Corporate Finance and Business Valuation of River Island Report

VerifiedAdded on 2023/01/17

|17

|4722

|76

Report

AI Summary

This report provides a comprehensive analysis of the financial situation and business valuation of River Island Clothing Co. Ltd. It begins with an overview of the company's background and the external environment, including market trends and competitive forces. The report then delves into a detailed financial analysis, utilizing ratio analysis to assess liquidity, profitability, and efficiency. It explores the current and quick ratios, as well as the return on assets, to evaluate the company's financial health. The report also forecasts future revenue and profitability using the geometric mean method. Furthermore, the report discusses the weighted average cost of capital (WACC) calculation, which is crucial for determining the discount rate in the discounted cash flow (DCF) valuation. It explains the components of WACC, including the cost of equity and the cost of debt. The report then provides a qualitative assessment of the company's value using the DCF method, outlining the key assumptions and methodologies employed. It also includes sensitivity analysis to assess the impact of different assumptions on the valuation results. Finally, the report concludes with a critique of the valuation models and a summary of the key findings.

Corporate finance and the business valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Analysis of the current business and the financial situation of the river clothing co. ltd........................3

Background.......................................................................................................................................3

External environment........................................................................................................................3

Analysis.................................................................................................................................................3

Appraisal and assessment of the appropriate weighted average cost of capital......................................7

A qualitative assessment of the value using the discounted cash flow...................................................8

Key Assumptions in Valuation and Sensitivity Analysis.....................................................................11

Methodologies for Valuation of Shares...............................................................................................14

Conclusion...........................................................................................................................................14

References...........................................................................................................................................16

Analysis of the current business and the financial situation of the river clothing co. ltd........................3

Background.......................................................................................................................................3

External environment........................................................................................................................3

Analysis.................................................................................................................................................3

Appraisal and assessment of the appropriate weighted average cost of capital......................................7

A qualitative assessment of the value using the discounted cash flow...................................................8

Key Assumptions in Valuation and Sensitivity Analysis.....................................................................11

Methodologies for Valuation of Shares...............................................................................................14

Conclusion...........................................................................................................................................14

References...........................................................................................................................................16

Analysis of the current business and the financial situation of the river clothing co. ltd.

Background

River Island is considered as the one of the greatest clothing company which is based

in United Kingdom and was established in 1948. The company is operating its operations in

the UK market. The clothing and the shoes and appraisal market in UK is anticipated to be of

£50.4bn in 2015 and it is considered to be develop to £62.9bn at 2020. This is considered that

the online market in the country is expected to grow to the 28.8% from the 20%. River Island

is considered to be one of the medium clothing firm that has competition from the subsequent

market and it is considered that M&S and the super dry PLC. The clothing market is

segmented into various firms which includes the high price and the elite class companies and

the other includes the medium firms, low firm and the initial firms which helps in increasing

the function of the company. For this the example can be considered to be as Boss, Polo ralph

Lauren etc.

External environment

The company is using the porters 5 forces through which the company external

environment could be checked. The company has the risk that is related to the competition in

the industry and which relate to the entry of the new entrants in the market in which the

company is working. River Island considered and use the differentiation method so as to grab

the opportunity to maximise the profit of the company. Additionally, risk of substitutes is

pretty excessive due to the similarity River Island has with other competitor which include

Ted Baker and so on. The River Island faces high competition in the clothing and the apparel

industry. It must be cited that River Island has various strengths. River Island makes use of

websites as a manner to market their merchandise and has a strong online presence that could

help the company to gain a range of sales which is anticipated to increase by 2020 via 8.8%

from 2015. Further, it makes use of different websites to sell its merchandise including ASOS

and Nelly.

Analysis

With respect to financial situation and current business of River Island Clothing Co

Limited (RICCL), a ratio analysis with respect to the organization will be performed.

Furthermore, to reflect upon the capability of River Island Clothing Co Limited for

converting assets readily into cash, liquidity ratios are being utilised that are significant for

assessing both internal and external financial situation of the organization (Hausman &

Background

River Island is considered as the one of the greatest clothing company which is based

in United Kingdom and was established in 1948. The company is operating its operations in

the UK market. The clothing and the shoes and appraisal market in UK is anticipated to be of

£50.4bn in 2015 and it is considered to be develop to £62.9bn at 2020. This is considered that

the online market in the country is expected to grow to the 28.8% from the 20%. River Island

is considered to be one of the medium clothing firm that has competition from the subsequent

market and it is considered that M&S and the super dry PLC. The clothing market is

segmented into various firms which includes the high price and the elite class companies and

the other includes the medium firms, low firm and the initial firms which helps in increasing

the function of the company. For this the example can be considered to be as Boss, Polo ralph

Lauren etc.

External environment

The company is using the porters 5 forces through which the company external

environment could be checked. The company has the risk that is related to the competition in

the industry and which relate to the entry of the new entrants in the market in which the

company is working. River Island considered and use the differentiation method so as to grab

the opportunity to maximise the profit of the company. Additionally, risk of substitutes is

pretty excessive due to the similarity River Island has with other competitor which include

Ted Baker and so on. The River Island faces high competition in the clothing and the apparel

industry. It must be cited that River Island has various strengths. River Island makes use of

websites as a manner to market their merchandise and has a strong online presence that could

help the company to gain a range of sales which is anticipated to increase by 2020 via 8.8%

from 2015. Further, it makes use of different websites to sell its merchandise including ASOS

and Nelly.

Analysis

With respect to financial situation and current business of River Island Clothing Co

Limited (RICCL), a ratio analysis with respect to the organization will be performed.

Furthermore, to reflect upon the capability of River Island Clothing Co Limited for

converting assets readily into cash, liquidity ratios are being utilised that are significant for

assessing both internal and external financial situation of the organization (Hausman &

