Derivatives and Risk Management Report for Elite Copper Corporation

VerifiedAdded on 2022/12/27

|15

|6046

|95

Report

AI Summary

This report presents a risk management consultation for Elite Copper Corporation, addressing potential risks associated with decisions to increase cash flows, company size, and valuation. It covers definitions of key terms and explores various risk management strategies, including the use of futures contracts, particularly copper and equity futures. The report discusses optimal hedge ratios, explaining how to calculate and apply them to mitigate price volatility. Furthermore, it analyzes historical spot and futures prices over a five-year period, illustrating market trends and fluctuations. The analysis includes the graphical representation of the market booms, recessions, recoveries, and troughs. The report offers insights into the short position strategy and the benefits of using financial futures, such as US treasury futures, for hedging. The report aims to provide a detailed overview of the risks and the possible strategies for the company to make informed decisions to safeguard itself from the risks.

Running head: DERIVATIVES 1

Risk management consulting report to elite Copper Corporation

Student’s name

Name of the university

Author’s note

Risk management consulting report to elite Copper Corporation

Student’s name

Name of the university

Author’s note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DERIVATIVES 2

Executive summary

This paper is a short consultation report to Mr Richard Morris and the elite copper

corporation. It is specifically a risk management report written in response to the raised points of

concern. The report covers aspects regarding the potential risks that the copper corporation is

likely to encounter while pursuing the intend decisions to increase its cash flows, company size

and valuation. Therefore the report highlights the various aspects of concern that need to be

critically assessed and analyzed before undertaking such decisions. Within the report, alternative

possible strategies that have to be undertaken are covered. These will be used guidelines or areas

of references when making company decisions. The report covers definitions and explanations of

important terms and concepts. All such explanations and elaborations are aimed at providing a

more informed

Introduction

The risk management report written to elite Copper Corporation is a guiding document

providing an insight into the aspects surrounding derivatives. The report goes further to provide

more detailed knowledge and understanding the types of risks that the company is exposed to.

The general discussion of the report, therefore, focuses around risk management strategies, the

positions to be taken by the firm in the copper mining industry, identifying these risks as well as

their impact on the firm. A risk is a possibility of or presence of a chance of losing something of

value. It can, therefore, be through damage, injury, liability and any other negative deviation

from the anticipated or intended result. In terms of finance, therefore, risk refers to the possibility

that a return on an investment will be lower or less than the expected return. Financial risk is

therefore subdivided into different categories. These may include risks such as capital risks,

economic risks, liquidity risks reinvestment risks and so many other types of risks. This report

will, therefore, provide explanations concerning some of the above types of risks as required for

better decision-making purposes.

Executive summary

This paper is a short consultation report to Mr Richard Morris and the elite copper

corporation. It is specifically a risk management report written in response to the raised points of

concern. The report covers aspects regarding the potential risks that the copper corporation is

likely to encounter while pursuing the intend decisions to increase its cash flows, company size

and valuation. Therefore the report highlights the various aspects of concern that need to be

critically assessed and analyzed before undertaking such decisions. Within the report, alternative

possible strategies that have to be undertaken are covered. These will be used guidelines or areas

of references when making company decisions. The report covers definitions and explanations of

important terms and concepts. All such explanations and elaborations are aimed at providing a

more informed

Introduction

The risk management report written to elite Copper Corporation is a guiding document

providing an insight into the aspects surrounding derivatives. The report goes further to provide

more detailed knowledge and understanding the types of risks that the company is exposed to.

The general discussion of the report, therefore, focuses around risk management strategies, the

positions to be taken by the firm in the copper mining industry, identifying these risks as well as

their impact on the firm. A risk is a possibility of or presence of a chance of losing something of

value. It can, therefore, be through damage, injury, liability and any other negative deviation

from the anticipated or intended result. In terms of finance, therefore, risk refers to the possibility

that a return on an investment will be lower or less than the expected return. Financial risk is

therefore subdivided into different categories. These may include risks such as capital risks,

economic risks, liquidity risks reinvestment risks and so many other types of risks. This report

will, therefore, provide explanations concerning some of the above types of risks as required for

better decision-making purposes.

DERIVATIVES 3

Discussion of the report

The futures and position that elite copper should use when hedging against exposure

Futures are derivative financial agreements the give contracting parties the duty to trade

or carry out transactions on a given asset or security at a specified future point in time and price.

When dealing with futures, the buyer or seller is obliged to either purchase or sell the asset at an

agreed price at the time of maturity. This, therefore, eliminates the possibility of refusal to buy or

sell at the maturity date in the futures market. The futures market, on the other hand, refers to an

auction or bid market through buyers and sellers trade commodities at predetermined prices at

maturity. The futures market includes the New York mercantile exchange, Kansas City Board of

trade, the Chicago mercantile exchange among others (Chen, 2019).

Among the possible types of futures that the firm can take include the equity futures. The

most immediate futures that elite copper should trade-in are the copper futures, equity futures are

as well an important alternative that the company can use when hedging against future risk.

Because the copper market prices are highly volatile, elite Copper Corporation needs to

effectively protect against possibilities of unfavourable price fluctuations. Equity futures act as a

protective strategy by creating high leverages to the firm. Additionally, equity futures would

provide the company with an option to choose a position before markets are opened or closed.

Elite Copper Corporation should use financial futures such as the US treasury futures (Hargrave,

2019). The benefit associated with using such futures is that the dollar is a global currency that is

used on a global scale. Furthermore, because the dollar is a relatively stable currency, the firm is

relatively safeguarded from the highly volatile market conditions within the metals market. This,

therefore, implies that the value of the firm’s commodity on the financial market is safeguarded

from risks arising out of price volatilities. Since elite Copper Corporation is seeking to safeguard

itself from prices volatilities, and because it is a mining company, the futures position it can take

is short. The short position, therefore, means that elite company will enter into a futures contract

with any other buyer. The short futures position is, therefore, the act of entering into a binding

contract for the sale of a commodity item at a predetermined price at maturity. Therefore, the

short position would require Elite Corporation to sell copper to a buyer at an agreed price in the

future.

