Financial Management Report: Rowlinson Knitwear Analysis

VerifiedAdded on 2023/01/13

|15

|4465

|85

Report

AI Summary

This report analyzes financial management concepts, using Rowlinson Knitwear as a case study. It examines the relationship between financial functions and other functional areas like production, marketing, and top management, and also explores the impact of financial objectives on decision-making, including profit maximization, return on investment, and cost minimization. The report differentiates between management and financial accounting, and it analyzes the impact of organizational and regulatory frameworks on financial management, including policies, governance, and compliance. Furthermore, it identifies challenges organizations face in accessing finance, such as time consumption and lack of goodwill. The report also differentiates between budget setting and financial forecasting, evaluates various budget setting approaches, develops a sample budget, and analyzes factors impacting budget management, including corrective actions and reporting procedures for budgetary variances.

Managing Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Examine relationship between financial function and functional areas................................1

1.2 Impact of financial objectives on decision making...............................................................2

1.3 Differentiate between management accounting and financial accounting............................3

1.4 Analyse the impact of organisational and regulatory frameworks on organisation's

approach to financial management..............................................................................................4

1.5 Analyse the challenges organisations face accessing finance...............................................5

TASK 2............................................................................................................................................6

2.1 Differentiate between budget setting and financial forecasting............................................6

2.2 Evaluate budget setting approaches used by organisation....................................................7

2.3 Develop and justify a budget for an area of management responsibility..............................9

2.4 Analyse the factors that impact on budget management.....................................................11

2.5 Specify corrective actions to be take in response to budgetary variance............................11

2.6 Reporting procedures for authorising corrective actions to a budget.................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Examine relationship between financial function and functional areas................................1

1.2 Impact of financial objectives on decision making...............................................................2

1.3 Differentiate between management accounting and financial accounting............................3

1.4 Analyse the impact of organisational and regulatory frameworks on organisation's

approach to financial management..............................................................................................4

1.5 Analyse the challenges organisations face accessing finance...............................................5

TASK 2............................................................................................................................................6

2.1 Differentiate between budget setting and financial forecasting............................................6

2.2 Evaluate budget setting approaches used by organisation....................................................7

2.3 Develop and justify a budget for an area of management responsibility..............................9

2.4 Analyse the factors that impact on budget management.....................................................11

2.5 Specify corrective actions to be take in response to budgetary variance............................11

2.6 Reporting procedures for authorising corrective actions to a budget.................................12

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Finance is one of the resources required by almost every organisation to run the business

smoothly and effectively. It is procured from numerous sources with a view to allocate them

optimally so that decided goals and objectives can be achieved efficiently (Madura, 2020). It is

important for an entity to track the utilisation of the funds available for every department. In this

file, Rowlinson Knitwear is chosen which is located in United Kingdom. Furthermore, this

assignment covers relationship of financial function with other functional areas, impact of

financial objectives on decision making, difference between management and financial

accounting and influence of organisational, regulatory frameworks and challenges faced by

entities in procuring funds. In addition to this, difference between budget setting and financial

forecasting, evaluation of various approaches of budget, factors impacting budget management,

measures for budgetary variance and reporting procedures.

TASK 1

1.1 Examine relationship between financial function and functional areas

Financial function with production department- This department comprises of the

activities of manufacturing of products staring from raw material to finished goods. There are so

many processes involved for making a final item which can be sold to customers. The raw

material is purchased only when there is adequate finance available. The production manager of

Rowlinson Kniteweat has to make decisions such as make or buy, on the basis of which funds

are allocated.

Top management – finance relationship- The main goal of top management is to

survive for long term for which there should be adequate funds. Rowlinson Knitwear can raise

funds from the investors on the basis of good financial statements only. Therefore, financial

function helps in providing the considerations which are taken into account for making decisions.

Financial function and marketing- Marketing is all about raising the awareness of the

products by reaching the target customers. This has direct impact on the profitability of

organisation. Marketing team working in Rowlinson Knitwear has to get the required finance for

carrying the activities of advertising, maintaining stock and many more (Finkler, Smith and

Calabrese, 2018).