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

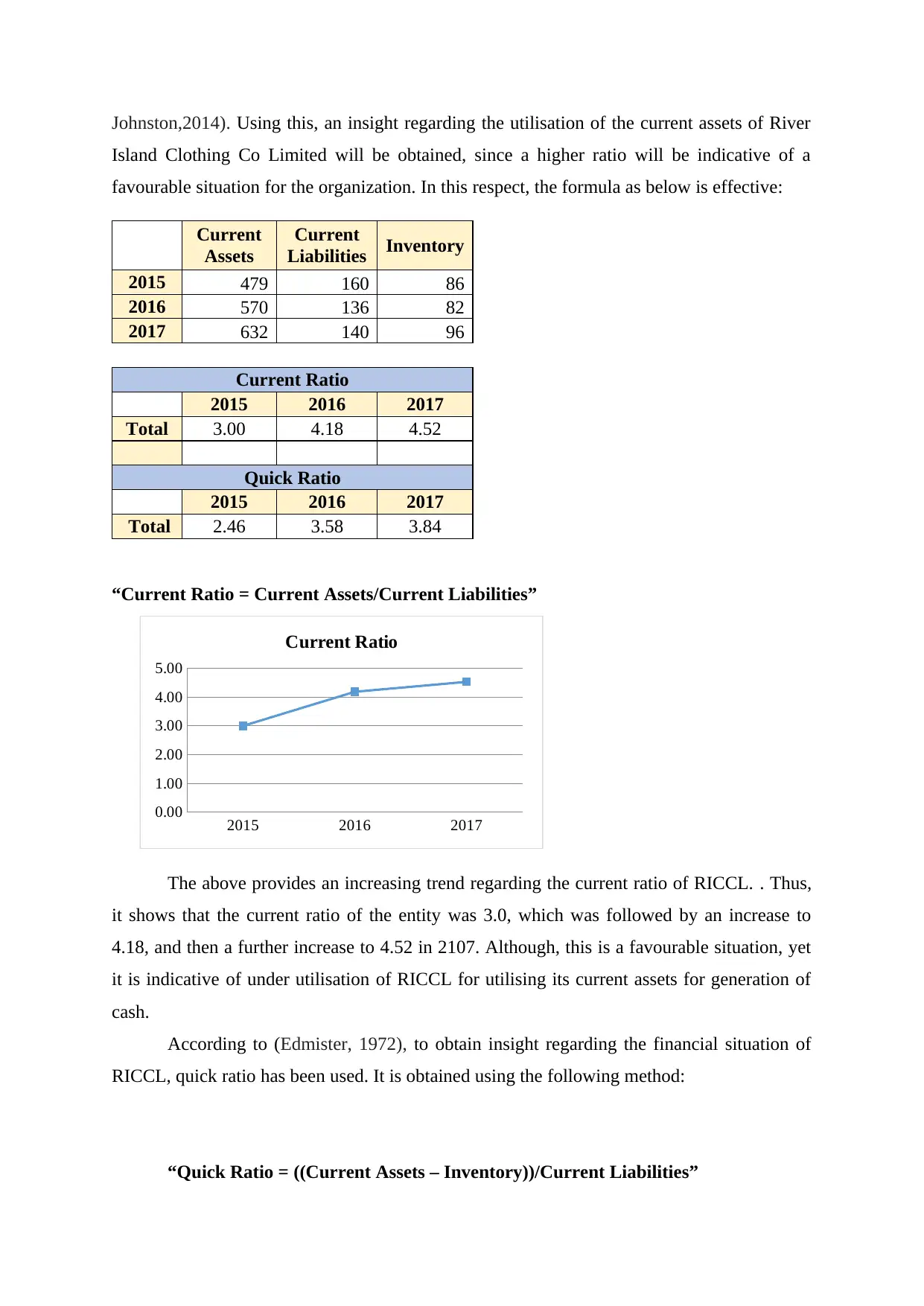

Johnston,2014). Using this, an insight regarding the utilisation of the current assets of River

Island Clothing Co Limited will be obtained, since a higher ratio will be indicative of a

favourable situation for the organization. In this respect, the formula as below is effective:

Current

Assets

Current

Liabilities Inventory

2015 479 160 86

2016 570 136 82

2017 632 140 96

Current Ratio

2015 2016 2017

Total 3.00 4.18 4.52

Quick Ratio

2015 2016 2017

Total 2.46 3.58 3.84

“Current Ratio = Current Assets/Current Liabilities”

2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

Current Ratio

The above provides an increasing trend regarding the current ratio of RICCL. . Thus,

it shows that the current ratio of the entity was 3.0, which was followed by an increase to

4.18, and then a further increase to 4.52 in 2107. Although, this is a favourable situation, yet

it is indicative of under utilisation of RICCL for utilising its current assets for generation of

cash.

According to (Edmister, 1972), to obtain insight regarding the financial situation of

RICCL, quick ratio has been used. It is obtained using the following method:

“Quick Ratio = ((Current Assets – Inventory))/Current Liabilities”

Island Clothing Co Limited will be obtained, since a higher ratio will be indicative of a

favourable situation for the organization. In this respect, the formula as below is effective:

Current

Assets

Current

Liabilities Inventory

2015 479 160 86

2016 570 136 82

2017 632 140 96

Current Ratio

2015 2016 2017

Total 3.00 4.18 4.52

Quick Ratio

2015 2016 2017

Total 2.46 3.58 3.84

“Current Ratio = Current Assets/Current Liabilities”

2015 2016 2017

0.00

1.00

2.00

3.00

4.00

5.00

Current Ratio

The above provides an increasing trend regarding the current ratio of RICCL. . Thus,

it shows that the current ratio of the entity was 3.0, which was followed by an increase to

4.18, and then a further increase to 4.52 in 2107. Although, this is a favourable situation, yet

it is indicative of under utilisation of RICCL for utilising its current assets for generation of

cash.

According to (Edmister, 1972), to obtain insight regarding the financial situation of

RICCL, quick ratio has been used. It is obtained using the following method:

“Quick Ratio = ((Current Assets – Inventory))/Current Liabilities”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 2016 2017

