Financial Analysis and Management of Rio Tinto (APO004-6 Report)

VerifiedAdded on 2022/11/14

|11

|2741

|430

Report

AI Summary

This report provides a comprehensive financial analysis of Rio Tinto, a prominent company in the mineral and metal mining industry. It begins with an introduction to the company, its core objectives, and the business environment in which it operates. The report then delves into the company's capital structure and dividend policy, analyzing its financial performance over a three-year period, including key metrics such as EBIT, net profit, debt, and dividends paid. The analysis highlights the company's efforts to reduce debt and its consistent dividend payouts. The report further explores various capital investment appraisal techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), Profitability Index (PI), Payback Period, and Accounting Rate of Return (ARR), explaining the implementation of each method and their relevance in investment decisions. The report concludes by summarizing the correlation between the company's objectives and its capital structure, emphasizing the importance of disciplined capital allocation and shareholder value creation.

FINANCIAL ANALYSIS AND MANAGEMENT

RIO TINTO

RIO TINTO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...............................................................................................................................2

Background of the company and the business environment...........................................2

Analysis of the capital structure and dividend policy of the company.............................3

Methods of capital investment appraisal..............................................................................4

Net Present Value (NPV)...................................................................................................4

Internal Rate of Return Method (IRR)..............................................................................5

Profitability Index Method (PI)...........................................................................................6

Pay Back Period..................................................................................................................6

Accounting Rate of Return Method (ARR)......................................................................7

Conclusion................................................................................................................................7

References...............................................................................................................................9

Introduction...............................................................................................................................2

Background of the company and the business environment...........................................2

Analysis of the capital structure and dividend policy of the company.............................3

Methods of capital investment appraisal..............................................................................4

Net Present Value (NPV)...................................................................................................4

Internal Rate of Return Method (IRR)..............................................................................5

Profitability Index Method (PI)...........................................................................................6

Pay Back Period..................................................................................................................6

Accounting Rate of Return Method (ARR)......................................................................7

Conclusion................................................................................................................................7

References...............................................................................................................................9

Introduction

Over the years, the globalised business practices have become all the more complex

and demand greater evaluation by the top management of the enterprise. One of the

most significant business decisions amounts to the choice of the capital structure

which refers to the careful balance between equity and debt that is used by the

businesses for the financing of the assets, day-to-day operations, and future growth

(Öztekin, 2015). The following work is aimed at analysing the various aspects of the

financial management in the context of the capital structure, investment appraisal

decisions and the various methods involved therein. The company chosen for the

analysis is Rio Tinto. The first section of the work would shed light on the core

objectives, the business environment, followed by the capital structure of the

company and the dividend policy of the company. The section would also comprise

of the analysis of the financial performance of the company together with the

comparison of the same. The next section of the company would elaborate on the

various techniques of the investment appraisal and the means of the implementation

of the same. Lastly, the work would highlight the correlation between the objectives

of the company and the capital structure.

The company Rio Tinto is known to be one of the most renowned companies that

are engaged in the mineral and metal mining industry. The core mining products of

the company include copper, diamonds, aluminium, uranium, coal and iron ore. The

company has its head offices in the UK as well as at Australia and is also dually

listed on both the London Stock exchange under the name Rio Tinto Plc and the

Australian Stock Exchange under the name Rio Tinto Limited. The company is

additionally forming a part of the FTSE 100 Index in the UK.

Background of the company and the business environment

The key business objective of the company as mentioned in the latest strategic

report of the company can be stated to be the creation of the superior value for

shareholders, meeting the needs of the customers’, maximisation of the cash from

the assets of the enterprise and the efficient allocation of the capital of the enterprise

(Rio Tinto, 2018a). The operations of the company are scattered in the areas of the

US, Canada, Japan, China, other parts of Europe and Asia, apart from the UK and

Over the years, the globalised business practices have become all the more complex

and demand greater evaluation by the top management of the enterprise. One of the

most significant business decisions amounts to the choice of the capital structure

which refers to the careful balance between equity and debt that is used by the

businesses for the financing of the assets, day-to-day operations, and future growth

(Öztekin, 2015). The following work is aimed at analysing the various aspects of the

financial management in the context of the capital structure, investment appraisal

decisions and the various methods involved therein. The company chosen for the

analysis is Rio Tinto. The first section of the work would shed light on the core

objectives, the business environment, followed by the capital structure of the

company and the dividend policy of the company. The section would also comprise

of the analysis of the financial performance of the company together with the

comparison of the same. The next section of the company would elaborate on the

various techniques of the investment appraisal and the means of the implementation

of the same. Lastly, the work would highlight the correlation between the objectives

of the company and the capital structure.

The company Rio Tinto is known to be one of the most renowned companies that

are engaged in the mineral and metal mining industry. The core mining products of

the company include copper, diamonds, aluminium, uranium, coal and iron ore. The

company has its head offices in the UK as well as at Australia and is also dually

listed on both the London Stock exchange under the name Rio Tinto Plc and the

Australian Stock Exchange under the name Rio Tinto Limited. The company is

additionally forming a part of the FTSE 100 Index in the UK.

