Cloths Ltd. Financial Analysis: ROI, RI, Variance Homework Solution

VerifiedAdded on 2023/02/01

|6

|1283

|97

Homework Assignment

AI Summary

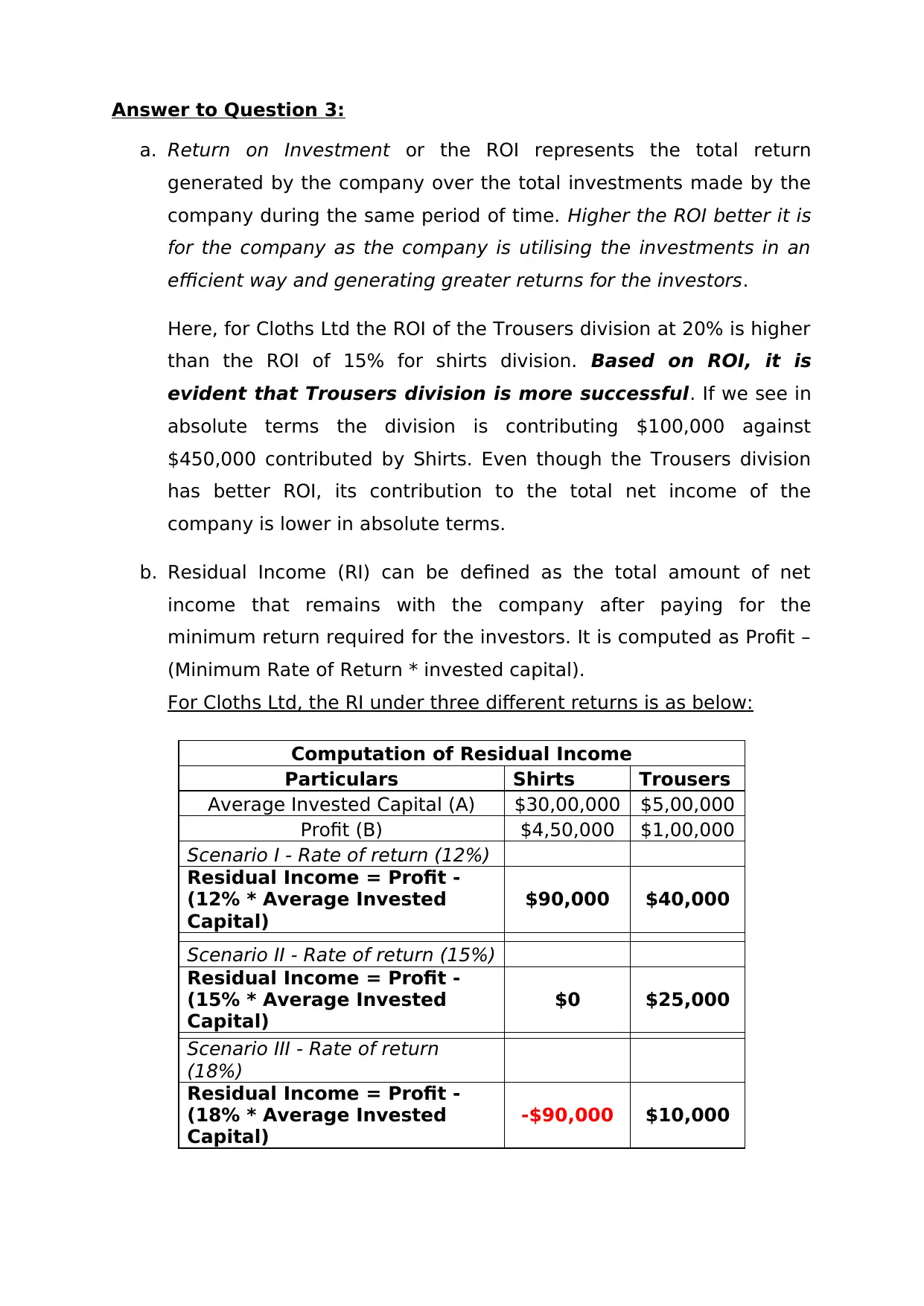

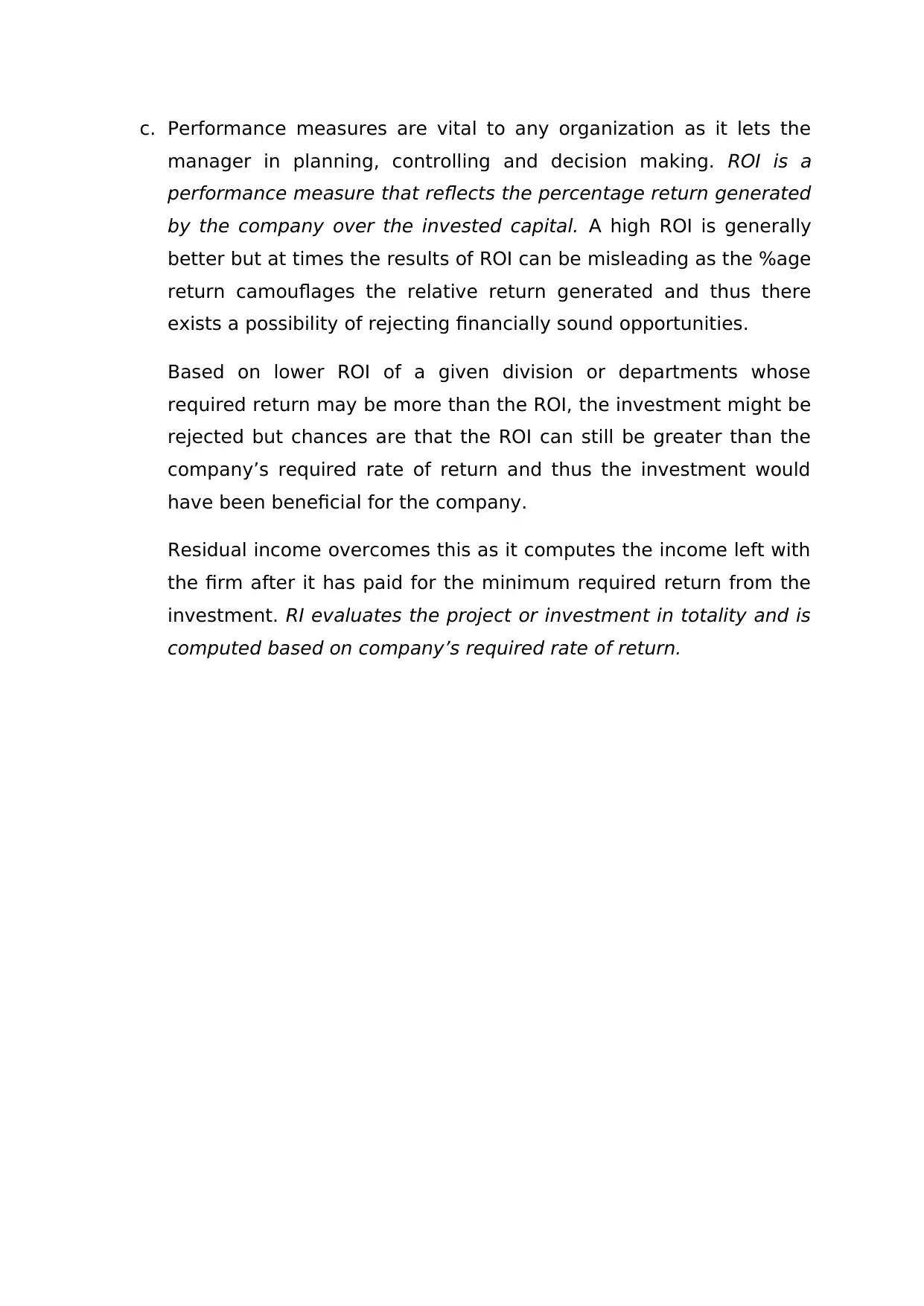

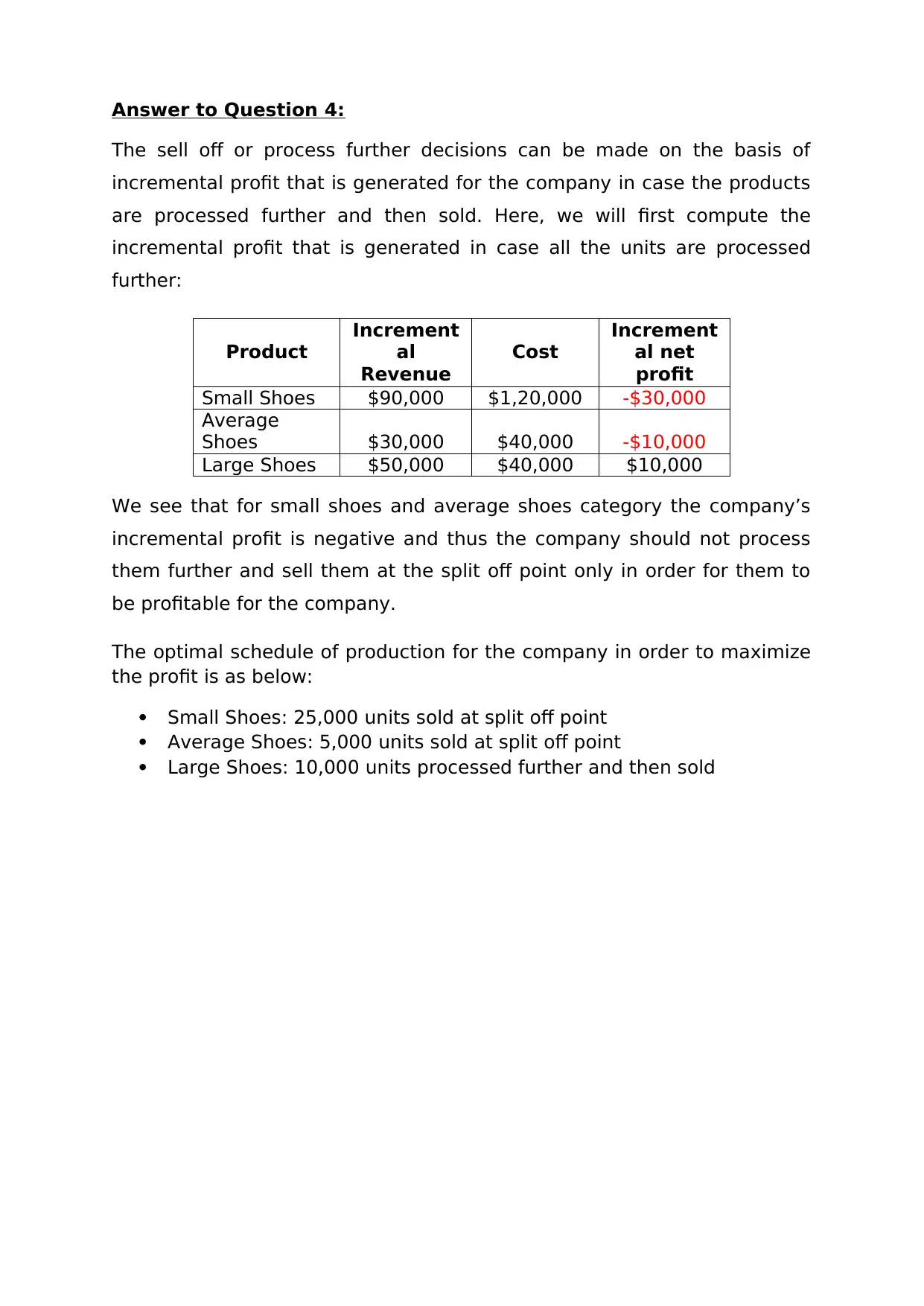