Discussion of the report

The futures and position that elite copper should use when hedging against exposure

Futures are derivative financial agreements the give contracting parties the duty to trade

or carry out transactions on a given asset or security at a specified future point in time and price.

When dealing with futures, the buyer or seller is obliged to either purchase or sell the asset at an

agreed price at the time of maturity. This, therefore, eliminates the possibility of refusal to buy or

sell at the maturity date in the futures market. The futures market, on the other hand, refers to an

auction or bid market through buyers and sellers trade commodities at predetermined prices at

maturity. The futures market includes the New York mercantile exchange, Kansas City Board of

trade, the Chicago mercantile exchange among others (Chen, 2019).

Among the possible types of futures that the firm can take include the equity futures. The

most immediate futures that elite copper should trade-in are the copper futures, equity futures are

as well an important alternative that the company can use when hedging against future risk.

Because the copper market prices are highly volatile, elite Copper Corporation needs to

effectively protect against possibilities of unfavourable price fluctuations. Equity futures act as a

protective strategy by creating high leverages to the firm. Additionally, equity futures would

provide the company with an option to choose a position before markets are opened or closed.

Elite Copper Corporation should use financial futures such as the US treasury futures (Hargrave,

2019). The benefit associated with using such futures is that the dollar is a global currency that is

used on a global scale. Furthermore, because the dollar is a relatively stable currency, the firm is

relatively safeguarded from the highly volatile market conditions within the metals market. This,

therefore, implies that the value of the firm’s commodity on the financial market is safeguarded

from risks arising out of price volatilities. Since elite Copper Corporation is seeking to safeguard

itself from prices volatilities, and because it is a mining company, the futures position it can take

is short. The short position, therefore, means that elite company will enter into a futures contract

with any other buyer. The short futures position is, therefore, the act of entering into a binding

contract for the sale of a commodity item at a predetermined price at maturity. Therefore, the

short position would require Elite Corporation to sell copper to a buyer at an agreed price in the

future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DERIVATIVES 4

Optimal hedge ratio

The minimum variance hedge ratio is also known as the optimal hedge ratio is a method

that is used to evaluate the correlation between the variance in the value of an asset or liability

and that of the instrument used for hedging (Chen, 2019). This concept is commonly used by

businesses or by investors to protect against threats and exposure. However, since there is no

perfect hedge, financial analysts need to calculate and determine the least variable optimal

hedge. This is specifically carried out to create a tradeoff between the existing exposure to risk

and possible alterations in the value of the underlying security at hand (Sehgal and

Agrawal,2019). Therefore, the formula for determining and calculating the optimal hedge is

given as follows:

h = ρ . σs

σf

Where: h represents the optimal hedge,ρ stands for correlation∧σ is the standard deviation. S is

the spot market price and f is the future market price.

According to the Chicago Mercantile Exchange market, the spot closing and open market prices

are $ 2.6245 and $ 2.6140. The December prices of copper futures are however given as $

2.6315 for the opening and $ 2.6420 for the closing mark. The December prices are used as the

spot prices whereas the December prices are used as the future quotations for this particular task.

It is these prices that are used for calculating the standard deviation of the copper futures when

finding the hedge ratio or optimal hedge.

Assuming that there is a high degree of correlation between the copper futures and copper, the

correlation would, therefore, be about 0.95. And that the spot and future standard deviation of the

in the prices on the market is about 0.3%. Hedge ratio would be 0.95 = 0.95( 0.003

0.0 03).

This method is an important approach that can be used in determining the highest number of

futures agreements that can be bought to acquire a hedge position (Kantox, 2017). This is

therefore calculated as a product of the correlation coefficient existing within the changes in the

Optimal hedge ratio

The minimum variance hedge ratio is also known as the optimal hedge ratio is a method

that is used to evaluate the correlation between the variance in the value of an asset or liability

and that of the instrument used for hedging (Chen, 2019). This concept is commonly used by

businesses or by investors to protect against threats and exposure. However, since there is no

perfect hedge, financial analysts need to calculate and determine the least variable optimal

hedge. This is specifically carried out to create a tradeoff between the existing exposure to risk

and possible alterations in the value of the underlying security at hand (Sehgal and

Agrawal,2019). Therefore, the formula for determining and calculating the optimal hedge is

given as follows:

h = ρ . σs

σf

Where: h represents the optimal hedge,ρ stands for correlation∧σ is the standard deviation. S is

the spot market price and f is the future market price.

According to the Chicago Mercantile Exchange market, the spot closing and open market prices

are $ 2.6245 and $ 2.6140. The December prices of copper futures are however given as $

2.6315 for the opening and $ 2.6420 for the closing mark. The December prices are used as the

spot prices whereas the December prices are used as the future quotations for this particular task.

It is these prices that are used for calculating the standard deviation of the copper futures when

finding the hedge ratio or optimal hedge.

Assuming that there is a high degree of correlation between the copper futures and copper, the

correlation would, therefore, be about 0.95. And that the spot and future standard deviation of the

in the prices on the market is about 0.3%. Hedge ratio would be 0.95 = 0.95( 0.003

0.0 03).

This method is an important approach that can be used in determining the highest number of

futures agreements that can be bought to acquire a hedge position (Kantox, 2017). This is

therefore calculated as a product of the correlation coefficient existing within the changes in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DERIVATIVES 5

spot and futures ratios of the standard deviation of future prices. With the optimal hedge ratio

being calculated, it is, therefore, possible to determine the optimal number of contracts that one

can obtain from a contract. This is done by dividing the optimal hedge product ratio together

with the total number of units of a position that is being taken by the size of a single futures

agreement. The number of contracts that one can obtain from a hedging contract can, therefore,

be calculated under the following formula.

