University Finance Module: Risk Management Techniques Portfolio Report

VerifiedAdded on 2021/12/21

|11

|1363

|25

Report

AI Summary

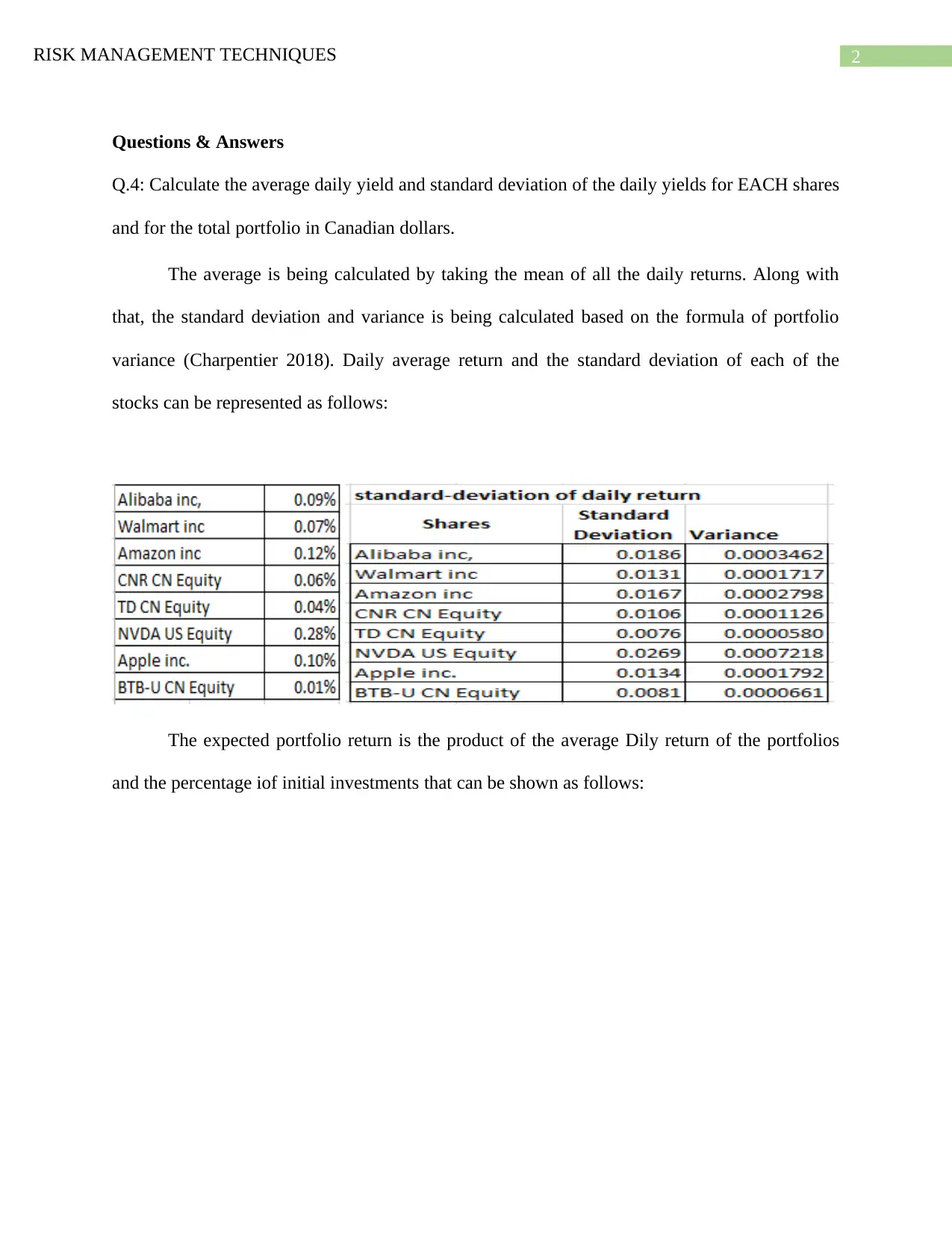

