BK7101 - Risk and Utility: Risk Management, Utility & Insurance

VerifiedAdded on 2023/06/04

|19

|4076

|489

Report

AI Summary

This report provides an in-depth analysis of risk and utility within the construction industry, focusing on insurance financing and risk management strategies. It explores the application of utility theory in assessing risks faced by construction workers, differentiating between skilled and clumsy builders. The report includes calculations for insurance premiums, maximum premium charges, and the evaluation of different coverage plans. It also addresses the implications of market failures in insurance coverage. The analysis uses a case study approach, applying mathematical models to determine optimal insurance strategies and coverage plans for construction firms. This document is available on Desklib, a platform offering a wide range of study resources, including past papers and solved assignments.

RISK AND UTILITY

Student’s Name

Risk and Utility

Course Studied

Unit Title

Unit Code

Professor’s Name

Institutional Affiliation

Department

Date

Student’s Name

Risk and Utility

Course Studied

Unit Title

Unit Code

Professor’s Name

Institutional Affiliation

Department

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Risk and Utility

Introduction

In the construction industry most of the workers incur a lot of risk either the worker is

skilled or not, thus methods of risk analysis have been implemented based on the theory of utility

(Kast, and Lapied, 2006). The theory focuses on the following sectors:

Economic situation data

Construction condition data

Seasonality

Supply and demand relationship

Apart from these factors decision making, utility function, records and probability are

very crucial. Utility function is a method that has a great impact for the decision makers that

include the site manager of construction, construction engineer who make a lot of risk.

In addition, for an effective construction key decisions have to be taken at different stages

to prevent dilemmas that may erupt. What is fundamental is the knowledge of making

decisions toward certain risk that may be incurred during the construction of a building.

Utility theory can be applied in these forms:

Ranking of the constructors

Economic history, lending of the consumers, small business operations

Transfer of risks, flexibility, scenario methods

Life cycle building

integrative management and standardization

socio-economic system qualitative evaluation

equilibrium and game theory

Construction of utility faces unprecedented disruption coming from all corners that may

include the global workforce challenges, improvement of safety measures, increasing adverse

weather conditions, infrastructure cyber-attacks and problems that arise from distributed

generation (Trevor, 2004). The construction industry has great impact on the global economy

thus represents 6% of the entire global GDP and there is an estimate of 180 million construction

workers in the entire world and 75% come from the developing countries. However, calamities

Introduction

In the construction industry most of the workers incur a lot of risk either the worker is

skilled or not, thus methods of risk analysis have been implemented based on the theory of utility

(Kast, and Lapied, 2006). The theory focuses on the following sectors:

Economic situation data

Construction condition data

Seasonality

Supply and demand relationship

Apart from these factors decision making, utility function, records and probability are

very crucial. Utility function is a method that has a great impact for the decision makers that

include the site manager of construction, construction engineer who make a lot of risk.

In addition, for an effective construction key decisions have to be taken at different stages

to prevent dilemmas that may erupt. What is fundamental is the knowledge of making

decisions toward certain risk that may be incurred during the construction of a building.

Utility theory can be applied in these forms:

Ranking of the constructors

Economic history, lending of the consumers, small business operations

Transfer of risks, flexibility, scenario methods

Life cycle building

integrative management and standardization

socio-economic system qualitative evaluation

equilibrium and game theory

Construction of utility faces unprecedented disruption coming from all corners that may

include the global workforce challenges, improvement of safety measures, increasing adverse

weather conditions, infrastructure cyber-attacks and problems that arise from distributed

generation (Trevor, 2004). The construction industry has great impact on the global economy

thus represents 6% of the entire global GDP and there is an estimate of 180 million construction

workers in the entire world and 75% come from the developing countries. However, calamities

that faced during the construction have great impact in the economy thus construction utility has

been stagnant for the last 20 years.

Nevertheless, construction market has risk and finance shortage and these suppresses

levels of productivity, cost and waste introduction, low ability of industries to add value to the

built environment.

These are some of the risk that an individual may be facing that may include: natural

disasters, asset prices volatility nature, liability creation and fear of losses if one may venture

into the business (Kassack, 2017). In business they are risks that are insurable, non-insurable,

avoidable and non-avoidable. These are the major types of risk that we have:

Enterprise risk

Fundamental and particular risk

Pure and speculative risk

Enterprise risk focuses on all the risk that are faced in a business enterprise that is

inclusive of the strategic risk, speculative risk, financial risk, pure risk and operational risk.

Fundamental economy affects the entire economy and a large population of people while the

particular risk affects the individual people. Moreover, in speculative risk there is possibility of

making both profit and losses at the same time while pure risk only gives one platform of either

masking profit or loss. maximum amount of cash to be insured

1.0 Utility premium Assessment

In order for a building to be erected in an appropriate manner builders play major role in

it. In most of the occasions contractors and the investors that may have great interest in the

construction industry have major challenge in identifying between a clumsy builder and a best

builder. Clumsy builders may have obtained the ideas and gathered knowledge in the field of

construction without going to the technical institutions for proper training and certification. The

been stagnant for the last 20 years.

