Financial Analysis of Rosetta Stone's 2009 IPO: A Case Study

VerifiedAdded on 2023/04/20

|18

|3798

|165

Case Study

AI Summary

This case study provides a financial analysis of Rosetta Stone's 2009 Initial Public Offering (IPO). It examines the company's business model, core strategies, and the advantages and disadvantages of undertaking an IPO. The report evaluates the use of the market-multiples approach for determining an exit value and calculates a suitable share price, considering relevant factors. It also explores a reasonable rate of return on investment and applies a free cash flow model to arrive at a valuation. The analysis covers the IPO process in the USA, including the costs and legal undertakings involved. The case study concludes with considerations for setting the final offer price for the IPO. Desklib provides access to this and other solved assignments for students.

Financial Entrepreneurial Initiatives

Rosetta Stone: Pricing the 2009 IPO

Rosetta Stone: Pricing the 2009 IPO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................................3

1.......................Key features of Rosetta Stone’s business model and explain its core business strategy

................................................................................................................................................................3

2. Advantages and disadvantages of Rosetta Stone undertaking an IPO...............................................4

2..........Evaluate the use of Market-Multiples approach for Rosetta Stone in determining an exit value

................................................................................................................................................................6

4 Calculation of suitable share price for Rosetta Stone’s IPO using Market-multiples approach and

considerations would need to be made...................................................................................................7

5. Reasonable rate of return on an investment in Rosetta Stone............................................................8

6. Free Cash Flow model to Rosetta Stone to arrive at a valuation.......................................................8

7. Offer price for the IPO.......................................................................................................................9

CONCLUSION........................................................................................................................................10

REFERENCES.........................................................................................................................................10

INTRODUCTION......................................................................................................................................3

1.......................Key features of Rosetta Stone’s business model and explain its core business strategy

................................................................................................................................................................3

2. Advantages and disadvantages of Rosetta Stone undertaking an IPO...............................................4

2..........Evaluate the use of Market-Multiples approach for Rosetta Stone in determining an exit value

................................................................................................................................................................6

4 Calculation of suitable share price for Rosetta Stone’s IPO using Market-multiples approach and

considerations would need to be made...................................................................................................7

5. Reasonable rate of return on an investment in Rosetta Stone............................................................8

6. Free Cash Flow model to Rosetta Stone to arrive at a valuation.......................................................8

7. Offer price for the IPO.......................................................................................................................9

CONCLUSION........................................................................................................................................10

REFERENCES.........................................................................................................................................10

INTRODUCTION

Financial market are those in which financial securities, commodities and other fungible items

are traded at various costs (Madura, 2014). The securities traded in financial markets includes stocks,

bonds, commodities etc. Initial public offering is the crucial sources of raising funds from the market

through offering equity and preference shares even debentures to public (Chemmanur and Krishnan,

2012). This is an initiative taken by an organization to public its stock however, is a long process to

register a company for IPO.

The report herewith is based on a case scenario of an USA based global education technology

Software Company, “Rosetta Stone” which deals with Language-Learning solutions products. As per

the case, business entity is moved further to the deal of going public in 2009. Therefore, this

investigation represents the advantages and disadvantages of Rosetta Stone to undertake an IPO.

Including this, key features of Rosetta Stone’s business model and its core business strategy are

explained in this report. Furthermore, Market-Multiples approach for Rosetta Stone is used to

determine an exit value along with calculating reasonable rate of return on an investment and free Cash

Flow model is applied to arrive at a valuation.

1 Key features of Rosetta Stone’s business model and explain its core business strategy

Rosetta Stone is an USA based global education technology Software Company deals with

developing language, learning and brain-fitness software. The organization is significantly known for

its innovative Language-Learning solutions products.

Business model of Rosetta stone

From the beginning, organization has started seeking more natural learning methods, therefore,

business model of Rosetta Stone is to use commuter technology to simulate the way people learn their

native languages. Along with this, business entity uses pictures and sounds to impart learning to the

individuals. The core area of business model is that how computer can be used to facilitate language

learning. In 1992, Stoltzfus and Fairfield came with Fairfield language technology, further the

emergence of CD-ROM technology has supported business of the cited company. The business model

of cited Company is specifically designed to distinguish the firm from other language companies and to

create an environment conducive to learning language naturally. The business model of company was

flexible and focused towards innovation. Further, in the year 1999, the organization has released its first

retail language training software product. The organization is continuously using series of CD ROMs

which is emerged as an effective ways to impart new learning to the individuals.

Business strategy of Rosetta Stone

Financial market are those in which financial securities, commodities and other fungible items

are traded at various costs (Madura, 2014). The securities traded in financial markets includes stocks,

bonds, commodities etc. Initial public offering is the crucial sources of raising funds from the market

through offering equity and preference shares even debentures to public (Chemmanur and Krishnan,

2012). This is an initiative taken by an organization to public its stock however, is a long process to

register a company for IPO.

The report herewith is based on a case scenario of an USA based global education technology

Software Company, “Rosetta Stone” which deals with Language-Learning solutions products. As per

the case, business entity is moved further to the deal of going public in 2009. Therefore, this

investigation represents the advantages and disadvantages of Rosetta Stone to undertake an IPO.

Including this, key features of Rosetta Stone’s business model and its core business strategy are

explained in this report. Furthermore, Market-Multiples approach for Rosetta Stone is used to

determine an exit value along with calculating reasonable rate of return on an investment and free Cash

Flow model is applied to arrive at a valuation.

1 Key features of Rosetta Stone’s business model and explain its core business strategy

Rosetta Stone is an USA based global education technology Software Company deals with

developing language, learning and brain-fitness software. The organization is significantly known for

its innovative Language-Learning solutions products.