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Quick Ratio

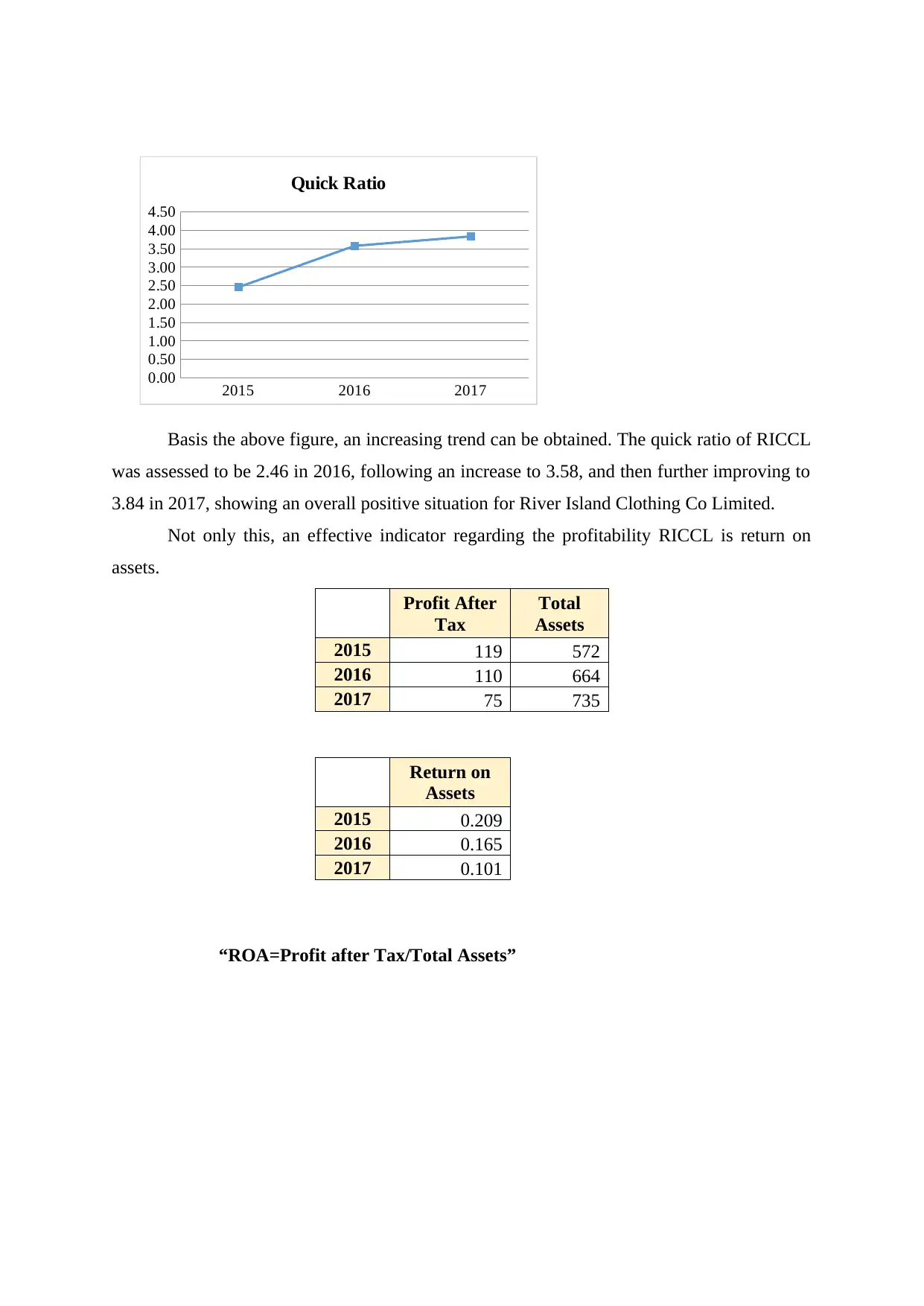

Basis the above figure, an increasing trend can be obtained. The quick ratio of RICCL

was assessed to be 2.46 in 2016, following an increase to 3.58, and then further improving to

3.84 in 2017, showing an overall positive situation for River Island Clothing Co Limited.

Not only this, an effective indicator regarding the profitability RICCL is return on

assets.

Profit After

Tax

Total

Assets

2015 119 572

2016 110 664

2017 75 735

Return on

Assets

2015 0.209

2016 0.165

2017 0.101

“ROA=Profit after Tax/Total Assets”

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Quick Ratio

Basis the above figure, an increasing trend can be obtained. The quick ratio of RICCL

was assessed to be 2.46 in 2016, following an increase to 3.58, and then further improving to

3.84 in 2017, showing an overall positive situation for River Island Clothing Co Limited.

Not only this, an effective indicator regarding the profitability RICCL is return on

assets.

Profit After

Tax

Total

Assets

2015 119 572

2016 110 664

2017 75 735

Return on

Assets

2015 0.209

2016 0.165

2017 0.101

“ROA=Profit after Tax/Total Assets”

2015 2016 2017

0.000

0.050

0.100

0.150

0.200

0.250

Return on Assets

Return on Assets

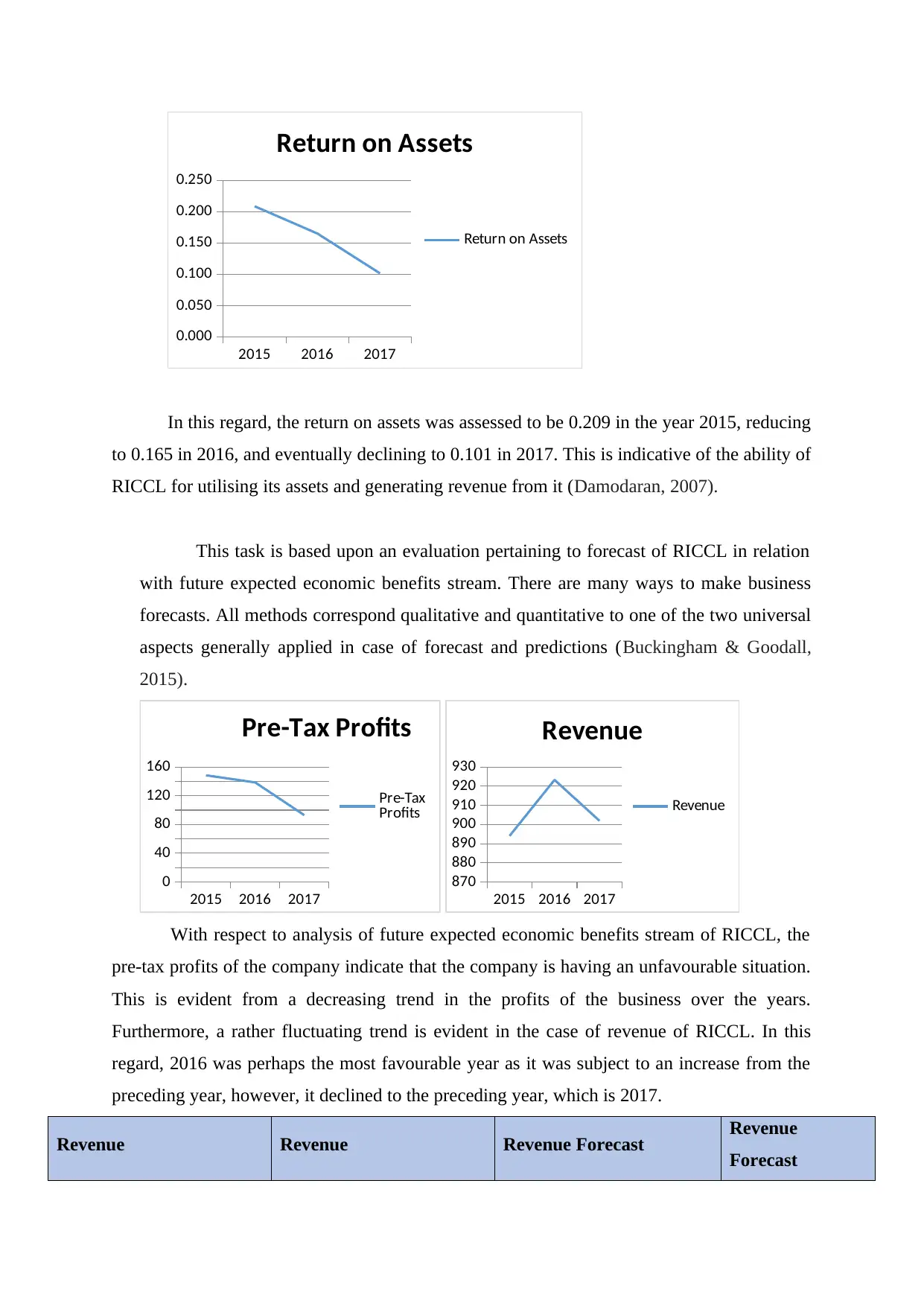

In this regard, the return on assets was assessed to be 0.209 in the year 2015, reducing

to 0.165 in 2016, and eventually declining to 0.101 in 2017. This is indicative of the ability of

RICCL for utilising its assets and generating revenue from it (Damodaran, 2007).

This task is based upon an evaluation pertaining to forecast of RICCL in relation

with future expected economic benefits stream. There are many ways to make business

forecasts. All methods correspond qualitative and quantitative to one of the two universal

aspects generally applied in case of forecast and predictions (Buckingham & Goodall,

2015).

2015 2016 2017

0

40

80

120

160

Pre-Tax Profits

Pre-Tax

Profits

2015 2016 2017

870

880

890

900

910

920

930

Revenue

Revenue

With respect to analysis of future expected economic benefits stream of RICCL, the

pre-tax profits of the company indicate that the company is having an unfavourable situation.

This is evident from a decreasing trend in the profits of the business over the years.

Furthermore, a rather fluctuating trend is evident in the case of revenue of RICCL. In this

regard, 2016 was perhaps the most favourable year as it was subject to an increase from the

preceding year, however, it declined to the preceding year, which is 2017.

