Financial Analysis of Roots Corporation: Board Report and Case Study

VerifiedAdded on 2022/09/18

|27

|9190

|26

Case Study

AI Summary

This case study analyzes the financial performance of Roots Corporation, examining its interim condensed consolidated financial statements for the 13 and 39 week periods ending November 2, 2019, and November 3, 2018. The analysis, prepared for a board of directors meeting, utilizes the financial analysis framework and financial ratios to assess the company's performance. It includes a review of the statement of financial position, statement of net income (loss), statement of comprehensive income (loss), statement of changes in shareholders' equity, and statement of cash flows. The report identifies areas of concern and potential improvements, offering a comprehensive overview of Roots Corporation's financial health. The analysis covers key financial metrics, including sales, cost of goods sold, gross profit, selling, general and administrative expenses, interest expense, and income taxes. The study also considers basic and diluted earnings per share. Finally, the report offers recommendations for the board's consideration and provides answers to questions that might be posed at the board meeting.

ROOTS CORPORATION

Interim Condensed Consolidated Financial Statements

For the 13 and 39 week periods ended November 2, 2019 and November 3, 2018

In Canadian dollars

(Unaudited)

Interim Condensed Consolidated Financial Statements

For the 13 and 39 week periods ended November 2, 2019 and November 3, 2018

In Canadian dollars

(Unaudited)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

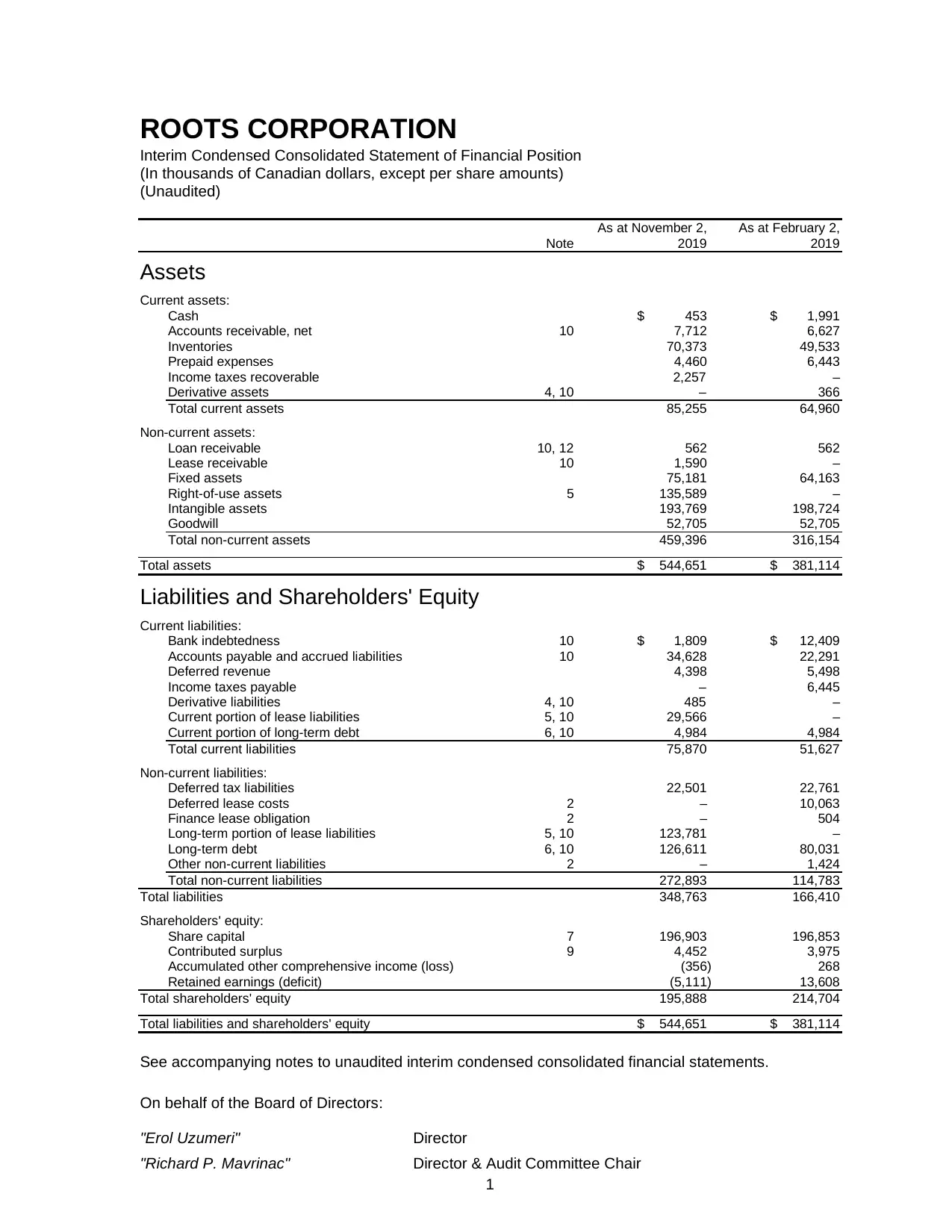

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Financial Position

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

As at November 2, As at February 2,

Note 2019 2019

Assets

Current assets:

Cash $ 453 $ 1,991

Accounts receivable, net 10 7,712 6,627

Inventories 70,373 49,533

Prepaid expenses 4,460 6,443

Income taxes recoverable 2,257 –

Derivative assets 4, 10 – 366

Total current assets 85,255 64,960

Non-current assets:

Loan receivable 10, 12 562 562

Lease receivable 10 1,590 –

Fixed assets 75,181 64,163

Right-of-use assets 5 135,589 –

Intangible assets 193,769 198,724

Goodwill 52,705 52,705

Total non-current assets 459,396 316,154

Total assets $ 544,651 $ 381,114

Liabilities and Shareholders' Equity

Current liabilities:

Bank indebtedness 10 $ 1,809 $ 12,409

Accounts payable and accrued liabilities 10 34,628 22,291

Deferred revenue 4,398 5,498

Income taxes payable – 6,445

Derivative liabilities 4, 10 485 –

Current portion of lease liabilities 5, 10 29,566 –

Current portion of long-term debt 6, 10 4,984 4,984

Total current liabilities 75,870 51,627

Non-current liabilities:

Deferred tax liabilities 22,501 22,761

Deferred lease costs 2 – 10,063

Finance lease obligation 2 – 504

Long-term portion of lease liabilities 5, 10 123,781 –

Long-term debt 6, 10 126,611 80,031

Other non-current liabilities 2 – 1,424

Total non-current liabilities 272,893 114,783

Total liabilities 348,763 166,410

Shareholders' equity:

Share capital 7 196,903 196,853

Contributed surplus 9 4,452 3,975

Accumulated other comprehensive income (loss) (356) 268

Retained earnings (deficit) (5,111) 13,608

Total shareholders' equity 195,888 214,704

Total liabilities and shareholders' equity $ 544,651 $ 381,114

See accompanying notes to unaudited interim condensed consolidated financial statements.

