Evaluation of Rio Tinto's Adherence to the Conceptual Framework

VerifiedAdded on 2023/06/15

|11

|2185

|211

Report

AI Summary

This report critically analyzes Rio Tinto's adherence to the conceptual framework for financial reporting, based on its annual report. It examines the company's compliance with the five basic elements of the framework: assets, liabilities, equity, income, and expenses. The report assesses whether Rio Tinto meets the recognition criteria and fundamental qualitative characteristics (relevance and faithful representation), as well as enhancing qualitative characteristics (comparability, verifiability, timeliness, and understandability). The analysis concludes that Rio Tinto effectively incorporates all elements of the conceptual framework in its financial reporting, ensuring transparency and facilitating informed decision-making for stakeholders. Desklib provides access to similar reports and solved assignments for students.

CONTEMPORARY ISSSUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues

Abstract

The report sheds light on the Australian listed corporation that is Rio Tinto and a detailed

critical analysis is conducted of the company’s effectiveness to adhere to the conceptual

framework. The main area of report is based on the annual report of the company wherein the

five basic elements of the conceptual framework is dealt in. various arguments are put forth

to provide a better understanding and Rio Tinto is studied in an in-depth manner. The report

initiates with an introduction followed by the five main elements and ending with a

conclusion that provides that all the elements are met by the company.

2

Abstract

The report sheds light on the Australian listed corporation that is Rio Tinto and a detailed

critical analysis is conducted of the company’s effectiveness to adhere to the conceptual

framework. The main area of report is based on the annual report of the company wherein the

five basic elements of the conceptual framework is dealt in. various arguments are put forth

to provide a better understanding and Rio Tinto is studied in an in-depth manner. The report

initiates with an introduction followed by the five main elements and ending with a

conclusion that provides that all the elements are met by the company.

2

Contemporary Issues

Contents

Introduction...........................................................................................................................................3

Satisfaction of objectives of conceptual framework..............................................................................4

Recognition criteria...............................................................................................................................4

Fundamental qualitative characteristics.................................................................................................5

Enhancing qualitative characteristics.....................................................................................................6

Conclusion.............................................................................................................................................8

Bibliography..........................................................................................................................................9

3

Contents

Introduction...........................................................................................................................................3

Satisfaction of objectives of conceptual framework..............................................................................4

Recognition criteria...............................................................................................................................4

Fundamental qualitative characteristics.................................................................................................5

Enhancing qualitative characteristics.....................................................................................................6

Conclusion.............................................................................................................................................8

Bibliography..........................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Issues

Introduction

The conceptual framework for financial reporting plays a key role in underlying the

presentation and preparation of financial statements for users to assist them in making

effective decisions. Decision making is vastly influenced with the help of conceptual

framework as it provides a strong foundation. Hence, it is very important to them because it

allows them to understand the limitations of financial reporting. Furthermore, in order to

adhere to the requirements of the conceptual framework, the IASB has laid down various

qualitative characteristics like materiality, relevance, reliability, etc that must be fulfilled by

every company. Furthermore, the framework also specifies a recognition criterion that must

be effectively met in order to report asset, liabilities, expenses, income, and equity in the

financial statements (Conceptual Framework, 2016). For the purpose of this report, the

annual report of Rio Tinto has been selected and it will be evaluated whether the company

has complied with the requirements of the conceptual framework.

4

Introduction

The conceptual framework for financial reporting plays a key role in underlying the

presentation and preparation of financial statements for users to assist them in making

effective decisions. Decision making is vastly influenced with the help of conceptual

framework as it provides a strong foundation. Hence, it is very important to them because it

allows them to understand the limitations of financial reporting. Furthermore, in order to

adhere to the requirements of the conceptual framework, the IASB has laid down various

qualitative characteristics like materiality, relevance, reliability, etc that must be fulfilled by

every company. Furthermore, the framework also specifies a recognition criterion that must

be effectively met in order to report asset, liabilities, expenses, income, and equity in the

financial statements (Conceptual Framework, 2016). For the purpose of this report, the

annual report of Rio Tinto has been selected and it will be evaluated whether the company

has complied with the requirements of the conceptual framework.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues

Satisfaction of objectives of conceptual framework

Based on the auditors’ report of Rio Tinto, it can be seen that its annual report has been

prepared in compliance with the norms and procedures of IFRS (International Financial

Reporting Standards). Furthermore, it can also be observed that such financial statements are

in accordance with Article 4 of the IAS Regulation and the Companies Act 2006 that assists

the IASB in the development of consistent and coherent accounting standards. Moreover, it

can also be observed that based on the AASB (Australian Accounting Standards Board), the

financial statements of the Group reflect a true and fair view of its performance, which

clearly proves the fact that the company has met the objectives of the conceptual framework.

