Accounting Issues: Rolls Royce, FASB Proposal Analysis

VerifiedAdded on 2019/10/30

|13

|2740

|134

Report

AI Summary

This report critically analyzes current accounting issues, focusing on the KPMG investigation into the Rolls-Royce audit and the Financial Accounting Standards Board (FASB) proposal on employee share-based payments. The report delves into the Rolls-Royce case, examining the implications of bribery allegations, the role of the Financial Reporting Council (FRC), and the application of public interest and reputational theories. It also evaluates the FASB proposal, considering responses from various firms regarding accounting standard updates for stock-based compensation, including discussions on tax benefits, expense volatility, and the symmetrical equity approach. The analysis highlights areas of agreement and disagreement among respondents, providing a comprehensive overview of the proposal's significance and potential impact on financial reporting practices.

Running head: REVIEW OF CURRENT ACCOUNTING ISSUES

Review of Current Accounting Issues

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Review of Current Accounting Issues

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1REVIEW OF CURRENT ACCOUNTING ISSUES

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Executive Summary:....................................................................................................................4

Introduction:................................................................................................................................4

Proposal:......................................................................................................................................4

Debate so far:...............................................................................................................................5

Significance of the proposal:.......................................................................................................6

Conclusion:..................................................................................................................................7

References:......................................................................................................................................8

Appendix:......................................................................................................................................10

Name:

Student Number:

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................4

Executive Summary:....................................................................................................................4

Introduction:................................................................................................................................4

Proposal:......................................................................................................................................4

Debate so far:...............................................................................................................................5

Significance of the proposal:.......................................................................................................6

Conclusion:..................................................................................................................................7

References:......................................................................................................................................8

Appendix:......................................................................................................................................10

Name:

Student Number:

2REVIEW OF CURRENT ACCOUNTING ISSUES

Answer to Question 1:

