Starbucks Acquisition: Financial Analysis of Roast Ltd's Performance

VerifiedAdded on 2023/01/17

|16

|4387

|61

Report

AI Summary

This report provides a comprehensive financial analysis of Roast Ltd, evaluating its performance to support Starbucks' potential acquisition decision. The analysis includes an industry review of the UK coffee market, highlighting key trends and challenges. The core of the report focuses on Roast Ltd's business performance, examining its financial statements, including the profit and loss account, balance sheet, and cash flow statement. Ratio analysis is performed to assess profitability (gross profit margin, operating profit margin, net profit margin), liquidity (current ratio), financial leverage (debt-to-equity ratio), and efficiency (return on capital employed, operating cash cycle). The analysis reveals improvements in sales, profitability, and operational efficiency. The report also highlights the company's cash flow dynamics and dividend policy, concluding with an assessment of Roast Ltd's overall financial health and its suitability for acquisition.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Financial Decision-making implies to an organised process or collection of tasks which

help in creation of systematic framework for taking finance and fund related decisions in quick

manner (Brown-Liburd, Issa and Lombardi, 2015). The study-report summaries comprehensive

analysis and evaluation of business performance of Roast Ltd that help to assess that company is

quite profitable and financial performance has also improved as compare to previous year. This

analysis is done through review of company's financial statements and other supporting materials

with aim to support CFO of Starbucks in evaluation of Roast Ltd's attractiveness and

effectiveness as a target company for acquisition-decision by Starbucks. This has been find that

company's overall efficiencies and performance has been enhanced over the year.

MAIN BODY

Part 1 – Industry Review:

On the UK market, common customers like tea and coffee as it was found that every four

adults out of five like coffee. There are also similar kinds of customers that like coffee. In 2019

retail coffee sales hit 69 million kg, up approximately 8% from 2014. The inflation or cultural

trend has produced 17% rise, which amounts to approximately GBP1.27billion. Actually, the

coffee industry, including soil coffee, beans etc., is leading the 65% share in the UK market. UK

retailers or wholesalers are targeting the young age demographic because they are crazier than

the older group. Property costs, labour and Brexit effects are three major challenges in this

industry.

In 2019, the café industry produced approximately GBP6billion in sales, with the sector

growing and reaching around 16200. The coffee market is facing enormous growth between

year-2014 and 2019 and that's about 6.1 per cent, there are 101,034 jobs. The coffee industry's

statistics are growing due to high consumer demand. The sector will expand by an average rate

of around 4.8% over the course of 5-years. The currently growth-rate is 1.9-percent and it

should hit £6.6 billion, this involves current growth (Trend in UK's Coffee Industry. 2019).

Increasing in household spendings towards non-alcoholic beverages and foods is key opportunity

for business.

Costa Ltd, Starbucks Coffee, Pret A Manger (Europe) Ltd and Caffe Nero Group

Holdings Ltd are key players in this industry. Pret A Manger (Europe) Ltd.

Financial Decision-making implies to an organised process or collection of tasks which

help in creation of systematic framework for taking finance and fund related decisions in quick

manner (Brown-Liburd, Issa and Lombardi, 2015). The study-report summaries comprehensive

analysis and evaluation of business performance of Roast Ltd that help to assess that company is

quite profitable and financial performance has also improved as compare to previous year. This

analysis is done through review of company's financial statements and other supporting materials

with aim to support CFO of Starbucks in evaluation of Roast Ltd's attractiveness and

effectiveness as a target company for acquisition-decision by Starbucks. This has been find that

company's overall efficiencies and performance has been enhanced over the year.

MAIN BODY

Part 1 – Industry Review:

On the UK market, common customers like tea and coffee as it was found that every four

adults out of five like coffee. There are also similar kinds of customers that like coffee. In 2019

retail coffee sales hit 69 million kg, up approximately 8% from 2014. The inflation or cultural

trend has produced 17% rise, which amounts to approximately GBP1.27billion. Actually, the

coffee industry, including soil coffee, beans etc., is leading the 65% share in the UK market. UK

retailers or wholesalers are targeting the young age demographic because they are crazier than

the older group. Property costs, labour and Brexit effects are three major challenges in this

industry.

In 2019, the café industry produced approximately GBP6billion in sales, with the sector

growing and reaching around 16200. The coffee market is facing enormous growth between

year-2014 and 2019 and that's about 6.1 per cent, there are 101,034 jobs. The coffee industry's

statistics are growing due to high consumer demand. The sector will expand by an average rate

of around 4.8% over the course of 5-years. The currently growth-rate is 1.9-percent and it

should hit £6.6 billion, this involves current growth (Trend in UK's Coffee Industry. 2019).

Increasing in household spendings towards non-alcoholic beverages and foods is key opportunity

for business.

Costa Ltd, Starbucks Coffee, Pret A Manger (Europe) Ltd and Caffe Nero Group

Holdings Ltd are key players in this industry. Pret A Manger (Europe) Ltd.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part 2 – Business performance analysis:

2.1 Statement of profit and loss account:

A profit&loss account or P&L account shows a corporation's profitability position as it

involves all the incomes and expenditures. P&L statement also reflects organization's quality to

make revenues/sales, handling expenses, and provide profits and net income. Analysis of this

systems offers wide range of information about company's actual profitability level. This

statements offers comprehensive and more detailed information of company's direct and indirect

expenses along with sources of income (Brunsson and Olsen, 2018).

Roast Limited has reported overall sales of GBP2534000 in year-2018 while company's

sales in year-2017 was just GBP2022000 reflecting around 25.32 percent growth. Business's cost

of sales figures has been increased by around 32.23 percent (From 1505000 GBP to 1990000

GBP during year-2017 to 2018. Gross profits of such corporation has been rose to 544000 GBP

in year-2018 that was 517000 GBP in 2017, this enhancement in the level of gross profit is

indicator of increasing gross profit generation capabilities of company. Operating income in

year-2017 was just nil while in next year there was operating income of 60000GBP.

In business operating profits has been increased from 51000 GBP to 127000 GBP

indicating that business's operational efficiencies in terms of generation of profits has been

increased. Finance costs of business has been increased substantially from 6000 GBP in year-

2017 to 26000 GBP in year 2018 such major rise shows that company has borrowed funds.

