Financial Management Report: FINM202 - Risk, Return and Governance

VerifiedAdded on 2021/05/31

|8

|1804

|260

Report

AI Summary

This report, prepared for the Financial Management course (FINM202), examines risk and return for portfolios and the role of finance managers in corporate governance within the Australian finance sector. The first section analyzes operating and financial leverage for two hypothetical companies, calculating key metrics like return on equity and providing working notes. The second part delves into corporate governance, outlining the principles that guide finance managers' responsibilities within organizations like NAB, emphasizing accountability, ethical conduct, risk management, and transparent reporting. The report references several academic sources to support its findings and recommendations.

Financial management

Course Bachelor of Business / Bachelor of Accounting

Unit Financial Management

Unit Code FINM202

Type of Assessment Assessment 3 – Group Report

Course Bachelor of Business / Bachelor of Accounting

Unit Financial Management

Unit Code FINM202

Type of Assessment Assessment 3 – Group Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1........................................................................................................................................3

Risk and return for portfolios......................................................................................................3

Assumption..................................................................................................................................3

Analysis.......................................................................................................................................4

Question 2........................................................................................................................................4

The role of finance manager on cooperate governess in a finance sector company in Australia.

.....................................................................................................................................................4

Principal 1....................................................................................................................................5

Principal 2....................................................................................................................................6

Principal 3....................................................................................................................................6

Principal 4....................................................................................................................................6

Principal 5....................................................................................................................................6

References........................................................................................................................................8

Question 1........................................................................................................................................3

Risk and return for portfolios......................................................................................................3

Assumption..................................................................................................................................3

Analysis.......................................................................................................................................4

Question 2........................................................................................................................................4

The role of finance manager on cooperate governess in a finance sector company in Australia.

.....................................................................................................................................................4

Principal 1....................................................................................................................................5

Principal 2....................................................................................................................................6

Principal 3....................................................................................................................................6

Principal 4....................................................................................................................................6

Principal 5....................................................................................................................................6

References........................................................................................................................................8