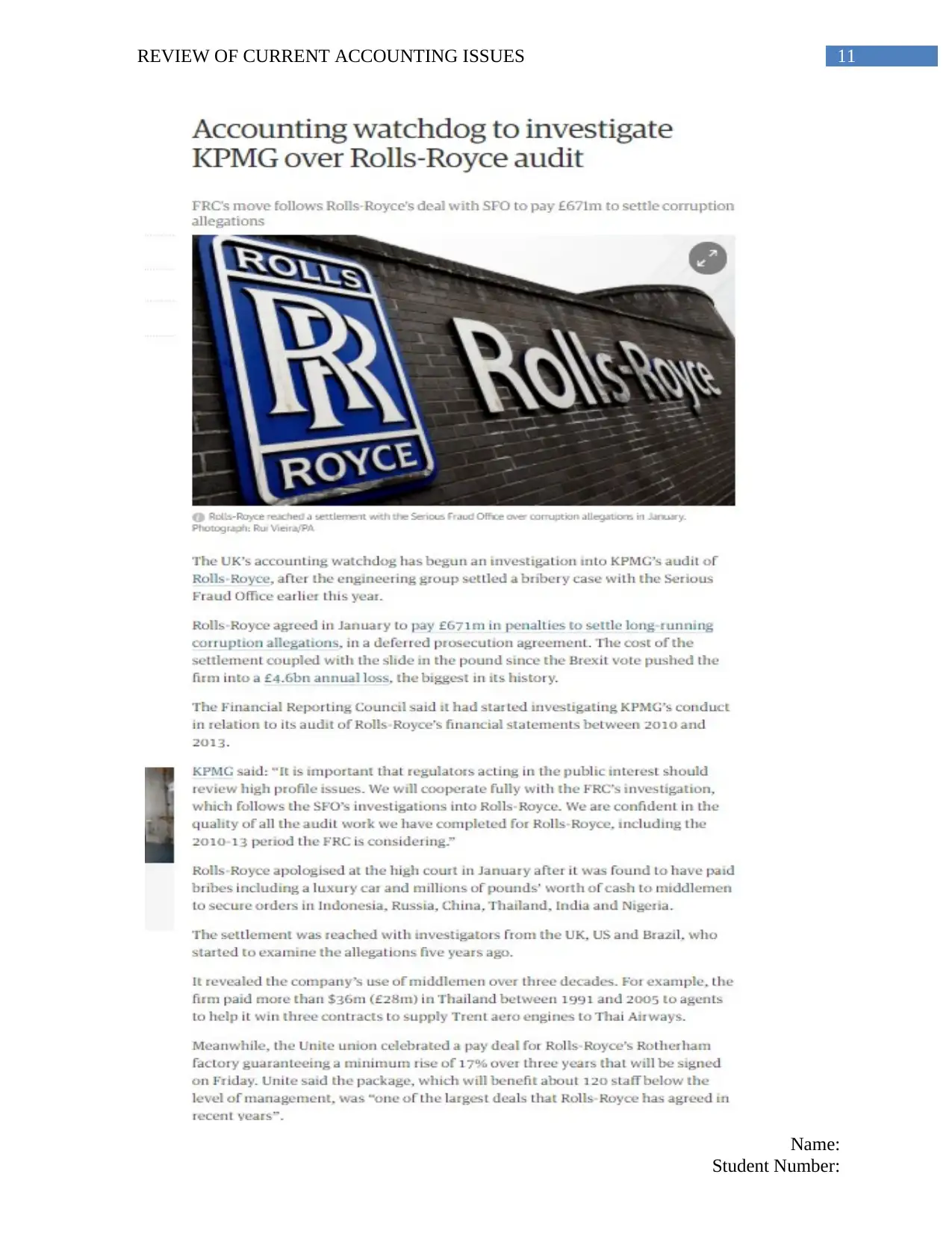

The article chosen for accomplishing the goal of this task is the ““Accounting watchdog

to investigate KPMG over Rolls-Royce audit”. This specific article has been obtained from the

Guardian and it has been published on 4th May 2017. Other articles are available in providing an

effective understanding of the theoretical issues; however, the illegal practices of some audit

firms have adverse effect on the related stakeholders of the concerned firms (Bebbington &

Larrinaga, 2014).

It has been observed that majority of the organisations functioning in the global market

have the intention to increase their overall profit levels. This has been accomplished by

implementing different company strategies primarily in winning the confidence and trust of the

various stakeholders. The main reason behind winning such confidence and trust would enhance

the business operations of the international organisations. As a result, it would help in increasing

the rates of growth and future cash flows (Blayney, Kalyuga & Sweller, 2015). This specific

article intends to explain the step of the “Financial Reporting Council (FRC)” to review the deal

of Rolls Royce with “Serious Fraud Office (SFO) for incurring £671 million in order to settle the

allegations related to corruption. As this specific issue has reached the public, FRC (the

accounting watchdog of UK) has initiated an investigation into the KPMG audit with Rolls

Royce. The reason behind such investigation is that there is involvement of the engineering

group in settling a bribery case with SFO previously in 2017.

Rolls Royce has come to an agreement to incur £671 million in order to settle long-term

allegations of corruption associated with an agreement of deferred prosecution. The cost of

settlement and pound value depreciation because of the Brexit effect has lead to a yearly loss of

4.6 billion. This is the largest for the organisation in its years of operation. Due to this reason,

FRC has carried out its examination to review the KPMG audit associated with the financial

statements of Rolls Royce between 2010 and 2013. The owner of KPMG states that the

regulators need to review the issues related to the public interest. However, according to the

demand of KPMG, the audit work of Rolls Royce has been carried out effectively with full care

ad due diligence for assuring the overall quality of audit. It is to be noted that an apology has

been made on the part of Rolls Royce, as it has bribed the middlepersons to secure orders in

Name:

Student Number:

Answer to Question 1:

The article chosen for accomplishing the goal of this task is the ““Accounting watchdog

to investigate KPMG over Rolls-Royce audit”. This specific article has been obtained from the

Guardian and it has been published on 4th May 2017. Other articles are available in providing an

effective understanding of the theoretical issues; however, the illegal practices of some audit

firms have adverse effect on the related stakeholders of the concerned firms (Bebbington &

Larrinaga, 2014).

It has been observed that majority of the organisations functioning in the global market

have the intention to increase their overall profit levels. This has been accomplished by

implementing different company strategies primarily in winning the confidence and trust of the

various stakeholders. The main reason behind winning such confidence and trust would enhance

the business operations of the international organisations. As a result, it would help in increasing

the rates of growth and future cash flows (Blayney, Kalyuga & Sweller, 2015). This specific

article intends to explain the step of the “Financial Reporting Council (FRC)” to review the deal

of Rolls Royce with “Serious Fraud Office (SFO) for incurring £671 million in order to settle the

allegations related to corruption. As this specific issue has reached the public, FRC (the

accounting watchdog of UK) has initiated an investigation into the KPMG audit with Rolls

Royce. The reason behind such investigation is that there is involvement of the engineering

group in settling a bribery case with SFO previously in 2017.

