Management Accounting Report: Rowlinson Knitwear Case Study Analysis

VerifiedAdded on 2020/10/22

|22

|5372

|284

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on a case study of Rowlinson Knitwear, a UK-based clothing manufacturer. The report begins with an introduction to management accounting systems, including different types and their applications, emphasizing their role in organizational decision-making. Task 1 delves into the management accounting system, exploring its origins and the distinctions between management and financial accounting. It also examines various management accounting systems like cost accounting, inventory management, and job costing systems, highlighting their benefits for Rowlinson Knitwear. Task 2 discusses different methods of management accounting reporting, such as inventory management reports, account receivable reports, and batch costing reports, and their importance in tracking financial performance. Task 3 focuses on planning tools used for budgetary control, comparing their advantages and disadvantages, and analyzing their application in resolving financial issues. Task 4 compares Rowlinson Knitwear with other organizations to solve financial issues and evaluates planning tools for responding to financial issues. The report also covers costing methods, including marginal and absorption costing, with calculations of net profitability. The integration of management accounting systems within organizational processes is also discussed.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting system along with their types.........................................................1

Different methods of management accounting reporting.......................................................4

Integration of management accounting systems in organisational process............................5

TASK 2............................................................................................................................................5

Costing methods along with the net calculation of net profitability......................................5

TASK 3............................................................................................................................................9

Different planning tool used for budgetary control with their advantages and disadvantages9

Types of budget techniques..................................................................................................10

Analysis of various planning tools and their application.....................................................11

TASK 4..........................................................................................................................................11

Compare with other organisation regarding to solve financial issues..................................11

Critical analysis of financial issues......................................................................................12

Evaluation of planning tools for responding to financial issues...........................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

APPENDIX....................................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting system along with their types.........................................................1

Different methods of management accounting reporting.......................................................4

Integration of management accounting systems in organisational process............................5

TASK 2............................................................................................................................................5

Costing methods along with the net calculation of net profitability......................................5

TASK 3............................................................................................................................................9

Different planning tool used for budgetary control with their advantages and disadvantages9

Types of budget techniques..................................................................................................10

Analysis of various planning tools and their application.....................................................11

TASK 4..........................................................................................................................................11

Compare with other organisation regarding to solve financial issues..................................11

Critical analysis of financial issues......................................................................................12

Evaluation of planning tools for responding to financial issues...........................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

APPENDIX....................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting may be referred as the process of planning, recording,

summarizing and interpreting financial as well as non-financial data in order to facilitate

managers to make a valuable decisions for the betterment of an organisation (Management

accounting, 2018). Thus, they are playing an important role in growth and success of company

by preparing reports containing statistical as well as financial information that will help in

analysing the actual financial position of an organisation which enables manager to make efforts

for further improvements. The present assignment is based on Rowlinson Knitwear which is

engaged in manufacturing clothing products for school and corporate professionals in UK . The

project discusses the different types of budgets along with the budgetary control planning tools.

In addition with this, management accounting and reporting systems are also covered under this

report along with their beneficial outcome to company. The project also described the costing

methods with proper illustration of calculation of net profitability using marginal and absorption

costing methods. Planning tools to resolve financial issues are also summarised under this report

along with the comparison to other company engaged in similar sector.

TASK 1

Management accounting system along with their types

Origin of Management Accounting: This is the concept which came into existence in the

year 1950. It first formally described in a report entitled “Management Accounting” in 1950. The

report was first published by the Anglo American Council of Productivity Management

Accounting Team after its visit to US in the first quarter of 1950.

Management accounting system is the process of recording and managing valuable

information related with financial as well as non-financial data in order to facilitate managers of

an organisation to make an effective decisions and suitable plans for the betterment of an

organisation. For this, mutual support by different departments is necessary as the reliability and

accuracy of information of different divisions are much depends on the managers of different

departments. Such departments includes production, marketing, finance, human resource etc.

whose informations of their operations are recorded at one place (Amidu, Effah and Abor,

2011).

1

Management accounting may be referred as the process of planning, recording,

summarizing and interpreting financial as well as non-financial data in order to facilitate

managers to make a valuable decisions for the betterment of an organisation (Management

accounting, 2018). Thus, they are playing an important role in growth and success of company

by preparing reports containing statistical as well as financial information that will help in

analysing the actual financial position of an organisation which enables manager to make efforts

for further improvements. The present assignment is based on Rowlinson Knitwear which is

engaged in manufacturing clothing products for school and corporate professionals in UK . The

project discusses the different types of budgets along with the budgetary control planning tools.