Moreover, the report of directors prevalent in the annual report of Rio Tinto is also consistent

with the disclosed financial statements that play a key role in assisting users in understanding

the purposes and limitations of financial reporting (Rio Tinto, 2016). Overall, the financial

statements and annual report of Rio Tinto are clearly in accordance with the company’s

obligations to satisfy the presentation and preparation of consolidated accounts under the

Corporations Act 2001 of Australia. This projects that the company has complied with the

obligations stressing on the strong management of the company.

Recognition criteria

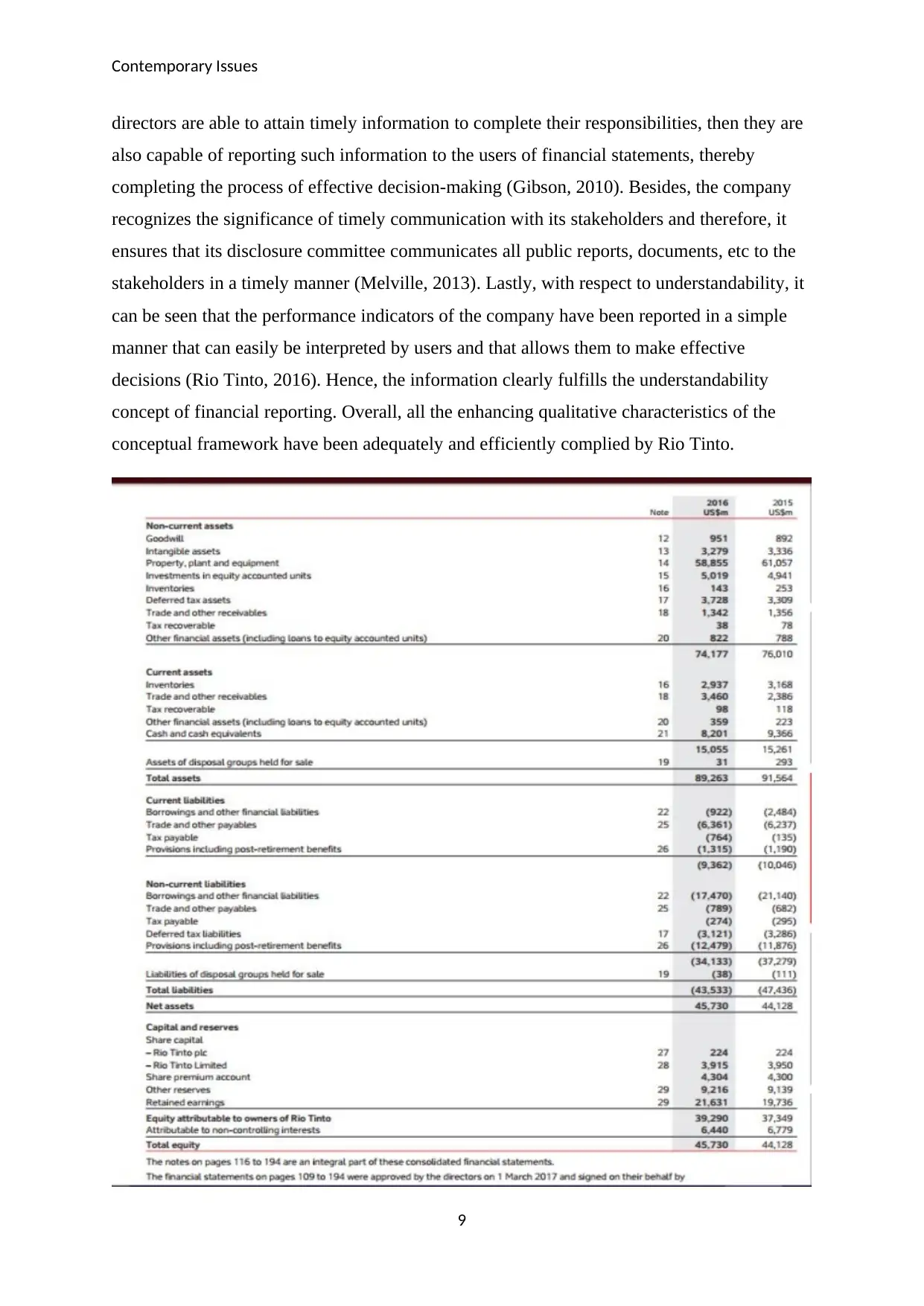

It can be observed from the financial statements of Rio Tinto that compliance with the

recognition criteria to report all the necessary five elements of the conceptual framework has

been appropriately done. In relation to assets, the same are presented in the statement of

financial position of the company as non-current and current assets1. For example, based on

IAS 12 (recognition of deferred tax assets for unrealized losses) has been amended in order to

clarify users how to account for such assets associated with debt instruments that are

measured at fair value (Rio Tinto, 2016). Furthermore, the Group has reported about its

intangible assets that are recognized at their original cost.

1 Seilber J 2015, FASB removes concept of extraordinary, retains guidance on unusual item,

viewed 5 December 2017, http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-

01-fasb-extraordinary-unusual-items.pdf

5

Satisfaction of objectives of conceptual framework

Based on the auditors’ report of Rio Tinto, it can be seen that its annual report has been

prepared in compliance with the norms and procedures of IFRS (International Financial

Reporting Standards). Furthermore, it can also be observed that such financial statements are

in accordance with Article 4 of the IAS Regulation and the Companies Act 2006 that assists

the IASB in the development of consistent and coherent accounting standards. Moreover, it

can also be observed that based on the AASB (Australian Accounting Standards Board), the

financial statements of the Group reflect a true and fair view of its performance, which

clearly proves the fact that the company has met the objectives of the conceptual framework.

Moreover, the report of directors prevalent in the annual report of Rio Tinto is also consistent

with the disclosed financial statements that play a key role in assisting users in understanding

