Valuation and Strategic Analysis of Rosetta Stone's IPO Initiative

VerifiedAdded on 2019/12/04

|24

|7458

|167

Project

AI Summary

This project provides a comprehensive financial and strategic analysis of Rosetta Stone's Initial Public Offering (IPO). It begins by describing the key features of Rosetta Stone's business model, including its cloud-based approach to language learning solutions and its strategic acquisitions. The project then evaluates the advantages and disadvantages of the company undertaking an IPO, considering factors such as capital raising and increased public scrutiny. Furthermore, it applies both the market-multiples approach and a free cash flow valuation model to determine a suitable share price for the IPO. The analysis includes an assessment of the reasonable rate of return on an investment in Rosetta Stone and concludes with recommendations on deciding an offer price for the IPO, providing a well-rounded evaluation of the company's financial prospects and strategic positioning. The project is a detailed examination of the key elements involved in the IPO process and the factors influencing the valuation of the company.

Financial entrepreneurial

initiatives

1

initiatives

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Rosetta Stone .......................................................................................................................................3

1. Describe the key features of Rosetta Stone's business model and its strategy............................3

2. Advantage and disadvantage of Rosseta stone undertaking an IPO............................................4

3. Market-Multiples approach to identify range of prices for an IPO.............................................6

4. Application of Market-Multiple approach to arrive at a suitable share price for IPO.................7

5. Reasonable rate of return on an investment in Rosetta Stone......................................................8

6. Apply a Free Cash Flow model to Rosetta Stone to arrive at valuation......................................9

7. Deciding an offer price for Rosetta Stone's IPO........................................................................11

REFERENCES...................................................................................................................................12

2

Rosetta Stone .......................................................................................................................................3

1. Describe the key features of Rosetta Stone's business model and its strategy............................3

2. Advantage and disadvantage of Rosseta stone undertaking an IPO............................................4

3. Market-Multiples approach to identify range of prices for an IPO.............................................6

4. Application of Market-Multiple approach to arrive at a suitable share price for IPO.................7

5. Reasonable rate of return on an investment in Rosetta Stone......................................................8

6. Apply a Free Cash Flow model to Rosetta Stone to arrive at valuation......................................9

7. Deciding an offer price for Rosetta Stone's IPO........................................................................11

REFERENCES...................................................................................................................................12

2

ROSETTA STONE

Initial public offering refers to business initiatives which is carried out to list its stock on a

public stock exchange for the first time. In other words, it can be said that first sale of stock made

by the company to the public is known as initial public offerings (Boulton and Campbell, 2016).

Present project report will apply both market-multiple approach and free cash flow valuation model

to decide suitable share prices for Rosseta Stone's IPO. It is a public company which operates in

software development industry. Company develops language, software and other language-learning

solution products for the customers.

1. Describe the key features of Rosetta stone’s business model and its strategy

Rosseta Stone's has cloud-based business model in which company focuses to develop

language learning solutions and software to provide deeper knowledge into the education

technology. It comprises both C.D Rom and online services to consumers, corporate clients, foreign

institutes etc. It use advanced and upgraded technologies to help learners to learn different kind of

languages. Key acquisition of Rosseta Stone are Vivity Labs Inc, Tell Me More, Livemocha and

Lexia Learning which helps to increase its revenue to a major extent (Crook, 2013). Acquisition of

Lexia enhance Rosetta Stone's potential by adding more on literacy products and expertise (Sohn,

2013). Over the time, its model relies upon its sales force to maintain strong relationship with the

corporate clients and enhance their satisfaction level. It expands its market with the key partners,

Books-A-Million and London Drugs, Sprial Toys etc (Rosseta Stone expands North American retail

presence with the key partners, n.d.). Recently, it creates a partnership with Speak for the future

period (Rosetta Stone becomes key partner of Speak to the future, 2014). It drive value by recruiting

skilled and highly experienced sales force and providing innovative language-learning solutions to

the corporate clients. Its customer segments includes individual, governmental agencies, armed

forces, educational institutions and corporate clients as well. Its revenue stream includes sales of

innovative and language learning software of latest version and licensed the products. Till 2009,

Rosseta Stone's business model is to provide interacting language learning software to the domestic

(US clients) as well as foreign customers and international institutions. The model focuses on

selling language-learning software which comprises both online and CD Rom to the consumers. Its

online subscriptions enable company to charge very high prices so as to increase their revenue,

market share and profitability to compete effectively.

Porter’s 5 forces:

Bargaining power of suppliers: Similar kinds of inputs are used by all the companies in

their operations while distribution channel is diverse. However, suppliers are competing with each

3

Initial public offering refers to business initiatives which is carried out to list its stock on a

public stock exchange for the first time. In other words, it can be said that first sale of stock made

by the company to the public is known as initial public offerings (Boulton and Campbell, 2016).

Present project report will apply both market-multiple approach and free cash flow valuation model

to decide suitable share prices for Rosseta Stone's IPO. It is a public company which operates in

software development industry. Company develops language, software and other language-learning

solution products for the customers.

1. Describe the key features of Rosetta stone’s business model and its strategy

Rosseta Stone's has cloud-based business model in which company focuses to develop

language learning solutions and software to provide deeper knowledge into the education

technology. It comprises both C.D Rom and online services to consumers, corporate clients, foreign

institutes etc. It use advanced and upgraded technologies to help learners to learn different kind of

languages. Key acquisition of Rosseta Stone are Vivity Labs Inc, Tell Me More, Livemocha and

Lexia Learning which helps to increase its revenue to a major extent (Crook, 2013). Acquisition of

Lexia enhance Rosetta Stone's potential by adding more on literacy products and expertise (Sohn,

2013). Over the time, its model relies upon its sales force to maintain strong relationship with the

corporate clients and enhance their satisfaction level. It expands its market with the key partners,

Books-A-Million and London Drugs, Sprial Toys etc (Rosseta Stone expands North American retail

presence with the key partners, n.d.). Recently, it creates a partnership with Speak for the future

period (Rosetta Stone becomes key partner of Speak to the future, 2014). It drive value by recruiting

skilled and highly experienced sales force and providing innovative language-learning solutions to

the corporate clients. Its customer segments includes individual, governmental agencies, armed

forces, educational institutions and corporate clients as well. Its revenue stream includes sales of

innovative and language learning software of latest version and licensed the products. Till 2009,

Rosseta Stone's business model is to provide interacting language learning software to the domestic

(US clients) as well as foreign customers and international institutions. The model focuses on

selling language-learning software which comprises both online and CD Rom to the consumers. Its

online subscriptions enable company to charge very high prices so as to increase their revenue,

market share and profitability to compete effectively.