Revenue Revenue Revenue Forecast Revenue

Forecast

0.000

0.050

0.100

0.150

0.200

0.250

Return on Assets

Return on Assets

In this regard, the return on assets was assessed to be 0.209 in the year 2015, reducing

to 0.165 in 2016, and eventually declining to 0.101 in 2017. This is indicative of the ability of

RICCL for utilising its assets and generating revenue from it (Damodaran, 2007).

This task is based upon an evaluation pertaining to forecast of RICCL in relation

with future expected economic benefits stream. There are many ways to make business

forecasts. All methods correspond qualitative and quantitative to one of the two universal

aspects generally applied in case of forecast and predictions (Buckingham & Goodall,

2015).

2015 2016 2017

0

40

80

120

160

Pre-Tax Profits

Pre-Tax

Profits

2015 2016 2017

870

880

890

900

910

920

930

Revenue

Revenue

With respect to analysis of future expected economic benefits stream of RICCL, the

pre-tax profits of the company indicate that the company is having an unfavourable situation.

This is evident from a decreasing trend in the profits of the business over the years.

Furthermore, a rather fluctuating trend is evident in the case of revenue of RICCL. In this

regard, 2016 was perhaps the most favourable year as it was subject to an increase from the

preceding year, however, it declined to the preceding year, which is 2017.

Revenue Revenue Revenue Forecast Revenue

Forecast

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

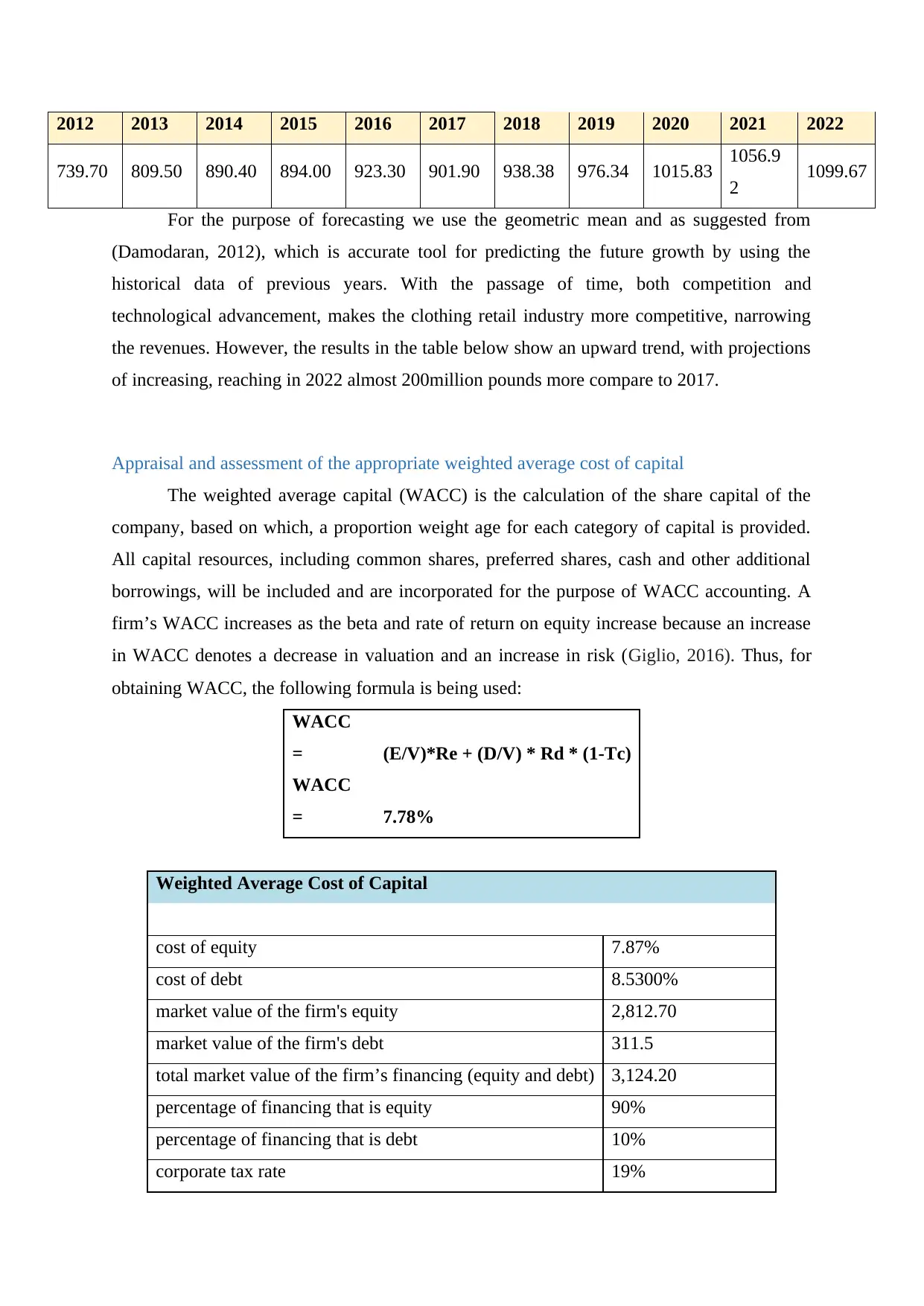

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

739.70 809.50 890.40 894.00 923.30 901.90 938.38 976.34 1015.83 1056.9

2 1099.67

For the purpose of forecasting we use the geometric mean and as suggested from

(Damodaran, 2012), which is accurate tool for predicting the future growth by using the

historical data of previous years. With the passage of time, both competition and

technological advancement, makes the clothing retail industry more competitive, narrowing

the revenues. However, the results in the table below show an upward trend, with projections

of increasing, reaching in 2022 almost 200million pounds more compare to 2017.

Appraisal and assessment of the appropriate weighted average cost of capital

The weighted average capital (WACC) is the calculation of the share capital of the

company, based on which, a proportion weight age for each category of capital is provided.

All capital resources, including common shares, preferred shares, cash and other additional

borrowings, will be included and are incorporated for the purpose of WACC accounting. A

firm’s WACC increases as the beta and rate of return on equity increase because an increase

in WACC denotes a decrease in valuation and an increase in risk (Giglio, 2016). Thus, for

obtaining WACC, the following formula is being used:

WACC

= (E/V)*Re + (D/V) * Rd * (1-Tc)

WACC

= 7.78%

Weighted Average Cost of Capital

cost of equity 7.87%

cost of debt 8.5300%

market value of the firm's equity 2,812.70

market value of the firm's debt 311.5

total market value of the firm’s financing (equity and debt) 3,124.20

percentage of financing that is equity 90%

percentage of financing that is debt 10%

corporate tax rate 19%

739.70 809.50 890.40 894.00 923.30 901.90 938.38 976.34 1015.83 1056.9

2 1099.67

For the purpose of forecasting we use the geometric mean and as suggested from

(Damodaran, 2012), which is accurate tool for predicting the future growth by using the

historical data of previous years. With the passage of time, both competition and

technological advancement, makes the clothing retail industry more competitive, narrowing

the revenues. However, the results in the table below show an upward trend, with projections

of increasing, reaching in 2022 almost 200million pounds more compare to 2017.