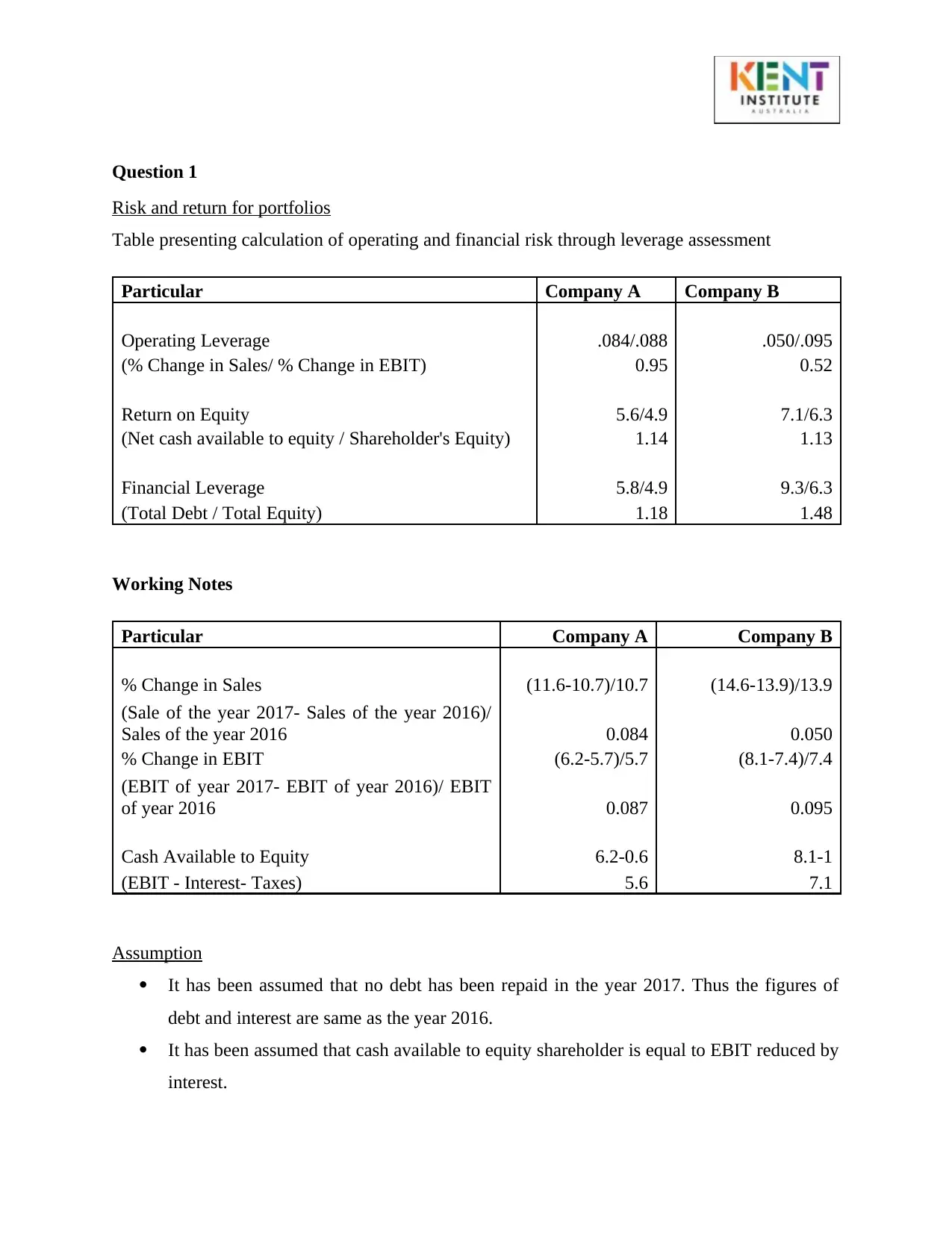

Question 1

Risk and return for portfolios

Table presenting calculation of operating and financial risk through leverage assessment

Particular Company A Company B

Operating Leverage .084/.088 .050/.095

(% Change in Sales/ % Change in EBIT) 0.95 0.52

Return on Equity 5.6/4.9 7.1/6.3

(Net cash available to equity / Shareholder's Equity) 1.14 1.13

Financial Leverage 5.8/4.9 9.3/6.3

(Total Debt / Total Equity) 1.18 1.48

Working Notes

Particular Company A Company B

% Change in Sales (11.6-10.7)/10.7 (14.6-13.9)/13.9

(Sale of the year 2017- Sales of the year 2016)/

Sales of the year 2016 0.084 0.050

% Change in EBIT (6.2-5.7)/5.7 (8.1-7.4)/7.4

(EBIT of year 2017- EBIT of year 2016)/ EBIT

of year 2016 0.087 0.095

Cash Available to Equity 6.2-0.6 8.1-1

(EBIT - Interest- Taxes) 5.6 7.1

Assumption

It has been assumed that no debt has been repaid in the year 2017. Thus the figures of

debt and interest are same as the year 2016.

It has been assumed that cash available to equity shareholder is equal to EBIT reduced by

interest.

Risk and return for portfolios

Table presenting calculation of operating and financial risk through leverage assessment

Particular Company A Company B

Operating Leverage .084/.088 .050/.095

(% Change in Sales/ % Change in EBIT) 0.95 0.52

Return on Equity 5.6/4.9 7.1/6.3

(Net cash available to equity / Shareholder's Equity) 1.14 1.13

Financial Leverage 5.8/4.9 9.3/6.3

(Total Debt / Total Equity) 1.18 1.48

Working Notes

Particular Company A Company B

% Change in Sales (11.6-10.7)/10.7 (14.6-13.9)/13.9

(Sale of the year 2017- Sales of the year 2016)/

Sales of the year 2016 0.084 0.050

% Change in EBIT (6.2-5.7)/5.7 (8.1-7.4)/7.4

(EBIT of year 2017- EBIT of year 2016)/ EBIT

of year 2016 0.087 0.095

Cash Available to Equity 6.2-0.6 8.1-1

(EBIT - Interest- Taxes) 5.6 7.1

Assumption

It has been assumed that no debt has been repaid in the year 2017. Thus the figures of

debt and interest are same as the year 2016.

It has been assumed that cash available to equity shareholder is equal to EBIT reduced by

interest.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As no tax detail has been provided, the same has been ignored for calculation of cash

available to equity shareholders.

