Risk Management Models and Investment Analysis Assignment

VerifiedAdded on 2021/04/16

|6

|940

|87

Homework Assignment

AI Summary

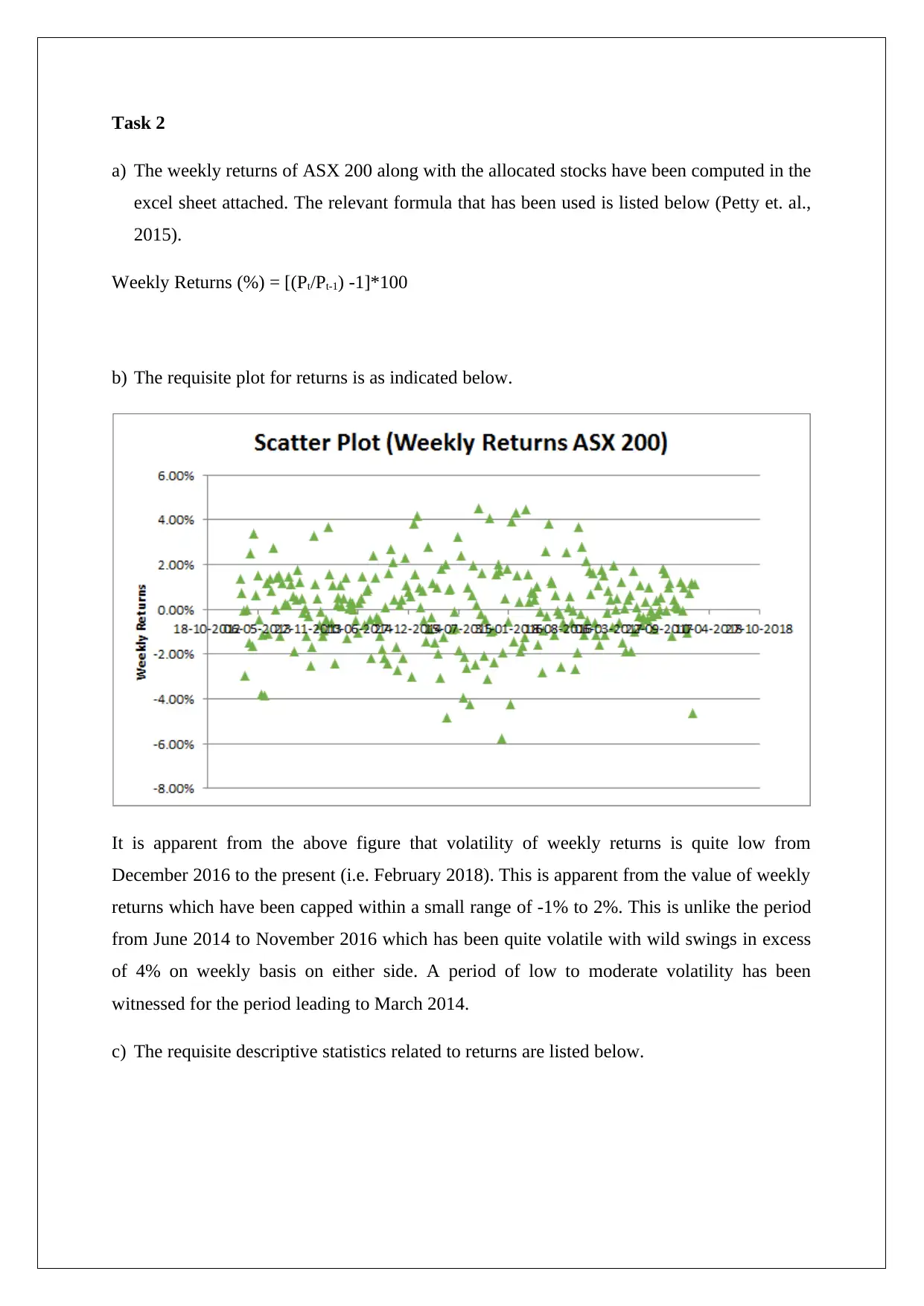

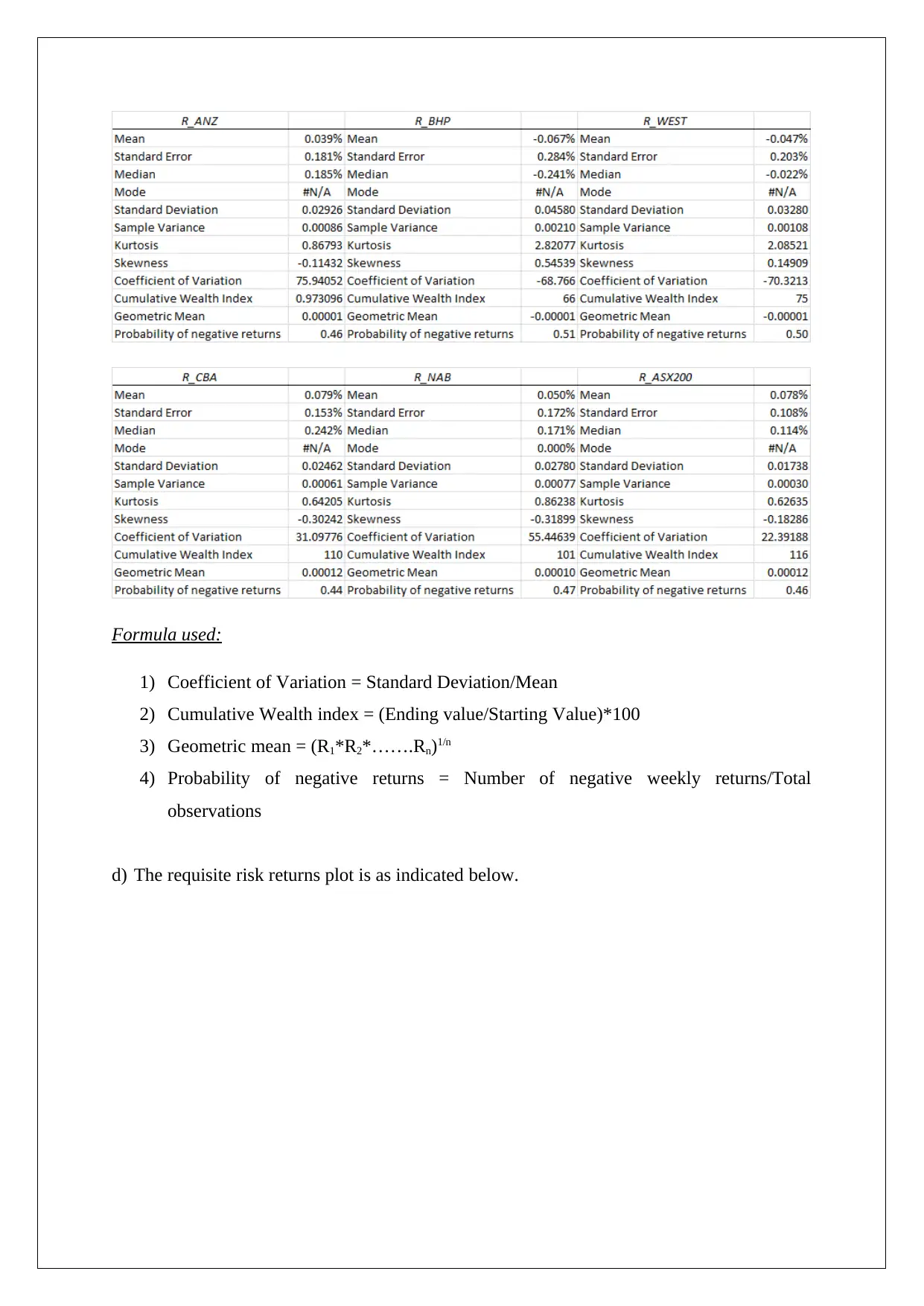

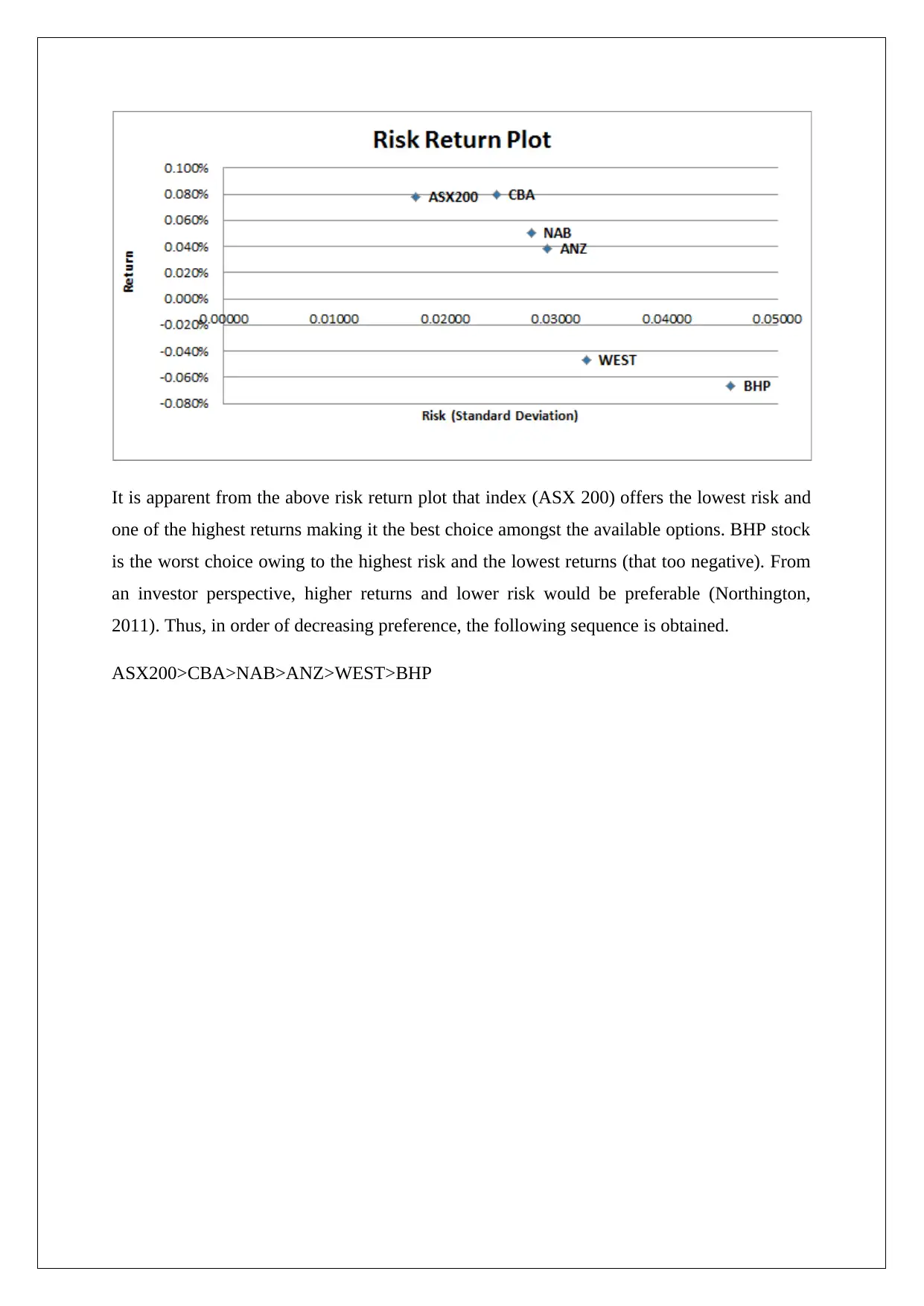

This assignment delves into risk management models and their application in financial analysis. It begins by emphasizing the importance of considering both risk and returns when evaluating financial assets, highlighting the use of historical data, future scenario projections, and probability assignments to determine mean returns and associated risks. The assignment discusses risk management techniques such as Value at Risk (VAR) and portfolio diversification to mitigate potential losses. It stresses the significance of continuous quantitative analysis and the consideration of qualitative factors in investment decisions. The practical section of the assignment analyzes the weekly returns of ASX 200 and allocated stocks using provided formulas and descriptive statistics, including the calculation of weekly returns, coefficient of variation, cumulative wealth index, and geometric mean. The analysis reveals volatility trends and presents a risk-return plot, allowing for a comparative assessment of investment options, ultimately ranking the stocks based on their risk-return profiles, with ASX200 being the preferred choice and BHP the least desirable.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.