Porter’s 5 forces:

Bargaining power of suppliers: Similar kinds of inputs are used by all the companies in

their operations while distribution channel is diverse. However, suppliers are competing with each

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other to deliver their goods and services; therefore, bargaining power of suppliers is high.

Bargaining power of customers: Customer prefer Rosetta Stone’s product because of best

quality and also they have limited choice available; henceforth, their bargaining power is

comparatively low.

Threat of rivalry: Rosetta Stone has very less number of competitors such as Memrise,

Fluenz, Livemocha etc. therefore, it can be said that company is not facing intense level of

competition in the market.

Threat of substitutes: Substitue that are providing by the other companies is of inferior

quality and also limited in number. Thus, it becomes clear that threat of substitute is low.

Threat of new competitors: Geographic factors limit the competition level in the industry,

henceforth; threat of new entrepreneurs is less.

Contrary to this, its strategy is to enhance its competitive strength by developing new and

innovative products and software which enable people to learn new languages. Moreover, it makes

continuous improvement through investment in research and development activities. Along with

this, Rosetta Stone focuses on the most prolific devices like Samsung, Chrome Book, iPhone, iPad

etc. to grab larger market share across the globe (Seave, 2014). Its strategy is highly concerned with

increasing business turnover and yield as well to compete effectively in the market place. Its

strategic focus is to maintain better control over material, cash availability, and relationship with the

clients, introduction of new software and learning solutions and making growth of Kiosks,

Enterprise and Education business (E&E), etc. Moreover, it focuses to distribute services more on

online and expand its product portfolio (Hall, 2015). Recently, it launched Kids reading, brain

fitness, innovative devices, apps etc. to increase its product offerings and increase its customer base.

Its market strategy is to focus on enhancing the level of consumer satisfaction by advertising on

Google, display ads and other search ads. Contrary to this, its competitive strategy is focuses on

enterprise resource centre and attracting high number of multinational institutions and foreign

clients (Four reason for a business language strategy, 2015). Moreover, its strategic focus is to

deliver value to the shareholders by the use of share buy-back program.

4

Bargaining power of customers: Customer prefer Rosetta Stone’s product because of best

quality and also they have limited choice available; henceforth, their bargaining power is

comparatively low.

Threat of rivalry: Rosetta Stone has very less number of competitors such as Memrise,

Fluenz, Livemocha etc. therefore, it can be said that company is not facing intense level of

competition in the market.

Threat of substitutes: Substitue that are providing by the other companies is of inferior

quality and also limited in number. Thus, it becomes clear that threat of substitute is low.

Threat of new competitors: Geographic factors limit the competition level in the industry,

henceforth; threat of new entrepreneurs is less.

Contrary to this, its strategy is to enhance its competitive strength by developing new and

innovative products and software which enable people to learn new languages. Moreover, it makes

continuous improvement through investment in research and development activities. Along with

this, Rosetta Stone focuses on the most prolific devices like Samsung, Chrome Book, iPhone, iPad

etc. to grab larger market share across the globe (Seave, 2014). Its strategy is highly concerned with

increasing business turnover and yield as well to compete effectively in the market place. Its

strategic focus is to maintain better control over material, cash availability, and relationship with the

clients, introduction of new software and learning solutions and making growth of Kiosks,

Enterprise and Education business (E&E), etc. Moreover, it focuses to distribute services more on

online and expand its product portfolio (Hall, 2015). Recently, it launched Kids reading, brain

fitness, innovative devices, apps etc. to increase its product offerings and increase its customer base.

Its market strategy is to focus on enhancing the level of consumer satisfaction by advertising on

Google, display ads and other search ads. Contrary to this, its competitive strategy is focuses on

enterprise resource centre and attracting high number of multinational institutions and foreign

clients (Four reason for a business language strategy, 2015). Moreover, its strategic focus is to

deliver value to the shareholders by the use of share buy-back program.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