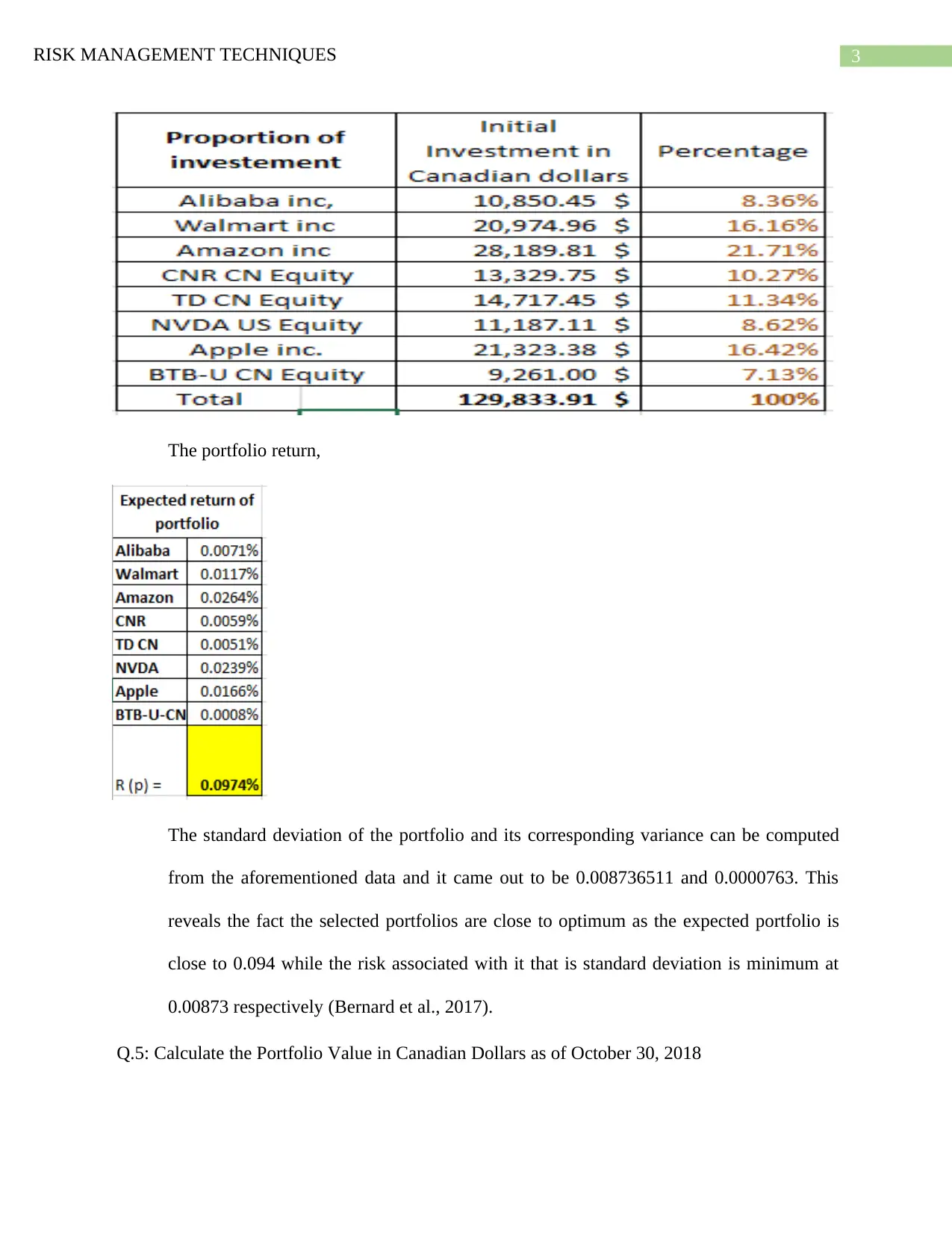

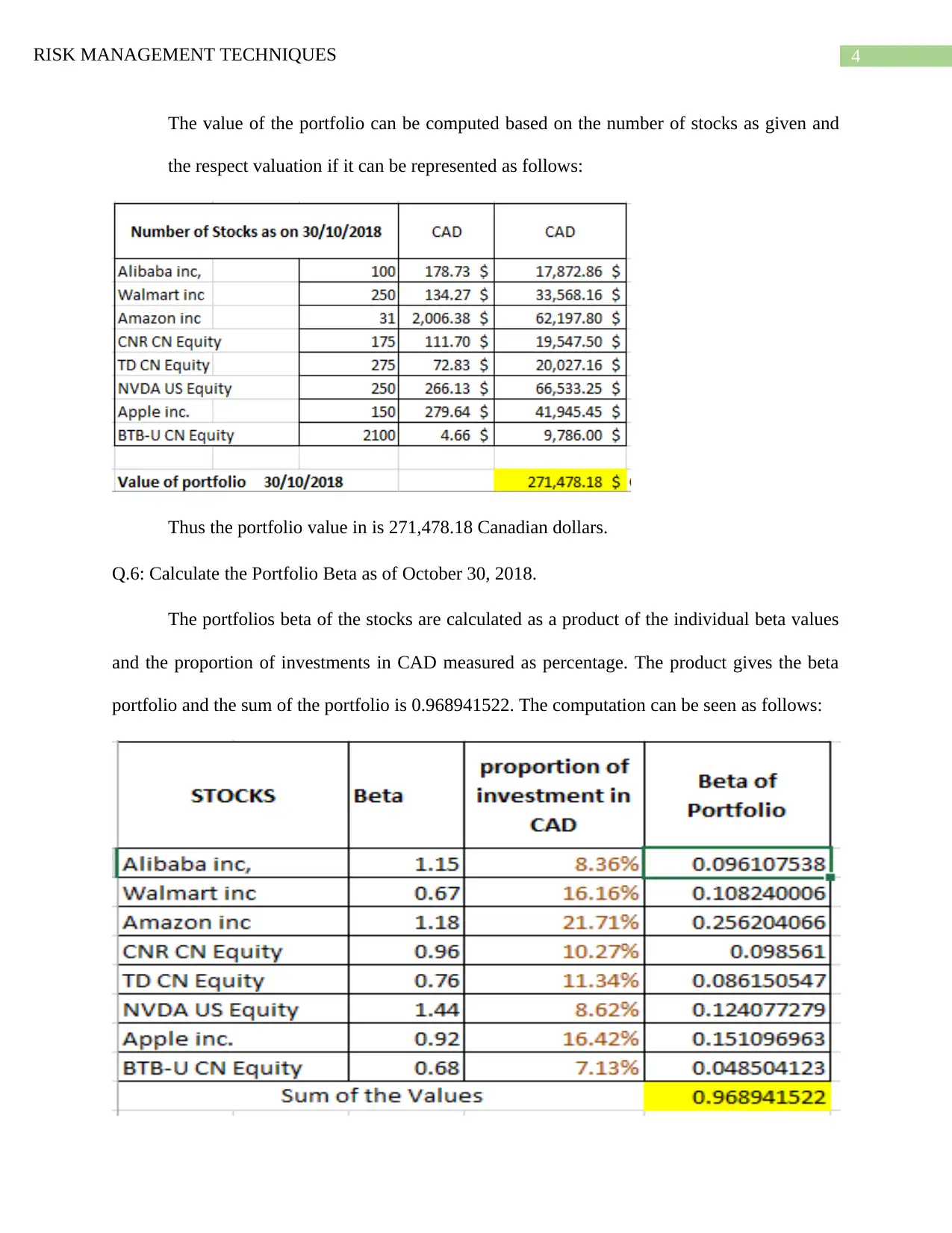

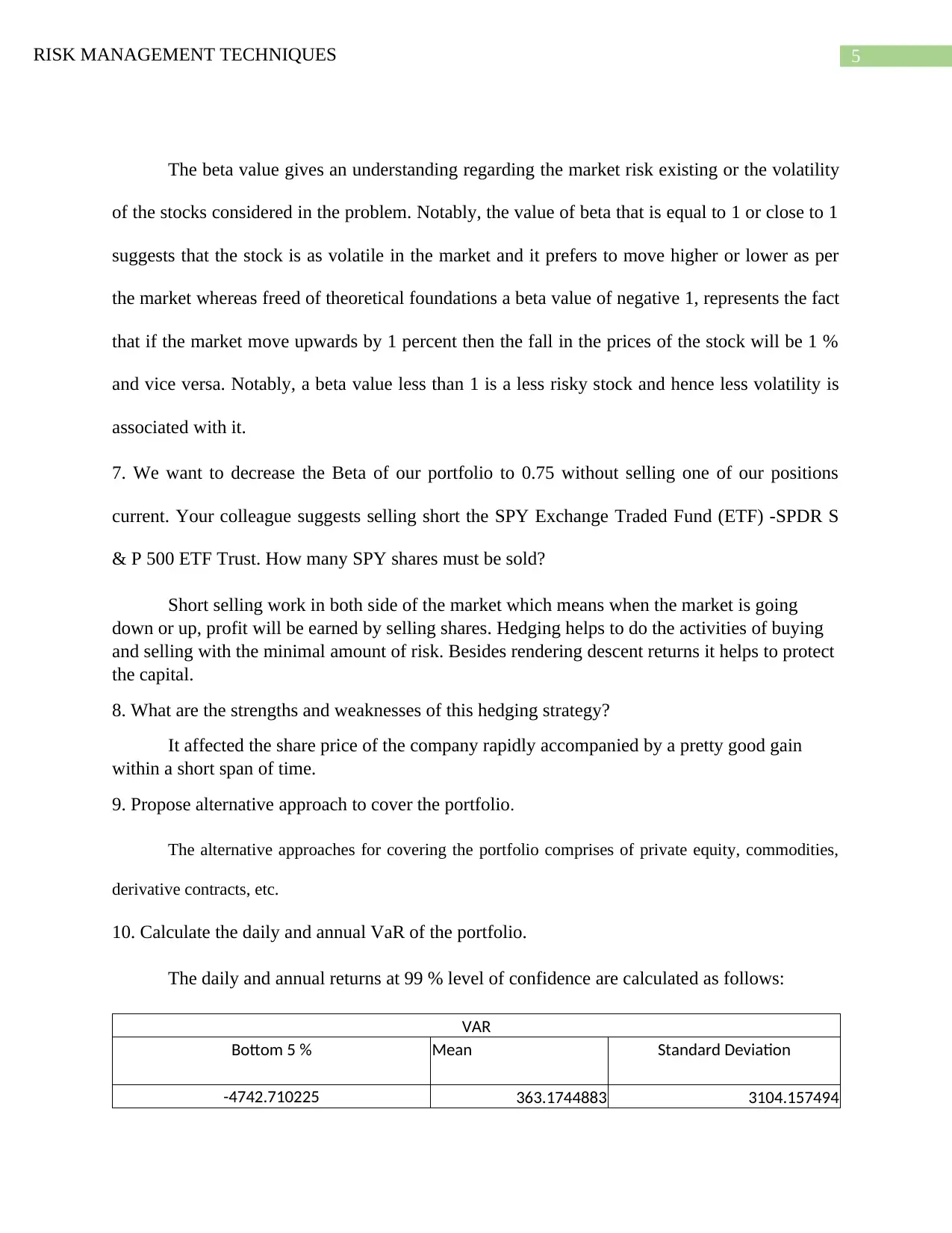

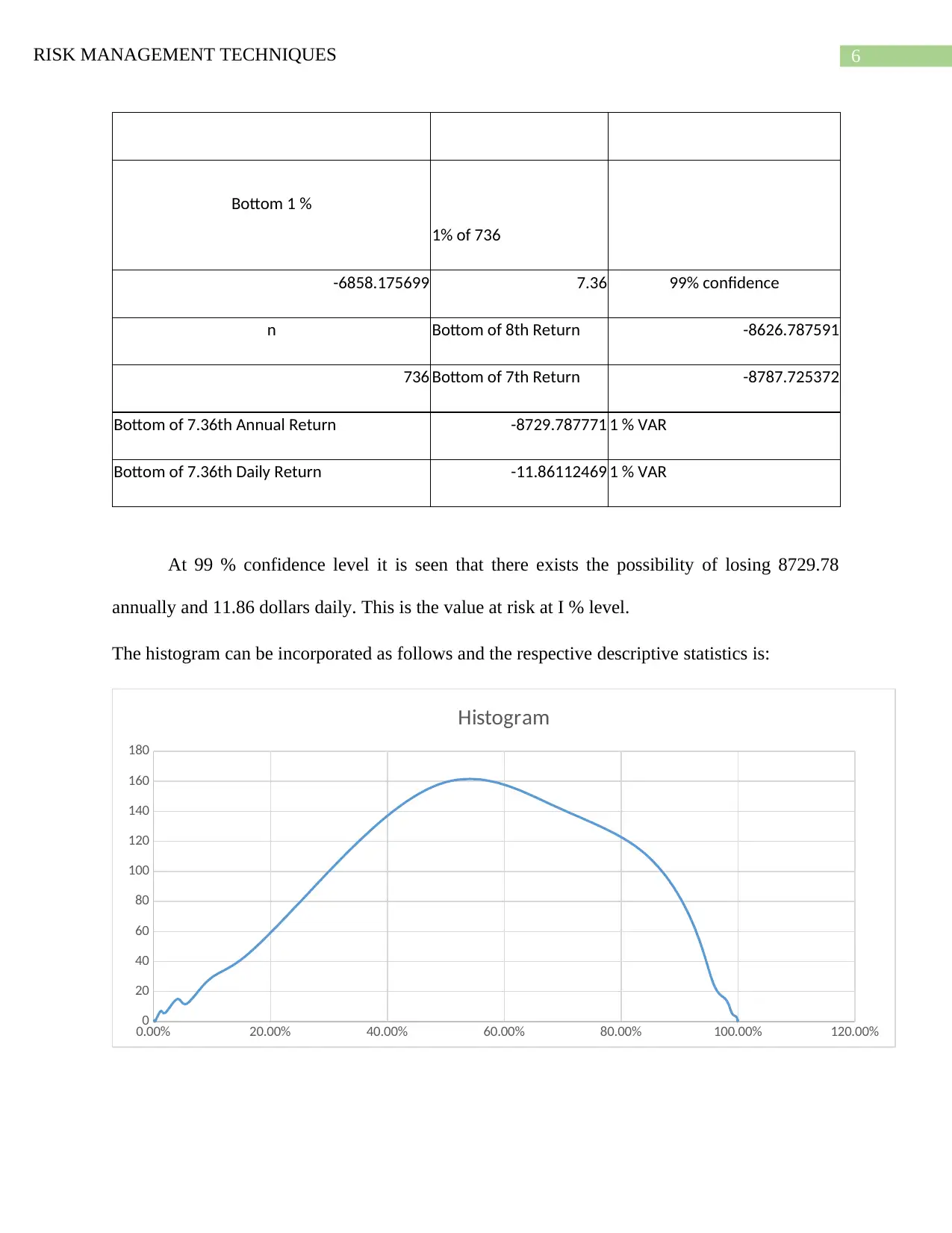

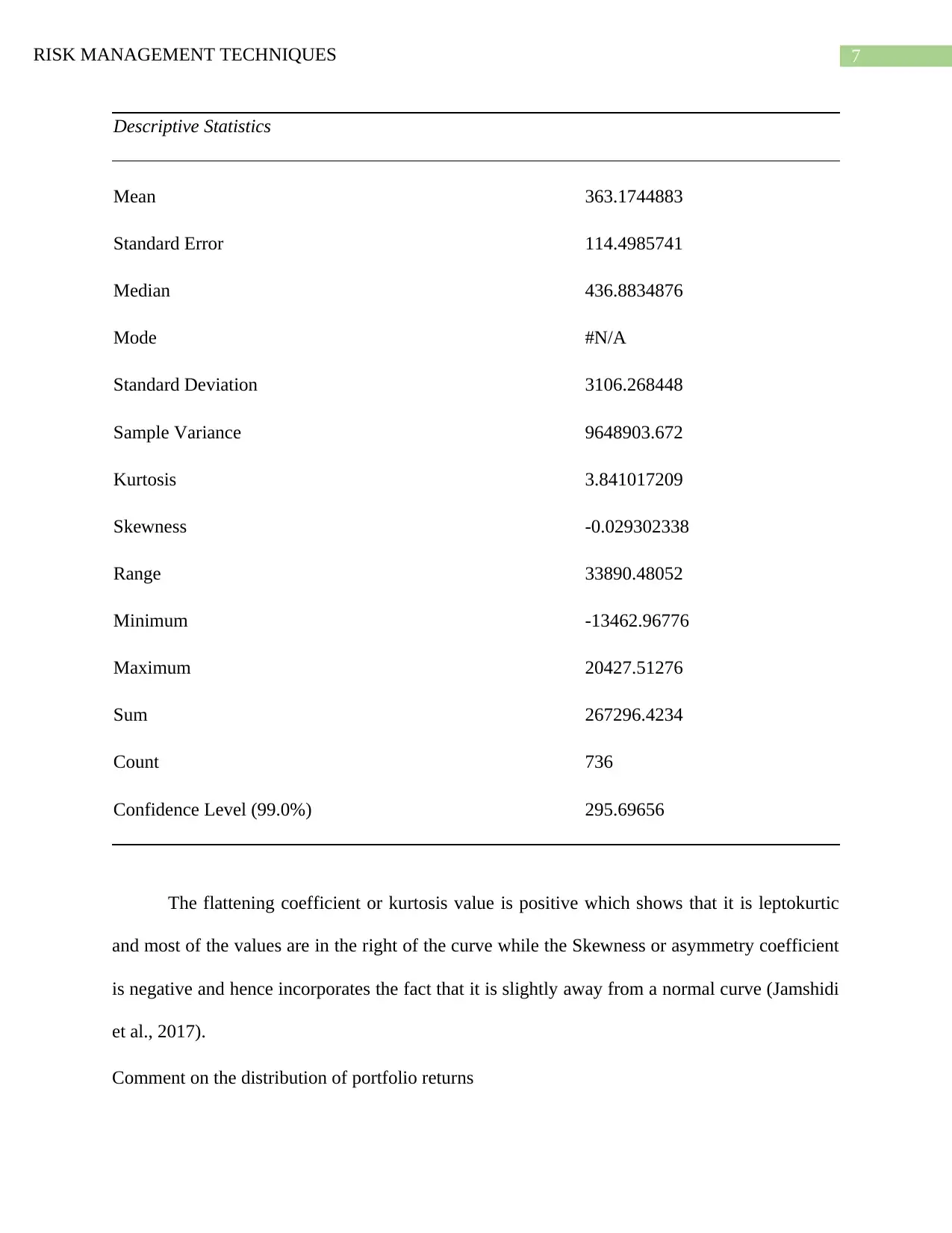

