Financial Analysis of Roast Ltd: Performance, Investment, and Ratios

VerifiedAdded on 2023/01/16

|13

|4191

|69

Report

AI Summary

This report provides a comprehensive financial analysis of Roast Ltd, a UK coffee house, assessing its performance and attractiveness for potential acquisition. The analysis includes an industry review, a detailed examination of the company's financial statements (profit and loss, financial position, and cash flow), and the calculation of key financial ratios such as gross profit, operating profit, net profit, debt-equity, current, quick, and operating cash cycle. The report evaluates the company's profitability, liquidity, and solvency, and assesses the financial impact of a proposed investment using techniques like Net Present Value (NPV), Accounting Rate of Return (ARR), and payback period. The report also recommends financial strategies, such as securing a bank loan, to facilitate project goals. Findings reveal that while the company's performance improved from 2017 to 2018 in terms of profitability, its liquidity declined. The operating cash cycle increased, suggesting a longer time to convert current assets to cash, which may indicate potential financial challenges.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Present report is based upon Roast Ltd which is one of the famous coffee houses of UK

which is Roast Ltd. The employee of finance department of Starbucks is asked by the Chief

Financial Officer to analyse the financial position and attractiveness of the company to acquire it

in future. For this purpose all the final accounts are analysed for which ratios such as net,

operating and gross profit, debt equity, current, quick ratios along with operating cycle are

calculated. The enterprise have decided to invest around 500 pounds in the business and to

determine the profitability of this investment different techniques are used. These are net present

value, accounting rate of return and pay back period. The entity is required to arrange finance to

fund the proposed project therefore the management is recommended to take a bank loan from a

bank so that goals related to project could be accomplished successfully.

PART 1: Industry Review

Top line review of current UK coffee house industry

The Coffee house industry of UK is large enough as it contributes in the development of

the whole economy. In order to analyse the industry review of it following points could be

considered:

According to a research total contribution of the coffee sector in the GDP for year 2017

was around 3.7 billion pounds (Contribution of coffee house industry in UK's GDP,

2019).

It has been estimated that in upcoming years the revenues of the industry will rise by

4.8% and the total amount of them will be around 6.6 billion pounds.

There are various organisations which are operating business in this industry. These are

Coffee Republic, Raost Ltd. Starbucks, Costa Coffee, Cafe 2U, Muffin Break, Caffe

Ritazza, Puccino's, Caffe Nero etc.

The major opportunity which is available to the entities operating in this sector is to

launch such coffee or other beverages which are made of it that are best suitable to the

fitness freak individuals as they ignore to have coffee with milk.

1

Present report is based upon Roast Ltd which is one of the famous coffee houses of UK

which is Roast Ltd. The employee of finance department of Starbucks is asked by the Chief

Financial Officer to analyse the financial position and attractiveness of the company to acquire it

in future. For this purpose all the final accounts are analysed for which ratios such as net,

operating and gross profit, debt equity, current, quick ratios along with operating cycle are

calculated. The enterprise have decided to invest around 500 pounds in the business and to

determine the profitability of this investment different techniques are used. These are net present

value, accounting rate of return and pay back period. The entity is required to arrange finance to

fund the proposed project therefore the management is recommended to take a bank loan from a

bank so that goals related to project could be accomplished successfully.

PART 1: Industry Review

Top line review of current UK coffee house industry

The Coffee house industry of UK is large enough as it contributes in the development of

the whole economy. In order to analyse the industry review of it following points could be

considered:

According to a research total contribution of the coffee sector in the GDP for year 2017

was around 3.7 billion pounds (Contribution of coffee house industry in UK's GDP,

2019).

It has been estimated that in upcoming years the revenues of the industry will rise by

4.8% and the total amount of them will be around 6.6 billion pounds.

There are various organisations which are operating business in this industry. These are

Coffee Republic, Raost Ltd. Starbucks, Costa Coffee, Cafe 2U, Muffin Break, Caffe

Ritazza, Puccino's, Caffe Nero etc.

The major opportunity which is available to the entities operating in this sector is to

launch such coffee or other beverages which are made of it that are best suitable to the

fitness freak individuals as they ignore to have coffee with milk.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 2: Business Performance Analysis

2.1 Statement of profit and loss

All the business entities generate an account on yearly basis for the purpose of recording

all the direct, indirect, operating and non operating expenses along with incomes so that

profitability could be estimated. In order to attract large number of investors it is very important

for an enterprise to make sure that its income statement is formed in systematic manner so that

external parties can estimate the possible returns which could be generated by them in future

(Almenberg and Dreber, 2015). The exhibit 1 is based upon statement of profit and loss of Roast

Ltd shows that in 2017 revenues of the enterprise were 2022 which are increased up to 2534

which means it will help the entity to maximise its profitability. Total gross profits for the year

ending 2018 are also increased from 517 to 544. Due to this operating profits are also enhanced

from 51 to 127 for 2017. The income statement is also showing an increment in net profit. For

2017 it was 36 and for 2018 it is increased up to 81. For the purpose of analysing financial

performance of the enterprise following ratios are calculated:

Gross profit ratio: In order to determine relation between gross profit and revenues this

ratio is calculated. Main purpose behind using it is to measure operational performance of an

enterprise. In order to measure that Roast Ltd is able to generate good profits or not this ratio

could be calculated.

Operating profit ratio: This ratio is calculated for the purpose of measuring the ability

of an entity to generate profit after paying all the variable costs. It will also be calculated by the

managers to measure the capacity of Roast Ltd to generate profits for upcoming period (Barth,

Papageorge and Thom, 2017).