Rolls Royce has come to an agreement to incur £671 million in order to settle long-term

allegations of corruption associated with an agreement of deferred prosecution. The cost of

settlement and pound value depreciation because of the Brexit effect has lead to a yearly loss of

4.6 billion. This is the largest for the organisation in its years of operation. Due to this reason,

FRC has carried out its examination to review the KPMG audit associated with the financial

statements of Rolls Royce between 2010 and 2013. The owner of KPMG states that the

regulators need to review the issues related to the public interest. However, according to the

demand of KPMG, the audit work of Rolls Royce has been carried out effectively with full care

ad due diligence for assuring the overall quality of audit. It is to be noted that an apology has

been made on the part of Rolls Royce, as it has bribed the middlepersons to secure orders in

Name:

Student Number:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3REVIEW OF CURRENT ACCOUNTING ISSUES

India, Russia, China, Indonesia, Thailand and Nigeria. For example, the organisation has paid

£28 million to the middlepersons in Thailand in order to obtain few contracts (Chatfield &

Vangermeersch, 2014).

Based on the above discussion, the public interest theory and the reputational theory

could be related to this particular article. The theory of public interest states that there is high

fragility in the market and it has the tendency to operate ineffectively in order to favour an

individual rather than benefitting the entire community (Henderson et al., 2015). Thus, for

monitoring this market, the government intervention is required. The pronouncer of this theory

states that there is development of regulations in the public interest in order to correct the

ineffective practices. However, Hodder & Hopkins (2014) argued that from the social

perspective, there are inefficient regulations and there is utilisation of them on the part of the

private players to restrict the entry of competitors in the market.

In this case, it has found out that Rolls Royce has bribed the SFO to settle the corruption

charges. This has resulted in violation of the public interest, since SFO has concentrated on

protecting the actions of the organisation. Moreover, the middlepersons of the different above-

depicted nations have undertaken bribes for securing the organisational contracts. Hence, this is

an unscrupulous measure, which Rolls Royce has conducted in preventing the competitors from

making entry into the markets. Because of the allegations, there is intervention of FRC in

investigating the matter and it has applied stringent regulations on the audit organisations for

evaluating and disclosing the financial statements of the organisation effectively.

According to the reputational theory, the investors normally prefer in dealing with such

organisations with strong reputation in the market along with effective financial growth. In the

words of Kanodia & Sapra (2016), cost-benefit analysis over long-term would represent that the

dishonest actions do not take place for ensuring the overall organisational interests. However, as

argued by Klimczak & Krasodomska (2017), since such action is for long-term, the dishonest

behaviour is likely to obtain short-term benefits. For Rolls Royce, the organisation has made an

unethical practice with SFO for settling its corruption obligations. The primary intention is to

retain the trust of the investors in order to accumulate greater funds for funding capital projects.

From 2010 to 2013, the annual reports of the organisation contain misstatement, which has

enabled Rolls Royce to gather sufficient funds from the investors in undertaking new contracts.

Name:

Student Number:

India, Russia, China, Indonesia, Thailand and Nigeria. For example, the organisation has paid

£28 million to the middlepersons in Thailand in order to obtain few contracts (Chatfield &

Vangermeersch, 2014).

Based on the above discussion, the public interest theory and the reputational theory

could be related to this particular article. The theory of public interest states that there is high

fragility in the market and it has the tendency to operate ineffectively in order to favour an

individual rather than benefitting the entire community (Henderson et al., 2015). Thus, for

monitoring this market, the government intervention is required. The pronouncer of this theory

states that there is development of regulations in the public interest in order to correct the

ineffective practices. However, Hodder & Hopkins (2014) argued that from the social

perspective, there are inefficient regulations and there is utilisation of them on the part of the

private players to restrict the entry of competitors in the market.

