7244AFE Derivatives & Risk Management: Risk Analysis Report for Copper

VerifiedAdded on 2022/11/30

|14

|4701

|307

Report

AI Summary

This report provides a comprehensive risk analysis for Elite Copper Corporation, addressing the volatility of copper prices and offering strategies for risk management. The report explores the use of futures contracts to hedge against price fluctuations, determining the optimal hedge ratio and comparing spot and futures prices over a five-year period. It calculates the company's exposure, the number of contracts needed in the derivative market, and the margin requirements. Furthermore, the report identifies the major risks faced by Elite Copper beyond price changes, including factors influencing copper extraction and market dynamics, providing a detailed consulting report for the client's risk mitigation strategies. The report is a response to a take-home assignment for the course 7244AFE Derivatives & Risk Management.

Elite Copper Corporation

Risk Analysis Report

NAME OF STUDENT

risk net

Risk Analysis Report

NAME OF STUDENT

risk net

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................3

Issues..........................................................................................................................................4

Conclusions..............................................................................................................................10

References................................................................................................................................11

Executive Summary...................................................................................................................2

Introduction................................................................................................................................3

Issues..........................................................................................................................................4

Conclusions..............................................................................................................................10

References................................................................................................................................11

Executive Summary

This assignment talks about the derivative contract that we should choose especially in case

of commodity derivative. So, this assignment has got a commodity name copper, for which

prices are fluctuating and the hedger wants to hedge the complete risk and asks us in which

type of contract he should fall. (Kampf, 2013) Prospects contract executed in item exchanges

can be physically settled upon contract advancement or is cash settled (as instructed by the

commodity exchange). The outcome structure is straight concerning the market cost at the

time of settlement. (TOWN, 2016) Supporting the commodity worth peril using exchange

traded auxiliary contracts will all in all cut down the cost of supporting as diverged from

undertaking an over-the counter auxiliary contract for the inspiration driving supporting –

especially where the traded subordinate contract is significantly liquid. (Petry, 2014) This is,

as it were, credited to the lower spreads on the referred to subordinate costs when appeared

differently in relation to the over-the counter promotes which don't require any additional

trade (again as done on the over-the-counter grandstand) and the certifiable cost is

fundamentally credited to margin upkeep. (Y, 2016) This is fundamental for those

associations that don't have the significant ability to pass on the costs of thing worth change

and supports on to the customer – due to contention in addition, other market loads. (Cooper,

2017) (Henderson & Hobson, 2010)

This assignment talks about the derivative contract that we should choose especially in case

of commodity derivative. So, this assignment has got a commodity name copper, for which

prices are fluctuating and the hedger wants to hedge the complete risk and asks us in which

type of contract he should fall. (Kampf, 2013) Prospects contract executed in item exchanges

can be physically settled upon contract advancement or is cash settled (as instructed by the

commodity exchange). The outcome structure is straight concerning the market cost at the

time of settlement. (TOWN, 2016) Supporting the commodity worth peril using exchange

traded auxiliary contracts will all in all cut down the cost of supporting as diverged from

undertaking an over-the counter auxiliary contract for the inspiration driving supporting –

especially where the traded subordinate contract is significantly liquid. (Petry, 2014) This is,

as it were, credited to the lower spreads on the referred to subordinate costs when appeared

differently in relation to the over-the counter promotes which don't require any additional

trade (again as done on the over-the-counter grandstand) and the certifiable cost is

fundamentally credited to margin upkeep. (Y, 2016) This is fundamental for those

associations that don't have the significant ability to pass on the costs of thing worth change

and supports on to the customer – due to contention in addition, other market loads. (Cooper,

2017) (Henderson & Hobson, 2010)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

This report will talk about the- risk involve in the commodity market especially copper in the

present case. How to handle the fluctuations in the price of copper. How to hedge, what to

hedge. Below is the introduction to commodity risk management.

Item worth risk is the money related danger on a component's cash related execution/ profit

upon instabilities in the expenses of things that are out of the control of the substance since

they are basically dictated by external market powers. Sharp fluctuations in commodity

expenses are making tremendous business challenges that can impact creation costs, thing

esteeming, benefit and credit availability. This worth precariousness makes it fundamental for

a substance to manage the impact of item worth changes over its value chain to effectively

manage its cash related execution and profitability. The fundamental establishments of item

chance organization come back to the out of date events. Business trades in the early

grandstands routinely incorporated an arrangement understanding between two parties that

were now and again composed as a forward contract with various features/choices on the

comprehension.

The understanding could vary from openly sorted out between two social occasions to a

formal and approved understanding based on developed rules and even law. Certain terms

and conditions of such understandings are there in the future contract. A comprehension for a

future arrangement would usually have a course of action that would permit the purchaser to

decay transport if the passed-on items were seen to be of lacking quality exactly when

appeared differently in relation to the principal model. (Hanisch, 2019)As reflected in notarial

contradictions expanding back to old-fashioned events, logical inconsistency over what

included adequate transport was a commonplace occasion. (Elfarhani, Mkaddem, Rubaiee,

Jarraya & Haddar, 2019) Both these upgrades are by and large related with the extending

centralization of business development, from the outset at the colossal medieval market fairs

and, later, on the bourses and exchanges. (Chan, Jacobi & Zhu, 2019) Securitization of mass

commodity trades was supported by applying trading methods that had been being utilized

for a serious in length time in the exhibit for bills of exchange. (Fu, Tang & Chen, 2019)

This report will talk about the- risk involve in the commodity market especially copper in the

present case. How to handle the fluctuations in the price of copper. How to hedge, what to

hedge. Below is the introduction to commodity risk management.