Net profit ratio: In order to analyse the actual percentage of profits generated for the

year this ratio is calculated as it is calculated after paying all the expenses, dividends, interests

and taxes. It could be used to determine that Roast Ltd is able to reach the goal of acquiring

profits or not.

Calculations for all the above described ratios are as follows:

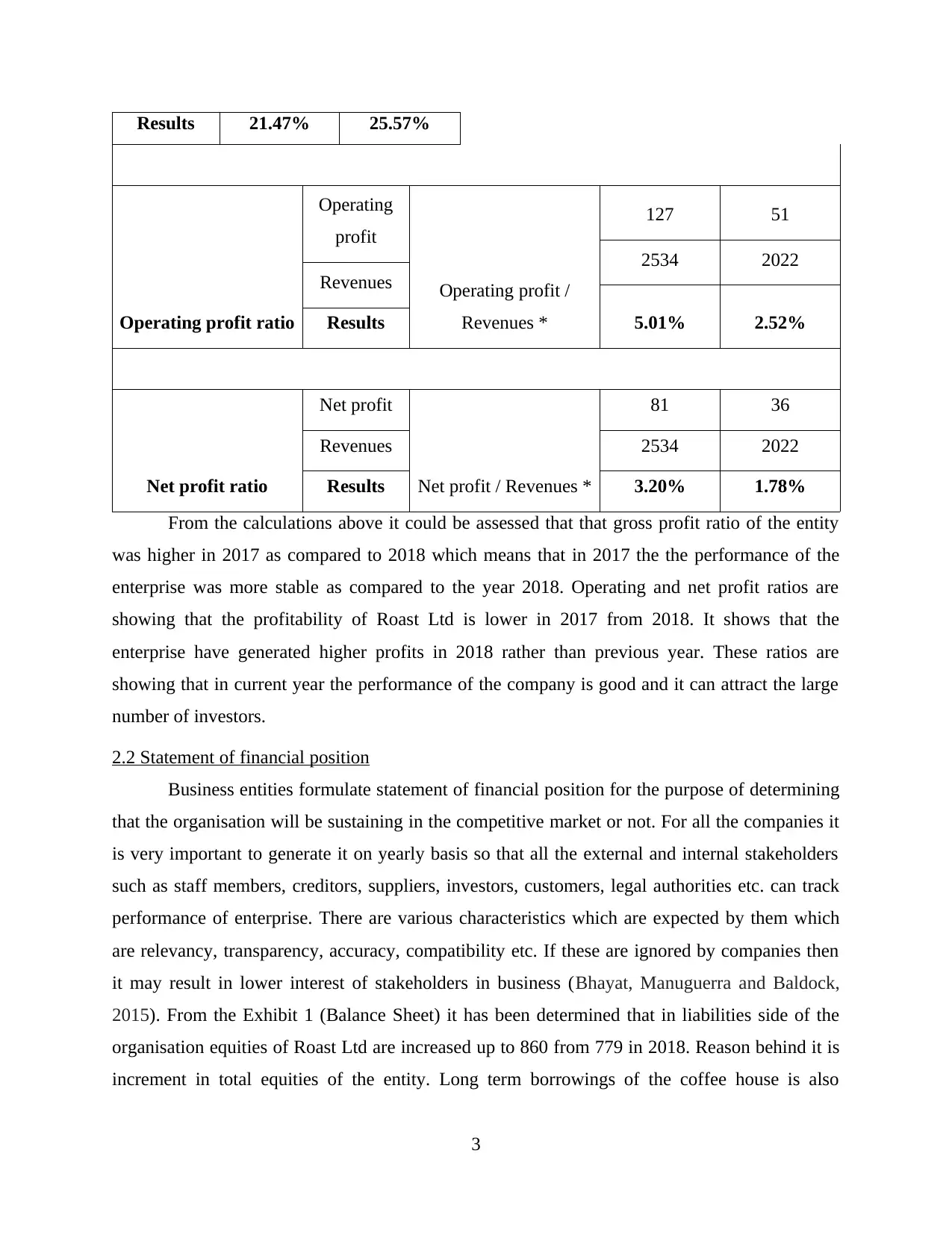

Name of ratio Particulars Formula 2018 2017

Gross profit ratio

Gross profit Gross profit /

Revenues *

544 517

Revenues 2534 2022

2

2.1 Statement of profit and loss

All the business entities generate an account on yearly basis for the purpose of recording

all the direct, indirect, operating and non operating expenses along with incomes so that

profitability could be estimated. In order to attract large number of investors it is very important

for an enterprise to make sure that its income statement is formed in systematic manner so that

external parties can estimate the possible returns which could be generated by them in future

(Almenberg and Dreber, 2015). The exhibit 1 is based upon statement of profit and loss of Roast

Ltd shows that in 2017 revenues of the enterprise were 2022 which are increased up to 2534

which means it will help the entity to maximise its profitability. Total gross profits for the year

ending 2018 are also increased from 517 to 544. Due to this operating profits are also enhanced

from 51 to 127 for 2017. The income statement is also showing an increment in net profit. For

2017 it was 36 and for 2018 it is increased up to 81. For the purpose of analysing financial

performance of the enterprise following ratios are calculated:

Gross profit ratio: In order to determine relation between gross profit and revenues this

ratio is calculated. Main purpose behind using it is to measure operational performance of an

enterprise. In order to measure that Roast Ltd is able to generate good profits or not this ratio

could be calculated.