1

Finance is one of the resources required by almost every organisation to run the business

smoothly and effectively. It is procured from numerous sources with a view to allocate them

optimally so that decided goals and objectives can be achieved efficiently (Madura, 2020). It is

important for an entity to track the utilisation of the funds available for every department. In this

file, Rowlinson Knitwear is chosen which is located in United Kingdom. Furthermore, this

assignment covers relationship of financial function with other functional areas, impact of

financial objectives on decision making, difference between management and financial

accounting and influence of organisational, regulatory frameworks and challenges faced by

entities in procuring funds. In addition to this, difference between budget setting and financial

forecasting, evaluation of various approaches of budget, factors impacting budget management,

measures for budgetary variance and reporting procedures.

TASK 1

1.1 Examine relationship between financial function and functional areas

Financial function with production department- This department comprises of the

activities of manufacturing of products staring from raw material to finished goods. There are so

many processes involved for making a final item which can be sold to customers. The raw

material is purchased only when there is adequate finance available. The production manager of

Rowlinson Kniteweat has to make decisions such as make or buy, on the basis of which funds

are allocated.

Top management – finance relationship- The main goal of top management is to

survive for long term for which there should be adequate funds. Rowlinson Knitwear can raise

funds from the investors on the basis of good financial statements only. Therefore, financial

function helps in providing the considerations which are taken into account for making decisions.

Financial function and marketing- Marketing is all about raising the awareness of the

products by reaching the target customers. This has direct impact on the profitability of

organisation. Marketing team working in Rowlinson Knitwear has to get the required finance for

carrying the activities of advertising, maintaining stock and many more (Finkler, Smith and

Calabrese, 2018).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Economics- finance interface- This relationship is related with complying with the

various economic policies as developed by the government of a country. There are several

standards and guidelines according to which the organisations have to maintain minimum level

of finance with it. It is a core finance function which takes into account the marginal benefits and

costs.

Accounting and financial functions- Many people use these terms interchangeably but

both of these have different functions. Financial function is related with preparing budgets and

procurement of funds on the basis of budgets developed. On the other hand, accounting is more

about controlling. Therefore, these two departments work closely where the accounting

department records every details of financial transactions in order to help the management make

financial decisions (Burtonshaw-Gunn, 2017).

1.2 Impact of financial objectives on decision making

Profit maximisation: Financial objectives helps the manager to make those polices and

procedure which help in enhancing profitability rate of the entity. Company increase their

profitability rate through increasing earning per share of their products.

Return on investment: Financial objective of the organisation help to maximize the

return on investment. Manager of Rowlinson Knitwear after analysing market condition,

take decision to invest in those portfolio securities which helps to reduced their risk ratio

on investment and increase profitability return rate.

Cost minimization: Main purpose of financial objectives are minimize the cost of

company,through reducing fixed cost of the company. Manger take those decision which

are beneficial for them to reduce variable and extra fixed cost charging on assets.

Rowlinson Knitwear reduce their cost through cutting expense of promote and

advertisement (Martin, 2016).

Tax minimization: Financial objectives helps in planning those policies which helps to

reduce tax liability on company. Manager of Rowlinson Knitwear take decision to invest

in those assets on which government provides deduction on their tax liability.

Corporate governance: It includes all the ethical rules and regulation which an

organisation needs to follow. Financial objective helps entities to work according in

ethical way,Each entity make those decision which are not harmful for environment. The

2

various economic policies as developed by the government of a country. There are several

standards and guidelines according to which the organisations have to maintain minimum level

of finance with it. It is a core finance function which takes into account the marginal benefits and

costs.

Accounting and financial functions- Many people use these terms interchangeably but

both of these have different functions. Financial function is related with preparing budgets and

procurement of funds on the basis of budgets developed. On the other hand, accounting is more

about controlling. Therefore, these two departments work closely where the accounting

department records every details of financial transactions in order to help the management make

financial decisions (Burtonshaw-Gunn, 2017).

1.2 Impact of financial objectives on decision making

Profit maximisation: Financial objectives helps the manager to make those polices and

procedure which help in enhancing profitability rate of the entity. Company increase their

profitability rate through increasing earning per share of their products.

Return on investment: Financial objective of the organisation help to maximize the

return on investment. Manager of Rowlinson Knitwear after analysing market condition,

take decision to invest in those portfolio securities which helps to reduced their risk ratio

on investment and increase profitability return rate.

Cost minimization: Main purpose of financial objectives are minimize the cost of

company,through reducing fixed cost of the company. Manger take those decision which

are beneficial for them to reduce variable and extra fixed cost charging on assets.