The optimal number of contracts = ( ¿ the portfolio

contract ¿ the futures contract ) * h

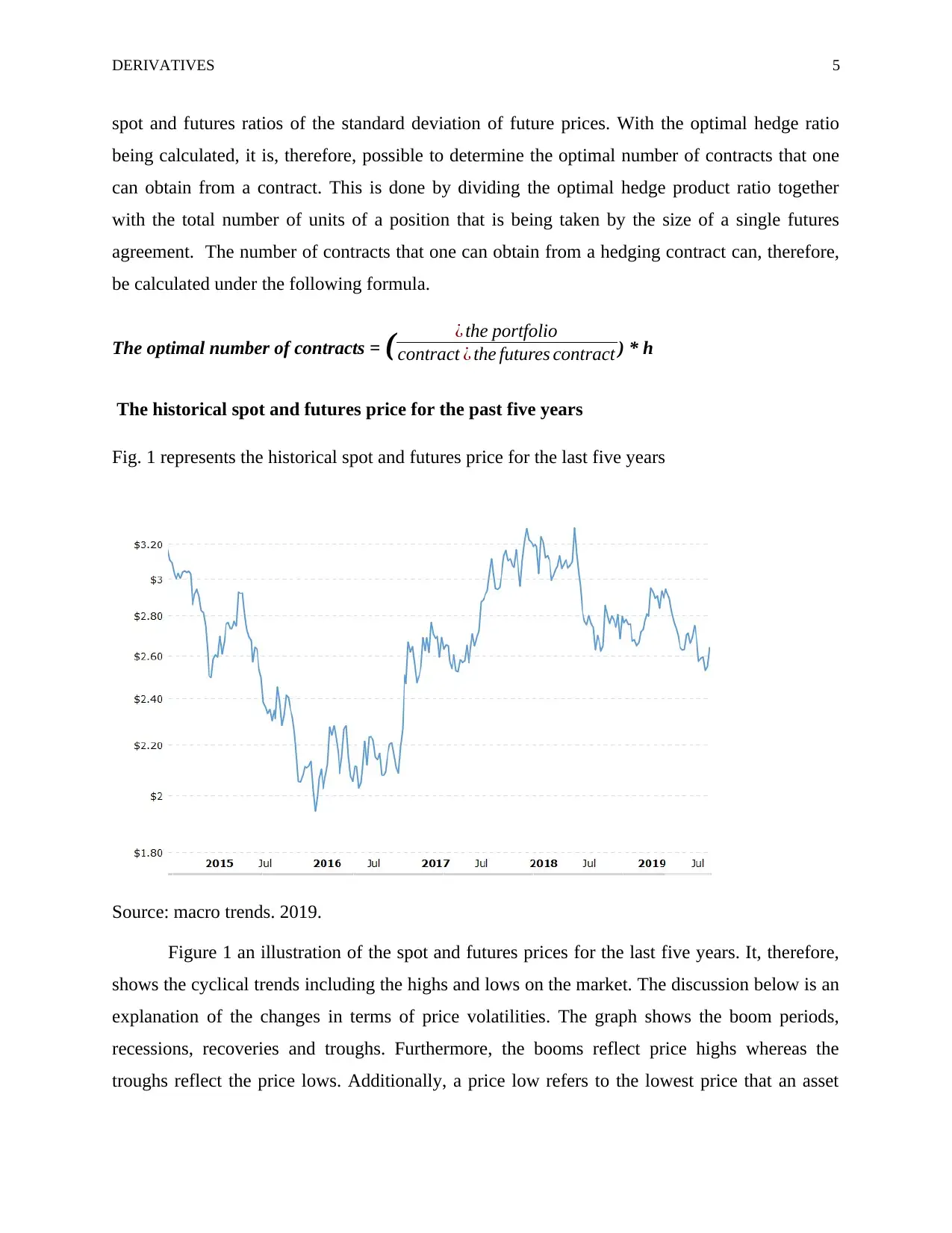

The historical spot and futures price for the past five years

Fig. 1 represents the historical spot and futures price for the last five years

Source: macro trends. 2019.

Figure 1 an illustration of the spot and futures prices for the last five years. It, therefore,

shows the cyclical trends including the highs and lows on the market. The discussion below is an

explanation of the changes in terms of price volatilities. The graph shows the boom periods,

recessions, recoveries and troughs. Furthermore, the booms reflect price highs whereas the

troughs reflect the price lows. Additionally, a price low refers to the lowest price that an asset

spot and futures ratios of the standard deviation of future prices. With the optimal hedge ratio

being calculated, it is, therefore, possible to determine the optimal number of contracts that one

can obtain from a contract. This is done by dividing the optimal hedge product ratio together

with the total number of units of a position that is being taken by the size of a single futures

agreement. The number of contracts that one can obtain from a hedging contract can, therefore,

be calculated under the following formula.

The optimal number of contracts = ( ¿ the portfolio

contract ¿ the futures contract ) * h

The historical spot and futures price for the past five years

Fig. 1 represents the historical spot and futures price for the last five years

Source: macro trends. 2019.

Figure 1 an illustration of the spot and futures prices for the last five years. It, therefore,

shows the cyclical trends including the highs and lows on the market. The discussion below is an

explanation of the changes in terms of price volatilities. The graph shows the boom periods,

recessions, recoveries and troughs. Furthermore, the booms reflect price highs whereas the

troughs reflect the price lows. Additionally, a price low refers to the lowest price that an asset

DERIVATIVES 6

can be traded for on the derivatives market. A price high on the other hand can be defined as the

highest price that an individual or trader can pay to purchase a given unit off an assets or security

on the derivatives or stock market. A trough is a point is simply a period when the prices on the

market are performing poorly or very low, a recovery, on the other hand, refers to the situation

when the security prices are beginning to rise. The recession, therefore, represents the period

when prices are falling with time whereas the boom is a time when prices are at their highest

point. With a clear understanding of the technical terms, an explanation of the above graph is

provided below:

According to the graphical illustration, the last quarter of 2014 reflects that the futures

and spot prices were undergoing a recession. This is shown by the fall from a price of $3.20 to a

price slightly below $2.60 during the first quarter of 2015.this fall or recession in the prices

created a trough at a low of an estimated $2.49 during the same period. From such a fall or

recession, the graph further continues to reflect a recovery in the spot and futures prices. This

was however recorded around the second quarter of the year 2015 to an estimated price of $2.87

which is slightly above the $2.80 mark. From such an increase, the curve proceeds with a decline

in the prices creating a record low at an estimated $1.94 in the market. This record low in prices

created the trough din the cyclical futures and spot prices. It was approximately recorded during

the first quarter of the year 2016. This poor performance however continued with a slight

recovery in the prices of the futures and spot exchanges. This can further be illustrated by a

forecast of around $2.33 within the same year of2016. Between the third quarter of 2016 up to

around the first quarter of 2017, the prices, however, reflect a different trend altogether. There is

a seeming tendency of consistency in the prices. This consistent trend in the copper prices is

reflection of a more stable trading environment on the market. Either the demand was equal to

supply or there was no trade at all. This is an implication that the prices were most likely stable

during such periods. This is reflected through the relatively constant level that is maintained

within this period.