Nevertheless, construction market has risk and finance shortage and these suppresses

levels of productivity, cost and waste introduction, low ability of industries to add value to the

built environment.

These are some of the risk that an individual may be facing that may include: natural

disasters, asset prices volatility nature, liability creation and fear of losses if one may venture

into the business (Kassack, 2017). In business they are risks that are insurable, non-insurable,

avoidable and non-avoidable. These are the major types of risk that we have:

Enterprise risk

Fundamental and particular risk

Pure and speculative risk

Enterprise risk focuses on all the risk that are faced in a business enterprise that is

inclusive of the strategic risk, speculative risk, financial risk, pure risk and operational risk.

Fundamental economy affects the entire economy and a large population of people while the

particular risk affects the individual people. Moreover, in speculative risk there is possibility of

making both profit and losses at the same time while pure risk only gives one platform of either

masking profit or loss. maximum amount of cash to be insured

1.0 Utility premium Assessment

In order for a building to be erected in an appropriate manner builders play major role in

it. In most of the occasions contractors and the investors that may have great interest in the

construction industry have major challenge in identifying between a clumsy builder and a best

builder. Clumsy builders may have obtained the ideas and gathered knowledge in the field of

construction without going to the technical institutions for proper training and certification. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

construction ideas from a clumsy builder in most occasions are obtained from observation from

more skilled builders.

Moreover, the construction managers and engineers should adopt and put into practice

the art of hiring construction firms that have builders who have undergone training in recognized

institutions that know the risk and challenges’ that an individual may encounter during

construction (Knox, Pollock, and Ritchie, 2011). The construction work is costly in most

scenarios if the amateurs are given duty and make mistakes thus it vital to find experienced and

skilled builders in that field of work that offer a clear competitive rates.

The calculations bellow illustrates the solutions to most of the questions asked under the

utility assessment section of this paper.

a) How Much Is Charged by Safe Build for Each Type of $1 In Medical

Coverage

Following the fact that Safe Build has to act fairly, charges on clumsy and skilled builders should

consider the probabilities of involvement into an accident of the two categories. However, the

probability of involvement into an accident is inversely proportional to the charges made.

Therefore, give $1 then:

The skilled builders should be charged

(100%-90%)/ 100*1

0.1*1

=$0.1

On the other hand, the clumsy boulders should be charged as follows

(100%-30%)/100*1

more skilled builders.

Moreover, the construction managers and engineers should adopt and put into practice

the art of hiring construction firms that have builders who have undergone training in recognized

institutions that know the risk and challenges’ that an individual may encounter during

construction (Knox, Pollock, and Ritchie, 2011). The construction work is costly in most

scenarios if the amateurs are given duty and make mistakes thus it vital to find experienced and

skilled builders in that field of work that offer a clear competitive rates.

The calculations bellow illustrates the solutions to most of the questions asked under the

utility assessment section of this paper.

a) How Much Is Charged by Safe Build for Each Type of $1 In Medical

Coverage

Following the fact that Safe Build has to act fairly, charges on clumsy and skilled builders should

consider the probabilities of involvement into an accident of the two categories. However, the

probability of involvement into an accident is inversely proportional to the charges made.

Therefore, give $1 then:

The skilled builders should be charged

(100%-90%)/ 100*1

0.1*1

=$0.1

On the other hand, the clumsy boulders should be charged as follows

(100%-30%)/100*1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.7*1

=$0.7

B) Insurance Quantity

Uclumsy = (Cclumsy).7 utility for consumption of clumsy builder

Uskillful = (Cskillful).5 utility for consumption of skilled builders

There is an actuarially fair premium charge for insurances if safe build could faultlessly

be able to classify if each builder either clumsy or skilled the premium charges could vary.

Nevertheless, both builders would suffer $50 remedial bills when engaged in an accident and the

chances of either of the builders to be engaged in accident is 50%

Clumsy builders = 90% chances of getting into an accident

Skilled builder = 30% chances of getting into an accident

In addition, there is an increment or an overtime pay of cash $100 for evening jobs and

the builders use their earnings firstly to offset their medicals bills before spending the cash for

other basic needs.

Probability of a builder being clumsy or skilled = P(C S) = P (C) P (S)

Probability of clumsy builder getting into an accident and paying medical bills= P(B C) =

P(B) P(C)

Insurance Bought by Clumsy

90% $100 =?

90/100× $50 =$90

Insurance Bought by Skilled

30%*$100

30/100*100

=$30

C) Remaining Income for Consumption if they Get Involved in the Accident

=$0.7

B) Insurance Quantity

Uclumsy = (Cclumsy).7 utility for consumption of clumsy builder

Uskillful = (Cskillful).5 utility for consumption of skilled builders

There is an actuarially fair premium charge for insurances if safe build could faultlessly

be able to classify if each builder either clumsy or skilled the premium charges could vary.

Nevertheless, both builders would suffer $50 remedial bills when engaged in an accident and the

chances of either of the builders to be engaged in accident is 50%

Clumsy builders = 90% chances of getting into an accident

Skilled builder = 30% chances of getting into an accident

In addition, there is an increment or an overtime pay of cash $100 for evening jobs and

the builders use their earnings firstly to offset their medicals bills before spending the cash for

other basic needs.