Item worth risk is the money related danger on a component's cash related execution/ profit

upon instabilities in the expenses of things that are out of the control of the substance since

they are basically dictated by external market powers. Sharp fluctuations in commodity

expenses are making tremendous business challenges that can impact creation costs, thing

esteeming, benefit and credit availability. This worth precariousness makes it fundamental for

a substance to manage the impact of item worth changes over its value chain to effectively

manage its cash related execution and profitability. The fundamental establishments of item

chance organization come back to the out of date events. Business trades in the early

grandstands routinely incorporated an arrangement understanding between two parties that

were now and again composed as a forward contract with various features/choices on the

comprehension.

The understanding could vary from openly sorted out between two social occasions to a

formal and approved understanding based on developed rules and even law. Certain terms

and conditions of such understandings are there in the future contract. A comprehension for a

future arrangement would usually have a course of action that would permit the purchaser to

decay transport if the passed-on items were seen to be of lacking quality exactly when

appeared differently in relation to the principal model. (Hanisch, 2019)As reflected in notarial

contradictions expanding back to old-fashioned events, logical inconsistency over what

included adequate transport was a commonplace occasion. (Elfarhani, Mkaddem, Rubaiee,

Jarraya & Haddar, 2019) Both these upgrades are by and large related with the extending

centralization of business development, from the outset at the colossal medieval market fairs

and, later, on the bourses and exchanges. (Chan, Jacobi & Zhu, 2019) Securitization of mass

commodity trades was supported by applying trading methods that had been being utilized

for a serious in length time in the exhibit for bills of exchange. (Fu, Tang & Chen, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Issues

Issue 1: In the present case Elite copper is facing issues related to the prices of the copper

which is fluctuating. There annual production is about 12 kilo tonnes. As the price is Volatile,

we will be using future contact to hedge the risk.

Response 1: The merchant of the futures contract (the gathering with a short position)

consents to offer the hidden item to the purchaser at termination at the fixed deals cost. Over

the long haul, the agreement's value changes with respect to the fixed cost at which the

exchange was started. This makes benefits or misfortunes for the broker. (Oktavia, Siregar,

Wardhani & Rahayu, 2019)

The company should sell futures, if the company is sure that the prices of the copper will fall

in future. As by selling the future, the company will save itself from the risk of the FUTUREs

index being falling. (Hung, 2019) (Panda, Nanda & Paital, 2019)

Issue 2: This question asks us about the optimal hedge ratio. A hedge ratio is the proportion

of introduction to a supporting instrument to the estimation of the supported resource. A

proportion of 1 or 100% implies that the position is completely supported and a proportion of

0 methods it isn't supported in any way. Hedge ratio is a significant measurement in hazard

the executives since it discloses to us the degree to which the danger of any unfriendly

development in our advantage or risk will be met by any counterbalancing development in

the supporting instrument. The fence proportion changes because of changes in estimation of

the supporting instrument as well as the supported resource or risk.

Response 2: As the change in the market price of copper is very volatile, we should fully

hedge the risk in order to avoid the variations in prices of copper. So, the optimal hedge ratio

should be 100%.

An optimal hedge ratio (likewise called least difference support proportion) is a ratio that tells

utilize the level of our benefit or risk presentation that we should support. (Ramachandran,

Lengnick-Hall & Badrinarayanan, 2019).It rises to the result of the relationship between the

costs of the supporting instrument and the supported instrument and the instability of the

supported instrument isolated by the unpredictability of the supporting instrument. An ideal

Issue 1: In the present case Elite copper is facing issues related to the prices of the copper

which is fluctuating. There annual production is about 12 kilo tonnes. As the price is Volatile,

we will be using future contact to hedge the risk.

Response 1: The merchant of the futures contract (the gathering with a short position)

consents to offer the hidden item to the purchaser at termination at the fixed deals cost. Over

the long haul, the agreement's value changes with respect to the fixed cost at which the

exchange was started. This makes benefits or misfortunes for the broker. (Oktavia, Siregar,

Wardhani & Rahayu, 2019)

The company should sell futures, if the company is sure that the prices of the copper will fall

in future. As by selling the future, the company will save itself from the risk of the FUTUREs

index being falling. (Hung, 2019) (Panda, Nanda & Paital, 2019)

Issue 2: This question asks us about the optimal hedge ratio. A hedge ratio is the proportion

of introduction to a supporting instrument to the estimation of the supported resource. A

proportion of 1 or 100% implies that the position is completely supported and a proportion of

0 methods it isn't supported in any way. Hedge ratio is a significant measurement in hazard

the executives since it discloses to us the degree to which the danger of any unfriendly

development in our advantage or risk will be met by any counterbalancing development in

the supporting instrument. The fence proportion changes because of changes in estimation of

the supporting instrument as well as the supported resource or risk.

