Southern Cross University: ACC00716 Finance Risk and Return Analysis

VerifiedAdded on 2023/01/19

|12

|2329

|74

Report

AI Summary

This finance report analyzes the securities of CSL Ltd, a biotechnology company, focusing on risk and return relationships. It applies the Capital Asset Pricing Model (CAPM) to demonstrate these relationships and uses graphical representations. The report covers systematic and unsystematic risks, portfolio management strategies, and the Security Market Line (SML) to evaluate investment options. The assessment includes calculations and analysis of CAPM components, risk factors, and diversification strategies, concluding with an evaluation of portfolio returns and beta. The report provides a comprehensive overview of investment decision-making processes, highlighting the importance of risk assessment and portfolio diversification in finance.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

1

Table of Contents

Answer to question 1a:...............................................................................................................2

Answer to question 1b:...............................................................................................................2

Answer to question 1c:...............................................................................................................2

Answer to question 1d:...............................................................................................................2

Answer to question 1e:...............................................................................................................3

Answer to question 1f:...............................................................................................................3

Answer to question 2a:...............................................................................................................3

Answer to question 2b:...............................................................................................................4

Answer to question 3a:...............................................................................................................4

References:...............................................................................................................................10

1

Table of Contents

Answer to question 1a:...............................................................................................................2

Answer to question 1b:...............................................................................................................2

Answer to question 1c:...............................................................................................................2

Answer to question 1d:...............................................................................................................2

Answer to question 1e:...............................................................................................................3

Answer to question 1f:...............................................................................................................3

Answer to question 2a:...............................................................................................................3

Answer to question 2b:...............................................................................................................4

Answer to question 3a:...............................................................................................................4

References:...............................................................................................................................10

FINANCE

2

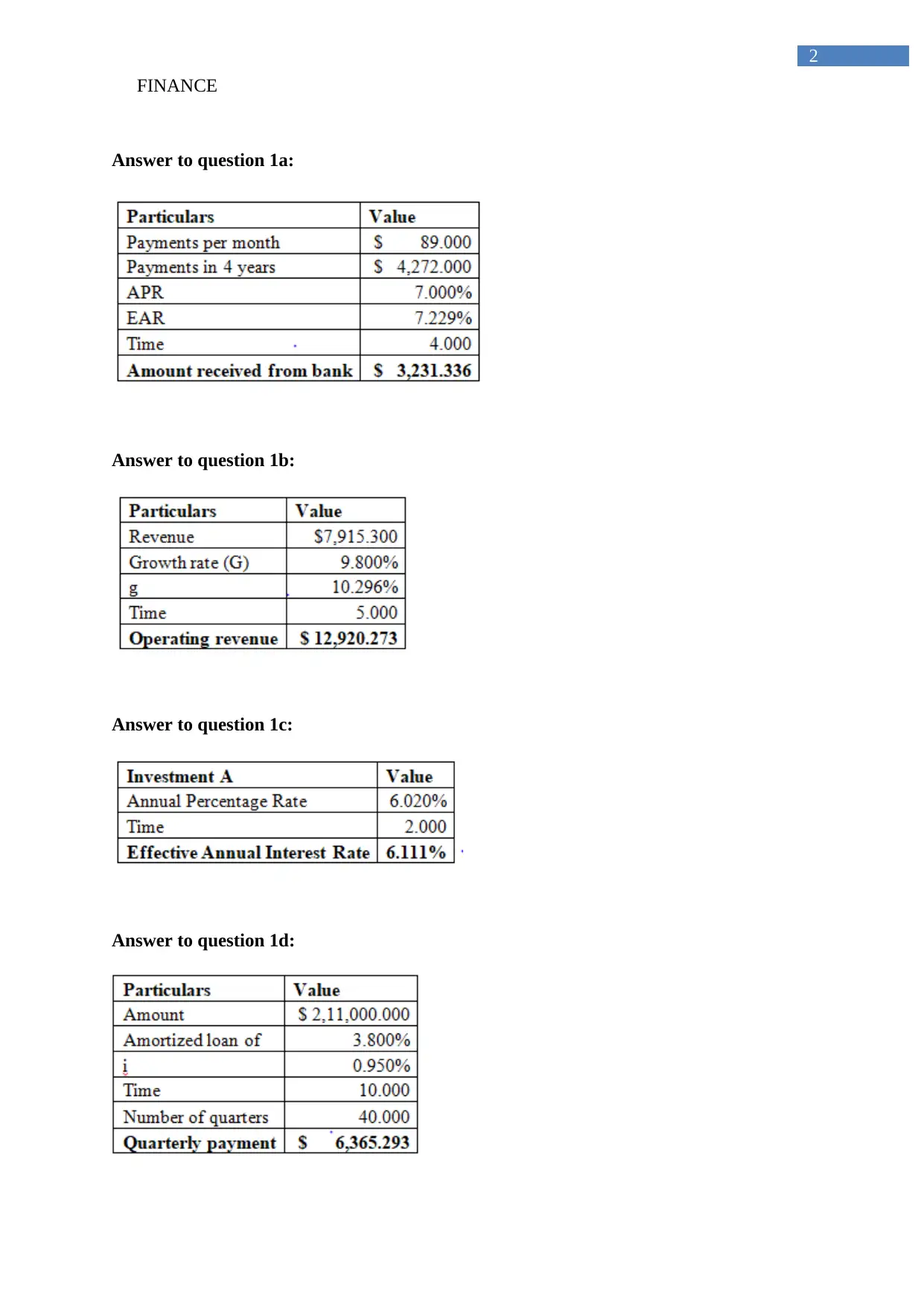

Answer to question 1a:

Answer to question 1b:

Answer to question 1c:

Answer to question 1d:

2

Answer to question 1a:

Answer to question 1b:

Answer to question 1c:

Answer to question 1d:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

3

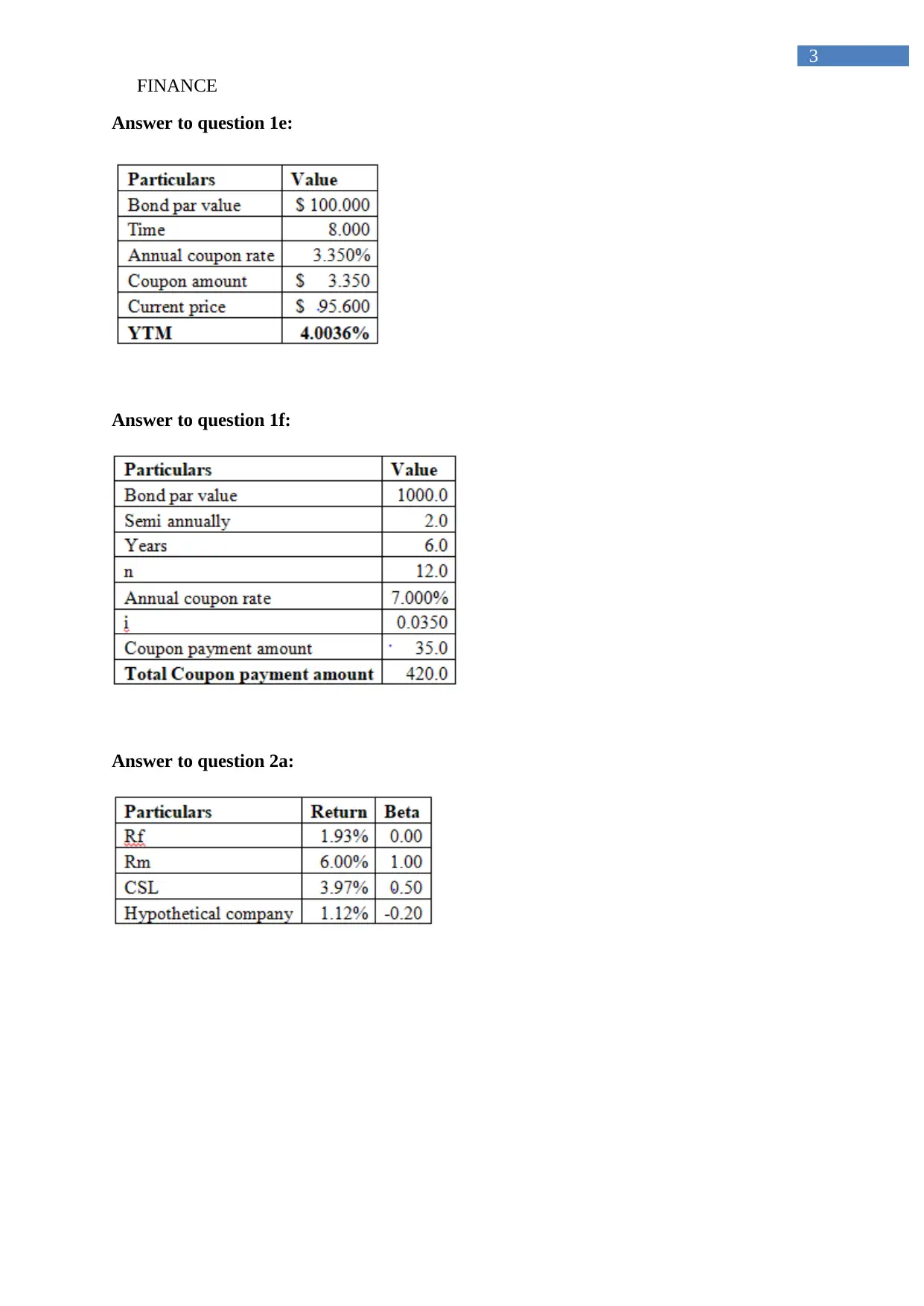

Answer to question 1e:

Answer to question 1f:

Answer to question 2a:

3

Answer to question 1e:

Answer to question 1f:

Answer to question 2a:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

4

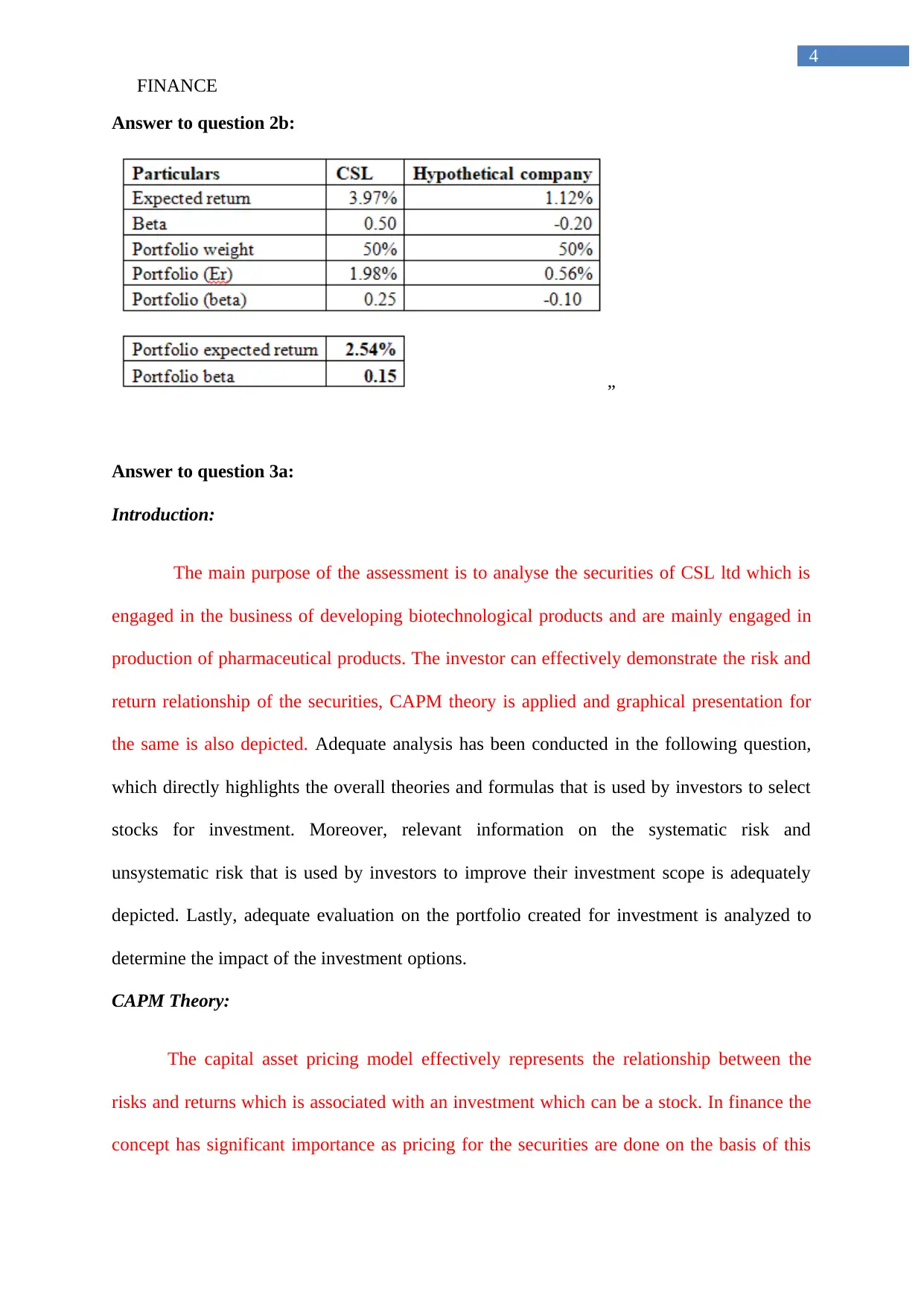

Answer to question 2b:

”

Answer to question 3a:

Introduction:

The main purpose of the assessment is to analyse the securities of CSL ltd which is

engaged in the business of developing biotechnological products and are mainly engaged in

production of pharmaceutical products. The investor can effectively demonstrate the risk and

return relationship of the securities, CAPM theory is applied and graphical presentation for

the same is also depicted. Adequate analysis has been conducted in the following question,

which directly highlights the overall theories and formulas that is used by investors to select

stocks for investment. Moreover, relevant information on the systematic risk and

unsystematic risk that is used by investors to improve their investment scope is adequately

depicted. Lastly, adequate evaluation on the portfolio created for investment is analyzed to

determine the impact of the investment options.

CAPM Theory:

The capital asset pricing model effectively represents the relationship between the

risks and returns which is associated with an investment which can be a stock. In finance the

concept has significant importance as pricing for the securities are done on the basis of this

4

Answer to question 2b:

”

Answer to question 3a:

Introduction:

The main purpose of the assessment is to analyse the securities of CSL ltd which is

engaged in the business of developing biotechnological products and are mainly engaged in

production of pharmaceutical products. The investor can effectively demonstrate the risk and

return relationship of the securities, CAPM theory is applied and graphical presentation for

the same is also depicted. Adequate analysis has been conducted in the following question,

which directly highlights the overall theories and formulas that is used by investors to select

stocks for investment. Moreover, relevant information on the systematic risk and

unsystematic risk that is used by investors to improve their investment scope is adequately

depicted. Lastly, adequate evaluation on the portfolio created for investment is analyzed to

determine the impact of the investment options.

CAPM Theory:

The capital asset pricing model effectively represents the relationship between the

risks and returns which is associated with an investment which can be a stock. In finance the

concept has significant importance as pricing for the securities are done on the basis of this

FINANCE

5

model and this is generally used for pricing of risky securities. The CAPM model considers

the risks which is associated with the securities and the time value of money concept for the

securities and effectively computes results on the same. Therefore, it can be established that

CAPM model helps investors to take appropriate decisions regarding investment stocks.