On behalf of the Board of Directors:

"Erol Uzumeri" Director

"Richard P. Mavrinac" Director & Audit Committee Chair

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Financial Position

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

As at November 2, As at February 2,

Note 2019 2019

Assets

Current assets:

Cash $ 453 $ 1,991

Accounts receivable, net 10 7,712 6,627

Inventories 70,373 49,533

Prepaid expenses 4,460 6,443

Income taxes recoverable 2,257 –

Derivative assets 4, 10 – 366

Total current assets 85,255 64,960

Non-current assets:

Loan receivable 10, 12 562 562

Lease receivable 10 1,590 –

Fixed assets 75,181 64,163

Right-of-use assets 5 135,589 –

Intangible assets 193,769 198,724

Goodwill 52,705 52,705

Total non-current assets 459,396 316,154

Total assets $ 544,651 $ 381,114

Liabilities and Shareholders' Equity

Current liabilities:

Bank indebtedness 10 $ 1,809 $ 12,409

Accounts payable and accrued liabilities 10 34,628 22,291

Deferred revenue 4,398 5,498

Income taxes payable – 6,445

Derivative liabilities 4, 10 485 –

Current portion of lease liabilities 5, 10 29,566 –

Current portion of long-term debt 6, 10 4,984 4,984

Total current liabilities 75,870 51,627

Non-current liabilities:

Deferred tax liabilities 22,501 22,761

Deferred lease costs 2 – 10,063

Finance lease obligation 2 – 504

Long-term portion of lease liabilities 5, 10 123,781 –

Long-term debt 6, 10 126,611 80,031

Other non-current liabilities 2 – 1,424

Total non-current liabilities 272,893 114,783

Total liabilities 348,763 166,410

Shareholders' equity:

Share capital 7 196,903 196,853

Contributed surplus 9 4,452 3,975

Accumulated other comprehensive income (loss) (356) 268

Retained earnings (deficit) (5,111) 13,608

Total shareholders' equity 195,888 214,704

Total liabilities and shareholders' equity $ 544,651 $ 381,114

See accompanying notes to unaudited interim condensed consolidated financial statements.

On behalf of the Board of Directors:

"Erol Uzumeri" Director

"Richard P. Mavrinac" Director & Audit Committee Chair

2

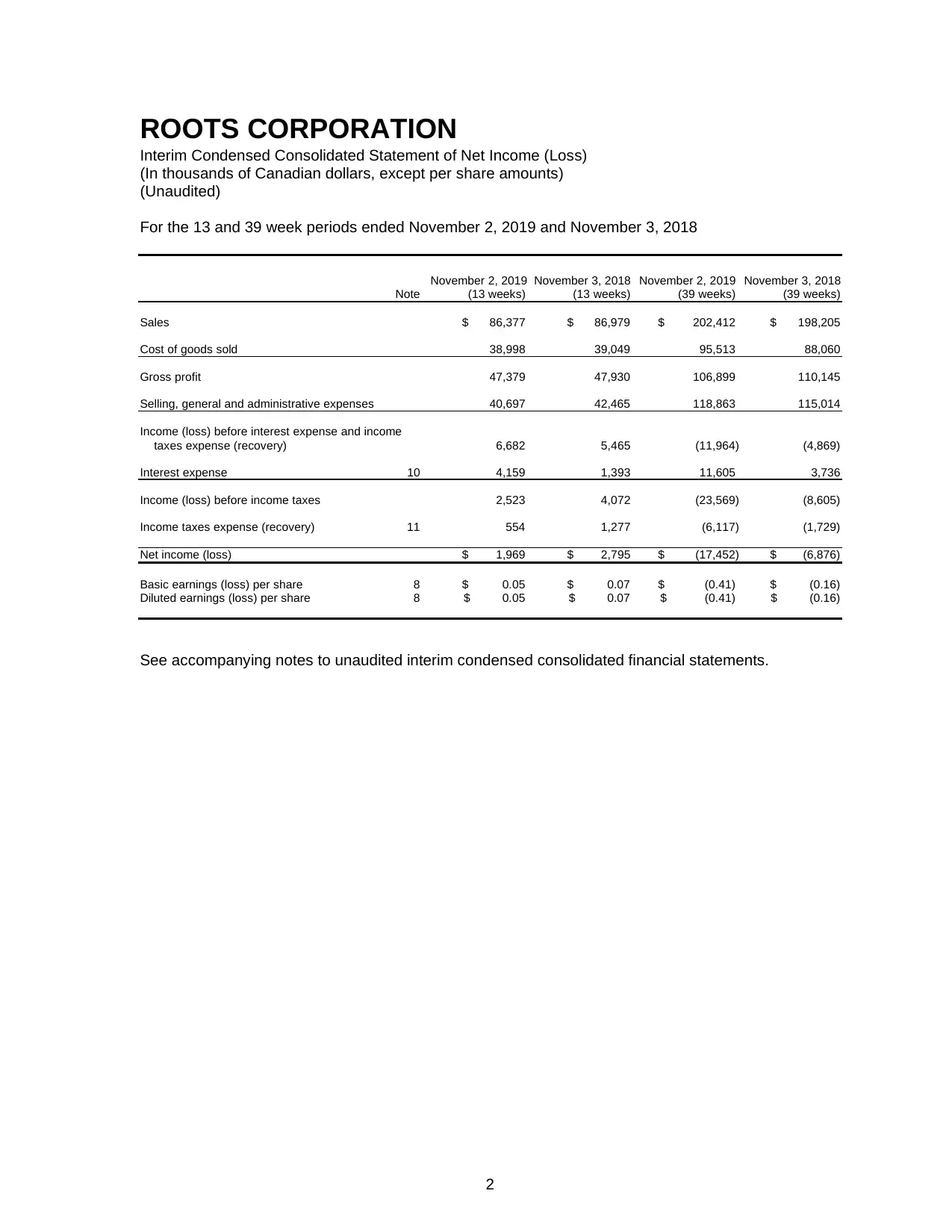

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Net Income (Loss)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 13 and 39 week periods ended November 2, 2019 and November 3, 2018

November 2, 2019 November 3, 2018 November 2, 2019 November 3, 2018

Note (13 weeks) (13 weeks) (39 weeks) (39 weeks)

Sales $ 86,377 $ 86,979 $ 202,412 $ 198,205

Cost of goods sold 38,998 39,049 95,513 88,060

Gross profit 47,379 47,930 106,899 110,145

Selling, general and administrative expenses 40,697 42,465 118,863 115,014

Income (loss) before interest expense and income

taxes expense (recovery) 6,682 5,465 (11,964) (4,869)

Interest expense 10 4,159 1,393 11,605 3,736

Income (loss) before income taxes 2,523 4,072 (23,569) (8,605)

Income taxes expense (recovery) 11 554 1,277 (6,117) (1,729)

Net income (loss) $ 1,969 $ 2,795 $ (17,452) $ (6,876)

Basic earnings (loss) per share 8 $ 0.05 $ 0.07 $ (0.41) $ (0.16)

Diluted earnings (loss) per share 8 $ 0.05 $ 0.07 $ (0.41) $ (0.16)

See accompanying notes to unaudited interim condensed consolidated financial statements.