While Net-profits are 81000 GBP and 36000 GBP in year-2018 and year-2017 respectively

disclosing a increasing or upward trend in net profitability level. It simply means that company is

efficient to generate net profits and such efficiency level has been grown over the period.

However for interpretation of relationship between different items of income-statement, ratio-

analysis would be effective. In this context following are several ratios related to P&L accounts

items of Roast Ltd, as below:

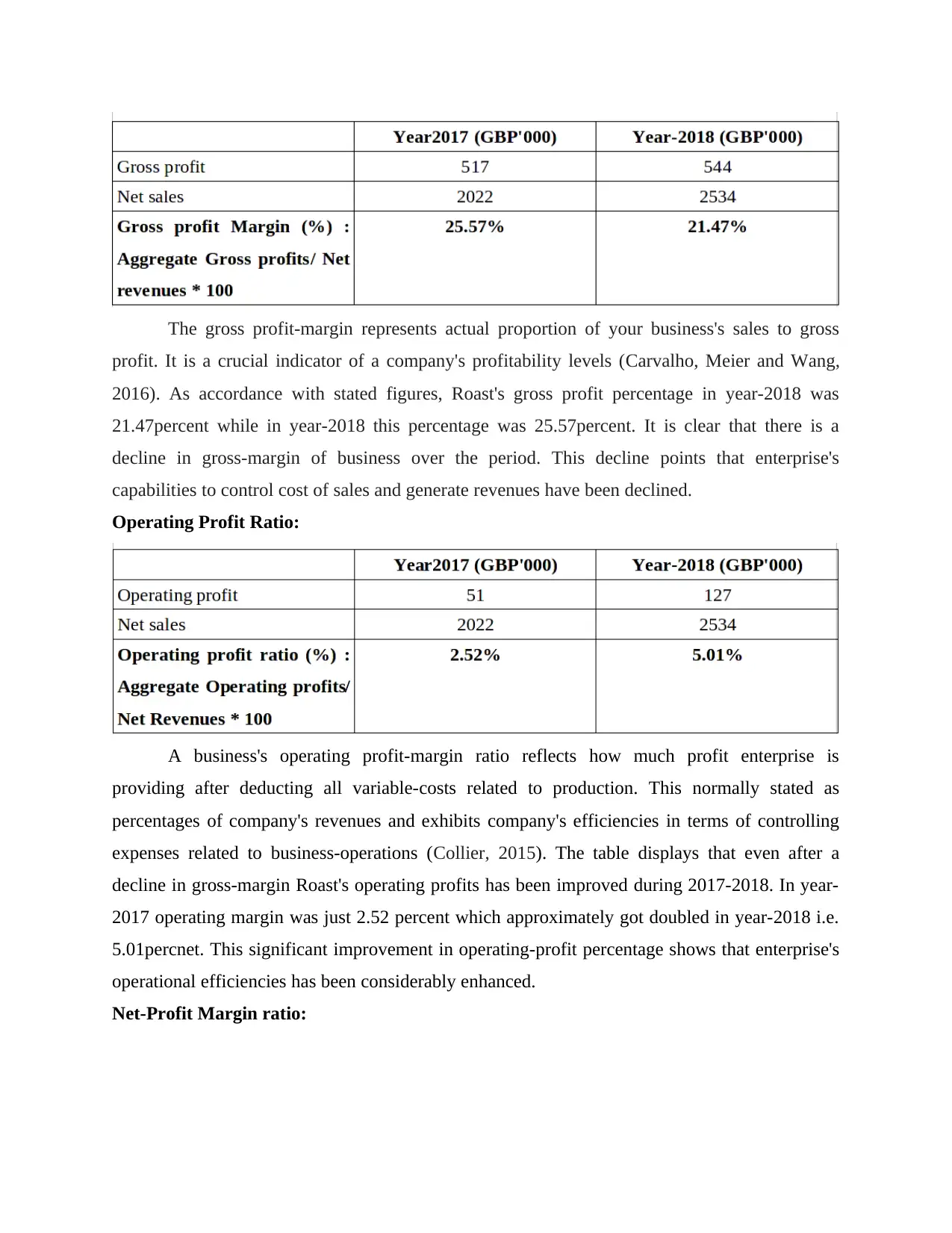

Gross Profit Ratio:

2.1 Statement of profit and loss account:

A profit&loss account or P&L account shows a corporation's profitability position as it

involves all the incomes and expenditures. P&L statement also reflects organization's quality to

make revenues/sales, handling expenses, and provide profits and net income. Analysis of this

systems offers wide range of information about company's actual profitability level. This

statements offers comprehensive and more detailed information of company's direct and indirect

expenses along with sources of income (Brunsson and Olsen, 2018).

Roast Limited has reported overall sales of GBP2534000 in year-2018 while company's

sales in year-2017 was just GBP2022000 reflecting around 25.32 percent growth. Business's cost

of sales figures has been increased by around 32.23 percent (From 1505000 GBP to 1990000

GBP during year-2017 to 2018. Gross profits of such corporation has been rose to 544000 GBP

in year-2018 that was 517000 GBP in 2017, this enhancement in the level of gross profit is

indicator of increasing gross profit generation capabilities of company. Operating income in

year-2017 was just nil while in next year there was operating income of 60000GBP.

In business operating profits has been increased from 51000 GBP to 127000 GBP

indicating that business's operational efficiencies in terms of generation of profits has been

increased. Finance costs of business has been increased substantially from 6000 GBP in year-

2017 to 26000 GBP in year 2018 such major rise shows that company has borrowed funds.

While Net-profits are 81000 GBP and 36000 GBP in year-2018 and year-2017 respectively

disclosing a increasing or upward trend in net profitability level. It simply means that company is

efficient to generate net profits and such efficiency level has been grown over the period.