Response 2: As the change in the market price of copper is very volatile, we should fully

hedge the risk in order to avoid the variations in prices of copper. So, the optimal hedge ratio

should be 100%.

An optimal hedge ratio (likewise called least difference support proportion) is a ratio that tells

utilize the level of our benefit or risk presentation that we should support. (Ramachandran,

Lengnick-Hall & Badrinarayanan, 2019).It rises to the result of the relationship between the

costs of the supporting instrument and the supported instrument and the instability of the

supported instrument isolated by the unpredictability of the supporting instrument. An ideal

fence proportion is most important where the qualities of the supported instrument and the

supporting instrument are diverse for example in a cross support. (Park, Chung & Kwon,

2018) (Ramlall, 2018)

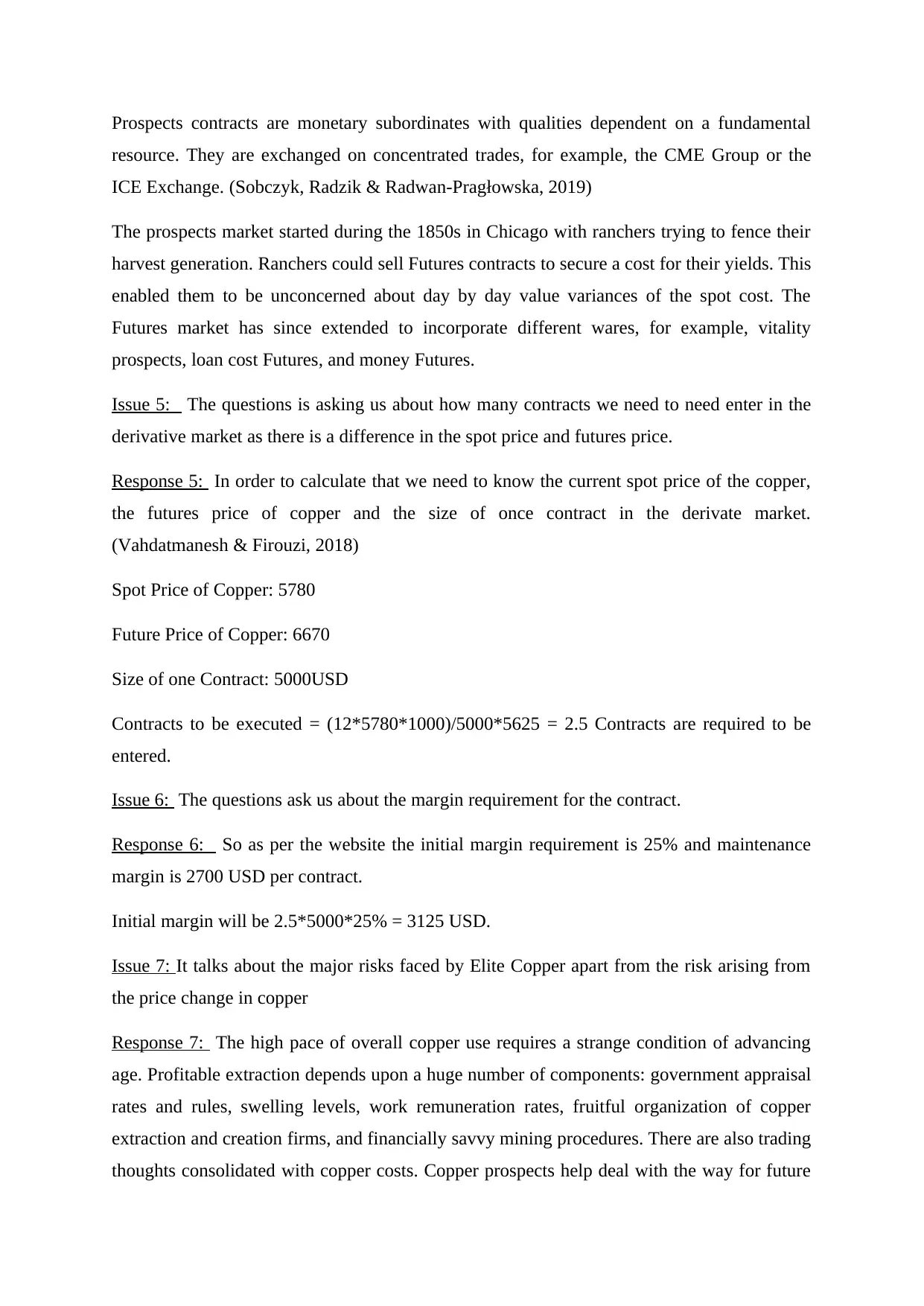

Issue 3: It is asking us to draw a chart for 5 year between the spot price and future price of

copper. As both the price are different. We got the know the difference between the two.

Response 3: As you see in 2013, spot price is around $4000 and the future price is around

$4500. The futures prices are different from the spot prices. As convenience yield is

involved, interest is also involved and dividend is also involved while calculating the prices.

