Financial Reporting 1 Report: Analysis of Rio Tinto Annual Report

VerifiedAdded on 2023/04/21

|9

|2056

|162

Report

AI Summary

This report provides an analysis of Rio Tinto's annual report, focusing on its compliance with Australian Accounting Standards (AASBs) and the disclosure of relevant information. The report examines the application of the AASB Conceptual Framework, particularly concerning social accountability in financial reporting. It explores the necessity of establishing and developing AASBs in Australian business practices and details the types of financial and non-financial information disclosed by Rio Tinto. The report further investigates the incentives given to managers to disclose certain information and assesses the reaction of investors and the securities market to the disclosed information. The analysis concludes that Rio Tinto's annual report generally complies with the objectives of financial reporting, providing relevant information for stakeholders to make informed decisions, with a focus on both financial and non-financial aspects, including key performance indicators and sustainable development.

Financial Reporting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present aims to examine the annual report of Rio Tinto in context to its compliance

with disclosure requirement and to check whether annual report all report information which is

very important for the society. It has been found that Rio Tinto has been successful in reporting

all the relevant information for all users of the annual report so that they can take their

judgments in correct manner.

2

The present aims to examine the annual report of Rio Tinto in context to its compliance

with disclosure requirement and to check whether annual report all report information which is

very important for the society. It has been found that Rio Tinto has been successful in reporting

all the relevant information for all users of the annual report so that they can take their

judgments in correct manner.

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part 1: Analysis of the statement ‘Social Accountability is considered in the AASB Conceptual

Framework as a part of the Objectives of the General Purpose Financial Report (GPFR)’............4

Part 2: Necessity of Establishing and Developing AASBs in Australian Business Practices.........4

Part 3: Types of information disclosed in the annual report of Rio Tinto.......................................5

Part 4: Incentives given to the managers to disclose the certain type of information in the annual

report................................................................................................................................................5

Part 5: Reaction of investors or securities market on disclosure of certain information provided

in the annual report..........................................................................................................................8

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part 1: Analysis of the statement ‘Social Accountability is considered in the AASB Conceptual

Framework as a part of the Objectives of the General Purpose Financial Report (GPFR)’............4

Part 2: Necessity of Establishing and Developing AASBs in Australian Business Practices.........4

Part 3: Types of information disclosed in the annual report of Rio Tinto.......................................5

Part 4: Incentives given to the managers to disclose the certain type of information in the annual

report................................................................................................................................................5

Part 5: Reaction of investors or securities market on disclosure of certain information provided

in the annual report..........................................................................................................................8

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The present report is developed to undertake an analysis of the information provided in

the annual report of a company listed on the Australian Stock Exchange (ASX). The evaluation

particularly focuses on examining whether the information presented in the annual report

complies with the relevant Australian Accounting Standards (AASBs). The company selected

for the analysis purpose is Rio Tinto, an Australian based metal and mining corporation

recognized as one of the leader within the mining sector across the world.

Part 1: Analysis of the statement ‘Social Accountability is considered in the AASB

Conceptual Framework as a part of the Objectives of the General Purpose Financial

Report (GPFR)’

The objective of the general purpose financial reporting as stated by the AASB

conceptual framework is to communicate the present and potential investors, lenders and

creditors relevant information that assists them in making accurate investment decision.

However, this objective has relatively ignored the importance of communicating the information

in relation to the transaction between the firm and its nearby communities and environment. The

increasing impact of the firm activities on the environment and the communities is causing the

pressure on them to integrate social consideration by disclosing the information relating to such

matters. Social accountability can be defined as responsibility taken by businesses to provide

information in relation to their social and environmental impact. The adoption of social

responsibility accounting as an objective of general purpose financial reporting has been

established by the AASB conceptual framework to report its financial outcomes from a social

perspective as business impact the societies as a whole (Sabha and Shoubaki, 2013). This will

help in providing a measure of the methods adopted by businesses for maximizing the welfare of

the society and environment in which they carry out their business activities. Businesses carry

out their operational activities by drawing inputs from the society and environment and therefore

are responsible for ensuring their protection. Therefore, developing social accountability as an

objective of GPFR would help the business owners to fulfill its stewardship function for the

society.