Business model of Rosetta stone

From the beginning, organization has started seeking more natural learning methods, therefore,

business model of Rosetta Stone is to use commuter technology to simulate the way people learn their

native languages. Along with this, business entity uses pictures and sounds to impart learning to the

individuals. The core area of business model is that how computer can be used to facilitate language

learning. In 1992, Stoltzfus and Fairfield came with Fairfield language technology, further the

emergence of CD-ROM technology has supported business of the cited company. The business model

of cited Company is specifically designed to distinguish the firm from other language companies and to

create an environment conducive to learning language naturally. The business model of company was

flexible and focused towards innovation. Further, in the year 1999, the organization has released its first

retail language training software product. The organization is continuously using series of CD ROMs

which is emerged as an effective ways to impart new learning to the individuals.

Business strategy of Rosetta Stone

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The core business strategy of Rosetta Stone is to combined in language learning software with

test, images, sounds to teach various vocabulary terms and grammatical functions, initially the company

has focused towards school and government sales then it moved towards retail market in 2001. The

mentioned company has announced hiring of Tom Adams, who is a businessman with international

experience, as a CEO, which is found be the core strategy for getting an international exposure. He

played an important role in guiding the company’s expansionary strategy. The core competences of the

business includes Pedagogy, Widgets, Speech, community and live features. The company is creating

new value in the economy through continuous innovations. The name of company was changed in

2006 to Rosetta Stone, Ltd as it converted business from an S to a C corporation. With a unique

business strategy of going public, the company has filed an Initial public offering with the Securities

and Exchange Commission, how, after 2009, the organization is listed New York Stock Exchange. In

2008, Rosetta Stone has won Deloitte's Technology Fast Award and in 2009, it was awarded with 9

Stevie Executive of the Year Award.

An a compirtiotive strategy, the company has expanded n manufactiring and distribution to reach to

success. The organization is commited to minimise costs by achieving efficient in mannufacting. The

sales channle have alos bene aranged to minimise the logistic cost.

2. Advantages and disadvantages of Rosetta Stone undertaking an IPO

Being a private company, Rosetta Stone is evident with limited corporate investment as from

private sources company was raising limited amount of capital. The risk of takeover by other company

with the needed resources, was there on Rosetta Stone. The private investors was also concerned about

recognising the gains achieved through investing in the mentioned company, however, there was a

test, images, sounds to teach various vocabulary terms and grammatical functions, initially the company

has focused towards school and government sales then it moved towards retail market in 2001. The

mentioned company has announced hiring of Tom Adams, who is a businessman with international

experience, as a CEO, which is found be the core strategy for getting an international exposure. He

played an important role in guiding the company’s expansionary strategy. The core competences of the

business includes Pedagogy, Widgets, Speech, community and live features. The company is creating

new value in the economy through continuous innovations. The name of company was changed in

2006 to Rosetta Stone, Ltd as it converted business from an S to a C corporation. With a unique

business strategy of going public, the company has filed an Initial public offering with the Securities

and Exchange Commission, how, after 2009, the organization is listed New York Stock Exchange. In

2008, Rosetta Stone has won Deloitte's Technology Fast Award and in 2009, it was awarded with 9

Stevie Executive of the Year Award.

An a compirtiotive strategy, the company has expanded n manufactiring and distribution to reach to

success. The organization is commited to minimise costs by achieving efficient in mannufacting. The

sales channle have alos bene aranged to minimise the logistic cost.

2. Advantages and disadvantages of Rosetta Stone undertaking an IPO

Being a private company, Rosetta Stone is evident with limited corporate investment as from

private sources company was raising limited amount of capital. The risk of takeover by other company

with the needed resources, was there on Rosetta Stone. The private investors was also concerned about

recognising the gains achieved through investing in the mentioned company, however, there was a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

uncertainty of taking a relatively young company in the market, Adams, a CEO of mentioned company

moved further to the deal of going public in 2009. The impressive financial growth with 53% increase

in revenues has supported decision despite the global economic contraction. The decision for going

public was an opportunity for aforesaid company to establish business creditably as well as it was

going to support corporate entity in building a strong brand image in global marketplace. From the case

study, it has been evident that Rosetta Stone was one among the companies which can have successful

IPO.