Probability of a builder being clumsy or skilled = P(C S) = P (C) P (S)

Probability of clumsy builder getting into an accident and paying medical bills= P(B C) =

P(B) P(C)

Insurance Bought by Clumsy

90% $100 =?

90/100× $50 =$90

Insurance Bought by Skilled

30%*$100

30/100*100

=$30

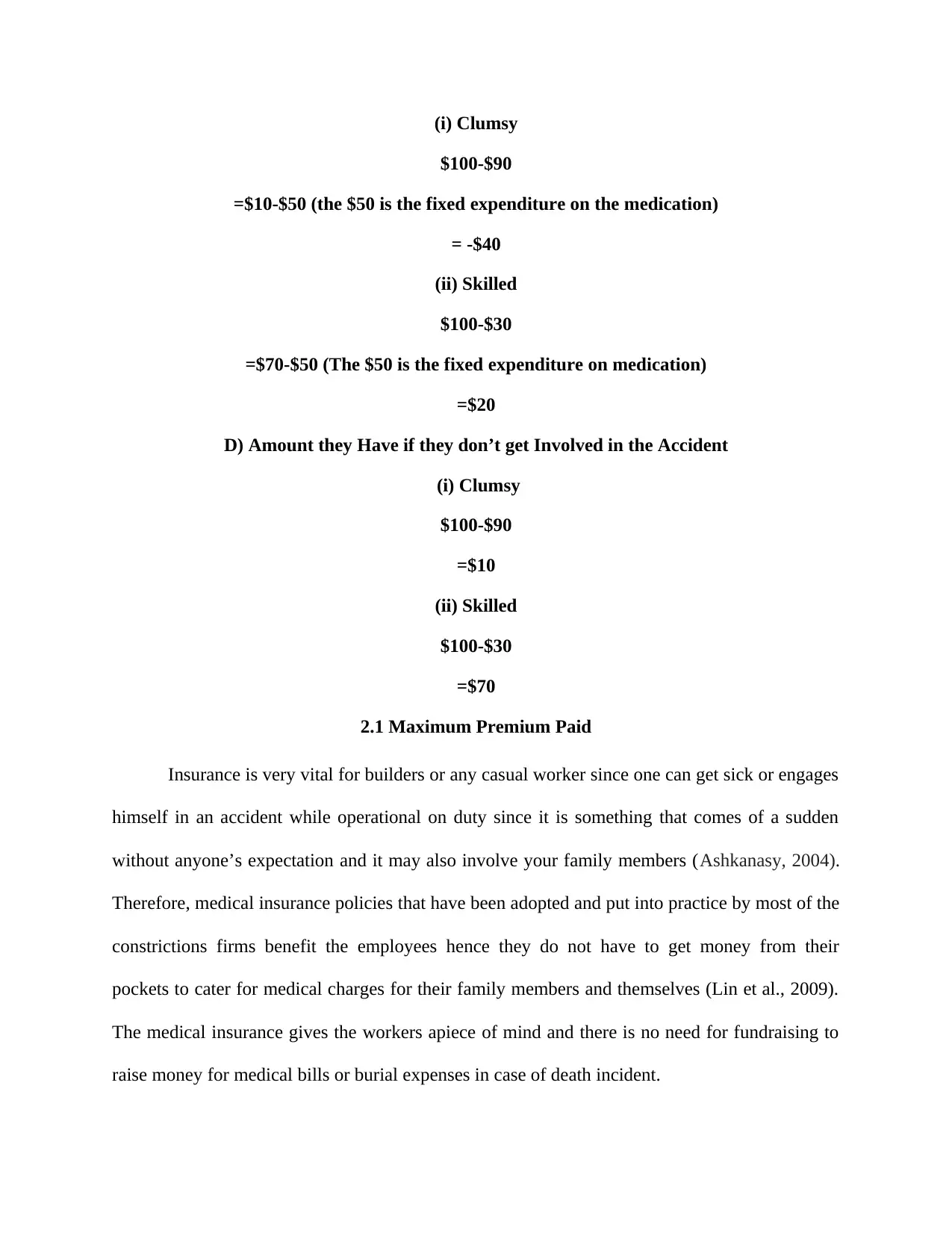

C) Remaining Income for Consumption if they Get Involved in the Accident

(i) Clumsy

$100-$90

=$10-$50 (the $50 is the fixed expenditure on the medication)

= -$40

(ii) Skilled

$100-$30

=$70-$50 (The $50 is the fixed expenditure on medication)

=$20

D) Amount they Have if they don’t get Involved in the Accident

(i) Clumsy

$100-$90

=$10

(ii) Skilled

$100-$30

=$70

2.1 Maximum Premium Paid

Insurance is very vital for builders or any casual worker since one can get sick or engages

himself in an accident while operational on duty since it is something that comes of a sudden

without anyone’s expectation and it may also involve your family members (Ashkanasy, 2004).

Therefore, medical insurance policies that have been adopted and put into practice by most of the

constrictions firms benefit the employees hence they do not have to get money from their

pockets to cater for medical charges for their family members and themselves (Lin et al., 2009).