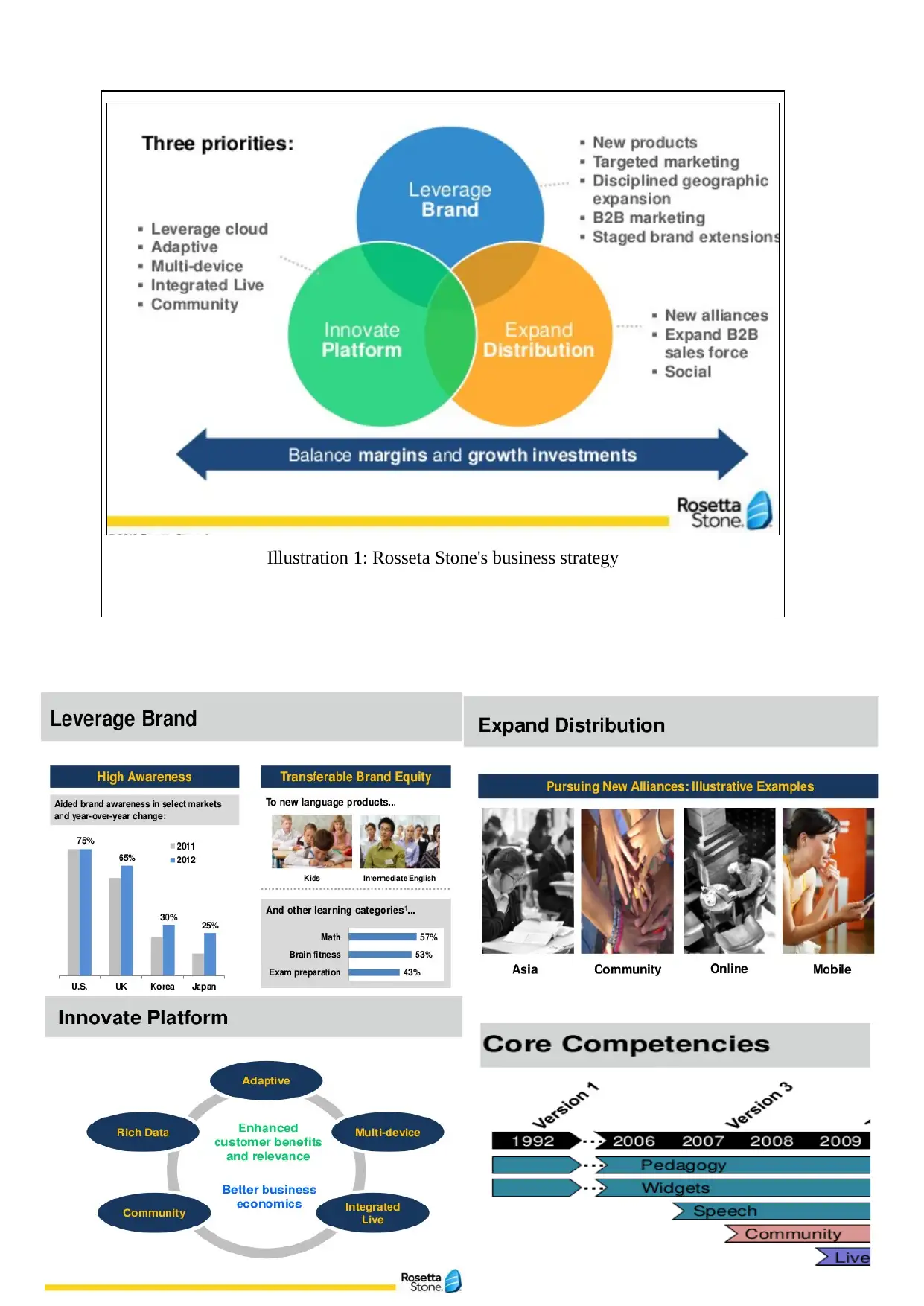

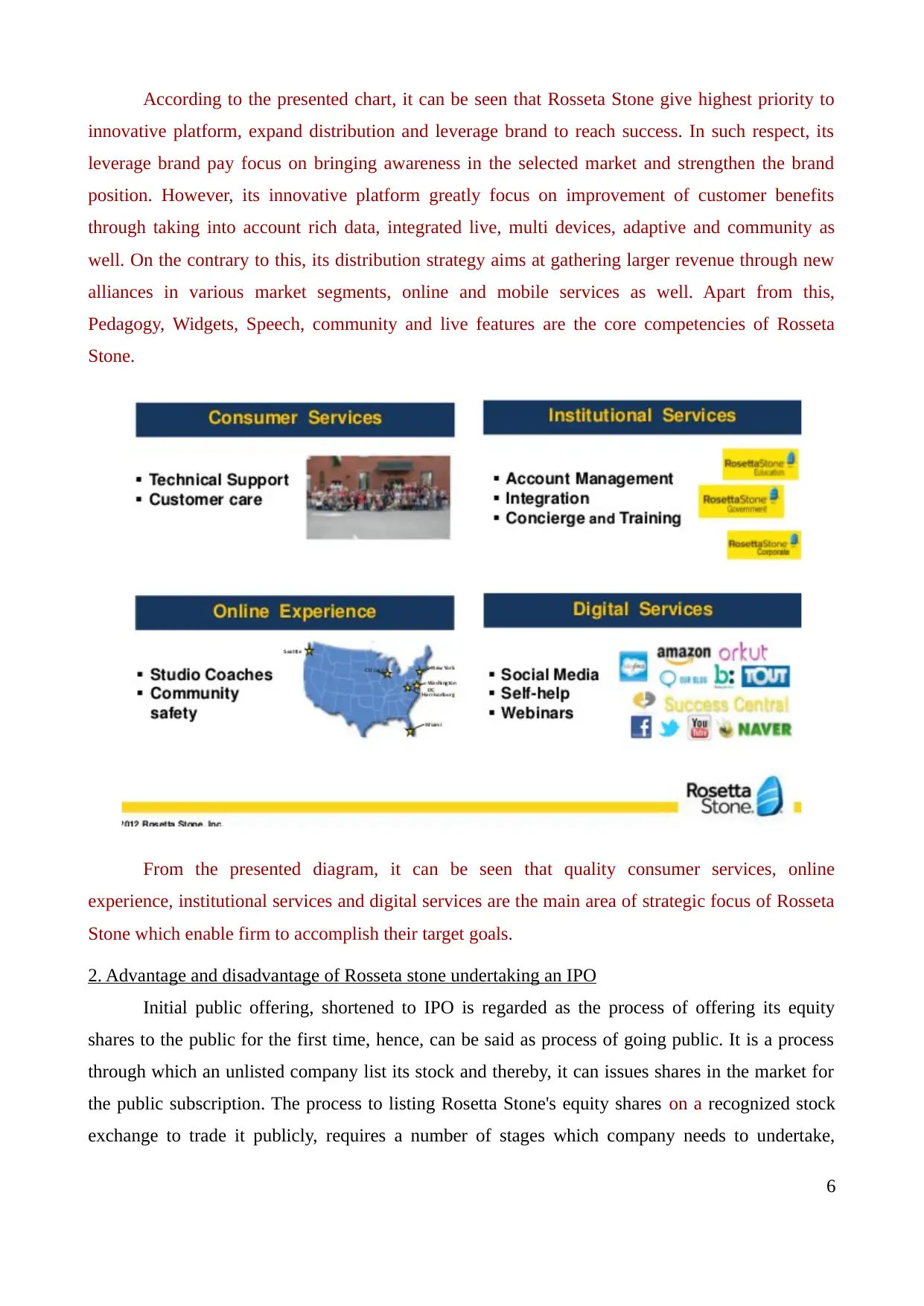

Illustration 1: Rosseta Stone's business strategy

Illustration 1: Rosseta Stone's business strategy

According to the presented chart, it can be seen that Rosseta Stone give highest priority to

