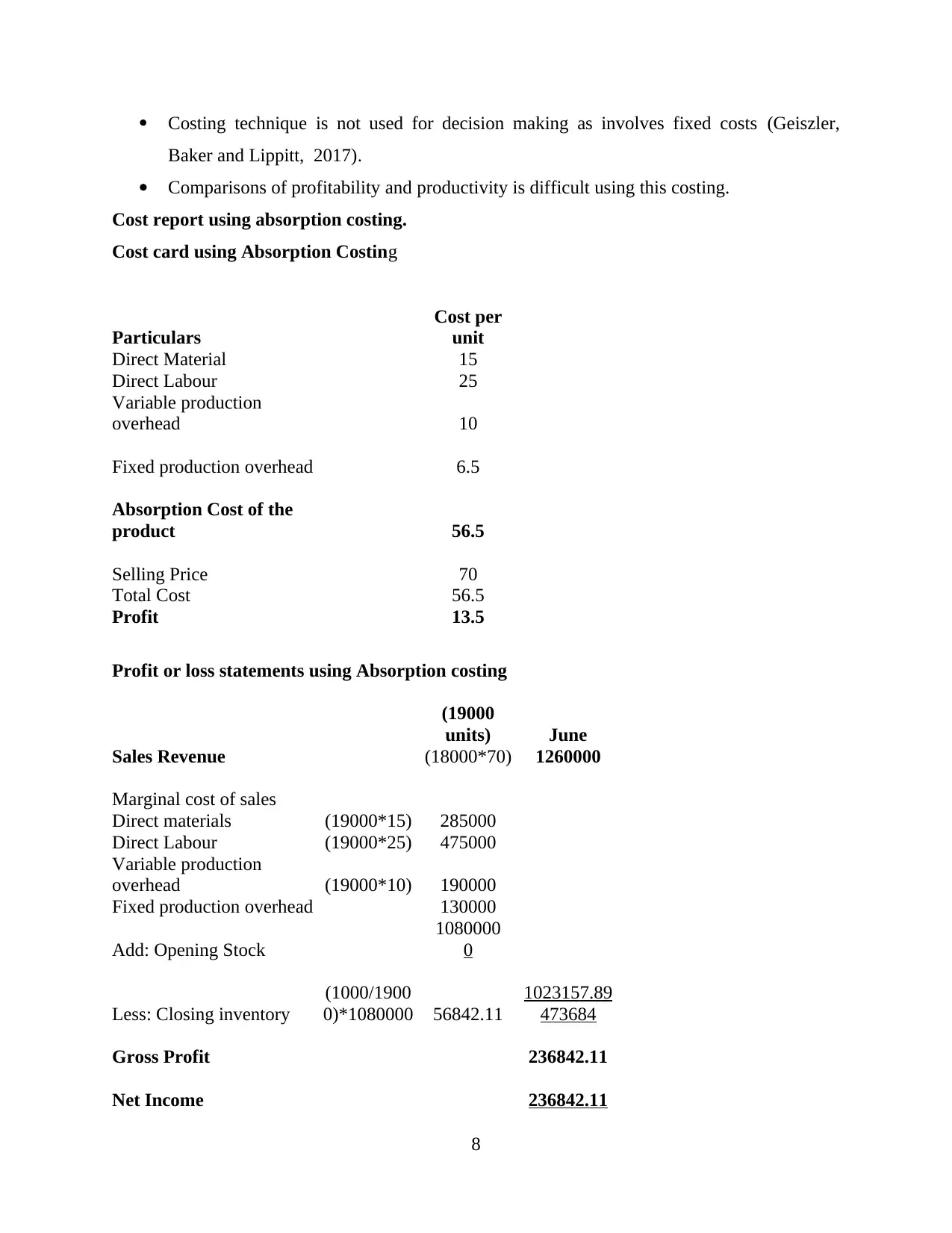

Costing technique is not used for decision making as involves fixed costs (Geiszler,

Baker and Lippitt, 2017).

Comparisons of profitability and productivity is difficult using this costing.

Cost report using absorption costing.