Background of the company and the business environment

The key business objective of the company as mentioned in the latest strategic

report of the company can be stated to be the creation of the superior value for

shareholders, meeting the needs of the customers’, maximisation of the cash from

the assets of the enterprise and the efficient allocation of the capital of the enterprise

(Rio Tinto, 2018a). The operations of the company are scattered in the areas of the

US, Canada, Japan, China, other parts of Europe and Asia, apart from the UK and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australia. Thus, one of the significant factors that guide the business activities of the

enterprise is the regional and international statutes and regulations. Yet another key

factors that impact the operations of the enterprise very deeply are the geopolitical

uncertainties around the world and its economic and social implications.

It has been stated by the management of the company that one of the main strategic

business objectives of the company is the disciplined capital allocation together with

the sanctioning of the expenditure for the new investment projects (Rio Tinto, 2018b,

p. 12). Besides, the management of the company ensures that the expenditure for

the growth is always weighed against the return to the shareholders on the capital

employed.

In the context of the accounting framework, the management of the entity uses the

IFRS measures as well as the non-GAAP measures to assess the performance of

the enterprise as a whole.

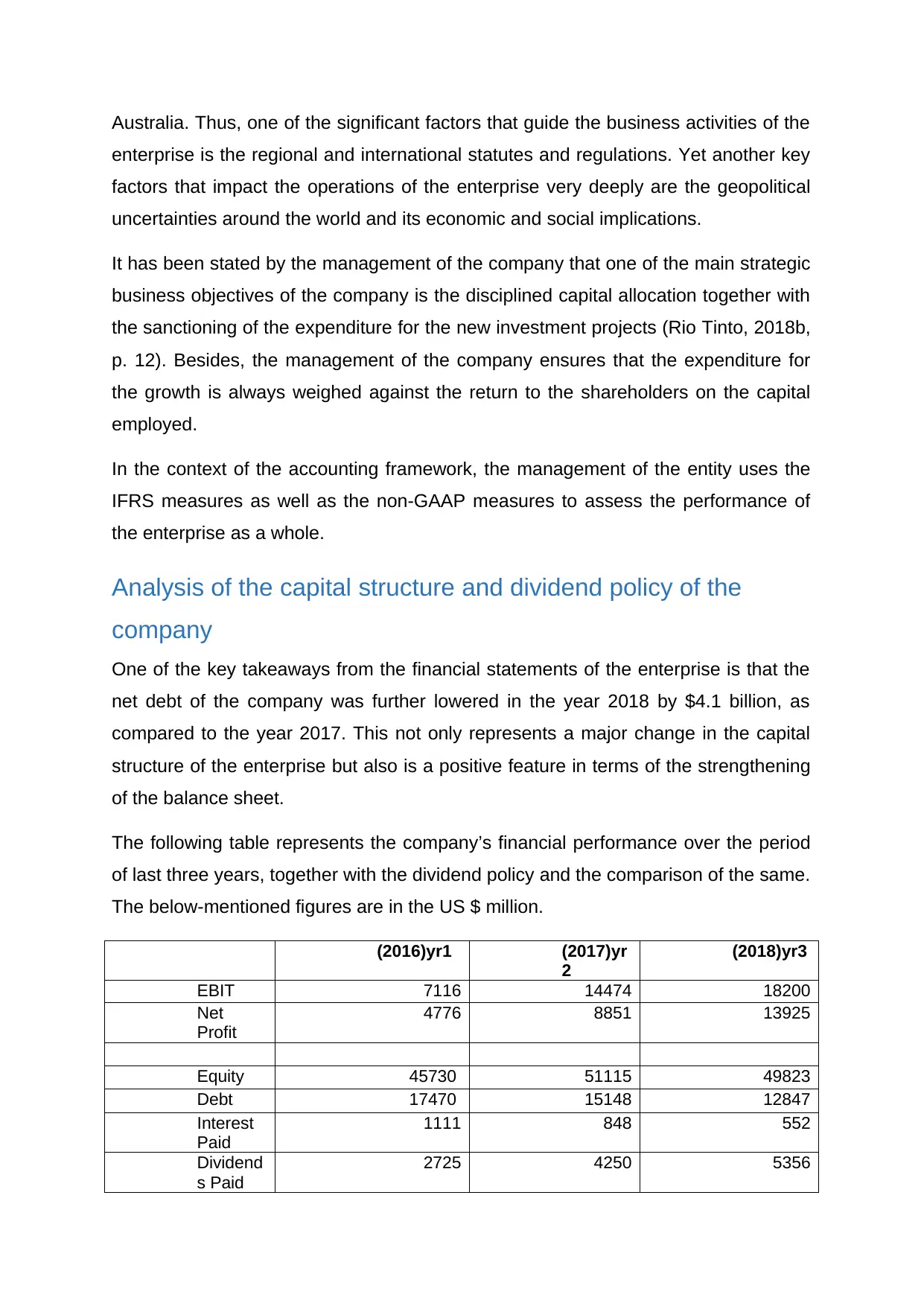

Analysis of the capital structure and dividend policy of the

company

One of the key takeaways from the financial statements of the enterprise is that the

net debt of the company was further lowered in the year 2018 by $4.1 billion, as

compared to the year 2017. This not only represents a major change in the capital

structure of the enterprise but also is a positive feature in terms of the strengthening

of the balance sheet.