In addition with this, management accounting and reporting systems are also covered under this

report along with their beneficial outcome to company. The project also described the costing

methods with proper illustration of calculation of net profitability using marginal and absorption

costing methods. Planning tools to resolve financial issues are also summarised under this report

along with the comparison to other company engaged in similar sector.

TASK 1

Management accounting system along with their types

Origin of Management Accounting: This is the concept which came into existence in the

year 1950. It first formally described in a report entitled “Management Accounting” in 1950. The

report was first published by the Anglo American Council of Productivity Management

Accounting Team after its visit to US in the first quarter of 1950.

Management accounting system is the process of recording and managing valuable

information related with financial as well as non-financial data in order to facilitate managers of

an organisation to make an effective decisions and suitable plans for the betterment of an

organisation. For this, mutual support by different departments is necessary as the reliability and

accuracy of information of different divisions are much depends on the managers of different

departments. Such departments includes production, marketing, finance, human resource etc.

whose informations of their operations are recorded at one place (Amidu, Effah and Abor,

2011).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

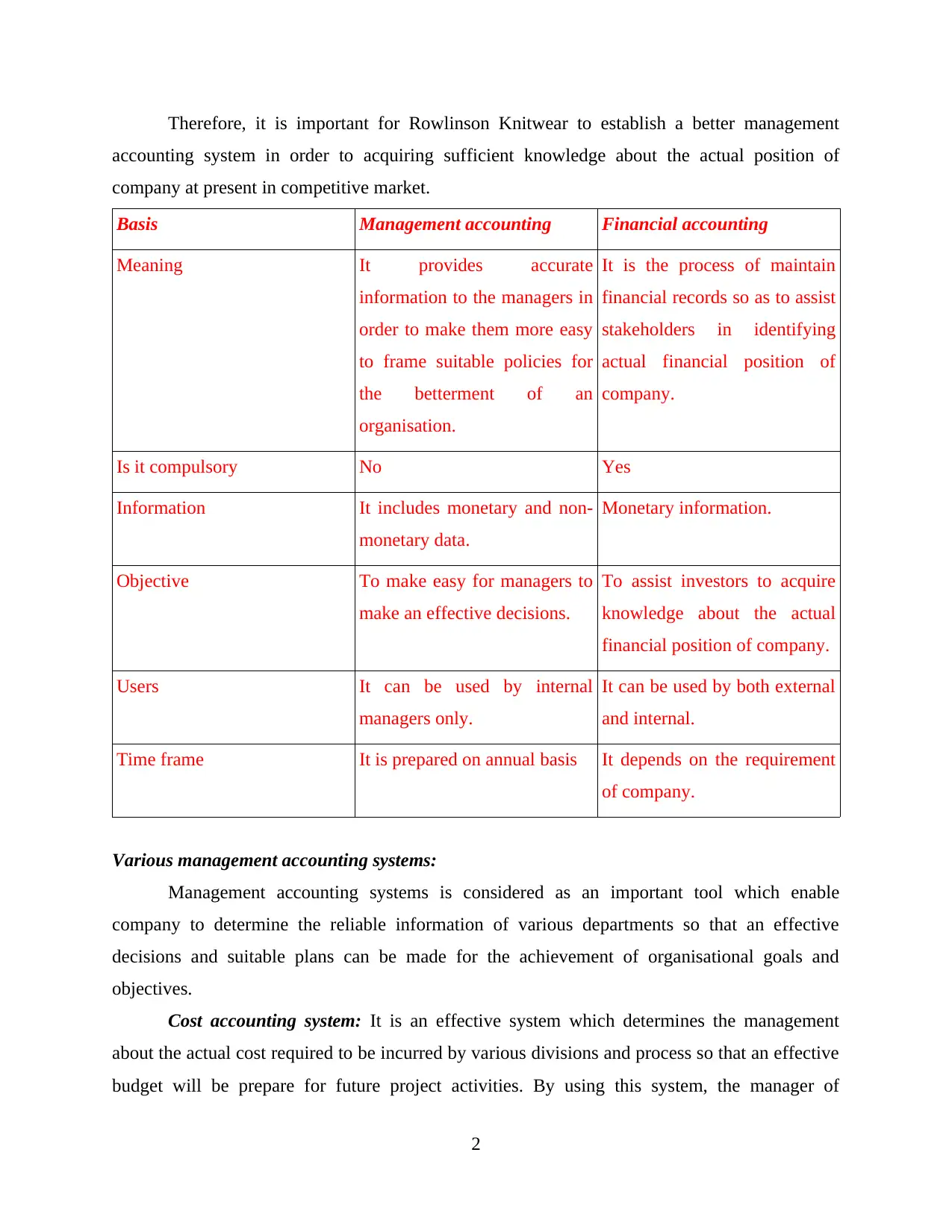

Therefore, it is important for Rowlinson Knitwear to establish a better management

accounting system in order to acquiring sufficient knowledge about the actual position of

company at present in competitive market.