innovative platform, expand distribution and leverage brand to reach success. In such respect, its

leverage brand pay focus on bringing awareness in the selected market and strengthen the brand

position. However, its innovative platform greatly focus on improvement of customer benefits

through taking into account rich data, integrated live, multi devices, adaptive and community as

well. On the contrary to this, its distribution strategy aims at gathering larger revenue through new

alliances in various market segments, online and mobile services as well. Apart from this,

Pedagogy, Widgets, Speech, community and live features are the core competencies of Rosseta

Stone.

From the presented diagram, it can be seen that quality consumer services, online

experience, institutional services and digital services are the main area of strategic focus of Rosseta

Stone which enable firm to accomplish their target goals.

2. Advantage and disadvantage of Rosseta stone undertaking an IPO

Initial public offering, shortened to IPO is regarded as the process of offering its equity

shares to the public for the first time, hence, can be said as process of going public. It is a process

through which an unlisted company list its stock and thereby, it can issues shares in the market for

the public subscription. The process to listing Rosetta Stone's equity shares on a recognized stock

exchange to trade it publicly, requires a number of stages which company needs to undertake,

6

innovative platform, expand distribution and leverage brand to reach success. In such respect, its

leverage brand pay focus on bringing awareness in the selected market and strengthen the brand

position. However, its innovative platform greatly focus on improvement of customer benefits

through taking into account rich data, integrated live, multi devices, adaptive and community as

well. On the contrary to this, its distribution strategy aims at gathering larger revenue through new

alliances in various market segments, online and mobile services as well. Apart from this,

Pedagogy, Widgets, Speech, community and live features are the core competencies of Rosseta

Stone.

From the presented diagram, it can be seen that quality consumer services, online

experience, institutional services and digital services are the main area of strategic focus of Rosseta

Stone which enable firm to accomplish their target goals.

2. Advantage and disadvantage of Rosseta stone undertaking an IPO

Initial public offering, shortened to IPO is regarded as the process of offering its equity

shares to the public for the first time, hence, can be said as process of going public. It is a process

through which an unlisted company list its stock and thereby, it can issues shares in the market for

the public subscription. The process to listing Rosetta Stone's equity shares on a recognized stock

exchange to trade it publicly, requires a number of stages which company needs to undertake,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

described below:1. Creating pitch: At the initial stage, Rosetta Stone has to fulfil prerequisites requirement

about generating a credible plan, recruiting a qualified management team, create board of

directors (BOD), construct financial statement and audit it, measure performance, financial

projection, develop relationship with the lenders, investment bankers, accountants and

lawyers as well (Boone, Floros and Johnson, 2016). Further, bake-off meeting are conducted

to recruit underwriter for the sale of its stock. In this regard, important discussion regarding

proposed commission, historical track records and distribution abilities of the underwriters

etc. are analysed by Rosetta stone.2. Kick-off meeting: After fulfilling the prerequisites, company has to organize a meeting in

which all the parties such as management, auditors, directors, accountants, investment bank,

legal counsel etc. will be invited to take decisions for underwriter and issuing firm. At this

stage, legal contracts or agreements are framed with specific terms and conditions. With

regards to prospectus, it is the legal obligation on Rosetta stone to not publish any

information which are outside the prospectus (Filatotchev, Chahine and Bruton, 2016).

Moreover, it cannot advertise the information to increase public awareness about its name,

products, services, market segments etc. to create a positive image toward its equity stock. If

it happen, that will be consider illegal activities and SEC prohibited such acts and mistakes,

also called quiet period.3. Filling registration statement and due diligence: At this stage, SEC required registration

statement, of which, Part – I is preparation of prospectus whilst Part- II includes

underwriter agreements, Rosetta Stone's charter, laws and a specimen of security as well.

Contrary to this, due diligence refers to restriction of disclosing untrue and material

misstatement in the prospectus. In this, tax return, contracts, necessary documents etc. are

provided to the SEC. Beside this, underwriter prepare syndicate which includes various

investment bankers which are agreed to buy shares at price less underwriter discount.4. SEC review: In this, SEC review all the filled documents whether it complied with the

Security Act, 1933 or not. Registration statement will be effective after 20 days of the

filling date. While, if any untrue information has been disclosed in the statement than SEC

will sent letter of comment to the company and gives 20 day warning period to file amended

statement (Esfahanipour, Goodarzi and Jahanbin, 2016).5. Road show: In this, Rosetta stone’s managers will meet potential investors to assess market

demand about the new issues and increase their interest. 1-2 week road shows are organized

by the underwriter to enable manager to discuss their investment plan across the country

7

about generating a credible plan, recruiting a qualified management team, create board of

directors (BOD), construct financial statement and audit it, measure performance, financial

projection, develop relationship with the lenders, investment bankers, accountants and

lawyers as well (Boone, Floros and Johnson, 2016). Further, bake-off meeting are conducted

to recruit underwriter for the sale of its stock. In this regard, important discussion regarding

proposed commission, historical track records and distribution abilities of the underwriters

etc. are analysed by Rosetta stone.2. Kick-off meeting: After fulfilling the prerequisites, company has to organize a meeting in

which all the parties such as management, auditors, directors, accountants, investment bank,

legal counsel etc. will be invited to take decisions for underwriter and issuing firm. At this

stage, legal contracts or agreements are framed with specific terms and conditions. With

regards to prospectus, it is the legal obligation on Rosetta stone to not publish any

information which are outside the prospectus (Filatotchev, Chahine and Bruton, 2016).