The following table represents the company’s financial performance over the period

of last three years, together with the dividend policy and the comparison of the same.

The below-mentioned figures are in the US $ million.

(2016)yr1 (2017)yr

2

(2018)yr3

EBIT 7116 14474 18200

Net

Profit

4776 8851 13925

Equity 45730 51115 49823

Debt 17470 15148 12847

Interest

Paid

1111 848 552

Dividend

s Paid

2725 4250 5356

enterprise is the regional and international statutes and regulations. Yet another key

factors that impact the operations of the enterprise very deeply are the geopolitical

uncertainties around the world and its economic and social implications.

It has been stated by the management of the company that one of the main strategic

business objectives of the company is the disciplined capital allocation together with

the sanctioning of the expenditure for the new investment projects (Rio Tinto, 2018b,

p. 12). Besides, the management of the company ensures that the expenditure for

the growth is always weighed against the return to the shareholders on the capital

employed.

In the context of the accounting framework, the management of the entity uses the

IFRS measures as well as the non-GAAP measures to assess the performance of

the enterprise as a whole.

Analysis of the capital structure and dividend policy of the

company

One of the key takeaways from the financial statements of the enterprise is that the

net debt of the company was further lowered in the year 2018 by $4.1 billion, as

compared to the year 2017. This not only represents a major change in the capital

structure of the enterprise but also is a positive feature in terms of the strengthening

of the balance sheet.

The following table represents the company’s financial performance over the period

of last three years, together with the dividend policy and the comparison of the same.

The below-mentioned figures are in the US $ million.

(2016)yr1 (2017)yr

2

(2018)yr3

EBIT 7116 14474 18200

Net

Profit

4776 8851 13925

Equity 45730 51115 49823

Debt 17470 15148 12847

Interest

Paid

1111 848 552

Dividend

s Paid

2725 4250 5356

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above EBIT has been calculated by the subtraction of the cost of goods sold

and the operating expenses from total revenue of the enterprise Rio Tinto.

As depicted from the table above, the enterprise is consistently lowering the debt

components in the capital structure and thereby reducing the interest payments as

well. The move is in line with the company's objectives of expanding yet being self-

sufficient. The significant reduction in the debt levels can also be attributed to the

overall reduction in the debt level in the mining sector as a whole (Rio Tinto, 2018b).

Further, it is vital to note that the company Rio Tinto has been consistently on the

positive trends in the context of the earning of the profits and the same are

generously shared with the shareholders of the enterprise in the form of the

dividends. Thus, as the profits are on the rising trends, so are the dividends paid by

the entity, which describes that a healthy balance has been created between the

growth objectives of the company and the distribution of what is earned.

It must be also noted that the overall return on capital employed (ROCE) for the

shareholders thus accounts to be to 19 per cent for the year 2018. The reduction in

the debt of the company from the capital structure would further lead to the

stabilisation of the share prices of the company, to gain a strategic advantage over

the competitors of the enterprise.

Methods of capital investment appraisal

The five primary techniques that can be used by the management for the evaluation

of the investment appraisal projects are the Internal rate of return method (IRR), Net

Present Value (NPV) method, Profitability Index (PI) method, Accounting Rate of

Return (ARR) method and lastly the payback period method. The management of

the enterprise can use one or more of the above-mentioned techniques depending

on the project and the options available. The implementation of each of the project is

explained as follows.