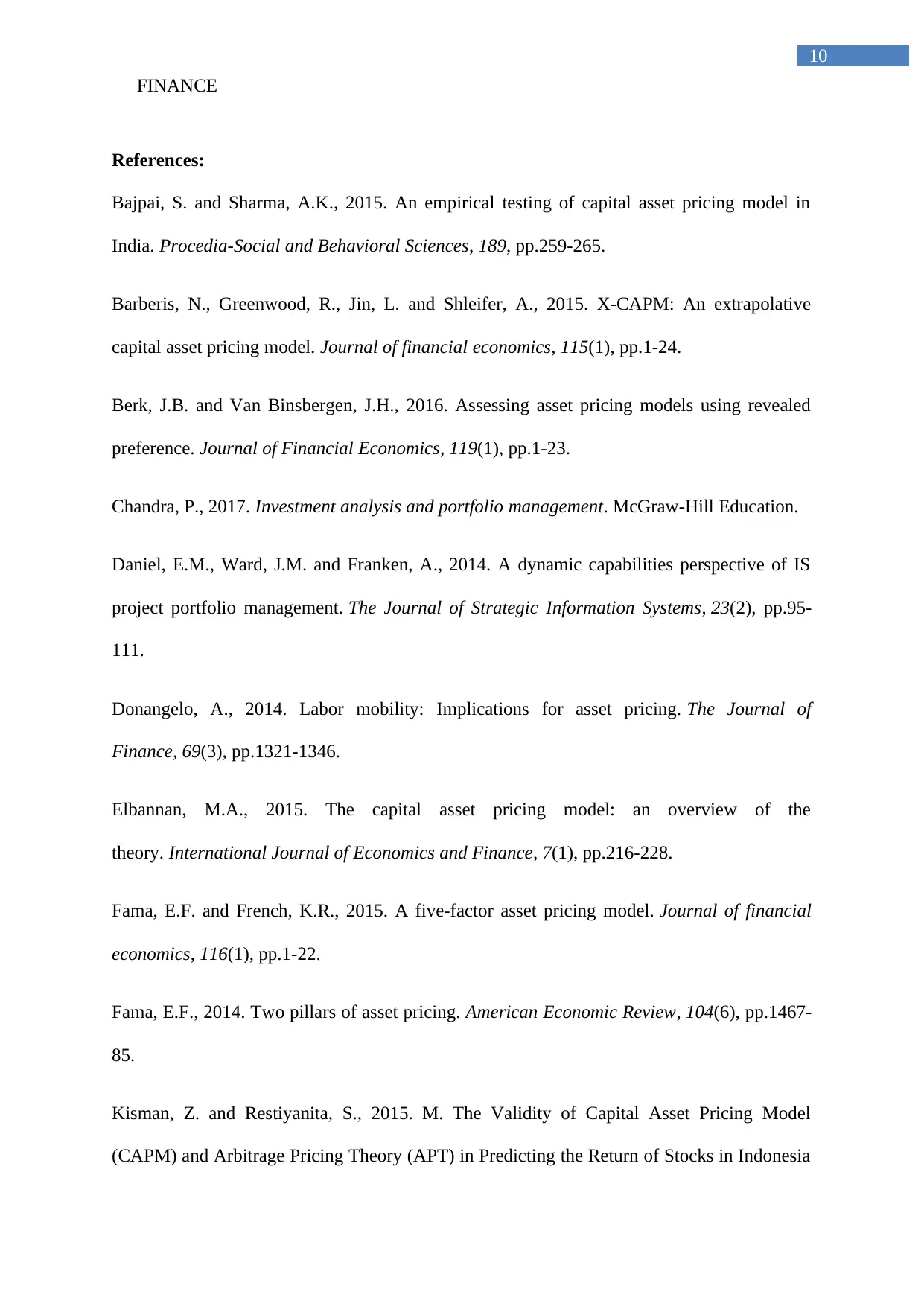

Figure 1: CAPM formula

(Source: Zabarankin, Pavlikov and Uryasev 2014)

The formula used in the above figure provides information regarding the expected

return of a stock, which can be used investors by evaluating risk free rate, market return, and

beta. The Capital Asset pricing model formula is depicted in the above figure, which can

allow the investors to detect the investment options that can support investment strategy. The

Capital Asset pricing model mainly relies on the risk factors of a stock and determines the

expected return on the basis of the overall risk that needs to be obtained by the investors.

Elbannan (2015) mentioned that with the information provided by CAPM model investors

can combine low risk and high-risk stocks, which can have higher returns from investment.

The different components which are used in CAPM formula are related to different

factors which affects the decisions of an investor. It a known fact that an investor invests in

stocks for enhancing his returns and he expects to be compensated for risk undertaken and

also time value of money. The risk-free rate which is used in CAPM Model accounts for the

time value of money. While the beta signifies the level of risks which is associated with the

5

model and this is generally used for pricing of risky securities. The CAPM model considers

the risks which is associated with the securities and the time value of money concept for the

securities and effectively computes results on the same. Therefore, it can be established that

CAPM model helps investors to take appropriate decisions regarding investment stocks.

Figure 1: CAPM formula

(Source: Zabarankin, Pavlikov and Uryasev 2014)

The formula used in the above figure provides information regarding the expected

return of a stock, which can be used investors by evaluating risk free rate, market return, and

beta. The Capital Asset pricing model formula is depicted in the above figure, which can

allow the investors to detect the investment options that can support investment strategy. The

Capital Asset pricing model mainly relies on the risk factors of a stock and determines the

expected return on the basis of the overall risk that needs to be obtained by the investors.

Elbannan (2015) mentioned that with the information provided by CAPM model investors

can combine low risk and high-risk stocks, which can have higher returns from investment.

The different components which are used in CAPM formula are related to different

factors which affects the decisions of an investor. It a known fact that an investor invests in

stocks for enhancing his returns and he expects to be compensated for risk undertaken and

also time value of money. The risk-free rate which is used in CAPM Model accounts for the

time value of money. While the beta signifies the level of risks which is associated with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

6

investment. The value of beta would be higher than 1 if the stock is risky in nature and

similar a beta value of less than 1 represent that the overall risk in the portfolio is low. Market

risk premium represent the return which is expected by the investor about the risk-free rate of

return. It is to be noted that the main purpose of applying CAPM model in a business is to

effectively measure whether the considered stock is fairly valued when the risks associated

with the stock and time value of the investment is measured in terms of returns which is

generated by the stock.