Part 2: Necessity of Establishing and Developing AASBs in Australian Business Practices

The financial reporting requirements within Australia as per the nature of entity and

therefore have a different disclosure regime. The corporation law has established that all

disclosing entities within Australia are required to accurately maintain the records of their

financial transactions for enabling the preparation of financial statements. The type of

information disclosed within the different annual financial statements of an entity such as

balance sheet, profit and loss statement and cash flow statement need to be provided as per the

Australian Accounting Standards Board (AASB). AASB standard are developed in consultation

4

The present report is developed to undertake an analysis of the information provided in

the annual report of a company listed on the Australian Stock Exchange (ASX). The evaluation

particularly focuses on examining whether the information presented in the annual report

complies with the relevant Australian Accounting Standards (AASBs). The company selected

for the analysis purpose is Rio Tinto, an Australian based metal and mining corporation

recognized as one of the leader within the mining sector across the world.

Part 1: Analysis of the statement ‘Social Accountability is considered in the AASB

Conceptual Framework as a part of the Objectives of the General Purpose Financial

Report (GPFR)’

The objective of the general purpose financial reporting as stated by the AASB

conceptual framework is to communicate the present and potential investors, lenders and

creditors relevant information that assists them in making accurate investment decision.

However, this objective has relatively ignored the importance of communicating the information

in relation to the transaction between the firm and its nearby communities and environment. The

increasing impact of the firm activities on the environment and the communities is causing the

pressure on them to integrate social consideration by disclosing the information relating to such

matters. Social accountability can be defined as responsibility taken by businesses to provide

information in relation to their social and environmental impact. The adoption of social

responsibility accounting as an objective of general purpose financial reporting has been

established by the AASB conceptual framework to report its financial outcomes from a social

perspective as business impact the societies as a whole (Sabha and Shoubaki, 2013). This will

help in providing a measure of the methods adopted by businesses for maximizing the welfare of

the society and environment in which they carry out their business activities. Businesses carry

out their operational activities by drawing inputs from the society and environment and therefore

are responsible for ensuring their protection. Therefore, developing social accountability as an

objective of GPFR would help the business owners to fulfill its stewardship function for the

society.

Part 2: Necessity of Establishing and Developing AASBs in Australian Business Practices

The financial reporting requirements within Australia as per the nature of entity and

therefore have a different disclosure regime. The corporation law has established that all

disclosing entities within Australia are required to accurately maintain the records of their

financial transactions for enabling the preparation of financial statements. The type of

information disclosed within the different annual financial statements of an entity such as

balance sheet, profit and loss statement and cash flow statement need to be provided as per the

Australian Accounting Standards Board (AASB). AASB standard are developed in consultation

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

with the public comments and each standard have an application clause to specific the entity to

which that standard should be applied. The corporation law has mandated all the financial

reporting entities of Australia to comply with the AASB standards for providing reliable and

accurate information to the investors for assisting them in their decision-making process. AASB

standard are developed in conformity with the global financial reporting standard of IFRS

(International Financial Reporting Standards). Thus, their application within Australian business

entities is essential to meet their specific disclosure requirements as well as to increase the

comparability of their financial information as per the global accounting standards (Australian

Government: Treasury, 2019).

Part 3: Types of information disclosed in the annual report of Rio Tinto

AASB 101 provided the basis of presentation of the financial report and it also provide

what type of information must be included in the annual report. This accounting standard is

mainly refers to the presentation of financial information and does not link to the other type of

information that is also needed to disclose in the annual report. As a part of social responsibility

it is also important to disclose such information to the society as it is essential for society and

prove stewardship of the business. It means management of the company must be responsible for

their act and must disclose all information which is material in respect to the society.

As per the annual report of the Rio Tinto, both financial as well as non financial

information was disclosed. Rio Tinto has followed AASB 101 for disclosing all the financial

information. Rio Tinto has followed AASB 101 and has disclosed all the financial information

required to provide in annual report as per para 10 of AASB 101. Para 101 requires company

should provide statement of financial position, financial performance (profit and loss account),

other comprehensive income for the period, statement of changes in equity, cash flow statement

and notes to accounts. In addition to this para 10 clearly mentions that any material financial

information must be disclosed by the company if it is required to do so (AASB 101, 2015, para

10).

With respect to non financial information, annual report of Rio Tinto consists of

information such as key performance indicators, principle risks and relative measures,

sustainable development, governance report that includes remunerations information,

accountability and other important information (Annual Report, 2017).

Part 4: Incentives given to the managers to disclose the certain type of information in the

annual report

As discussed in part 3 of the report there is requirement to disclose certain information in

the annual report so that users of financial statement can make proper judgments and decisions.