However for interpretation of relationship between different items of income-statement, ratio-

analysis would be effective. In this context following are several ratios related to P&L accounts

items of Roast Ltd, as below:

Gross Profit Ratio:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The gross profit-margin represents actual proportion of your business's sales to gross

profit. It is a crucial indicator of a company's profitability levels (Carvalho, Meier and Wang,

2016). As accordance with stated figures, Roast's gross profit percentage in year-2018 was

21.47percent while in year-2018 this percentage was 25.57percent. It is clear that there is a

decline in gross-margin of business over the period. This decline points that enterprise's

capabilities to control cost of sales and generate revenues have been declined.

Operating Profit Ratio:

A business's operating profit-margin ratio reflects how much profit enterprise is

providing after deducting all variable-costs related to production. This normally stated as

percentages of company's revenues and exhibits company's efficiencies in terms of controlling

expenses related to business-operations (Collier, 2015). The table displays that even after a

decline in gross-margin Roast's operating profits has been improved during 2017-2018. In year-

2017 operating margin was just 2.52 percent which approximately got doubled in year-2018 i.e.

5.01percnet. This significant improvement in operating-profit percentage shows that enterprise's

operational efficiencies has been considerably enhanced.

Net-Profit Margin ratio:

profit. It is a crucial indicator of a company's profitability levels (Carvalho, Meier and Wang,

2016). As accordance with stated figures, Roast's gross profit percentage in year-2018 was

21.47percent while in year-2018 this percentage was 25.57percent. It is clear that there is a

decline in gross-margin of business over the period. This decline points that enterprise's

capabilities to control cost of sales and generate revenues have been declined.

Operating Profit Ratio:

A business's operating profit-margin ratio reflects how much profit enterprise is

providing after deducting all variable-costs related to production. This normally stated as

percentages of company's revenues and exhibits company's efficiencies in terms of controlling

expenses related to business-operations (Collier, 2015). The table displays that even after a

decline in gross-margin Roast's operating profits has been improved during 2017-2018. In year-

2017 operating margin was just 2.52 percent which approximately got doubled in year-2018 i.e.

5.01percnet. This significant improvement in operating-profit percentage shows that enterprise's

operational efficiencies has been considerably enhanced.

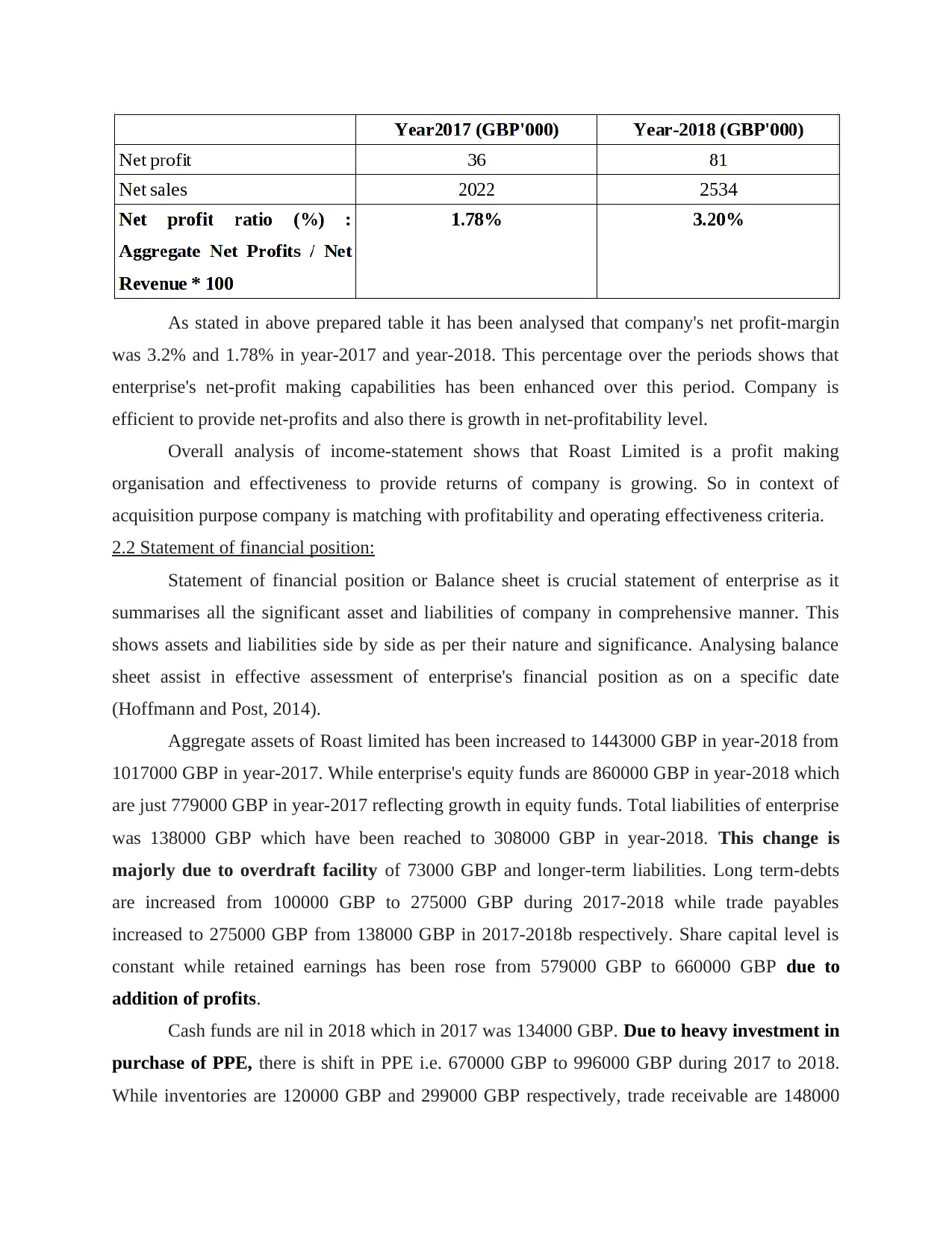

Net-Profit Margin ratio:

As stated in above prepared table it has been analysed that company's net profit-margin

was 3.2% and 1.78% in year-2017 and year-2018. This percentage over the periods shows that

enterprise's net-profit making capabilities has been enhanced over this period. Company is

efficient to provide net-profits and also there is growth in net-profitability level.