Impact of Systematic risk and Unsystematic risk:

Systematic Risks

These risks reflect the risks which are inherent to the entire market or market

segment. These risks are also known as undiversifiable risks and affects the overall market

and not just a particular stock. The main concern regarding such a risk is that it is completely

unavoidable and unpredictable. An example of systematic risk can be provided of the Great

Depression of 2008 which saw drastic changes in securities market. An appropriate

representation of the systematic risk can be derived from analysis of a beta which effectively

measures the risks which is associated with the stock in comparison to market. A beat which

is greater than 1 signifies that the systematic risk is more while if the beta is valued at less

than 1 than systematic risk is low.

Unsystematic Risks

Unsystematic risks are the risks which can be avoided or minimized by the investor

by following appropriate strategies such as diversification. In other words, unsystematic

risk refers to the risk which emerges out of controlled and known variables and the same are

industry specific or specific to the security which is being considered. In addition to this,

6

investment. The value of beta would be higher than 1 if the stock is risky in nature and

similar a beta value of less than 1 represent that the overall risk in the portfolio is low. Market

risk premium represent the return which is expected by the investor about the risk-free rate of

return. It is to be noted that the main purpose of applying CAPM model in a business is to

effectively measure whether the considered stock is fairly valued when the risks associated

with the stock and time value of the investment is measured in terms of returns which is

generated by the stock.

Impact of Systematic risk and Unsystematic risk:

Systematic Risks

These risks reflect the risks which are inherent to the entire market or market

segment. These risks are also known as undiversifiable risks and affects the overall market

and not just a particular stock. The main concern regarding such a risk is that it is completely

unavoidable and unpredictable. An example of systematic risk can be provided of the Great

Depression of 2008 which saw drastic changes in securities market. An appropriate

representation of the systematic risk can be derived from analysis of a beta which effectively

measures the risks which is associated with the stock in comparison to market. A beat which

is greater than 1 signifies that the systematic risk is more while if the beta is valued at less

than 1 than systematic risk is low.

Unsystematic Risks

Unsystematic risks are the risks which can be avoided or minimized by the investor

by following appropriate strategies such as diversification. In other words, unsystematic

risk refers to the risk which emerges out of controlled and known variables and the same are

industry specific or specific to the security which is being considered. In addition to this,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

7

unsystematic risks take place due to internal factors and therefore the same can be controlled

by the investor. The most approach which is applied by the investor for managing such a risk

is by properly diversifying the portfolio (Sicotte, Drouin and Delerue 2014).

It is to be noted that systematic risks and unsystematic risks of a portfolio combines to

make total risk which is associated with the stock and the same needs to be considered before

taking any investment decisions. Both Systematic and Unsystematic risk lingers with an

investment, which allows the investor to detect how much risk can be diversified to minimize

the impact on its overall investment. Diversification is one of the major contributors of risk

aversion, as it allows the investors to minimize the negative impact on their overall

investment exposure. As per the diversification strategy, investors can effectively add new

securities in the portfolio for the purpose of spreading out the risks which is associated with

the portfolio (Szegö 2014). This is also done for balancing the portfolio so that risks can be

maintained and more returns can be generated. Moreover, the investors can diversify

unsystematic risk after utilizing adequate hedging measures. On the other hand, high systemic

risk present in a stock could directly hamper the investment capital of an investor (Kisman

and Restiyanita 2015).

Portfolio Management

One of the main steps which can be taken by an investor for appropriately managing

the risks of a group of stocks is by establishing a portfolio. Portfolio management can be

defined as the process by which investors take important decisions regarding different

investments mix in order to minimize the risks which is associated with the group of

securities (Kock, Heising and Gemünden 2015). In addition to this, portfolio management is

also used for the purpose of matching investments and also proper allocation of the asset

(Chandra 2017). In addition to this, the investor also has the option of properly diversifying

the portfolio so that the overall risks which is associated with the securities is significantly

7

unsystematic risks take place due to internal factors and therefore the same can be controlled

by the investor. The most approach which is applied by the investor for managing such a risk

is by properly diversifying the portfolio (Sicotte, Drouin and Delerue 2014).

It is to be noted that systematic risks and unsystematic risks of a portfolio combines to

make total risk which is associated with the stock and the same needs to be considered before

taking any investment decisions. Both Systematic and Unsystematic risk lingers with an

investment, which allows the investor to detect how much risk can be diversified to minimize

the impact on its overall investment. Diversification is one of the major contributors of risk

aversion, as it allows the investors to minimize the negative impact on their overall

investment exposure. As per the diversification strategy, investors can effectively add new

securities in the portfolio for the purpose of spreading out the risks which is associated with

the portfolio (Szegö 2014). This is also done for balancing the portfolio so that risks can be

maintained and more returns can be generated. Moreover, the investors can diversify

unsystematic risk after utilizing adequate hedging measures. On the other hand, high systemic

risk present in a stock could directly hamper the investment capital of an investor (Kisman

and Restiyanita 2015).

Portfolio Management

One of the main steps which can be taken by an investor for appropriately managing

the risks of a group of stocks is by establishing a portfolio. Portfolio management can be

defined as the process by which investors take important decisions regarding different

investments mix in order to minimize the risks which is associated with the group of

securities (Kock, Heising and Gemünden 2015). In addition to this, portfolio management is

also used for the purpose of matching investments and also proper allocation of the asset

(Chandra 2017). In addition to this, the investor also has the option of properly diversifying

the portfolio so that the overall risks which is associated with the securities is significantly

FINANCE

8

lowered. Portfolio management is all about determining strengths, weaknesses, opportunities

and threats and creating an appropriate mix of securities which can maximise the returns and

minimise the risks of the investor.