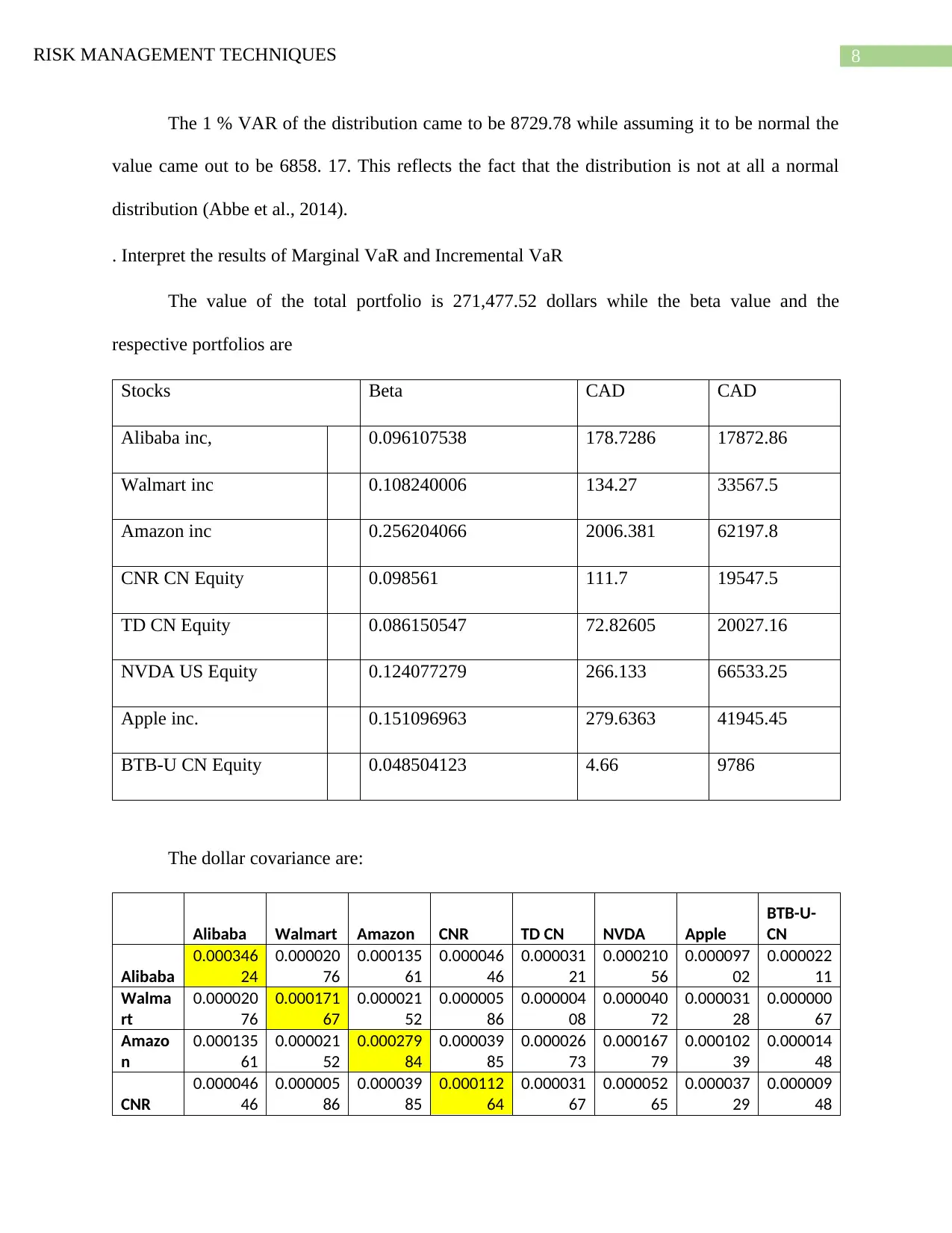

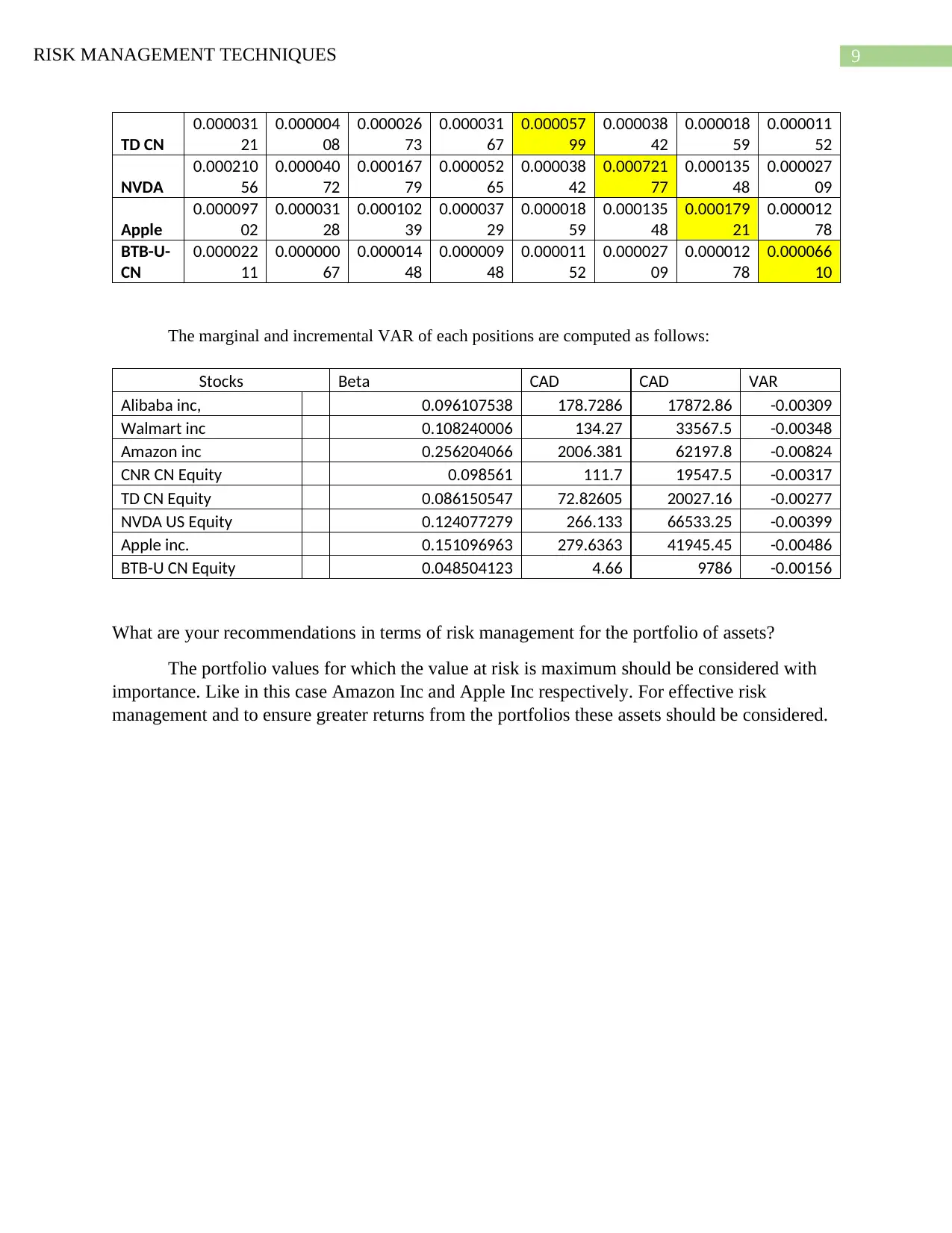

This report delves into financial risk management techniques, offering a comprehensive analysis of a given investment portfolio. It begins by calculating the average daily yield and standard deviation for each share and the total portfolio, providing insights into the expected portfolio return and associated risk. The report then determines the portfolio's value in Canadian dollars and calculates its beta, offering an understanding of market risk and volatility. Furthermore, it explores hedging strategies, proposing and evaluating the use of short selling SPY ETF shares to reduce portfolio beta. The report also suggests alternative approaches to cover the portfolio and calculates both daily and annual Value at Risk (VaR) at a 99% confidence level, offering a detailed interpretation of the results, including marginal and incremental VaR. Finally, the report provides recommendations for effective risk management, emphasizing the importance of considering assets with maximum value at risk for optimal portfolio management.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.