Cost card using Absorption Costing

Particulars

Cost per

unit

Direct Material 15

Direct Labour 25

Variable production

overhead 10

Fixed production overhead 6.5

Absorption Cost of the

product 56.5

Selling Price 70

Total Cost 56.5

Profit 13.5

Profit or loss statements using Absorption costing

(19000

units) June

Sales Revenue (18000*70) 1260000

Marginal cost of sales

Direct materials (19000*15) 285000

Direct Labour (19000*25) 475000

Variable production

overhead (19000*10) 190000

Fixed production overhead 130000

1080000

Add: Opening Stock 0

Less: Closing inventory

(1000/1900

0)*1080000 56842.11

1023157.89

473684

Gross Profit 236842.11

Net Income 236842.11

8

Baker and Lippitt, 2017).

Comparisons of profitability and productivity is difficult using this costing.

Cost report using absorption costing.

Cost card using Absorption Costing

Particulars

Cost per

unit

Direct Material 15

Direct Labour 25

Variable production

overhead 10

Fixed production overhead 6.5

Absorption Cost of the

product 56.5

Selling Price 70

Total Cost 56.5

Profit 13.5

Profit or loss statements using Absorption costing

(19000

units) June

Sales Revenue (18000*70) 1260000

Marginal cost of sales

Direct materials (19000*15) 285000

Direct Labour (19000*25) 475000

Variable production

overhead (19000*10) 190000

Fixed production overhead 130000

1080000

Add: Opening Stock 0

Less: Closing inventory

(1000/1900

0)*1080000 56842.11

1023157.89

473684

Gross Profit 236842.11

Net Income 236842.11

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

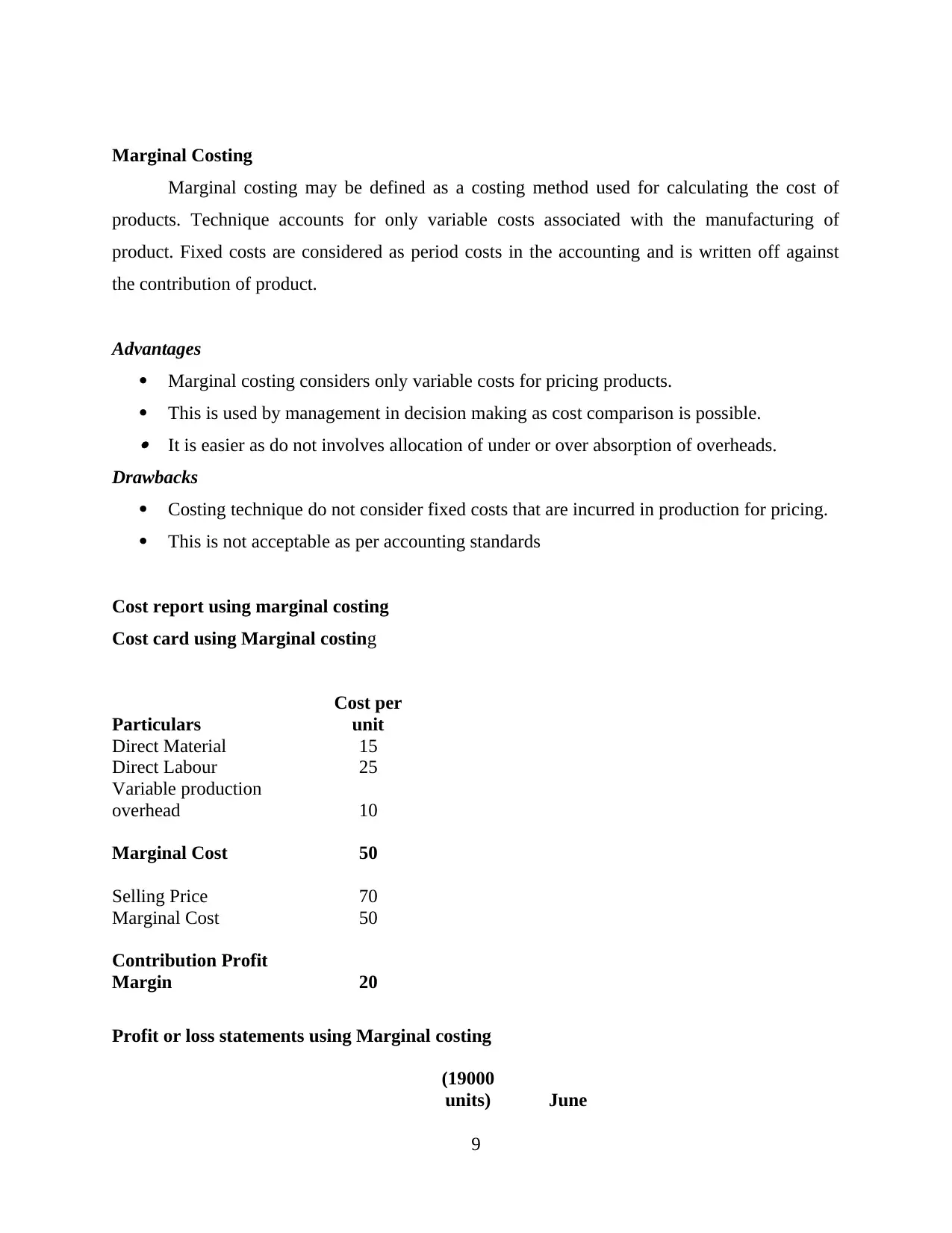

Marginal Costing