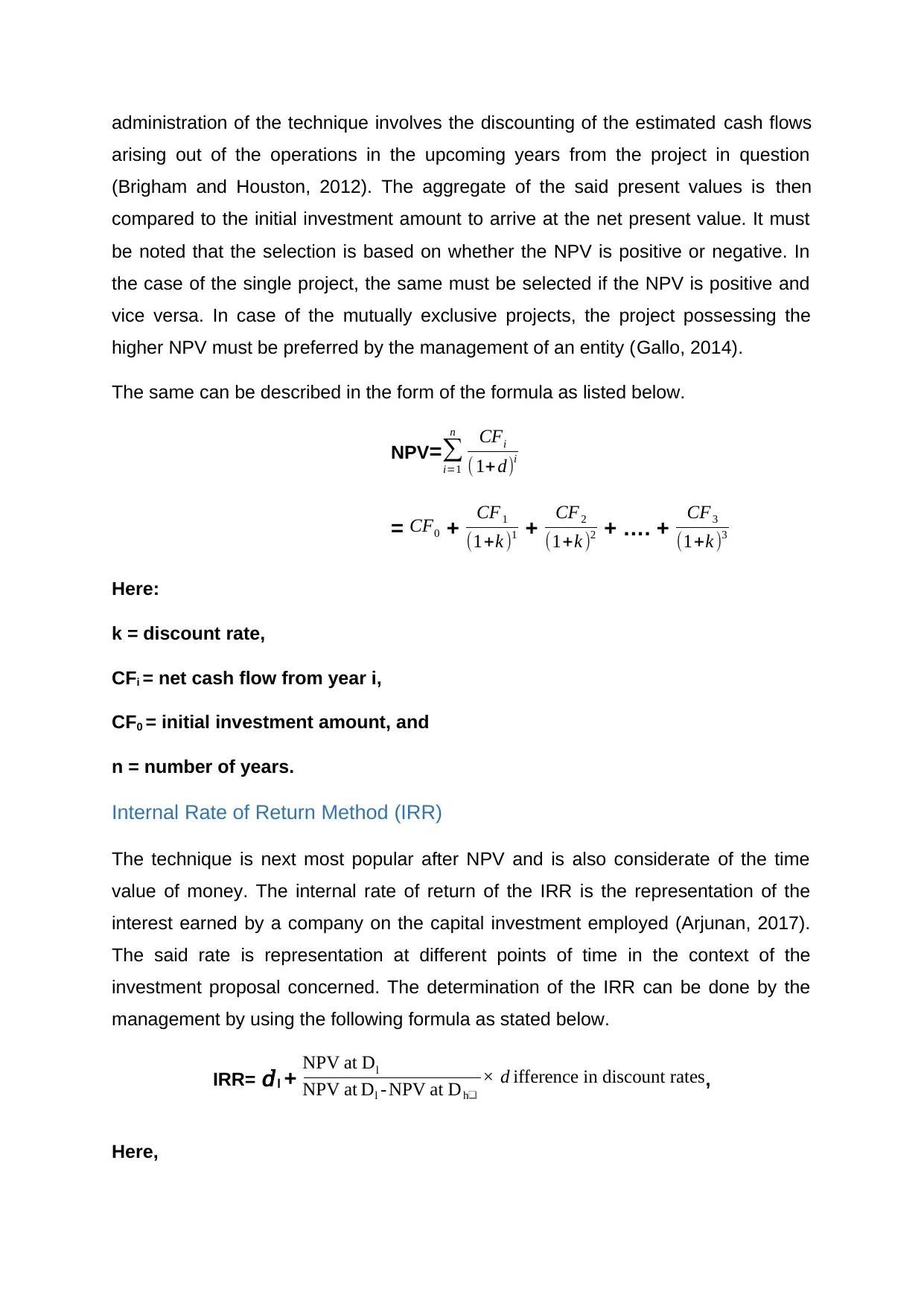

Net Present Value (NPV)

The technique is the most popular one and employs the time value of money to

arrive the decision of the selection of the project or the projects. Initially, the cost of

the capital is computed to be used as the discounting rate for the technique. The

and the operating expenses from total revenue of the enterprise Rio Tinto.

As depicted from the table above, the enterprise is consistently lowering the debt

components in the capital structure and thereby reducing the interest payments as

well. The move is in line with the company's objectives of expanding yet being self-

sufficient. The significant reduction in the debt levels can also be attributed to the

overall reduction in the debt level in the mining sector as a whole (Rio Tinto, 2018b).

Further, it is vital to note that the company Rio Tinto has been consistently on the

positive trends in the context of the earning of the profits and the same are

generously shared with the shareholders of the enterprise in the form of the

dividends. Thus, as the profits are on the rising trends, so are the dividends paid by

the entity, which describes that a healthy balance has been created between the

growth objectives of the company and the distribution of what is earned.

It must be also noted that the overall return on capital employed (ROCE) for the

shareholders thus accounts to be to 19 per cent for the year 2018. The reduction in

the debt of the company from the capital structure would further lead to the

stabilisation of the share prices of the company, to gain a strategic advantage over

the competitors of the enterprise.

Methods of capital investment appraisal

The five primary techniques that can be used by the management for the evaluation

of the investment appraisal projects are the Internal rate of return method (IRR), Net

Present Value (NPV) method, Profitability Index (PI) method, Accounting Rate of

Return (ARR) method and lastly the payback period method. The management of

the enterprise can use one or more of the above-mentioned techniques depending

on the project and the options available. The implementation of each of the project is

explained as follows.

Net Present Value (NPV)

The technique is the most popular one and employs the time value of money to

arrive the decision of the selection of the project or the projects. Initially, the cost of

the capital is computed to be used as the discounting rate for the technique. The

administration of the technique involves the discounting of the estimated cash flows

arising out of the operations in the upcoming years from the project in question

(Brigham and Houston, 2012). The aggregate of the said present values is then

compared to the initial investment amount to arrive at the net present value. It must

be noted that the selection is based on whether the NPV is positive or negative. In

the case of the single project, the same must be selected if the NPV is positive and

vice versa. In case of the mutually exclusive projects, the project possessing the

higher NPV must be preferred by the management of an entity (Gallo, 2014).

The same can be described in the form of the formula as listed below.

NPV=∑

i=1

n CFi

(1+ d)i

= CF0 + CF 1

(1+k )1 + CF 2

(1+k )2 + …. + CF3

(1+k )3

Here:

k = discount rate,

CFi = net cash flow from year i,

CF0 = initial investment amount, and

n = number of years.

Internal Rate of Return Method (IRR)

The technique is next most popular after NPV and is also considerate of the time

value of money. The internal rate of return of the IRR is the representation of the

interest earned by a company on the capital investment employed (Arjunan, 2017).