Right from the first quarter of 2017, price increases were yet experienced yet again. This

is reflected through the recovery within the first quarter of 2017. The rise from a low of less than

$2.20 shows the increases in the futures and spot prices. During the first quarter there a rise in

the prices which is above $2.60. At this point, a constant trend in the prices is as well

can be traded for on the derivatives market. A price high on the other hand can be defined as the

highest price that an individual or trader can pay to purchase a given unit off an assets or security

on the derivatives or stock market. A trough is a point is simply a period when the prices on the

market are performing poorly or very low, a recovery, on the other hand, refers to the situation

when the security prices are beginning to rise. The recession, therefore, represents the period

when prices are falling with time whereas the boom is a time when prices are at their highest

point. With a clear understanding of the technical terms, an explanation of the above graph is

provided below:

According to the graphical illustration, the last quarter of 2014 reflects that the futures

and spot prices were undergoing a recession. This is shown by the fall from a price of $3.20 to a

price slightly below $2.60 during the first quarter of 2015.this fall or recession in the prices

created a trough at a low of an estimated $2.49 during the same period. From such a fall or

recession, the graph further continues to reflect a recovery in the spot and futures prices. This

was however recorded around the second quarter of the year 2015 to an estimated price of $2.87

which is slightly above the $2.80 mark. From such an increase, the curve proceeds with a decline

in the prices creating a record low at an estimated $1.94 in the market. This record low in prices

created the trough din the cyclical futures and spot prices. It was approximately recorded during

the first quarter of the year 2016. This poor performance however continued with a slight

recovery in the prices of the futures and spot exchanges. This can further be illustrated by a

forecast of around $2.33 within the same year of2016. Between the third quarter of 2016 up to

around the first quarter of 2017, the prices, however, reflect a different trend altogether. There is

a seeming tendency of consistency in the prices. This consistent trend in the copper prices is

reflection of a more stable trading environment on the market. Either the demand was equal to

supply or there was no trade at all. This is an implication that the prices were most likely stable

during such periods. This is reflected through the relatively constant level that is maintained

within this period.

Right from the first quarter of 2017, price increases were yet experienced yet again. This

is reflected through the recovery within the first quarter of 2017. The rise from a low of less than

$2.20 shows the increases in the futures and spot prices. During the first quarter there a rise in

the prices which is above $2.60. At this point, a constant trend in the prices is as well

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DERIVATIVES 7

experienced on the market. The consistency in the prices continues up to around the second

quarter of 2017 where prices again to a low of around $2.50. Prices however again sharply pick

up to rise to $ 3.30 which is one of the record highs in the prices. This record high is, however,

record in around the last quarter of the year 2017 to show a boom in the prices cycles. At this

point, prices become a bit constant thereby reflecting yet another high of $3.30 in the second

quarter of 2018. From this point, the pries again fall into a recession which consequently

becomes corrected when it reaches $2.65 around the third quarter of 2018. Form this point,

prices slightly recover and fall characterized by minimal volatilities reaching a high of an

estimated $2.95 during the first quarter of 2019. This is however followed by a fall in the prices

to a low of about $2.63 especially within the second quarter of the same year 2019. Therefore

such is a brief explanation of the moving trend in the futures and spot prices for the past five

years on the market. The curve was explained taking into consideration the last quarter of 2014

up to the second quarter of 2019. It further shows that prices on the financial market are

constantly characterized by declines, recoveries and in sometimes points of consistency.

However, all such changes and movements in the prices are highly subjected to several

influencing factors. These may include current information on the market, interest rates, inflation

and so many other factors.

The company’s exposure in pounds of copper

In measuring the company’s exposure, a method known as the delta exposure or dollar

delta will be used. The delta exposure is therefore used to measure the first order of price

sensitivity of a derivatives contract. This takes into account the futures and options. Such

measures are made Concerning the variances in the prices of the underlying assets. This method

is however mostly accurate in circumstances where the portfolio of assets or securities do not

contain options. This should, however, be combined with small changes in the values of

underlying assets. The level of exposure will be 0.05% which is obtained by Lessing the amount

of copper that is hedged form the total amount that the company is holding. This would give an

amount of about 0.6 kilotons at risk of exposure.

Number of copper futures contracts that should be traded

experienced on the market. The consistency in the prices continues up to around the second

quarter of 2017 where prices again to a low of around $2.50. Prices however again sharply pick

up to rise to $ 3.30 which is one of the record highs in the prices. This record high is, however,

record in around the last quarter of the year 2017 to show a boom in the prices cycles. At this

point, prices become a bit constant thereby reflecting yet another high of $3.30 in the second

quarter of 2018. From this point, the pries again fall into a recession which consequently

becomes corrected when it reaches $2.65 around the third quarter of 2018. Form this point,

prices slightly recover and fall characterized by minimal volatilities reaching a high of an

estimated $2.95 during the first quarter of 2019. This is however followed by a fall in the prices

to a low of about $2.63 especially within the second quarter of the same year 2019. Therefore

such is a brief explanation of the moving trend in the futures and spot prices for the past five

years on the market. The curve was explained taking into consideration the last quarter of 2014

up to the second quarter of 2019. It further shows that prices on the financial market are

constantly characterized by declines, recoveries and in sometimes points of consistency.