Operating profit ratio: This ratio is calculated for the purpose of measuring the ability

of an entity to generate profit after paying all the variable costs. It will also be calculated by the

managers to measure the capacity of Roast Ltd to generate profits for upcoming period (Barth,

Papageorge and Thom, 2017).

Net profit ratio: In order to analyse the actual percentage of profits generated for the

year this ratio is calculated as it is calculated after paying all the expenses, dividends, interests

and taxes. It could be used to determine that Roast Ltd is able to reach the goal of acquiring

profits or not.

Calculations for all the above described ratios are as follows:

Name of ratio Particulars Formula 2018 2017

Gross profit ratio

Gross profit Gross profit /

Revenues *

544 517

Revenues 2534 2022

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Results 21.47% 25.57%

Operating profit ratio

Operating

profit

Operating profit /

Revenues *

127 51

2534 2022

Revenues

5.01% 2.52%Results

Net profit ratio

Net profit

Net profit / Revenues *

81 36

Revenues 2534 2022

Results 3.20% 1.78%

From the calculations above it could be assessed that that gross profit ratio of the entity

was higher in 2017 as compared to 2018 which means that in 2017 the the performance of the

enterprise was more stable as compared to the year 2018. Operating and net profit ratios are

showing that the profitability of Roast Ltd is lower in 2017 from 2018. It shows that the

enterprise have generated higher profits in 2018 rather than previous year. These ratios are

showing that in current year the performance of the company is good and it can attract the large

number of investors.

2.2 Statement of financial position

Business entities formulate statement of financial position for the purpose of determining

that the organisation will be sustaining in the competitive market or not. For all the companies it

is very important to generate it on yearly basis so that all the external and internal stakeholders

such as staff members, creditors, suppliers, investors, customers, legal authorities etc. can track

performance of enterprise. There are various characteristics which are expected by them which

are relevancy, transparency, accuracy, compatibility etc. If these are ignored by companies then

it may result in lower interest of stakeholders in business (Bhayat, Manuguerra and Baldock,

2015). From the Exhibit 1 (Balance Sheet) it has been determined that in liabilities side of the

organisation equities of Roast Ltd are increased up to 860 from 779 in 2018. Reason behind it is

increment in total equities of the entity. Long term borrowings of the coffee house is also

3

Operating profit ratio

Operating

profit

Operating profit /

Revenues *

127 51

2534 2022

Revenues

5.01% 2.52%Results

Net profit ratio

Net profit

Net profit / Revenues *

81 36

Revenues 2534 2022

Results 3.20% 1.78%

From the calculations above it could be assessed that that gross profit ratio of the entity

was higher in 2017 as compared to 2018 which means that in 2017 the the performance of the

enterprise was more stable as compared to the year 2018. Operating and net profit ratios are

showing that the profitability of Roast Ltd is lower in 2017 from 2018. It shows that the

enterprise have generated higher profits in 2018 rather than previous year. These ratios are

showing that in current year the performance of the company is good and it can attract the large

number of investors.

2.2 Statement of financial position

Business entities formulate statement of financial position for the purpose of determining

that the organisation will be sustaining in the competitive market or not. For all the companies it

is very important to generate it on yearly basis so that all the external and internal stakeholders

such as staff members, creditors, suppliers, investors, customers, legal authorities etc. can track

performance of enterprise. There are various characteristics which are expected by them which

are relevancy, transparency, accuracy, compatibility etc. If these are ignored by companies then

it may result in lower interest of stakeholders in business (Bhayat, Manuguerra and Baldock,

2015). From the Exhibit 1 (Balance Sheet) it has been determined that in liabilities side of the

organisation equities of Roast Ltd are increased up to 860 from 779 in 2018. Reason behind it is

increment in total equities of the entity. Long term borrowings of the coffee house is also

3

increased which shows that the management have taken loan to carry out operations in future.

Current liabilities of the organisation are also increased from 138 to 308. The causes of this

increment are bank overdraft and inclined trade payables. The assets side is showing increased

non current assets which means that the enterprise have bought new property, plant and

equipments for effective execution of operational activities. Current assets are also increased in

current year due to enhancement in receivables and inventories. For the purpose of analysis of

performance following ratios are also calculated in context of Roast Ltd. Description of all of

them is as follows:

Debt equity ratio: It is one of the common ratio which is used for the purpose of

measuring financial leverage. For all the organisations it is vital to use external liabilities more

than internal funds so that ability of generating higher returns could be improved. In order to

determine the same ability of Roast Ltd this ratio will be calculated (Chambers, Echenique and

Saito, 2016).

Current ratio: It is a type of liquidity ratio which is calculated for the purpose of

determining that an entity can meet all the short term obligation in the period of 12 months or

not. It could be used to determine the liquidity level of Roast Ltd.

Quick ratio: Under this ratio core current assets are taken for the purpose of calculation

in order to determine the ability to meet short term obligation with the help of cash and cash

equivalents. In order to analyse that Roast Ltd is able to pay the current liabilities with quick

assets this ratio will be calculated.