The said rate is representation at different points of time in the context of the

investment proposal concerned. The determination of the IRR can be done by the

management by using the following formula as stated below.

IRR= 𝑑l + NPV at Dl

NPV at Dl -NPV at Dh❑

× d ifference in discount rates,

Here,

arising out of the operations in the upcoming years from the project in question

(Brigham and Houston, 2012). The aggregate of the said present values is then

compared to the initial investment amount to arrive at the net present value. It must

be noted that the selection is based on whether the NPV is positive or negative. In

the case of the single project, the same must be selected if the NPV is positive and

vice versa. In case of the mutually exclusive projects, the project possessing the

higher NPV must be preferred by the management of an entity (Gallo, 2014).

The same can be described in the form of the formula as listed below.

NPV=∑

i=1

n CFi

(1+ d)i

= CF0 + CF 1

(1+k )1 + CF 2

(1+k )2 + …. + CF3

(1+k )3

Here:

k = discount rate,

CFi = net cash flow from year i,

CF0 = initial investment amount, and

n = number of years.

Internal Rate of Return Method (IRR)

The technique is next most popular after NPV and is also considerate of the time

value of money. The internal rate of return of the IRR is the representation of the

interest earned by a company on the capital investment employed (Arjunan, 2017).

The said rate is representation at different points of time in the context of the

investment proposal concerned. The determination of the IRR can be done by the

management by using the following formula as stated below.

IRR= 𝑑l + NPV at Dl

NPV at Dl -NPV at Dh❑

× d ifference in discount rates,

Here,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

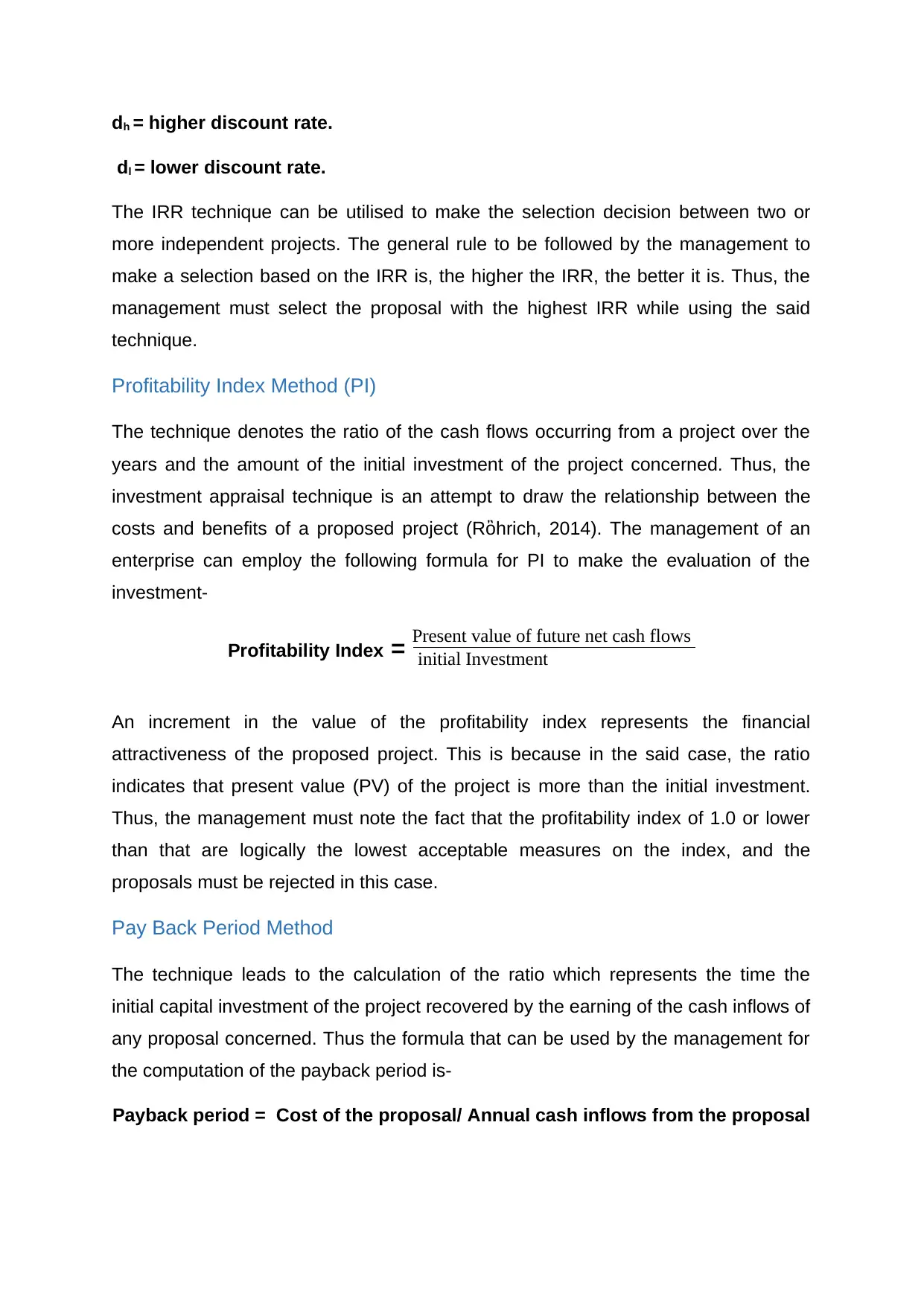

dh = higher discount rate.

dl = lower discount rate.