As you see in 2017, the spot price has taken a significant jump, as due to time value of

money, future price in 2017 is a little higher because cost of interest savings is also added in

futures price as you have to keep only margin amount to trade in them.

As you see the graph. This price is changing for a commodity. As convenience yield is

involved, interest is also involved and dividend is also involved while calculating the prices.

The principle contrasts between the spot and futures price are the cost and date of delivery. A

commodity spot price is the cost at which the commodity could be exchanged at some

random time in the commercial centre. Interestingly, an item's Futures cost is the cost of the

spot in connection to its present spot value, time until conveyance, chance free loan fee and

capacity costs at a future date. The premise is the variety between the spot cost of a

deliverable item and the overall cost of the Futures contract for the equivalent real that has

the briefest span until development. Premise is a pivotal idea for portfolio chiefs and dealers

since this connection among money and prospects costs influences the estimation of the

agreements utilized in supporting. As there are holes among spot and relative cost until the

expiry of the closest contract, the premise isn't really precise. Notwithstanding the deviations

made in light of the time hole between the expiry of the prospects contract and the spot, item

quality, area of conveyance and the actuals may likewise change. By and large, the premise is

utilized by speculators to check the benefit of conveyance of money or the real and is

likewise used to look for exchange openings. (Rendtorff, 2019) (Sobczyk, Radzik & Radwan-

Pragłowska, 2019)

supporting instrument are diverse for example in a cross support. (Park, Chung & Kwon,

2018) (Ramlall, 2018)

Issue 3: It is asking us to draw a chart for 5 year between the spot price and future price of

copper. As both the price are different. We got the know the difference between the two.

Response 3: As you see in 2013, spot price is around $4000 and the future price is around

$4500. The futures prices are different from the spot prices. As convenience yield is

involved, interest is also involved and dividend is also involved while calculating the prices.

As you see in 2017, the spot price has taken a significant jump, as due to time value of

money, future price in 2017 is a little higher because cost of interest savings is also added in

futures price as you have to keep only margin amount to trade in them.

As you see the graph. This price is changing for a commodity. As convenience yield is

involved, interest is also involved and dividend is also involved while calculating the prices.

The principle contrasts between the spot and futures price are the cost and date of delivery. A

commodity spot price is the cost at which the commodity could be exchanged at some

random time in the commercial centre. Interestingly, an item's Futures cost is the cost of the

spot in connection to its present spot value, time until conveyance, chance free loan fee and

capacity costs at a future date. The premise is the variety between the spot cost of a

deliverable item and the overall cost of the Futures contract for the equivalent real that has

the briefest span until development. Premise is a pivotal idea for portfolio chiefs and dealers

since this connection among money and prospects costs influences the estimation of the

agreements utilized in supporting. As there are holes among spot and relative cost until the

expiry of the closest contract, the premise isn't really precise. Notwithstanding the deviations

made in light of the time hole between the expiry of the prospects contract and the spot, item

quality, area of conveyance and the actuals may likewise change. By and large, the premise is

utilized by speculators to check the benefit of conveyance of money or the real and is

likewise used to look for exchange openings. (Rendtorff, 2019) (Sobczyk, Radzik & Radwan-

Pragłowska, 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Issue 4:

It is asking us about the exposure of the copper. That simply means how much risk are we

carrying.

Reponses 4: As we are taking future contract for the full 12Killo Tone. Our exposure will be

accordingly according to the futures prices. Let say the futures price is 5825USD/MT. Then

our exposure will be 5825 * 12 = 69,900 USD.

As we are selling futures, as we have a fear that falling prices of future will generate us

income. So, we are totally hedged as, if the prices rise than we will be able to generate the

profit by selling the copper and compensate the loss by the extra profit that we are going to

earn.

There are two fundamental members in the prospect’s markets: hedgers are trying to deal

with their value hazard for items, and examiners need to benefit off of value variances for

commoditys. Examiners give a lot of liquidity to the prospect’s markets. Futures contracts

enable theorists to go out on a limb with less capital because of the high level of influence

included.

2012 2013 2014 2015 2016 2017

0

1000

2000

3000

4000

5000

6000

7000

Spot and Futures Price

Spot

Futures

Price in $

It is asking us about the exposure of the copper. That simply means how much risk are we

carrying.

Reponses 4: As we are taking future contract for the full 12Killo Tone. Our exposure will be

accordingly according to the futures prices. Let say the futures price is 5825USD/MT. Then

our exposure will be 5825 * 12 = 69,900 USD.

As we are selling futures, as we have a fear that falling prices of future will generate us

income. So, we are totally hedged as, if the prices rise than we will be able to generate the

profit by selling the copper and compensate the loss by the extra profit that we are going to

earn.

There are two fundamental members in the prospect’s markets: hedgers are trying to deal

with their value hazard for items, and examiners need to benefit off of value variances for

commoditys. Examiners give a lot of liquidity to the prospect’s markets. Futures contracts

enable theorists to go out on a limb with less capital because of the high level of influence

included.