Calculation of all the ratios are as follows:

Name of ratio Particulars Formula 2018 2017

Debt equity ratio

Total debts

Total debts / Total

equities

583 238

Total equities 860 779

Results 0.68 0.31

Current ratio

Current assets Current assets /

Current liabilities

447 347

Current liabilities 308 138

Results 1.45 2.51

4

Current liabilities of the organisation are also increased from 138 to 308. The causes of this

increment are bank overdraft and inclined trade payables. The assets side is showing increased

non current assets which means that the enterprise have bought new property, plant and

equipments for effective execution of operational activities. Current assets are also increased in

current year due to enhancement in receivables and inventories. For the purpose of analysis of

performance following ratios are also calculated in context of Roast Ltd. Description of all of

them is as follows:

Debt equity ratio: It is one of the common ratio which is used for the purpose of

measuring financial leverage. For all the organisations it is vital to use external liabilities more

than internal funds so that ability of generating higher returns could be improved. In order to

determine the same ability of Roast Ltd this ratio will be calculated (Chambers, Echenique and

Saito, 2016).

Current ratio: It is a type of liquidity ratio which is calculated for the purpose of

determining that an entity can meet all the short term obligation in the period of 12 months or

not. It could be used to determine the liquidity level of Roast Ltd.

Quick ratio: Under this ratio core current assets are taken for the purpose of calculation

in order to determine the ability to meet short term obligation with the help of cash and cash

equivalents. In order to analyse that Roast Ltd is able to pay the current liabilities with quick

assets this ratio will be calculated.

Calculation of all the ratios are as follows:

Name of ratio Particulars Formula 2018 2017

Debt equity ratio

Total debts

Total debts / Total

equities

583 238

Total equities 860 779

Results 0.68 0.31

Current ratio

Current assets Current assets /

Current liabilities

447 347

Current liabilities 308 138

Results 1.45 2.51

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratio

Quick assets

Quick assets /

Current liabilities

148 227

Current liabilities 308 138

Results 0.48 times 1.64 times

From the above calculations it has been determined that ability of Roast Ltd to use debts

more than equities is increased in 2018 that reflects the changes in the performance of the

company with time. Results from current ratio are showing that liquidity of the entity is low in

year 2018 as compared to 2017. On the other hand, quick ratio is also very low for 2018. Both of

them are showing that liquidity of the entity is very low. According to statement of financial

position the performance of Roast Ltd is not good because of lower liquidity. Main reason

behind it is zero cash in 2018. Due to this ability of the enterprise to pay the amount of short

term liabilities is also reduced.

2.3 Statement of cash flows

All the business entities formulate a statement to record information regarding cash

inflows and outflows so that actual liquidity of the organisation could be determined it is known

as statement of cash flows. Main purpose behind its formulation is to analyse that the enterprise

is able to meet all the long term goals or not. With the help of it, management can determine that

they can spend money upon future operations or not. While forming it three different activities

are recorded in it which are operating, investing and financing. At the end total of all the

activities is generated so that it can be determined that enterprise have received cash or paid it to

the external parties (Füllbrunn and Luhan, 2015). From the cash flow statement of Roast Ltd it

has been determined that operating profit for the year 2018 is 127 and total cash generated from

operations is 22. Net cash out flow from operating activities of the organisation is 24 and for

investing activities the amount is 358. An inflow of 175 is recorded in the cash flow statement

for financing related operations. Closing balance of cash flow is 73 which is a negative balance.

For the purpose of determining the performance of the company operating cash cycle is

calculated which is as follows:

Operating cash cycle: It is also known as cash conversion cycle which is mainly used by

organisations for the purpose of analysing that how long an enterprise will have liquid assets if

5

Quick assets

Quick assets /

Current liabilities

148 227

Current liabilities 308 138

Results 0.48 times 1.64 times

From the above calculations it has been determined that ability of Roast Ltd to use debts

more than equities is increased in 2018 that reflects the changes in the performance of the

company with time. Results from current ratio are showing that liquidity of the entity is low in

year 2018 as compared to 2017. On the other hand, quick ratio is also very low for 2018. Both of

them are showing that liquidity of the entity is very low. According to statement of financial

position the performance of Roast Ltd is not good because of lower liquidity. Main reason

behind it is zero cash in 2018. Due to this ability of the enterprise to pay the amount of short

term liabilities is also reduced.

2.3 Statement of cash flows

All the business entities formulate a statement to record information regarding cash

inflows and outflows so that actual liquidity of the organisation could be determined it is known

as statement of cash flows. Main purpose behind its formulation is to analyse that the enterprise

is able to meet all the long term goals or not. With the help of it, management can determine that

they can spend money upon future operations or not. While forming it three different activities

are recorded in it which are operating, investing and financing. At the end total of all the

activities is generated so that it can be determined that enterprise have received cash or paid it to

the external parties (Füllbrunn and Luhan, 2015). From the cash flow statement of Roast Ltd it

has been determined that operating profit for the year 2018 is 127 and total cash generated from

operations is 22. Net cash out flow from operating activities of the organisation is 24 and for

investing activities the amount is 358. An inflow of 175 is recorded in the cash flow statement

for financing related operations. Closing balance of cash flow is 73 which is a negative balance.

For the purpose of determining the performance of the company operating cash cycle is

calculated which is as follows:

Operating cash cycle: It is also known as cash conversion cycle which is mainly used by

organisations for the purpose of analysing that how long an enterprise will have liquid assets if