In this case, it has found out that Rolls Royce has bribed the SFO to settle the corruption

charges. This has resulted in violation of the public interest, since SFO has concentrated on

protecting the actions of the organisation. Moreover, the middlepersons of the different above-

depicted nations have undertaken bribes for securing the organisational contracts. Hence, this is

an unscrupulous measure, which Rolls Royce has conducted in preventing the competitors from

making entry into the markets. Because of the allegations, there is intervention of FRC in

investigating the matter and it has applied stringent regulations on the audit organisations for

evaluating and disclosing the financial statements of the organisation effectively.

According to the reputational theory, the investors normally prefer in dealing with such

organisations with strong reputation in the market along with effective financial growth. In the

words of Kanodia & Sapra (2016), cost-benefit analysis over long-term would represent that the

dishonest actions do not take place for ensuring the overall organisational interests. However, as

argued by Klimczak & Krasodomska (2017), since such action is for long-term, the dishonest

behaviour is likely to obtain short-term benefits. For Rolls Royce, the organisation has made an

unethical practice with SFO for settling its corruption obligations. The primary intention is to

retain the trust of the investors in order to accumulate greater funds for funding capital projects.

From 2010 to 2013, the annual reports of the organisation contain misstatement, which has

enabled Rolls Royce to gather sufficient funds from the investors in undertaking new contracts.

Name:

Student Number:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4REVIEW OF CURRENT ACCOUNTING ISSUES

As a result, the organisation would make progress in the short-run. However, due to the

publicity of allegations, it has lead to a record loss for the organisation because of loss in the

confidence of the investors. Hence, it could be stated that the allegations imposed on Rolls

Royce could be identical with reputational and public interest theories that necessitate the

requirement for stringent regulations for the audit organisations.

Answer to Question 2:

Executive Summary:

This segment intends to evaluate the improvement proposal, which the “Financial

Accounting Standards Board (FASB)” related with the employee payment share-based

accounting related to the stock of compensation. There are four respondents, which have been

taken into account to provide comments on the exposure draft. The analysis of this segment

signifies that the excess tax benefit and realisation of deficiency in the income statement should

not be undertaken. Along with this, the symmetrical equity approach could be introduced to

minimise the volatility of expenses from the income statement.

Introduction:

FASB has introduced and recommended various accounting standards, as it allows

exposure drafts and comments from various industries and corporate firms. The proposal, which

is under discussion, considers the accounting standard to update the stock-based compensation

and it has the topic number of 718. More particularly, the standard is “Improvements to Non-

employee Share-Based Payment Accounting”. In order to assure cost reduction, it is needed for

improving the non-staff share-based payment. However, certain complexities are related to

prepare and maintain the usefulness of information, which is laid out in the financial statements

of the organisation (Lodhia & Hess, 2014). Finally, the report would concentrate on the various

agreed and non-agreed comments about the initiation of such standard to improve the procedure

of accounting for ascertaining its idealness.

Proposal:

It has been found out that progress in non-staff share-based payment accounting are

critical to maintain the sentiments of the staffs for conducting the business operations in an

effective fashion. This standard has laid forward numerous ideas for encouraging each

Name:

Student Number:

As a result, the organisation would make progress in the short-run. However, due to the

publicity of allegations, it has lead to a record loss for the organisation because of loss in the

confidence of the investors. Hence, it could be stated that the allegations imposed on Rolls

Royce could be identical with reputational and public interest theories that necessitate the

requirement for stringent regulations for the audit organisations.

Answer to Question 2:

Executive Summary:

This segment intends to evaluate the improvement proposal, which the “Financial

Accounting Standards Board (FASB)” related with the employee payment share-based

accounting related to the stock of compensation. There are four respondents, which have been

taken into account to provide comments on the exposure draft. The analysis of this segment

signifies that the excess tax benefit and realisation of deficiency in the income statement should

not be undertaken. Along with this, the symmetrical equity approach could be introduced to

minimise the volatility of expenses from the income statement.

Introduction:

FASB has introduced and recommended various accounting standards, as it allows

exposure drafts and comments from various industries and corporate firms. The proposal, which

is under discussion, considers the accounting standard to update the stock-based compensation

and it has the topic number of 718. More particularly, the standard is “Improvements to Non-

employee Share-Based Payment Accounting”. In order to assure cost reduction, it is needed for

improving the non-staff share-based payment. However, certain complexities are related to

prepare and maintain the usefulness of information, which is laid out in the financial statements

of the organisation (Lodhia & Hess, 2014). Finally, the report would concentrate on the various

agreed and non-agreed comments about the initiation of such standard to improve the procedure

of accounting for ascertaining its idealness.