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Net Income (Loss)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 13 and 39 week periods ended November 2, 2019 and November 3, 2018

November 2, 2019 November 3, 2018 November 2, 2019 November 3, 2018

Note (13 weeks) (13 weeks) (39 weeks) (39 weeks)

Sales $ 86,377 $ 86,979 $ 202,412 $ 198,205

Cost of goods sold 38,998 39,049 95,513 88,060

Gross profit 47,379 47,930 106,899 110,145

Selling, general and administrative expenses 40,697 42,465 118,863 115,014

Income (loss) before interest expense and income

taxes expense (recovery) 6,682 5,465 (11,964) (4,869)

Interest expense 10 4,159 1,393 11,605 3,736

Income (loss) before income taxes 2,523 4,072 (23,569) (8,605)

Income taxes expense (recovery) 11 554 1,277 (6,117) (1,729)

Net income (loss) $ 1,969 $ 2,795 $ (17,452) $ (6,876)

Basic earnings (loss) per share 8 $ 0.05 $ 0.07 $ (0.41) $ (0.16)

Diluted earnings (loss) per share 8 $ 0.05 $ 0.07 $ (0.41) $ (0.16)

See accompanying notes to unaudited interim condensed consolidated financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

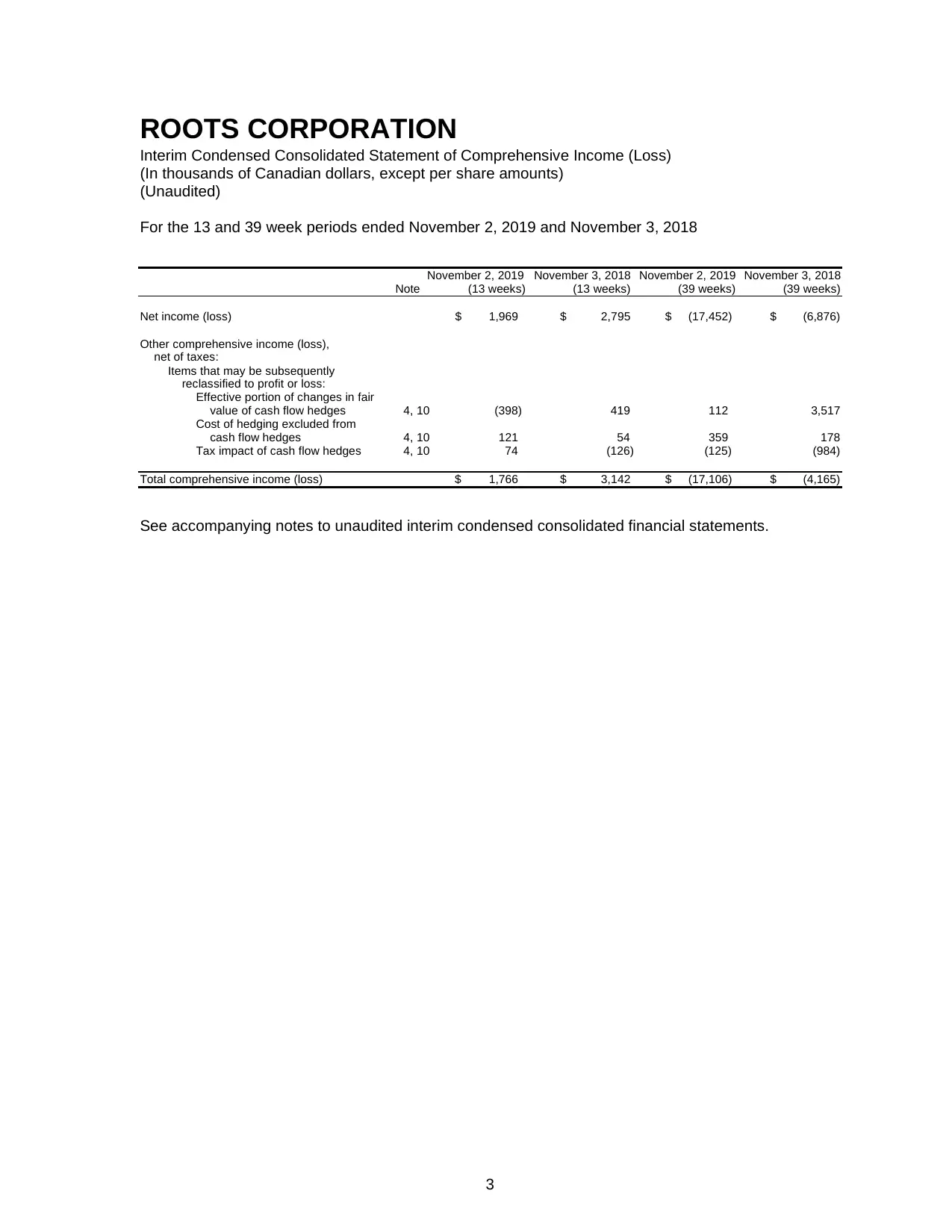

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Comprehensive Income (Loss)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 13 and 39 week periods ended November 2, 2019 and November 3, 2018

November 2, 2019 November 3, 2018 November 2, 2019 November 3, 2018

Note (13 weeks) (13 weeks) (39 weeks) (39 weeks)

Net income (loss) $ 1,969 $ 2,795 $ (17,452) $ (6,876)

Other comprehensive income (loss),

net of taxes:

Items that may be subsequently

reclassified to profit or loss:

Effective portion of changes in fair

value of cash flow hedges 4, 10 (398) 419 112 3,517

Cost of hedging excluded from

cash flow hedges 4, 10 121 54 359 178

Tax impact of cash flow hedges 4, 10 74 (126) (125) (984)

Total comprehensive income (loss) $ 1,766 $ 3,142 $ (17,106) $ (4,165)

See accompanying notes to unaudited interim condensed consolidated financial statements.

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Comprehensive Income (Loss)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 13 and 39 week periods ended November 2, 2019 and November 3, 2018

November 2, 2019 November 3, 2018 November 2, 2019 November 3, 2018

Note (13 weeks) (13 weeks) (39 weeks) (39 weeks)

Net income (loss) $ 1,969 $ 2,795 $ (17,452) $ (6,876)

Other comprehensive income (loss),

net of taxes:

Items that may be subsequently

reclassified to profit or loss:

Effective portion of changes in fair

value of cash flow hedges 4, 10 (398) 419 112 3,517

Cost of hedging excluded from

cash flow hedges 4, 10 121 54 359 178

Tax impact of cash flow hedges 4, 10 74 (126) (125) (984)

Total comprehensive income (loss) $ 1,766 $ 3,142 $ (17,106) $ (4,165)

See accompanying notes to unaudited interim condensed consolidated financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

