Audit and Assurance Compliance: Risk Assessment of Cerise Enterprise

VerifiedAdded on 2023/06/07

|11

|2088

|353

Report

AI Summary

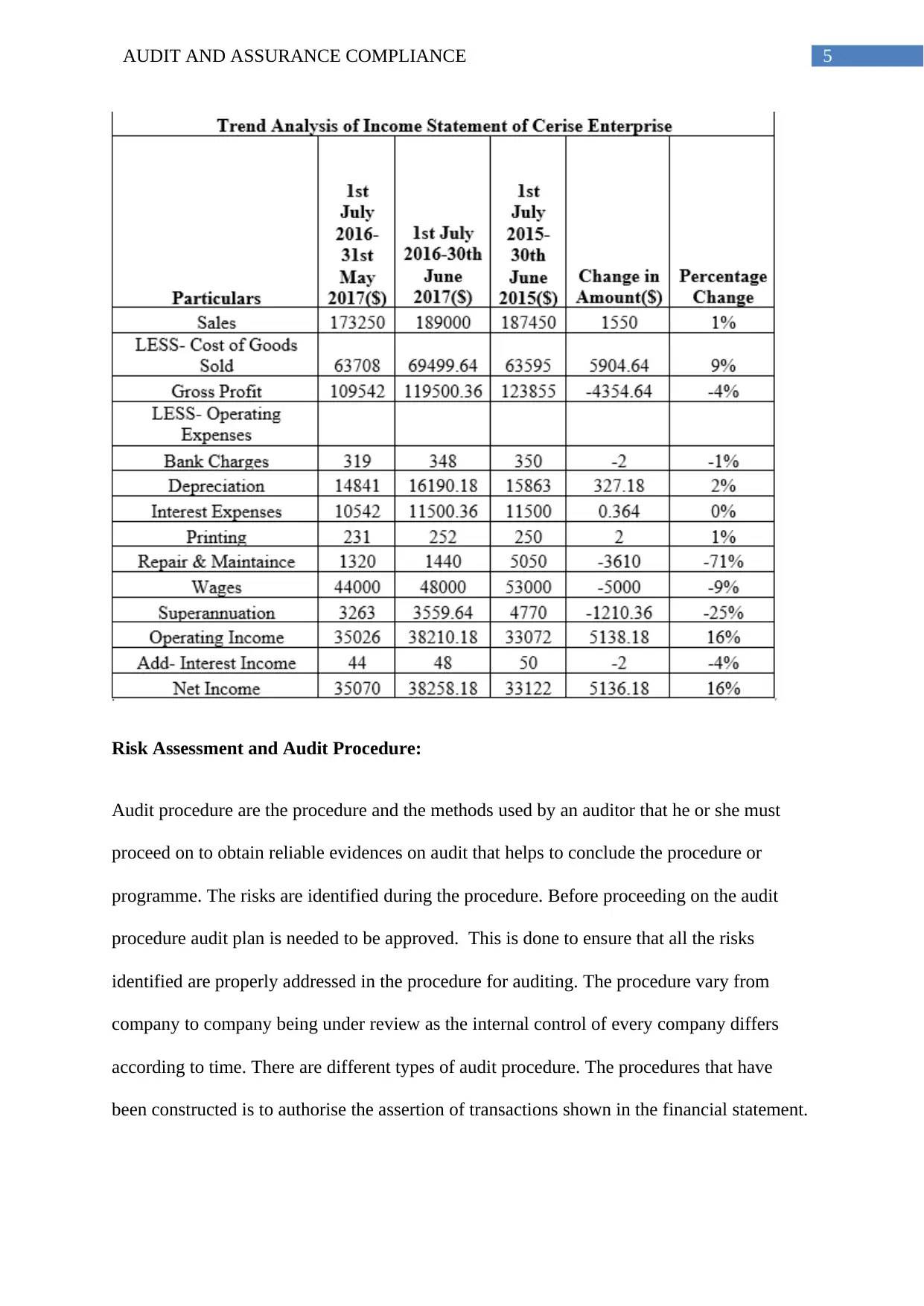

This report provides an analysis of audit and assurance compliance, with a focus on risk assessment within Cerise Enterprise. It begins with a preliminary assessment of materiality for the financial report, calculating the audit budget and comparing it to the suggested budget, highlighting potential areas needing further scrutiny. An analytical review is conducted, emphasizing the importance of identifying potential risk areas and performing substantive tests to gather reliable evidence. The report identifies several accounts at risk of material misstatement, including wages, superannuation, repair and maintenance, and cost of goods sold, outlining specific audit procedures for each. It also addresses the issue of fraud risk, cautioning against dismissing it based solely on employee trustworthiness. The report concludes by stressing the importance of proactive risk management and the successful implementation of audit procedures to ensure a true and fair view of the company's financial standing.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.