Marginal costing may be defined as a costing method used for calculating the cost of

products. Technique accounts for only variable costs associated with the manufacturing of

product. Fixed costs are considered as period costs in the accounting and is written off against

the contribution of product.

Advantages

Marginal costing considers only variable costs for pricing products.

This is used by management in decision making as cost comparison is possible. It is easier as do not involves allocation of under or over absorption of overheads.

Drawbacks

Costing technique do not consider fixed costs that are incurred in production for pricing.

This is not acceptable as per accounting standards

Cost report using marginal costing

Cost card using Marginal costing

Particulars

Cost per

unit

Direct Material 15

Direct Labour 25

Variable production

overhead 10

Marginal Cost 50

Selling Price 70

Marginal Cost 50

Contribution Profit

Margin 20

Profit or loss statements using Marginal costing

(19000

units) June

9

Marginal costing may be defined as a costing method used for calculating the cost of

products. Technique accounts for only variable costs associated with the manufacturing of

product. Fixed costs are considered as period costs in the accounting and is written off against

the contribution of product.

Advantages

Marginal costing considers only variable costs for pricing products.

This is used by management in decision making as cost comparison is possible. It is easier as do not involves allocation of under or over absorption of overheads.

Drawbacks

Costing technique do not consider fixed costs that are incurred in production for pricing.