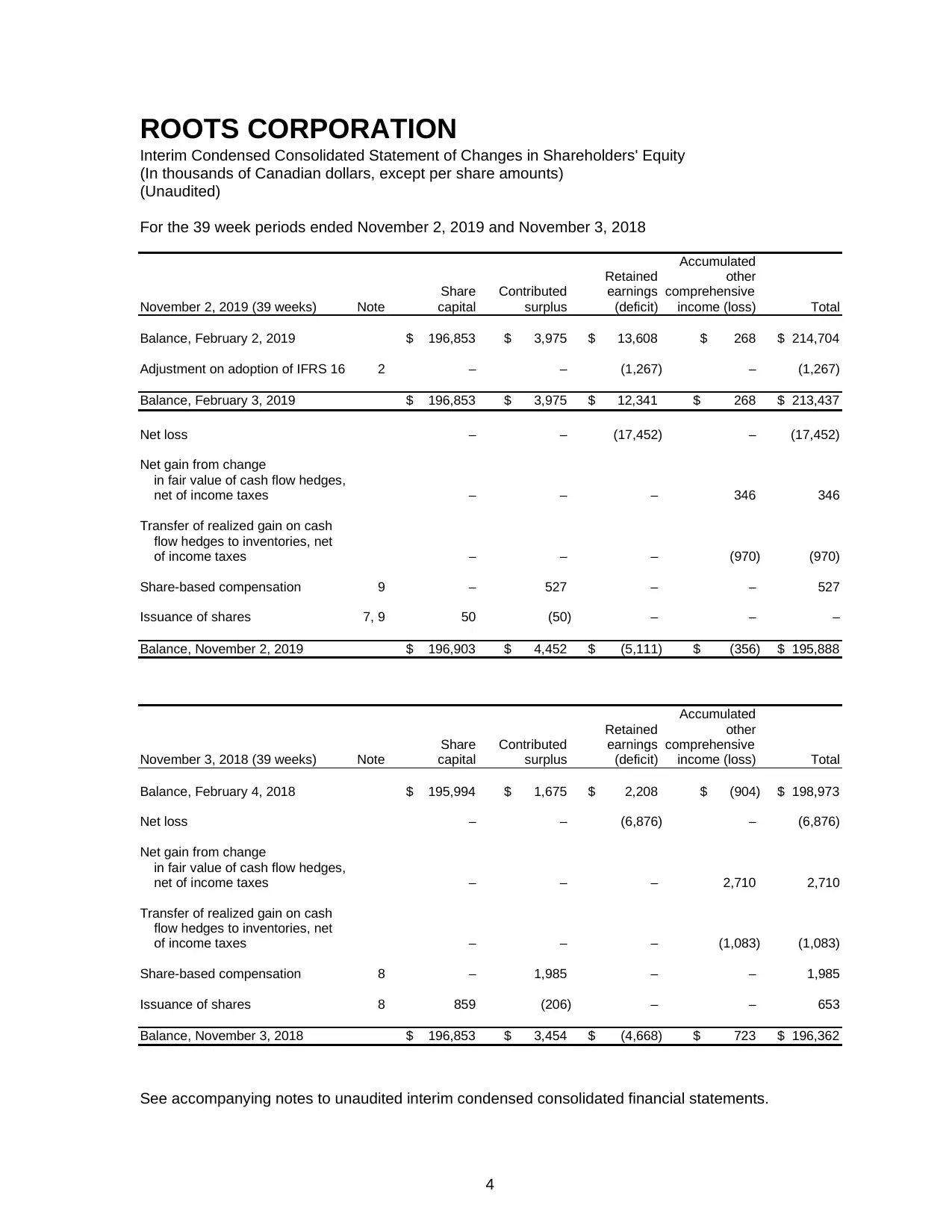

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Changes in Shareholders' Equity

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 39 week periods ended November 2, 2019 and November 3, 2018

Accumulated

Retained other

Share Contributed earnings comprehensive

November 2, 2019 (39 weeks) Note capital surplus (deficit) income (loss) Total

Balance, February 2, 2019 $ 196,853 $ 3,975 $ 13,608 $ 268 $ 214,704

Adjustment on adoption of IFRS 16 2 – – (1,267) – (1,267)

Balance, February 3, 2019 $ 196,853 $ 3,975 $ 12,341 $ 268 $ 213,437

Net loss – – (17,452) – (17,452)

Net gain from change

in fair value of cash flow hedges,

net of income taxes – – – 346 346

Transfer of realized gain on cash

flow hedges to inventories, net

of income taxes – – – (970) (970)

Share-based compensation 9 – 527 – – 527

Issuance of shares 7, 9 50 (50) – – –

Balance, November 2, 2019 $ 196,903 $ 4,452 $ (5,111) $ (356) $ 195,888

Accumulated

Retained other

Share Contributed earnings comprehensive

November 3, 2018 (39 weeks) Note capital surplus (deficit) income (loss) Total

Balance, February 4, 2018 $ 195,994 $ 1,675 $ 2,208 $ (904) $ 198,973

Net loss – – (6,876) – (6,876)

Net gain from change

in fair value of cash flow hedges,

net of income taxes – – – 2,710 2,710

Transfer of realized gain on cash

flow hedges to inventories, net

of income taxes – – – (1,083) (1,083)

Share-based compensation 8 – 1,985 – – 1,985

Issuance of shares 8 859 (206) – – 653

Balance, November 3, 2018 $ 196,853 $ 3,454 $ (4,668) $ 723 $ 196,362

See accompanying notes to unaudited interim condensed consolidated financial statements.

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Changes in Shareholders' Equity

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 39 week periods ended November 2, 2019 and November 3, 2018

Accumulated

Retained other

Share Contributed earnings comprehensive

November 2, 2019 (39 weeks) Note capital surplus (deficit) income (loss) Total

Balance, February 2, 2019 $ 196,853 $ 3,975 $ 13,608 $ 268 $ 214,704

Adjustment on adoption of IFRS 16 2 – – (1,267) – (1,267)

Balance, February 3, 2019 $ 196,853 $ 3,975 $ 12,341 $ 268 $ 213,437

Net loss – – (17,452) – (17,452)

Net gain from change

in fair value of cash flow hedges,

net of income taxes – – – 346 346

Transfer of realized gain on cash

flow hedges to inventories, net

of income taxes – – – (970) (970)

Share-based compensation 9 – 527 – – 527

Issuance of shares 7, 9 50 (50) – – –

Balance, November 2, 2019 $ 196,903 $ 4,452 $ (5,111) $ (356) $ 195,888

Accumulated

Retained other

Share Contributed earnings comprehensive

November 3, 2018 (39 weeks) Note capital surplus (deficit) income (loss) Total

Balance, February 4, 2018 $ 195,994 $ 1,675 $ 2,208 $ (904) $ 198,973

Net loss – – (6,876) – (6,876)

Net gain from change

in fair value of cash flow hedges,

net of income taxes – – – 2,710 2,710

Transfer of realized gain on cash

flow hedges to inventories, net

of income taxes – – – (1,083) (1,083)

Share-based compensation 8 – 1,985 – – 1,985

Issuance of shares 8 859 (206) – – 653

Balance, November 3, 2018 $ 196,853 $ 3,454 $ (4,668) $ 723 $ 196,362

See accompanying notes to unaudited interim condensed consolidated financial statements.