The medical insurance gives the workers apiece of mind and there is no need for fundraising to

raise money for medical bills or burial expenses in case of death incident.

$100-$90

=$10-$50 (the $50 is the fixed expenditure on the medication)

= -$40

(ii) Skilled

$100-$30

=$70-$50 (The $50 is the fixed expenditure on medication)

=$20

D) Amount they Have if they don’t get Involved in the Accident

(i) Clumsy

$100-$90

=$10

(ii) Skilled

$100-$30

=$70

2.1 Maximum Premium Paid

Insurance is very vital for builders or any casual worker since one can get sick or engages

himself in an accident while operational on duty since it is something that comes of a sudden

without anyone’s expectation and it may also involve your family members (Ashkanasy, 2004).

Therefore, medical insurance policies that have been adopted and put into practice by most of the

constrictions firms benefit the employees hence they do not have to get money from their

pockets to cater for medical charges for their family members and themselves (Lin et al., 2009).

The medical insurance gives the workers apiece of mind and there is no need for fundraising to

raise money for medical bills or burial expenses in case of death incident.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

When selecting the suitable medical insurance policies, these are some of the observations that

one should put emphasis on:

medical treatment that cover both inpatient and outpatient treatment

the one that has the last expense cover that caters for the funeral expenses

E(U) clumsy, No insurance E(U) skilled No insurance

Following the case provided, below are the calculations for the maximum amount pays

for each boulder in order to attain full insurance for the cost incurred during the accident.

CLUMMSY

$100 overtime

90/100× $50 =$45

10/100 $100 =$10

$45 +$10 =$55

SKILLLED

(30/100 $ 50=$15) + (70/100$50 =$35)

=$50

The amount of insurance cash will differ greatly since complete insurance is caters for all

the entire damage cost on the commodity to be insured thus the premium rates of insurance will

be high compared to the actuarially insurance that the consumers or the customers expect fair

premium charges that will be equal to the compensations that will be received in case of damage.

2.2 Maximum Premium Charged

It has come to the senses of majority of the builder that our health is fundamental and

irreplaceable as well hence one must take good care of it in order to have a long and productive

life. Since one cannot predict the eventuality of sickness or accident it is better have health

one should put emphasis on:

medical treatment that cover both inpatient and outpatient treatment

the one that has the last expense cover that caters for the funeral expenses

E(U) clumsy, No insurance E(U) skilled No insurance

Following the case provided, below are the calculations for the maximum amount pays

for each boulder in order to attain full insurance for the cost incurred during the accident.

CLUMMSY

$100 overtime

90/100× $50 =$45

10/100 $100 =$10

$45 +$10 =$55

SKILLLED

(30/100 $ 50=$15) + (70/100$50 =$35)

=$50

The amount of insurance cash will differ greatly since complete insurance is caters for all

the entire damage cost on the commodity to be insured thus the premium rates of insurance will

be high compared to the actuarially insurance that the consumers or the customers expect fair

premium charges that will be equal to the compensations that will be received in case of damage.

2.2 Maximum Premium Charged

It has come to the senses of majority of the builder that our health is fundamental and

irreplaceable as well hence one must take good care of it in order to have a long and productive

life. Since one cannot predict the eventuality of sickness or accident it is better have health

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

insurance and not use it rather not have the insurance but yawn for treatment when there is

shortage of cash.

Majority of the companies are trying to put measures that will ensure that the medical

insurance is affordable to all the employees (Pilbeam, 2018). Costs and premiums matter a lot

when choosing for best medical insurance cover but that does not mean that the builders should

rush for a lower rates insurance cover since it may provide an inferior medical cover at that low

cost. It’s advisable to closely and keenly examine the medical covers by making comparisons

before making any haste decision thus by ensuring that you get most the value of your money

(Deniz, 2006).

E(U) clumsy, full insurance E(U) skilled full insurance

Following the provided sample, below is the maximum premium charged by the sage.