Rowlinson Knitwear reduce their cost through cutting expense of promote and

advertisement (Martin, 2016).

Tax minimization: Financial objectives helps in planning those policies which helps to

reduce tax liability on company. Manager of Rowlinson Knitwear take decision to invest

in those assets on which government provides deduction on their tax liability.

Corporate governance: It includes all the ethical rules and regulation which an

organisation needs to follow. Financial objective helps entities to work according in

ethical way,Each entity make those decision which are not harmful for environment. The

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manager of Rowlinson Knitwear make those policies which fulfil all rules imposed by

government.

Capital structure: Success of an entity depends on the capital structure of the company.

Capital structure denotes the ratio of equity and debt of the organisation. Manager of an

organisation take decision regarding making capital structure depends on the financial

capacity of the company. The decision regarding capital structure of Rowlinson Knitwear

totally depends on last 3 years profitability rate.

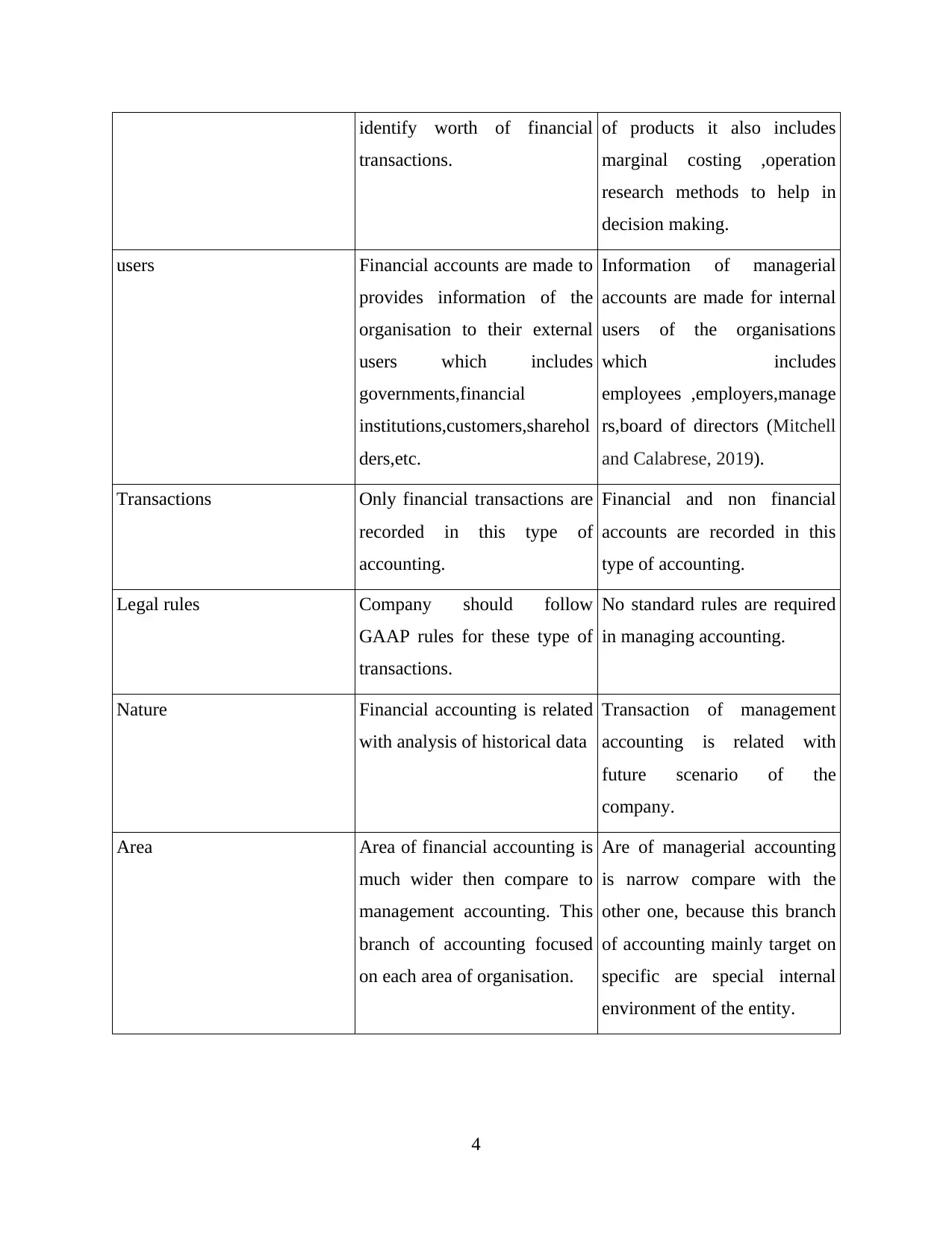

1.3 Differentiate between management accounting and financial accounting

Particulars Financial accounting Management accounting

Definition It is a branch of accounting

which is used to analysis

financial performance of an

organisation through

analysing, collecting,recording

and summarizing financial

transaction of the entity

(Cornwall, Vang and Hartman,

2019).

