Finance Assignment: Risk and Return Analysis for ACC00716 Course

VerifiedAdded on 2022/08/26

|8

|1777

|17

Report

AI Summary

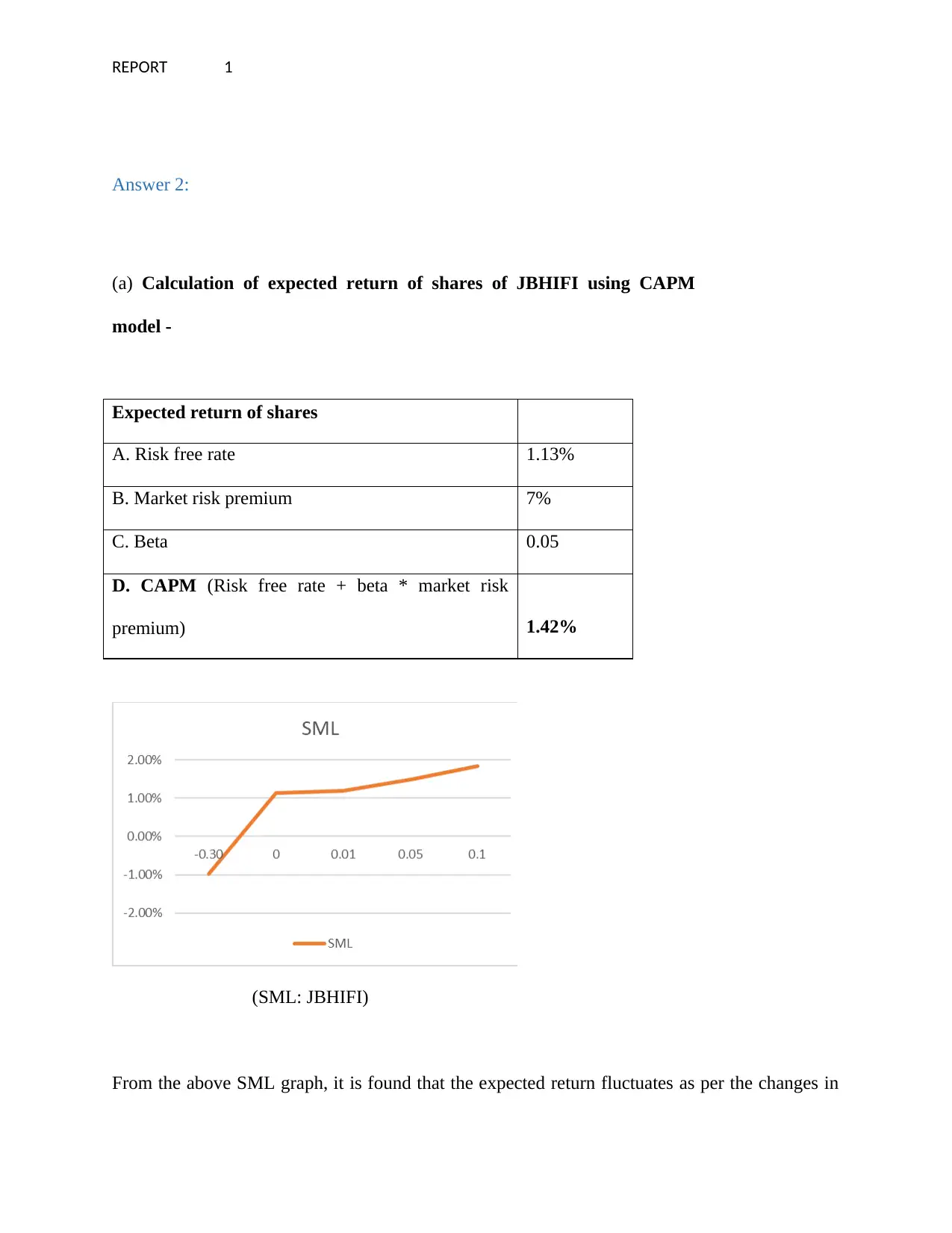

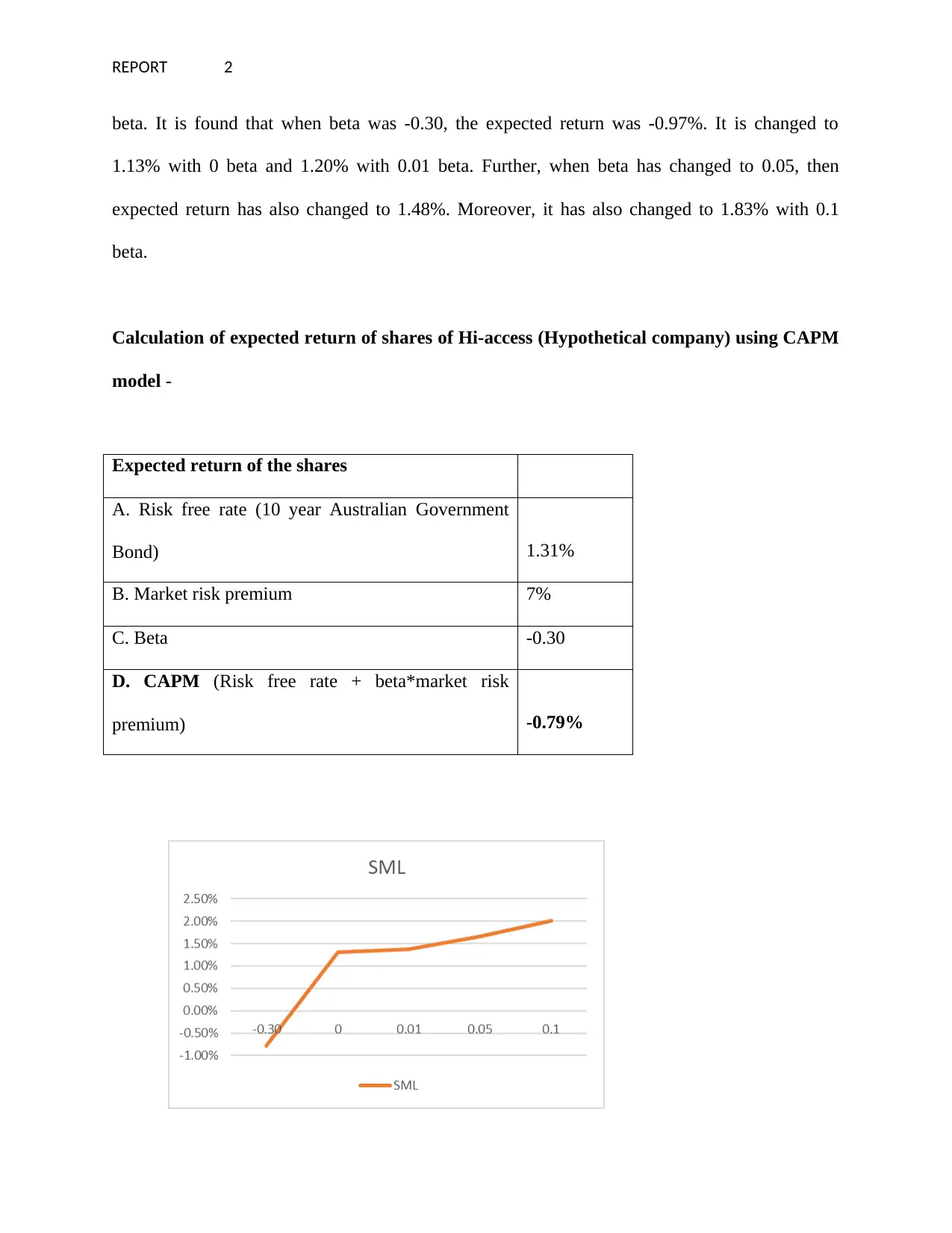

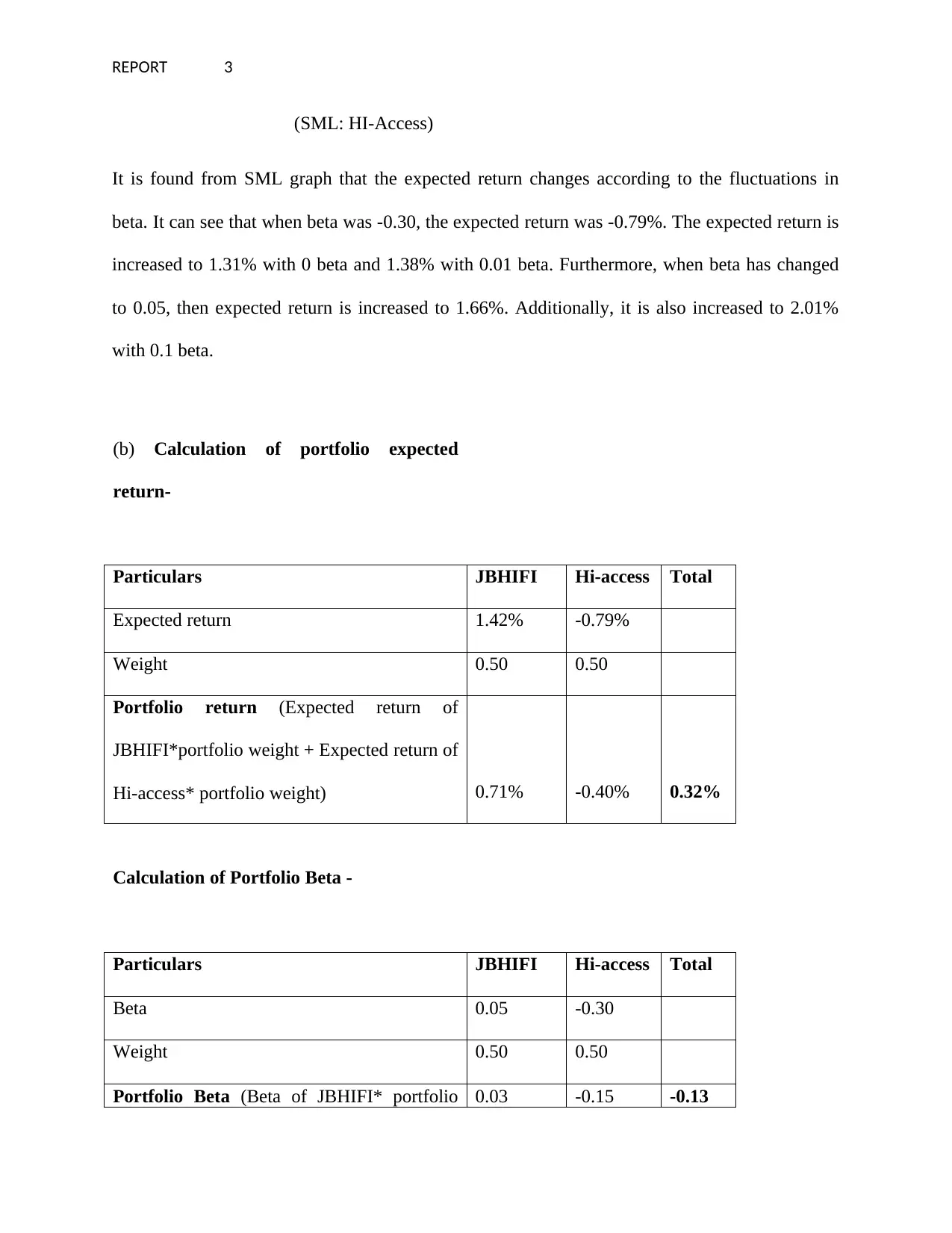

This assignment analyzes the expected return of shares for JBHIFI and a hypothetical company, Hi-access, using the Capital Asset Pricing Model (CAPM). The analysis includes calculating the risk-free rate, market risk premium, beta, and the resulting expected return for each company. The report then calculates the portfolio expected return and portfolio beta, considering the weights of each stock in the portfolio. Furthermore, the report discusses the concepts of beta, systematic risk, and the application of CAPM, including its formula and the interpretation of results. It also presents a Standard Security Market Line (SML) graph to illustrate the relationship between beta and expected return. The assignment also includes a discussion on the limitations of the CAPM model and the use of standard deviation to evaluate overall risk. Finally, the report references relevant academic literature to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.