Basis Management accounting Financial accounting

Meaning It provides accurate

information to the managers in

order to make them more easy

to frame suitable policies for

the betterment of an

organisation.

It is the process of maintain

financial records so as to assist

stakeholders in identifying

actual financial position of

company.

Is it compulsory No Yes

Information It includes monetary and non-

monetary data.

Monetary information.

Objective To make easy for managers to

make an effective decisions.

To assist investors to acquire

knowledge about the actual

financial position of company.

Users It can be used by internal

managers only.

It can be used by both external

and internal.

Time frame It is prepared on annual basis It depends on the requirement

of company.

Various management accounting systems:

Management accounting systems is considered as an important tool which enable

company to determine the reliable information of various departments so that an effective

decisions and suitable plans can be made for the achievement of organisational goals and

objectives.

Cost accounting system: It is an effective system which determines the management

about the actual cost required to be incurred by various divisions and process so that an effective

budget will be prepare for future project activities. By using this system, the manager of

2

accounting system in order to acquiring sufficient knowledge about the actual position of

company at present in competitive market.

Basis Management accounting Financial accounting

Meaning It provides accurate

information to the managers in

order to make them more easy

to frame suitable policies for

the betterment of an

organisation.

It is the process of maintain

financial records so as to assist

stakeholders in identifying

actual financial position of

company.

Is it compulsory No Yes

Information It includes monetary and non-

monetary data.

Monetary information.

Objective To make easy for managers to

make an effective decisions.

To assist investors to acquire

knowledge about the actual

financial position of company.

Users It can be used by internal

managers only.

It can be used by both external

and internal.

Time frame It is prepared on annual basis It depends on the requirement

of company.

Various management accounting systems:

Management accounting systems is considered as an important tool which enable

company to determine the reliable information of various departments so that an effective

decisions and suitable plans can be made for the achievement of organisational goals and

objectives.

Cost accounting system: It is an effective system which determines the management

about the actual cost required to be incurred by various divisions and process so that an effective

budget will be prepare for future project activities. By using this system, the manager of

2

Rowlinson Knitwear is able to record, categorise and estimate the total cost which will be

incurred in future business operations so that maximum profitability can be achieved (Ax and

Greve, 2017). Such system is categorised into three types which includes normal, direct and

standard cost. Such system assist an organisation in handling material, labour and overhead costs

accurately so as to determine accurately the unit cost. Rowlinson Knitwear is engaged in

manufacture school and corporate wear garments due to which such system brings more

beneficial outcome in terms of identifying the cost and budget to execute different functions of

business. It minimises the expenses as well as enhanced profit of company. Types of costs are

given as under:

Direct cost: Such kind of cost in inconsistent and fluctuated on the basis of trends and

changes in the market. Such price is wholly attributed for manufacturing products and creating

services.

Standard cost: It defined as the process of comparing desired cost with actual cost in the

accounts and records. It enables management to identify the deviations which can restrict

employees to execute activities within allotted cost. Benefit: It assist management of Rowlinson Knitwear to prepare accurate budget for

future business operations after analysing the actual cost incurred in previous year. It

minimises the wastage of funds which makes positive impact on the profitability of

company (Drury, 2013).

Inventory management system: It is such system related which brings awareness towards

managers about the actual level of inventory the company have at present. It is further classified

into two parts which includes periodic and perpetual system. Periodic system is adopted to

record the transactions related with inventory on monthly or weekly basis. On the other hand,

perpetual system is adopted to update the managers after the selling or acquiring products.

Rowlinson Knitwear is following FIFO and LIFO analyse which makes easy for managers to get

information about available resources with company. It assist managers to decide whether the

company have sufficient amount of inventory or should order from the suppliers in order to

continue business operations smoothly. It can facilitate company to meet customers needs and

requirements on time due to which the loyalty of customers can be easily achieved. Benefits: It facilitate Rowlinson Knitwear in maintaining adequate level of inventory as

as to make easy for managers to take orders of products from the customers and supply

3

incurred in future business operations so that maximum profitability can be achieved (Ax and

Greve, 2017). Such system is categorised into three types which includes normal, direct and

standard cost. Such system assist an organisation in handling material, labour and overhead costs

accurately so as to determine accurately the unit cost. Rowlinson Knitwear is engaged in

manufacture school and corporate wear garments due to which such system brings more

beneficial outcome in terms of identifying the cost and budget to execute different functions of

business. It minimises the expenses as well as enhanced profit of company. Types of costs are

given as under:

Direct cost: Such kind of cost in inconsistent and fluctuated on the basis of trends and

changes in the market. Such price is wholly attributed for manufacturing products and creating

services.