It is a systematic process of

recording and analysing all

transactions in a way so that

managers performs their

managerialfunctions

effectively.

Objective Main purpose of financial

accounting is profit

maximization,and maximize

their wealth.

The main objective of

management accounting is

helps in decision making and

enhance the capabilities of

managers to perform their

managerial functions.

Techniques In financial accounting

managers use financial

statements,budgets,marginal

costing, break even analysis to

Managers use absorption

costing,job costing,trading and

manufacturing statements for

the purpose of identifies cost

3

government.

Capital structure: Success of an entity depends on the capital structure of the company.

Capital structure denotes the ratio of equity and debt of the organisation. Manager of an

organisation take decision regarding making capital structure depends on the financial

capacity of the company. The decision regarding capital structure of Rowlinson Knitwear

totally depends on last 3 years profitability rate.

1.3 Differentiate between management accounting and financial accounting

Particulars Financial accounting Management accounting

Definition It is a branch of accounting

which is used to analysis

financial performance of an

organisation through

analysing, collecting,recording

and summarizing financial

transaction of the entity

(Cornwall, Vang and Hartman,

2019).

It is a systematic process of

recording and analysing all

transactions in a way so that

managers performs their

managerialfunctions

effectively.

Objective Main purpose of financial

accounting is profit

maximization,and maximize

their wealth.

The main objective of

management accounting is

helps in decision making and

enhance the capabilities of

managers to perform their

managerial functions.

Techniques In financial accounting

managers use financial

statements,budgets,marginal

costing, break even analysis to

Managers use absorption

costing,job costing,trading and

manufacturing statements for

the purpose of identifies cost

3

identify worth of financial

transactions.

of products it also includes

marginal costing ,operation

research methods to help in

decision making.

users Financial accounts are made to

provides information of the

organisation to their external

users which includes

governments,financial

institutions,customers,sharehol

ders,etc.

Information of managerial

accounts are made for internal

users of the organisations

which includes

employees ,employers,manage

rs,board of directors (Mitchell

and Calabrese, 2019).

Transactions Only financial transactions are

recorded in this type of

accounting.

Financial and non financial

accounts are recorded in this

type of accounting.

Legal rules Company should follow

GAAP rules for these type of

transactions.

No standard rules are required

in managing accounting.

Nature Financial accounting is related

with analysis of historical data

Transaction of management

accounting is related with

future scenario of the

company.

Area Area of financial accounting is

much wider then compare to

management accounting. This

branch of accounting focused

on each area of organisation.

Are of managerial accounting

is narrow compare with the

other one, because this branch

of accounting mainly target on

specific are special internal

environment of the entity.

4

transactions.

of products it also includes

marginal costing ,operation

research methods to help in

decision making.

users Financial accounts are made to

provides information of the

organisation to their external

users which includes

governments,financial

institutions,customers,sharehol

ders,etc.

Information of managerial

accounts are made for internal

users of the organisations

which includes

employees ,employers,manage

rs,board of directors (Mitchell

and Calabrese, 2019).

Transactions Only financial transactions are

recorded in this type of

accounting.

Financial and non financial

accounts are recorded in this

type of accounting.

Legal rules Company should follow

GAAP rules for these type of

transactions.

No standard rules are required

in managing accounting.

Nature Financial accounting is related

with analysis of historical data

Transaction of management

accounting is related with

future scenario of the

company.

Area Area of financial accounting is

much wider then compare to

management accounting. This

branch of accounting focused

on each area of organisation.