5

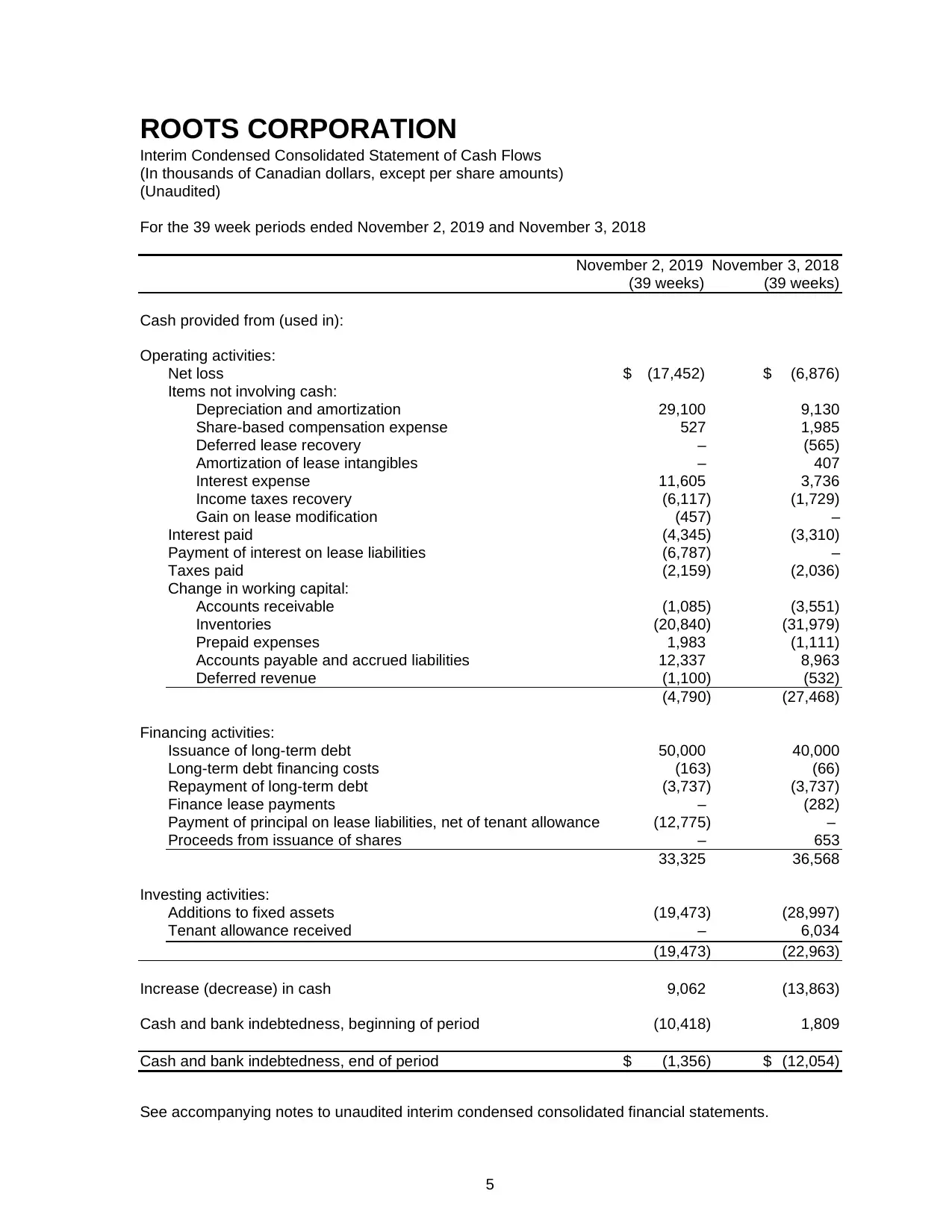

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Cash Flows

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 39 week periods ended November 2, 2019 and November 3, 2018

November 2, 2019 November 3, 2018

(39 weeks) (39 weeks)

Cash provided from (used in):

Operating activities:

Net loss $ (17,452) $ (6,876)

Items not involving cash:

Depreciation and amortization 29,100 9,130

Share-based compensation expense 527 1,985

Deferred lease recovery – (565)

Amortization of lease intangibles – 407

Interest expense 11,605 3,736

Income taxes recovery (6,117) (1,729)

Gain on lease modification (457) –

Interest paid (4,345) (3,310)

Payment of interest on lease liabilities (6,787) –

Taxes paid (2,159) (2,036)

Change in working capital:

Accounts receivable (1,085) (3,551)

Inventories (20,840) (31,979)

Prepaid expenses 1,983 (1,111)

Accounts payable and accrued liabilities 12,337 8,963

Deferred revenue (1,100) (532)

(4,790) (27,468)

Financing activities:

Issuance of long-term debt 50,000 40,000

Long-term debt financing costs (163) (66)

Repayment of long-term debt (3,737) (3,737)

Finance lease payments – (282)

Payment of principal on lease liabilities, net of tenant allowance (12,775) –

Proceeds from issuance of shares – 653

33,325 36,568

Investing activities:

Additions to fixed assets (19,473) (28,997)

Tenant allowance received – 6,034

(19,473) (22,963)

Increase (decrease) in cash 9,062 (13,863)

Cash and bank indebtedness, beginning of period (10,418) 1,809

Cash and bank indebtedness, end of period $ (1,356) $ (12,054)

See accompanying notes to unaudited interim condensed consolidated financial statements.

ROOTS CORPORATION

Interim Condensed Consolidated Statement of Cash Flows

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

For the 39 week periods ended November 2, 2019 and November 3, 2018

November 2, 2019 November 3, 2018

(39 weeks) (39 weeks)

Cash provided from (used in):

Operating activities:

Net loss $ (17,452) $ (6,876)

Items not involving cash:

Depreciation and amortization 29,100 9,130

Share-based compensation expense 527 1,985

Deferred lease recovery – (565)

Amortization of lease intangibles – 407

Interest expense 11,605 3,736

Income taxes recovery (6,117) (1,729)

Gain on lease modification (457) –

Interest paid (4,345) (3,310)

Payment of interest on lease liabilities (6,787) –

Taxes paid (2,159) (2,036)

Change in working capital:

Accounts receivable (1,085) (3,551)

Inventories (20,840) (31,979)

Prepaid expenses 1,983 (1,111)

Accounts payable and accrued liabilities 12,337 8,963

Deferred revenue (1,100) (532)

(4,790) (27,468)

Financing activities:

Issuance of long-term debt 50,000 40,000

Long-term debt financing costs (163) (66)

Repayment of long-term debt (3,737) (3,737)

Finance lease payments – (282)

Payment of principal on lease liabilities, net of tenant allowance (12,775) –

Proceeds from issuance of shares – 653

33,325 36,568

Investing activities:

Additions to fixed assets (19,473) (28,997)

Tenant allowance received – 6,034

(19,473) (22,963)

Increase (decrease) in cash 9,062 (13,863)

Cash and bank indebtedness, beginning of period (10,418) 1,809

Cash and bank indebtedness, end of period $ (1,356) $ (12,054)

See accompanying notes to unaudited interim condensed consolidated financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ROOTS CORPORATION

Notes to Interim Condensed Consolidated Financial Statements

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

6

1. Nature of operations and basis of presentation

Nature of operations

Established in 1973, Roots is a premium outdoor lifestyle brand. We unite the best of cabin and city

through unmistakable style built with uncompromising comfort and quality. We offer a broad range of

products that embody a comfortable cabin-meets-city style including: women’s and men’s apparel,

leather goods, footwear, accessories, and kids, toddler and baby apparel. Starting from a little cabin in

Algonquin Park, Canada, Roots has grown to become a global brand. As at November 2, 2019, we had

115 corporate retail stores in Canada, seven corporate retail stores in the United States, 114 partner-

operated stores in Taiwan, 35 partner-operated stores in China, one partner-operated store in Hong

Kong, and a global eCommerce platform. Roots Corporation is a Canadian corporation doing business

as “Roots” and “Roots Canada”.

Roots Corporation was incorporated under the Canada Business Corporations Act on October 14,

2015. Its head office and registered office is located at 1400 Castlefield Avenue, Toronto, Ontario M6B

4C4. Roots Corporation and its subsidiaries are collectively referred to in these interim condensed

consolidated financial statements (the “interim financial statements”) as the “Company” or “Roots

Corporation”.

The Company’s common shares (“Shares”) are listed on the Toronto Stock Exchange (“TSX”) under

the trading symbol “ROOT”.

The Company experiences seasonal fluctuations in the financial results of its retail business, as a

meaningful portion of its sales and earnings occur in the third and fourth fiscal quarters. The Company’s

working capital requirements generally increase in the periods preceding these peak periods, and it is

not uncommon for net income (loss) before interest expense, income taxes expense (recovery) and

depreciation and amortization (“EBITDA”) to be negative in the first two fiscal quarters.

Basis of presentation

(a) Statement of compliance:

These interim financial statements have been prepared in accordance with International

Accounting Standard (“IAS”) 34, Interim Financial Reporting, as issued by the International

Accounting Standards Board (“IASB”) and the accounting policies described in the

Company’s audited consolidated financial statements as at and for the 52 week period ended

February 2, 2019 (“annual financial statements”), except for the new standards adopted

during the 39 week period ended November 2, 2019, as described below. They do not include

all of the information required for a complete set of International Financial Reporting

Standards (“IFRS”) financial statements. However, select explanatory notes are included to

explain events and transactions that are significant to an understanding of the changes in

the Company’s financial position and performance since the annual financial statements.