the purposes and limitations of financial reporting (Rio Tinto, 2016). Overall, the financial

statements and annual report of Rio Tinto are clearly in accordance with the company’s

obligations to satisfy the presentation and preparation of consolidated accounts under the

Corporations Act 2001 of Australia. This projects that the company has complied with the

obligations stressing on the strong management of the company.

Recognition criteria

It can be observed from the financial statements of Rio Tinto that compliance with the

recognition criteria to report all the necessary five elements of the conceptual framework has

been appropriately done. In relation to assets, the same are presented in the statement of

financial position of the company as non-current and current assets1. For example, based on

IAS 12 (recognition of deferred tax assets for unrealized losses) has been amended in order to

clarify users how to account for such assets associated with debt instruments that are

measured at fair value (Rio Tinto, 2016). Furthermore, the Group has reported about its

intangible assets that are recognized at their original cost.

1 Seilber J 2015, FASB removes concept of extraordinary, retains guidance on unusual item,

viewed 5 December 2017, http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-

01-fasb-extraordinary-unusual-items.pdf

5

Contemporary Issues

Similarly, PPE of the company is also recognized at cost minus accumulated impairment

losses and depreciation (IAS 16). In relation to liabilities, the financial liabilities and other

borrowings of the company including trade payables are also in compliance with the

recognition criteria, as the company has reported on their initial recognition at fair value

(Everingham et al. 2007). Such liabilities are recognized at a net of incurred transaction

expenses and thereafter, stated at amortized cost. Rio has also reported about its recognition

of deferred tax liabilities on the mining rights that might have been identified in its

acquisitions (Seilber, 2015). Hence, a clear observation has been made and the same is

reported in a proper manner leading to a better disclosure.

In relation to equity, since it is defined as residual, Rio Tinto has effectively sub-classified

the same in its balance sheet. For instance, reserves, share premium, and retained earnings

have been separately recognized by the company in its annual report2. Such classifications

can assist the users in their decision-making process because it indicates legal or other

restrictions on the company’s capability to distribute or apply its equity (Rio Tinto, 2016).