Overall analysis of income-statement shows that Roast Limited is a profit making

organisation and effectiveness to provide returns of company is growing. So in context of

acquisition purpose company is matching with profitability and operating effectiveness criteria.

2.2 Statement of financial position:

Statement of financial position or Balance sheet is crucial statement of enterprise as it

summarises all the significant asset and liabilities of company in comprehensive manner. This

shows assets and liabilities side by side as per their nature and significance. Analysing balance

sheet assist in effective assessment of enterprise's financial position as on a specific date

(Hoffmann and Post, 2014).

Aggregate assets of Roast limited has been increased to 1443000 GBP in year-2018 from

1017000 GBP in year-2017. While enterprise's equity funds are 860000 GBP in year-2018 which

are just 779000 GBP in year-2017 reflecting growth in equity funds. Total liabilities of enterprise

was 138000 GBP which have been reached to 308000 GBP in year-2018. This change is

majorly due to overdraft facility of 73000 GBP and longer-term liabilities. Long term-debts

are increased from 100000 GBP to 275000 GBP during 2017-2018 while trade payables

increased to 275000 GBP from 138000 GBP in 2017-2018b respectively. Share capital level is

constant while retained earnings has been rose from 579000 GBP to 660000 GBP due to

addition of profits.

Cash funds are nil in 2018 which in 2017 was 134000 GBP. Due to heavy investment in

purchase of PPE, there is shift in PPE i.e. 670000 GBP to 996000 GBP during 2017 to 2018.

While inventories are 120000 GBP and 299000 GBP respectively, trade receivable are 148000

was 3.2% and 1.78% in year-2017 and year-2018. This percentage over the periods shows that

enterprise's net-profit making capabilities has been enhanced over this period. Company is

efficient to provide net-profits and also there is growth in net-profitability level.

Overall analysis of income-statement shows that Roast Limited is a profit making

organisation and effectiveness to provide returns of company is growing. So in context of

acquisition purpose company is matching with profitability and operating effectiveness criteria.

2.2 Statement of financial position:

Statement of financial position or Balance sheet is crucial statement of enterprise as it

summarises all the significant asset and liabilities of company in comprehensive manner. This

shows assets and liabilities side by side as per their nature and significance. Analysing balance

sheet assist in effective assessment of enterprise's financial position as on a specific date

(Hoffmann and Post, 2014).

Aggregate assets of Roast limited has been increased to 1443000 GBP in year-2018 from

1017000 GBP in year-2017. While enterprise's equity funds are 860000 GBP in year-2018 which

are just 779000 GBP in year-2017 reflecting growth in equity funds. Total liabilities of enterprise

was 138000 GBP which have been reached to 308000 GBP in year-2018. This change is

majorly due to overdraft facility of 73000 GBP and longer-term liabilities. Long term-debts

are increased from 100000 GBP to 275000 GBP during 2017-2018 while trade payables

increased to 275000 GBP from 138000 GBP in 2017-2018b respectively. Share capital level is

constant while retained earnings has been rose from 579000 GBP to 660000 GBP due to

addition of profits.

Cash funds are nil in 2018 which in 2017 was 134000 GBP. Due to heavy investment in

purchase of PPE, there is shift in PPE i.e. 670000 GBP to 996000 GBP during 2017 to 2018.

While inventories are 120000 GBP and 299000 GBP respectively, trade receivable are 148000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