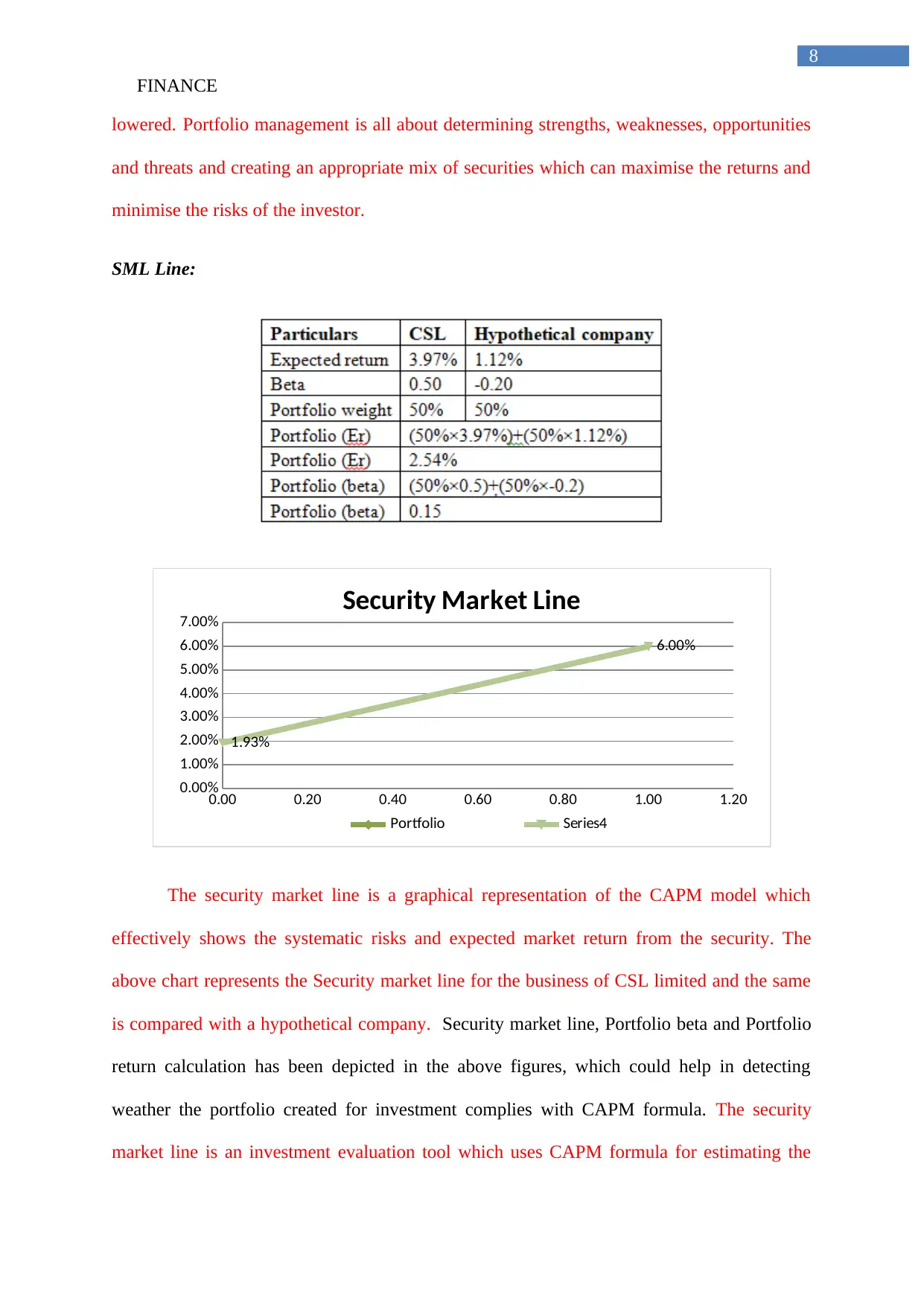

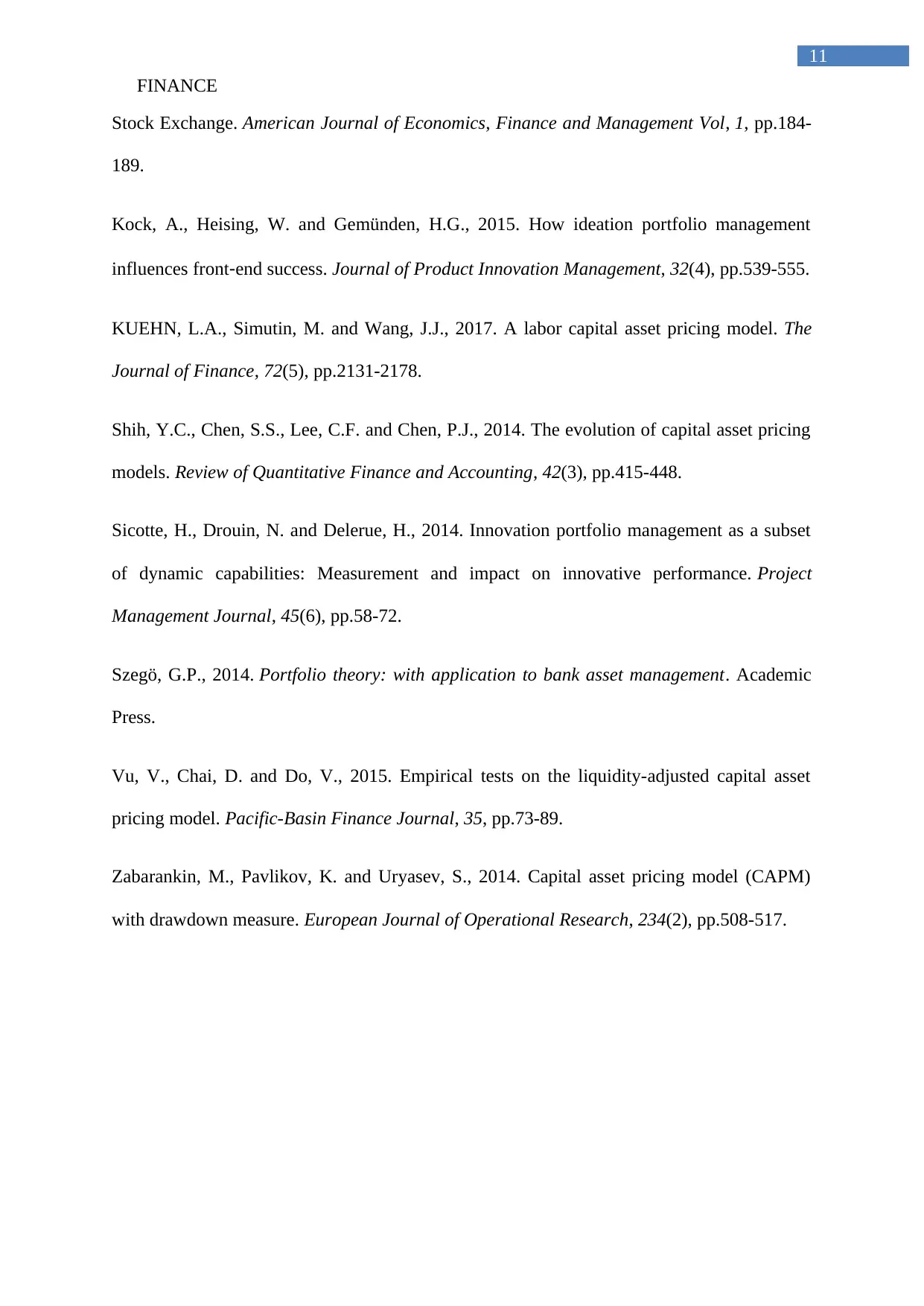

SML Line:

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

1.93%

6.00%

Security Market Line

Portfolio Series4

The security market line is a graphical representation of the CAPM model which

effectively shows the systematic risks and expected market return from the security. The

above chart represents the Security market line for the business of CSL limited and the same

is compared with a hypothetical company. Security market line, Portfolio beta and Portfolio

return calculation has been depicted in the above figures, which could help in detecting

weather the portfolio created for investment complies with CAPM formula. The security

market line is an investment evaluation tool which uses CAPM formula for estimating the

8

lowered. Portfolio management is all about determining strengths, weaknesses, opportunities

and threats and creating an appropriate mix of securities which can maximise the returns and

minimise the risks of the investor.

SML Line:

0.00 0.20 0.40 0.60 0.80 1.00 1.20

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

1.93%

6.00%

Security Market Line

Portfolio Series4

The security market line is a graphical representation of the CAPM model which

effectively shows the systematic risks and expected market return from the security. The

above chart represents the Security market line for the business of CSL limited and the same

is compared with a hypothetical company. Security market line, Portfolio beta and Portfolio

return calculation has been depicted in the above figures, which could help in detecting

weather the portfolio created for investment complies with CAPM formula. The security

market line is an investment evaluation tool which uses CAPM formula for estimating the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE

9

risk-return relationship of the investment (Daniel, Ward and Franken 2014). The graph is

based on the assumption that the investor would be compensated for the time value of money