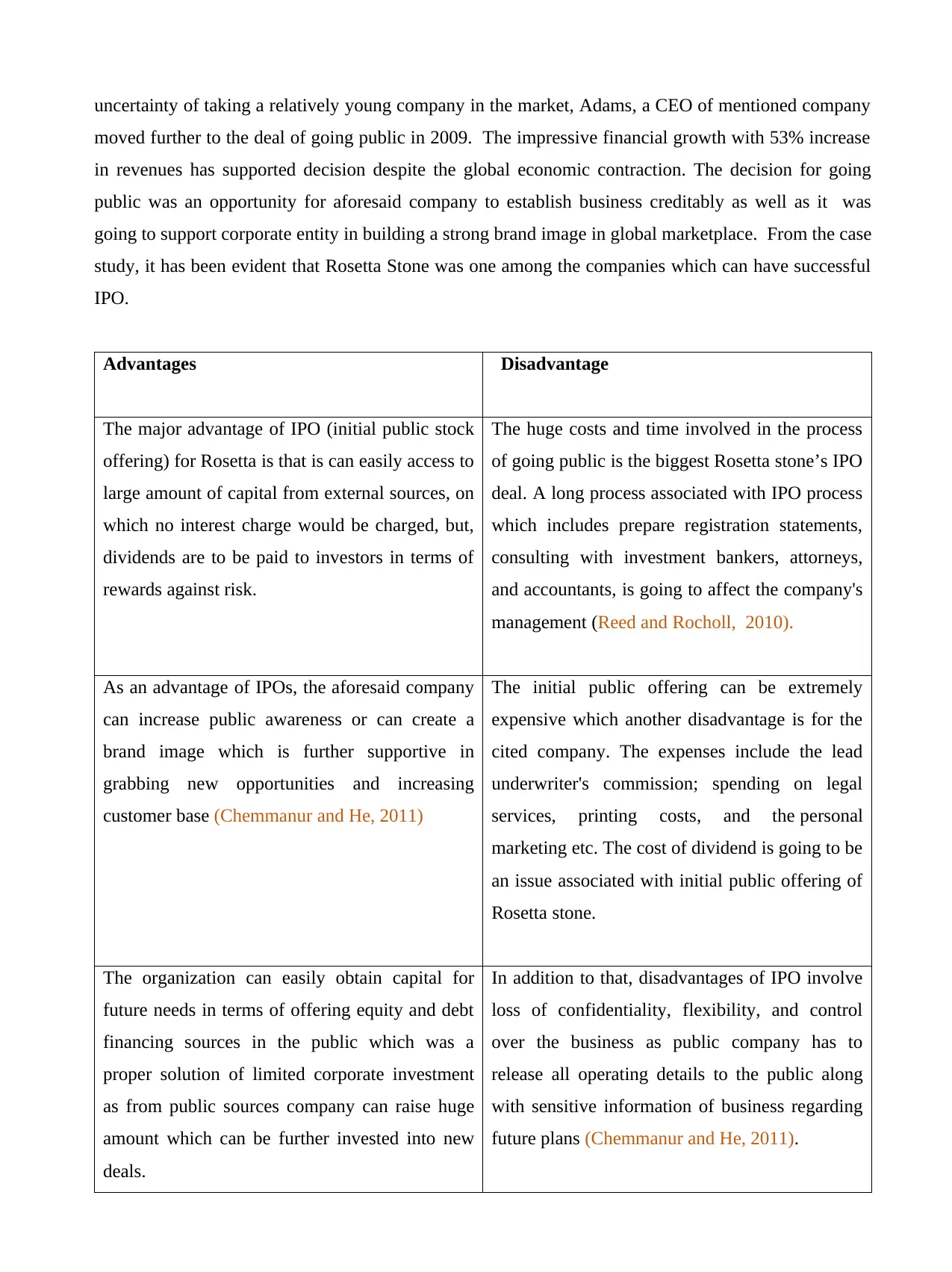

Advantages Disadvantage

The major advantage of IPO (initial public stock

offering) for Rosetta is that is can easily access to

large amount of capital from external sources, on

which no interest charge would be charged, but,

dividends are to be paid to investors in terms of

rewards against risk.

The huge costs and time involved in the process

of going public is the biggest Rosetta stone’s IPO

deal. A long process associated with IPO process

which includes prepare registration statements,

consulting with investment bankers, attorneys,

and accountants, is going to affect the company's

management (Reed and Rocholl, 2010).

As an advantage of IPOs, the aforesaid company

can increase public awareness or can create a

brand image which is further supportive in

grabbing new opportunities and increasing

customer base (Chemmanur and He, 2011)

The initial public offering can be extremely

expensive which another disadvantage is for the

cited company. The expenses include the lead

underwriter's commission; spending on legal

services, printing costs, and the personal

marketing etc. The cost of dividend is going to be

an issue associated with initial public offering of

Rosetta stone.

The organization can easily obtain capital for

future needs in terms of offering equity and debt

financing sources in the public which was a

proper solution of limited corporate investment

as from public sources company can raise huge

amount which can be further invested into new

deals.

In addition to that, disadvantages of IPO involve

loss of confidentiality, flexibility, and control

over the business as public company has to

release all operating details to the public along

with sensitive information of business regarding

future plans (Chemmanur and He, 2011).

moved further to the deal of going public in 2009. The impressive financial growth with 53% increase

in revenues has supported decision despite the global economic contraction. The decision for going

public was an opportunity for aforesaid company to establish business creditably as well as it was

going to support corporate entity in building a strong brand image in global marketplace. From the case

study, it has been evident that Rosetta Stone was one among the companies which can have successful

IPO.

Advantages Disadvantage

The major advantage of IPO (initial public stock

offering) for Rosetta is that is can easily access to

large amount of capital from external sources, on

which no interest charge would be charged, but,

dividends are to be paid to investors in terms of

rewards against risk.

The huge costs and time involved in the process

of going public is the biggest Rosetta stone’s IPO

deal. A long process associated with IPO process

which includes prepare registration statements,

consulting with investment bankers, attorneys,

and accountants, is going to affect the company's

management (Reed and Rocholl, 2010).

As an advantage of IPOs, the aforesaid company

can increase public awareness or can create a

brand image which is further supportive in

grabbing new opportunities and increasing

customer base (Chemmanur and He, 2011)

The initial public offering can be extremely

expensive which another disadvantage is for the

cited company. The expenses include the lead

underwriter's commission; spending on legal

services, printing costs, and the personal

marketing etc. The cost of dividend is going to be

an issue associated with initial public offering of

Rosetta stone.

The organization can easily obtain capital for

future needs in terms of offering equity and debt

financing sources in the public which was a

proper solution of limited corporate investment

as from public sources company can raise huge

amount which can be further invested into new

deals.

In addition to that, disadvantages of IPO involve

loss of confidentiality, flexibility, and control

over the business as public company has to

release all operating details to the public along

with sensitive information of business regarding

future plans (Chemmanur and He, 2011).

The market awareness can be further created as

in IPO process, information about the company is

printed in newspapers which is circulated over

the globe, and hence, company can generate

increased attention in media and among existing

and potential customers (Reed and Rocholl,

2010)

Initial public offerings can enhance the

credibility of Rosetta stone with its suppliers,

customers, and lenders, which is going to

improve credit terms. Hence, it could be said that

an initial public offering offers a public valuation

of mentioned organization.

Valuation of IP for Rosetta stone’s

Valuation & offer price

Price Valuation: $38048

Original price projection: $15-$17

Offering price: $26

Issuing share: 6.25million share

However, the cost of IPO in USA is The cost of IPO in USA is approximately $1 million which

includes listing, printing and legal fees etc.