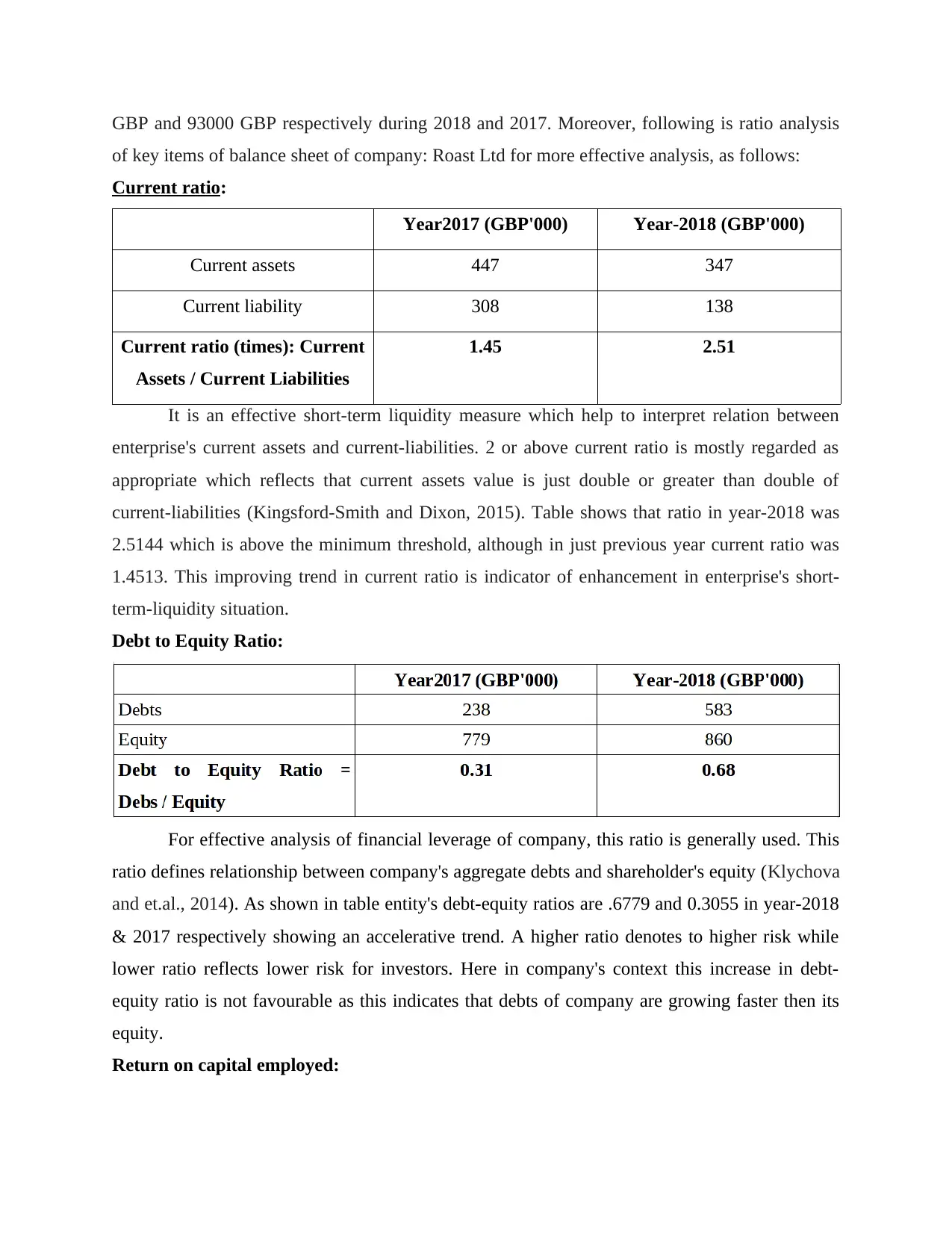

GBP and 93000 GBP respectively during 2018 and 2017. Moreover, following is ratio analysis

of key items of balance sheet of company: Roast Ltd for more effective analysis, as follows:

Current ratio:

Year2017 (GBP'000) Year-2018 (GBP'000)

Current assets 447 347

Current liability 308 138

Current ratio (times): Current

Assets / Current Liabilities

1.45 2.51

It is an effective short-term liquidity measure which help to interpret relation between

enterprise's current assets and current-liabilities. 2 or above current ratio is mostly regarded as

appropriate which reflects that current assets value is just double or greater than double of

current-liabilities (Kingsford-Smith and Dixon, 2015). Table shows that ratio in year-2018 was

2.5144 which is above the minimum threshold, although in just previous year current ratio was

1.4513. This improving trend in current ratio is indicator of enhancement in enterprise's short-

term-liquidity situation.

Debt to Equity Ratio:

For effective analysis of financial leverage of company, this ratio is generally used. This

ratio defines relationship between company's aggregate debts and shareholder's equity (Klychova

and et.al., 2014). As shown in table entity's debt-equity ratios are .6779 and 0.3055 in year-2018

& 2017 respectively showing an accelerative trend. A higher ratio denotes to higher risk while

lower ratio reflects lower risk for investors. Here in company's context this increase in debt-

equity ratio is not favourable as this indicates that debts of company are growing faster then its

equity.

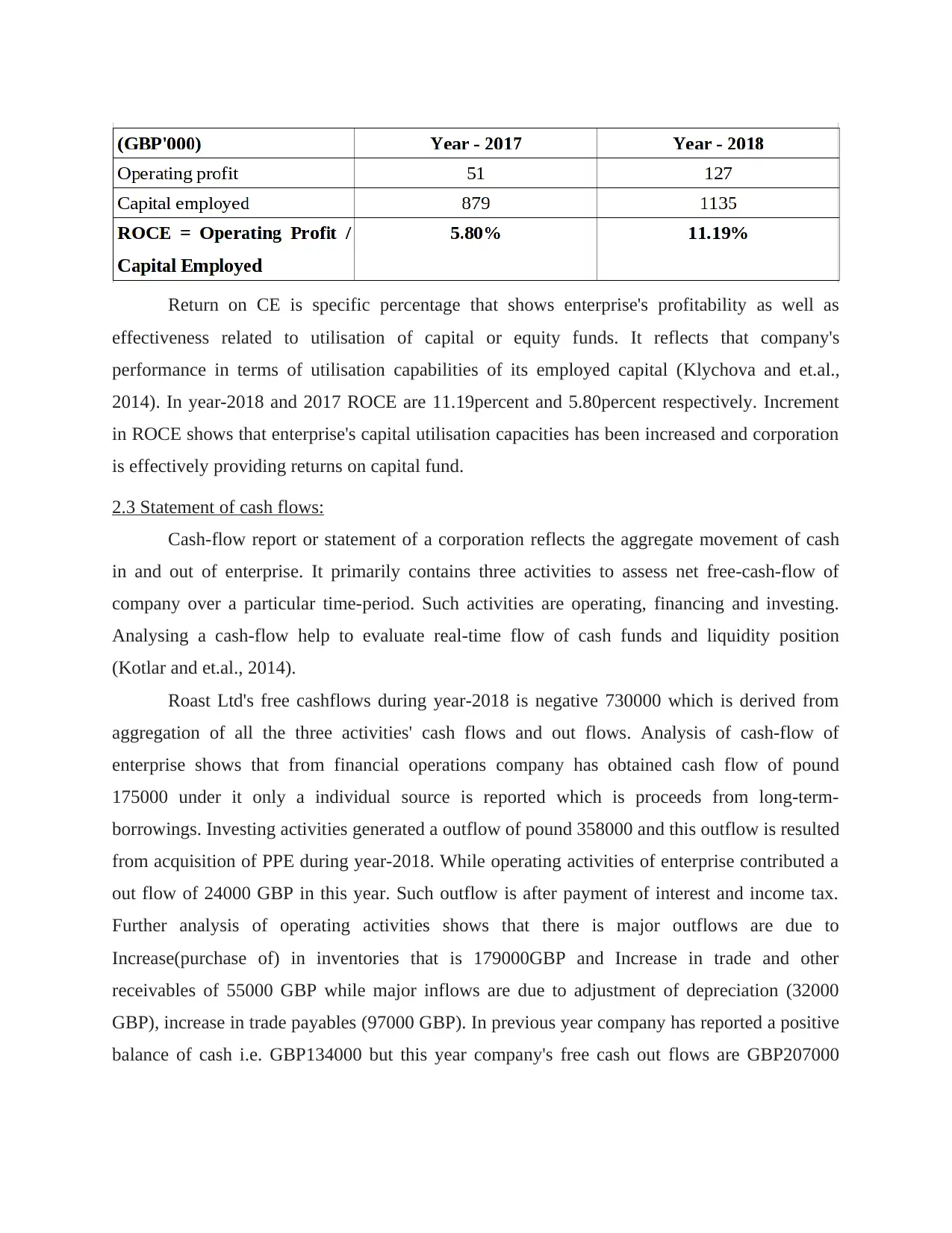

Return on capital employed:

of key items of balance sheet of company: Roast Ltd for more effective analysis, as follows:

Current ratio:

Year2017 (GBP'000) Year-2018 (GBP'000)

Current assets 447 347

Current liability 308 138

Current ratio (times): Current

Assets / Current Liabilities

1.45 2.51

It is an effective short-term liquidity measure which help to interpret relation between

enterprise's current assets and current-liabilities. 2 or above current ratio is mostly regarded as

appropriate which reflects that current assets value is just double or greater than double of

current-liabilities (Kingsford-Smith and Dixon, 2015). Table shows that ratio in year-2018 was

2.5144 which is above the minimum threshold, although in just previous year current ratio was

1.4513. This improving trend in current ratio is indicator of enhancement in enterprise's short-

term-liquidity situation.