There are problems such as voluntary disclosures of financial information and agency conflicts

that give rise to proper allocation of resources in the capital market. Accounting standards and

5

which that standard should be applied. The corporation law has mandated all the financial

reporting entities of Australia to comply with the AASB standards for providing reliable and

accurate information to the investors for assisting them in their decision-making process. AASB

standard are developed in conformity with the global financial reporting standard of IFRS

(International Financial Reporting Standards). Thus, their application within Australian business

entities is essential to meet their specific disclosure requirements as well as to increase the

comparability of their financial information as per the global accounting standards (Australian

Government: Treasury, 2019).

Part 3: Types of information disclosed in the annual report of Rio Tinto

AASB 101 provided the basis of presentation of the financial report and it also provide

what type of information must be included in the annual report. This accounting standard is

mainly refers to the presentation of financial information and does not link to the other type of

information that is also needed to disclose in the annual report. As a part of social responsibility

it is also important to disclose such information to the society as it is essential for society and

prove stewardship of the business. It means management of the company must be responsible for

their act and must disclose all information which is material in respect to the society.

As per the annual report of the Rio Tinto, both financial as well as non financial

information was disclosed. Rio Tinto has followed AASB 101 for disclosing all the financial

information. Rio Tinto has followed AASB 101 and has disclosed all the financial information

required to provide in annual report as per para 10 of AASB 101. Para 101 requires company

should provide statement of financial position, financial performance (profit and loss account),

other comprehensive income for the period, statement of changes in equity, cash flow statement

and notes to accounts. In addition to this para 10 clearly mentions that any material financial

information must be disclosed by the company if it is required to do so (AASB 101, 2015, para

10).

With respect to non financial information, annual report of Rio Tinto consists of

information such as key performance indicators, principle risks and relative measures,

sustainable development, governance report that includes remunerations information,

accountability and other important information (Annual Report, 2017).

Part 4: Incentives given to the managers to disclose the certain type of information in the

annual report

As discussed in part 3 of the report there is requirement to disclose certain information in

the annual report so that users of financial statement can make proper judgments and decisions.

There are problems such as voluntary disclosures of financial information and agency conflicts

that give rise to proper allocation of resources in the capital market. Accounting standards and

5

regulators helps to enhance the credibility of management disclosures and also to remove all

such issues (Farvaque, Alexandre and Saïdane, 2011). There is high agency cost involved for

disclosing all the relevant information in the annual report. Without the information asymmetry

it is not possible to make all the information available known to managers disclosed to the

managers. Basically there are two types of information that need to disclose in the financial

statements, one is compulsory and other one is voluntary. Management has no power to not to

disclose compulsory information while it is their choice to disclose voluntary information. It is

the place where the question of agency cost arises and it leads to endless discussion as it is up to

the management on disclosing the information the annual report (Velashani and ArabSalehi,

2008).

