Risk and Return Analysis: ABC Co. and XYZ Co. Investment Portfolio

VerifiedAdded on 2022/11/23

|4

|703

|296

Homework Assignment

AI Summary

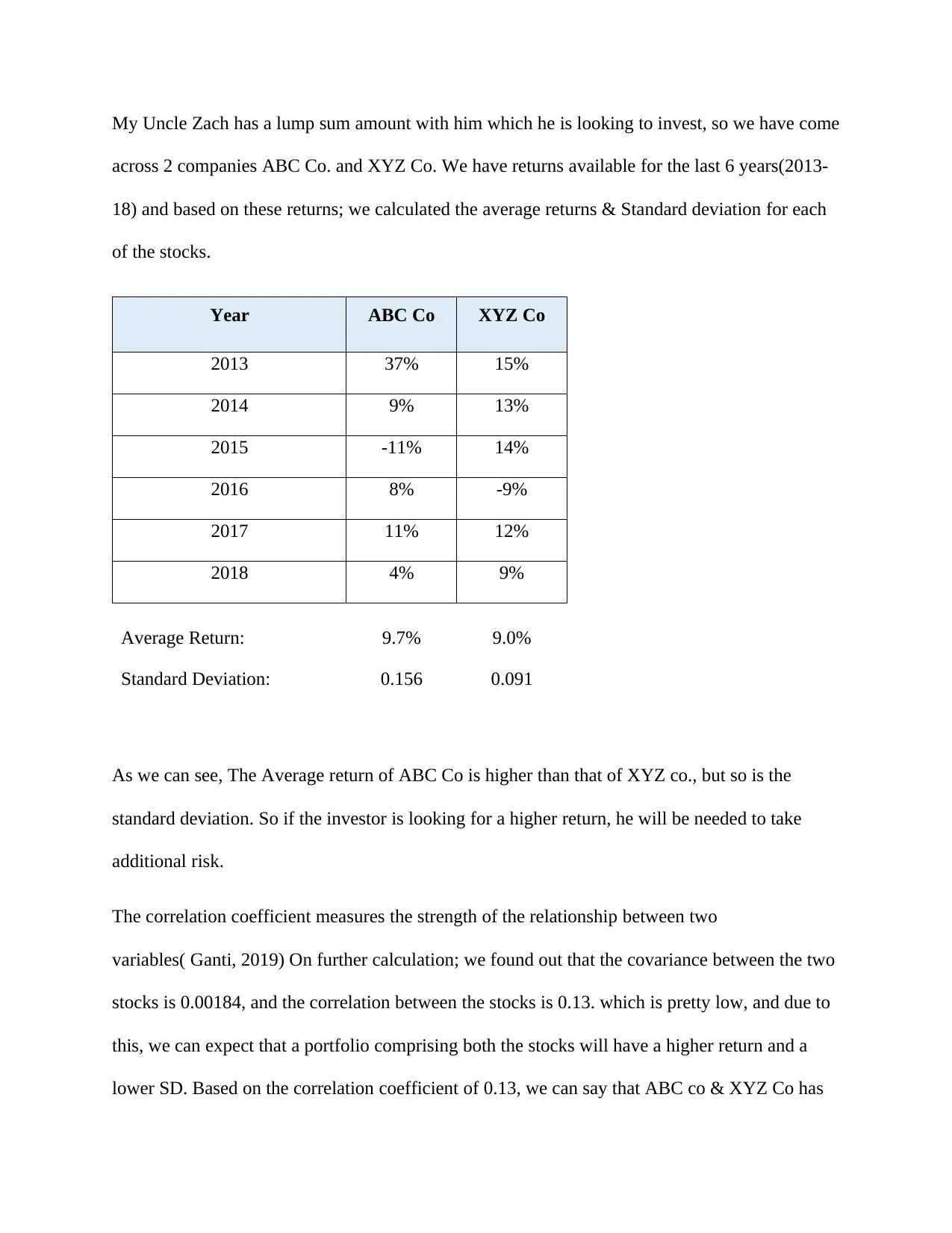

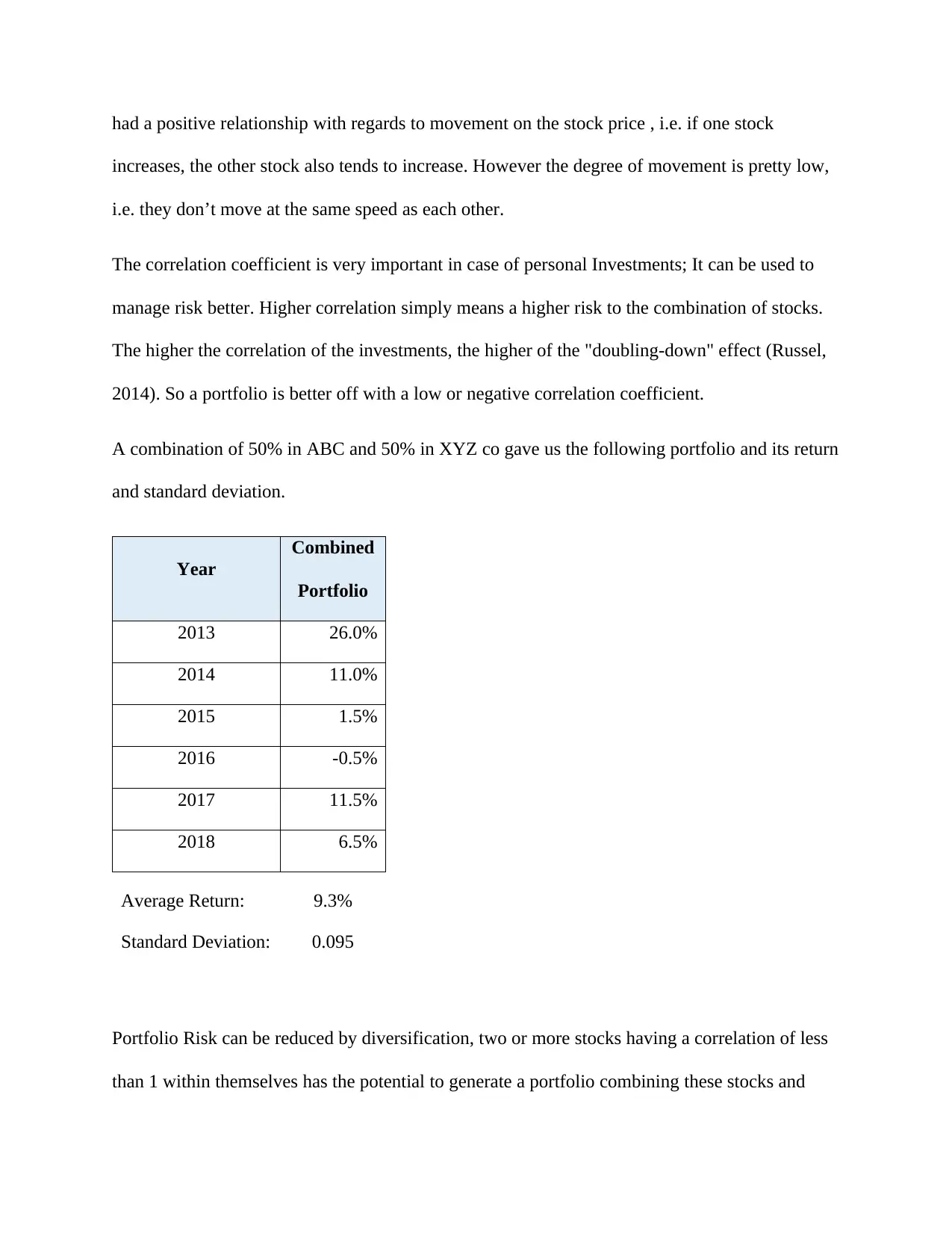

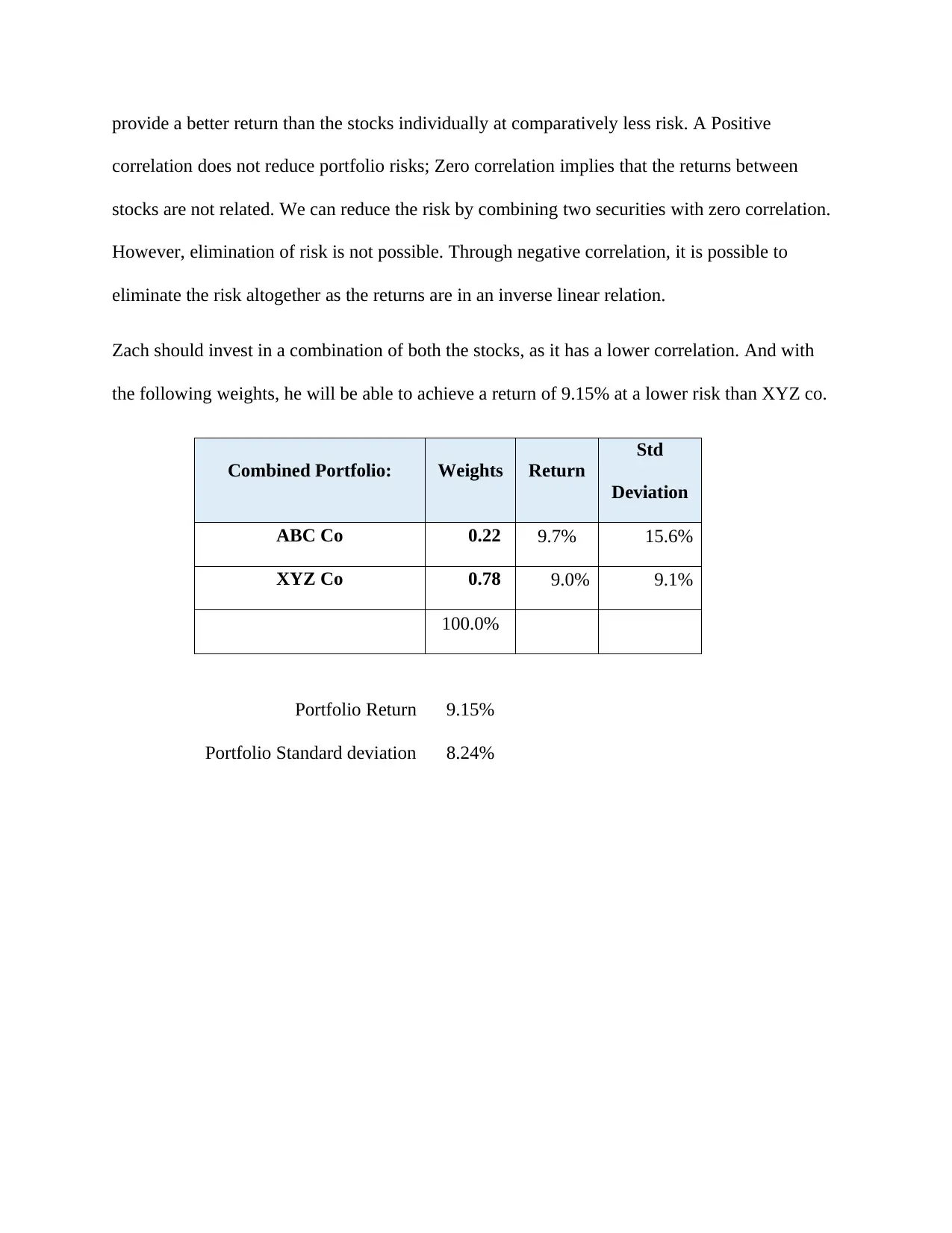

This assignment presents an analysis of two investment options, ABC Co. and XYZ Co., based on their historical returns from 2013 to 2018. The analysis calculates average returns, standard deviations, and the correlation coefficient to assess the risk and potential return of each stock. It explores the benefits of portfolio diversification, demonstrating how combining the two stocks can lead to a higher return with reduced risk compared to investing in either stock individually. The assignment suggests an optimal portfolio allocation, considering the correlation coefficient between the stocks, and discusses the importance of correlation in managing investment risk. The conclusion emphasizes the advantages of a diversified portfolio with a low correlation to achieve better risk-adjusted returns for investors. The document also contains references to several sources on asset allocation, diversification, and risk management.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.