Debt to Equity Ratio:

For effective analysis of financial leverage of company, this ratio is generally used. This

ratio defines relationship between company's aggregate debts and shareholder's equity (Klychova

and et.al., 2014). As shown in table entity's debt-equity ratios are .6779 and 0.3055 in year-2018

& 2017 respectively showing an accelerative trend. A higher ratio denotes to higher risk while

lower ratio reflects lower risk for investors. Here in company's context this increase in debt-

equity ratio is not favourable as this indicates that debts of company are growing faster then its

equity.

Return on capital employed:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Return on CE is specific percentage that shows enterprise's profitability as well as

effectiveness related to utilisation of capital or equity funds. It reflects that company's

performance in terms of utilisation capabilities of its employed capital (Klychova and et.al.,

2014). In year-2018 and 2017 ROCE are 11.19percent and 5.80percent respectively. Increment

in ROCE shows that enterprise's capital utilisation capacities has been increased and corporation

is effectively providing returns on capital fund.

2.3 Statement of cash flows:

Cash-flow report or statement of a corporation reflects the aggregate movement of cash

in and out of enterprise. It primarily contains three activities to assess net free-cash-flow of

company over a particular time-period. Such activities are operating, financing and investing.

Analysing a cash-flow help to evaluate real-time flow of cash funds and liquidity position

(Kotlar and et.al., 2014).

Roast Ltd's free cashflows during year-2018 is negative 730000 which is derived from

aggregation of all the three activities' cash flows and out flows. Analysis of cash-flow of

enterprise shows that from financial operations company has obtained cash flow of pound

175000 under it only a individual source is reported which is proceeds from long-term-

borrowings. Investing activities generated a outflow of pound 358000 and this outflow is resulted

from acquisition of PPE during year-2018. While operating activities of enterprise contributed a

out flow of 24000 GBP in this year. Such outflow is after payment of interest and income tax.

Further analysis of operating activities shows that there is major outflows are due to

Increase(purchase of) in inventories that is 179000GBP and Increase in trade and other

receivables of 55000 GBP while major inflows are due to adjustment of depreciation (32000

GBP), increase in trade payables (97000 GBP). In previous year company has reported a positive

balance of cash i.e. GBP134000 but this year company's free cash out flows are GBP207000

effectiveness related to utilisation of capital or equity funds. It reflects that company's

performance in terms of utilisation capabilities of its employed capital (Klychova and et.al.,

2014). In year-2018 and 2017 ROCE are 11.19percent and 5.80percent respectively. Increment

in ROCE shows that enterprise's capital utilisation capacities has been increased and corporation

is effectively providing returns on capital fund.

2.3 Statement of cash flows:

Cash-flow report or statement of a corporation reflects the aggregate movement of cash

in and out of enterprise. It primarily contains three activities to assess net free-cash-flow of

company over a particular time-period. Such activities are operating, financing and investing.

Analysing a cash-flow help to evaluate real-time flow of cash funds and liquidity position

(Kotlar and et.al., 2014).

Roast Ltd's free cashflows during year-2018 is negative 730000 which is derived from

aggregation of all the three activities' cash flows and out flows. Analysis of cash-flow of

enterprise shows that from financial operations company has obtained cash flow of pound

175000 under it only a individual source is reported which is proceeds from long-term-

borrowings. Investing activities generated a outflow of pound 358000 and this outflow is resulted

from acquisition of PPE during year-2018. While operating activities of enterprise contributed a

out flow of 24000 GBP in this year. Such outflow is after payment of interest and income tax.

Further analysis of operating activities shows that there is major outflows are due to

Increase(purchase of) in inventories that is 179000GBP and Increase in trade and other

receivables of 55000 GBP while major inflows are due to adjustment of depreciation (32000

GBP), increase in trade payables (97000 GBP). In previous year company has reported a positive

balance of cash i.e. GBP134000 but this year company's free cash out flows are GBP207000

before considering prior year free-cash-flow. Company has not paid any dividend sum over the

period.

The whole analysis of entire cash-flow statement exhibits that entity's cash liquidity

position is not so much favourable as negative cash flow also an indicator of poor working

capital management.