Appraisal and assessment of the appropriate weighted average cost of capital

The weighted average capital (WACC) is the calculation of the share capital of the

company, based on which, a proportion weight age for each category of capital is provided.

All capital resources, including common shares, preferred shares, cash and other additional

borrowings, will be included and are incorporated for the purpose of WACC accounting. A

firm’s WACC increases as the beta and rate of return on equity increase because an increase

in WACC denotes a decrease in valuation and an increase in risk (Giglio, 2016). Thus, for

obtaining WACC, the following formula is being used:

WACC

= (E/V)*Re + (D/V) * Rd * (1-Tc)

WACC

= 7.78%

Weighted Average Cost of Capital

cost of equity 7.87%

cost of debt 8.5300%

market value of the firm's equity 2,812.70

market value of the firm's debt 311.5

total market value of the firm’s financing (equity and debt) 3,124.20

percentage of financing that is equity 90%

percentage of financing that is debt 10%

corporate tax rate 19%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Where:

Re = equity

Rd = debt

E = market value in relation with equity of the firm

D = market value of the debt of the firm

V = E + D = (equity and debt)

E/V = percentage of financing comprising of equity

D/V = percentage of financing comprising of debt

Tc = corporate tax rate

WACC is calculated using cost of Equity and Cost of Debt. The calculations of cost

of equity is as follows.

The betas of comparable companies were used and averaged. The capital structure of

these companies were also averaged. Using the average capital structure, beta was unlevered,

and then re-levered using the targeted capital structure of River Island Clothing Co Limited.

Cost of debt includes the required returns that lenders expect if they offer financing to the

company. The cost of debt and the cost of equity includes a series of calculations that exists

briefly in excel file. Therefore, UK government bond yield is added with the market risk

premium as an assumption to calculate the required rate of lenders.

The WACC is the average financing cost that corresponds to the use of various weight

ages in a given situation (Gitman, Juchau & Flanagan, 2015). Based on a weighted average, it

can be used determine the amount of the company's interest on the debt.

Debt and capital are the two components of a company's financial capital. Debt and

stakeholders should achieve some productivity in their investments or assets (Grisse &

Nitschka, 2015). Since the cost of capital is an expected return to stakeholders (or

shareholders) and debt, the WACC determines a return for both types of stakeholders

(shareholders and creditors).

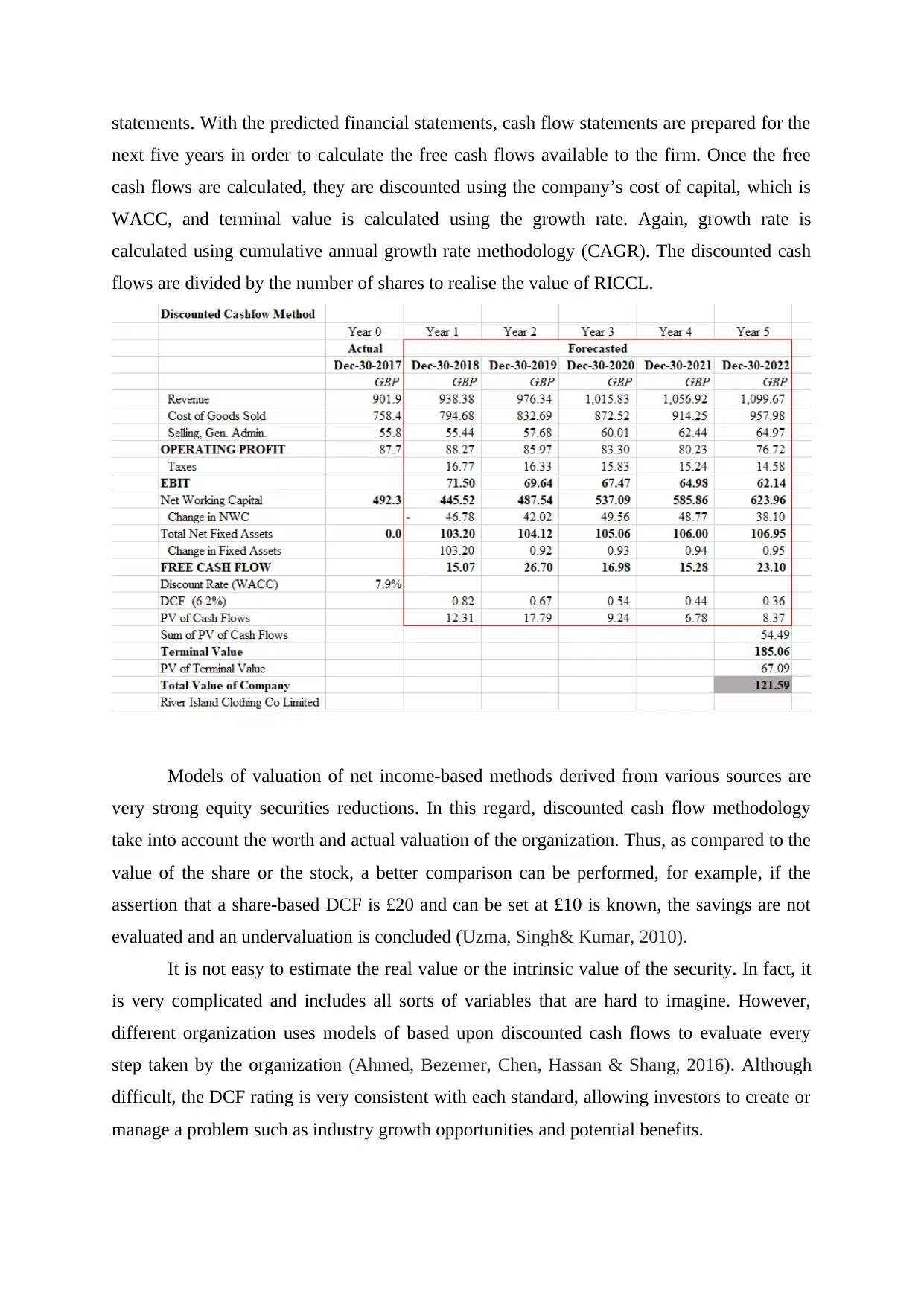

A qualitative assessment of the value using the discounted cash flow

In this example, balance sheet and income statements are forecasted by making

several assumptions for each component of the statements. The forecast is made for the next

five years. In some cases, cumulative annual growth rate is used, while in other, relative less

sensitive components, moving average methodology is used to forecast the components of

Re = equity

Rd = debt

E = market value in relation with equity of the firm

D = market value of the debt of the firm

V = E + D = (equity and debt)

E/V = percentage of financing comprising of equity

D/V = percentage of financing comprising of debt

Tc = corporate tax rate

WACC is calculated using cost of Equity and Cost of Debt. The calculations of cost

of equity is as follows.

The betas of comparable companies were used and averaged. The capital structure of

these companies were also averaged. Using the average capital structure, beta was unlevered,

and then re-levered using the targeted capital structure of River Island Clothing Co Limited.

Cost of debt includes the required returns that lenders expect if they offer financing to the

company. The cost of debt and the cost of equity includes a series of calculations that exists

briefly in excel file. Therefore, UK government bond yield is added with the market risk

premium as an assumption to calculate the required rate of lenders.