Notes to Interim Condensed Consolidated Financial Statements

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

6

1. Nature of operations and basis of presentation

Nature of operations

Established in 1973, Roots is a premium outdoor lifestyle brand. We unite the best of cabin and city

through unmistakable style built with uncompromising comfort and quality. We offer a broad range of

products that embody a comfortable cabin-meets-city style including: women’s and men’s apparel,

leather goods, footwear, accessories, and kids, toddler and baby apparel. Starting from a little cabin in

Algonquin Park, Canada, Roots has grown to become a global brand. As at November 2, 2019, we had

115 corporate retail stores in Canada, seven corporate retail stores in the United States, 114 partner-

operated stores in Taiwan, 35 partner-operated stores in China, one partner-operated store in Hong

Kong, and a global eCommerce platform. Roots Corporation is a Canadian corporation doing business

as “Roots” and “Roots Canada”.

Roots Corporation was incorporated under the Canada Business Corporations Act on October 14,

2015. Its head office and registered office is located at 1400 Castlefield Avenue, Toronto, Ontario M6B

4C4. Roots Corporation and its subsidiaries are collectively referred to in these interim condensed

consolidated financial statements (the “interim financial statements”) as the “Company” or “Roots

Corporation”.

The Company’s common shares (“Shares”) are listed on the Toronto Stock Exchange (“TSX”) under

the trading symbol “ROOT”.

The Company experiences seasonal fluctuations in the financial results of its retail business, as a

meaningful portion of its sales and earnings occur in the third and fourth fiscal quarters. The Company’s

working capital requirements generally increase in the periods preceding these peak periods, and it is

not uncommon for net income (loss) before interest expense, income taxes expense (recovery) and

depreciation and amortization (“EBITDA”) to be negative in the first two fiscal quarters.

Basis of presentation

(a) Statement of compliance:

These interim financial statements have been prepared in accordance with International

Accounting Standard (“IAS”) 34, Interim Financial Reporting, as issued by the International

Accounting Standards Board (“IASB”) and the accounting policies described in the

Company’s audited consolidated financial statements as at and for the 52 week period ended

February 2, 2019 (“annual financial statements”), except for the new standards adopted

during the 39 week period ended November 2, 2019, as described below. They do not include

all of the information required for a complete set of International Financial Reporting

Standards (“IFRS”) financial statements. However, select explanatory notes are included to

explain events and transactions that are significant to an understanding of the changes in

the Company’s financial position and performance since the annual financial statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ROOTS CORPORATION

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

7

These interim financial statements were authorized for issue by the Company’s Board of

Directors on December 5, 2019.

(b) Basis of measurement:

These interim financial statements were prepared on a historical cost basis, except for

derivative financial instruments consisting of forward hedging contracts, and share-based

compensation, which are measured at fair value.

(c) Use of estimates and judgments:

In preparing these interim financial statements, management has made judgments,

estimates and assumptions that affect the application of accounting policies and the reported

amounts of assets and liabilities, income and expense. Actual results may differ from these

estimates.

The significant judgments made by management in applying the Company’s accounting

policies and the key sources of estimation uncertainty were the same as those that applied

to the annual financial statements, except as described in Note 2.

2. Significant accounting policies

Except as described below, the significant accounting policies as disclosed in the annual financial

statements have been applied consistently in the preparation of these interim financial statements:

(a) New standards and interpretations adopted in the period:

In 2016, the IASB issued IFRS 16, Leases (“IFRS 16”), replacing IAS 17, Leases (“IAS 17”),

and related interpretations. The standard introduces a single on-balance sheet recognition

and measurement model for lessees, eliminating the distinction between operating and

finance leases. The lessee recognizes a right-of-use asset representing its control of and

right to use the underlying asset and a lease liability representing its obligation to make future

lease payments. Lessors continue to classify leases as finance and operating leases.

IFRS 16 became effective for annual periods beginning on or after January 1, 2019. The

Company adopted the standard on February 3, 2019 under the modified retrospective

approach, with no restatement of the prior comparative period.

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

7

These interim financial statements were authorized for issue by the Company’s Board of

Directors on December 5, 2019.

(b) Basis of measurement:

These interim financial statements were prepared on a historical cost basis, except for

derivative financial instruments consisting of forward hedging contracts, and share-based

compensation, which are measured at fair value.

(c) Use of estimates and judgments:

In preparing these interim financial statements, management has made judgments,

estimates and assumptions that affect the application of accounting policies and the reported

amounts of assets and liabilities, income and expense. Actual results may differ from these

estimates.

The significant judgments made by management in applying the Company’s accounting

policies and the key sources of estimation uncertainty were the same as those that applied

to the annual financial statements, except as described in Note 2.

2. Significant accounting policies

Except as described below, the significant accounting policies as disclosed in the annual financial

statements have been applied consistently in the preparation of these interim financial statements:

(a) New standards and interpretations adopted in the period:

In 2016, the IASB issued IFRS 16, Leases (“IFRS 16”), replacing IAS 17, Leases (“IAS 17”),

and related interpretations. The standard introduces a single on-balance sheet recognition

and measurement model for lessees, eliminating the distinction between operating and

finance leases. The lessee recognizes a right-of-use asset representing its control of and

right to use the underlying asset and a lease liability representing its obligation to make future

lease payments. Lessors continue to classify leases as finance and operating leases.

IFRS 16 became effective for annual periods beginning on or after January 1, 2019. The

Company adopted the standard on February 3, 2019 under the modified retrospective

approach, with no restatement of the prior comparative period.

ROOTS CORPORATION

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

8

Substantially all of the Company’s existing leases are real estate leases for its retail stores,

distribution centres, leather factory, and corporate head office, and all were classified as

operating leases prior to adoption of IFRS 16. Other operating leases include IT equipment

and certain machinery. On February 3, 2019, the Company recognized right-of-use assets

and lease liabilities for its leases previously classified as operating leases under IAS 17,

except for certain classes of underlying assets for which the lease terms are 12 months or

less. The depreciation expense on right-of-use assets and interest expense on lease

liabilities replaced rent expense, which was previously recognized on a straight-line basis

under IAS 17 over the term of a lease. There are no significant impacts to the Company’s

existing finance leases under IAS 17.

The weighted average lessee’s incremental borrowing rate applied to lease liabilities

recognized in the interim condensed consolidated statement of financial position on February

3, 2019 was 5.8%. The average lease term remaining as at February 3, 2019 was 4.8 years.

IFRS 16 permits the use of recognition exemptions and practical expedients. The Company

applied the following recognition exemptions and practical expedients:

• contracts that were identified as leases under IAS 17 were not reassessed under IFRS

16;

• a single discount rate was applied to a portfolio of leases with reasonably similar

underlying characteristics;

• certain short-term leases were excluded from IFRS 16 lease accounting;

• initial direct costs were excluded in the measurement of the right-of-use assets on

transition; and

• hindsight was used in determining lease term at the date of initial application.

On the date of initial application, the Company applied the requirements of IAS 36,

Impairment of Assets, and recorded a post-tax impairment of $1,267 on right-of-use assets

on February 3, 2019.