Proposal:

It has been found out that progress in non-staff share-based payment accounting are

critical to maintain the sentiments of the staffs for conducting the business operations in an

effective fashion. This standard has laid forward numerous ideas for encouraging each

Name:

Student Number:

5REVIEW OF CURRENT ACCOUNTING ISSUES

organisation to participate in the comment process for gaining feedback (Lubbe, Modack &

Watson, 2014). The FASB has depicted the modifications in the form of questions and the

companies are required to comment on the same for obtaining their views. Along with this, the

companies are needed to provide comments on those questions, which are related directly to their

overall business operations. Few questions of the standard comprise of tax benefits and

deficiencies, complexity and cost along with maintaining information evident in the financial

statements. Moreover, they take into account the relation between additional tax benefits and

cash inflows, permission for the entities to undertake the accounting policy election, tax payment

procedure and proposed expansion of the business. By accumulating the feedbacks, the

usefulness of these modifications could be determined for the entire economy.

Debate so far:

The answers that have been gathered from the chosen four respondents are discussed

briefly as follows:

Heiskell and MacGillivray and Associates:

It is an accounting and auditing firm in Australia and it has agreed to the elimination of

the accounting tool of PIC to minimise the level of cost and issues in the process of accounting.

Moreover, it has shown its agreement to incorporate compensation expense in the income

statement, which needs the implementation of tax deficits and benefits. In case of the third

question related to tax cash flow classification, it agrees that these actions could be considered in

the form of operating activity. Hence, the organisation has agreed with all the modifications,

which FASB has proposed, since these questions are in line with the public interest and the

standard of accounting is crucial for both the staffs and organisations (Smith, 2017).

Raytheon Company:

Raytheon Company is a leading technological and innovation firm, which has developed

its brand image in the global market due to defence technologies, software related to civil market

and security tools. It is an US-based organisation intending to form effective corporate

governance. The organisation has answered the questions 2, 3 and 5, which are present in the

exposure draft. It has not agreed with Heiskell and MacGillivary and Associates about

identifying the additional tax benefits and deficiencies in the income statement. Instead, it has

Name:

Student Number:

organisation to participate in the comment process for gaining feedback (Lubbe, Modack &

Watson, 2014). The FASB has depicted the modifications in the form of questions and the

companies are required to comment on the same for obtaining their views. Along with this, the

companies are needed to provide comments on those questions, which are related directly to their

overall business operations. Few questions of the standard comprise of tax benefits and

deficiencies, complexity and cost along with maintaining information evident in the financial

statements. Moreover, they take into account the relation between additional tax benefits and

cash inflows, permission for the entities to undertake the accounting policy election, tax payment

procedure and proposed expansion of the business. By accumulating the feedbacks, the

usefulness of these modifications could be determined for the entire economy.

Debate so far:

The answers that have been gathered from the chosen four respondents are discussed

briefly as follows:

Heiskell and MacGillivray and Associates:

It is an accounting and auditing firm in Australia and it has agreed to the elimination of

the accounting tool of PIC to minimise the level of cost and issues in the process of accounting.

Moreover, it has shown its agreement to incorporate compensation expense in the income

statement, which needs the implementation of tax deficits and benefits. In case of the third

question related to tax cash flow classification, it agrees that these actions could be considered in

the form of operating activity. Hence, the organisation has agreed with all the modifications,

which FASB has proposed, since these questions are in line with the public interest and the

standard of accounting is crucial for both the staffs and organisations (Smith, 2017).

Raytheon Company:

Raytheon Company is a leading technological and innovation firm, which has developed

its brand image in the global market due to defence technologies, software related to civil market

and security tools. It is an US-based organisation intending to form effective corporate

governance. The organisation has answered the questions 2, 3 and 5, which are present in the

exposure draft. It has not agreed with Heiskell and MacGillivary and Associates about

identifying the additional tax benefits and deficiencies in the income statement. Instead, it has

Name:

Student Number:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6REVIEW OF CURRENT ACCOUNTING ISSUES

suggested the symmetrical equity approach to obtain effective outcomes. This is because such

realisation would only accomplish the public interest; however, the organisational interest would

be ignored completely. Moreover, this would not be identical with the capture theory as well.