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

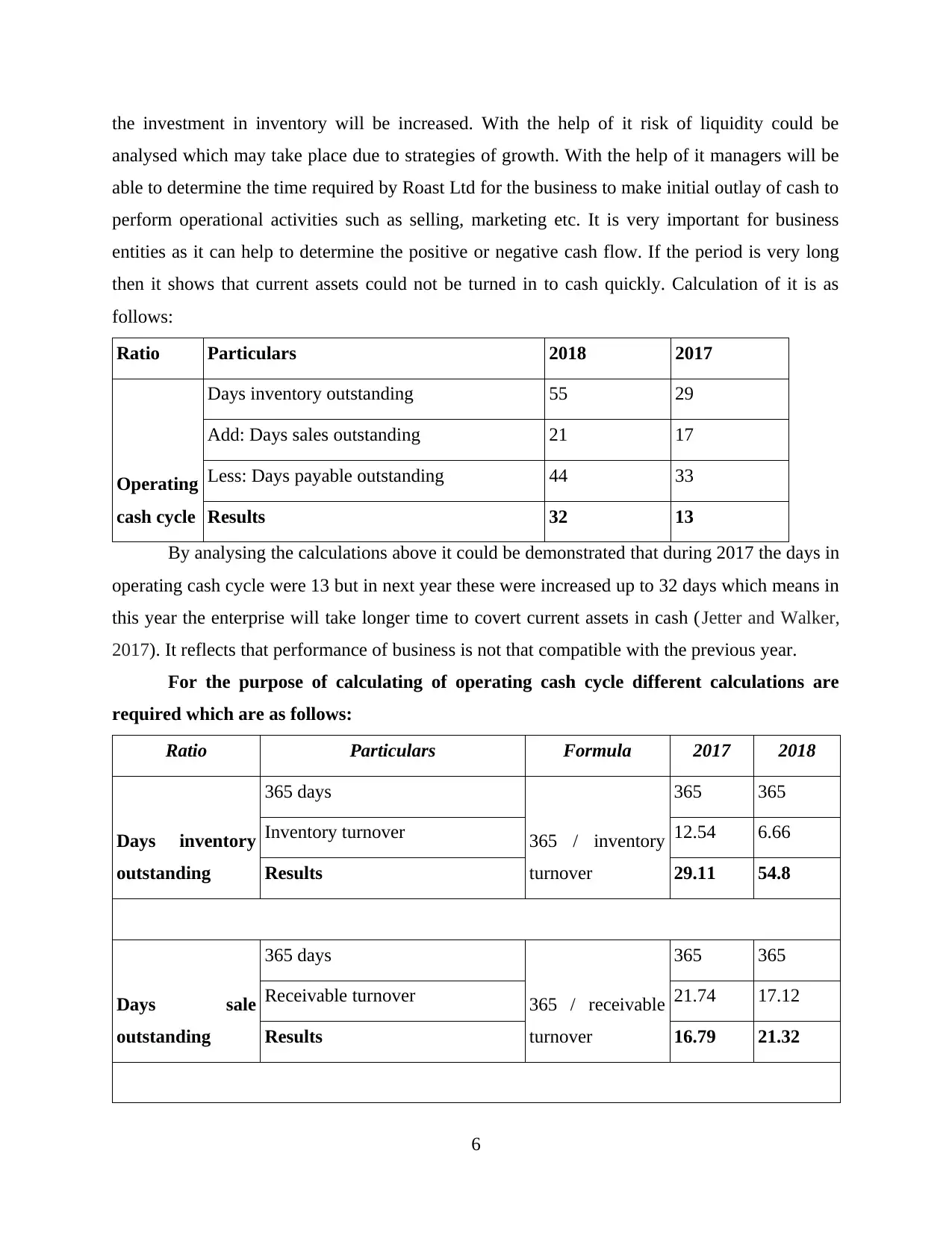

the investment in inventory will be increased. With the help of it risk of liquidity could be

analysed which may take place due to strategies of growth. With the help of it managers will be

able to determine the time required by Roast Ltd for the business to make initial outlay of cash to

perform operational activities such as selling, marketing etc. It is very important for business

entities as it can help to determine the positive or negative cash flow. If the period is very long

then it shows that current assets could not be turned in to cash quickly. Calculation of it is as

follows:

Ratio Particulars 2018 2017

Operating

cash cycle

Days inventory outstanding 55 29

Add: Days sales outstanding 21 17

Less: Days payable outstanding 44 33

Results 32 13

By analysing the calculations above it could be demonstrated that during 2017 the days in

operating cash cycle were 13 but in next year these were increased up to 32 days which means in

this year the enterprise will take longer time to covert current assets in cash (Jetter and Walker,

2017). It reflects that performance of business is not that compatible with the previous year.

For the purpose of calculating of operating cash cycle different calculations are

required which are as follows:

Ratio Particulars Formula 2017 2018

Days inventory

outstanding

365 days

365 / inventory

turnover

365 365

Inventory turnover 12.54 6.66

Results 29.11 54.8

Days sale

outstanding

365 days

365 / receivable

turnover

365 365

Receivable turnover 21.74 17.12

Results 16.79 21.32

6

analysed which may take place due to strategies of growth. With the help of it managers will be

able to determine the time required by Roast Ltd for the business to make initial outlay of cash to

perform operational activities such as selling, marketing etc. It is very important for business

entities as it can help to determine the positive or negative cash flow. If the period is very long

then it shows that current assets could not be turned in to cash quickly. Calculation of it is as

follows:

Ratio Particulars 2018 2017

Operating

cash cycle

Days inventory outstanding 55 29

Add: Days sales outstanding 21 17

Less: Days payable outstanding 44 33

Results 32 13

By analysing the calculations above it could be demonstrated that during 2017 the days in

operating cash cycle were 13 but in next year these were increased up to 32 days which means in

this year the enterprise will take longer time to covert current assets in cash (Jetter and Walker,

2017). It reflects that performance of business is not that compatible with the previous year.