Are of managerial accounting

is narrow compare with the

other one, because this branch

of accounting mainly target on

specific are special internal

environment of the entity.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.4 Analyse the impact of organisational and regulatory frameworks on organisation's approach

to financial management

Organisational frameworks- It is a set of actions which should be followed in an

organisation to attain goals and objectives of an entity. Some of the elements have been defined

which may impact financial management of Rowlinson Knitwear:

Policies and procedures: These are the basic documents which state guidelines and

directions by following which all the activities are to be carried. These should be modified with

the changes taking place for financial management in the entity (Atmadja and Saputra, 2018).

Governance: This is related with the compliance with all the laws and rules in order to

make the company lawful. Rowlinson Knitwear should abide by the principles and standards by

which financial statements and reports are prepared.

Protocols: These are the set of rules which exist in every company as it has to act by

being within these. There are may different protocols which have direct impact on financial

management as no budget can be set without considering the protocol.

Financial misconduct- It the management of Rowlinson Knitwear has determined any

sort of financial misconduct, the it should switch to that approach of financial management

which can prevent occurrence of such events in future.

Regulatory framework- These are the laws which should be abide by an organisation for

carrying the operations lawfully. These are as follows:

Companies Act, 2006- Every company has to get itself registered under this act in order

to commence the activities. Since, Rowlinson Knitwear is a SME, if it is raising funds from

investors for using it the purpose specified in the prospectus, then it has to use for that motive

only. As there are punishments and fines for the same (Loke, 2017).

International Financial Reporting Standards: This standard provides an uniform set

which should be followed by companies during financial reporting. Rowlinson Knitwear should

abide by these standards in order to report which can be understood by the investors in every

country. Without following this, it will be problematic for it to attract investors.

General Data Protection Regulation (GDPR), 2018- This act is for protecting the

personal information of investors and customers who have interest in the business. In the context

to Rowlinson Knitwear, it should focus on providing adequate security in order to protect the

information which may be confidential.

5

to financial management

Organisational frameworks- It is a set of actions which should be followed in an

organisation to attain goals and objectives of an entity. Some of the elements have been defined

which may impact financial management of Rowlinson Knitwear:

Policies and procedures: These are the basic documents which state guidelines and

directions by following which all the activities are to be carried. These should be modified with

the changes taking place for financial management in the entity (Atmadja and Saputra, 2018).

Governance: This is related with the compliance with all the laws and rules in order to

make the company lawful. Rowlinson Knitwear should abide by the principles and standards by

which financial statements and reports are prepared.

Protocols: These are the set of rules which exist in every company as it has to act by

being within these. There are may different protocols which have direct impact on financial

management as no budget can be set without considering the protocol.

Financial misconduct- It the management of Rowlinson Knitwear has determined any

sort of financial misconduct, the it should switch to that approach of financial management

which can prevent occurrence of such events in future.

Regulatory framework- These are the laws which should be abide by an organisation for

carrying the operations lawfully. These are as follows:

Companies Act, 2006- Every company has to get itself registered under this act in order

to commence the activities. Since, Rowlinson Knitwear is a SME, if it is raising funds from

investors for using it the purpose specified in the prospectus, then it has to use for that motive

only. As there are punishments and fines for the same (Loke, 2017).

International Financial Reporting Standards: This standard provides an uniform set

which should be followed by companies during financial reporting. Rowlinson Knitwear should

abide by these standards in order to report which can be understood by the investors in every

country. Without following this, it will be problematic for it to attract investors.

General Data Protection Regulation (GDPR), 2018- This act is for protecting the

personal information of investors and customers who have interest in the business. In the context

to Rowlinson Knitwear, it should focus on providing adequate security in order to protect the

information which may be confidential.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.5 Analyse the challenges organisations face accessing finance

Finance is an essential part of running organisation. It is the source of providing money to

an organisation. Accessing finance is like an art for manager and the capabilities of manager can

be analysis on the basis of how well they access their finance from various sources.

Organisations faces so many problems while collecting sources of finance. Rowlinson Knitwear

is an small organisation which provides school and corporate wear to their customer. Market are

of the company is not so broad the company facing so many problems of accessing finance,

which are mention below:

Time consumption: The procedure of collecting finance from various source is too long

and it take more time, thus the company not get finance at the right time when they needed it.

Rowlinson Knitwear is small enterprises and they follow all the rules and procedure of corporate

ethics thus it becomes a time consuming process of accessing finance (Karadag, 2017).

Lack of goodwill: the brand value of small size entreprise4s is not so strong

competitively from large size organisations thus big financial institutions and banks are afraid to

provide them loan and other financial facilities. The goodwill of Rowlinson Knitwear is not so

good in the market place they did not get loan easily from banks.