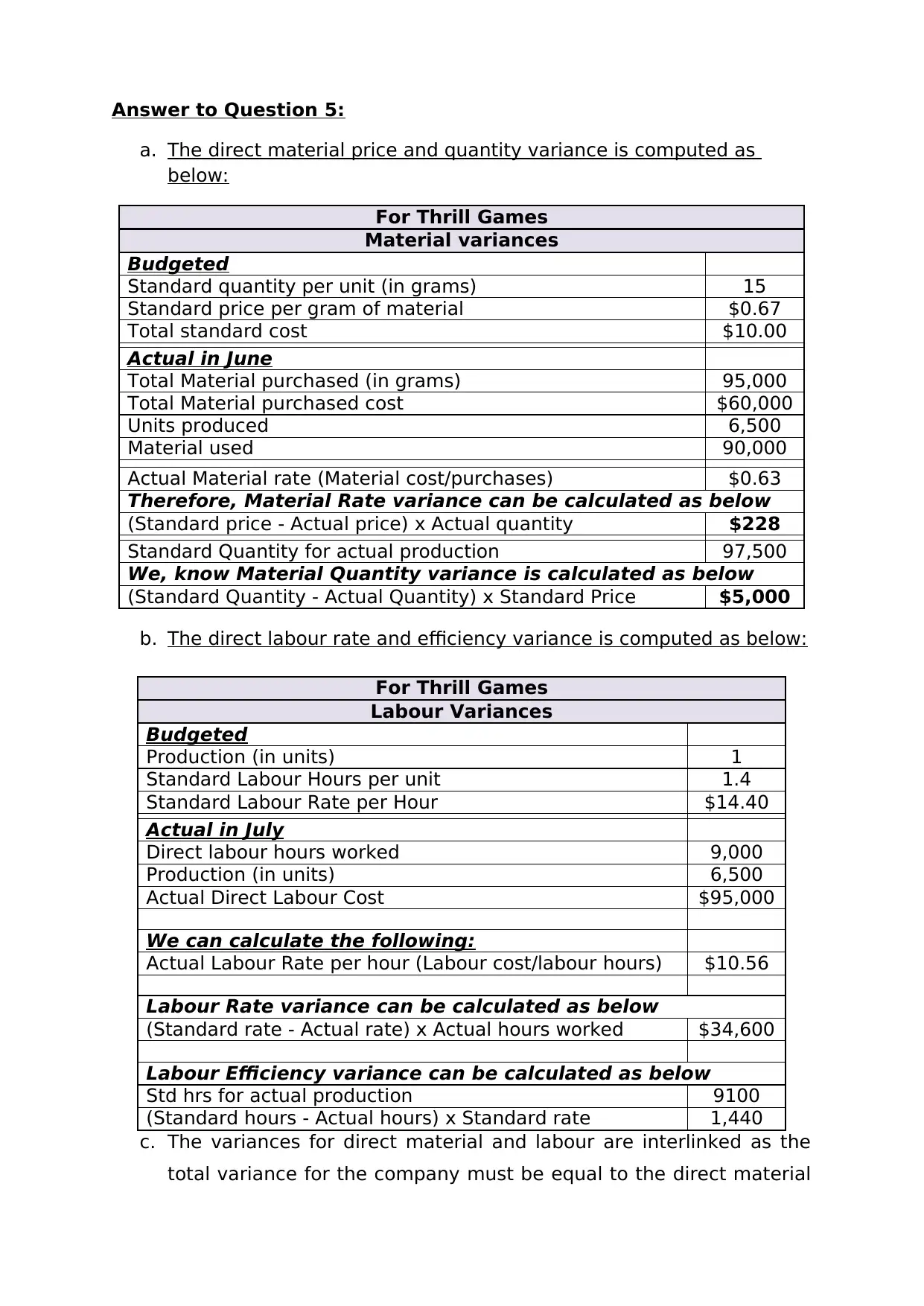

This homework assignment provides solutions to questions on financial performance analysis, specifically focusing on Return on Investment (ROI), Residual Income (RI), and variance analysis. The assignment analyzes the financial performance of Cloths Ltd., comparing the ROI of its Trousers and Shirts divisions and calculating RI under different rates of return. It also covers make or buy decisions based on incremental profit and the optimal production schedule. Furthermore, the solution includes calculations for direct material and labor variances, including rate and efficiency variances, offering insights into cost control and efficiency improvements. References to relevant accounting resources are provided.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.