Analysis

High leverage ratio represents that organization has been aggressive in financing its growth

through the assistance of debt. In the present case, it can be assessed that Company B is having

high financial leverage in comparison to Company A, the same signifies that it is dependent on

debt in order to attain predetermined objectives and growth. Further, as company B has lower

operating leverage which signifies that company will not be able to earn a higher profit on

additional sales. In addition to this;s it will not require generating additional sales for covering

the fixed cost.

Question 2

The role of finance manager on cooperates governess in a finance sector company in Australia.

Corporate governance is the means, procedure and relationship by which companies are

monitored and controlled. Governance frameworks and principles are determined by delegating

rights and responsibilities between various participants involved in the corporation like financial

managers, the board of directors and other related stakeholders and inclusive of the rules and

process for decision making in company affairs. Further corporate governance is inclusive of the

procedure through goals of companies are established and followed in terms of market,

regulatory and social environment (Tricker and Tricker, 2015). The fact of corporate governance

significance cannot be denied in present developing and competitive business environment. It is

very important for Authorities of NAB to the attainment of a new edge of competitiveness and

profitability. Corporate governance addresses the ways by which financial suppliers ensure

corporations of receiving a higher investment return.

Good corporate governance will ensure the company with integrity and fair ethics while making

sure that all the engaged shareholders are treated in a viable and fair manner. Along with this,

corporate is also very important in considering whether the board have enough skills to offer

insights and meaningful advice to managerial authorities.

available to equity shareholders.

Analysis

High leverage ratio represents that organization has been aggressive in financing its growth

through the assistance of debt. In the present case, it can be assessed that Company B is having

high financial leverage in comparison to Company A, the same signifies that it is dependent on

debt in order to attain predetermined objectives and growth. Further, as company B has lower

operating leverage which signifies that company will not be able to earn a higher profit on

additional sales. In addition to this;s it will not require generating additional sales for covering

the fixed cost.

Question 2

The role of finance manager on cooperates governess in a finance sector company in Australia.

Corporate governance is the means, procedure and relationship by which companies are

monitored and controlled. Governance frameworks and principles are determined by delegating

rights and responsibilities between various participants involved in the corporation like financial

managers, the board of directors and other related stakeholders and inclusive of the rules and

process for decision making in company affairs. Further corporate governance is inclusive of the

procedure through goals of companies are established and followed in terms of market,

regulatory and social environment (Tricker and Tricker, 2015). The fact of corporate governance

significance cannot be denied in present developing and competitive business environment. It is

very important for Authorities of NAB to the attainment of a new edge of competitiveness and

profitability. Corporate governance addresses the ways by which financial suppliers ensure

corporations of receiving a higher investment return.

Good corporate governance will ensure the company with integrity and fair ethics while making

sure that all the engaged shareholders are treated in a viable and fair manner. Along with this,

corporate is also very important in considering whether the board have enough skills to offer

insights and meaningful advice to managerial authorities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate governance arising from the agency concept describes it with relation to how holders

of equity and debt can impact the firm’s manager to act in their best interest to whom they have

offered capital and the soundness with which firm managers will assign the resources at disposal

based on the scale to the motivation of the creditor or shareholder. In the financial structure, the

corporate governance is said to be the key to identify the health and ability of the overall

financial system to succeed or survive from economic downturns (Davies, 2016). The financial

system health is highly based on the underlying effectiveness of individual elements and the

relationship among them like financial institutions as well as payments systems. In exchange,

their efficiency of this is highly based on their ability to determine, monitor, consider and control

risks. Further, corporate governance will allow NAB authorities to place positive characteristics

and strengths on display. With their purpose showcased, NAB authorities will be more likely to

be accountable on their conduct and actins with their best interests, Thereby, more willing to

separate themselves from risk and unfaithfulness (Larcker and Tayan, 2015). Corporate

governance is purposed to raise the corporate accountability and to prevent huge risks and

damage before they take place.