Administrative capabilities: Due to lack of financial capital and technological

advancement strategies regarding marketing of their products are not so effective thus investor

not interested to invest their money in Rowlinson Knitwear .

Attitude to risk and innovation:It is the rule of business the more they take risk the

more they get profit. The management team of small size organisations are not willing to invest

their finance in risky securities,even they did not borrow loan from those institutions whose

interest rate is high they afraid of taking risk and innovate new products. Manager of Rowlinson

Knitwear not invest in risky securities. Thus the earning of the company from their portfolio

securities is not so high.

TASK 2

2.1 Differentiate between budget setting and financial forecasting

Budgeting and financial forecasting are techniques of financial accounting. Manager use

these techniques for making financial plans (Shanmugam and et. al., 2017). Both techniques has

6

Finance is an essential part of running organisation. It is the source of providing money to

an organisation. Accessing finance is like an art for manager and the capabilities of manager can

be analysis on the basis of how well they access their finance from various sources.

Organisations faces so many problems while collecting sources of finance. Rowlinson Knitwear

is an small organisation which provides school and corporate wear to their customer. Market are

of the company is not so broad the company facing so many problems of accessing finance,

which are mention below:

Time consumption: The procedure of collecting finance from various source is too long

and it take more time, thus the company not get finance at the right time when they needed it.

Rowlinson Knitwear is small enterprises and they follow all the rules and procedure of corporate

ethics thus it becomes a time consuming process of accessing finance (Karadag, 2017).

Lack of goodwill: the brand value of small size entreprise4s is not so strong

competitively from large size organisations thus big financial institutions and banks are afraid to

provide them loan and other financial facilities. The goodwill of Rowlinson Knitwear is not so

good in the market place they did not get loan easily from banks.

Administrative capabilities: Due to lack of financial capital and technological

advancement strategies regarding marketing of their products are not so effective thus investor

not interested to invest their money in Rowlinson Knitwear .

Attitude to risk and innovation:It is the rule of business the more they take risk the

more they get profit. The management team of small size organisations are not willing to invest

their finance in risky securities,even they did not borrow loan from those institutions whose

interest rate is high they afraid of taking risk and innovate new products. Manager of Rowlinson

Knitwear not invest in risky securities. Thus the earning of the company from their portfolio

securities is not so high.

TASK 2

2.1 Differentiate between budget setting and financial forecasting

Budgeting and financial forecasting are techniques of financial accounting. Manager use

these techniques for making financial plans (Shanmugam and et. al., 2017). Both techniques has

6

their own merits and demerits organisations use both techniques .There are some differences

between Budget setting and financial forecasting theses are describe as follows:

Particular Budget setting Financial forecasting

Definition Budget setting is a process of

preparing numerical financial

statement which showcase

income and expenditure of an

organisation at fixed period of

time.

It is the process of predicting

future outcomes of an

organisation on the basis of

analysing historical data.

Basis The process of preparing

budget is based on future data.

The process of forecasting is

related with collection of past

data of an organisation

Time Budgeting is related with short

period of time.

It is prepared for longer period

of time.

Focus Budgeting is focusing on

planned events (Prawitz and

Cohart, 2016).

Forecasting is focusing on

anticipating or probable

events.

Results Forecasting end with preparing

of planning process

Budgeting started with

planning process.

Controlling tool Budgeting is act as controlling

tool in management process.

Forecasting is not a tool of

controlling process.

Responsibility It is the duty of top level

managers to make budget

Researchers analysers are

liable for financial forecasting.

2.2 Evaluate budget setting approaches used by organisation

Budget setting is a process of preparing budget. It is essential part of budgetary control. There

are various type of techniques which are used by organisations for preparing a budget,followings

are mention as above:

7

between Budget setting and financial forecasting theses are describe as follows:

Particular Budget setting Financial forecasting

Definition Budget setting is a process of

preparing numerical financial

statement which showcase

income and expenditure of an

organisation at fixed period of

time.

It is the process of predicting

future outcomes of an

organisation on the basis of

analysing historical data.

Basis The process of preparing

budget is based on future data.

The process of forecasting is

related with collection of past

data of an organisation

Time Budgeting is related with short

period of time.

It is prepared for longer period

of time.