factor and also for the level of risk which is undertaken by the investor. The portfolio returns

and risk is on the security market line as depicted in the above figure, which states that the

CAPM formula is correctly used, while detecting the expected Returns. The overall portfolio

return is calculated to be at the levels of 2.54%, while the beta is at 0.15. The Combination of

return and risk is due to the equal portfolio weights, which has relatively reduced the overall

risk attributes of the combined portfolio (Fama 2014).

Conclusion:

The above discussion effectively shows the risks and return relationship of an

investment and how the same needs to be considered by an investor before taking any

investment decisions. In order to effectively manage the risks of a group of stocks, an

investor has an option of creating a portfolio. Portfolios are considered to be one of the major

component of investment, as it allows the investors to minimize risk attributes of an

investment. Moreover, investors directly utilize the diversification method to minimize the

risk attribute of an investment. The investor has the option of adding more securities to the

portfolio for the purpose of effectively managing the risks which is associated with the

portfolio. Furthermore, adequate formulas have been used to derive the portfolio return and

Peter after accommodating the optical company and CSL in the portfolio.

9

risk-return relationship of the investment (Daniel, Ward and Franken 2014). The graph is

based on the assumption that the investor would be compensated for the time value of money

factor and also for the level of risk which is undertaken by the investor. The portfolio returns

and risk is on the security market line as depicted in the above figure, which states that the

CAPM formula is correctly used, while detecting the expected Returns. The overall portfolio

return is calculated to be at the levels of 2.54%, while the beta is at 0.15. The Combination of

return and risk is due to the equal portfolio weights, which has relatively reduced the overall

risk attributes of the combined portfolio (Fama 2014).