Furthermore, with respect to income and expense, the same has also been reported by the

company in various ways to provide relevant information to users. In relation to income, the

Group has made sure that no material measurement differences are recognized betwixt IFRS

15 and IAS 18 (present revenue recognition standard). It also ensures under IAS 18 that all its

shipping and freight revenue are identified and associated expenses are accrued in full on

loading. Moreover, the impact of treating freight as a different performance obligation cannot

affect earnings, cost, or earnings (Conceptual Framework, 2016). Furthermore, Rio does not

recognize additional losses unless legal obligations to make payments on behalf of equity

accounted units are incurred.

Fundamental qualitative characteristics

With respect to relevance, it can be seen that the company has offered meaningful financial

indicators to the users that can be utilized to evaluate its performance. For instance, it has

offered information of its underlying earnings in the current year and compared it with the

previous year in order to report changes in such segment (Rio Tinto, 2016). Therefore, with

2 Tysiac K 2015, No more extraordinary items: FASB simplifies GAAP, viewed 5 December

2017, http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-

201511630.html

6

Similarly, PPE of the company is also recognized at cost minus accumulated impairment

losses and depreciation (IAS 16). In relation to liabilities, the financial liabilities and other

borrowings of the company including trade payables are also in compliance with the

recognition criteria, as the company has reported on their initial recognition at fair value

(Everingham et al. 2007). Such liabilities are recognized at a net of incurred transaction

expenses and thereafter, stated at amortized cost. Rio has also reported about its recognition

of deferred tax liabilities on the mining rights that might have been identified in its

acquisitions (Seilber, 2015). Hence, a clear observation has been made and the same is

reported in a proper manner leading to a better disclosure.

In relation to equity, since it is defined as residual, Rio Tinto has effectively sub-classified

the same in its balance sheet. For instance, reserves, share premium, and retained earnings

have been separately recognized by the company in its annual report2. Such classifications

can assist the users in their decision-making process because it indicates legal or other

restrictions on the company’s capability to distribute or apply its equity (Rio Tinto, 2016).

Furthermore, with respect to income and expense, the same has also been reported by the

company in various ways to provide relevant information to users. In relation to income, the

Group has made sure that no material measurement differences are recognized betwixt IFRS

15 and IAS 18 (present revenue recognition standard). It also ensures under IAS 18 that all its

shipping and freight revenue are identified and associated expenses are accrued in full on

loading. Moreover, the impact of treating freight as a different performance obligation cannot

affect earnings, cost, or earnings (Conceptual Framework, 2016). Furthermore, Rio does not

recognize additional losses unless legal obligations to make payments on behalf of equity

accounted units are incurred.

Fundamental qualitative characteristics

With respect to relevance, it can be seen that the company has offered meaningful financial

indicators to the users that can be utilized to evaluate its performance. For instance, it has

offered information of its underlying earnings in the current year and compared it with the

previous year in order to report changes in such segment (Rio Tinto, 2016). Therefore, with