For the purpose of calculating of operating cash cycle different calculations are

required which are as follows:

Ratio Particulars Formula 2017 2018

Days inventory

outstanding

365 days

365 / inventory

turnover

365 365

Inventory turnover 12.54 6.66

Results 29.11 54.8

Days sale

outstanding

365 days

365 / receivable

turnover

365 365

Receivable turnover 21.74 17.12

Results 16.79 21.32

6

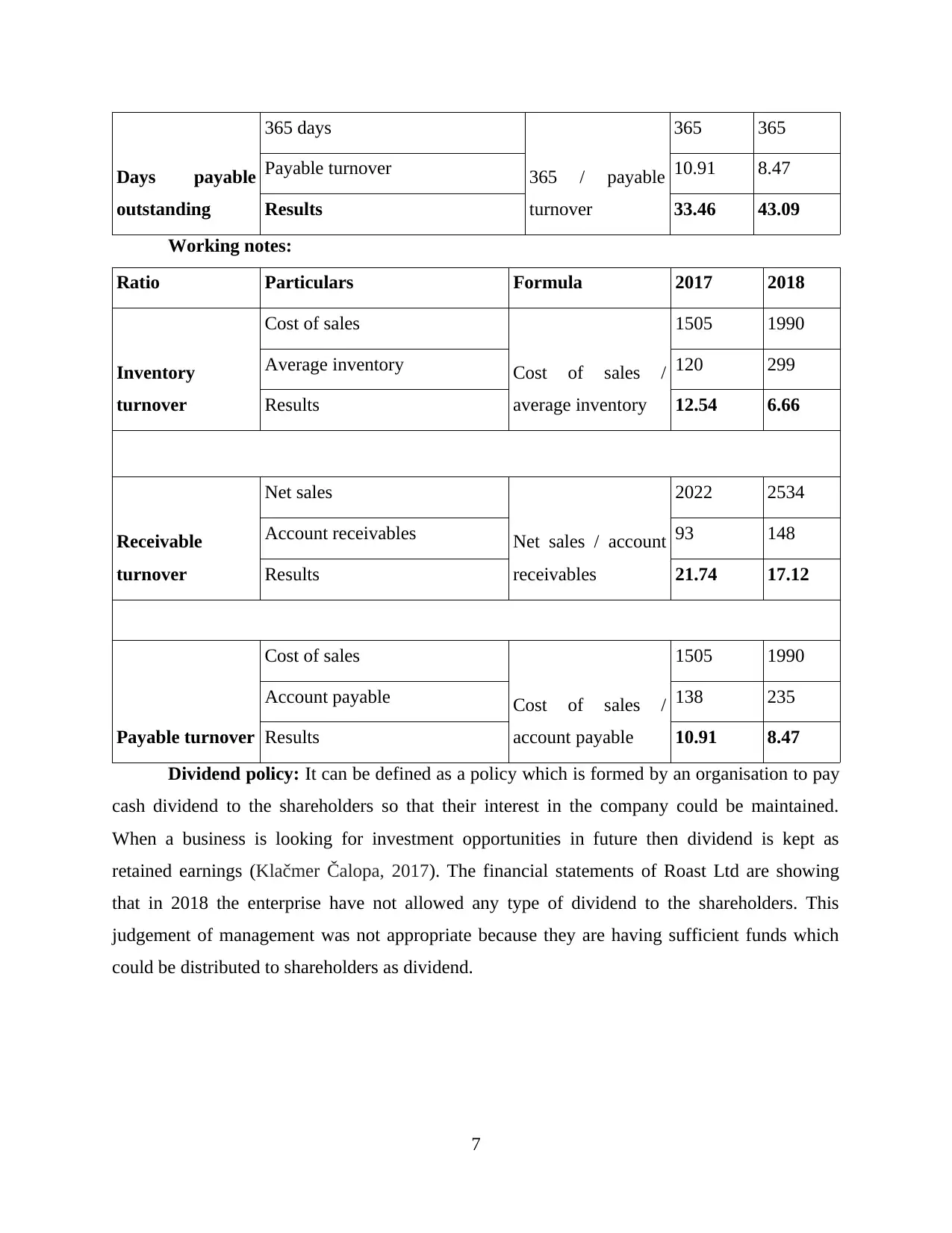

Days payable

outstanding

365 days

365 / payable

turnover

365 365

Payable turnover 10.91 8.47

Results 33.46 43.09

Working notes:

Ratio Particulars Formula 2017 2018

Inventory

turnover

Cost of sales

Cost of sales /

average inventory

1505 1990

Average inventory 120 299

Results 12.54 6.66

Receivable

turnover

Net sales

Net sales / account

receivables

2022 2534

Account receivables 93 148

Results 21.74 17.12

Payable turnover

Cost of sales

Cost of sales /

account payable

1505 1990

Account payable 138 235

Results 10.91 8.47

Dividend policy: It can be defined as a policy which is formed by an organisation to pay

cash dividend to the shareholders so that their interest in the company could be maintained.

When a business is looking for investment opportunities in future then dividend is kept as

retained earnings (Klačmer Čalopa, 2017). The financial statements of Roast Ltd are showing

that in 2018 the enterprise have not allowed any type of dividend to the shareholders. This

judgement of management was not appropriate because they are having sufficient funds which

could be distributed to shareholders as dividend.