However, all such changes and movements in the prices are highly subjected to several

influencing factors. These may include current information on the market, interest rates, inflation

and so many other factors.

The company’s exposure in pounds of copper

In measuring the company’s exposure, a method known as the delta exposure or dollar

delta will be used. The delta exposure is therefore used to measure the first order of price

sensitivity of a derivatives contract. This takes into account the futures and options. Such

measures are made Concerning the variances in the prices of the underlying assets. This method

is however mostly accurate in circumstances where the portfolio of assets or securities do not

contain options. This should, however, be combined with small changes in the values of

underlying assets. The level of exposure will be 0.05% which is obtained by Lessing the amount

of copper that is hedged form the total amount that the company is holding. This would give an

amount of about 0.6 kilotons at risk of exposure.

Number of copper futures contracts that should be traded

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DERIVATIVES 8

To determine the number of contracts that Elite Copper Corporation needs to trade, the notional

value approach will be used for this paper. The notional value, therefore, refers to the total

amount that the total underlying amount of a futures contract or transaction. This value is always

higher than the market value due to concepts of leverage. The term leverage kin this case refers

to the ability to use a small amount of money to have an anticipated control over a larger value or

sum of an underlying asset. The notional value technique is commonly used in the derivatives

market to describe contracts such as the futures, options and other currency markets. The formula

for this method is given as; notional value = size of the contract multiplied by the price of the

underlying security on the market. To find the number of contracts that can be signed the

market volume available of 552 and the annual value of the company together with the 0.95

hedge ratio will be used as the key information (Kenton, 2019).

Therefore, for the elite company the copper contacts that can be made will be obtained as

follows:

= (0.95 * 12 kilotons)/552

= 11.4 kilotons *552

= 6,293 contracts.

Therefore according to the approach used, the elite company will have to sign a total of about

6,293 contracts.

Initial margin requirement of September

An initial margin requirement can be defied a the amount of money that affirm or trader in the

derivatives market should pay to buy or sell a position in a contract. The margin requirement is a

vital concept that is highly necessary especially for traders and investors intending to trade assets

and other securities in the futures market. it is, therefore, an initial deposit that a company such

elite copper corporation should make before signing any futures contract. Additionally, this

initial margin requirement is highly dependent upon the level of price volatility in the market.

The higher the market price volatility, the higher the initial margin requirement that one has to

pay as an initial amount. Similarly, when the price volatilities are low, the margin requirement is

likely to below. This margin requirement is however determined by multiplying the price times

the volume of purchase. For the initial, margin requirement in the September period would be

obtained as follows: IMR = price * volume.

= $2.614*552

= $1,442.928

To determine the number of contracts that Elite Copper Corporation needs to trade, the notional

value approach will be used for this paper. The notional value, therefore, refers to the total

amount that the total underlying amount of a futures contract or transaction. This value is always

higher than the market value due to concepts of leverage. The term leverage kin this case refers

to the ability to use a small amount of money to have an anticipated control over a larger value or

sum of an underlying asset. The notional value technique is commonly used in the derivatives

market to describe contracts such as the futures, options and other currency markets. The formula

for this method is given as; notional value = size of the contract multiplied by the price of the

underlying security on the market. To find the number of contracts that can be signed the

market volume available of 552 and the annual value of the company together with the 0.95

hedge ratio will be used as the key information (Kenton, 2019).

Therefore, for the elite company the copper contacts that can be made will be obtained as

follows:

= (0.95 * 12 kilotons)/552

= 11.4 kilotons *552

= 6,293 contracts.

Therefore according to the approach used, the elite company will have to sign a total of about

6,293 contracts.

Initial margin requirement of September

An initial margin requirement can be defied a the amount of money that affirm or trader in the

derivatives market should pay to buy or sell a position in a contract. The margin requirement is a

vital concept that is highly necessary especially for traders and investors intending to trade assets

and other securities in the futures market. it is, therefore, an initial deposit that a company such

elite copper corporation should make before signing any futures contract. Additionally, this

initial margin requirement is highly dependent upon the level of price volatility in the market.

The higher the market price volatility, the higher the initial margin requirement that one has to

pay as an initial amount. Similarly, when the price volatilities are low, the margin requirement is

likely to below. This margin requirement is however determined by multiplying the price times

the volume of purchase. For the initial, margin requirement in the September period would be

obtained as follows: IMR = price * volume.

= $2.614*552

= $1,442.928

DERIVATIVES 9

Therefore In September, the initial margin requirement is $ 1,442.928. This implies that an

investor would have to pay such an amount as an initial deposit before signing a futures contract.

Other major risks that elite copper corporation is likely to face

Besides the price risks associated with price volatilities, the elite copper corporation is as well

subjected to several numerous other risks within the market. Among these risks include risks

such as market risks, credit risks, liquidity risks, and counterparty risks. The interconnection

risks are as well part of the risks associated with transacting in the derivatives market. Therefore,

to provide a more informed understanding of the concepts, elaborative explanations are provided

below.

The market risks: market risks can be referred to as those particular risks that are general to all

investors or buyers and sellers in the financial market (Investopedia,2019). Because investors

make decisions based on assumptions and forecasts, there is always a possibility of deviation

from the intended or required returns. For instance, an investor or trader such as the elite copper

corporation would decide on making a technical analysis. However, making a technical analysis

does not fully imply that future trends in prices will be as projected (Yilgor et al, 2016).

Unplanned for events could occur in the shortest period thereby significantly influencing the

operations of the market. It is also important to note that information plays a vital role in

influencing the market trend and behaviour. Therefore a technical analysis may reliably assess

the possibility of events such as the political instabilities within an economy. Since instabilities

can result in financial consequences such as inflation, then this makes market risk an important

factor of consideration.