2012 2013 2014 2015 2016 2017

0

1000

2000

3000

4000

5000

6000

7000

Spot and Futures Price

Spot

Futures

Price in $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prospects contracts are monetary subordinates with qualities dependent on a fundamental

resource. They are exchanged on concentrated trades, for example, the CME Group or the

ICE Exchange. (Sobczyk, Radzik & Radwan-Pragłowska, 2019)

The prospects market started during the 1850s in Chicago with ranchers trying to fence their

harvest generation. Ranchers could sell Futures contracts to secure a cost for their yields. This

enabled them to be unconcerned about day by day value variances of the spot cost. The

Futures market has since extended to incorporate different wares, for example, vitality

prospects, loan cost Futures, and money Futures.

Issue 5: The questions is asking us about how many contracts we need to need enter in the

derivative market as there is a difference in the spot price and futures price.

Response 5: In order to calculate that we need to know the current spot price of the copper,

the futures price of copper and the size of once contract in the derivate market.

(Vahdatmanesh & Firouzi, 2018)

Spot Price of Copper: 5780

Future Price of Copper: 6670

Size of one Contract: 5000USD

Contracts to be executed = (12*5780*1000)/5000*5625 = 2.5 Contracts are required to be

entered.

Issue 6: The questions ask us about the margin requirement for the contract.

Response 6: So as per the website the initial margin requirement is 25% and maintenance

margin is 2700 USD per contract.

Initial margin will be 2.5*5000*25% = 3125 USD.

Issue 7: It talks about the major risks faced by Elite Copper apart from the risk arising from

the price change in copper

Response 7: The high pace of overall copper use requires a strange condition of advancing

age. Profitable extraction depends upon a huge number of components: government appraisal

rates and rules, swelling levels, work remuneration rates, fruitful organization of copper

extraction and creation firms, and financially savvy mining procedures. There are also trading

thoughts consolidated with copper costs. Copper prospects help deal with the way for future

resource. They are exchanged on concentrated trades, for example, the CME Group or the

ICE Exchange. (Sobczyk, Radzik & Radwan-Pragłowska, 2019)

The prospects market started during the 1850s in Chicago with ranchers trying to fence their

harvest generation. Ranchers could sell Futures contracts to secure a cost for their yields. This

enabled them to be unconcerned about day by day value variances of the spot cost. The

Futures market has since extended to incorporate different wares, for example, vitality

prospects, loan cost Futures, and money Futures.

Issue 5: The questions is asking us about how many contracts we need to need enter in the

derivative market as there is a difference in the spot price and futures price.

Response 5: In order to calculate that we need to know the current spot price of the copper,

the futures price of copper and the size of once contract in the derivate market.

(Vahdatmanesh & Firouzi, 2018)

Spot Price of Copper: 5780

Future Price of Copper: 6670

Size of one Contract: 5000USD

Contracts to be executed = (12*5780*1000)/5000*5625 = 2.5 Contracts are required to be

entered.

Issue 6: The questions ask us about the margin requirement for the contract.

Response 6: So as per the website the initial margin requirement is 25% and maintenance

margin is 2700 USD per contract.

Initial margin will be 2.5*5000*25% = 3125 USD.

Issue 7: It talks about the major risks faced by Elite Copper apart from the risk arising from

the price change in copper

Response 7: The high pace of overall copper use requires a strange condition of advancing

age. Profitable extraction depends upon a huge number of components: government appraisal

rates and rules, swelling levels, work remuneration rates, fruitful organization of copper

extraction and creation firms, and financially savvy mining procedures. There are also trading

thoughts consolidated with copper costs. Copper prospects help deal with the way for future

endeavours, adventure progression and the number of firms in the copper business. The

development of adaptable speculations with a thing focus can truly construct transient

precariousness at copper costs through colossal purchases or arrangements. (Yadav, Pandey,

Shukla & Kumar, 2019)

It is hard to see most of the variables that effect the expense of any all around traded item.

Notwithstanding whether that were possible, it would be impressively progressively difficult

to measure these components appropriately. Henceforth, copper scholars have an effect in

driving business division costs reliant on the best suppositions of the present business

visionaries. Copper has its own ticker picture in the things promote (EHG). Like most

mechanical or provincial items, dealers should think about a colossal number of

macroeconomic components that effect copper esteem improvements, which consolidate the

expense of elective base metals, for instance, aluminium, nickel, lead and iron. Rising copper

costs during the focal point of the 2000s at last provoked pushed livelihoods of aluminium as

a substitute in power joins, electrical apparatus and refrigeration tubes. Systematic elements,

for instance, the atmosphere or time, can impact copper age, solicitation or transportation. A

huge section of the overall copper supply begins in South America, particularly in Peru and

Chile. Worker strikes against copper-conveying mines are not amazing in these regions, and

any worry over geopolitical insecurity can power costs upwards. On the contrary side of the

condition are the U.S. additionally, China, two nations that are incredibly huge buyers of

copper. The prosperity of the world's two greatest economies influences pretty much

everything.

Issue 8: It talks about the strategies we have given by hedging through Futures way.

Response 8:

Upsides: As you sell a future contract, you have kept yourself safe to the potential down side

if any as you will earn if the prices of the stock go down. Margin requirements for the

majority of the items and monetary forms are entrenched in the futures market. Accordingly,

a merchant knows how much margin he should set up in an agreement. A speculator needs to

place in a margin—a small amount of the aggregate sum (regularly 10% of the agreement

esteem)— to be put resources into prospects.