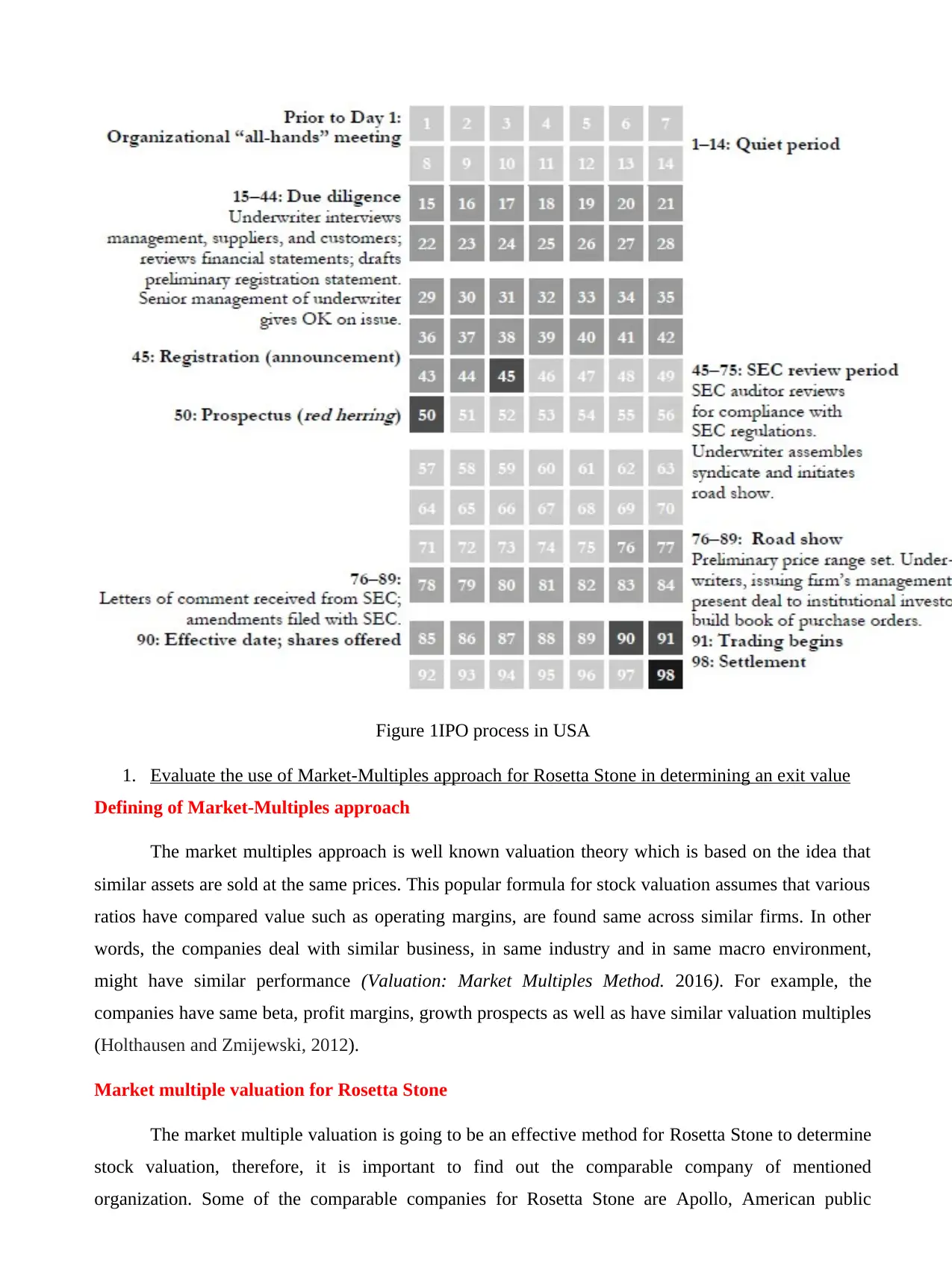

IPO process itself and the legal, financial and other undertakings necessary in “going public”

The IPO process of US is quite typical which was going to be followed by Rosetta stone it its

goes for initial public offerings. The process is completed in almost three months hence, is a long

process, which is going to be a disadvantage for firm (Blum, 2011).

Prior to initiate for a process, it becomes important to carry out a meeting with qualified

management team or board of directors to discuss about equity-issuance process. Including this,

board of members or responsible persons have to discuss about the IPO deals with various

investment bankers, lawyers and accountants before selecting a lead underwriter for which a

in IPO process, information about the company is

printed in newspapers which is circulated over

the globe, and hence, company can generate

increased attention in media and among existing

and potential customers (Reed and Rocholl,

2010)

Initial public offerings can enhance the

credibility of Rosetta stone with its suppliers,

customers, and lenders, which is going to

improve credit terms. Hence, it could be said that

an initial public offering offers a public valuation

of mentioned organization.

Valuation of IP for Rosetta stone’s

Valuation & offer price

Price Valuation: $38048

Original price projection: $15-$17

Offering price: $26

Issuing share: 6.25million share

However, the cost of IPO in USA is The cost of IPO in USA is approximately $1 million which

includes listing, printing and legal fees etc.

IPO process itself and the legal, financial and other undertakings necessary in “going public”

The IPO process of US is quite typical which was going to be followed by Rosetta stone it its

goes for initial public offerings. The process is completed in almost three months hence, is a long

process, which is going to be a disadvantage for firm (Blum, 2011).

Prior to initiate for a process, it becomes important to carry out a meeting with qualified

management team or board of directors to discuss about equity-issuance process. Including this,

board of members or responsible persons have to discuss about the IPO deals with various

investment bankers, lawyers and accountants before selecting a lead underwriter for which a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

significant cots is to be paid (Plotnicki and Szyszka, 2014). However, some additional meeting

are also to be initiated in mid for discussing on problems and reviews. The guidelines of SEC

prohibited company to carry huge publicity for company’s name, products and geographic

locations, but, a normal advertisement can be created.

The process further involves preparation for prospects which is prepared to gain specific

attention from parties along with this the company has to provide make a due diligence in which

management shows that nothing in untrue and not a single misleading information about

company is quoted in the registration statements.