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

8

Substantially all of the Company’s existing leases are real estate leases for its retail stores,

distribution centres, leather factory, and corporate head office, and all were classified as

operating leases prior to adoption of IFRS 16. Other operating leases include IT equipment

and certain machinery. On February 3, 2019, the Company recognized right-of-use assets

and lease liabilities for its leases previously classified as operating leases under IAS 17,

except for certain classes of underlying assets for which the lease terms are 12 months or

less. The depreciation expense on right-of-use assets and interest expense on lease

liabilities replaced rent expense, which was previously recognized on a straight-line basis

under IAS 17 over the term of a lease. There are no significant impacts to the Company’s

existing finance leases under IAS 17.

The weighted average lessee’s incremental borrowing rate applied to lease liabilities

recognized in the interim condensed consolidated statement of financial position on February

3, 2019 was 5.8%. The average lease term remaining as at February 3, 2019 was 4.8 years.

IFRS 16 permits the use of recognition exemptions and practical expedients. The Company

applied the following recognition exemptions and practical expedients:

• contracts that were identified as leases under IAS 17 were not reassessed under IFRS

16;

• a single discount rate was applied to a portfolio of leases with reasonably similar

underlying characteristics;

• certain short-term leases were excluded from IFRS 16 lease accounting;

• initial direct costs were excluded in the measurement of the right-of-use assets on

transition; and

• hindsight was used in determining lease term at the date of initial application.

On the date of initial application, the Company applied the requirements of IAS 36,

Impairment of Assets, and recorded a post-tax impairment of $1,267 on right-of-use assets

on February 3, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ROOTS CORPORATION

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

9

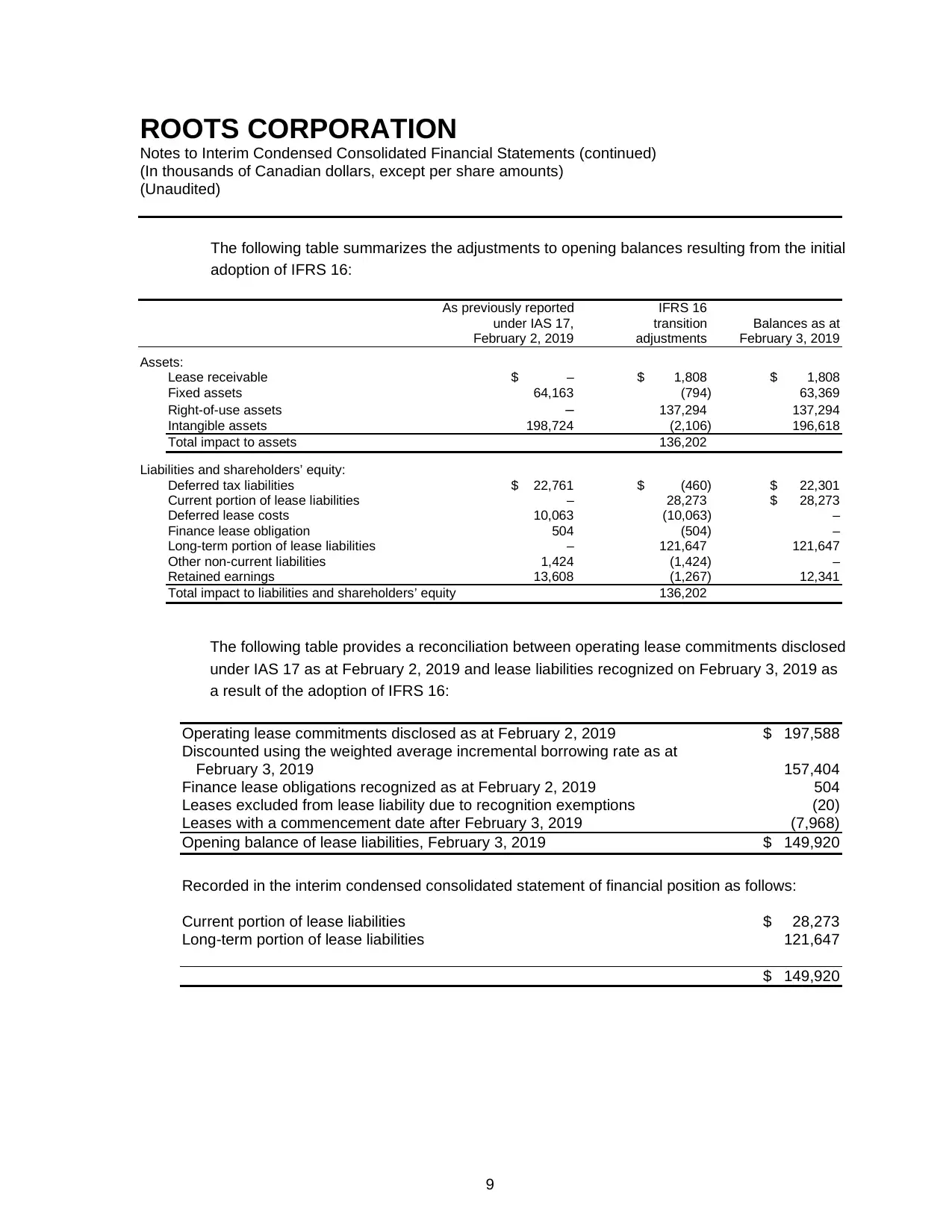

The following table summarizes the adjustments to opening balances resulting from the initial

adoption of IFRS 16:

As previously reported IFRS 16

under IAS 17, transition Balances as at

February 2, 2019 adjustments February 3, 2019

Assets:

Lease receivable $ – $ 1,808 $ 1,808

Fixed assets 64,163 (794) 63,369

Right-of-use assets – 137,294 137,294

Intangible assets 198,724 (2,106) 196,618

Total impact to assets 136,202

Liabilities and shareholders’ equity:

Deferred tax liabilities $ 22,761 $ (460) $ 22,301

Current portion of lease liabilities – 28,273 $ 28,273

Deferred lease costs 10,063 (10,063) –

Finance lease obligation 504 (504) –

Long-term portion of lease liabilities – 121,647 121,647

Other non-current liabilities 1,424 (1,424) –

Retained earnings 13,608 (1,267) 12,341

Total impact to liabilities and shareholders’ equity 136,202

The following table provides a reconciliation between operating lease commitments disclosed

under IAS 17 as at February 2, 2019 and lease liabilities recognized on February 3, 2019 as

a result of the adoption of IFRS 16:

Operating lease commitments disclosed as at February 2, 2019 $ 197,588

Discounted using the weighted average incremental borrowing rate as at

February 3, 2019 157,404

Finance lease obligations recognized as at February 2, 2019 504

Leases excluded from lease liability due to recognition exemptions (20)

Leases with a commencement date after February 3, 2019 (7,968)

Opening balance of lease liabilities, February 3, 2019 $ 149,920

Recorded in the interim condensed consolidated statement of financial position as follows:

Current portion of lease liabilities $ 28,273

Long-term portion of lease liabilities 121,647

$ 149,920

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

9

The following table summarizes the adjustments to opening balances resulting from the initial

adoption of IFRS 16:

As previously reported IFRS 16

under IAS 17, transition Balances as at

February 2, 2019 adjustments February 3, 2019

Assets:

Lease receivable $ – $ 1,808 $ 1,808

Fixed assets 64,163 (794) 63,369

Right-of-use assets – 137,294 137,294

Intangible assets 198,724 (2,106) 196,618

Total impact to assets 136,202

Liabilities and shareholders’ equity:

Deferred tax liabilities $ 22,761 $ (460) $ 22,301

Current portion of lease liabilities – 28,273 $ 28,273

Deferred lease costs 10,063 (10,063) –

Finance lease obligation 504 (504) –

Long-term portion of lease liabilities – 121,647 121,647

Other non-current liabilities 1,424 (1,424) –

Retained earnings 13,608 (1,267) 12,341

Total impact to liabilities and shareholders’ equity 136,202

The following table provides a reconciliation between operating lease commitments disclosed

under IAS 17 as at February 2, 2019 and lease liabilities recognized on February 3, 2019 as

a result of the adoption of IFRS 16:

Operating lease commitments disclosed as at February 2, 2019 $ 197,588

Discounted using the weighted average incremental borrowing rate as at

February 3, 2019 157,404

Finance lease obligations recognized as at February 2, 2019 504

Leases excluded from lease liability due to recognition exemptions (20)

Leases with a commencement date after February 3, 2019 (7,968)

Opening balance of lease liabilities, February 3, 2019 $ 149,920

Recorded in the interim condensed consolidated statement of financial position as follows:

Current portion of lease liabilities $ 28,273

Long-term portion of lease liabilities 121,647

$ 149,920

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ROOTS CORPORATION

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

10

As a result of adopting IFRS 16, the Company updated its lease accounting policies as

follows:

Leased assets

The Company recognizes a right-of-use asset and a lease liability as the present value of

future lease payments when the lessor makes the leased asset available for use by the

Company.

Lease liabilities include the net present value of fixed payments, variable lease payments

that are based on an index or a rate, amounts expected to be payable by the Company under

residual value guarantees, and the exercise price of a purchase option or penalties for

terminating the lease, if the Company is reasonably certain to exercise those purchase or

termination options. Lease liabilities are recognized net of lease incentives receivable. The

lease payments are discounted using the interest rate implicit in the lease, or, if that rate

cannot be readily determined, the lessee’s incremental borrowing rate. Subsequent to initial

measurement, the Company measures lease liabilities at amortized cost using the effective

interest rate method.

Lease terms applied are the contractual non-cancellable periods of the lease, plus periods

covered by renewal options or termination options, if the Company is reasonably certain to

exercise those options. Lease liabilities are remeasured when there is a change in lease

term, a change in the assessment of an option to purchase the leased asset, a change in

expected residual value guarantee, or a change in future lease payments resulting from a

change in an index or a rate used to determine those payments.

Right-of-use assets are measured at cost less accumulated depreciation and accumulated

impairment losses. Cost includes the amount of the initial measurement of the related lease

liability, plus any lease payments made at or before the commencement date and any initial

direct costs and future restoration costs, less any lease incentives received. Right-of-use

assets are depreciated on a straight-line basis from the date that the underlying asset is

available for use. Depreciation is recorded over the shorter of the lease term and the useful

life of the underlying asset, unless the lease transfers ownership of the underlying asset to

the lessee by the end of the lease term, in which case depreciation is recorded over the

useful life of the underlying asset.

Lease payments for assets that are exempt through the short-term exemption and variable

payments not based on an index or rate continue to be recognized in selling, general and

administrative expenses.

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

10

As a result of adopting IFRS 16, the Company updated its lease accounting policies as

follows:

Leased assets

The Company recognizes a right-of-use asset and a lease liability as the present value of

future lease payments when the lessor makes the leased asset available for use by the

Company.

Lease liabilities include the net present value of fixed payments, variable lease payments

that are based on an index or a rate, amounts expected to be payable by the Company under

residual value guarantees, and the exercise price of a purchase option or penalties for

terminating the lease, if the Company is reasonably certain to exercise those purchase or

termination options. Lease liabilities are recognized net of lease incentives receivable. The

lease payments are discounted using the interest rate implicit in the lease, or, if that rate

cannot be readily determined, the lessee’s incremental borrowing rate. Subsequent to initial

measurement, the Company measures lease liabilities at amortized cost using the effective

interest rate method.

Lease terms applied are the contractual non-cancellable periods of the lease, plus periods

covered by renewal options or termination options, if the Company is reasonably certain to

exercise those options. Lease liabilities are remeasured when there is a change in lease

term, a change in the assessment of an option to purchase the leased asset, a change in

expected residual value guarantee, or a change in future lease payments resulting from a

change in an index or a rate used to determine those payments.

Right-of-use assets are measured at cost less accumulated depreciation and accumulated

impairment losses. Cost includes the amount of the initial measurement of the related lease

liability, plus any lease payments made at or before the commencement date and any initial

direct costs and future restoration costs, less any lease incentives received. Right-of-use

assets are depreciated on a straight-line basis from the date that the underlying asset is

available for use. Depreciation is recorded over the shorter of the lease term and the useful

life of the underlying asset, unless the lease transfers ownership of the underlying asset to

the lessee by the end of the lease term, in which case depreciation is recorded over the

useful life of the underlying asset.

Lease payments for assets that are exempt through the short-term exemption and variable

payments not based on an index or rate continue to be recognized in selling, general and

administrative expenses.

ROOTS CORPORATION

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

11

Subleases

When the Company enters into sublease arrangements as an intermediate lessor, it

assesses whether the sublease is classified as a finance sublease or an operating sublease

by reference to the corresponding right-of-use asset arising from the head lease, rather than

by reference to the underlying asset. A sublease is a finance sublease if substantially all the

risks and rewards incidental to ownership of the related right-of-use asset on the head lease

have been transferred to the sub-lessee.

Use of estimates and judgments in lease accounting

The Company has applied judgment to determine the lease term for some lease contracts

that include renewal or termination options. The assessment of whether the Company is

reasonably certain to exercise such options impacts the lease term, which significantly affects

the amount of lease liabilities and right-of-use assets recognized.

The Company is required to estimate the incremental borrowing rates used to discount lease

liabilities if the interest rate implicit in the lease is not readily determined. In determining the

incremental borrowing rates, management considers the Company’s creditworthiness, the

security, the term, the value of the underlying leased asset, and the economic operational

environment of the leased asset. The incremental borrowing rates are subject to change

mainly due to macroeconomic changes.

(b) New standards and interpretations not yet adopted:

The IASB has not issued any significant new accounting standards that impact the Company

since the standards described in the most recent annual financial statements for the year

ended February 2, 2019. The Company continues to monitor future IFRS changes proposed

by the IASB that may have an impact on the Company’s results.

Notes to Interim Condensed Consolidated Financial Statements (continued)

(In thousands of Canadian dollars, except per share amounts)

(Unaudited)

11

Subleases

When the Company enters into sublease arrangements as an intermediate lessor, it

assesses whether the sublease is classified as a finance sublease or an operating sublease

by reference to the corresponding right-of-use asset arising from the head lease, rather than

by reference to the underlying asset. A sublease is a finance sublease if substantially all the

risks and rewards incidental to ownership of the related right-of-use asset on the head lease

have been transferred to the sub-lessee.

Use of estimates and judgments in lease accounting

The Company has applied judgment to determine the lease term for some lease contracts

that include renewal or termination options. The assessment of whether the Company is

reasonably certain to exercise such options impacts the lease term, which significantly affects

the amount of lease liabilities and right-of-use assets recognized.

The Company is required to estimate the incremental borrowing rates used to discount lease

liabilities if the interest rate implicit in the lease is not readily determined. In determining the

incremental borrowing rates, management considers the Company’s creditworthiness, the

security, the term, the value of the underlying leased asset, and the economic operational

environment of the leased asset. The incremental borrowing rates are subject to change

mainly due to macroeconomic changes.

(b) New standards and interpretations not yet adopted:

The IASB has not issued any significant new accounting standards that impact the Company

since the standards described in the most recent annual financial statements for the year

ended February 2, 2019. The Company continues to monitor future IFRS changes proposed

by the IASB that may have an impact on the Company’s results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.