ii) Maximum amount that sage build can charge

P= Max pUAccident + (1-pU) NoAccident

90/100× $50 =$45

70/100$50 =$35

$45 $35

=$10

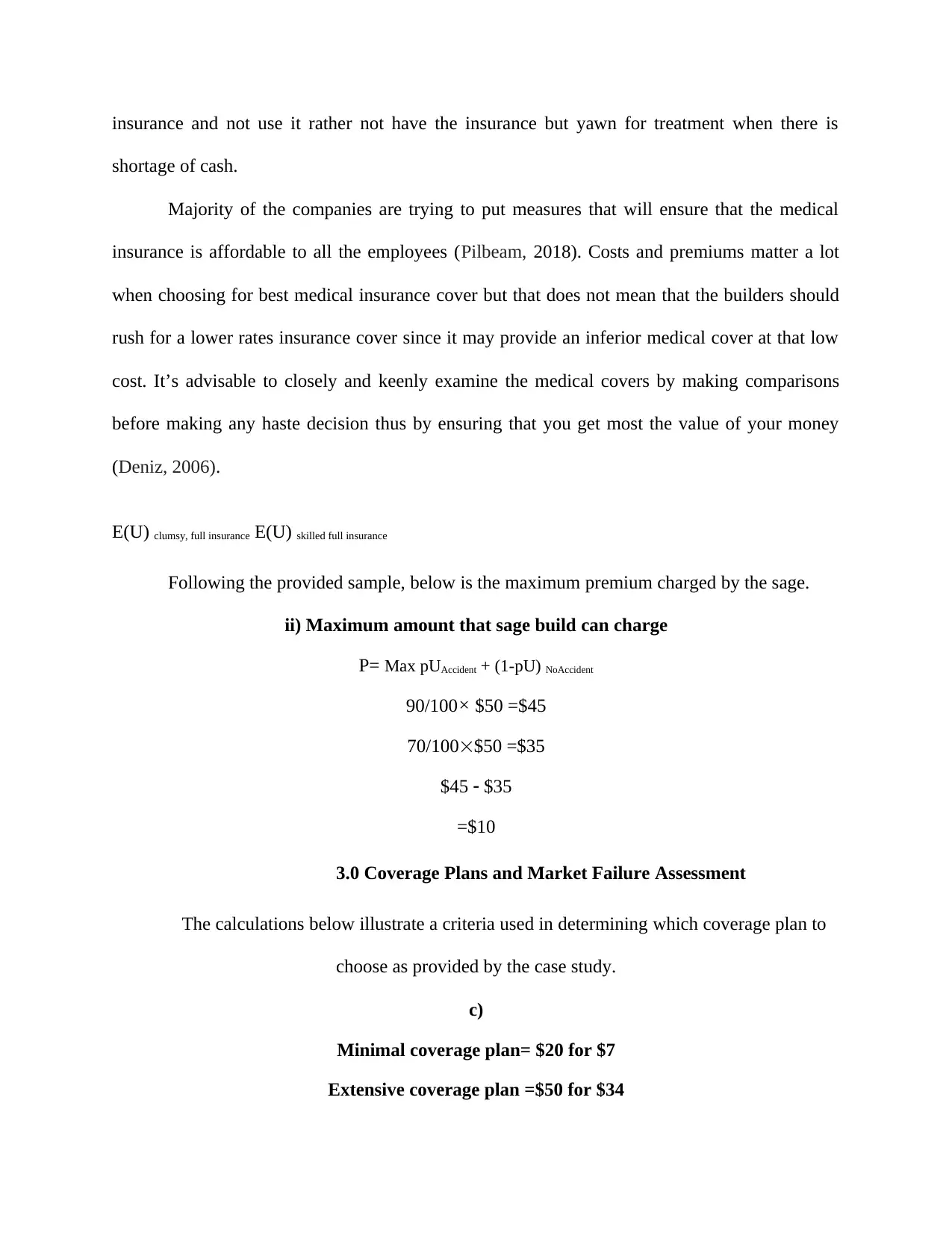

3.0 Coverage Plans and Market Failure Assessment

The calculations below illustrate a criteria used in determining which coverage plan to

choose as provided by the case study.

c)

Minimal coverage plan= $20 for $7

Extensive coverage plan =$50 for $34

shortage of cash.

Majority of the companies are trying to put measures that will ensure that the medical

insurance is affordable to all the employees (Pilbeam, 2018). Costs and premiums matter a lot

when choosing for best medical insurance cover but that does not mean that the builders should

rush for a lower rates insurance cover since it may provide an inferior medical cover at that low

cost. It’s advisable to closely and keenly examine the medical covers by making comparisons

before making any haste decision thus by ensuring that you get most the value of your money

(Deniz, 2006).

E(U) clumsy, full insurance E(U) skilled full insurance

Following the provided sample, below is the maximum premium charged by the sage.

ii) Maximum amount that sage build can charge

P= Max pUAccident + (1-pU) NoAccident

90/100× $50 =$45

70/100$50 =$35

$45 $35

=$10

3.0 Coverage Plans and Market Failure Assessment

The calculations below illustrate a criteria used in determining which coverage plan to

choose as provided by the case study.

c)

Minimal coverage plan= $20 for $7

Extensive coverage plan =$50 for $34

EXTENSIVE PLAN

SKILLED CLUMMSY TOTALS

OFFERS (30×50 ¿11 (9050)1 21,000

EXPENSE (7034)11 (1034)1 26,520

WEIGHTED TOTAL

OFFER

-5520

MINIMAL COVERAGE PLAN

SKILLED CLUMMSY TOTAL

OFFERS (3020)11 (9020)1 8400

EXPENSE (707)11 (107)1 6460

WEIGHTED

TOTALS OFFER

2940

In the table above, its fundamental to find out the weighted total offer of the two

premiums before deciding on which one to pick. The weighted total offer is found from

subtracting the expenses from the total offers. The total offer and expenses on the other hand are

determined by adding the totals of the skilled builders to the totals of the clumsy builders across

the column. However, its fundamental to consider the composition ratio of the clumsy against the

skilled builders in the company. Therefore, considering the case provided, the skilled builders are

eleven times as much as the clumsy boulders. The totals of the offers across the columns are

determined by multiplying the probability by the insurance coverage by the ratio value i.e.

