Comprehensive Report on Treasury and Risk Management Strategies

VerifiedAdded on 2023/06/04

|7

|1187

|294

Report

AI Summary

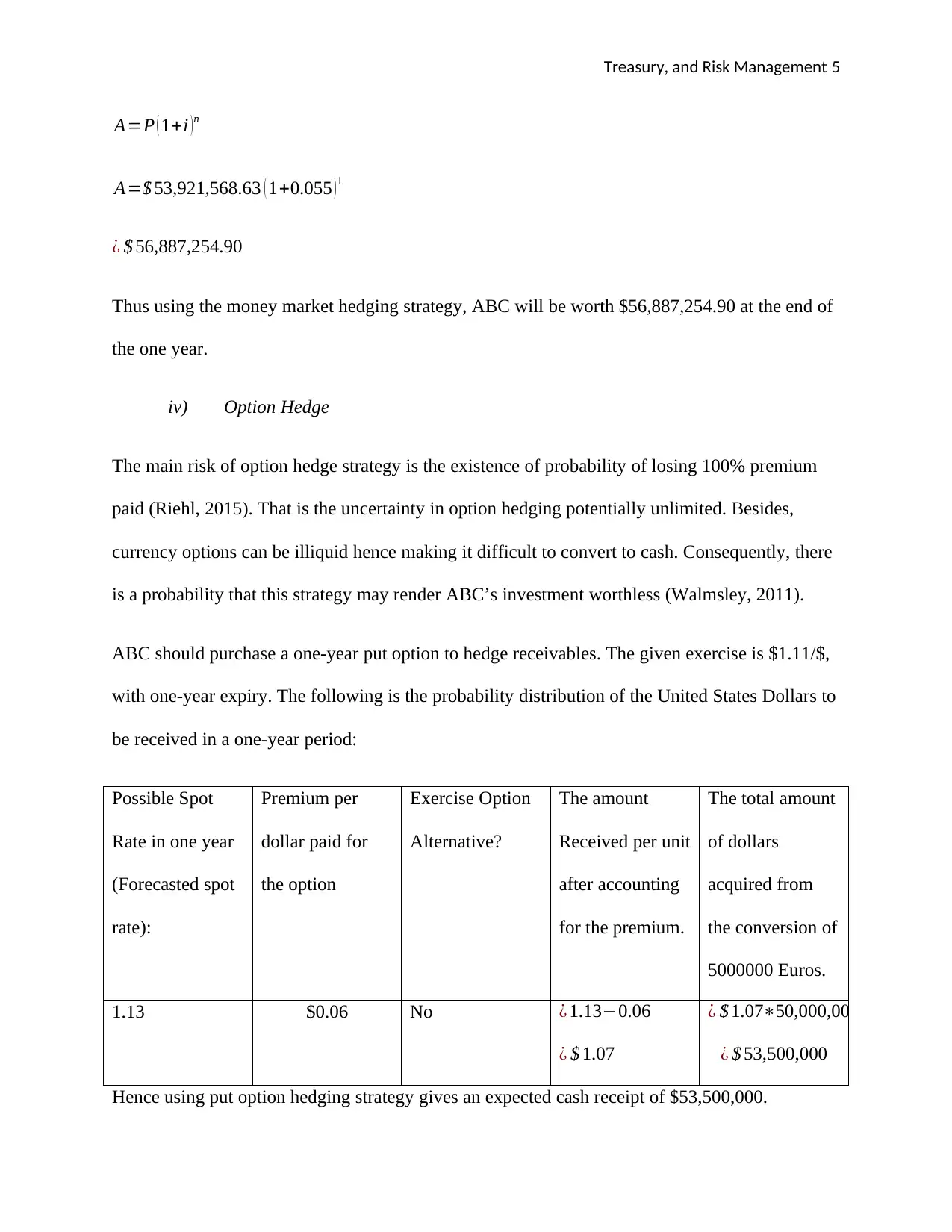

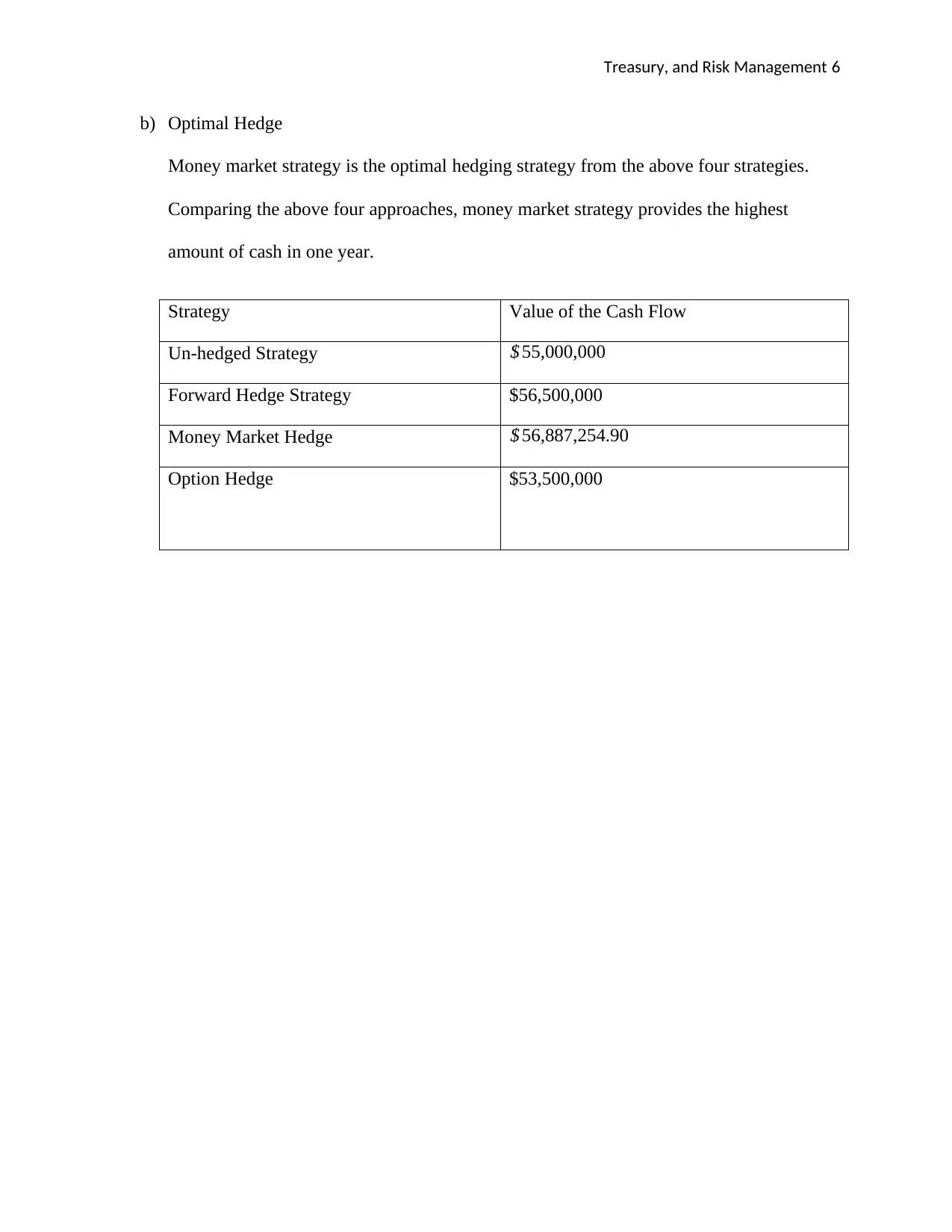

This report provides a comprehensive analysis of treasury and risk management strategies, focusing on a case study involving foreign exchange risk. It examines four primary hedging techniques: unhedged strategy, forward hedge strategy, money market hedge, and option hedge. The report calculates potential outcomes for each strategy, considering factors like interest rates and spot rates. It highlights the risks associated with each approach, such as transaction risk, counterparty risk, and the potential for loss. The analysis concludes by identifying the money market strategy as the optimal hedging approach based on the highest potential cash flow. The report references relevant literature to support its findings and provides a detailed comparison of the different strategies' effectiveness in mitigating financial risks.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.