The IRR technique can be utilised to make the selection decision between two or

more independent projects. The general rule to be followed by the management to

make a selection based on the IRR is, the higher the IRR, the better it is. Thus, the

management must select the proposal with the highest IRR while using the said

technique.

Profitability Index Method (PI)

The technique denotes the ratio of the cash flows occurring from a project over the

years and the amount of the initial investment of the project concerned. Thus, the

investment appraisal technique is an attempt to draw the relationship between the

costs and benefits of a proposed project (Rὂhrich, 2014). The management of an

enterprise can employ the following formula for PI to make the evaluation of the

investment-

Profitability Index = Present value of future net cash flows

initial Investment

An increment in the value of the profitability index represents the financial

attractiveness of the proposed project. This is because in the said case, the ratio

indicates that present value (PV) of the project is more than the initial investment.

Thus, the management must note the fact that the profitability index of 1.0 or lower

than that are logically the lowest acceptable measures on the index, and the

proposals must be rejected in this case.

Pay Back Period Method

The technique leads to the calculation of the ratio which represents the time the

initial capital investment of the project recovered by the earning of the cash inflows of

any proposal concerned. Thus the formula that can be used by the management for

the computation of the payback period is-

Payback period = Cost of the proposal/ Annual cash inflows from the proposal

dl = lower discount rate.

The IRR technique can be utilised to make the selection decision between two or

more independent projects. The general rule to be followed by the management to

make a selection based on the IRR is, the higher the IRR, the better it is. Thus, the

management must select the proposal with the highest IRR while using the said

technique.

Profitability Index Method (PI)

The technique denotes the ratio of the cash flows occurring from a project over the

years and the amount of the initial investment of the project concerned. Thus, the

investment appraisal technique is an attempt to draw the relationship between the

costs and benefits of a proposed project (Rὂhrich, 2014). The management of an

enterprise can employ the following formula for PI to make the evaluation of the

investment-

Profitability Index = Present value of future net cash flows

initial Investment

An increment in the value of the profitability index represents the financial

attractiveness of the proposed project. This is because in the said case, the ratio

indicates that present value (PV) of the project is more than the initial investment.

Thus, the management must note the fact that the profitability index of 1.0 or lower

than that are logically the lowest acceptable measures on the index, and the

proposals must be rejected in this case.

Pay Back Period Method

The technique leads to the calculation of the ratio which represents the time the

initial capital investment of the project recovered by the earning of the cash inflows of

any proposal concerned. Thus the formula that can be used by the management for

the computation of the payback period is-

Payback period = Cost of the proposal/ Annual cash inflows from the proposal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