However, it has been agreed that the taxable cash flows could be considered as operational

activity and it has allowed the stored amount to the highest marginal rate of tax applicable

(Marton, 2017).

Visa Inc:

The organisation is a global leader related to online payment technology intending to

improve the international procedure of payment. It has been assessed that the modifications

would provide several benefits; however, the disagreement is associated with the identification

of additional tax deficiencies and benefits in the income statement (Zhang et al., 2016). These

modifications would reduce complexities for majority of the organisations; however, the

volatility of expense related to income tax might be enhanced. Hence, these modifications

accomplish the overall public interest and organisational interest except the rejected one.

American Bankers Association:

This is an entity where the participants in the bank operate in USA and they tend to

enhance the overall banking system and operating activities. The company has shown its

agreement with all the FASB changes; however, it has compared the tracking of additional tax

benefits and deficiencies in the income statement. The cause behind such disagreement is that it

would lead to differences in the expenses of compensation and financial statements. Hence, in

accordance with this relationship, most of the suggestions would be helpful in assuring both

private and public interest.

Significance of the proposal:

This proposal is crucial to improve the procedures of stock compensation of the

international organisations. It has intended to enhance the preparation of the financial statements

along with reducing the pressure of the accountants and payments of cash related to the

employers for tax holding. The primary problem identified in the proposal is the detection of

additional tax benefits and deficiencies in the income statement of the organisation. This is

because it would help in ensuring the overall public interest to enhance the economy. However,

Name:

Student Number:

suggested the symmetrical equity approach to obtain effective outcomes. This is because such

realisation would only accomplish the public interest; however, the organisational interest would

be ignored completely. Moreover, this would not be identical with the capture theory as well.

However, it has been agreed that the taxable cash flows could be considered as operational

activity and it has allowed the stored amount to the highest marginal rate of tax applicable

(Marton, 2017).

Visa Inc:

The organisation is a global leader related to online payment technology intending to

improve the international procedure of payment. It has been assessed that the modifications

would provide several benefits; however, the disagreement is associated with the identification

of additional tax deficiencies and benefits in the income statement (Zhang et al., 2016). These

modifications would reduce complexities for majority of the organisations; however, the

volatility of expense related to income tax might be enhanced. Hence, these modifications

accomplish the overall public interest and organisational interest except the rejected one.

American Bankers Association:

This is an entity where the participants in the bank operate in USA and they tend to

enhance the overall banking system and operating activities. The company has shown its

agreement with all the FASB changes; however, it has compared the tracking of additional tax

benefits and deficiencies in the income statement. The cause behind such disagreement is that it

would lead to differences in the expenses of compensation and financial statements. Hence, in

accordance with this relationship, most of the suggestions would be helpful in assuring both

private and public interest.

Significance of the proposal:

This proposal is crucial to improve the procedures of stock compensation of the

international organisations. It has intended to enhance the preparation of the financial statements

along with reducing the pressure of the accountants and payments of cash related to the

employers for tax holding. The primary problem identified in the proposal is the detection of

additional tax benefits and deficiencies in the income statement of the organisation. This is

because it would help in ensuring the overall public interest to enhance the economy. However,

Name:

Student Number:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7REVIEW OF CURRENT ACCOUNTING ISSUES

it is required in assuring private interest along with enhancing the proposal validity even though

the public interest is achieved fully.

Conclusion:

Based on the above evaluation, it has been evaluated that Heiskell and MacGillivray and

Associates has agreed with all the modifications pointed out on the part of FASB. However, the

other respondents have failed to agree with the identification of additional tax deficiencies and

benefits in the income statement of the organisation. The reason behind this is that it might raise

the volatility of expense associated with income tax. Hence, it could be concluded that it is

necessary for FASB to assure public interest along with enhancing the validity of the proposal,

even though it helps in accomplishing the overall public interest.

Name:

Student Number:

it is required in assuring private interest along with enhancing the proposal validity even though

the public interest is achieved fully.

Conclusion:

Based on the above evaluation, it has been evaluated that Heiskell and MacGillivray and

Associates has agreed with all the modifications pointed out on the part of FASB. However, the

other respondents have failed to agree with the identification of additional tax deficiencies and

benefits in the income statement of the organisation. The reason behind this is that it might raise

the volatility of expense associated with income tax. Hence, it could be concluded that it is

necessary for FASB to assure public interest along with enhancing the validity of the proposal,

even though it helps in accomplishing the overall public interest.