The roles of finance manager on corporate governance in the NAB authorities in Australia can be

described in five principles which are enumerated as below:

Principal 1

The managing authorities of the NAB should be regulated by the effective team of board

members having accountability of governance. Managing authorities should have a clear

governance formation which is reflected by the demand and complexities of the organization

which is supported by the further basic working environment, policies, approach, principles,

company value, risk factors, and internal factors. Managing authorities should comprise its team

with highly skilled, experienced, well-informed and knowledgeable members (ArAs, 2016). The

monetary authorities of NAB are not required of running the committees, but they have a

responsibility to analyze and review companies function or issues. Further, they should provide

suggestions and recommendation to the authorities on the concerned issues of governance in

existing work environment. It should be ensured by the NAB that working technique should be

clear and powered with the sufficient senior management authority to develop healthy work

of equity and debt can impact the firm’s manager to act in their best interest to whom they have

offered capital and the soundness with which firm managers will assign the resources at disposal

based on the scale to the motivation of the creditor or shareholder. In the financial structure, the

corporate governance is said to be the key to identify the health and ability of the overall

financial system to succeed or survive from economic downturns (Davies, 2016). The financial

system health is highly based on the underlying effectiveness of individual elements and the

relationship among them like financial institutions as well as payments systems. In exchange,

their efficiency of this is highly based on their ability to determine, monitor, consider and control

risks. Further, corporate governance will allow NAB authorities to place positive characteristics

and strengths on display. With their purpose showcased, NAB authorities will be more likely to

be accountable on their conduct and actins with their best interests, Thereby, more willing to

separate themselves from risk and unfaithfulness (Larcker and Tayan, 2015). Corporate

governance is purposed to raise the corporate accountability and to prevent huge risks and

damage before they take place.

The roles of finance manager on corporate governance in the NAB authorities in Australia can be

described in five principles which are enumerated as below:

Principal 1

The managing authorities of the NAB should be regulated by the effective team of board

members having accountability of governance. Managing authorities should have a clear

governance formation which is reflected by the demand and complexities of the organization

which is supported by the further basic working environment, policies, approach, principles,

company value, risk factors, and internal factors. Managing authorities should comprise its team

with highly skilled, experienced, well-informed and knowledgeable members (ArAs, 2016). The

monetary authorities of NAB are not required of running the committees, but they have a

responsibility to analyze and review companies function or issues. Further, they should provide

suggestions and recommendation to the authorities on the concerned issues of governance in

existing work environment. It should be ensured by the NAB that working technique should be

clear and powered with the sufficient senior management authority to develop healthy work

environment so that work must be done in an efficient manner to ensure governance in financial

operations.

Principal 2

Directors are accountable for managing, supervising, and seamless working of the governance

company. Authorizes of NAB is responsible for doing the work according to applied government

rules and policies moreover it works in given framework which is predefined according to the

suitability of the company (Cheng, Ioannou and Serafeim, 2014). Companies strategy and

policies are planned and executed by the directors and are highly responsible for organizations

profits and loss. Performance and actions of the members are evaluated by the authorities on the

regular terms.

Principal 3

Business conduct and ethics- It is the responsibility of managerial authorities to sustain a good

business performance, reliability, and ethical behaviour. Authority should build up, retain and

put into operation a proficient interest plan (McCahery, Sautner and Starks, 2016). Authorities

have a duty to minimize and avoid conflict of interest moreover maintain their personal and

business affairs for the betterment of the governance. Authorities are legally responsible for

working for the better interest of the company.

Principal 4

Accountability for reviewing the organization's value and position managing authorities should

maintain proper and transparent planning system in a financial institution. A team of the

company should evaluate their policies and calculate their value and applicability in terms of

income and losses (Gitman, Juchau and Flanagan, 2015). Economic performance of the company

is reliant on the authorized team.

Principal 5

operations.

Principal 2

Directors are accountable for managing, supervising, and seamless working of the governance

company. Authorizes of NAB is responsible for doing the work according to applied government

rules and policies moreover it works in given framework which is predefined according to the

suitability of the company (Cheng, Ioannou and Serafeim, 2014). Companies strategy and

policies are planned and executed by the directors and are highly responsible for organizations

profits and loss. Performance and actions of the members are evaluated by the authorities on the

regular terms.

Principal 3

Business conduct and ethics- It is the responsibility of managerial authorities to sustain a good

business performance, reliability, and ethical behaviour. Authority should build up, retain and

put into operation a proficient interest plan (McCahery, Sautner and Starks, 2016). Authorities

have a duty to minimize and avoid conflict of interest moreover maintain their personal and

business affairs for the betterment of the governance. Authorities are legally responsible for

working for the better interest of the company.