7

outstanding

365 days

365 / payable

turnover

365 365

Payable turnover 10.91 8.47

Results 33.46 43.09

Working notes:

Ratio Particulars Formula 2017 2018

Inventory

turnover

Cost of sales

Cost of sales /

average inventory

1505 1990

Average inventory 120 299

Results 12.54 6.66

Receivable

turnover

Net sales

Net sales / account

receivables

2022 2534

Account receivables 93 148

Results 21.74 17.12

Payable turnover

Cost of sales

Cost of sales /

account payable

1505 1990

Account payable 138 235

Results 10.91 8.47

Dividend policy: It can be defined as a policy which is formed by an organisation to pay

cash dividend to the shareholders so that their interest in the company could be maintained.

When a business is looking for investment opportunities in future then dividend is kept as

retained earnings (Klačmer Čalopa, 2017). The financial statements of Roast Ltd are showing

that in 2018 the enterprise have not allowed any type of dividend to the shareholders. This

judgement of management was not appropriate because they are having sufficient funds which

could be distributed to shareholders as dividend.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART 3: Investment Appraisal

3.1 (a) Management forecast

When managers estimates future situations and then formulate decisions according to it

then it is known as management forecast. Main purpose of it is to analyse current trends in the

market and then formulate decision according to it so that it can help to reach long term business

goals. Managers in Roast Ltd. have planned to invest 500 million in a business project in

upcoming period. They have estimated that from year 2017 to 2021 the cash inflow will be 60,

112, 148, 180 and 224 million pounds. By analysing it it has been determined that managers

within the enterprise are expecting increment in the cash flow in the five years period. All the

estimations which are made by them are not based upon any significant elements so it will be

very complex for them to generate same cash inflow.

3.1 (b) Investment appraisal techniques

All the business entities use different types of techniques for the purpose of formulating

future decisions regarding making investment in a project in future. These are NPV, Pay back

period, ARR etc. which could be used by managers of Roast Ltd. for the purpose of making

decision of investing 500 million pounds in a project (Kumar and Goyal, 2015). Description of

all of them with their benefits and limitations is as follows:

Pay back period: It can be defined as a method which could be used by organisations

such as Roast Ltd. for the purpose of determining the time in which the cost which is invested by

them in a project will be recovered. The exhibit 3 shows that the enterprise can recover the

investment in 4 years which means it is a good option for investing 500 million pounds. Some of

the benefits and limitations of this technique are as follows:

Benefits: It is one of the simplest formula which can help the management to determine

that the investment option will be profitable or not. With the help of it, different options

could be evaluated quickly (Lee and Andrade, 2015).

Limitations: With the help of it managers cannot determine that the investment will

result in increased or decreased value of the firm. Apart from this time value of money is

also ignored in this technique which may result in inaccurate results.

Net present value: It can be defined as the process of measuring difference between

discounted cash inflow and initial investment. With the help of it the managers of Roast Ltd. will

8

3.1 (a) Management forecast

When managers estimates future situations and then formulate decisions according to it

then it is known as management forecast. Main purpose of it is to analyse current trends in the

market and then formulate decision according to it so that it can help to reach long term business

goals. Managers in Roast Ltd. have planned to invest 500 million in a business project in

upcoming period. They have estimated that from year 2017 to 2021 the cash inflow will be 60,

112, 148, 180 and 224 million pounds. By analysing it it has been determined that managers

within the enterprise are expecting increment in the cash flow in the five years period. All the

estimations which are made by them are not based upon any significant elements so it will be

very complex for them to generate same cash inflow.

3.1 (b) Investment appraisal techniques

All the business entities use different types of techniques for the purpose of formulating

future decisions regarding making investment in a project in future. These are NPV, Pay back

period, ARR etc. which could be used by managers of Roast Ltd. for the purpose of making

decision of investing 500 million pounds in a project (Kumar and Goyal, 2015). Description of

all of them with their benefits and limitations is as follows:

Pay back period: It can be defined as a method which could be used by organisations

such as Roast Ltd. for the purpose of determining the time in which the cost which is invested by

them in a project will be recovered. The exhibit 3 shows that the enterprise can recover the

investment in 4 years which means it is a good option for investing 500 million pounds. Some of

the benefits and limitations of this technique are as follows:

Benefits: It is one of the simplest formula which can help the management to determine

that the investment option will be profitable or not. With the help of it, different options

could be evaluated quickly (Lee and Andrade, 2015).

Limitations: With the help of it managers cannot determine that the investment will

result in increased or decreased value of the firm. Apart from this time value of money is

also ignored in this technique which may result in inaccurate results.

Net present value: It can be defined as the process of measuring difference between

discounted cash inflow and initial investment. With the help of it the managers of Roast Ltd. will

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

be able to determine the profitability of the project in which they are planning to invest 500

million pounds. The exhibit 3 is showing that the net present value of the project is 110 which is

a positive amount (Lichtenberg, Ficker and Rahman-Filipiak, 2016). Some of its benefits and

limitations are as follows:

Benefits: With the help of it accurate and transparent measurement of profitability could

be performed because time value of money is taken in to consideration in this technique.

It helps in better decision making because it provides accurate results.

Limitations: The method of calculating it is very difficult therefore the managers may

have to spend additional time for its calculations.

Accounting rate of return: It is used in capital budgeting for the purpose of determining

the rate of return which could be acquired on a project after a certain period of time. The exhibit

3 is showing that ARR for the investment for 500 million pound will be 18% therefore it will be

a profitable alternative for Roast Ltd. Its benefits and limitations are as follows:

Benefits: By using ARR technique the managers of the enterprise will be able to get a

clear picture of profitability of project in which they are planning to invest. It is the only

method which is based upon the accounting concepts and it results in accurate and

effective results (Lichtenberg, Qualls and Smyer, 2015).

Limitations: While using this method external factors are ignored that may leave

negative impact upon profitability of the enterprise.