The WACC is the average financing cost that corresponds to the use of various weight

ages in a given situation (Gitman, Juchau & Flanagan, 2015). Based on a weighted average, it

can be used determine the amount of the company's interest on the debt.

Debt and capital are the two components of a company's financial capital. Debt and

stakeholders should achieve some productivity in their investments or assets (Grisse &

Nitschka, 2015). Since the cost of capital is an expected return to stakeholders (or

shareholders) and debt, the WACC determines a return for both types of stakeholders

(shareholders and creditors).

A qualitative assessment of the value using the discounted cash flow

In this example, balance sheet and income statements are forecasted by making

several assumptions for each component of the statements. The forecast is made for the next

five years. In some cases, cumulative annual growth rate is used, while in other, relative less

sensitive components, moving average methodology is used to forecast the components of

statements. With the predicted financial statements, cash flow statements are prepared for the

next five years in order to calculate the free cash flows available to the firm. Once the free

cash flows are calculated, they are discounted using the company’s cost of capital, which is

WACC, and terminal value is calculated using the growth rate. Again, growth rate is

calculated using cumulative annual growth rate methodology (CAGR). The discounted cash

flows are divided by the number of shares to realise the value of RICCL.

Models of valuation of net income-based methods derived from various sources are

very strong equity securities reductions. In this regard, discounted cash flow methodology

take into account the worth and actual valuation of the organization. Thus, as compared to the

value of the share or the stock, a better comparison can be performed, for example, if the

assertion that a share-based DCF is £20 and can be set at £10 is known, the savings are not

evaluated and an undervaluation is concluded (Uzma, Singh& Kumar, 2010).

It is not easy to estimate the real value or the intrinsic value of the security. In fact, it

is very complicated and includes all sorts of variables that are hard to imagine. However,

different organization uses models of based upon discounted cash flows to evaluate every

step taken by the organization (Ahmed, Bezemer, Chen, Hassan & Shang, 2016). Although

difficult, the DCF rating is very consistent with each standard, allowing investors to create or

manage a problem such as industry growth opportunities and potential benefits.

next five years in order to calculate the free cash flows available to the firm. Once the free

cash flows are calculated, they are discounted using the company’s cost of capital, which is

WACC, and terminal value is calculated using the growth rate. Again, growth rate is

calculated using cumulative annual growth rate methodology (CAGR). The discounted cash

flows are divided by the number of shares to realise the value of RICCL.

Models of valuation of net income-based methods derived from various sources are

very strong equity securities reductions. In this regard, discounted cash flow methodology

take into account the worth and actual valuation of the organization. Thus, as compared to the

value of the share or the stock, a better comparison can be performed, for example, if the

assertion that a share-based DCF is £20 and can be set at £10 is known, the savings are not

evaluated and an undervaluation is concluded (Uzma, Singh& Kumar, 2010).

It is not easy to estimate the real value or the intrinsic value of the security. In fact, it

is very complicated and includes all sorts of variables that are hard to imagine. However,

different organization uses models of based upon discounted cash flows to evaluate every

step taken by the organization (Ahmed, Bezemer, Chen, Hassan & Shang, 2016). Although

difficult, the DCF rating is very consistent with each standard, allowing investors to create or

manage a problem such as industry growth opportunities and potential benefits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The cash payment formula (DCF) is the cash amount in each phase divided by the

reduction in points (WACC) in relation to the number of times.

Components of DCF Model

Cash Flow (CF) - DCF Form - Cash Flow

Cash flow (CF) is the money that investors earn to block security (storage, savings,

etc.) for a certain period of time. When creating a financial framework for a business, CF is

often called cash flow analysis. When establishing the levy, the FC represents the public

interest and / or payments.

2nd prize Reduction Formula DCF

In the enterprise valuation, the discount rate is usually the average consumer price

index. Investors use WACC because they provide the returns they need to be able to count on

their investment in the company. The discount rate is the interest rate of the asset.

3. Hour (s) of the time Formula DCF - Season

Each cash circle is granted for a certain period. The usual times are years, places or

months. The times may be the same or different. If it is different, it will be displayed in

decimal format.

The basic idea of DCF is simple: the value of the stock market is equal to the present

value of all future tax rates. The problem lies in this idea. The first step in evaluating security

through DCF is to estimate the future revenue stream that the business will reach. Many

effects are used to estimate the tax flow, but the growth of future and future profits of the

company is one of the most important (Barnes, Mukherji, Mullen & Sood, 2017). The

prediction of these variables is not just about future intelligence. In fact, one can often believe

that the action is more valuable (or less) than the real action.