Conclusion:

The above discussion effectively shows the risks and return relationship of an

investment and how the same needs to be considered by an investor before taking any

investment decisions. In order to effectively manage the risks of a group of stocks, an

investor has an option of creating a portfolio. Portfolios are considered to be one of the major

component of investment, as it allows the investors to minimize risk attributes of an

investment. Moreover, investors directly utilize the diversification method to minimize the

risk attribute of an investment. The investor has the option of adding more securities to the

portfolio for the purpose of effectively managing the risks which is associated with the

portfolio. Furthermore, adequate formulas have been used to derive the portfolio return and

Peter after accommodating the optical company and CSL in the portfolio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

10

References:

Bajpai, S. and Sharma, A.K., 2015. An empirical testing of capital asset pricing model in

India. Procedia-Social and Behavioral Sciences, 189, pp.259-265.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Berk, J.B. and Van Binsbergen, J.H., 2016. Assessing asset pricing models using revealed

preference. Journal of Financial Economics, 119(1), pp.1-23.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Daniel, E.M., Ward, J.M. and Franken, A., 2014. A dynamic capabilities perspective of IS

project portfolio management. The Journal of Strategic Information Systems, 23(2), pp.95-

111.

Donangelo, A., 2014. Labor mobility: Implications for asset pricing. The Journal of

Finance, 69(3), pp.1321-1346.

Elbannan, M.A., 2015. The capital asset pricing model: an overview of the

theory. International Journal of Economics and Finance, 7(1), pp.216-228.

Fama, E.F. and French, K.R., 2015. A five-factor asset pricing model. Journal of financial

economics, 116(1), pp.1-22.

Fama, E.F., 2014. Two pillars of asset pricing. American Economic Review, 104(6), pp.1467-

85.

Kisman, Z. and Restiyanita, S., 2015. M. The Validity of Capital Asset Pricing Model

(CAPM) and Arbitrage Pricing Theory (APT) in Predicting the Return of Stocks in Indonesia

10

References:

Bajpai, S. and Sharma, A.K., 2015. An empirical testing of capital asset pricing model in

India. Procedia-Social and Behavioral Sciences, 189, pp.259-265.

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Berk, J.B. and Van Binsbergen, J.H., 2016. Assessing asset pricing models using revealed

preference. Journal of Financial Economics, 119(1), pp.1-23.

Chandra, P., 2017. Investment analysis and portfolio management. McGraw-Hill Education.

Daniel, E.M., Ward, J.M. and Franken, A., 2014. A dynamic capabilities perspective of IS

project portfolio management. The Journal of Strategic Information Systems, 23(2), pp.95-

111.

Donangelo, A., 2014. Labor mobility: Implications for asset pricing. The Journal of

Finance, 69(3), pp.1321-1346.

Elbannan, M.A., 2015. The capital asset pricing model: an overview of the

theory. International Journal of Economics and Finance, 7(1), pp.216-228.

Fama, E.F. and French, K.R., 2015. A five-factor asset pricing model. Journal of financial

economics, 116(1), pp.1-22.

Fama, E.F., 2014. Two pillars of asset pricing. American Economic Review, 104(6), pp.1467-

85.

Kisman, Z. and Restiyanita, S., 2015. M. The Validity of Capital Asset Pricing Model

(CAPM) and Arbitrage Pricing Theory (APT) in Predicting the Return of Stocks in Indonesia

FINANCE

11

Stock Exchange. American Journal of Economics, Finance and Management Vol, 1, pp.184-

189.

Kock, A., Heising, W. and Gemünden, H.G., 2015. How ideation portfolio management

influences front‐end success. Journal of Product Innovation Management, 32(4), pp.539-555.

KUEHN, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Shih, Y.C., Chen, S.S., Lee, C.F. and Chen, P.J., 2014. The evolution of capital asset pricing

models. Review of Quantitative Finance and Accounting, 42(3), pp.415-448.

Sicotte, H., Drouin, N. and Delerue, H., 2014. Innovation portfolio management as a subset

of dynamic capabilities: Measurement and impact on innovative performance. Project

Management Journal, 45(6), pp.58-72.

Szegö, G.P., 2014. Portfolio theory: with application to bank asset management. Academic

Press.

Vu, V., Chai, D. and Do, V., 2015. Empirical tests on the liquidity-adjusted capital asset

pricing model. Pacific-Basin Finance Journal, 35, pp.73-89.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM)

with drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

11

Stock Exchange. American Journal of Economics, Finance and Management Vol, 1, pp.184-

189.

Kock, A., Heising, W. and Gemünden, H.G., 2015. How ideation portfolio management

influences front‐end success. Journal of Product Innovation Management, 32(4), pp.539-555.

KUEHN, L.A., Simutin, M. and Wang, J.J., 2017. A labor capital asset pricing model. The

Journal of Finance, 72(5), pp.2131-2178.

Shih, Y.C., Chen, S.S., Lee, C.F. and Chen, P.J., 2014. The evolution of capital asset pricing

models. Review of Quantitative Finance and Accounting, 42(3), pp.415-448.

Sicotte, H., Drouin, N. and Delerue, H., 2014. Innovation portfolio management as a subset

of dynamic capabilities: Measurement and impact on innovative performance. Project

Management Journal, 45(6), pp.58-72.

Szegö, G.P., 2014. Portfolio theory: with application to bank asset management. Academic

Press.

Vu, V., Chai, D. and Do, V., 2015. Empirical tests on the liquidity-adjusted capital asset

pricing model. Pacific-Basin Finance Journal, 35, pp.73-89.

Zabarankin, M., Pavlikov, K. and Uryasev, S., 2014. Capital asset pricing model (CAPM)

with drawdown measure. European Journal of Operational Research, 234(2), pp.508-517.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.