Standard cost: It defined as the process of comparing desired cost with actual cost in the

accounts and records. It enables management to identify the deviations which can restrict

employees to execute activities within allotted cost. Benefit: It assist management of Rowlinson Knitwear to prepare accurate budget for

future business operations after analysing the actual cost incurred in previous year. It

minimises the wastage of funds which makes positive impact on the profitability of

company (Drury, 2013).

Inventory management system: It is such system related which brings awareness towards

managers about the actual level of inventory the company have at present. It is further classified

into two parts which includes periodic and perpetual system. Periodic system is adopted to

record the transactions related with inventory on monthly or weekly basis. On the other hand,

perpetual system is adopted to update the managers after the selling or acquiring products.

Rowlinson Knitwear is following FIFO and LIFO analyse which makes easy for managers to get

information about available resources with company. It assist managers to decide whether the

company have sufficient amount of inventory or should order from the suppliers in order to

continue business operations smoothly. It can facilitate company to meet customers needs and

requirements on time due to which the loyalty of customers can be easily achieved. Benefits: It facilitate Rowlinson Knitwear in maintaining adequate level of inventory as

as to make easy for managers to take orders of products from the customers and supply

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

them on time. It establishes trust and gain loyalty of customers towards company for

longer period of time.

Job costing system: It is the system which enables managers to determine the costs and

expenses allocated to a particular product and service so that estimation of profits will be

determined. Costs is the valuation of efforts, resources, time etc. which are utilised in execution

of various process of organisation. Such system is categorised into two types which includes

batch and process costing. Using such system by the managers of Rowlinson Knitwear enable

them to calculate the necessary cost of workers and production accordingly in order to achieve

huge profits and revenues (Gibassier and Schaltegger, 2015). It increases capabilities of an

organisation to meet customers requirements through producing products which are more in

demanded. It provides an opportunity to company to achieve loyalty of existing customers and

attract new customers.

Benefit: Using such system facilitate the management of Rowlinson Knitwear to

determine the overall cost of workers' efforts which will assist them to make an effective

decisions regarding distribution of resources and expenses required to incurred in

execution of business operations.

Different methods of management accounting reporting

Every organisation always tried to achieve huge sustainability and profitability in market

so as to increase their brand position among their rivals. It can be possible through maintaining

accounting reports related to the cost and budget of various departments working for the

betterment of an organisation. For this, the management is held liable to prepare and manage

such reports on quarterly basis so as to determine the financial stability of company. Therefore,

the management of Rowlinson Knitwear should maintain accounting reports ion regular basis if

wants to expand its business to large scale. There are various kinds of reports such as

performance reports, account receivable reports etc. which are further discussed as under:

Inventory management report: Such reports detailing the information about the level of

inventory the company have at present so that further decision of filling inventory are made.

Preparing such report enables the managers of Rowlinson Knitwear to manage the stocks

movements and reviewing the current stocks by using time and location of movements of

inventory. There are various methods and techniques which can be adopted by Rowlinson

Knitwear such as Just-in-time, EOQ, and Turnover ratio. As Rowlinson Knitwear is engaged in

4

longer period of time.

Job costing system: It is the system which enables managers to determine the costs and

expenses allocated to a particular product and service so that estimation of profits will be

determined. Costs is the valuation of efforts, resources, time etc. which are utilised in execution

of various process of organisation. Such system is categorised into two types which includes

batch and process costing. Using such system by the managers of Rowlinson Knitwear enable

them to calculate the necessary cost of workers and production accordingly in order to achieve

huge profits and revenues (Gibassier and Schaltegger, 2015). It increases capabilities of an

organisation to meet customers requirements through producing products which are more in

demanded. It provides an opportunity to company to achieve loyalty of existing customers and

attract new customers.

Benefit: Using such system facilitate the management of Rowlinson Knitwear to

determine the overall cost of workers' efforts which will assist them to make an effective

decisions regarding distribution of resources and expenses required to incurred in

execution of business operations.