Moreover, it cannot advertise the information to increase public awareness about its name,

products, services, market segments etc. to create a positive image toward its equity stock. If

it happen, that will be consider illegal activities and SEC prohibited such acts and mistakes,

also called quiet period.3. Filling registration statement and due diligence: At this stage, SEC required registration

statement, of which, Part – I is preparation of prospectus whilst Part- II includes

underwriter agreements, Rosetta Stone's charter, laws and a specimen of security as well.

Contrary to this, due diligence refers to restriction of disclosing untrue and material

misstatement in the prospectus. In this, tax return, contracts, necessary documents etc. are

provided to the SEC. Beside this, underwriter prepare syndicate which includes various

investment bankers which are agreed to buy shares at price less underwriter discount.4. SEC review: In this, SEC review all the filled documents whether it complied with the

Security Act, 1933 or not. Registration statement will be effective after 20 days of the

filling date. While, if any untrue information has been disclosed in the statement than SEC

will sent letter of comment to the company and gives 20 day warning period to file amended

statement (Esfahanipour, Goodarzi and Jahanbin, 2016).5. Road show: In this, Rosetta stone’s managers will meet potential investors to assess market

demand about the new issues and increase their interest. 1-2 week road shows are organized

by the underwriter to enable manager to discuss their investment plan across the country

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Blum, 2011).

6. Pricing meeting: In this stage, company management will negotiate the final offering price

and the underwriter discount on the basis of investor demand and external market conditions

(Boulton and Campbell, 2016).

7. Allocation: Once the price decided, syndicate member will sell share to the potential

investors and final copy of the prospectus and sales confirmation also will be provided to

them. In this, underwriter will cancel the deal if payment is not receive in 5 days after

delivering confirmation of sale.

8. Trading: After finalising the allocation, trading get started hence, public can buy and sell

the shares. According to the rule of SEC, 10b – 7, underwriter has no right to get involve in

price stabilising activities while distribution securities. Offering settlement will be closed

after 10 days of the effective date, which is mentioned in the underwriter agreement (Boone,

Floros and Johnson, 2016). Security certificate will be delivered to the underwriter and

updated comfort letter will be given to the individual accountants.

From the above analysis, it becomes clear that the IPO process very length which consume a

lot of time of the managers because they are required to conduct meetings, necessary

documentation, conduct road show, organize price meeting, appoint underwriter etc. Along with

this, underwriter commission, preparation of documents such as registration and filling of tax

return, contracts etc. impose cost to the business and results in lower yield. Therefore, it can attract

high managerial focus on the IPO process for listing of shares, which in turn, may reduce the focus

of managers on the effective administration of daily business operations and activities.

Advantage of IPO Disadvantage of IPO

It helps to raise money for the business

expansion, research and development,

capital expenditures and pay back long

term debts and loans of Rosetta stone

by attracting high number of investors.

It is an advantage because through

using this facility, Rosseta Stone can

meet their capital requirement and run

operations successfully in the

competitive market.

Rosetta Stone will need to disclose its

audited financial reports in the front of

shareholders to communicate its business

performance. It will be a disadvantage

because company will be liable to audit its

annual financial account timely thus,

confidentiality cannot be maintained.

Moreover, organization has to pay fees to

the auditor which increase cost and decline

net yield.

8

6. Pricing meeting: In this stage, company management will negotiate the final offering price

and the underwriter discount on the basis of investor demand and external market conditions

(Boulton and Campbell, 2016).

7. Allocation: Once the price decided, syndicate member will sell share to the potential

investors and final copy of the prospectus and sales confirmation also will be provided to

them. In this, underwriter will cancel the deal if payment is not receive in 5 days after

delivering confirmation of sale.

8. Trading: After finalising the allocation, trading get started hence, public can buy and sell

the shares. According to the rule of SEC, 10b – 7, underwriter has no right to get involve in

price stabilising activities while distribution securities. Offering settlement will be closed

after 10 days of the effective date, which is mentioned in the underwriter agreement (Boone,

Floros and Johnson, 2016). Security certificate will be delivered to the underwriter and

updated comfort letter will be given to the individual accountants.

From the above analysis, it becomes clear that the IPO process very length which consume a

lot of time of the managers because they are required to conduct meetings, necessary

documentation, conduct road show, organize price meeting, appoint underwriter etc. Along with

this, underwriter commission, preparation of documents such as registration and filling of tax

return, contracts etc. impose cost to the business and results in lower yield. Therefore, it can attract

high managerial focus on the IPO process for listing of shares, which in turn, may reduce the focus

of managers on the effective administration of daily business operations and activities.

Advantage of IPO Disadvantage of IPO

It helps to raise money for the business

expansion, research and development,

capital expenditures and pay back long

term debts and loans of Rosetta stone

by attracting high number of investors.

It is an advantage because through

using this facility, Rosseta Stone can

meet their capital requirement and run

operations successfully in the

competitive market.

Rosetta Stone will need to disclose its

audited financial reports in the front of

shareholders to communicate its business

performance. It will be a disadvantage

because company will be liable to audit its

annual financial account timely thus,

confidentiality cannot be maintained.

Moreover, organization has to pay fees to

the auditor which increase cost and decline

net yield.

8

It also creates positive image of

Rosetta stone by trading its securities

publicly. The reason behind this is it

helps to attract more suppliers,

customers and bank also will be

willing to lend funds to the listed

companies rather than unlisted

(Mantell, 2016).

It facilitates Rosetta stone to carry out

mergers and acquisition by driving

larger market. Rosseta Stone can

acquire and merge with other

organizations, by this, it can increase

its revenue, profitability and market

share as well. This in turn, company

will be able to gain competitive

advantages and reach success.

Company will be obliged to comply with

the rules and regulations of SEC and

Security Act, 1933, which may incur high

cost (Boone, Floros and Johnson, 2016).