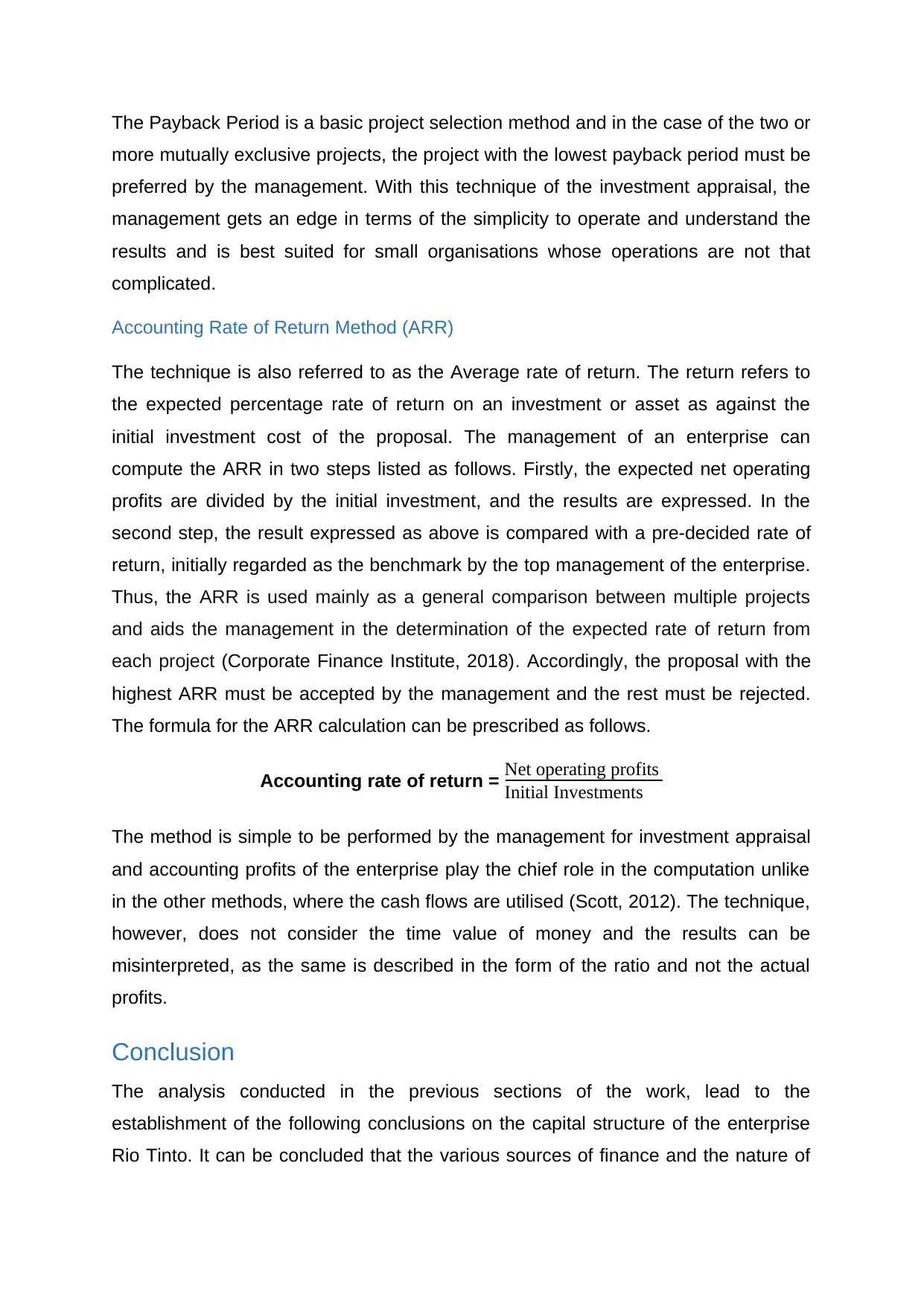

The Payback Period is a basic project selection method and in the case of the two or

more mutually exclusive projects, the project with the lowest payback period must be

preferred by the management. With this technique of the investment appraisal, the

management gets an edge in terms of the simplicity to operate and understand the

results and is best suited for small organisations whose operations are not that

complicated.

Accounting Rate of Return Method (ARR)

The technique is also referred to as the Average rate of return. The return refers to

the expected percentage rate of return on an investment or asset as against the

initial investment cost of the proposal. The management of an enterprise can

compute the ARR in two steps listed as follows. Firstly, the expected net operating

profits are divided by the initial investment, and the results are expressed. In the

second step, the result expressed as above is compared with a pre-decided rate of

return, initially regarded as the benchmark by the top management of the enterprise.

Thus, the ARR is used mainly as a general comparison between multiple projects

and aids the management in the determination of the expected rate of return from

each project (Corporate Finance Institute, 2018). Accordingly, the proposal with the

highest ARR must be accepted by the management and the rest must be rejected.

The formula for the ARR calculation can be prescribed as follows.

Accounting rate of return = Net operating profits

Initial Investments

The method is simple to be performed by the management for investment appraisal

and accounting profits of the enterprise play the chief role in the computation unlike

in the other methods, where the cash flows are utilised (Scott, 2012). The technique,

however, does not consider the time value of money and the results can be

misinterpreted, as the same is described in the form of the ratio and not the actual

profits.

Conclusion

The analysis conducted in the previous sections of the work, lead to the

establishment of the following conclusions on the capital structure of the enterprise

Rio Tinto. It can be concluded that the various sources of finance and the nature of

more mutually exclusive projects, the project with the lowest payback period must be

preferred by the management. With this technique of the investment appraisal, the

management gets an edge in terms of the simplicity to operate and understand the

results and is best suited for small organisations whose operations are not that

complicated.

Accounting Rate of Return Method (ARR)

The technique is also referred to as the Average rate of return. The return refers to

the expected percentage rate of return on an investment or asset as against the

initial investment cost of the proposal. The management of an enterprise can

compute the ARR in two steps listed as follows. Firstly, the expected net operating

profits are divided by the initial investment, and the results are expressed. In the

second step, the result expressed as above is compared with a pre-decided rate of

return, initially regarded as the benchmark by the top management of the enterprise.

Thus, the ARR is used mainly as a general comparison between multiple projects

and aids the management in the determination of the expected rate of return from

each project (Corporate Finance Institute, 2018). Accordingly, the proposal with the

highest ARR must be accepted by the management and the rest must be rejected.

The formula for the ARR calculation can be prescribed as follows.

Accounting rate of return = Net operating profits

Initial Investments

The method is simple to be performed by the management for investment appraisal

and accounting profits of the enterprise play the chief role in the computation unlike

in the other methods, where the cash flows are utilised (Scott, 2012). The technique,

however, does not consider the time value of money and the results can be

misinterpreted, as the same is described in the form of the ratio and not the actual

profits.

Conclusion

The analysis conducted in the previous sections of the work, lead to the

establishment of the following conclusions on the capital structure of the enterprise

Rio Tinto. It can be concluded that the various sources of finance and the nature of

borrowings are significant elements of the balance sheet and are rightly termed as

the strategic business decisions because of the amount involved and the impact on

the business. The decision concerning the capital structure must be efficient enough

to be in line with the overall corporate objectives of an enterprise. As seen from the

case study of the company Rio Tinto, which is a well-known name in the field of the

metal and mining industry, it can be stated that sound capital allocation policies lead

to the stabilised business operations and facilitate the company to gain a competitive

advantage as well. The company Rio Tinto has been consistently investing in major

capital assets and projects and the success can be rightly attributed to the sound

capital structure. Currently, the company is engaged in the reduction of the debt

component. Thus, The capital structure of the company has improved as that from

the last year. The company has been additionally considering major capital

investments to attain the overall development objectives and growth of the entity.