Different methods of management accounting reporting

Every organisation always tried to achieve huge sustainability and profitability in market

so as to increase their brand position among their rivals. It can be possible through maintaining

accounting reports related to the cost and budget of various departments working for the

betterment of an organisation. For this, the management is held liable to prepare and manage

such reports on quarterly basis so as to determine the financial stability of company. Therefore,

the management of Rowlinson Knitwear should maintain accounting reports ion regular basis if

wants to expand its business to large scale. There are various kinds of reports such as

performance reports, account receivable reports etc. which are further discussed as under:

Inventory management report: Such reports detailing the information about the level of

inventory the company have at present so that further decision of filling inventory are made.

Preparing such report enables the managers of Rowlinson Knitwear to manage the stocks

movements and reviewing the current stocks by using time and location of movements of

inventory. There are various methods and techniques which can be adopted by Rowlinson

Knitwear such as Just-in-time, EOQ, and Turnover ratio. As Rowlinson Knitwear is engaged in

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manufacturing clothing products fro school and corporate professionals which is always more in

demanded. Therefore, it is important for management to have knowledge about their current

level of inventory (Griffin, 2017).

Account receivable report: Such kinds of report contains the information about the

unpaid customer bills and unused names which makes easy for managers to identify the debtors

from which the unpaid amount will be recovered. It also facilitate managers to determine the

unpaid consumers and recover the amount within due date. Therefore, the management of

Rowlinson Knitwear required to maintain these kind of reports in order to make suitable changes

in credit policies so that financial stability can be maintained for longer period of time.

Batch costing report: These kind of reports assist management of Rowlinson Knitwear to

track the expenses and costs of activities performed by the workers. Such reports will make easy

for management to evaluate and control overall cost incurred in production and selling activities.

This will increases the chances of generating huge profits and revenue (Lavia López and Hiebl,

2014).

Integration of management accounting systems in organisational process

Rowlinson Knitwear is utilizing the management accounting as well as reporting system

for giving information and data of financials to the different investor and speculator. The

interconnection between reporting and management system in business process is termed as

integrated accounting system. For example, inventory management system and reporting assist

manager to identify the actual level of inventory with company at present which enable them to

take orders from the suppliers so that production department can perform its functions without

any interruptions and meet the customers requirements on time. It achieved loyalty and trust of

customers. On the other hand, using account receivable report provides the list of unpaid debtors

so that it can be recovered on time. Failure of recovery of due amount may affect their pricing

strategies on sales and revenues. Therefore, it is essential to maintain such kind of report in order

to enhance financial stability of company.

5

demanded. Therefore, it is important for management to have knowledge about their current

level of inventory (Griffin, 2017).

Account receivable report: Such kinds of report contains the information about the

unpaid customer bills and unused names which makes easy for managers to identify the debtors

from which the unpaid amount will be recovered. It also facilitate managers to determine the

unpaid consumers and recover the amount within due date. Therefore, the management of

Rowlinson Knitwear required to maintain these kind of reports in order to make suitable changes

in credit policies so that financial stability can be maintained for longer period of time.

Batch costing report: These kind of reports assist management of Rowlinson Knitwear to

track the expenses and costs of activities performed by the workers. Such reports will make easy

for management to evaluate and control overall cost incurred in production and selling activities.

This will increases the chances of generating huge profits and revenue (Lavia López and Hiebl,

2014).

Integration of management accounting systems in organisational process

Rowlinson Knitwear is utilizing the management accounting as well as reporting system

for giving information and data of financials to the different investor and speculator. The

interconnection between reporting and management system in business process is termed as

integrated accounting system. For example, inventory management system and reporting assist

manager to identify the actual level of inventory with company at present which enable them to

take orders from the suppliers so that production department can perform its functions without

any interruptions and meet the customers requirements on time. It achieved loyalty and trust of

customers. On the other hand, using account receivable report provides the list of unpaid debtors

so that it can be recovered on time. Failure of recovery of due amount may affect their pricing

strategies on sales and revenues. Therefore, it is essential to maintain such kind of report in order

to enhance financial stability of company.

5

TASK 2

Costing methods along with the net calculation of net profitability

Cost: It may be defined as the amount of value which is invested in produce or acquire

something to gain huge profits. In other words, it is a valuation of different aspects such as

efforts, time, resources etc. which are necessary to utilise in production process.

Management of Rowlinson Knitwear should prepare an effective budget for the execution of

future business activities in which allocation of cost, time and efforts are allocated properly after

analysing the effectiveness and profitability of future activities. Cost is classified into two types

which includes marginal and absorption costing method that will be adopted on the basis of

needs and requirements so that maximum profitability can be achieved (Mokhtar, Jusoh and

Zulkifli, 2016).