Downsides: As you sell the future contract, your profit will remain the same. There will be

no impact on your profit as you did a total hedge. Even if the price goes up you have to pay to

th e future buyer.The margin is a security that the speculator needs to keep with the trade on

development of adaptable speculations with a thing focus can truly construct transient

precariousness at copper costs through colossal purchases or arrangements. (Yadav, Pandey,

Shukla & Kumar, 2019)

It is hard to see most of the variables that effect the expense of any all around traded item.

Notwithstanding whether that were possible, it would be impressively progressively difficult

to measure these components appropriately. Henceforth, copper scholars have an effect in

driving business division costs reliant on the best suppositions of the present business

visionaries. Copper has its own ticker picture in the things promote (EHG). Like most

mechanical or provincial items, dealers should think about a colossal number of

macroeconomic components that effect copper esteem improvements, which consolidate the

expense of elective base metals, for instance, aluminium, nickel, lead and iron. Rising copper

costs during the focal point of the 2000s at last provoked pushed livelihoods of aluminium as

a substitute in power joins, electrical apparatus and refrigeration tubes. Systematic elements,

for instance, the atmosphere or time, can impact copper age, solicitation or transportation. A

huge section of the overall copper supply begins in South America, particularly in Peru and

Chile. Worker strikes against copper-conveying mines are not amazing in these regions, and

any worry over geopolitical insecurity can power costs upwards. On the contrary side of the

condition are the U.S. additionally, China, two nations that are incredibly huge buyers of

copper. The prosperity of the world's two greatest economies influences pretty much

everything.

Issue 8: It talks about the strategies we have given by hedging through Futures way.

Response 8:

Upsides: As you sell a future contract, you have kept yourself safe to the potential down side

if any as you will earn if the prices of the stock go down. Margin requirements for the

majority of the items and monetary forms are entrenched in the futures market. Accordingly,

a merchant knows how much margin he should set up in an agreement. A speculator needs to

place in a margin—a small amount of the aggregate sum (regularly 10% of the agreement

esteem)— to be put resources into prospects.

Downsides: As you sell the future contract, your profit will remain the same. There will be

no impact on your profit as you did a total hedge. Even if the price goes up you have to pay to

th e future buyer.The margin is a security that the speculator needs to keep with the trade on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the off chance that the market moves inverse to the position he has taken and he brings about

loses. This might be more than the margin sum; in which case the financial specialist needs to

pay more to carry the margin to a support level. What exchanging Futures basically implies

for the speculator is that he can open himself to a lot more noteworthy estimation of stocks

than he could when purchasing the first socks. What's more, in this way his benefits likewise

increase if the market moves toward him (multiple times if margin prerequisite is 10%).

Issue 9: It talks about the historical development of the commodity futures (especially those

related to copper) in the past few decades

Response 9: For as long as year, copper exchanged like a teeter-totter on the on-once more,

off-again any expectations of a U.S. what's more, China exchange accord. Presently it's

progressively similar to a rollercoaster ride down. The emphasis is progressively on the harm

brought about by the destruction of an exchange question between the world's two greatest

economies. The expansive applications for copper mean it's especially powerless against the

synchronized spiral being seen in everything from vehicle making and earth-moving

hardware to business property and progressed electronic segments. What the hard information

is letting us know is that end-use request is moderate and in numerous spots getting kicked

very hard, Oliver Nugent, a metals strategist at Citigroup Inc., said by telephone from

London. China's commodity concentrated economy is as powerless as it's been in late history.

On Friday, copper got through an exchanging range that is kept going since July 2018, hitting

another two-year low. With zinc and aluminium likewise diving, here are six graphs

demonstrating the base metals markets' expanding request emergency.

Issue 10: It talks about how to commodity future market will look like in next 5 years.

Response 10: The future may has cut its year conjecture at copper costs to $4,800 per ton

fully expecting mining cost emptying, higher yield and a stoppage in Chinese interest

development(BuHamdan, Alwisy, Bouferguene & Al-Hussein, 2019)The re-examined

conjectures, which are $400 underneath its past evaluations, restore it as the most bearish

standard venture bank covering the copper showcase, outperforming Bank of America, which

is determining a normal copper cost of $4,969 for 2016. (Davcik & Grigoriou, 2019) I am

being bearish on the copper advertise for as far back as more than two years; however, it is

currently gauging costs 20% beneath spot levels and 30% underneath accord gauges.

(Akcura, Sinapuelas & Wang, 2019)

loses. This might be more than the margin sum; in which case the financial specialist needs to

pay more to carry the margin to a support level. What exchanging Futures basically implies

for the speculator is that he can open himself to a lot more noteworthy estimation of stocks

than he could when purchasing the first socks. What's more, in this way his benefits likewise

increase if the market moves toward him (multiple times if margin prerequisite is 10%).