This is not acceptable as per accounting standards

Cost report using marginal costing

Cost card using Marginal costing

Particulars

Cost per

unit

Direct Material 15

Direct Labour 25

Variable production

overhead 10

Marginal Cost 50

Selling Price 70

Marginal Cost 50

Contribution Profit

Margin 20

Profit or loss statements using Marginal costing

(19000

units) June

9

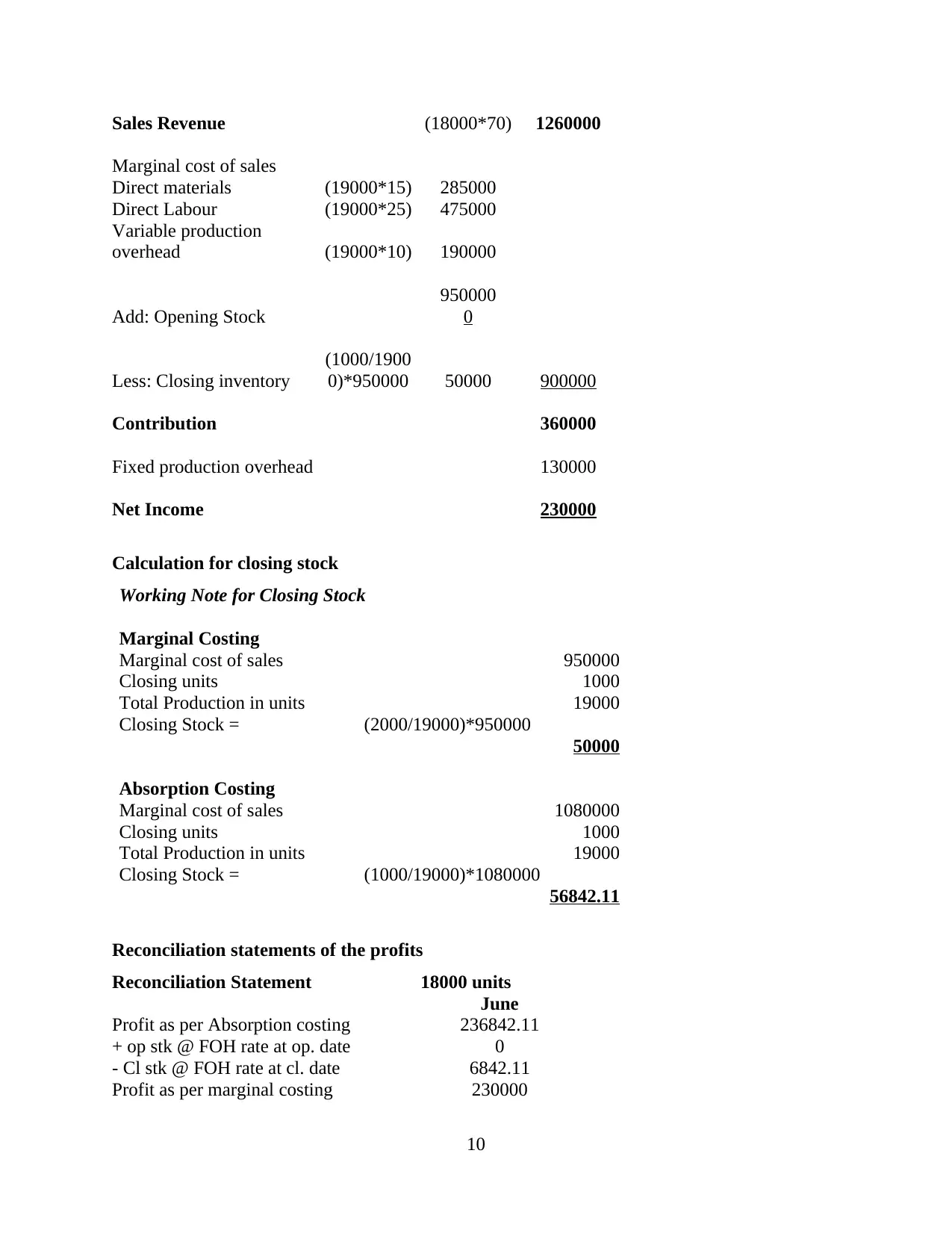

Sales Revenue (18000*70) 1260000

Marginal cost of sales

Direct materials (19000*15) 285000

Direct Labour (19000*25) 475000

Variable production

overhead (19000*10) 190000

950000

Add: Opening Stock 0

Less: Closing inventory

(1000/1900

0)*950000 50000 900000

Contribution 360000

Fixed production overhead 130000

Net Income 230000

Calculation for closing stock

Working Note for Closing Stock

Marginal Costing

Marginal cost of sales 950000

Closing units 1000

Total Production in units 19000

Closing Stock = (2000/19000)*950000

50000

Absorption Costing

Marginal cost of sales 1080000

Closing units 1000

Total Production in units 19000

Closing Stock = (1000/19000)*1080000

56842.11

Reconciliation statements of the profits

Reconciliation Statement 18000 units

June

Profit as per Absorption costing 236842.11

+ op stk @ FOH rate at op. date 0

- Cl stk @ FOH rate at cl. date 6842.11

Profit as per marginal costing 230000

10

Marginal cost of sales

Direct materials (19000*15) 285000

Direct Labour (19000*25) 475000

Variable production

overhead (19000*10) 190000

950000

Add: Opening Stock 0

Less: Closing inventory

(1000/1900

0)*950000 50000 900000

Contribution 360000

Fixed production overhead 130000

Net Income 230000

Calculation for closing stock

Working Note for Closing Stock

Marginal Costing

Marginal cost of sales 950000

Closing units 1000

Total Production in units 19000

Closing Stock = (2000/19000)*950000

50000

Absorption Costing

Marginal cost of sales 1080000

Closing units 1000

Total Production in units 19000

Closing Stock = (1000/19000)*1080000

56842.11

Reconciliation statements of the profits

Reconciliation Statement 18000 units

June

Profit as per Absorption costing 236842.11

+ op stk @ FOH rate at op. date 0

- Cl stk @ FOH rate at cl. date 6842.11

Profit as per marginal costing 230000

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.