30*20*11 respectively for the skilled boulders. On the other side the expense totals for each cell

are found by multiplying the probability by the insurance cost by the ratio value i.e. 10*7*1

respectively for the clumsy boulders.

Therefore, following the weighted total offers, the company is likely to take on the

minimum coverage plan rather than the extensive coverage plan as per the size of the values in

the cells. Under normal conditions, it will be irrational for the company to incur a lot of

insurance cost while the largest percentage of its members are skilled i.e. lower chances of

SKILLED CLUMMSY TOTALS

OFFERS (30×50 ¿11 (9050)1 21,000

EXPENSE (7034)11 (1034)1 26,520

WEIGHTED TOTAL

OFFER

-5520

MINIMAL COVERAGE PLAN

SKILLED CLUMMSY TOTAL

OFFERS (3020)11 (9020)1 8400

EXPENSE (707)11 (107)1 6460

WEIGHTED

TOTALS OFFER

2940

In the table above, its fundamental to find out the weighted total offer of the two

premiums before deciding on which one to pick. The weighted total offer is found from

subtracting the expenses from the total offers. The total offer and expenses on the other hand are

determined by adding the totals of the skilled builders to the totals of the clumsy builders across

the column. However, its fundamental to consider the composition ratio of the clumsy against the

skilled builders in the company. Therefore, considering the case provided, the skilled builders are

eleven times as much as the clumsy boulders. The totals of the offers across the columns are

determined by multiplying the probability by the insurance coverage by the ratio value i.e.

30*20*11 respectively for the skilled boulders. On the other side the expense totals for each cell

are found by multiplying the probability by the insurance cost by the ratio value i.e. 10*7*1

respectively for the clumsy boulders.

Therefore, following the weighted total offers, the company is likely to take on the

minimum coverage plan rather than the extensive coverage plan as per the size of the values in

the cells. Under normal conditions, it will be irrational for the company to incur a lot of

insurance cost while the largest percentage of its members are skilled i.e. lower chances of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

insurance. In such a case, it’s advisable for the company to secure less insurance coverage at a

lower cost since the company has lower probability for accidents.

Coverage plan is core for Sale builders and any investor regardless of it being minimal or

extensive plan. Suitable insurance plan is key mechanisms that have enabled societies and

organizations to be able to manage risk over a significant number of years. Insurance provides an

efficient channel of managing risk by providing both regulations of increasing risk behavior and

material damage compensation (Buchholz et al., 2006). Private insurance is a sector that was

established long ago within modern service economies and welfare organizations that has been

merged by co operations that are into making profits. Furthermore, these private insurance

organizations provide a wide range of financial support and adequate services to their clients.

Modern capitalist societies cannot operate without insurance either privately or provided by the

state since it provides a platform of risk taking and provides financial safety in case of any

uncertainty.

Nevertheless, market failure can be described any feature in both local and international

market that reduces the locative efficiency thus causes the resources to be expanded and

utilized in a way that does not maximize overall benefit to the society (Noe, et al., 2006).

Government intervention can increase economic welfare benefit in cases like that. Failure

market in the society has been triggered by the following factors:

Incomplete markets

Information asymmetries

Failure of competition

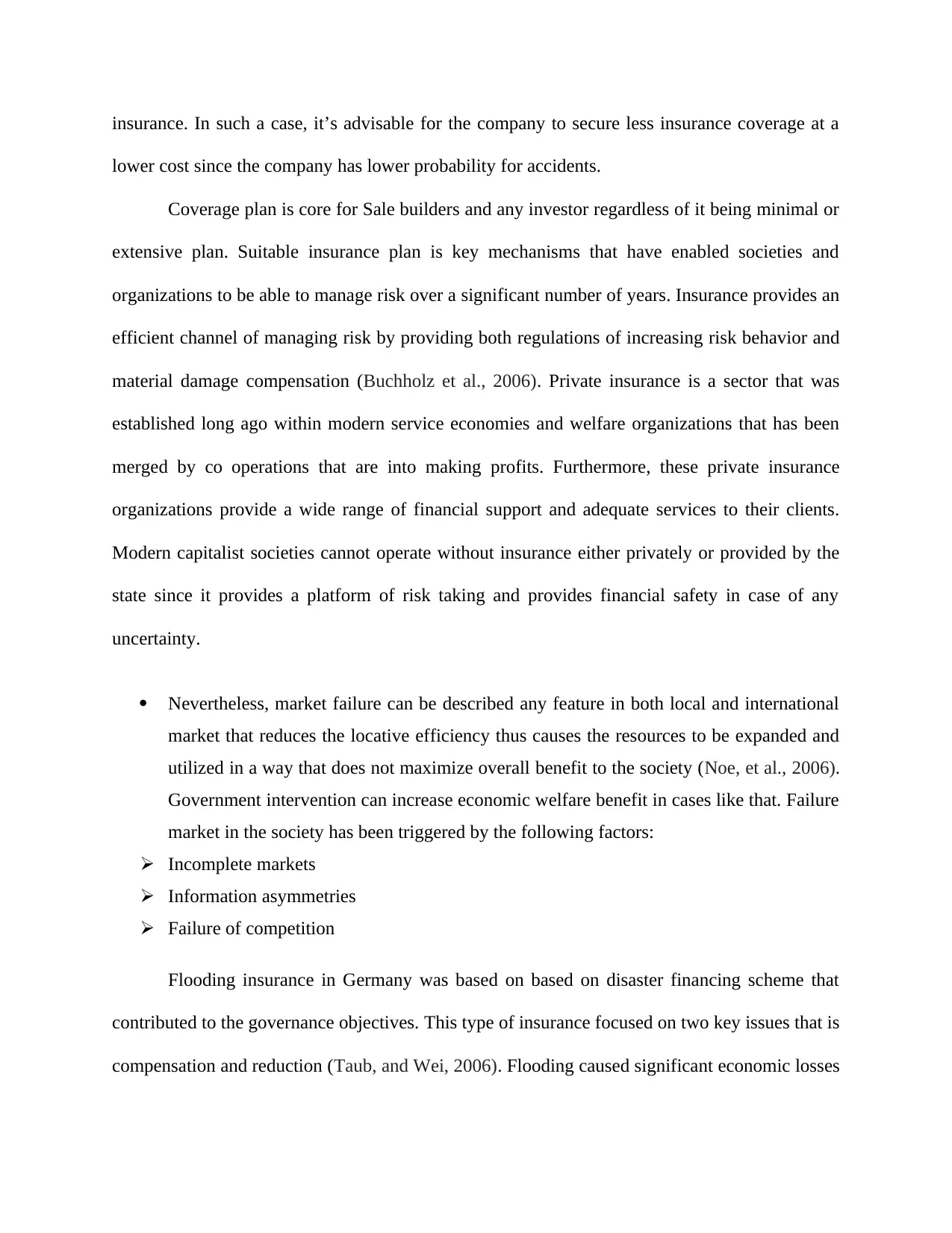

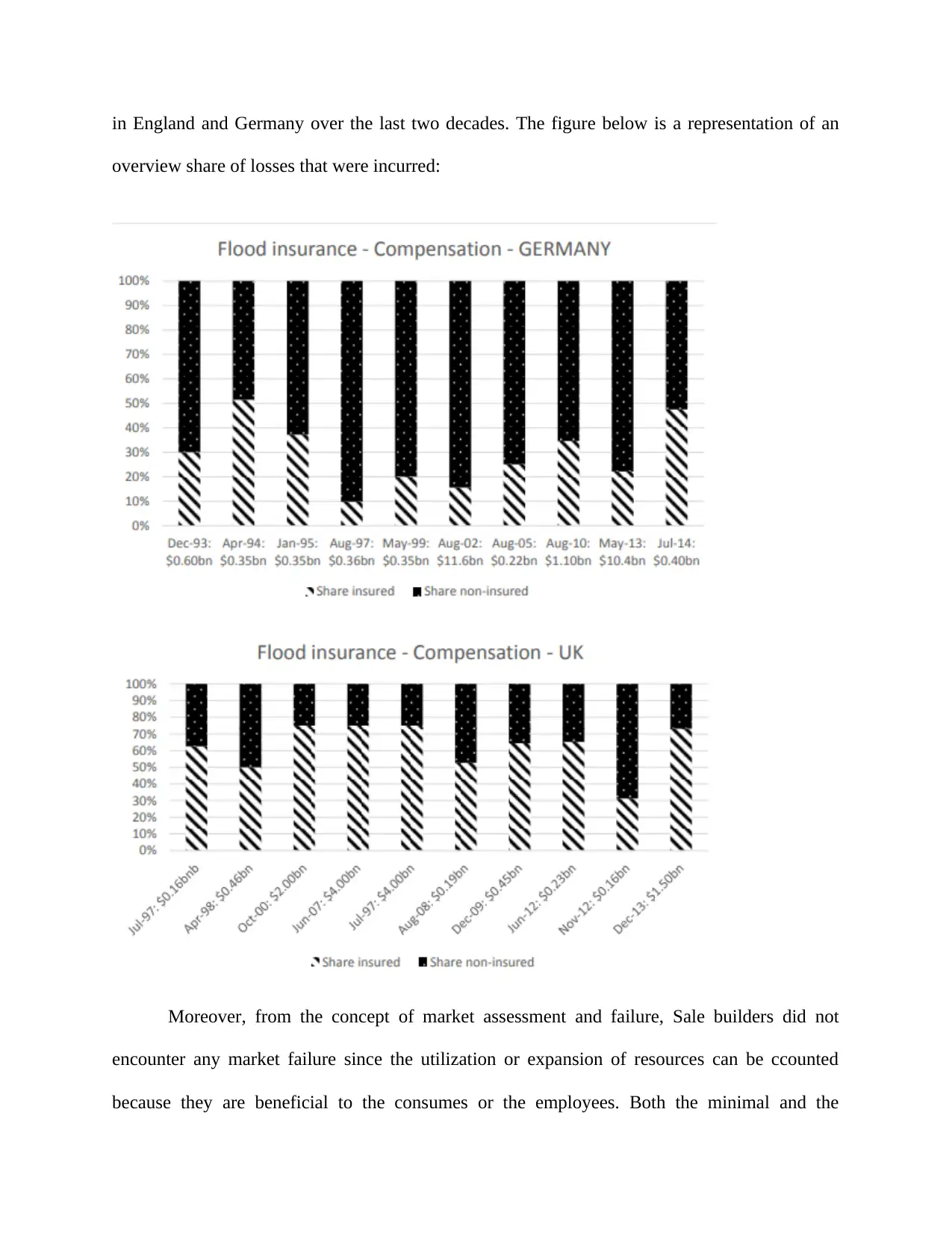

Flooding insurance in Germany was based on based on disaster financing scheme that

contributed to the governance objectives. This type of insurance focused on two key issues that is

compensation and reduction (Taub, and Wei, 2006). Flooding caused significant economic losses

lower cost since the company has lower probability for accidents.