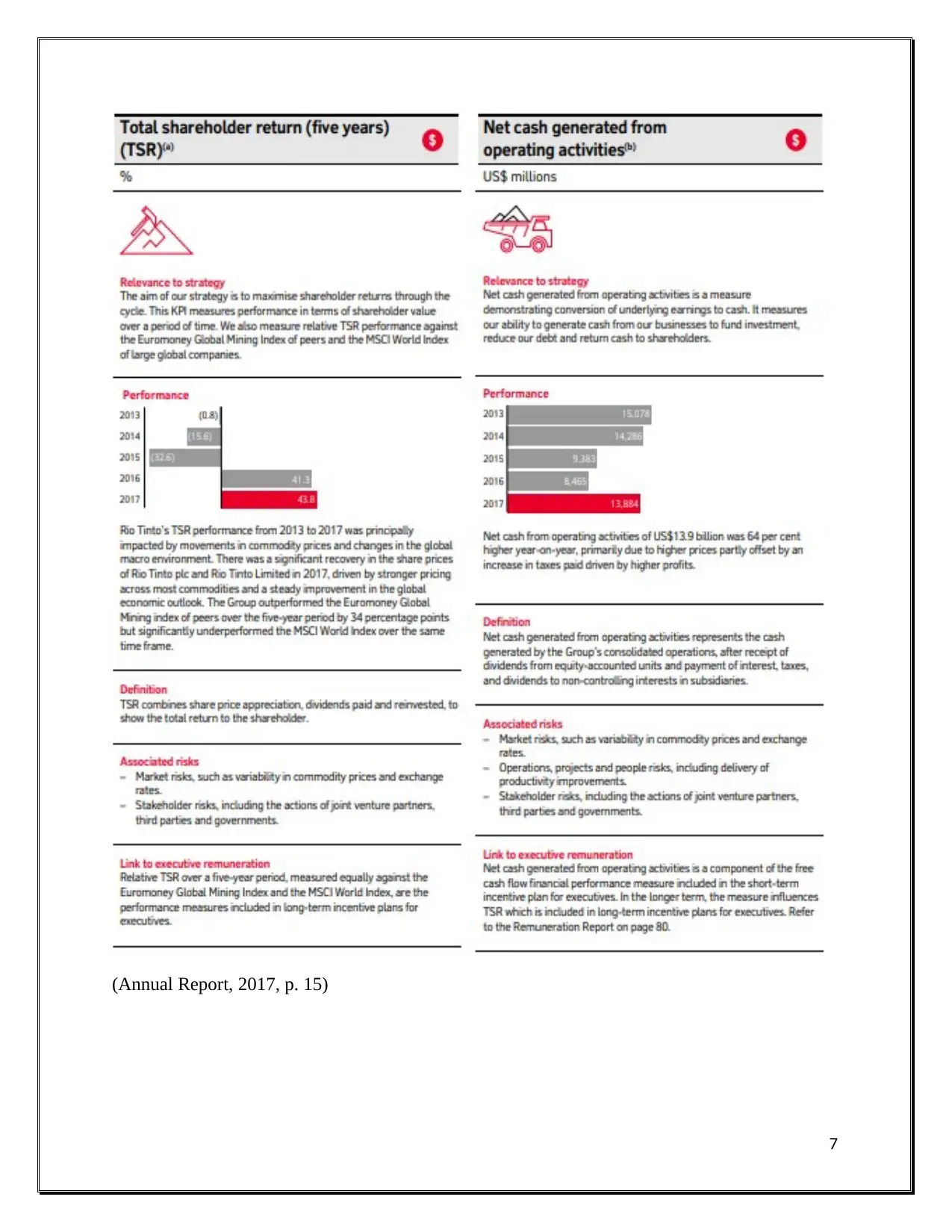

Rio Tinto has short term as well as long term incentive plan for the executives as well as

for the managers that aims to maximise the shareholder’s wealth and also aims to disclose all the

relevant information in the annual report. Information such as total shareholder return (TSR) has

been linked with executive remuneration and Euromoney Global Mining Index and the MSCI

World Index are the measures that is used to decide the long term incentives for the executives.

In this way managers will continue to focus on increasing the total shareholder’s wealth and also

disclose them effectively in order to get more incentives (Annual Report, 2017, p. 15). Similarly,

net cash generated from the operating activity, underlying earnings and other information has

been linked with executive incentives plans that force the management to disclose such

information in the annual report. All such information is voluntary and does not require by

accounting standard to disclose (Annual Report, 2017, p. 16-17). There has been bonus deferral

scheme for the executives that ensure proper alignment between executives and shareholders in

relation to the information disclosed (Annual Report, 2017, p. 74-75).

6

such issues (Farvaque, Alexandre and Saïdane, 2011). There is high agency cost involved for

disclosing all the relevant information in the annual report. Without the information asymmetry

it is not possible to make all the information available known to managers disclosed to the

managers. Basically there are two types of information that need to disclose in the financial

statements, one is compulsory and other one is voluntary. Management has no power to not to

disclose compulsory information while it is their choice to disclose voluntary information. It is

the place where the question of agency cost arises and it leads to endless discussion as it is up to

the management on disclosing the information the annual report (Velashani and ArabSalehi,

2008).

Rio Tinto has short term as well as long term incentive plan for the executives as well as

for the managers that aims to maximise the shareholder’s wealth and also aims to disclose all the

relevant information in the annual report. Information such as total shareholder return (TSR) has

been linked with executive remuneration and Euromoney Global Mining Index and the MSCI

World Index are the measures that is used to decide the long term incentives for the executives.

In this way managers will continue to focus on increasing the total shareholder’s wealth and also

disclose them effectively in order to get more incentives (Annual Report, 2017, p. 15). Similarly,

net cash generated from the operating activity, underlying earnings and other information has

been linked with executive incentives plans that force the management to disclose such

information in the annual report. All such information is voluntary and does not require by

accounting standard to disclose (Annual Report, 2017, p. 16-17). There has been bonus deferral

scheme for the executives that ensure proper alignment between executives and shareholders in

relation to the information disclosed (Annual Report, 2017, p. 74-75).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Annual Report, 2017, p. 15)

7

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part 5: Reaction of investors or securities market on disclosure of certain information

provided in the annual report

The disclosure of financial and non financial information in the annual report certainly

impact investors and securities markets. After publication of annual report 2017, investors have

a positive response in Rio Tinto as market securities in relation to Rio Tinto shares shows

positive growth. As per the news article published in “Intelligent Investor”, it was mentioned

that results of Rio Tinto for year 2017 was very impressive and enough to attract large number

of investors and also hold current shareholders. It was most expected from the results of year

2017, that share price of company will rise more in future year and it is better to hold until Rio

Tinto delivers its best (Sodhi, 2018).