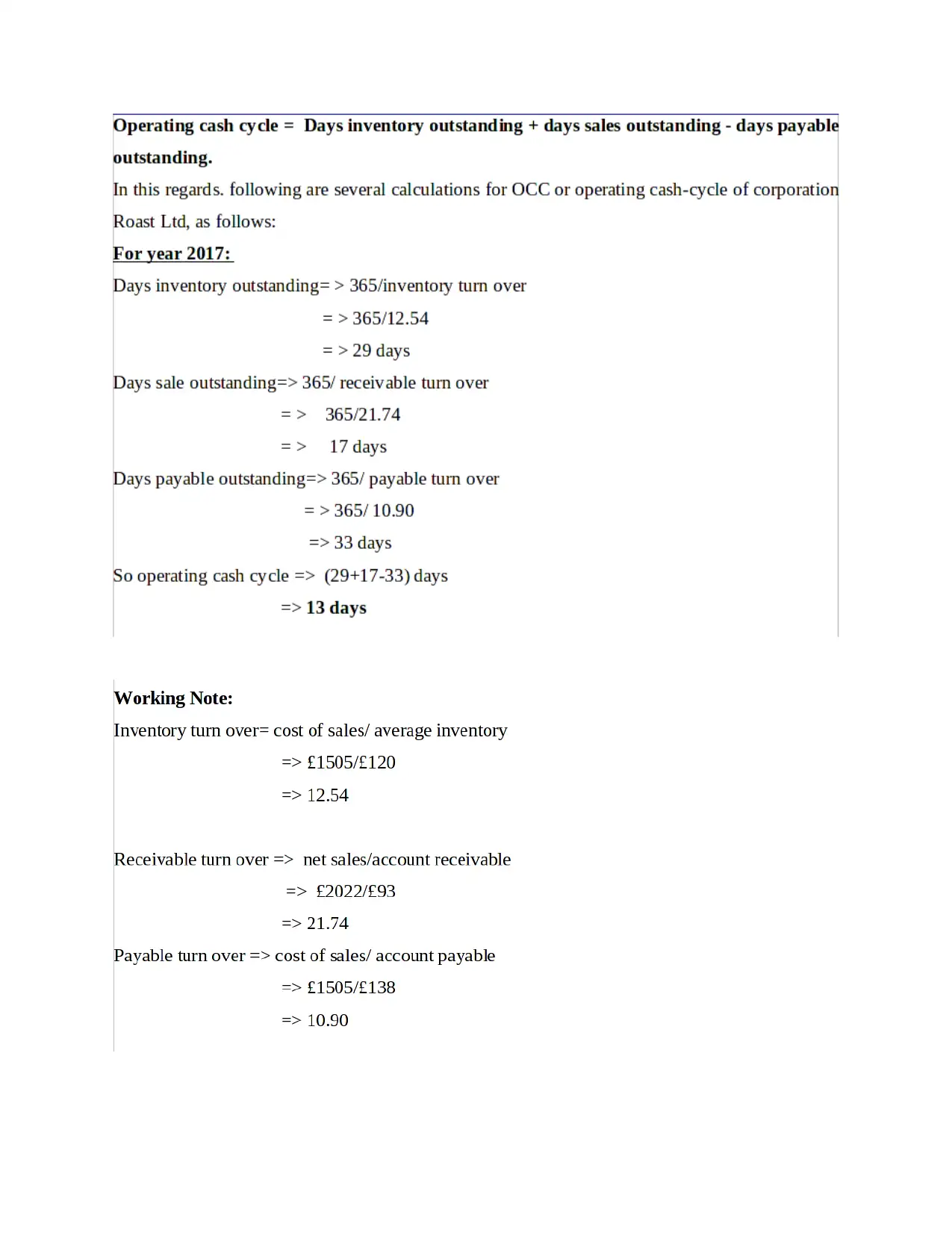

Operating cash cycle: A business cycle is actual length of time an enterprise takes to buy a

product, deliver it and collect money from its buyers in exchange for sold stock. The operating

period of a product depends on a variety of variables, including payments to its clients and

expanded by its vendors to the business (Petersen, Kushwaha and Kumar, 2015). If an enterprise

has more time to make inventory payments to its suppliers, the business cycle can be shortened

by reducing the spending on cash. Nevertheless, if a business allows more time to its buyers to

pay for purchased products, the operational period will increase, since the company needs to wait

even longer for all its cash to be collected.

period.

The whole analysis of entire cash-flow statement exhibits that entity's cash liquidity

position is not so much favourable as negative cash flow also an indicator of poor working

capital management.

Operating cash cycle: A business cycle is actual length of time an enterprise takes to buy a

product, deliver it and collect money from its buyers in exchange for sold stock. The operating

period of a product depends on a variety of variables, including payments to its clients and

expanded by its vendors to the business (Petersen, Kushwaha and Kumar, 2015). If an enterprise

has more time to make inventory payments to its suppliers, the business cycle can be shortened

by reducing the spending on cash. Nevertheless, if a business allows more time to its buyers to

pay for purchased products, the operational period will increase, since the company needs to wait

even longer for all its cash to be collected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