The cost of IPO in USA is approximately $1

million which includes listing, printing and

legal fees etc.

Investors also have controlling power

through which they can take part in the

decision-making hence, dilution of control

is also a disadvantage of going public.

Listing the shares enable entrepreneur

to maintain liquidity because it allows

venture capitalists to liquidate their

holdings.

It also imposes reporting requirement on

Rosetta stone through which, it has to report

its operations, financial position etc. to the

investors. In case, when Rosseta Stone does

not have profitability and running in loss,

then it will create negative impact on the

shareholders and they can sale their

investment. Moreover, it will be very

difficult for the company to take borrowings

from banks because financial institutions

only provide money to the profit gaining

enterprises for their fund security.

The success and growth of the business

is also based upon shareholder’s value

Company will have to pay return to the

shareholders in the terms of dividend which

9

Rosetta stone by trading its securities

publicly. The reason behind this is it

helps to attract more suppliers,

customers and bank also will be

willing to lend funds to the listed

companies rather than unlisted

(Mantell, 2016).

It facilitates Rosetta stone to carry out

mergers and acquisition by driving

larger market. Rosseta Stone can

acquire and merge with other

organizations, by this, it can increase

its revenue, profitability and market

share as well. This in turn, company

will be able to gain competitive

advantages and reach success.

Company will be obliged to comply with

the rules and regulations of SEC and

Security Act, 1933, which may incur high

cost (Boone, Floros and Johnson, 2016).

The cost of IPO in USA is approximately $1

million which includes listing, printing and

legal fees etc.

Investors also have controlling power

through which they can take part in the

decision-making hence, dilution of control

is also a disadvantage of going public.

Listing the shares enable entrepreneur

to maintain liquidity because it allows

venture capitalists to liquidate their

holdings.

It also imposes reporting requirement on

Rosetta stone through which, it has to report

its operations, financial position etc. to the

investors. In case, when Rosseta Stone does

not have profitability and running in loss,

then it will create negative impact on the

shareholders and they can sale their

investment. Moreover, it will be very

difficult for the company to take borrowings

from banks because financial institutions

only provide money to the profit gaining

enterprises for their fund security.

The success and growth of the business

is also based upon shareholder’s value

Company will have to pay return to the

shareholders in the terms of dividend which

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Esfahanipour, Goodarzi and Jahanbin,

2016). Henceforth, by providing larger

the return to the investors out of its

earnings, enable firm to enhance

shareholders worth and build a strong

market image.

increase cost and decline net yield

(Filatotchev, Chahine and Bruton, 2016).

On the basis of above discussion, it can be said that Rosseta Stone has to list its shares

because although the cost of going public is approximately $1 million but still, it offers wide range

of advantages to the Rosseta stone as compare to the cost of gathering funds through external

borrowings. Hence, it becomes clear that manager has to go for IPO process to list its shares on a

recognized stock exchange.

3. Market-Multiples approach to identify range of prices for an IPO

Market multiple approach is a valuation model, according to which, stock prices can be

decided by taking into account the similar kind of assets at similar prices. The term “Market

Multiple” is a generic term which use number of components or indicators to value the stock of the

Rosetta stone. For instance, price to earnings (P/E) ratio is one of the multiples which can be used

by the businesses to decide offering prices for their IPO (Pinto, Robinson and Stowe, 2015). Out of

this, P/E ratio is often use factor which indicates the ratio between market price (MP) and earning

per share (EPS). According to this multiple, if Rosetta stone has less P/E ratio than, it will be

consider as undervalued firm than its competitors. In this method, valuation is based upon the

competitors which are operating in same industry (Cornell and Gokhale, 2016). With regards to

Rosetto Stone, Apollo Group Inc, American Public Education Inc, Corinthian Education Corp,

Capella Education, Strayer Education, DeVRY Inc, ITT Educational Service Inc. K12 Inc., Grand

Canyon Education, Inc. and New Oriental Ed. & Tech. Group Inc are its major competitors.

Another multiple of this approach is enterprise value which refers to the market

capitalization of Rosetta Stone by eliminating the impact of its financial assets and liabilities

(Moghaddam and Talebnia, 2016). As per this factor, enterprise value can be determined through

using following formula:

Enterprise value (EV) = Market capitalization + Debt fund + Minority interest – Cash and

equivalents – investment

Apart from that, this approach also use EV to EBITDA (Earnings before interest, tax,

10

2016). Henceforth, by providing larger

the return to the investors out of its

earnings, enable firm to enhance

shareholders worth and build a strong

market image.

increase cost and decline net yield

(Filatotchev, Chahine and Bruton, 2016).

On the basis of above discussion, it can be said that Rosseta Stone has to list its shares

because although the cost of going public is approximately $1 million but still, it offers wide range

of advantages to the Rosseta stone as compare to the cost of gathering funds through external

borrowings. Hence, it becomes clear that manager has to go for IPO process to list its shares on a

recognized stock exchange.

3. Market-Multiples approach to identify range of prices for an IPO

Market multiple approach is a valuation model, according to which, stock prices can be

decided by taking into account the similar kind of assets at similar prices. The term “Market

Multiple” is a generic term which use number of components or indicators to value the stock of the

Rosetta stone. For instance, price to earnings (P/E) ratio is one of the multiples which can be used

by the businesses to decide offering prices for their IPO (Pinto, Robinson and Stowe, 2015). Out of

this, P/E ratio is often use factor which indicates the ratio between market price (MP) and earning

per share (EPS). According to this multiple, if Rosetta stone has less P/E ratio than, it will be

consider as undervalued firm than its competitors. In this method, valuation is based upon the

competitors which are operating in same industry (Cornell and Gokhale, 2016). With regards to

Rosetto Stone, Apollo Group Inc, American Public Education Inc, Corinthian Education Corp,

Capella Education, Strayer Education, DeVRY Inc, ITT Educational Service Inc. K12 Inc., Grand

Canyon Education, Inc. and New Oriental Ed. & Tech. Group Inc are its major competitors.