The process of underwriting then stared in which number of investment banks who are agreed to

buy portions, after then SEC review period started, After reviewing the registration process,

letter of comment received from SEC is received. After completing this three months of long

process the organization can trade in equity shares as by getting effective dates and share

offered (Blum, 2011).

are also to be initiated in mid for discussing on problems and reviews. The guidelines of SEC

prohibited company to carry huge publicity for company’s name, products and geographic

locations, but, a normal advertisement can be created.

The process further involves preparation for prospects which is prepared to gain specific

attention from parties along with this the company has to provide make a due diligence in which

management shows that nothing in untrue and not a single misleading information about

company is quoted in the registration statements.

The process of underwriting then stared in which number of investment banks who are agreed to

buy portions, after then SEC review period started, After reviewing the registration process,

letter of comment received from SEC is received. After completing this three months of long

process the organization can trade in equity shares as by getting effective dates and share

offered (Blum, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 1IPO process in USA

1. Evaluate the use of Market-Multiples approach for Rosetta Stone in determining an exit value

Defining of Market-Multiples approach

The market multiples approach is well known valuation theory which is based on the idea that

similar assets are sold at the same prices. This popular formula for stock valuation assumes that various

ratios have compared value such as operating margins, are found same across similar firms. In other

words, the companies deal with similar business, in same industry and in same macro environment,

might have similar performance (Valuation: Market Multiples Method. 2016). For example, the

companies have same beta, profit margins, growth prospects as well as have similar valuation multiples

(Holthausen and Zmijewski, 2012).

Market multiple valuation for Rosetta Stone

The market multiple valuation is going to be an effective method for Rosetta Stone to determine

stock valuation, therefore, it is important to find out the comparable company of mentioned

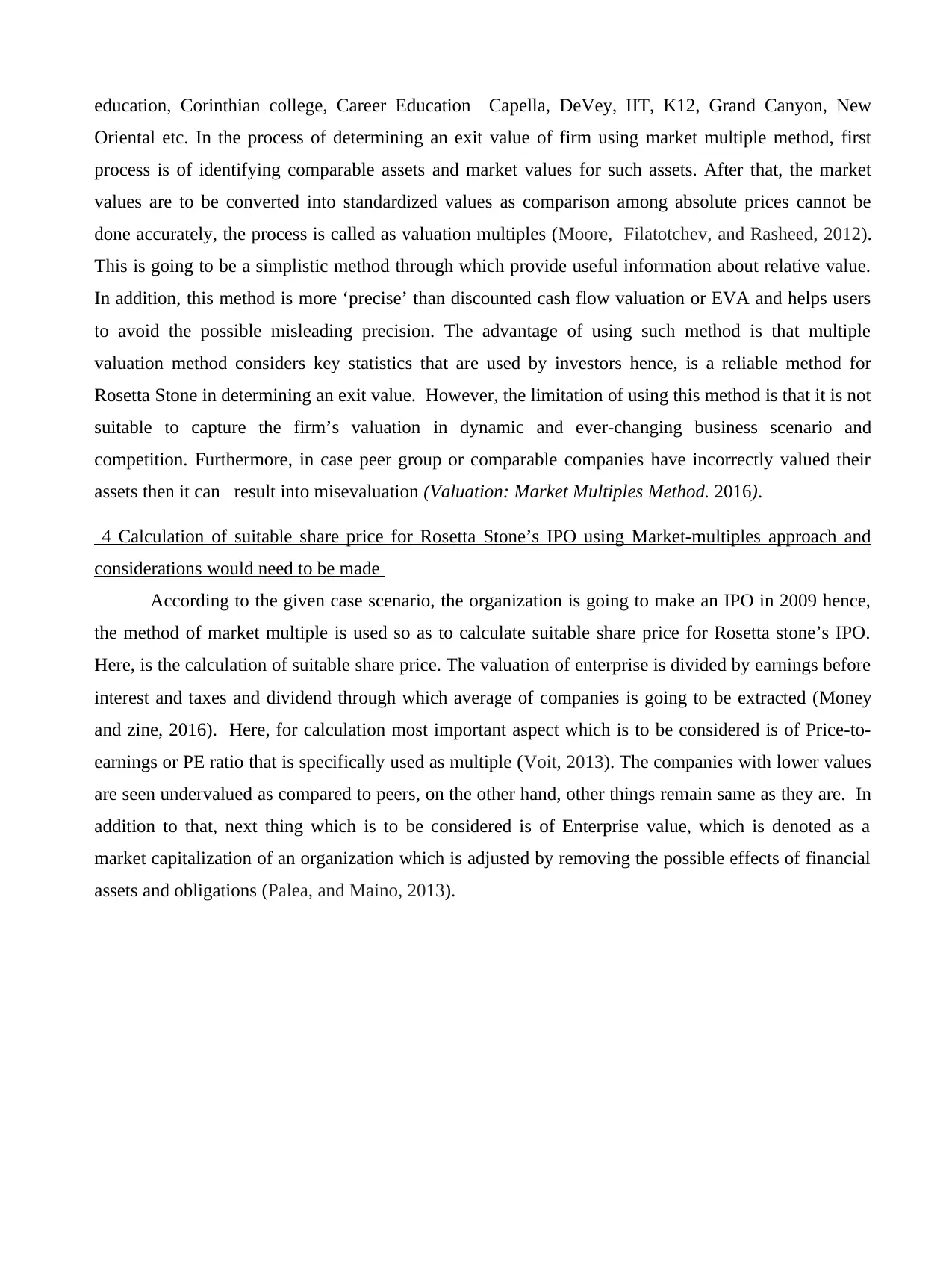

organization. Some of the comparable companies for Rosetta Stone are Apollo, American public

1. Evaluate the use of Market-Multiples approach for Rosetta Stone in determining an exit value

Defining of Market-Multiples approach

The market multiples approach is well known valuation theory which is based on the idea that

similar assets are sold at the same prices. This popular formula for stock valuation assumes that various

ratios have compared value such as operating margins, are found same across similar firms. In other

words, the companies deal with similar business, in same industry and in same macro environment,

might have similar performance (Valuation: Market Multiples Method. 2016). For example, the

companies have same beta, profit margins, growth prospects as well as have similar valuation multiples

(Holthausen and Zmijewski, 2012).