Conclusion

Overall analysis of annual report of Rio Tinto provide information that annual report is

prepared in accordance with the conceptual framework and also complies all the objectives of

the financial reporting especially in context of social accountability. All financial as well as non

financial information required to disclose in annual report and is important for the society as

well as for stakeholders have been properly disclosed in the annual report of Rio Tinto.

8

provided in the annual report

The disclosure of financial and non financial information in the annual report certainly

impact investors and securities markets. After publication of annual report 2017, investors have

a positive response in Rio Tinto as market securities in relation to Rio Tinto shares shows

positive growth. As per the news article published in “Intelligent Investor”, it was mentioned

that results of Rio Tinto for year 2017 was very impressive and enough to attract large number

of investors and also hold current shareholders. It was most expected from the results of year

2017, that share price of company will rise more in future year and it is better to hold until Rio

Tinto delivers its best (Sodhi, 2018).

Conclusion

Overall analysis of annual report of Rio Tinto provide information that annual report is

prepared in accordance with the conceptual framework and also complies all the objectives of

the financial reporting especially in context of social accountability. All financial as well as non

financial information required to disclose in annual report and is important for the society as

well as for stakeholders have been properly disclosed in the annual report of Rio Tinto.

8

References

AASB 101. 2015. Presentation of Financial Statements. [Online]. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed on: 11

February, 2019].

Annual Report. 2017. Rio Tinto. [Online]. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed on: 11

February, 2019].

Australian Government: Treasury. 2019. Financial Reporting Requirements and Accounting

Standards. [Online]. Available at: https://treasury.gov.au/publication/making-transparency-

transparent-an-australian-assessment/chapter-5-financial-reporting-requirements-and-

accounting-standards/ [Accessed on: 11 February, 2019].

Farvaque, E., Alexandre, C.R. and Saïdane, D. 2011. Corporate disclosure: a review of its

(direct and indirect) benefits and costs. Economic international, 4(1), pp. 5-31.

Sabha, S.A. and Shoubaki, Y. 2013. The Importance of Implementing Social Responsibility

Accounting (SRA) in Public Shareholding Companies in Jordan and Its Impact on Their

Sustainability. International Journal of Business and Social Science, 4(6), pp. 270-281.

Sodhi, G. 2018. Rio Tinto: Result 2017 The headline number is impressive, but the deeper you

delve the better it gets. [Online]. Available at: https://www.intelligentinvestor.com.au/rio-tinto-

result-2017-1884846 [Accessed on: 11 February, 2019].

Velashani, M.A. and ArabSalehi, M. 2008. Benefits of telling all: Voluntary disclosure. Monash

Business Review, 4(2), pp. 1-8.

9

AASB 101. 2015. Presentation of Financial Statements. [Online]. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed on: 11

February, 2019].

Annual Report. 2017. Rio Tinto. [Online]. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed on: 11

February, 2019].

Australian Government: Treasury. 2019. Financial Reporting Requirements and Accounting

Standards. [Online]. Available at: https://treasury.gov.au/publication/making-transparency-

transparent-an-australian-assessment/chapter-5-financial-reporting-requirements-and-

accounting-standards/ [Accessed on: 11 February, 2019].

Farvaque, E., Alexandre, C.R. and Saïdane, D. 2011. Corporate disclosure: a review of its

(direct and indirect) benefits and costs. Economic international, 4(1), pp. 5-31.

Sabha, S.A. and Shoubaki, Y. 2013. The Importance of Implementing Social Responsibility

Accounting (SRA) in Public Shareholding Companies in Jordan and Its Impact on Their

Sustainability. International Journal of Business and Social Science, 4(6), pp. 270-281.

Sodhi, G. 2018. Rio Tinto: Result 2017 The headline number is impressive, but the deeper you

delve the better it gets. [Online]. Available at: https://www.intelligentinvestor.com.au/rio-tinto-

result-2017-1884846 [Accessed on: 11 February, 2019].

Velashani, M.A. and ArabSalehi, M. 2008. Benefits of telling all: Voluntary disclosure. Monash

Business Review, 4(2), pp. 1-8.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.