Marginal costing:

It is also known as variable costing method which includes only variable cost and avoid

fixed cost. It is a costing method which is mostly used to adopt when an organisation

manufactures extra unit of products and services. It focuses on variable cost which includes

direct material and labour involved, selling price etc. Mostly Small-scale organisation are using

such method in order to show increment in net profitability in their financial statement so that

investors can be easily towards them with a hope of getting maximum return in future (Nixon

and Burns, 2012).

Absorption costing:

It is considered as an effective costing method which assist company to represent actual

total cost incurred and net profitability generated in their financial statements by including

variable and fixed costs. It is adopted by large sized organisation such as Rowlinson Knitwear in

order to show their actual financial position to their existing investors so that their trust and

loyalty will be successfully retained with company for longer period of time.

These both costing methods are adopted by company to determine the net profitability of

company. It can be better understood through a following illustration:

Income statement on the basis of Marginal costing method:

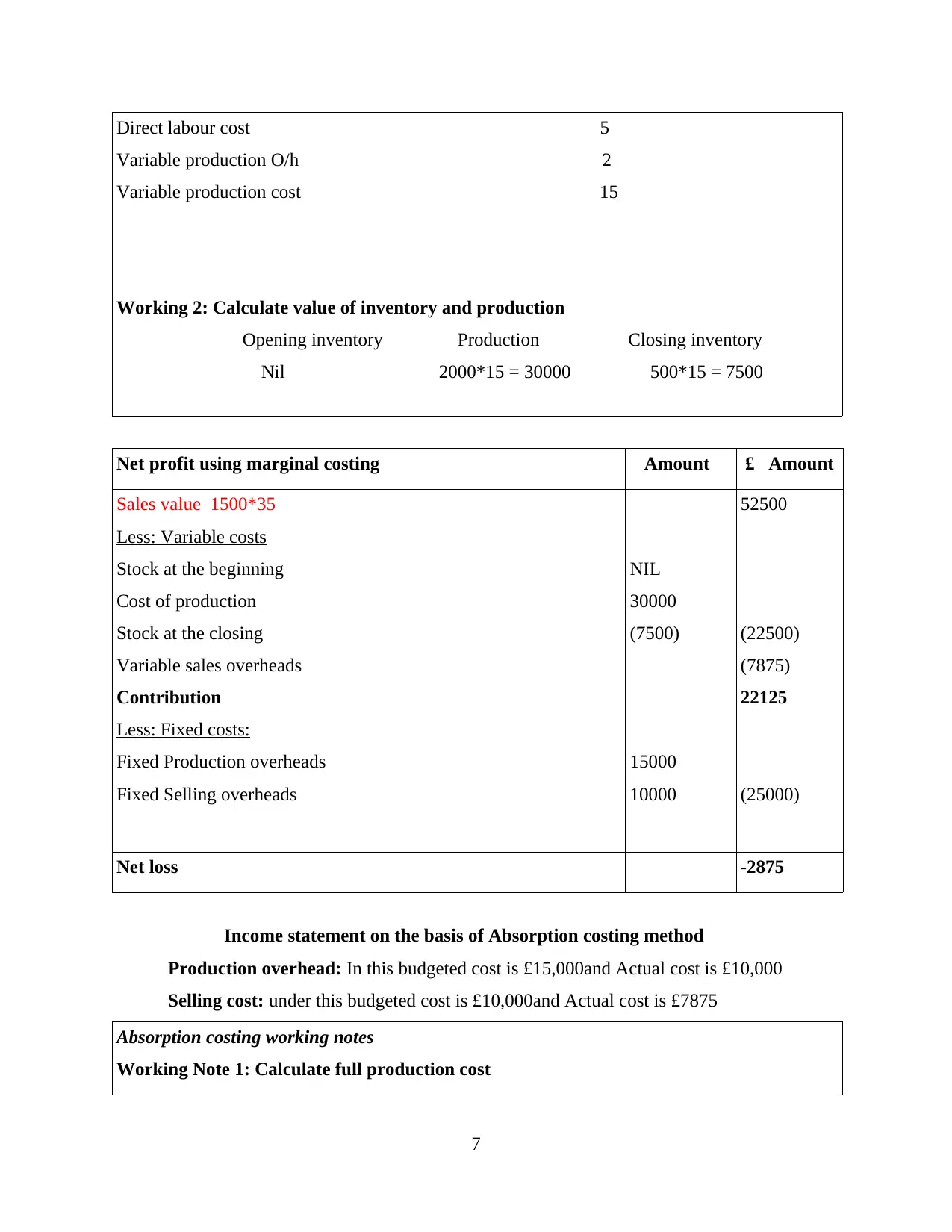

Working 1: Calculate variable production cost £

Direct material cost 8

6

Costing methods along with the net calculation of net profitability

Cost: It may be defined as the amount of value which is invested in produce or acquire

something to gain huge profits. In other words, it is a valuation of different aspects such as

efforts, time, resources etc. which are necessary to utilise in production process.