Market multiple valuation for Rosetta Stone

The market multiple valuation is going to be an effective method for Rosetta Stone to determine

stock valuation, therefore, it is important to find out the comparable company of mentioned

organization. Some of the comparable companies for Rosetta Stone are Apollo, American public

education, Corinthian college, Career Education Capella, DeVey, IIT, K12, Grand Canyon, New

Oriental etc. In the process of determining an exit value of firm using market multiple method, first

process is of identifying comparable assets and market values for such assets. After that, the market

values are to be converted into standardized values as comparison among absolute prices cannot be

done accurately, the process is called as valuation multiples (Moore, Filatotchev, and Rasheed, 2012).

This is going to be a simplistic method through which provide useful information about relative value.

In addition, this method is more ‘precise’ than discounted cash flow valuation or EVA and helps users

to avoid the possible misleading precision. The advantage of using such method is that multiple

valuation method considers key statistics that are used by investors hence, is a reliable method for

Rosetta Stone in determining an exit value. However, the limitation of using this method is that it is not

suitable to capture the firm’s valuation in dynamic and ever-changing business scenario and

competition. Furthermore, in case peer group or comparable companies have incorrectly valued their

assets then it can result into misevaluation (Valuation: Market Multiples Method. 2016).

4 Calculation of suitable share price for Rosetta Stone’s IPO using Market-multiples approach and

considerations would need to be made

According to the given case scenario, the organization is going to make an IPO in 2009 hence,

the method of market multiple is used so as to calculate suitable share price for Rosetta stone’s IPO.

Here, is the calculation of suitable share price. The valuation of enterprise is divided by earnings before

interest and taxes and dividend through which average of companies is going to be extracted (Money

and zine, 2016). Here, for calculation most important aspect which is to be considered is of Price-to-

earnings or PE ratio that is specifically used as multiple (Voit, 2013). The companies with lower values

are seen undervalued as compared to peers, on the other hand, other things remain same as they are. In

addition to that, next thing which is to be considered is of Enterprise value, which is denoted as a

market capitalization of an organization which is adjusted by removing the possible effects of financial

assets and obligations (Palea, and Maino, 2013).

Oriental etc. In the process of determining an exit value of firm using market multiple method, first

process is of identifying comparable assets and market values for such assets. After that, the market

values are to be converted into standardized values as comparison among absolute prices cannot be

done accurately, the process is called as valuation multiples (Moore, Filatotchev, and Rasheed, 2012).

This is going to be a simplistic method through which provide useful information about relative value.

In addition, this method is more ‘precise’ than discounted cash flow valuation or EVA and helps users

to avoid the possible misleading precision. The advantage of using such method is that multiple

valuation method considers key statistics that are used by investors hence, is a reliable method for

Rosetta Stone in determining an exit value. However, the limitation of using this method is that it is not

suitable to capture the firm’s valuation in dynamic and ever-changing business scenario and

competition. Furthermore, in case peer group or comparable companies have incorrectly valued their

assets then it can result into misevaluation (Valuation: Market Multiples Method. 2016).

4 Calculation of suitable share price for Rosetta Stone’s IPO using Market-multiples approach and

considerations would need to be made

According to the given case scenario, the organization is going to make an IPO in 2009 hence,

the method of market multiple is used so as to calculate suitable share price for Rosetta stone’s IPO.

Here, is the calculation of suitable share price. The valuation of enterprise is divided by earnings before

interest and taxes and dividend through which average of companies is going to be extracted (Money

and zine, 2016). Here, for calculation most important aspect which is to be considered is of Price-to-

earnings or PE ratio that is specifically used as multiple (Voit, 2013). The companies with lower values

are seen undervalued as compared to peers, on the other hand, other things remain same as they are. In

addition to that, next thing which is to be considered is of Enterprise value, which is denoted as a

market capitalization of an organization which is adjusted by removing the possible effects of financial

assets and obligations (Palea, and Maino, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