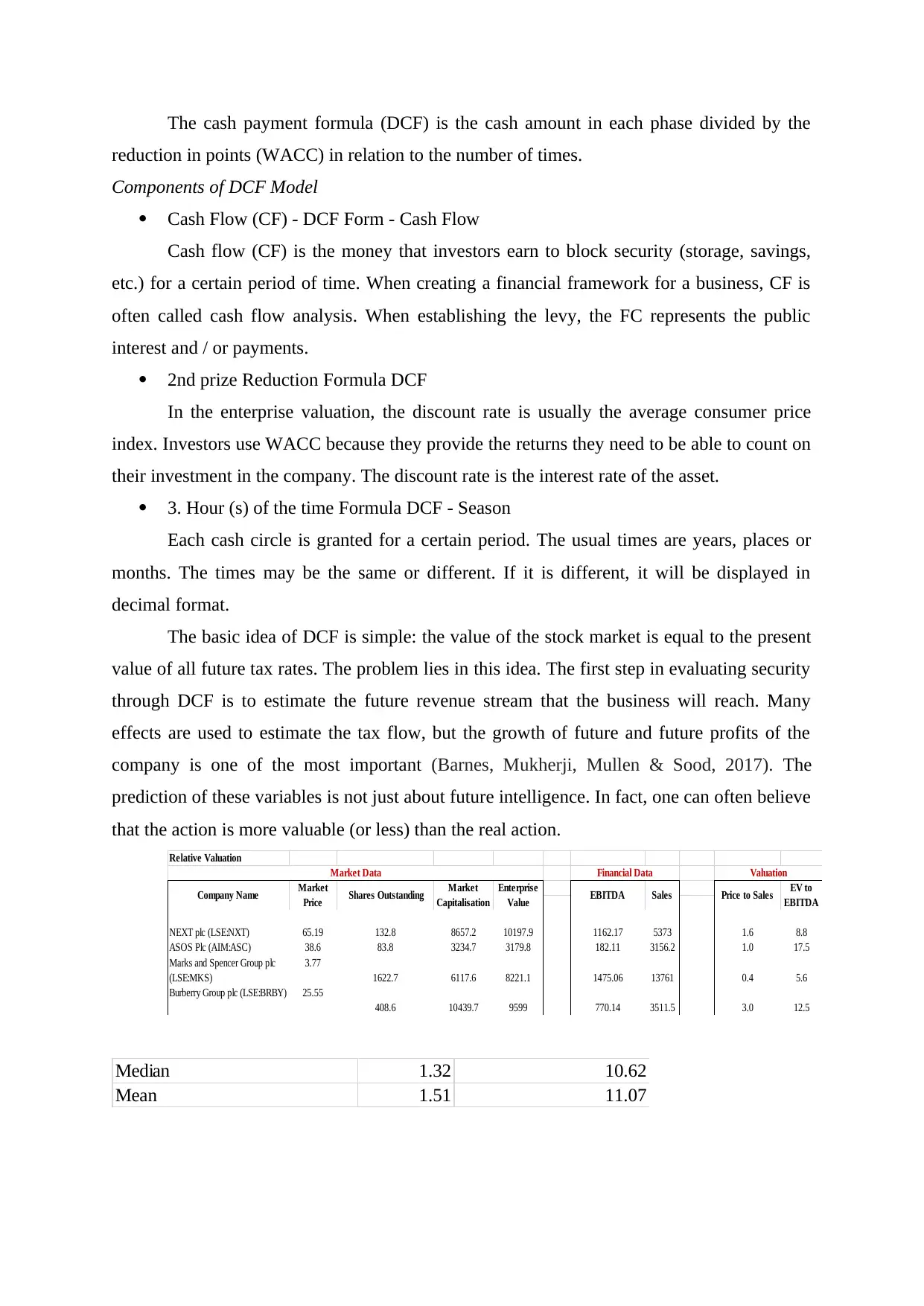

Relative Valuation

NEXT plc (LSE:NXT) 65.19 132.8 8657.2 10197.9 1162.17 5373 1.6 8.8

ASOS Plc (AIM:ASC) 38.6 83.8 3234.7 3179.8 182.11 3156.2 1.0 17.5

Marks and Spencer Group plc

(LSE:MKS)

3.77

1622.7 6117.6 8221.1 1475.06 13761 0.4 5.6

Burberry Group plc (LSE:BRBY) 25.55

408.6 10439.7 9599 770.14 3511.5 3.0 12.5

Market Data Financial Data Valuation

Company Name Market

Price Shares Outstanding Market

Capitalisation

Enterprise

Value EBITDA Sales Price to Sales EV to

EBITDA

Median 1.32 10.62

Mean 1.51 11.07

reduction in points (WACC) in relation to the number of times.

Components of DCF Model

Cash Flow (CF) - DCF Form - Cash Flow

Cash flow (CF) is the money that investors earn to block security (storage, savings,

etc.) for a certain period of time. When creating a financial framework for a business, CF is

often called cash flow analysis. When establishing the levy, the FC represents the public

interest and / or payments.

2nd prize Reduction Formula DCF

In the enterprise valuation, the discount rate is usually the average consumer price

index. Investors use WACC because they provide the returns they need to be able to count on

their investment in the company. The discount rate is the interest rate of the asset.

3. Hour (s) of the time Formula DCF - Season

Each cash circle is granted for a certain period. The usual times are years, places or

months. The times may be the same or different. If it is different, it will be displayed in

decimal format.

The basic idea of DCF is simple: the value of the stock market is equal to the present

value of all future tax rates. The problem lies in this idea. The first step in evaluating security

through DCF is to estimate the future revenue stream that the business will reach. Many

effects are used to estimate the tax flow, but the growth of future and future profits of the

company is one of the most important (Barnes, Mukherji, Mullen & Sood, 2017). The

prediction of these variables is not just about future intelligence. In fact, one can often believe

that the action is more valuable (or less) than the real action.

Relative Valuation

NEXT plc (LSE:NXT) 65.19 132.8 8657.2 10197.9 1162.17 5373 1.6 8.8

ASOS Plc (AIM:ASC) 38.6 83.8 3234.7 3179.8 182.11 3156.2 1.0 17.5

Marks and Spencer Group plc

(LSE:MKS)

3.77

1622.7 6117.6 8221.1 1475.06 13761 0.4 5.6

Burberry Group plc (LSE:BRBY) 25.55

408.6 10439.7 9599 770.14 3511.5 3.0 12.5

Market Data Financial Data Valuation

Company Name Market

Price Shares Outstanding Market

Capitalisation

Enterprise

Value EBITDA Sales Price to Sales EV to

EBITDA

Median 1.32 10.62

Mean 1.51 11.07

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

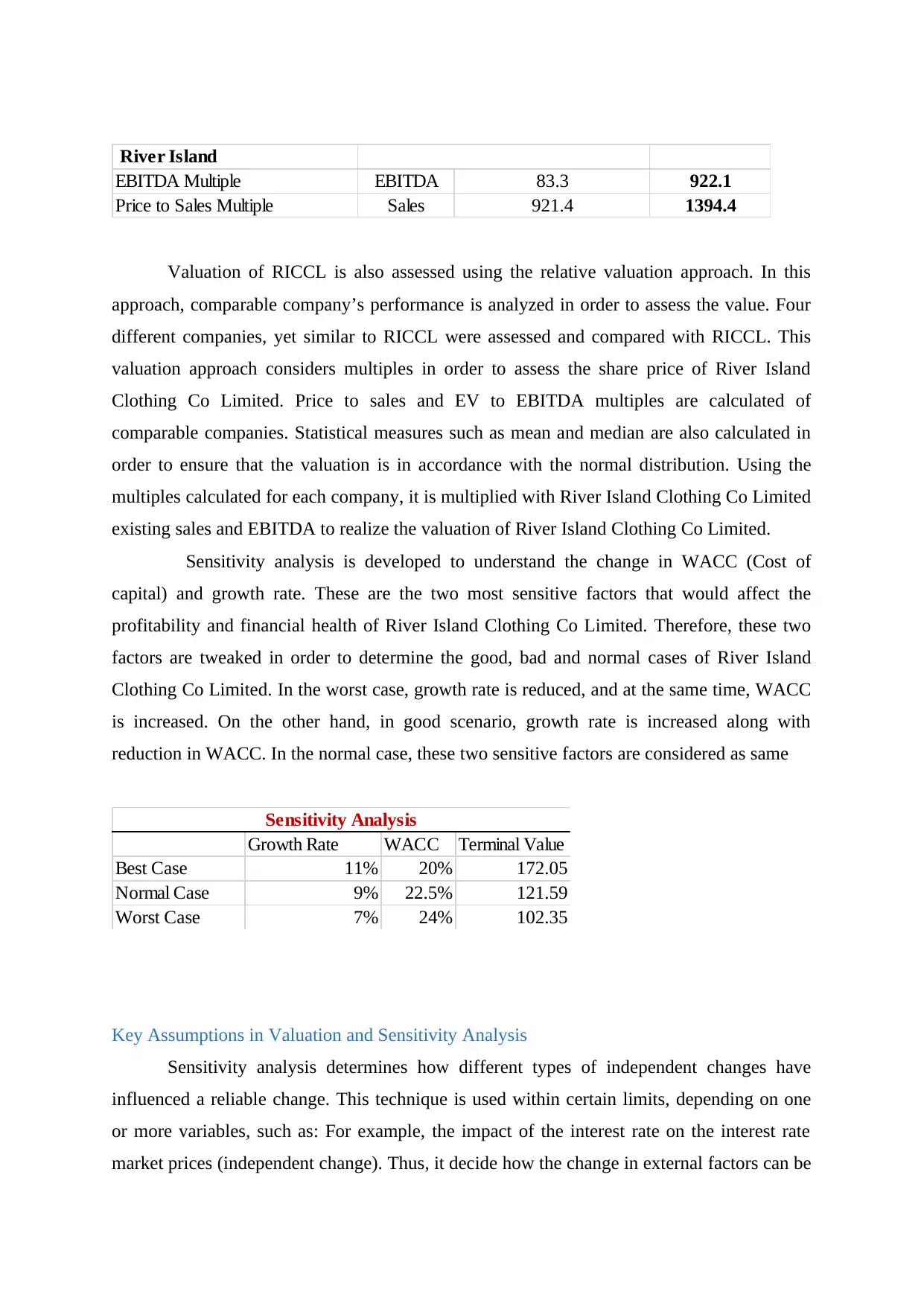

River Island

EBITDA Multiple EBITDA 83.3 922.1

Price to Sales Multiple Sales 921.4 1394.4

Valuation of RICCL is also assessed using the relative valuation approach. In this

approach, comparable company’s performance is analyzed in order to assess the value. Four

different companies, yet similar to RICCL were assessed and compared with RICCL. This

valuation approach considers multiples in order to assess the share price of River Island