Focus Budgeting is focusing on

planned events (Prawitz and

Cohart, 2016).

Forecasting is focusing on

anticipating or probable

events.

Results Forecasting end with preparing

of planning process

Budgeting started with

planning process.

Controlling tool Budgeting is act as controlling

tool in management process.

Forecasting is not a tool of

controlling process.

Responsibility It is the duty of top level

managers to make budget

Researchers analysers are

liable for financial forecasting.

2.2 Evaluate budget setting approaches used by organisation

Budget setting is a process of preparing budget. It is essential part of budgetary control. There

are various type of techniques which are used by organisations for preparing a budget,followings

are mention as above:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incremental budgeting:Organisations use previous years data to make budget. For this

purpose they collect information from past year budgets, and summery of past year

transactions.

Advantages: It is simple and quick method of preparing budget (Grafova and et. al.,

2017).

These method gives accurate results for those organisations whose market conditions are

stable.

Disadvantage: This technique is totally based on historical data which means company

may consider historical errors in preparing budget.

In this technique the budget is based on the assumption is that the given data is accurate

and reliable.

Zero Based Budgeting: It is one of the most famous technique of preparing budget. In

this type of technique the company prepare their budget from zero level that means they

did not consider any past years data. Organisation ake budget on the basis of their on

assumptions and new researchers of environment.

Advantage: The technique is based on proactive approach,it make budget on the basis of

analysing realistic data.

It helps the organisation to connect with business plans. This technique is focused on

achieving organisational objective.

Disadvantage: It is time consuming process of preparing budget (Qamar, Khemta and Jamil,

2016).

This technique cannot be applicable on globally as not each entity star with initial level

because they have prior commitment with their employees,and work.

Contingency budgeting:It includes preparing budget on the basis of estimated data,it

will be prepare in short time period. Contingency level of a budget totally depands on the

accuracy level of a budget. If the budget is 705 accurate then contingency budget will be

prepare for 305.

Advantage: It will be easy and quick process of setting budget.

Disadvantage: It will be hard process for monitoring when setting budget by using this

technique.

8

purpose they collect information from past year budgets, and summery of past year

transactions.

Advantages: It is simple and quick method of preparing budget (Grafova and et. al.,

2017).

These method gives accurate results for those organisations whose market conditions are

stable.

Disadvantage: This technique is totally based on historical data which means company

may consider historical errors in preparing budget.

In this technique the budget is based on the assumption is that the given data is accurate

and reliable.

Zero Based Budgeting: It is one of the most famous technique of preparing budget. In

this type of technique the company prepare their budget from zero level that means they

did not consider any past years data. Organisation ake budget on the basis of their on

assumptions and new researchers of environment.

Advantage: The technique is based on proactive approach,it make budget on the basis of

analysing realistic data.

It helps the organisation to connect with business plans. This technique is focused on

achieving organisational objective.

Disadvantage: It is time consuming process of preparing budget (Qamar, Khemta and Jamil,

2016).

This technique cannot be applicable on globally as not each entity star with initial level

because they have prior commitment with their employees,and work.

Contingency budgeting:It includes preparing budget on the basis of estimated data,it

will be prepare in short time period. Contingency level of a budget totally depands on the

accuracy level of a budget. If the budget is 705 accurate then contingency budget will be

prepare for 305.

Advantage: It will be easy and quick process of setting budget.

Disadvantage: It will be hard process for monitoring when setting budget by using this

technique.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Budgeting: Budgets are prepared on the basis of how much cost an

organisation provides for operating each activity. This technique is useful only when each area

of functional department is separated and cost of every unit can be calculated easily.

Advantage: Organisation can easily allocate their resources.

Most expensive activity can be identified easily and it will help in reducing cost.

Disadvantage: This technique of budgeting is not applicable on service based industries

where services are flexible to provide their customers.

Cash limited budgeting: In this technique budget is prepared on the basis of set limit of

cash. Organisation decided a fixed amount of cash and all decisions are taken on the basis of

decided limit.

Advantage: This technique is useful to eliminate wastage activities from future.

Disadvantage: This technique is not useful for large scale of organisations because they

need to change their technologies and innovate new product to stay in competitive market for

that they need to change their budget policies and need more cash capital,they cannot make

budget by using fixed amount of cash.

The management team of Rowlinson Knitwear can be choose incremental budgeting technique

for preparing budget because their organisation was established since 1935 and they can make

budget plan after analysing past year data. This will be help them to analysis their mistakes and

they will make plans to overcome their errors.