Liquidity risks: besides the market risks, the elite copper corporation is highly subjected to risks

resulting from liquidity (Marverick, 2018). This type of risks, however, results from an assets’

inability to be traded on the market. For example, the Elite Copper Corporation is subjected to

this type of risk because the company is trading in copper which may not have the ability to be

quickly traded. Such a scenario can consequently result in cases of low liquidity levels thereby

making coppery unmarketable. Because investors prefer trading in assets or securities that highly

liquid, they are most likely to enter into futures contracts involving highly liquid assets or

securities. This would, therefore, imply that the company will not have an effective and reliable

market for its assets. Ultimately due to liquidity risks, the copper prices will decline to low levels

of demand hence low profitability for the company. It is therefore important to take into

consideration the bid and ask spreads to assess the level costs associated.

The counterparty credit risks are as well as other types of risks that the elite company should

consider. Counterparty credit risks are risks that result from the possibilities of defaulting or

breaching the contract. This can be done by either the buyer or seller's refusal to uphold the terms

of the futures contract. Such risks are however most common in the over the counter

transactions. Since the transactions in the over the counter markets are not highly regulated and

Therefore In September, the initial margin requirement is $ 1,442.928. This implies that an

investor would have to pay such an amount as an initial deposit before signing a futures contract.

Other major risks that elite copper corporation is likely to face

Besides the price risks associated with price volatilities, the elite copper corporation is as well

subjected to several numerous other risks within the market. Among these risks include risks

such as market risks, credit risks, liquidity risks, and counterparty risks. The interconnection

risks are as well part of the risks associated with transacting in the derivatives market. Therefore,

to provide a more informed understanding of the concepts, elaborative explanations are provided

below.

The market risks: market risks can be referred to as those particular risks that are general to all

investors or buyers and sellers in the financial market (Investopedia,2019). Because investors

make decisions based on assumptions and forecasts, there is always a possibility of deviation

from the intended or required returns. For instance, an investor or trader such as the elite copper

corporation would decide on making a technical analysis. However, making a technical analysis

does not fully imply that future trends in prices will be as projected (Yilgor et al, 2016).

Unplanned for events could occur in the shortest period thereby significantly influencing the

operations of the market. It is also important to note that information plays a vital role in

influencing the market trend and behaviour. Therefore a technical analysis may reliably assess

the possibility of events such as the political instabilities within an economy. Since instabilities

can result in financial consequences such as inflation, then this makes market risk an important

factor of consideration.

Liquidity risks: besides the market risks, the elite copper corporation is highly subjected to risks

resulting from liquidity (Marverick, 2018). This type of risks, however, results from an assets’

inability to be traded on the market. For example, the Elite Copper Corporation is subjected to

this type of risk because the company is trading in copper which may not have the ability to be

quickly traded. Such a scenario can consequently result in cases of low liquidity levels thereby

making coppery unmarketable. Because investors prefer trading in assets or securities that highly

liquid, they are most likely to enter into futures contracts involving highly liquid assets or

securities. This would, therefore, imply that the company will not have an effective and reliable

market for its assets. Ultimately due to liquidity risks, the copper prices will decline to low levels

of demand hence low profitability for the company. It is therefore important to take into

consideration the bid and ask spreads to assess the level costs associated.

The counterparty credit risks are as well as other types of risks that the elite company should

consider. Counterparty credit risks are risks that result from the possibilities of defaulting or

breaching the contract. This can be done by either the buyer or seller's refusal to uphold the terms

of the futures contract. Such risks are however most common in the over the counter

transactions. Since the transactions in the over the counter markets are not highly regulated and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DERIVATIVES 10

controlled, the likelihood of defaulting and breach of contracts is significantly very high.

Therefore, if the elite copper corporation is to enter into futures contracts with an over the

counter arrangement, it would present a high level of risks. Such risks can, however, be

controlled if Richard Morris can enter into futures contracts with investors and individuals that

are well known to him. The other possible solution that Richard can use as a way of guarding

against such risks is by entering into contracts that are within highly regulated in the market. For

example, instead of using over the counter arrangements, the company should opt for the

ordinary trade exchanges.

Currency risks: a currency risk is the possibility of loss that results from the exchange

fluctuations that an investor or company trading in the market is exposed to. This normally

appears in circumstances when such an investor is transacting in a foreign currency such as the

dollar ( Caspers et al,2017). The possible fluctuations that may occur due in the market

consequently imply that the underlying value of the assets or securities will as well decline in the

long run. The elite copper corporation would be subjected to such a type of risk when it decides

to trade and sign futures contracts in other foreign currencies other than its domestic currency.

Such currency risks are commonly generated out of changes in the financial market in a country.

For example, if the elite company chose to create a futures contract in using the US dollar

currency, a fall in the interests in the United States would imply that the dollar would have lost

value. The outcome of such a loss in value to due fall in interest rates consequently affects the

value of copper on the derivatives market.

Interconnection risks: interconnection risks are risks that arise out of the reliance on the value

of other underlying assets. Because derivatives derive value for other assets, this creates a close

relationship between two different kinds of markets. The threat here comes from the possibility

of exposure to numerous factors resulting from external conditions happening to the underlying

asset's market. These consequently have a direct impact on the futures and options which at times

is not a favourable outcome. In summary one market significantly influences another market

altogether (Haotanto, 2017).

The upsides and downsides of the recommended strategies

One of the recommendations made to the company is the position to choose. In the report, Mr

Richard is advised to take a short position as one of the recommendations. However, taking a

short position has consequential outcomes that may be unfavourable in the long run. For

instance, if Mr Morris decides to take a short position, then this will likely result in

circumstances such as speculations. These buyers, for example, are likely to consider taking a

short position as speculation and yet the sellers consider this as an approach of hedging (Houllier

and Murphy, 2017). Ultimately this creates a situation of contradictions among the two parties.

The buyers will want to sign a futures contract at very low prices are even low many prices and

controlled, the likelihood of defaulting and breach of contracts is significantly very high.

Therefore, if the elite copper corporation is to enter into futures contracts with an over the

counter arrangement, it would present a high level of risks. Such risks can, however, be

controlled if Richard Morris can enter into futures contracts with investors and individuals that

are well known to him. The other possible solution that Richard can use as a way of guarding

against such risks is by entering into contracts that are within highly regulated in the market. For

example, instead of using over the counter arrangements, the company should opt for the

ordinary trade exchanges.