Another multiple of this approach is enterprise value which refers to the market

capitalization of Rosetta Stone by eliminating the impact of its financial assets and liabilities

(Moghaddam and Talebnia, 2016). As per this factor, enterprise value can be determined through

using following formula:

Enterprise value (EV) = Market capitalization + Debt fund + Minority interest – Cash and

equivalents – investment

Apart from that, this approach also use EV to EBITDA (Earnings before interest, tax,

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depreciation and amortization) multiple to decide share price for going public. This method is

considered as more realistic method as compare to DCF valuation. The advantage of this method is

that it use investors ratios like earning per share, price-to-earnings ratio etc. to decide share price

(Reed and Rocholl, 2010). Contrary to this, the limitation of this method is that it does not provide

assistance to value share price in changing and competitive business era. Moreover, if competitors

valued their share price incorrectly than it may provide misleading results.

Questions with market-multiple approach:

One of the key problems that come first when applying market-multiple is to select the

correct comparables. It is because, there may be number of competitors operating in the market, in

such case, it is essential for the analyst to determine the most suitable and appropriate comparable.

In such respect, company has to select those peers which have similar return on capital employed

and growth rate as well. Moreover, as said earlier, that there are number of multiples henceforth,

business has to select the best multiple to determine the share price for Initial Public Offering (IPO).

In such regards, business has to select forward-looking multiples rather than historical results.

Movements in balance sheet:

Movement in balance sheet also affect the share pricing by market-multiple approach. For

instance, price earning multiple is greatly affected by the changes in capital structure and P/E is

usually higher in unlevered firm and lower in levered. Further, analyst also has to make necessary

adjustments regards to excess cash, non-operating assets, pension, employee stock option etc so as

to identify the correct price for IPO listing.

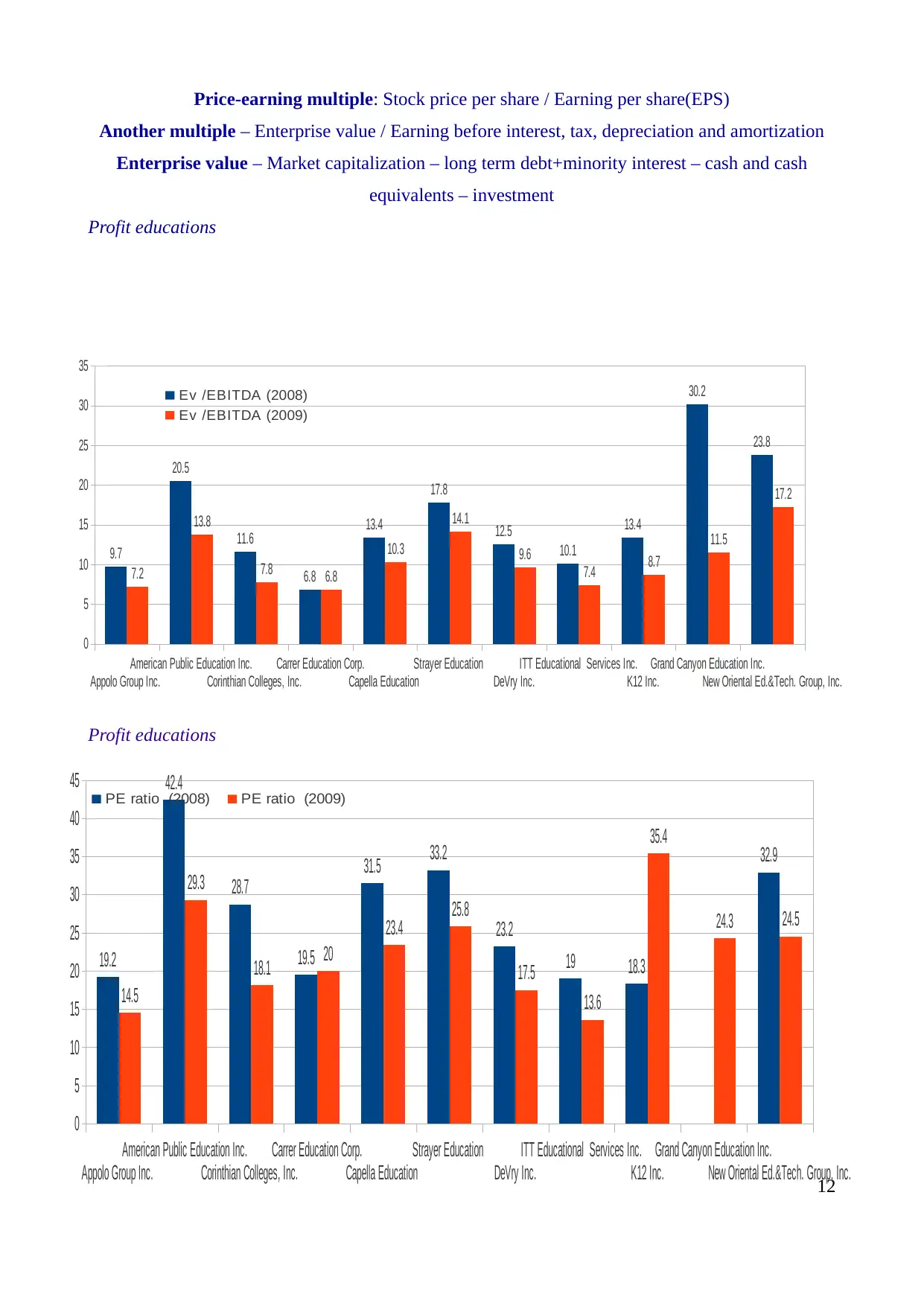

4. Application of Market-Multiple approach to arrive at a suitable share price for IPO

The market multiple approach emphasizes on ascertaining market value of the organization

on the basis of performance of company’s competitors. As per the cited scenario, Rosetta Stone is

desiring to list its share for IPO in 2009. Many of the analysts mostly prefer EV/EBITDA or