Name:

Student Number:

8REVIEW OF CURRENT ACCOUNTING ISSUES

References:

Bebbington, J., & Larrinaga, C. (2014). Accounting and sustainable development: An

exploration. Accounting, Organizations and Society, 39(6), 395-413.

Blayney, P., Kalyuga, S., & Sweller, J. (2015). Using cognitive load theory to tailor instruction

to levels of accounting students' expertise. Journal of Educational Technology &

Society, 18(4), 199.

Chatfield, M., & Vangermeersch, R. (2014). The history of accounting (RLE accounting): an

international encylopedia. Routledge.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

Hodder, L. D., & Hopkins, P. E. (2014). Agency problems, accounting slack, and banks’

response to proposed reporting of loan fair values. Accounting, Organizations and

Society, 39(2), 117-133.

Kanodia, C., & Sapra, H. (2016). A real effects perspective to accounting measurement and

disclosure: Implications and insights for future research. Journal of Accounting

Research, 54(2), 623-676.

Klimczak, K. M., & Krasodomska, J. (2017). The role and current status of IFRS in the

completion of national accounting rules–Evidence from Poland. Accounting in Europe, 1-

6.

Lodhia, S., & Hess, N. (2014). Sustainability accounting and reporting in the mining industry:

current literature and directions for future research. Journal of cleaner production, 84,

43-50.

Lubbe, I., Modack, G., & Watson, A. (2014). Financial Accounting GAAP Principles. OUP

Catalogue.

Marton, J. (2017). The role and current status of IFRS in the completion of national accounting

rules–Evidence from Sweden. Accounting in Europe, 1-10.

Name:

Student Number:

References:

Bebbington, J., & Larrinaga, C. (2014). Accounting and sustainable development: An

exploration. Accounting, Organizations and Society, 39(6), 395-413.

Blayney, P., Kalyuga, S., & Sweller, J. (2015). Using cognitive load theory to tailor instruction

to levels of accounting students' expertise. Journal of Educational Technology &

Society, 18(4), 199.

Chatfield, M., & Vangermeersch, R. (2014). The history of accounting (RLE accounting): an

international encylopedia. Routledge.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

Hodder, L. D., & Hopkins, P. E. (2014). Agency problems, accounting slack, and banks’

response to proposed reporting of loan fair values. Accounting, Organizations and

Society, 39(2), 117-133.

Kanodia, C., & Sapra, H. (2016). A real effects perspective to accounting measurement and

disclosure: Implications and insights for future research. Journal of Accounting

Research, 54(2), 623-676.

Klimczak, K. M., & Krasodomska, J. (2017). The role and current status of IFRS in the

completion of national accounting rules–Evidence from Poland. Accounting in Europe, 1-

6.

Lodhia, S., & Hess, N. (2014). Sustainability accounting and reporting in the mining industry:

current literature and directions for future research. Journal of cleaner production, 84,

43-50.

Lubbe, I., Modack, G., & Watson, A. (2014). Financial Accounting GAAP Principles. OUP

Catalogue.

Marton, J. (2017). The role and current status of IFRS in the completion of national accounting

rules–Evidence from Sweden. Accounting in Europe, 1-10.

Name:

Student Number:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9REVIEW OF CURRENT ACCOUNTING ISSUES

Smith, M. (2017). Research methods in accounting. Sage.

Zhang, X., Yan, C., Sun, X., & Xiang, Y. (2016). Research Issues and Methods of Contemporary

Accounting Research and the Progress in Internationalizing Accounting Research in

China: An Analysis of Research Articles in International Accounting Journals During

2009-2013. Contemporary Accounting Review, 1, 001.

Name:

Student Number:

Smith, M. (2017). Research methods in accounting. Sage.

Zhang, X., Yan, C., Sun, X., & Xiang, Y. (2016). Research Issues and Methods of Contemporary

Accounting Research and the Progress in Internationalizing Accounting Research in

China: An Analysis of Research Articles in International Accounting Journals During

2009-2013. Contemporary Accounting Review, 1, 001.

Name:

Student Number:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10REVIEW OF CURRENT ACCOUNTING ISSUES

Appendix:

Name:

Student Number:

Appendix:

Name:

Student Number:

11REVIEW OF CURRENT ACCOUNTING ISSUES

Name:

Student Number:

Name:

Student Number:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.