Management of Rowlinson Knitwear should prepare an effective budget for the execution of

future business activities in which allocation of cost, time and efforts are allocated properly after

analysing the effectiveness and profitability of future activities. Cost is classified into two types

which includes marginal and absorption costing method that will be adopted on the basis of

needs and requirements so that maximum profitability can be achieved (Mokhtar, Jusoh and

Zulkifli, 2016).

Marginal costing:

It is also known as variable costing method which includes only variable cost and avoid

fixed cost. It is a costing method which is mostly used to adopt when an organisation

manufactures extra unit of products and services. It focuses on variable cost which includes

direct material and labour involved, selling price etc. Mostly Small-scale organisation are using

such method in order to show increment in net profitability in their financial statement so that

investors can be easily towards them with a hope of getting maximum return in future (Nixon

and Burns, 2012).

Absorption costing:

It is considered as an effective costing method which assist company to represent actual

total cost incurred and net profitability generated in their financial statements by including

variable and fixed costs. It is adopted by large sized organisation such as Rowlinson Knitwear in

order to show their actual financial position to their existing investors so that their trust and

loyalty will be successfully retained with company for longer period of time.

These both costing methods are adopted by company to determine the net profitability of

company. It can be better understood through a following illustration:

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value 1500*35

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

7

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value 1500*35

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

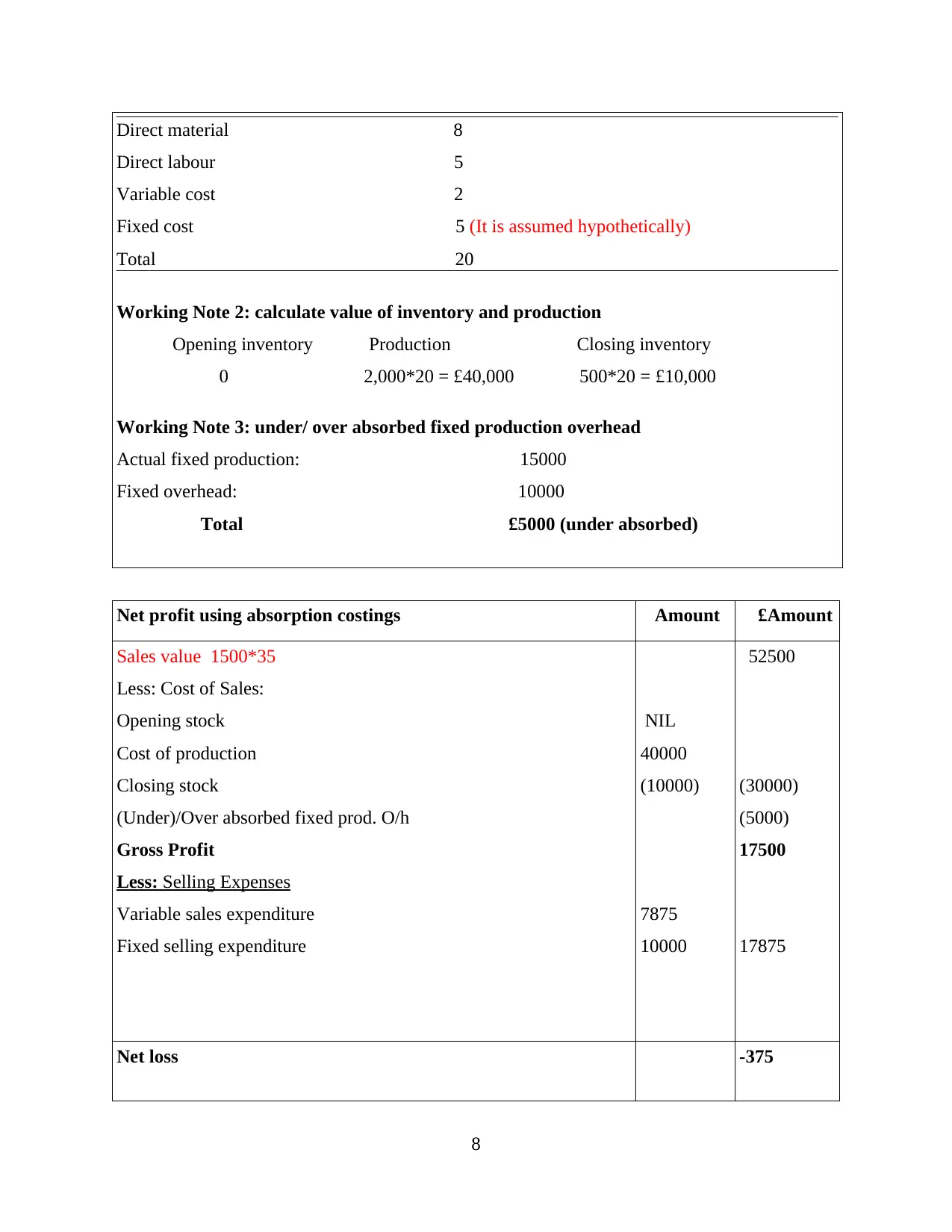

Working Note 1: Calculate full production cost

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5 (It is assumed hypothetically)

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value 1500*35

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

8

Direct labour £5

Variable cost £2

Fixed cost £5 (It is assumed hypothetically)

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value 1500*35

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

8

TASK 3

Different planning tool used for budgetary control with their advantages and disadvantages

Budget: It is the predicted costs and funds which is necessary for performing the various

business operations in an organisation. It is the process of allotting funds for doing the activities

of a firm after analysing the costs and profit of previous year.

Budgetary control: This is the process for controlling and regulating the various budgets

which are assigned to various departments and processes. It compares the expected results with

the actual outcomes for determining that the process is following the allotted budget properly or

not. It is useful for Rowlinson knitwear to determine the variations and gaps in their performance

and then take suitable and appropriate measures for removing the identified gaps in future

(Schaltegger and Burritt, 2017).

It is very necessary for the management of Rowlinson knitwear to control their budget of

various operations for improving their efficiency and profit. Budget control plan must be

formulated accordingly to the needs of departments for ensuring that the operations are carried