Clothing Co Limited. Price to sales and EV to EBITDA multiples are calculated of

comparable companies. Statistical measures such as mean and median are also calculated in

order to ensure that the valuation is in accordance with the normal distribution. Using the

multiples calculated for each company, it is multiplied with River Island Clothing Co Limited

existing sales and EBITDA to realize the valuation of River Island Clothing Co Limited.

Sensitivity analysis is developed to understand the change in WACC (Cost of

capital) and growth rate. These are the two most sensitive factors that would affect the

profitability and financial health of River Island Clothing Co Limited. Therefore, these two

factors are tweaked in order to determine the good, bad and normal cases of River Island

Clothing Co Limited. In the worst case, growth rate is reduced, and at the same time, WACC

is increased. On the other hand, in good scenario, growth rate is increased along with

reduction in WACC. In the normal case, these two sensitive factors are considered as same

Growth Rate WACC Terminal Value

Best Case 11% 20% 172.05

Normal Case 9% 22.5% 121.59

Worst Case 7% 24% 102.35

Sensitivity Analysis

Key Assumptions in Valuation and Sensitivity Analysis

Sensitivity analysis determines how different types of independent changes have

influenced a reliable change. This technique is used within certain limits, depending on one

or more variables, such as: For example, the impact of the interest rate on the interest rate

market prices (independent change). Thus, it decide how the change in external factors can be

EBITDA Multiple EBITDA 83.3 922.1

Price to Sales Multiple Sales 921.4 1394.4

Valuation of RICCL is also assessed using the relative valuation approach. In this

approach, comparable company’s performance is analyzed in order to assess the value. Four

different companies, yet similar to RICCL were assessed and compared with RICCL. This

valuation approach considers multiples in order to assess the share price of River Island

Clothing Co Limited. Price to sales and EV to EBITDA multiples are calculated of

comparable companies. Statistical measures such as mean and median are also calculated in

order to ensure that the valuation is in accordance with the normal distribution. Using the

multiples calculated for each company, it is multiplied with River Island Clothing Co Limited

existing sales and EBITDA to realize the valuation of River Island Clothing Co Limited.

Sensitivity analysis is developed to understand the change in WACC (Cost of

capital) and growth rate. These are the two most sensitive factors that would affect the

profitability and financial health of River Island Clothing Co Limited. Therefore, these two

factors are tweaked in order to determine the good, bad and normal cases of River Island

Clothing Co Limited. In the worst case, growth rate is reduced, and at the same time, WACC

is increased. On the other hand, in good scenario, growth rate is increased along with

reduction in WACC. In the normal case, these two sensitive factors are considered as same

Growth Rate WACC Terminal Value

Best Case 11% 20% 172.05

Normal Case 9% 22.5% 121.59

Worst Case 7% 24% 102.35

Sensitivity Analysis

Key Assumptions in Valuation and Sensitivity Analysis

Sensitivity analysis determines how different types of independent changes have

influenced a reliable change. This technique is used within certain limits, depending on one

or more variables, such as: For example, the impact of the interest rate on the interest rate

market prices (independent change). Thus, it decide how the change in external factors can be

changed. Inventories and reserves are particularly vulnerable to changes in interest rates.

Reduction is a key factor in determining the value of stocks. Economic growth and inflation

are also strongly influenced by the value of equities (Arnaboldi, Lapsley& Steccolini, 2015).

The emotional analysis is also performed at the lowest level. A company can imagine many

errors in the price change of the product.

According to the list of examinations, the organization is not more than 10 years old.

It is obvious that the economic future and the future are hard to see.

The first basic guidelines for analysts are in progress. Whatever the use of it, it

becomes cash flow or shareholders, analysts and therefore investors believe that the activity

will continue in the near future.

This assumption is generally valid since most companies have been in the market for

a long time. However, if investors trust a safe place and expect a close closure, they should be

careful to evaluate the business based on accepting losses that are not related to business

continuity (generally the case).

However, we can only continue the actions if some lines are created later. Every piece

of information we read tells us about future ideas. Some of these millions are clearly defined

while others are in the relationship.

It is important to know that each report or evaluation of the actions is valid as

perception. If, as investors, we do not follow the ideas in the report, we generally do not

accept the report.

As a good investor, he deliberately engages in fairness reports to confirm the value,

approve and analyze the report. In case of a change, investors can improve the construction

site to get the real cost of the investment.

To predict the evolution of future earnings over five or ten years, analysts will need to

consider how the company's revenues will be generated over the same period. If you think the

community is growing faster than you can invest in an internal change, you should also

evaluate the source and cost of that money.

By allocating past shares, the expected growth rate and free money, investors can

estimate the amount of the company's distribution. This interest payment is deductible from

corporate taxes, which reduces their growth. It is important to understand the validity of the

approval of the distribution of profits because the valuation of the company can vary

considerably, even if minor changes are made to the payment.

Reduction is a key factor in determining the value of stocks. Economic growth and inflation

are also strongly influenced by the value of equities (Arnaboldi, Lapsley& Steccolini, 2015).

The emotional analysis is also performed at the lowest level. A company can imagine many

errors in the price change of the product.

According to the list of examinations, the organization is not more than 10 years old.

It is obvious that the economic future and the future are hard to see.

The first basic guidelines for analysts are in progress. Whatever the use of it, it

becomes cash flow or shareholders, analysts and therefore investors believe that the activity

will continue in the near future.

This assumption is generally valid since most companies have been in the market for

a long time. However, if investors trust a safe place and expect a close closure, they should be

careful to evaluate the business based on accepting losses that are not related to business

continuity (generally the case).

However, we can only continue the actions if some lines are created later. Every piece

of information we read tells us about future ideas. Some of these millions are clearly defined

while others are in the relationship.

It is important to know that each report or evaluation of the actions is valid as

perception. If, as investors, we do not follow the ideas in the report, we generally do not

accept the report.

As a good investor, he deliberately engages in fairness reports to confirm the value,

approve and analyze the report. In case of a change, investors can improve the construction

site to get the real cost of the investment.

To predict the evolution of future earnings over five or ten years, analysts will need to

consider how the company's revenues will be generated over the same period. If you think the

community is growing faster than you can invest in an internal change, you should also

evaluate the source and cost of that money.

By allocating past shares, the expected growth rate and free money, investors can

estimate the amount of the company's distribution. This interest payment is deductible from

corporate taxes, which reduces their growth. It is important to understand the validity of the

approval of the distribution of profits because the valuation of the company can vary

considerably, even if minor changes are made to the payment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.