2.3 Develop and justify a budget for an area of management responsibility

Budget is the process of anticipating revenue and expenses for a particular point of time.

It is required to evaluate and monitor on a continuous basis for utilising it properly. It is a tool

used in internal management of organisation.

Budget is the process of anticipating revenue and expenses for a particular point of time. It is

required to evaluate and monitor on a continuous basis for utilising it properly. It is a tool used in

internal management of organisation. It is a statement which shows expected income and

expenses of an entity at fixed period of time Budget plays vital role in enhancing performance

level of the company. It helps in optimum utilization of resources. Every organisation needs to

prepare a budget in order to achieve their organisations goals.

Advantages of budget: Manager uses budget for taking decisions and preparing future

plans. Budget is helpful for analysing performance of workforce of the organisation. It helps to

9

organisation provides for operating each activity. This technique is useful only when each area

of functional department is separated and cost of every unit can be calculated easily.

Advantage: Organisation can easily allocate their resources.

Most expensive activity can be identified easily and it will help in reducing cost.

Disadvantage: This technique of budgeting is not applicable on service based industries

where services are flexible to provide their customers.

Cash limited budgeting: In this technique budget is prepared on the basis of set limit of

cash. Organisation decided a fixed amount of cash and all decisions are taken on the basis of

decided limit.

Advantage: This technique is useful to eliminate wastage activities from future.

Disadvantage: This technique is not useful for large scale of organisations because they

need to change their technologies and innovate new product to stay in competitive market for

that they need to change their budget policies and need more cash capital,they cannot make

budget by using fixed amount of cash.

The management team of Rowlinson Knitwear can be choose incremental budgeting technique

for preparing budget because their organisation was established since 1935 and they can make

budget plan after analysing past year data. This will be help them to analysis their mistakes and

they will make plans to overcome their errors.

2.3 Develop and justify a budget for an area of management responsibility

Budget is the process of anticipating revenue and expenses for a particular point of time.

It is required to evaluate and monitor on a continuous basis for utilising it properly. It is a tool

used in internal management of organisation.

Budget is the process of anticipating revenue and expenses for a particular point of time. It is

required to evaluate and monitor on a continuous basis for utilising it properly. It is a tool used in

internal management of organisation. It is a statement which shows expected income and

expenses of an entity at fixed period of time Budget plays vital role in enhancing performance

level of the company. It helps in optimum utilization of resources. Every organisation needs to

prepare a budget in order to achieve their organisations goals.

Advantages of budget: Manager uses budget for taking decisions and preparing future

plans. Budget is helpful for analysing performance of workforce of the organisation. It helps to

9

set target for all departments of an organisation and to control extra expenditures of the business

entity. It is a tool which is used to analysing risk and then make plans which helps the

organisation to minimize the risk.

Disadvantages of budget:

Preparing a budget is very time consuming and expensive process for organisations as it

take hugs time to collect and analysing data, from various sources. Preparing a budget is risk

taking process because the overall investment decision is based on budgets and it is not

necessary that situations are always in favourable for organisation. Budget is not based on

realistic activities, managers only consider cash related transactions in budget they ignore other

sources which affects on the organisations success strategy

Conflicts arises between manager of different departments due to allocation of expenses among

different department.

Budget £ 20000

Catering £ 3500

Health And Safety £ 4500

Insurance £ 2200

Equipment £ 1600

Transport services £ 1950

Maintenance work £ 1600

Availability of Playground £ 3750

Parking £ 900

10

entity. It is a tool which is used to analysing risk and then make plans which helps the

organisation to minimize the risk.

Disadvantages of budget:

Preparing a budget is very time consuming and expensive process for organisations as it

take hugs time to collect and analysing data, from various sources. Preparing a budget is risk

taking process because the overall investment decision is based on budgets and it is not

necessary that situations are always in favourable for organisation. Budget is not based on

realistic activities, managers only consider cash related transactions in budget they ignore other

sources which affects on the organisations success strategy

Conflicts arises between manager of different departments due to allocation of expenses among

different department.

Budget £ 20000

Catering £ 3500

Health And Safety £ 4500

Insurance £ 2200

Equipment £ 1600

Transport services £ 1950

Maintenance work £ 1600

Availability of Playground £ 3750

Parking £ 900

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.