The above discussion demonstrates that the investment option of 500 million pound will

be beneficial for Roast Ltd because all the techniques are showing positive results for it. The

long term goals such as higher profits and sales could be acquired by investing this amount in

business for future. By investing this amount in business the enterprise will be able to increase

the productivity and profitability for upcoming years.

3.2 Sources of finance

In order to perform all the operational and executional activities it is very important for

an organisation to arrange sufficient funds. As Roast Ltd is planning to invest 500 million

pounds so the managers are required to acquire finance for the same. There are various sources

from which monetary resources could be generated. Description of all of them along with their

benefits and drawbacks are as follows:

9

million pounds. The exhibit 3 is showing that the net present value of the project is 110 which is

a positive amount (Lichtenberg, Ficker and Rahman-Filipiak, 2016). Some of its benefits and

limitations are as follows:

Benefits: With the help of it accurate and transparent measurement of profitability could

be performed because time value of money is taken in to consideration in this technique.

It helps in better decision making because it provides accurate results.

Limitations: The method of calculating it is very difficult therefore the managers may

have to spend additional time for its calculations.

Accounting rate of return: It is used in capital budgeting for the purpose of determining

the rate of return which could be acquired on a project after a certain period of time. The exhibit

3 is showing that ARR for the investment for 500 million pound will be 18% therefore it will be

a profitable alternative for Roast Ltd. Its benefits and limitations are as follows:

Benefits: By using ARR technique the managers of the enterprise will be able to get a

clear picture of profitability of project in which they are planning to invest. It is the only

method which is based upon the accounting concepts and it results in accurate and

effective results (Lichtenberg, Qualls and Smyer, 2015).

Limitations: While using this method external factors are ignored that may leave

negative impact upon profitability of the enterprise.

The above discussion demonstrates that the investment option of 500 million pound will

be beneficial for Roast Ltd because all the techniques are showing positive results for it. The

long term goals such as higher profits and sales could be acquired by investing this amount in

business for future. By investing this amount in business the enterprise will be able to increase

the productivity and profitability for upcoming years.

3.2 Sources of finance

In order to perform all the operational and executional activities it is very important for

an organisation to arrange sufficient funds. As Roast Ltd is planning to invest 500 million

pounds so the managers are required to acquire finance for the same. There are various sources

from which monetary resources could be generated. Description of all of them along with their

benefits and drawbacks are as follows:

9

Issuing shares in the market: It is one of the long term source source of fund which can

help an enterprise to arrange funding for business operations. It could be used by Roast Ltd for

the purpose of financing the investment plan of 500 million pounds (Benefits and drawbacks of

issuing shares, 2019). There are various benefits and drawbacks of it which are as follows:

Benefits: It is an easy and long term source of fund which help an organisation to carry

out all the operational activities properly. The decision regarding offering dividend is

based upon the profits the entity is not bound to provide it on yearly basis to the

shareholders.

Drawbacks: If an organisation issues shares then owner have to share the power of

decision making with the external parties which are buying them.

Taking a bank loan: It is a source of fund which is used by business entities to take

external finance. If it is taken by Roast Ltd to fund its investment of 500 million pounds then it is

very important for it to pay interest on a fixed rate to the bank. All the benefits and drawback of

this source are as follows:

Benefits: The interest which is paid by the borrower to the bank is deductible under

income tax law therefore it will help to reduce the expenses and increase the incomes

(Musa, Musová and Debnárová, 2015).

Drawbacks: The interest rate in bank loan is very high due to which a specific amount of

profits will be required to be paid to bank.

From both the above described sources of funds it has been recommended to the

managers of Roast Ltd to select bank loan because if it is selected by them then the owners will

not have to share their power of decision making with the bank. Apart from this, it may also help

to increase the debt equity ratio because it will increase the use of external funds in the

operational activities (Spreng, Karlawish and Marson, 2016). Main reason for this

recommendation is that a bank loan will be paid off after a limited period of time and after than

the amount could be retained as profits.

10

help an enterprise to arrange funding for business operations. It could be used by Roast Ltd for

the purpose of financing the investment plan of 500 million pounds (Benefits and drawbacks of

issuing shares, 2019). There are various benefits and drawbacks of it which are as follows:

Benefits: It is an easy and long term source of fund which help an organisation to carry

out all the operational activities properly. The decision regarding offering dividend is

based upon the profits the entity is not bound to provide it on yearly basis to the

shareholders.

Drawbacks: If an organisation issues shares then owner have to share the power of

decision making with the external parties which are buying them.

Taking a bank loan: It is a source of fund which is used by business entities to take

external finance. If it is taken by Roast Ltd to fund its investment of 500 million pounds then it is

very important for it to pay interest on a fixed rate to the bank. All the benefits and drawback of

this source are as follows:

Benefits: The interest which is paid by the borrower to the bank is deductible under

income tax law therefore it will help to reduce the expenses and increase the incomes

(Musa, Musová and Debnárová, 2015).

Drawbacks: The interest rate in bank loan is very high due to which a specific amount of

profits will be required to be paid to bank.

From both the above described sources of funds it has been recommended to the

managers of Roast Ltd to select bank loan because if it is selected by them then the owners will

not have to share their power of decision making with the bank. Apart from this, it may also help

to increase the debt equity ratio because it will increase the use of external funds in the

operational activities (Spreng, Karlawish and Marson, 2016). Main reason for this

recommendation is that a bank loan will be paid off after a limited period of time and after than

the amount could be retained as profits.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.