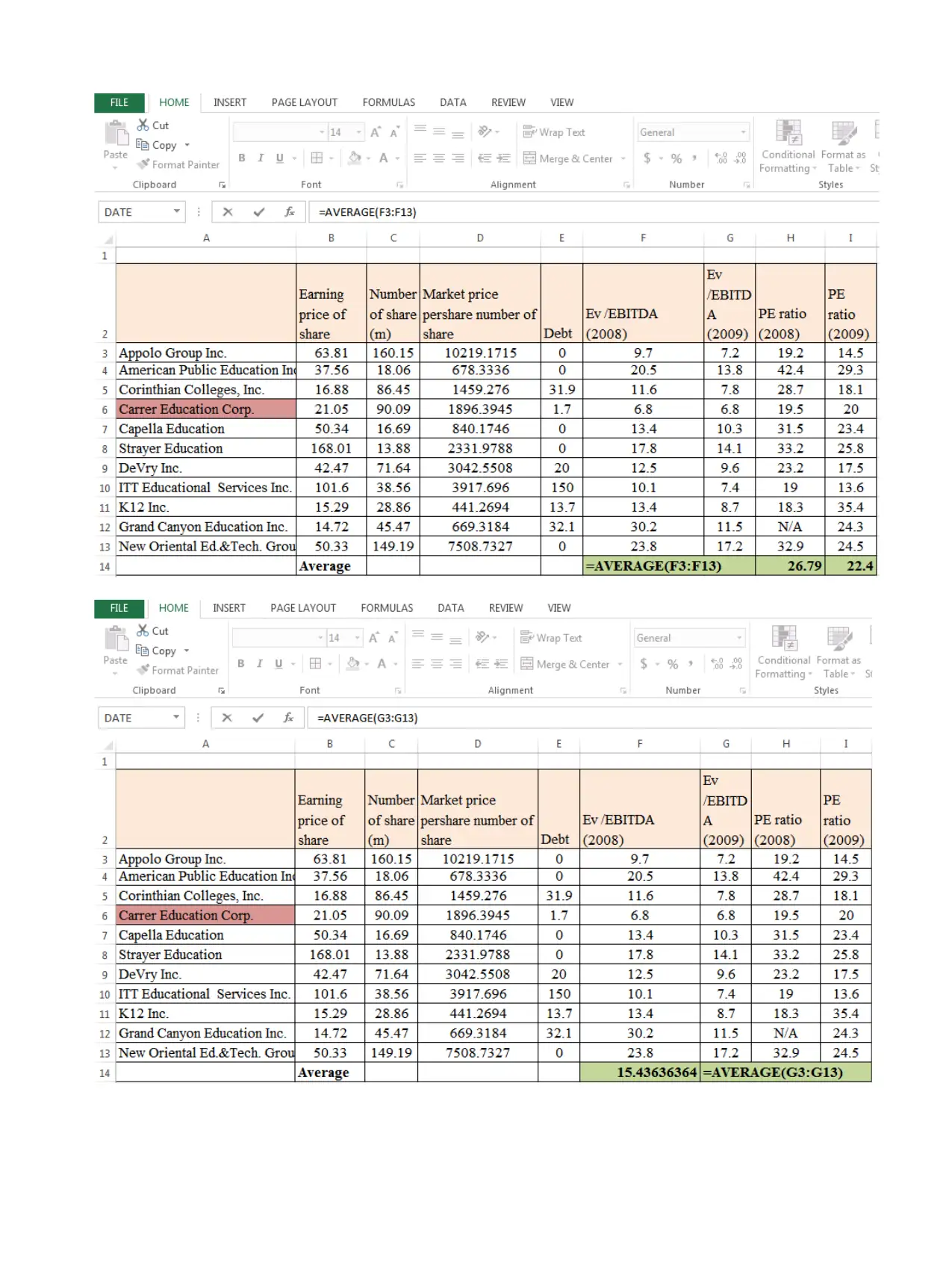

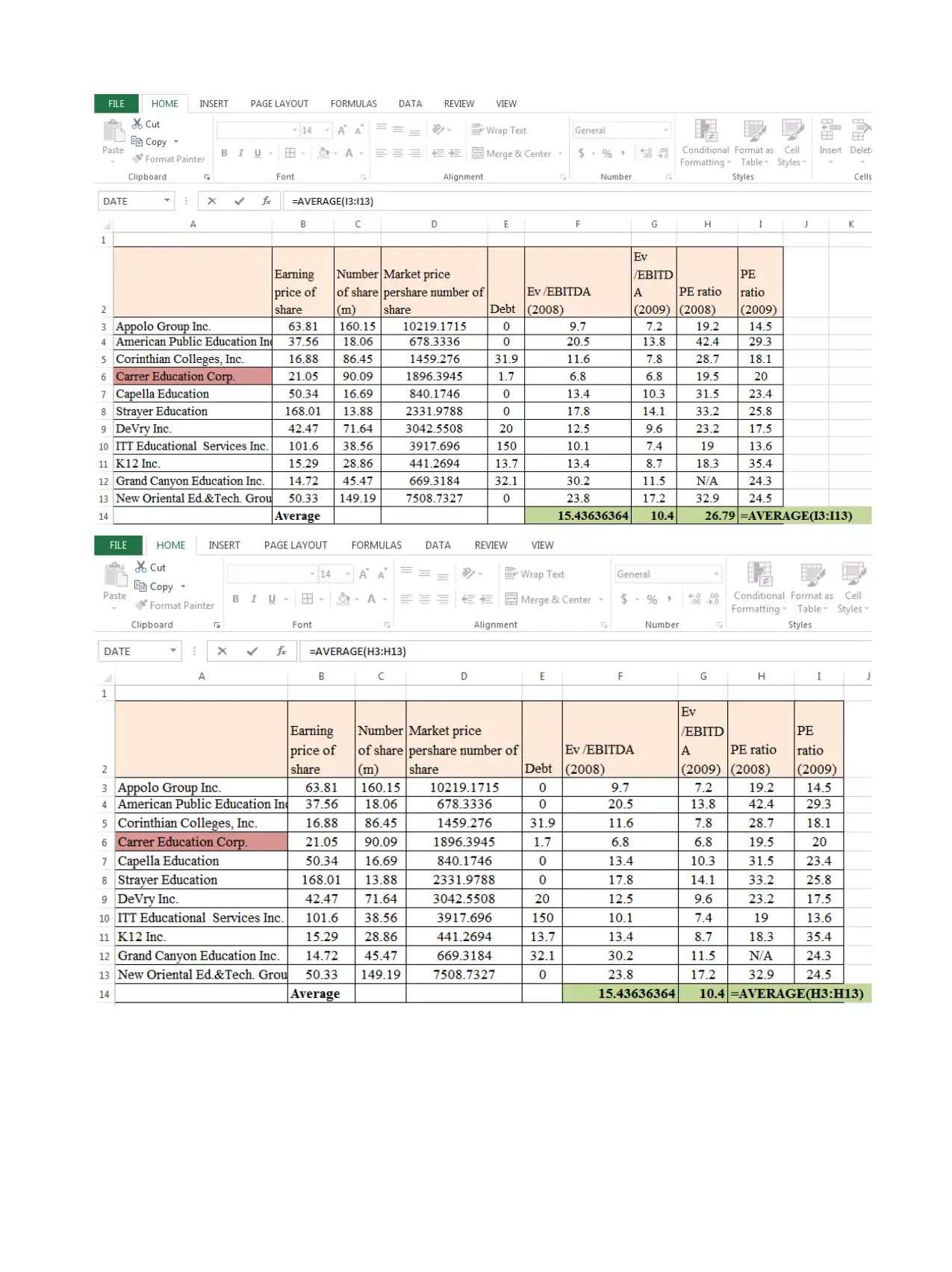

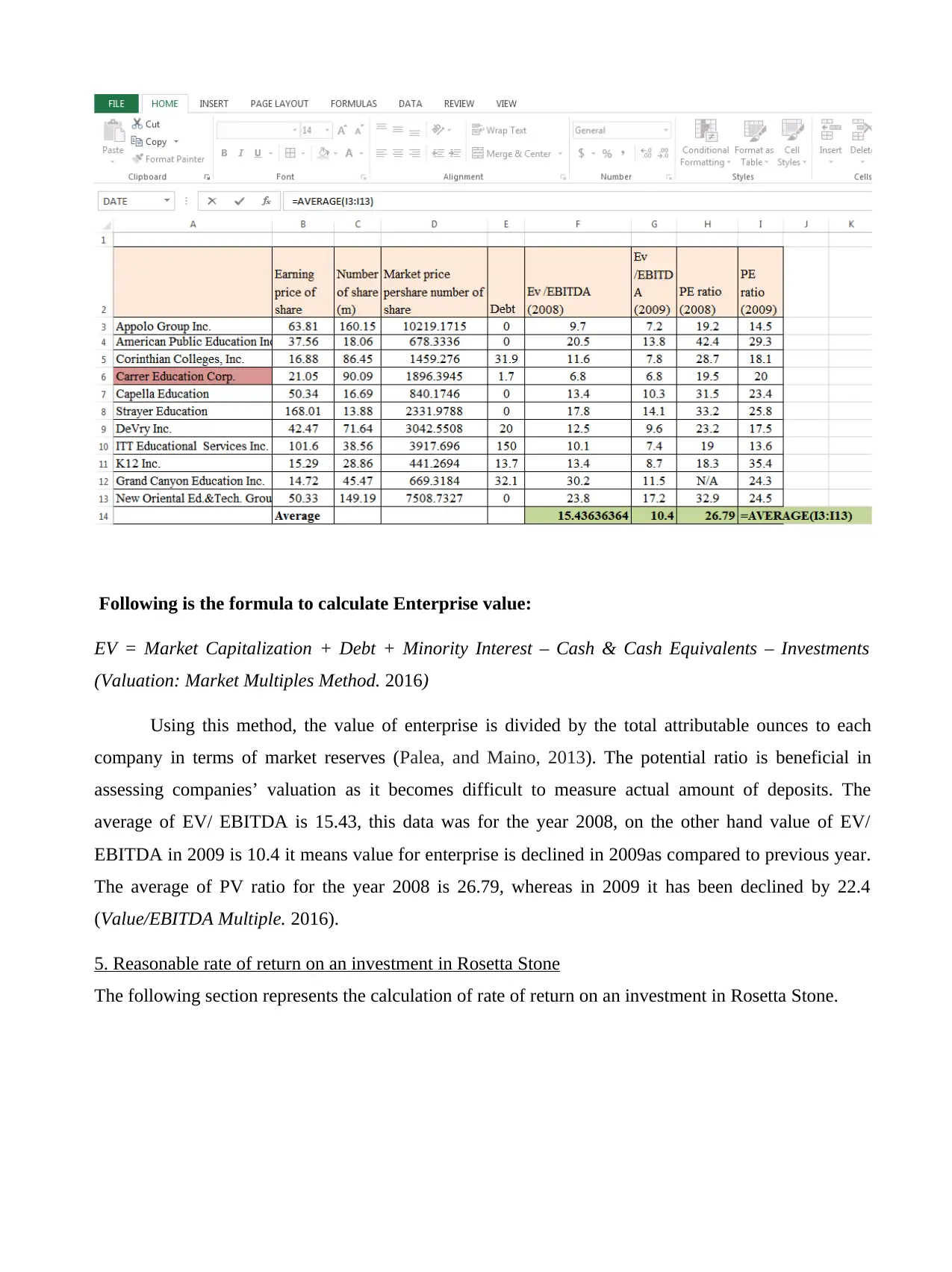

Following is the formula to calculate Enterprise value:

EV = Market Capitalization + Debt + Minority Interest – Cash & Cash Equivalents – Investments

(Valuation: Market Multiples Method. 2016)

Using this method, the value of enterprise is divided by the total attributable ounces to each

company in terms of market reserves (Palea, and Maino, 2013). The potential ratio is beneficial in

assessing companies’ valuation as it becomes difficult to measure actual amount of deposits. The

average of EV/ EBITDA is 15.43, this data was for the year 2008, on the other hand value of EV/

EBITDA in 2009 is 10.4 it means value for enterprise is declined in 2009as compared to previous year.

The average of PV ratio for the year 2008 is 26.79, whereas in 2009 it has been declined by 22.4

(Value/EBITDA Multiple. 2016).

5. Reasonable rate of return on an investment in Rosetta Stone

The following section represents the calculation of rate of return on an investment in Rosetta Stone.

EV = Market Capitalization + Debt + Minority Interest – Cash & Cash Equivalents – Investments

(Valuation: Market Multiples Method. 2016)

Using this method, the value of enterprise is divided by the total attributable ounces to each

company in terms of market reserves (Palea, and Maino, 2013). The potential ratio is beneficial in

assessing companies’ valuation as it becomes difficult to measure actual amount of deposits. The

average of EV/ EBITDA is 15.43, this data was for the year 2008, on the other hand value of EV/

EBITDA in 2009 is 10.4 it means value for enterprise is declined in 2009as compared to previous year.

The average of PV ratio for the year 2008 is 26.79, whereas in 2009 it has been declined by 22.4

(Value/EBITDA Multiple. 2016).

5. Reasonable rate of return on an investment in Rosetta Stone

The following section represents the calculation of rate of return on an investment in Rosetta Stone.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.