Currency risks: a currency risk is the possibility of loss that results from the exchange

fluctuations that an investor or company trading in the market is exposed to. This normally

appears in circumstances when such an investor is transacting in a foreign currency such as the

dollar ( Caspers et al,2017). The possible fluctuations that may occur due in the market

consequently imply that the underlying value of the assets or securities will as well decline in the

long run. The elite copper corporation would be subjected to such a type of risk when it decides

to trade and sign futures contracts in other foreign currencies other than its domestic currency.

Such currency risks are commonly generated out of changes in the financial market in a country.

For example, if the elite company chose to create a futures contract in using the US dollar

currency, a fall in the interests in the United States would imply that the dollar would have lost

value. The outcome of such a loss in value to due fall in interest rates consequently affects the

value of copper on the derivatives market.

Interconnection risks: interconnection risks are risks that arise out of the reliance on the value

of other underlying assets. Because derivatives derive value for other assets, this creates a close

relationship between two different kinds of markets. The threat here comes from the possibility

of exposure to numerous factors resulting from external conditions happening to the underlying

asset's market. These consequently have a direct impact on the futures and options which at times

is not a favourable outcome. In summary one market significantly influences another market

altogether (Haotanto, 2017).

The upsides and downsides of the recommended strategies

One of the recommendations made to the company is the position to choose. In the report, Mr

Richard is advised to take a short position as one of the recommendations. However, taking a

short position has consequential outcomes that may be unfavourable in the long run. For

instance, if Mr Morris decides to take a short position, then this will likely result in

circumstances such as speculations. These buyers, for example, are likely to consider taking a

short position as speculation and yet the sellers consider this as an approach of hedging (Houllier

and Murphy, 2017). Ultimately this creates a situation of contradictions among the two parties.

The buyers will want to sign a futures contract at very low prices are even low many prices and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DERIVATIVES 11

yet the sellers prefer to sell at higher prices. This creates an exploitative scenario in the market

and hence lowering the value of the assets and profitability especially for the seller.

The other limitation associated with short selling is that it can result in significant losses. Since

the signing futures contracts are binding to all the traders, the possibility of making, the wrong

forecast is very costly especially to the person taking a short position. For example, If Mr

Richard conducted a technical analysis and forecasted a decline in copper prices; he would then

opt for a futures contract that will safeguard him from such a loss. However, this type of

forecasting may not be the actual outcome at the time of maturity. This is very common in cases

where the spot price on the market is higher the agreed-upon price. Mr Richard would be under

obligation to sell out the copper to the buyer at a price much lower than the spot price at the time

of maturity. For example, in case Mr Richard agrees to sell a kiloton of copper at $15,000 at a

given time in December in anticipation that the spot price during such a time will be much less

than $15,000. Unfortunately when the maturity date of December comes the spot price of copper

per kiloton is $20,000. Mr Richard will have made a loss of $5,000 = (20,000-15,000) $ in per

kiloton at such a period. Therefore taking a short position is highly risky.

On the other hand, however, taking a short position can be beneficial to the company. The short

is primarily a hedging tool that is used to protect against future losses and price fluctuations. Due

to uncertainties, the possibility of future returns is subjected to several risks. Risks such as

systematic and unsystematic risks are a potential threat. Therefore for the elite copper

corporation, constant price fluctuations significantly increase the risks of exposure. It is also

important to note that the longer the investment period, the higher the risk of exposure. For a

reason, taking a short position would ultimately lower the risk of exposure in the long run. The

additional importance of short selling plays an important role in generating quick access to

capital and funds.

The recommendation to use the US treasury futures could b associated with risks such as losses

in the value of copper in the long run. Since these futures are traded in a foreign currency, there

is a high possibility of suffering losses in the case the dollar depreciates on the exchange market.

The implication of using such futures is that the company will be subjected to constant

undervalues of the assets in the market. The impacts of such tendencies of undervaluing are

consequential in terms of profitability to the company that intends to increase revenues. The

benefit, however, is that such treasury futures offer high levels of liquidity to the company. This

is important towards generating more income to finance activities yet they are further

characterized by relative levels of security in the long run (CME Group, 2019).

Historical development of the copper commodity futures

The copper commodity futures are standardized exchange agreements through which the

participants in a futures agreement agree to transact with each other specified quantities of

copper an agreed price in the future or the time of maturity. These copper futures can be traded

yet the sellers prefer to sell at higher prices. This creates an exploitative scenario in the market

and hence lowering the value of the assets and profitability especially for the seller.

The other limitation associated with short selling is that it can result in significant losses. Since

the signing futures contracts are binding to all the traders, the possibility of making, the wrong

forecast is very costly especially to the person taking a short position. For example, If Mr

Richard conducted a technical analysis and forecasted a decline in copper prices; he would then

opt for a futures contract that will safeguard him from such a loss. However, this type of

forecasting may not be the actual outcome at the time of maturity. This is very common in cases

where the spot price on the market is higher the agreed-upon price. Mr Richard would be under

obligation to sell out the copper to the buyer at a price much lower than the spot price at the time

of maturity. For example, in case Mr Richard agrees to sell a kiloton of copper at $15,000 at a

given time in December in anticipation that the spot price during such a time will be much less

than $15,000. Unfortunately when the maturity date of December comes the spot price of copper

per kiloton is $20,000. Mr Richard will have made a loss of $5,000 = (20,000-15,000) $ in per

kiloton at such a period. Therefore taking a short position is highly risky.

On the other hand, however, taking a short position can be beneficial to the company. The short

is primarily a hedging tool that is used to protect against future losses and price fluctuations. Due

to uncertainties, the possibility of future returns is subjected to several risks. Risks such as

systematic and unsystematic risks are a potential threat. Therefore for the elite copper

corporation, constant price fluctuations significantly increase the risks of exposure. It is also

important to note that the longer the investment period, the higher the risk of exposure. For a

reason, taking a short position would ultimately lower the risk of exposure in the long run. The

additional importance of short selling plays an important role in generating quick access to

capital and funds.