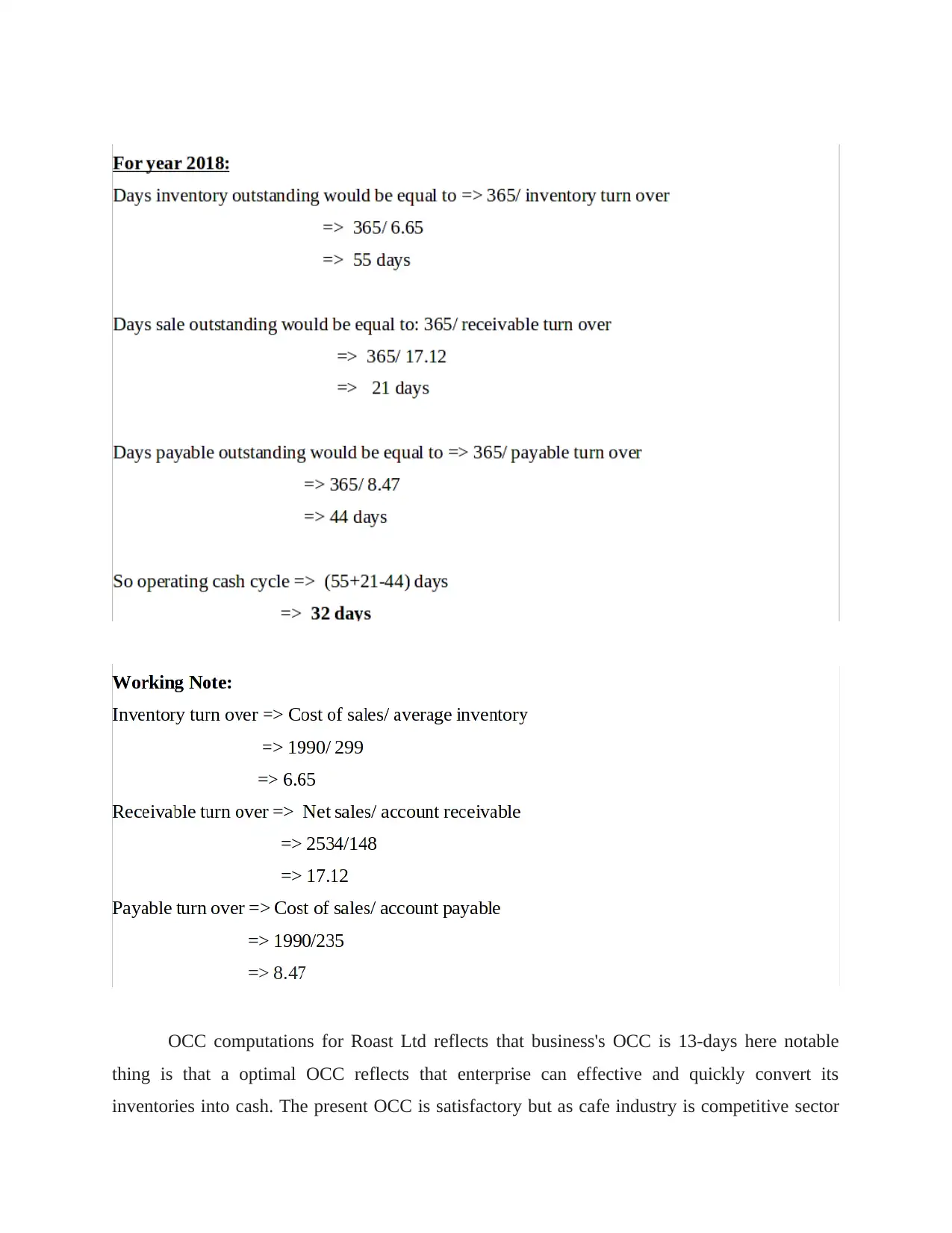

OCC computations for Roast Ltd reflects that business's OCC is 13-days here notable

thing is that a optimal OCC reflects that enterprise can effective and quickly convert its

inventories into cash. The present OCC is satisfactory but as cafe industry is competitive sector

thing is that a optimal OCC reflects that enterprise can effective and quickly convert its

inventories into cash. The present OCC is satisfactory but as cafe industry is competitive sector

this should be more lower. Although inventories-days-outstanding cycle is 29-days while Days-

sale-outstanding cycle is 13-days. On other hand, payable-days-outstanding cycle is 33-days.

Overall position of OCC in Roast Ltd case is good in context of acquisition purpose.

Dividend policy: A dividend policy of company relates to practices adopted by enterpises with

relation to payment of dividend. A company's dividend policy can be analysed through

evaluation of dividend payment pattern over prior period (Shepherd, Williams and Patzelt,

2015). This analysis help to interpret company's status in eyes of shareholders, because a regular

divined payment generally shows that investment in company would be profitable but it is not

necessary in exceptional cases like Roast ltd. As company is profit maker and able to provide

ROCE but enterprise has no or null dividend payment history. In year 2018 also company has

not made any dividend payments.

Part 3 – Investment appraisals

Part 3 – Investment appraisal and source of finance:

3.1 Investment Appraisal:

Management forecast: Predictions/Forecast is management of future events whereby, on

the grounds of the preceding prediction, they take potential decisions. In Roast Ltd's perspective,

the group agreed to spend £ 500 million for Romania's extension of its market. For 2017 to

2021, Corporation expects a cash outflow of GBP 6 2, GBP 112, GBP 148, GBP 180 and GBP

224. Roast Ltd's executives anticipated their profits over all of period to be increasing. But they

must ensure that they anticipate less in initial phase, because in better/favourable scenarios they

are faced with numerous complications. Here in project, Initial investment of respective

corporation is GBP 500million and further company's management has estimated revenues of

GBP300 million, GBP560 million, GBP740 million, GBP900 million and GBP1120 million

during the same period respectively. There is doubt about the forecasted figures and assumption

as these are not marching with current business environment as well as operating scale. Thus to

an certain extent assumptions seems not so much relevant for company. The United Kingdom

market already faces the numerous climate-changes threats impacting coffee production. They

must therefore study Romania's weather and choose the correct time to produce. In addition,

Romanian citizens ' interest in coffee must be recognized. It is appropriate for the business to

grow if they are interested in or wants to drink coffee.

Investment appraisal technique:

sale-outstanding cycle is 13-days. On other hand, payable-days-outstanding cycle is 33-days.

Overall position of OCC in Roast Ltd case is good in context of acquisition purpose.

Dividend policy: A dividend policy of company relates to practices adopted by enterpises with

relation to payment of dividend. A company's dividend policy can be analysed through

evaluation of dividend payment pattern over prior period (Shepherd, Williams and Patzelt,

2015). This analysis help to interpret company's status in eyes of shareholders, because a regular

divined payment generally shows that investment in company would be profitable but it is not

necessary in exceptional cases like Roast ltd. As company is profit maker and able to provide

ROCE but enterprise has no or null dividend payment history. In year 2018 also company has

not made any dividend payments.

Part 3 – Investment appraisals

Part 3 – Investment appraisal and source of finance:

3.1 Investment Appraisal:

Management forecast: Predictions/Forecast is management of future events whereby, on

the grounds of the preceding prediction, they take potential decisions. In Roast Ltd's perspective,

the group agreed to spend £ 500 million for Romania's extension of its market. For 2017 to

2021, Corporation expects a cash outflow of GBP 6 2, GBP 112, GBP 148, GBP 180 and GBP

224. Roast Ltd's executives anticipated their profits over all of period to be increasing. But they

must ensure that they anticipate less in initial phase, because in better/favourable scenarios they

are faced with numerous complications. Here in project, Initial investment of respective

corporation is GBP 500million and further company's management has estimated revenues of

GBP300 million, GBP560 million, GBP740 million, GBP900 million and GBP1120 million

during the same period respectively. There is doubt about the forecasted figures and assumption

as these are not marching with current business environment as well as operating scale. Thus to

an certain extent assumptions seems not so much relevant for company. The United Kingdom

market already faces the numerous climate-changes threats impacting coffee production. They

must therefore study Romania's weather and choose the correct time to produce. In addition,

Romanian citizens ' interest in coffee must be recognized. It is appropriate for the business to

grow if they are interested in or wants to drink coffee.

Investment appraisal technique:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.