2 Tysiac K 2015, No more extraordinary items: FASB simplifies GAAP, viewed 5 December

2017, http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-

201511630.html

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Issues

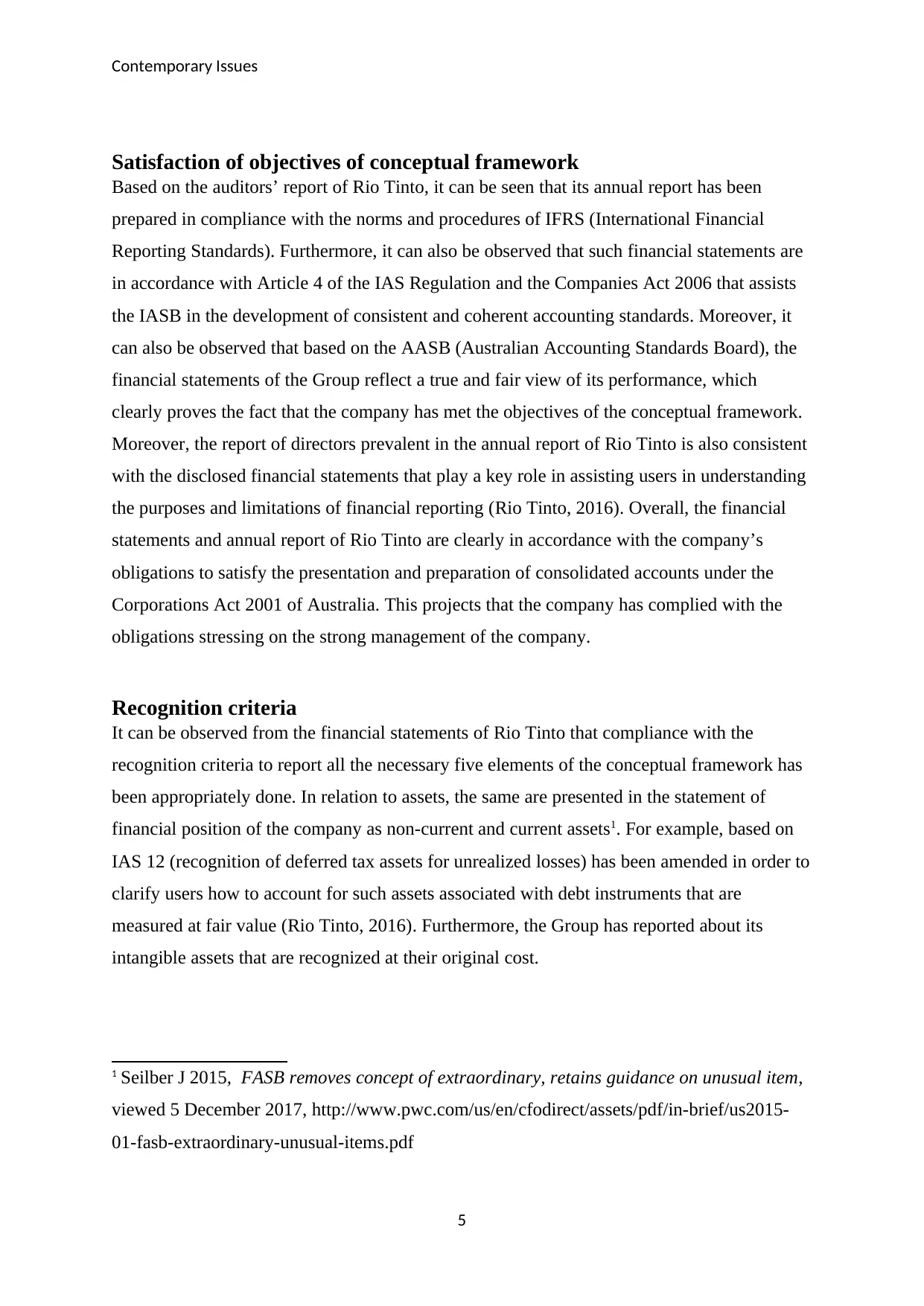

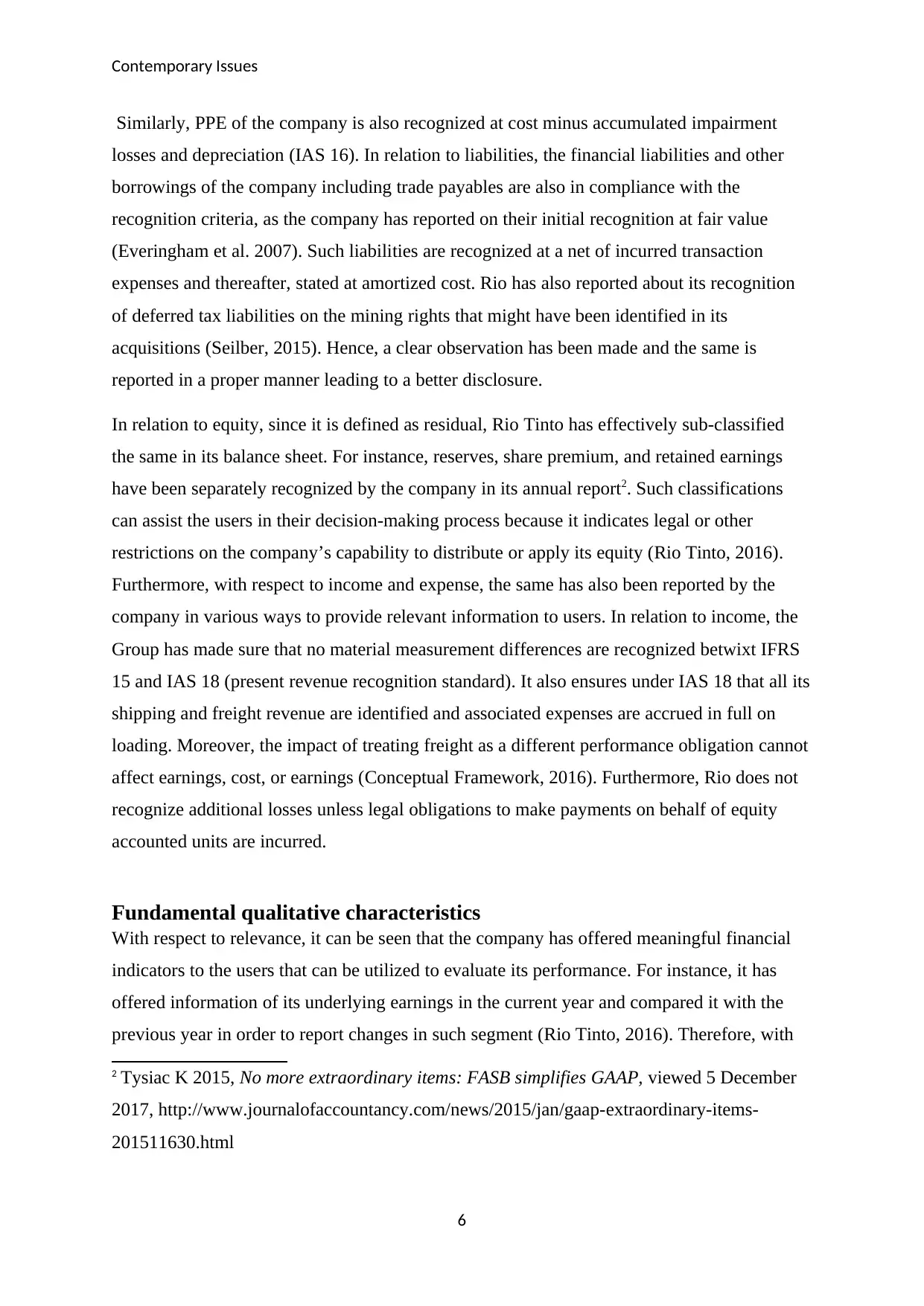

such comparison, users can easily judge whether the company is performing properly or not.

Furthermore, the company has also taken into account both financial and non-financial

aspects of the conceptual framework in order to satisfy the quality of relevance in its

reporting3. This can be proved by the fact that the auditors (PWC LLP) of the Group have

assured that the financial statements accommodate both financial and non-financial details so

that material ineffectiveness with the audited report or financial statements can be identified

easily (Conceptual Framework, 2016).

With respect to faithful representation, it can be seen that the company has adhered to the

same by offering a written declaration from its directors stating the fact that its annual report

clearly presents a true and fair view of its financial performance (Conceptual Framework,

2016). Moreover, in order to offer more surety to the same, the Group has also complied with

section 295A of the Corporations Act 2001 (Rio Tinto, 2016). The directors also consider that

the annual report of the company has been truly prepared in accordance with the applicable

accounting standards that is assisted by reasonable judgments and estimates. Therefore, the

company has efficiently adhered to the faithful representation and relevance concept in its

annual report.

3 Parrino, R., Kidwell, D. & Bates, T 2012, Fundamentals of corporate finance, Hoboken, NJ:

Wiley

7

such comparison, users can easily judge whether the company is performing properly or not.

Furthermore, the company has also taken into account both financial and non-financial

aspects of the conceptual framework in order to satisfy the quality of relevance in its

reporting3. This can be proved by the fact that the auditors (PWC LLP) of the Group have

assured that the financial statements accommodate both financial and non-financial details so

that material ineffectiveness with the audited report or financial statements can be identified

easily (Conceptual Framework, 2016).

