Corporate Finance Report: Analysis of Risk, Return, and Portfolios

VerifiedAdded on 2019/10/30

|9

|1912

|327

Report

AI Summary

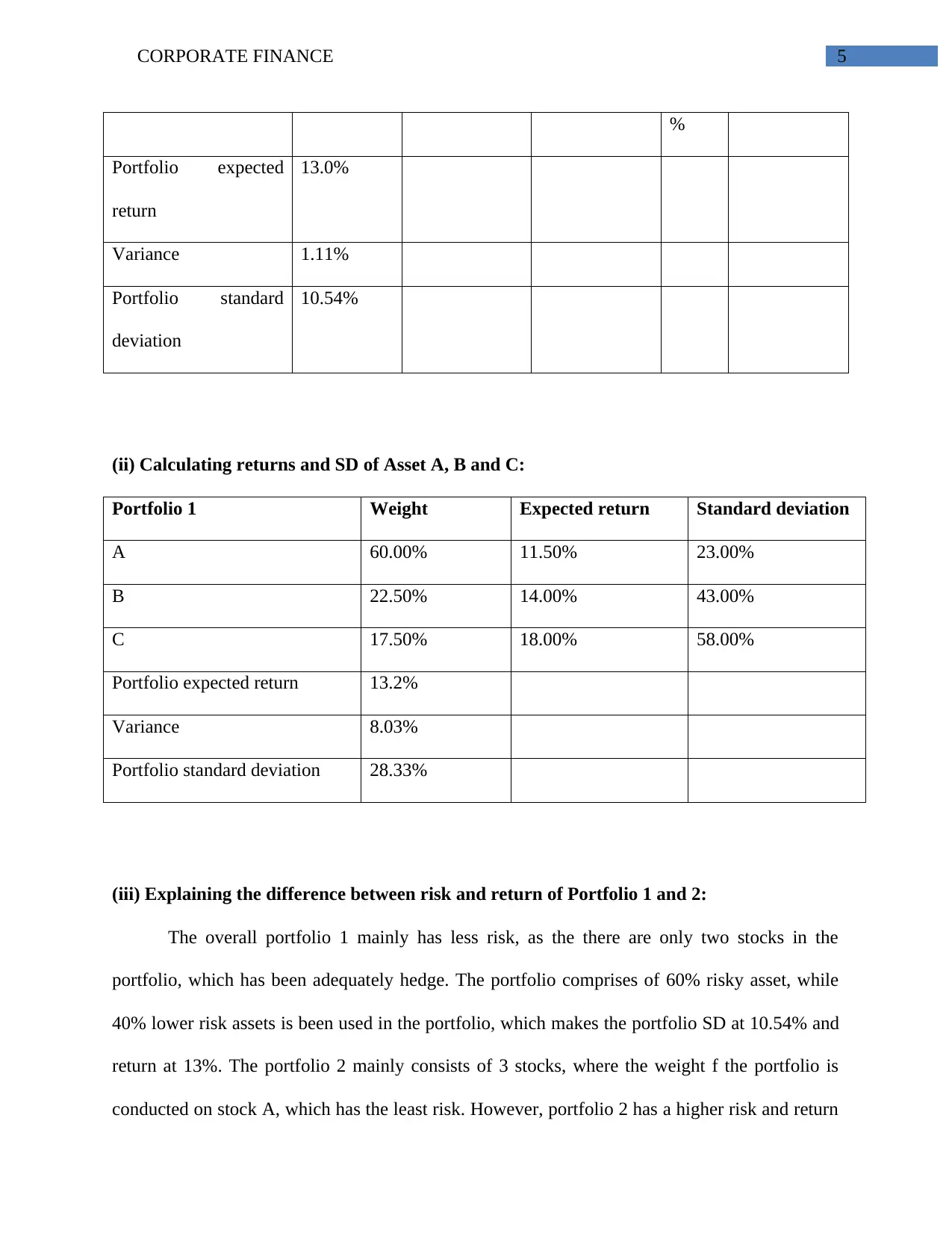

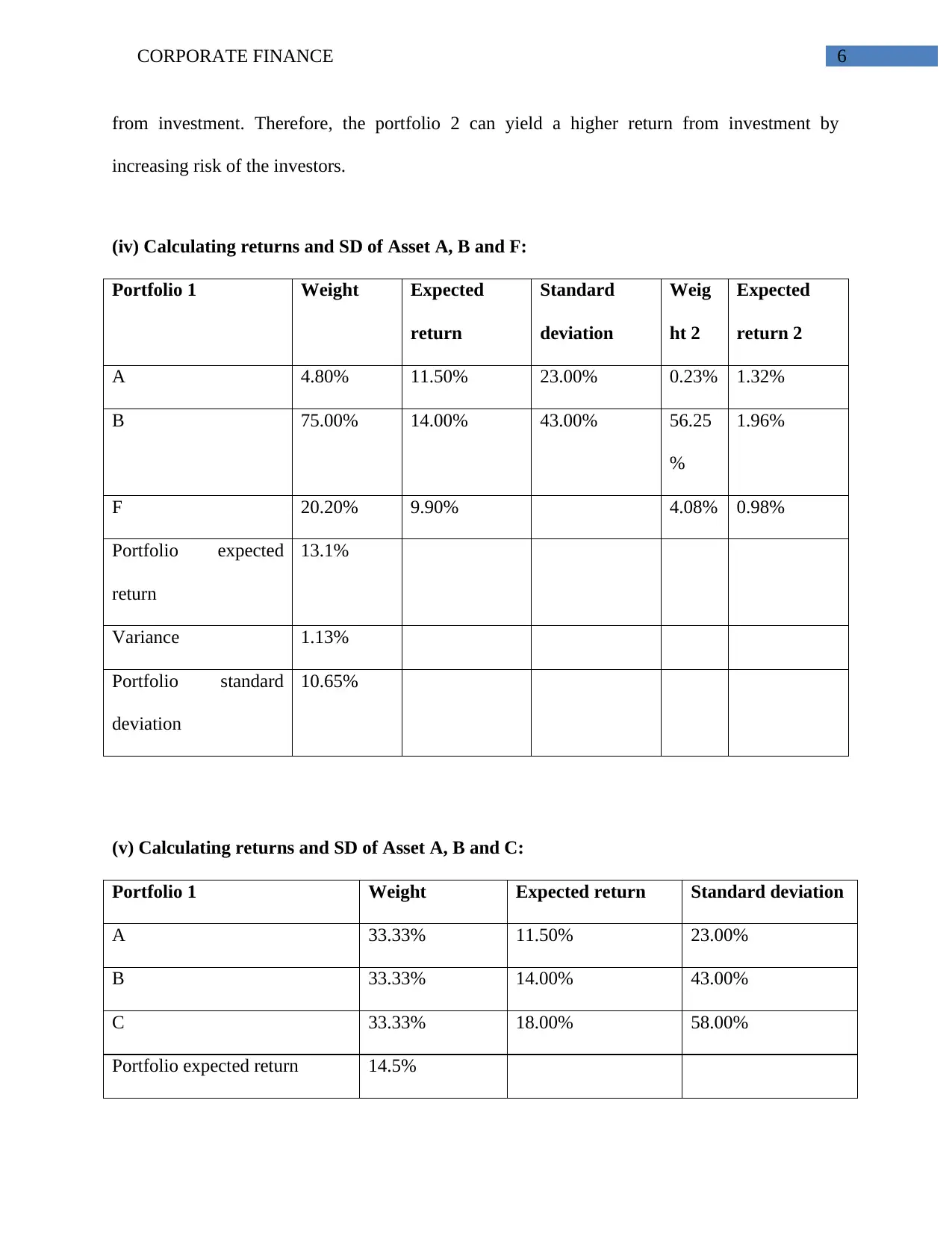

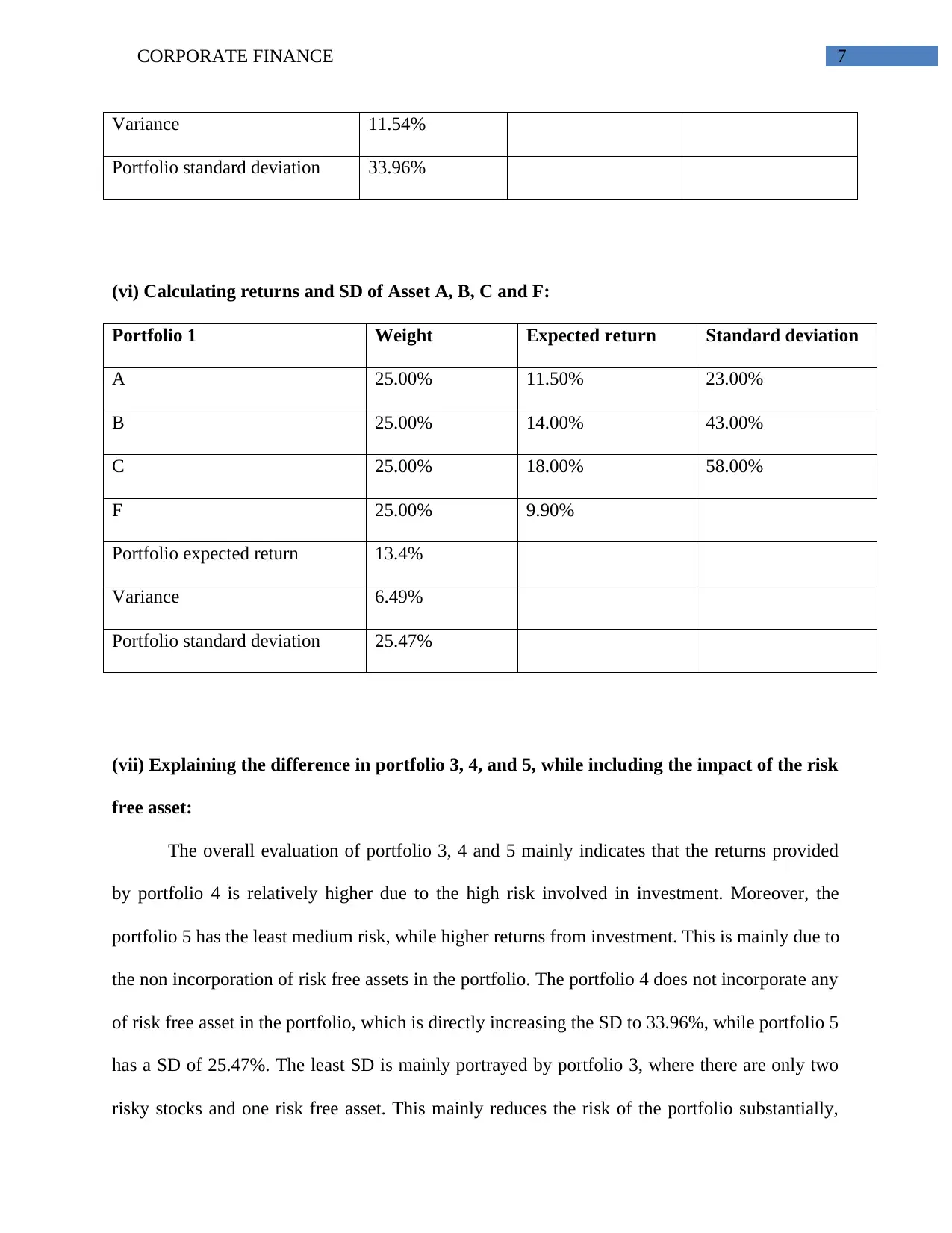

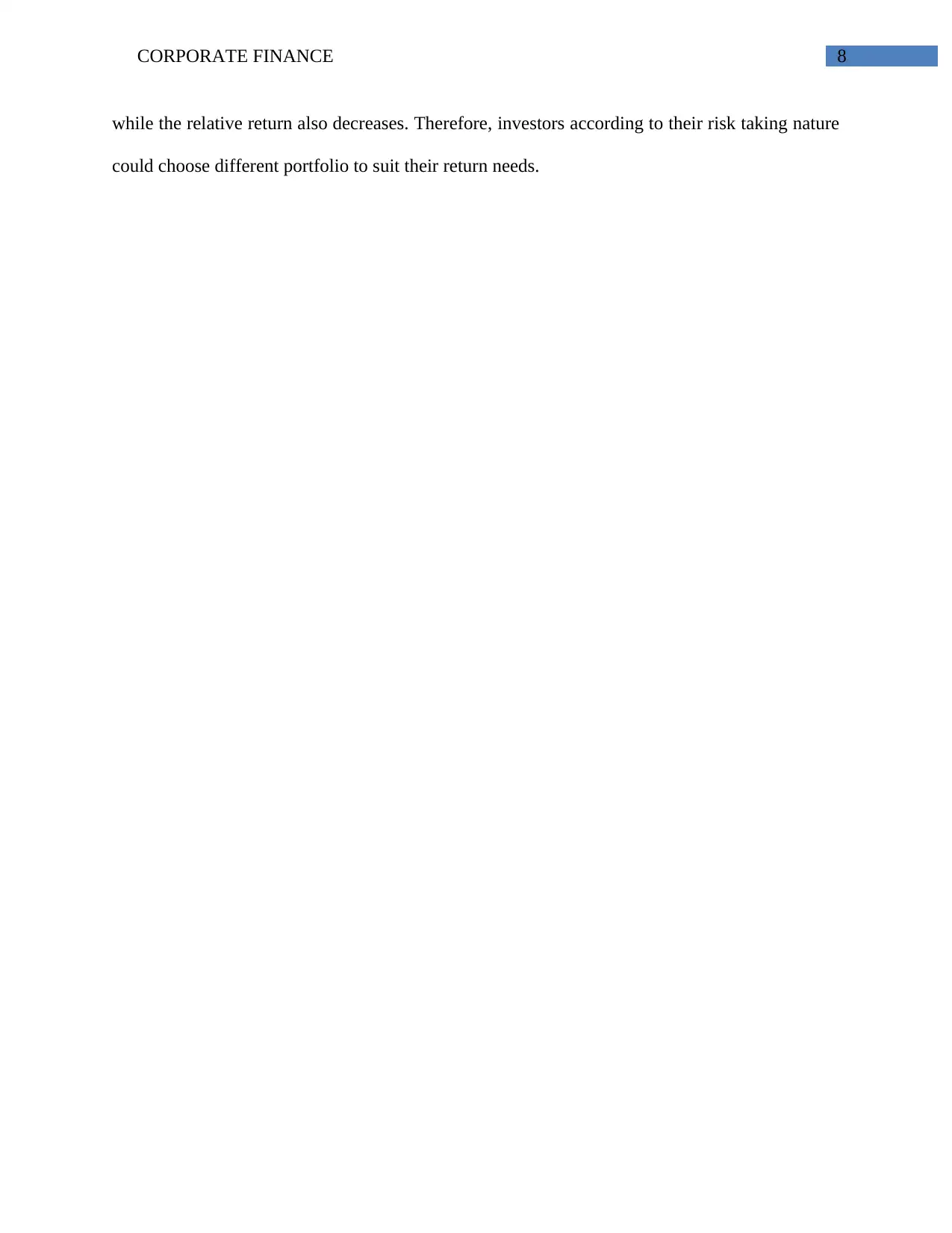

This report delves into key concepts of corporate finance, including risk assessment, return calculations, and portfolio management. The report begins by explaining how standard deviation is used to calculate the risk of shares and how adding more shares impacts portfolio risk and return. It also discusses the role of risk-free assets in portfolio risk calculation and distinguishes between systematic and unsystematic risk. Part 2 of the report provides detailed calculations of returns and standard deviations for different asset combinations and portfolios, analyzing the impact of diversification and the inclusion of a risk-free asset. The analysis includes comparisons between portfolios with varying levels of risk and return, offering insights into investment strategies. The report concludes with a synthesis of the findings, highlighting the trade-offs between risk and return in different portfolio configurations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.