In addition to the above, the work also highlighted the various methods of capital

appraisal which can be used by the management of the entities to assess the

viability of the capital expenditures. The administration of each investment appraisal

technique is different and has individual pros and cons.

the strategic business decisions because of the amount involved and the impact on

the business. The decision concerning the capital structure must be efficient enough

to be in line with the overall corporate objectives of an enterprise. As seen from the

case study of the company Rio Tinto, which is a well-known name in the field of the

metal and mining industry, it can be stated that sound capital allocation policies lead

to the stabilised business operations and facilitate the company to gain a competitive

advantage as well. The company Rio Tinto has been consistently investing in major

capital assets and projects and the success can be rightly attributed to the sound

capital structure. Currently, the company is engaged in the reduction of the debt

component. Thus, The capital structure of the company has improved as that from

the last year. The company has been additionally considering major capital

investments to attain the overall development objectives and growth of the entity.

In addition to the above, the work also highlighted the various methods of capital

appraisal which can be used by the management of the entities to assess the

viability of the capital expenditures. The administration of each investment appraisal

technique is different and has individual pros and cons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Arjunan, K. C. (2017). A New Method to Estimate NPV from the Capital Amortization

Schedule and an Insight into Why NPV Is Not the Appropriate Criterion for Capital

Investment Decision [online] Available from:

https://www.researchgate.net/publication/316228193_A_new_method_to_estimate_

NPV_and_IRR_from_the_capital_amortization_schedule_and_an_insight_into_why_

NPV_is_not_the_appropriate_criterion_for_capital_investment_decision [Accessed

on: 21/07/2019].

Brigham, E. F., and Houston, J. F. (2012) Fundamentals of Financial Management.

Boston MA: Cengage Learning.

Corporate Finance Institute (2018). ARR- Accounting Rate of Return [online]

Available from:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/arr-

accounting-rate-of-return/ [Accessed on: 21/07/2019].

Gallo, A. (2014). A refresher on net present value. Harvard Business Review [online]

Available from:

http://www.cogencygroup.ca/uploads/5/4/8/7/54873895/harvard_business_review-

a_refresher_on_net_present_value_november_19_2014.pdf [Accessed on:

21/07/2019].

Öztekin, Ö. (2015) Capital structure decisions around the world: which factors are

reliably important?. Journal of Financial and Quantitative Analysis, 50(3), pp. 301-

323.

Rio Tinto (2018a) 2018 Strategic report [online] Available from:

https://www.riotinto.com/documents/RT_2018_strategic_report.pdf [Accessed on:

21/07/2019].

Rio Tinto (2018b) 2018 Annual Report [online] Available from:

http://www.riotinto.com/documents/RT_2018_annual_report.pdf [Accessed on:

21/07/2019].

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a

Case Study. Boston: Walter de Gruyter GmbH & Co.

Arjunan, K. C. (2017). A New Method to Estimate NPV from the Capital Amortization

Schedule and an Insight into Why NPV Is Not the Appropriate Criterion for Capital

Investment Decision [online] Available from:

https://www.researchgate.net/publication/316228193_A_new_method_to_estimate_

NPV_and_IRR_from_the_capital_amortization_schedule_and_an_insight_into_why_

NPV_is_not_the_appropriate_criterion_for_capital_investment_decision [Accessed

on: 21/07/2019].

Brigham, E. F., and Houston, J. F. (2012) Fundamentals of Financial Management.

Boston MA: Cengage Learning.

Corporate Finance Institute (2018). ARR- Accounting Rate of Return [online]

Available from:

https://corporatefinanceinstitute.com/resources/knowledge/accounting/arr-

accounting-rate-of-return/ [Accessed on: 21/07/2019].

Gallo, A. (2014). A refresher on net present value. Harvard Business Review [online]

Available from:

http://www.cogencygroup.ca/uploads/5/4/8/7/54873895/harvard_business_review-

a_refresher_on_net_present_value_november_19_2014.pdf [Accessed on:

21/07/2019].

Öztekin, Ö. (2015) Capital structure decisions around the world: which factors are

reliably important?. Journal of Financial and Quantitative Analysis, 50(3), pp. 301-

323.

Rio Tinto (2018a) 2018 Strategic report [online] Available from:

https://www.riotinto.com/documents/RT_2018_strategic_report.pdf [Accessed on:

21/07/2019].

Rio Tinto (2018b) 2018 Annual Report [online] Available from:

http://www.riotinto.com/documents/RT_2018_annual_report.pdf [Accessed on:

21/07/2019].

Rὂhrich, M. (2014) Fundamentals of Investment Appraisal: An Illustration based on a

Case Study. Boston: Walter de Gruyter GmbH & Co.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution.

Oxford: Oxford University Press. p. 342.

Oxford: Oxford University Press. p. 342.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.