With respect to faithful representation, it can be seen that the company has adhered to the

same by offering a written declaration from its directors stating the fact that its annual report

clearly presents a true and fair view of its financial performance (Conceptual Framework,

2016). Moreover, in order to offer more surety to the same, the Group has also complied with

section 295A of the Corporations Act 2001 (Rio Tinto, 2016). The directors also consider that

the annual report of the company has been truly prepared in accordance with the applicable

accounting standards that is assisted by reasonable judgments and estimates. Therefore, the

company has efficiently adhered to the faithful representation and relevance concept in its

annual report.

3 Parrino, R., Kidwell, D. & Bates, T 2012, Fundamentals of corporate finance, Hoboken, NJ:

Wiley

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues

Enhancing qualitative characteristics

It can be seen from the annual report of Rio Tinto that the company has offered material

information of its performance data for a period of past five years. For instance, in the annual

report, the performance data of social, environment, and direct economic contribution of the

company from 2012-2016 has been reported. These aspects have further sub-headings that

clearly depict the performance of the company in different segments. Hence, the information

can be compared easily with that of past five years to determine whether the company has

been performing effectively in the mentioned areas (Rio Tinto, 2016). Therefore, this proves

that the company has adequately adhered to the comparability aspect of the conceptual

framework in its annual report4. Furthermore, the company has appropriate verification

procedures in place so that it can detect material errors if the data reported in the previous

years are not able to ensure comparability over time (Conceptual Framework, 2016). Besides,

if information can be easily compared with that of the past years, it can be easily verified

whether the performance of the company in such segment is effective or not (Horngren,

2013).

With respect to timely information, it can be seen that the directors of Rio Tinto attain timely

information so that they can fulfill their duties in an effective manner. This shows that if the

4 Williams, J 2012, Financial accounting, New York: McGraw-Hill/Irwin.

8

Enhancing qualitative characteristics

It can be seen from the annual report of Rio Tinto that the company has offered material

information of its performance data for a period of past five years. For instance, in the annual

report, the performance data of social, environment, and direct economic contribution of the

company from 2012-2016 has been reported. These aspects have further sub-headings that

clearly depict the performance of the company in different segments. Hence, the information

can be compared easily with that of past five years to determine whether the company has

been performing effectively in the mentioned areas (Rio Tinto, 2016). Therefore, this proves

that the company has adequately adhered to the comparability aspect of the conceptual

framework in its annual report4. Furthermore, the company has appropriate verification

procedures in place so that it can detect material errors if the data reported in the previous

years are not able to ensure comparability over time (Conceptual Framework, 2016). Besides,

if information can be easily compared with that of the past years, it can be easily verified

whether the performance of the company in such segment is effective or not (Horngren,

2013).

With respect to timely information, it can be seen that the directors of Rio Tinto attain timely

information so that they can fulfill their duties in an effective manner. This shows that if the

4 Williams, J 2012, Financial accounting, New York: McGraw-Hill/Irwin.

8

Contemporary Issues

directors are able to attain timely information to complete their responsibilities, then they are

also capable of reporting such information to the users of financial statements, thereby

completing the process of effective decision-making (Gibson, 2010). Besides, the company

recognizes the significance of timely communication with its stakeholders and therefore, it

ensures that its disclosure committee communicates all public reports, documents, etc to the

stakeholders in a timely manner (Melville, 2013). Lastly, with respect to understandability, it

can be seen that the performance indicators of the company have been reported in a simple

manner that can easily be interpreted by users and that allows them to make effective

decisions (Rio Tinto, 2016). Hence, the information clearly fulfills the understandability

concept of financial reporting. Overall, all the enhancing qualitative characteristics of the

conceptual framework have been adequately and efficiently complied by Rio Tinto.