Principal 4

Accountability for reviewing the organization's value and position managing authorities should

maintain proper and transparent planning system in a financial institution. A team of the

company should evaluate their policies and calculate their value and applicability in terms of

income and losses (Gitman, Juchau and Flanagan, 2015). Economic performance of the company

is reliant on the authorized team.

Principal 5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk management every business or company is directly affected by threats and risk, therefore

managing authorities should provide a good risk management plans that measures and control

the losses by the predefined way. NAB authorities are responsible for managing risk and flaws of

the company. The senior executive should help to manage risk by determining the companies

risk apatite, developing terms and policies, procedures, and control methods for identifying the

risk and managing the losses faced by the company.

Disclosure and reporting the authorities should make sure that appropriate and impartial

confession to stakeholders and seniors executives about the financial and economic position

should be made (Hong, Li and Minor, 2016). It is a duty of managing directors to hold the

information that the company has worked according to defined terms and policies and all the

officially authorized deadlines are met on time.

The study shows that corporate governance is particularly relevant when it comes to banking

institutions governance. Their norms for the banking and financial industry has considered

subsequent to the international economic reduction aroused by the conflict of the leading

companies of the world (Kraakman and Armour, 2017). Corporate governance can be widely

considered as the safeguarding of the interest of investors and an effective risk management

system.

managing authorities should provide a good risk management plans that measures and control

the losses by the predefined way. NAB authorities are responsible for managing risk and flaws of

the company. The senior executive should help to manage risk by determining the companies

risk apatite, developing terms and policies, procedures, and control methods for identifying the

risk and managing the losses faced by the company.

Disclosure and reporting the authorities should make sure that appropriate and impartial

confession to stakeholders and seniors executives about the financial and economic position

should be made (Hong, Li and Minor, 2016). It is a duty of managing directors to hold the

information that the company has worked according to defined terms and policies and all the

officially authorized deadlines are met on time.

The study shows that corporate governance is particularly relevant when it comes to banking

institutions governance. Their norms for the banking and financial industry has considered

subsequent to the international economic reduction aroused by the conflict of the leading

companies of the world (Kraakman and Armour, 2017). Corporate governance can be widely

considered as the safeguarding of the interest of investors and an effective risk management

system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Aras, G., 2016. A handbook of corporate governance and social responsibility. CRC Press.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic Management Journal, 35(1), pp.1-23.

Davies, A., 2016. Best practice in corporate governance: Building reputation and sustainable

success. Routledge.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hong, B., Li, Z. and Minor, D., 2016. Corporate governance and executive compensation for

corporate social responsibility. Journal of Business Ethics, 136(1), pp.199-213.

Kraakman, R. and Armour, J., 2017. The anatomy of corporate law: A comparative and

functional approach. Oxford University Press.

Larcker, D. and Tayan, B., 2015. Corporate governance matters A closer look at organizational

choices and their consequences. Pearson Education.

McCahery, J.A., Sautner, Z. and Starks, L.T., 2016. Behind the scenes: The corporate

governance preferences of institutional investors. The Journal of Finance, 71(6), pp.2905-2932.

Tricker, R.B. and Tricker, R.I., 2015. Corporate Governance: Principles, policies, and practices.

Oxford University Press, USA.

Aras, G., 2016. A handbook of corporate governance and social responsibility. CRC Press.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic Management Journal, 35(1), pp.1-23.

Davies, A., 2016. Best practice in corporate governance: Building reputation and sustainable

success. Routledge.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hong, B., Li, Z. and Minor, D., 2016. Corporate governance and executive compensation for

corporate social responsibility. Journal of Business Ethics, 136(1), pp.199-213.

Kraakman, R. and Armour, J., 2017. The anatomy of corporate law: A comparative and

functional approach. Oxford University Press.

Larcker, D. and Tayan, B., 2015. Corporate governance matters A closer look at organizational

choices and their consequences. Pearson Education.

McCahery, J.A., Sautner, Z. and Starks, L.T., 2016. Behind the scenes: The corporate

governance preferences of institutional investors. The Journal of Finance, 71(6), pp.2905-2932.

Tricker, R.B. and Tricker, R.I., 2015. Corporate Governance: Principles, policies, and practices.

Oxford University Press, USA.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.