Coverage plan is core for Sale builders and any investor regardless of it being minimal or

extensive plan. Suitable insurance plan is key mechanisms that have enabled societies and

organizations to be able to manage risk over a significant number of years. Insurance provides an

efficient channel of managing risk by providing both regulations of increasing risk behavior and

material damage compensation (Buchholz et al., 2006). Private insurance is a sector that was

established long ago within modern service economies and welfare organizations that has been

merged by co operations that are into making profits. Furthermore, these private insurance

organizations provide a wide range of financial support and adequate services to their clients.

Modern capitalist societies cannot operate without insurance either privately or provided by the

state since it provides a platform of risk taking and provides financial safety in case of any

uncertainty.

Nevertheless, market failure can be described any feature in both local and international

market that reduces the locative efficiency thus causes the resources to be expanded and

utilized in a way that does not maximize overall benefit to the society (Noe, et al., 2006).

Government intervention can increase economic welfare benefit in cases like that. Failure

market in the society has been triggered by the following factors:

Incomplete markets

Information asymmetries

Failure of competition

Flooding insurance in Germany was based on based on disaster financing scheme that

contributed to the governance objectives. This type of insurance focused on two key issues that is

compensation and reduction (Taub, and Wei, 2006). Flooding caused significant economic losses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in England and Germany over the last two decades. The figure below is a representation of an

overview share of losses that were incurred:

Moreover, from the concept of market assessment and failure, Sale builders did not

encounter any market failure since the utilization or expansion of resources can be ccounted

because they are beneficial to the consumes or the employees. Both the minimal and the

overview share of losses that were incurred:

Moreover, from the concept of market assessment and failure, Sale builders did not

encounter any market failure since the utilization or expansion of resources can be ccounted

because they are beneficial to the consumes or the employees. Both the minimal and the

extensive coverage plans add value to the life of the builders despite the premium charge of the

inurance since lower income eraning individual could prefer that package of $20 and high

income individual could also prefer that package of $50 since they are affordable to them.

4.1 Utility Assessment and Choice

Preference eliciting techniques have emerged from a desire to understand consumer

demand for goods and services in the fields where it was not possible to use the revealed

preference data on the correct choices made by individual beings. Similarly, these platform has

arisen due to products and services not traded on market that may include the new products that

are under development and not yet commercially available to the people. When variation in both

service and the product formed is not available the possibility of isolation of each attributed

product from overall utility derived from the product is not there.

At this point the investors and contractors are required to make a choice over a number of

hypothetical alternatives and each of the alternatives is described by several features that are

referred to us attributes. These kind of method is theoretically based and its random utility theory

relies on the assumption of economic utility maximization and the assumption of economic

rationality (Hall et al. 2004). Discrete Choice Experiment method is used to estimate margin

valuations of attributes the willingness to pay for a change in unit for each of the attribute

approximated (Drummond et al., 2005). There results can be analyzed by subgroup of

individuals and it is possible to put into consideration the individual features that impacts the

marginal valuations.

Similarly, selecting and defining attributes need proper understanding of the population

that is being targeted its perspective and experience (Horrocks and Coast, 2007). Policy concerns

inurance since lower income eraning individual could prefer that package of $20 and high

income individual could also prefer that package of $50 since they are affordable to them.

4.1 Utility Assessment and Choice

Preference eliciting techniques have emerged from a desire to understand consumer

demand for goods and services in the fields where it was not possible to use the revealed

preference data on the correct choices made by individual beings. Similarly, these platform has

arisen due to products and services not traded on market that may include the new products that

are under development and not yet commercially available to the people. When variation in both

service and the product formed is not available the possibility of isolation of each attributed

product from overall utility derived from the product is not there.

At this point the investors and contractors are required to make a choice over a number of

hypothetical alternatives and each of the alternatives is described by several features that are

referred to us attributes. These kind of method is theoretically based and its random utility theory

relies on the assumption of economic utility maximization and the assumption of economic

rationality (Hall et al. 2004). Discrete Choice Experiment method is used to estimate margin

valuations of attributes the willingness to pay for a change in unit for each of the attribute

approximated (Drummond et al., 2005). There results can be analyzed by subgroup of

individuals and it is possible to put into consideration the individual features that impacts the

marginal valuations.

Similarly, selecting and defining attributes need proper understanding of the population

that is being targeted its perspective and experience (Horrocks and Coast, 2007). Policy concerns

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.