9

directors are able to attain timely information to complete their responsibilities, then they are

also capable of reporting such information to the users of financial statements, thereby

completing the process of effective decision-making (Gibson, 2010). Besides, the company

recognizes the significance of timely communication with its stakeholders and therefore, it

ensures that its disclosure committee communicates all public reports, documents, etc to the

stakeholders in a timely manner (Melville, 2013). Lastly, with respect to understandability, it

can be seen that the performance indicators of the company have been reported in a simple

manner that can easily be interpreted by users and that allows them to make effective

decisions (Rio Tinto, 2016). Hence, the information clearly fulfills the understandability

concept of financial reporting. Overall, all the enhancing qualitative characteristics of the

conceptual framework have been adequately and efficiently complied by Rio Tinto.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contemporary Issues

Conclusion

After analyzing the annual report of Rio Tinto, it can be seen that the company has taken into

account all the five elements of a conceptual framework for reporting financial details in its

annual report. For such purpose, the company has effectively complied with the recognition

criteria to report such elements in its annual report. Furthermore, it has also ensured that all

the objectives of the conceptual framework are adequately met. For such purpose, it has also

complied with the fundamental and enhancing qualitative characteristics of corporate

reporting, which makes it clear that the users can easily make proper decisions based on such

financial information.

10

Conclusion

After analyzing the annual report of Rio Tinto, it can be seen that the company has taken into

account all the five elements of a conceptual framework for reporting financial details in its

annual report. For such purpose, the company has effectively complied with the recognition

criteria to report such elements in its annual report. Furthermore, it has also ensured that all

the objectives of the conceptual framework are adequately met. For such purpose, it has also

complied with the fundamental and enhancing qualitative characteristics of corporate

reporting, which makes it clear that the users can easily make proper decisions based on such

financial information.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contemporary Issues

Bibliography

Conceptual Framework 2016, Conceptual Framework Pronouncements, viewed 5 December

2017, http://www.aasb.gov.au/Pronouncements/Conceptual-framework.aspx

Everingham, G.K, Kleynhans, J.E & Posthumus, L.C 2007, Principles of Generally Accepted

Accounting Practice, Juta and Company Ltd.

Gibson, C 2010, Financial Reporting and Analysis: Using Financial Accounting Information,

Cengage Learning.

Horngren, C 2013, Financial accounting, Frenchs Forest, N.S.W: Pearson Australia Group.

Melville, A 2013, International Financial Reporting – A Practical Guide, Pearson, Education

Limited, UK

Parrino, R., Kidwell, D. & Bates, T 2012, Fundamentals of corporate finance, Hoboken, NJ:

Wiley

Rio Tinto 2016, Rio Tinto Annual Report and accounts 2016, viewed 11 September 2017

http://www.riotinto.com/documents/RT_2016_Annual_report.pdf

Seilber J 2015, FASB removes concept of extraordinary, retains guidance on unusual item,

viewed 5 December 2017, http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-

01-fasb-extraordinary-unusual-items.pdf

Tysiac K 2015, No more extraordinary items: FASB simplifies GAAP, viewed 5 December

2017, http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-

201511630.html

Williams, J 2012, Financial accounting, New York: McGraw-Hill/Irwin.

11

Bibliography

Conceptual Framework 2016, Conceptual Framework Pronouncements, viewed 5 December

2017, http://www.aasb.gov.au/Pronouncements/Conceptual-framework.aspx

Everingham, G.K, Kleynhans, J.E & Posthumus, L.C 2007, Principles of Generally Accepted

Accounting Practice, Juta and Company Ltd.

Gibson, C 2010, Financial Reporting and Analysis: Using Financial Accounting Information,

Cengage Learning.

Horngren, C 2013, Financial accounting, Frenchs Forest, N.S.W: Pearson Australia Group.

Melville, A 2013, International Financial Reporting – A Practical Guide, Pearson, Education

Limited, UK

Parrino, R., Kidwell, D. & Bates, T 2012, Fundamentals of corporate finance, Hoboken, NJ:

Wiley

Rio Tinto 2016, Rio Tinto Annual Report and accounts 2016, viewed 11 September 2017

http://www.riotinto.com/documents/RT_2016_Annual_report.pdf

Seilber J 2015, FASB removes concept of extraordinary, retains guidance on unusual item,

viewed 5 December 2017, http://www.pwc.com/us/en/cfodirect/assets/pdf/in-brief/us2015-

01-fasb-extraordinary-unusual-items.pdf

Tysiac K 2015, No more extraordinary items: FASB simplifies GAAP, viewed 5 December

2017, http://www.journalofaccountancy.com/news/2015/jan/gaap-extraordinary-items-

201511630.html

Williams, J 2012, Financial accounting, New York: McGraw-Hill/Irwin.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.