Issue 9: It talks about the historical development of the commodity futures (especially those

related to copper) in the past few decades

Response 9: For as long as year, copper exchanged like a teeter-totter on the on-once more,

off-again any expectations of a U.S. what's more, China exchange accord. Presently it's

progressively similar to a rollercoaster ride down. The emphasis is progressively on the harm

brought about by the destruction of an exchange question between the world's two greatest

economies. The expansive applications for copper mean it's especially powerless against the

synchronized spiral being seen in everything from vehicle making and earth-moving

hardware to business property and progressed electronic segments. What the hard information

is letting us know is that end-use request is moderate and in numerous spots getting kicked

very hard, Oliver Nugent, a metals strategist at Citigroup Inc., said by telephone from

London. China's commodity concentrated economy is as powerless as it's been in late history.

On Friday, copper got through an exchanging range that is kept going since July 2018, hitting

another two-year low. With zinc and aluminium likewise diving, here are six graphs

demonstrating the base metals markets' expanding request emergency.

Issue 10: It talks about how to commodity future market will look like in next 5 years.

Response 10: The future may has cut its year conjecture at copper costs to $4,800 per ton

fully expecting mining cost emptying, higher yield and a stoppage in Chinese interest

development(BuHamdan, Alwisy, Bouferguene & Al-Hussein, 2019)The re-examined

conjectures, which are $400 underneath its past evaluations, restore it as the most bearish

standard venture bank covering the copper showcase, outperforming Bank of America, which

is determining a normal copper cost of $4,969 for 2016. (Davcik & Grigoriou, 2019) I am

being bearish on the copper advertise for as far back as more than two years; however, it is

currently gauging costs 20% beneath spot levels and 30% underneath accord gauges.

(Akcura, Sinapuelas & Wang, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusions

Item worth risk normally is the defencelessness looked by corporates to source or sell a thing

at an expense. The nature and sort of item cost danger changes from industry to industry.

Every association getting a certain thing will defy the trial of ground-breaking esteem the

officials. Depending on the item, it will in general be treated as an "acquisition commodity

danger" or "tradable commodity possibility". Verifying danger is progressively connected

with towards the physical store system side of the business however tradable peril is on the

cash related risk and

supporting of the business. Inside the thing worth chain, corporates are looked with changed

sorts of item threats including 'stock worth shot' with the risk of falling expenses, 'reason

danger' which is the differentiation in benchmark cost of the physical item and the auxiliary

instrument used to help the thing cost, and hedge shot which for a creator is on the risk of

falling expenses, and buyers on increasing expenses. Corporates revealed on the acquisition

side of the value chain from the outset overview the feasibility of lessening the impact of

rising commodity costs by passing it on to the customer on the wrapped-up items. Then

again, such corporates similarly will all in all counsel with their suppliers towards a fixed

worth comprehension which transforms into an inconvenient trouble where the esteem

disclosure and benchmark costs of that thing are clear and viably open to all market

individuals. Basically, corporates revealed on the arrangements side of the value chain

structure assessing limits or through wandered cost bunches inside the arrangement which act

as an introduced backup. Then again, most corporates look towards supporting their

arrangements should the thing benchmark cost be available to help through a subordinate

instrument. (Malenbaum, 2019) Corporates on the overall scale have progressed and today

utilize the liquid benchmarks to trade on the exchange additionally, bolster the commodity

worth danger using backup things. Exchange traded backups has its ideal conditions of clear

assessing, organized contracts and no default risk. To a gigantic degree business keep on look

into the over-the-counter ('OTC') auxiliaries promotes similarly as in the commodity

exchanges. (Song & Liao, 2019)The OTC markets outfit such corporates with the limit to

alter the understanding that best fits with the presentation profile of the Company - which

isn't open in the exchange publicize due to trustee need of the organization of understandings.

Another safeguard for looking into the OTC market when in doubt stems where the

benchmark costs open in the exchanges are not acclimated to the expense disclosure approach

for verifying or selling the item by the corporate. (Ju, 2019)

Item worth risk normally is the defencelessness looked by corporates to source or sell a thing

at an expense. The nature and sort of item cost danger changes from industry to industry.

Every association getting a certain thing will defy the trial of ground-breaking esteem the

officials. Depending on the item, it will in general be treated as an "acquisition commodity

danger" or "tradable commodity possibility". Verifying danger is progressively connected

with towards the physical store system side of the business however tradable peril is on the

cash related risk and

supporting of the business. Inside the thing worth chain, corporates are looked with changed

sorts of item threats including 'stock worth shot' with the risk of falling expenses, 'reason

danger' which is the differentiation in benchmark cost of the physical item and the auxiliary

instrument used to help the thing cost, and hedge shot which for a creator is on the risk of

falling expenses, and buyers on increasing expenses. Corporates revealed on the acquisition

side of the value chain from the outset overview the feasibility of lessening the impact of

rising commodity costs by passing it on to the customer on the wrapped-up items. Then

again, such corporates similarly will all in all counsel with their suppliers towards a fixed

worth comprehension which transforms into an inconvenient trouble where the esteem

disclosure and benchmark costs of that thing are clear and viably open to all market

individuals. Basically, corporates revealed on the arrangements side of the value chain

structure assessing limits or through wandered cost bunches inside the arrangement which act

as an introduced backup. Then again, most corporates look towards supporting their

arrangements should the thing benchmark cost be available to help through a subordinate

instrument. (Malenbaum, 2019) Corporates on the overall scale have progressed and today

utilize the liquid benchmarks to trade on the exchange additionally, bolster the commodity

worth danger using backup things. Exchange traded backups has its ideal conditions of clear

assessing, organized contracts and no default risk. To a gigantic degree business keep on look

into the over-the-counter ('OTC') auxiliaries promotes similarly as in the commodity

exchanges. (Song & Liao, 2019)The OTC markets outfit such corporates with the limit to

alter the understanding that best fits with the presentation profile of the Company - which

isn't open in the exchange publicize due to trustee need of the organization of understandings.