Enterprise value as their market-multiple of comparable firms who are operating in the industry to

value their share price. In such respect, EV/EBITDA states that how much amount of money, buyer

is required to pay in order to acquire the proxy cash flows (Caution, Platt and Platt, 2011). The main

benefit of this multiple over price-earning ratio is it does not affected by the capital structure of the

company as it is a measure of capital intensity. With regards to the current scenario, the sample of

companies are extracted from the industry to which Rossetto Stone belongs to. There are two

multiple will be use that are price earning ratio and EV/EBITDA to identify the stock price of IPO

for Rosseta Stone. Here. The formula of P/E multiple is as under:

11

considered as more realistic method as compare to DCF valuation. The advantage of this method is

that it use investors ratios like earning per share, price-to-earnings ratio etc. to decide share price

(Reed and Rocholl, 2010). Contrary to this, the limitation of this method is that it does not provide

assistance to value share price in changing and competitive business era. Moreover, if competitors

valued their share price incorrectly than it may provide misleading results.

Questions with market-multiple approach:

One of the key problems that come first when applying market-multiple is to select the

correct comparables. It is because, there may be number of competitors operating in the market, in

such case, it is essential for the analyst to determine the most suitable and appropriate comparable.

In such respect, company has to select those peers which have similar return on capital employed

and growth rate as well. Moreover, as said earlier, that there are number of multiples henceforth,

business has to select the best multiple to determine the share price for Initial Public Offering (IPO).

In such regards, business has to select forward-looking multiples rather than historical results.

Movements in balance sheet:

Movement in balance sheet also affect the share pricing by market-multiple approach. For

instance, price earning multiple is greatly affected by the changes in capital structure and P/E is

usually higher in unlevered firm and lower in levered. Further, analyst also has to make necessary

adjustments regards to excess cash, non-operating assets, pension, employee stock option etc so as

to identify the correct price for IPO listing.

4. Application of Market-Multiple approach to arrive at a suitable share price for IPO

The market multiple approach emphasizes on ascertaining market value of the organization

on the basis of performance of company’s competitors. As per the cited scenario, Rosetta Stone is

desiring to list its share for IPO in 2009. Many of the analysts mostly prefer EV/EBITDA or

Enterprise value as their market-multiple of comparable firms who are operating in the industry to

value their share price. In such respect, EV/EBITDA states that how much amount of money, buyer

is required to pay in order to acquire the proxy cash flows (Caution, Platt and Platt, 2011). The main

benefit of this multiple over price-earning ratio is it does not affected by the capital structure of the

company as it is a measure of capital intensity. With regards to the current scenario, the sample of

companies are extracted from the industry to which Rossetto Stone belongs to. There are two

multiple will be use that are price earning ratio and EV/EBITDA to identify the stock price of IPO

for Rosseta Stone. Here. The formula of P/E multiple is as under:

11

Price-earning multiple: Stock price per share / Earning per share(EPS)

Another multiple – Enterprise value / Earning before interest, tax, depreciation and amortization

Enterprise value – Market capitalization – long term debt+minority interest – cash and cash

equivalents – investment

Profit educations

Profit educations

12

Appolo Group Inc.

American Public Education Inc.

Corinthian Colleges, Inc.

Carrer Education Corp.

Capella Education

Strayer Education

DeVry Inc.

ITT Educational Services Inc.

K12 Inc.

Grand Canyon Education Inc.

New Oriental Ed.&Tech. Group, Inc.

0

5

10

15

20

25

30

35

40

45

19.2

42.4

28.7

19.5

31.5 33.2

23.2

19 18.3

32.9

14.5

29.3

18.1 20

23.4 25.8

17.5

13.6

35.4

24.3 24.5

PE ratio (2008) PE ratio (2009)

Appolo Group Inc.

American Public Education Inc.

Corinthian Colleges, Inc.

Carrer Education Corp.

Capella Education

Strayer Education

DeVry Inc.

ITT Educational Services Inc.

K12 Inc.

Grand Canyon Education Inc.

New Oriental Ed.&Tech. Group, Inc.

0

5

10

15

20

25

30

35

9.7

20.5

11.6

6.8

13.4

17.8

12.5

10.1

13.4

30.2

23.8

7.2

13.8

7.8 6.8

10.3

14.1

9.6

7.4 8.7

11.5

17.2

Ev /EBITDA (2008)

Ev /EBITDA (2009)

Another multiple – Enterprise value / Earning before interest, tax, depreciation and amortization

Enterprise value – Market capitalization – long term debt+minority interest – cash and cash

equivalents – investment

Profit educations

Profit educations

12

Appolo Group Inc.

American Public Education Inc.

Corinthian Colleges, Inc.

Carrer Education Corp.

Capella Education

Strayer Education

DeVry Inc.

ITT Educational Services Inc.

K12 Inc.

Grand Canyon Education Inc.

New Oriental Ed.&Tech. Group, Inc.

0

5

10

15

20

25

30

35

40

45

19.2

42.4

28.7

19.5

31.5 33.2

23.2

19 18.3

32.9

14.5

29.3

18.1 20

23.4 25.8

17.5

13.6

35.4

24.3 24.5

PE ratio (2008) PE ratio (2009)

Appolo Group Inc.

American Public Education Inc.

Corinthian Colleges, Inc.

Carrer Education Corp.

Capella Education

Strayer Education

DeVry Inc.

ITT Educational Services Inc.

K12 Inc.

Grand Canyon Education Inc.

New Oriental Ed.&Tech. Group, Inc.

0

5

10

15

20

25

30

35

9.7

20.5

11.6

6.8

13.4

17.8

12.5

10.1

13.4

30.2

23.8

7.2

13.8

7.8 6.8

10.3

14.1

9.6

7.4 8.7

11.5

17.2

Ev /EBITDA (2008)

Ev /EBITDA (2009)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.