The recommendation to use the US treasury futures could b associated with risks such as losses

in the value of copper in the long run. Since these futures are traded in a foreign currency, there

is a high possibility of suffering losses in the case the dollar depreciates on the exchange market.

The implication of using such futures is that the company will be subjected to constant

undervalues of the assets in the market. The impacts of such tendencies of undervaluing are

consequential in terms of profitability to the company that intends to increase revenues. The

benefit, however, is that such treasury futures offer high levels of liquidity to the company. This

is important towards generating more income to finance activities yet they are further

characterized by relative levels of security in the long run (CME Group, 2019).

Historical development of the copper commodity futures

The copper commodity futures are standardized exchange agreements through which the

participants in a futures agreement agree to transact with each other specified quantities of

copper an agreed price in the future or the time of maturity. These copper futures can be traded

DERIVATIVES 12

on the market such as The London Metal Exchange, The New York Mercantile Exchange and

The Chicago Mercantile Exchange among other markets. The background and development of

the commodities market is traced back to around the 17th century in Japan, on the contrary, some

sources reveal that in 6000 before, china was already trading in the commodities market

(Abumustafa and AL-Abduljader,2011). However, an organized mode of trading in commodities

started in around the 1840s in America with the establishment of the Chicago Board Of Trade

(CBOT).

During the early twentieth century after the industrial revolution, three was a period of high

levels of technology. This meant that countries such as Britain had the capacity to melt metals

such as copper on a large scale. The capability to smelt this iron, therefore, led to the

development of a major copper deposit area in Chile, North America, and Australia among other

countries. This eased the process of lower-grade ores hence a global explosion in the copper

market. Such reasons for expansion significantly implied that there was a need for a better

trading environment. In around 1993, the creation of the COMEX was under undertaken. This

was to play a primary objective of acting as the futures and options market for metals. Among

such metals include gold, aluminium, silver among others. Effectively there was growth which

ultimately led to a merger forming the New York mercantile exchange which is the world's

largest physical trading platform today. It is such a brief background today forms the

commodities market.

The outlook of the futures commodities market in the coming years

Transacting in the commodities market involves several numerous uncertainties and risks. The

high levels of price volatilities are excessively very unpredictable and therefore one needs to

trade with great caution. Since the market is under significant influence from several factors such

as current information, price changes alone may not be a reliable method of predicting future

trends. For example, if the US-China trade war continues to take place in the next three to five

years, the metal market could as well, continue to dampen (Hong Vo et al, 2018). The

agricultural commodities market, on the other hand, is subjectively under influence resulting

from the changes in the global climate and weather changes. Since the factors that hampered

agricultural commodities have quite stabilized, there is a significant future improvement in the

market. The copper prices according to (Trading Economics, 2019) are expected to fall to an

anticipated price of $2.3876 by the 4th quarter of the year 2020. On the other hand, according to

the world report of 2019, crude oil consumption has been registering relative increases. This is

backed up the 1.1 percentage increase in crude oil early this year. From such a scenario one can

forecast the future of the commodities market will have negligible growth even further in the

coming years (Rubani, 2017). Such improved performances arise out of expansions in crude oil

consumptions in countries such as the United States, China, India. The natural gas market is as

well expected to pick over the coming periods especially in terms of prices. Coal prices, on the

other hand, are a well forecasted to undergo a recovery out of their previous poor performances

of 2018. Generally, looking back at the 2018 period, the commodities market was on a downfall.

on the market such as The London Metal Exchange, The New York Mercantile Exchange and

The Chicago Mercantile Exchange among other markets. The background and development of

the commodities market is traced back to around the 17th century in Japan, on the contrary, some

sources reveal that in 6000 before, china was already trading in the commodities market

(Abumustafa and AL-Abduljader,2011). However, an organized mode of trading in commodities

started in around the 1840s in America with the establishment of the Chicago Board Of Trade

(CBOT).

During the early twentieth century after the industrial revolution, three was a period of high

levels of technology. This meant that countries such as Britain had the capacity to melt metals

such as copper on a large scale. The capability to smelt this iron, therefore, led to the

development of a major copper deposit area in Chile, North America, and Australia among other

countries. This eased the process of lower-grade ores hence a global explosion in the copper

market. Such reasons for expansion significantly implied that there was a need for a better

trading environment. In around 1993, the creation of the COMEX was under undertaken. This

was to play a primary objective of acting as the futures and options market for metals. Among

such metals include gold, aluminium, silver among others. Effectively there was growth which

ultimately led to a merger forming the New York mercantile exchange which is the world's

largest physical trading platform today. It is such a brief background today forms the

commodities market.

The outlook of the futures commodities market in the coming years

Transacting in the commodities market involves several numerous uncertainties and risks. The

high levels of price volatilities are excessively very unpredictable and therefore one needs to

trade with great caution. Since the market is under significant influence from several factors such

as current information, price changes alone may not be a reliable method of predicting future

trends. For example, if the US-China trade war continues to take place in the next three to five

years, the metal market could as well, continue to dampen (Hong Vo et al, 2018). The

agricultural commodities market, on the other hand, is subjectively under influence resulting

from the changes in the global climate and weather changes. Since the factors that hampered

agricultural commodities have quite stabilized, there is a significant future improvement in the

market. The copper prices according to (Trading Economics, 2019) are expected to fall to an

anticipated price of $2.3876 by the 4th quarter of the year 2020. On the other hand, according to

the world report of 2019, crude oil consumption has been registering relative increases. This is

backed up the 1.1 percentage increase in crude oil early this year. From such a scenario one can

forecast the future of the commodities market will have negligible growth even further in the

coming years (Rubani, 2017). Such improved performances arise out of expansions in crude oil

consumptions in countries such as the United States, China, India. The natural gas market is as

well expected to pick over the coming periods especially in terms of prices. Coal prices, on the

other hand, are a well forecasted to undergo a recovery out of their previous poor performances

of 2018. Generally, looking back at the 2018 period, the commodities market was on a downfall.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.