Another safeguard for looking into the OTC market when in doubt stems where the

benchmark costs open in the exchanges are not acclimated to the expense disclosure approach

for verifying or selling the item by the corporate. (Ju, 2019)

References

Akcura, M., Sinapuelas, I., & Wang, H. (2019). Effects of multitier private labels on

marketing national brands. Journal Of Product & Brand Management, 28(3), 391-407. doi:

10.1108/jpbm-10-2017-1623

BuHamdan, S., Alwisy, A., Bouferguene, A., & Al-Hussein, M. (2019). The application of

multi-attribute utility theory for a market share-based design evaluation. International Journal

Of Housing Markets And Analysis. doi: 10.1108/ijhma-11-2018-0087

Chan, J., Jacobi, L., & Zhu, D. (2019). How Sensitive Are VAR Forecasts to Prior

Hyperparameters? An Automated Sensitivity Analysis. Advances In Econometrics, 229-248.

doi: 10.1108/s0731-90532019000040a010

Cooper, G. (2017). The interpretation of the generalised derivative operator. Geophysical

Prospecting, 66(1), 197-206. doi: 10.1111/1365-2478.12539

Davcik, N., & Grigoriou, N. (2019). How an unequal intra-firm resources distribution affect

market share. Marketing Intelligence & Planning. doi: 10.1108/mip-03-2019-0170

Elfarhani, M., Mkaddem, A., Rubaiee, S., Jarraya, A., & Haddar, M. (2019). Prediction of

foam impulse response through combination of hereditary and fractional derivative

approaches. Multidiscipline Modeling In Materials And Structures, 15(4), 800-817. doi:

10.1108/mmms-10-2018-0164

Fu, J., Tang, H., & Chen, H. (2019). Rapid computation of rotary derivatives for subsonic and

low transonic flows. Engineering Computations, ahead-of-print(ahead-of-print). doi:

10.1108/ec-09-2018-0399

Hanisch, A. (2019). Factors influencing the propensity of real estate investors in the UK to

employ property derivatives. Journal Of Property Investment & Finance, 37(2), 194-214. doi:

10.1108/jpif-01-2018-0005

Henderson, V., & Hobson, D. (2010). OPTIMAL LIQUIDATION OF DERIVATIVE

PORTFOLIOS. Mathematical Finance, 21(3), 365-382. doi: 10.1111/j.1467-

9965.2010.00455.x

Akcura, M., Sinapuelas, I., & Wang, H. (2019). Effects of multitier private labels on

marketing national brands. Journal Of Product & Brand Management, 28(3), 391-407. doi:

10.1108/jpbm-10-2017-1623

BuHamdan, S., Alwisy, A., Bouferguene, A., & Al-Hussein, M. (2019). The application of

multi-attribute utility theory for a market share-based design evaluation. International Journal

Of Housing Markets And Analysis. doi: 10.1108/ijhma-11-2018-0087

Chan, J., Jacobi, L., & Zhu, D. (2019). How Sensitive Are VAR Forecasts to Prior

Hyperparameters? An Automated Sensitivity Analysis. Advances In Econometrics, 229-248.

doi: 10.1108/s0731-90532019000040a010

Cooper, G. (2017). The interpretation of the generalised derivative operator. Geophysical

Prospecting, 66(1), 197-206. doi: 10.1111/1365-2478.12539

Davcik, N., & Grigoriou, N. (2019). How an unequal intra-firm resources distribution affect

market share. Marketing Intelligence & Planning. doi: 10.1108/mip-03-2019-0170

Elfarhani, M., Mkaddem, A., Rubaiee, S., Jarraya, A., & Haddar, M. (2019). Prediction of

foam impulse response through combination of hereditary and fractional derivative

approaches. Multidiscipline Modeling In Materials And Structures, 15(4), 800-817. doi:

10.1108/mmms-10-2018-0164

Fu, J., Tang, H., & Chen, H. (2019). Rapid computation of rotary derivatives for subsonic and

low transonic flows. Engineering Computations, ahead-of-print(ahead-of-print). doi:

10.1108/ec-09-2018-0399

Hanisch, A. (2019). Factors influencing the propensity of real estate investors in the UK to

employ property derivatives. Journal Of Property Investment & Finance, 37(2), 194-214. doi:

10.1108/jpif-01-2018-0005

Henderson, V., & Hobson, D. (2010). OPTIMAL LIQUIDATION OF DERIVATIVE

PORTFOLIOS. Mathematical Finance, 21(3), 365-382. doi: 10.1111/j.1467-

9965.2010.00455.x

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.