out properly for accomplishing the desired goals and objectives of the firm. Various tools of

budget control are used by the companies to determine their financials which are given below:

Forecasting tools: It is an effective tool which helps organisations in estimating the

future situations and scenarios through analysing the trends of past and present. The data is

gathered through various internal and external functions of the firm so it is reliable to use. It will

help the Rowlinson knitwear to identify the future trends which can effects the performance of

the company in future (Song, Wang and Zhu, 2018).

Advantage: This tool provides the valuable and necessary information to the business for

taking important decisions for the future which will benefits the company.

Disadvantage: The future can't be predicted accurately as the nature of future is

qualitative and dynamic.

Contingency tools: This tool is useful for determining the future risk factors which can

effects the business operations of the firm. This tool is used by Rowlinson Knitwear for

examining the performance and productivity of the business. Rowlinson knitwear must recognise

such risky factor and implement suitable measures for overcoming them.

9

Different planning tool used for budgetary control with their advantages and disadvantages

Budget: It is the predicted costs and funds which is necessary for performing the various

business operations in an organisation. It is the process of allotting funds for doing the activities

of a firm after analysing the costs and profit of previous year.

Budgetary control: This is the process for controlling and regulating the various budgets

which are assigned to various departments and processes. It compares the expected results with

the actual outcomes for determining that the process is following the allotted budget properly or

not. It is useful for Rowlinson knitwear to determine the variations and gaps in their performance

and then take suitable and appropriate measures for removing the identified gaps in future

(Schaltegger and Burritt, 2017).

It is very necessary for the management of Rowlinson knitwear to control their budget of

various operations for improving their efficiency and profit. Budget control plan must be

formulated accordingly to the needs of departments for ensuring that the operations are carried

out properly for accomplishing the desired goals and objectives of the firm. Various tools of

budget control are used by the companies to determine their financials which are given below:

Forecasting tools: It is an effective tool which helps organisations in estimating the

future situations and scenarios through analysing the trends of past and present. The data is

gathered through various internal and external functions of the firm so it is reliable to use. It will

help the Rowlinson knitwear to identify the future trends which can effects the performance of

the company in future (Song, Wang and Zhu, 2018).

Advantage: This tool provides the valuable and necessary information to the business for

taking important decisions for the future which will benefits the company.

Disadvantage: The future can't be predicted accurately as the nature of future is

qualitative and dynamic.

Contingency tools: This tool is useful for determining the future risk factors which can

effects the business operations of the firm. This tool is used by Rowlinson Knitwear for

examining the performance and productivity of the business. Rowlinson knitwear must recognise

such risky factor and implement suitable measures for overcoming them.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.